real estate market in brazil - urban land institute the... · real estate market in brazil -...

TRANSCRIPT

Real Estate Industry in Brazil

15Th

ULI Europe Annual Conference

February, 2011

2

Agenda

1. Macro Scenario

2. The Real Estate Market in Brazil

Residential

Office

Hospitality

Industrial

Shopping center

3. Sonae Sierra Brasil at a Glance

3

Growth

Over the last decade, Brazil experienced an unparalleled growth trend and should continue to

grow at solid rates in the foreseeable future…

Source: IBGE, MCM

GDP Growth Brazil

Source: MCM

Brazil

Area: 8.6 million sq km

Population (09): 193.7million

GDP (10E): US$ 2.0 trillion

GDP per capita (10E): US$ 10.4k

1.2%

5.7%

3.2%

3.9%

6.1%

5.2%

-0.7%

7.5%

4.5% 4.5% 4.6% 4.6%

2003 2004 2005 2006 2007 2008 2009 2010E 2011E 2012E 2013E 2014E

4

Decreasing Unemployment & Credit Expansion

Favorable economic conditions have led unemployment rate to its lowest level since 2003, and

have boosted both demand for credit and the purchasing power of middle class families mainly…

Unemployment Rate

Source: MCM

12.3%

11.5%

9.9% 10.0%

9.3%

7.9% 8.1%

7.3%

2003 2004 2005 2006 2007 2008 2009 2010E

Total Credit to Individuals Outstanding (R$ bn)

Source: Cetelem “O Observador 2010, Itau Securities

5

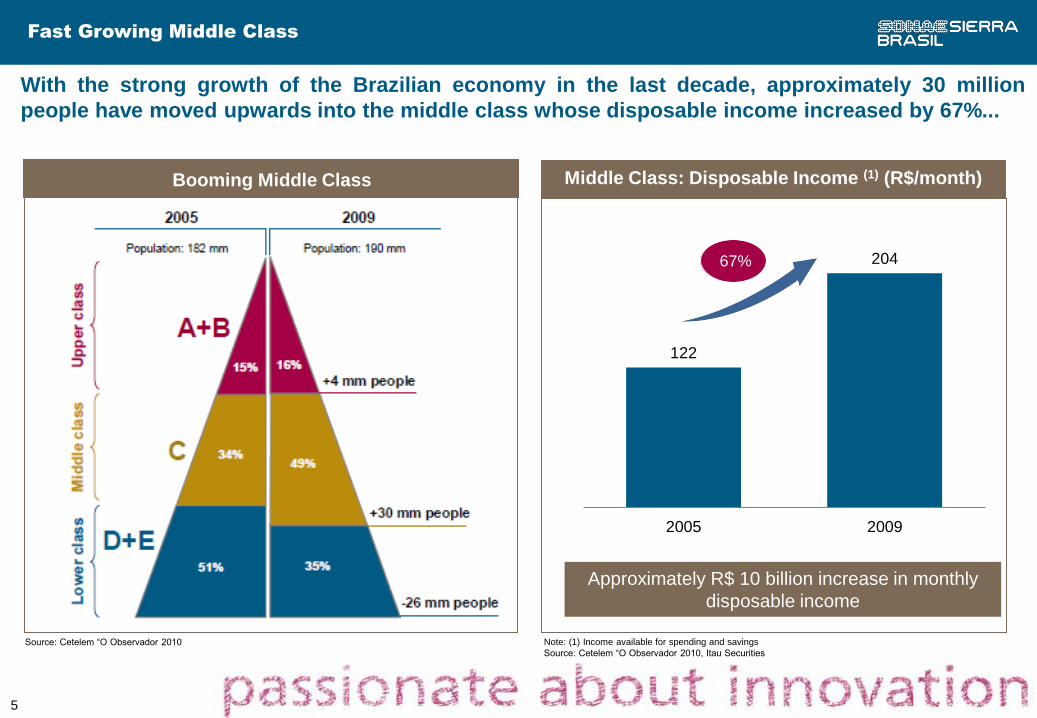

With the strong growth of the Brazilian economy in the last decade, approximately 30 million

people have moved upwards into the middle class whose disposable income increased by 67%...

Source: Cetelem “O Observador 2010

Fast Growing Middle Class

Middle Class: Disposable Income (1) (R$/month) Booming Middle Class

122

204

2005 2009

Note: (1) Income available for spending and savings

Source: Cetelem “O Observador 2010, Itau Securities

67%

Approximately R$ 10 billion increase in monthly

disposable income

6

Agenda

1. Macro Scenario

2. The Real Estate Market in Brazil

Residential

Office

Hospitality

Industrial

Shopping center

3. Sonae Sierra Brasil at a Glance

7

Real Estate Market in Brazil - Residential Market

Sound potential demand of circa R$173 billion with 58% in the mid and upper-mid income classes

and 42% in the affordable entry-level segment

En

try-le

ve

l fa

mili

es

Mid

an

d U

pp

er

mid

in

co

me

fa

mil

ies

Total households (million)

R$16k -

R$32K

R$8,000 –

R$16,000

R$4,000 – R$8,000

R$2,000 – R$4,000

R$1,000 – R$2,000

Up to R$1,000

Above R$32k

Total

0 0.3

0.3 1.3

1.1 4.3

3.3 11.0

8.4 21.8

15.5 27.6

31.7 29.1

Monthly Income Bracket

13

43

139

335

583

526

(113)

1,526

# Annual households (demand in thousand) 2007 2030e

60.3 95.4

Annual Potential Demand

(R$ bn)

Total volume

(R$ bn) 101

Households

(thousand) 530

Total volume

(R$ bn) 72

Households

(thousand) 846

Source: press releases of listed companies

(1)

(1) It includes only 50% of the potential annual households from R$1,000 – R$2,000 bracket

8

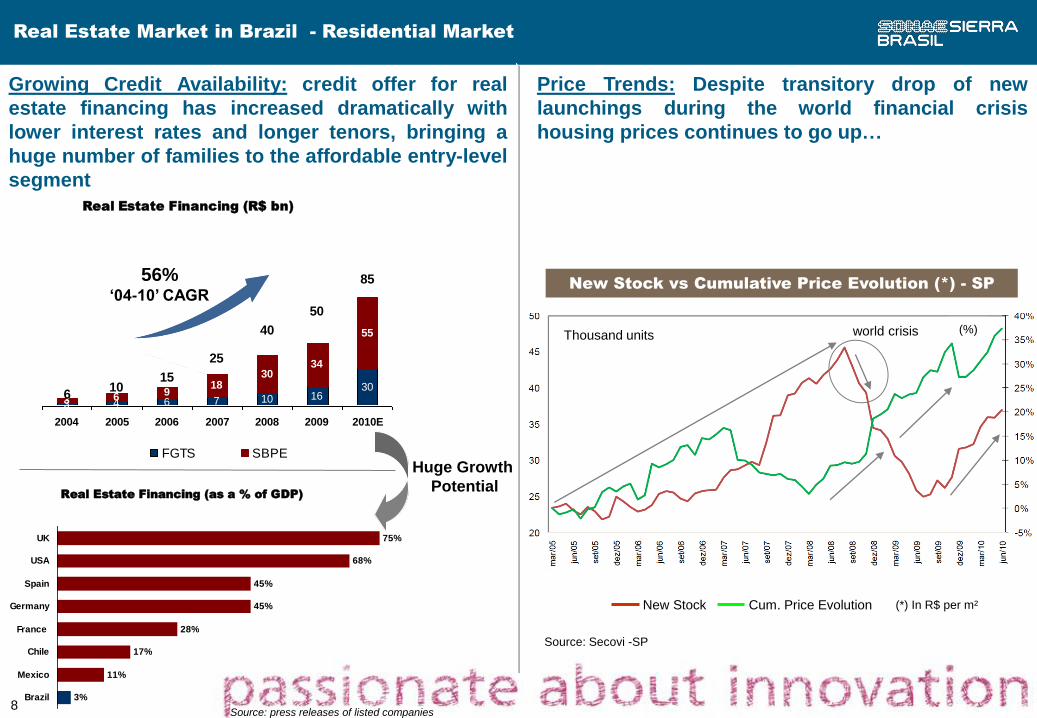

Real Estate Market in Brazil - Residential Market

Growing Credit Availability: credit offer for real

estate financing has increased dramatically with

lower interest rates and longer tenors, bringing a

huge number of families to the affordable entry-level

segment

Real Estate Financing (R$ bn)

3 4 6 7 10 1630

3 6 918

3034

55

610

15

25

40

50

85

2004 2005 2006 2007 2008 2009 2010E

FGTS SBPE

56% ‘04-10’ CAGR

Real Estate Financing (as a % of GDP)

75%

68%

45%

45%

28%

17%

11%

3%

UK

USA

Spain

Germany

France

Chile

Mexico

Brazil

Huge Growth

Potential

Source: press releases of listed companies

New Stock vs Cumulative Price Evolution (*) - SP

Thousand units (%) world crisis

New Stock Cum. Price Evolution

Source: Secovi -SP

(*) In R$ per m²

Price Trends: Despite transitory drop of new

launchings during the world financial crisis

housing prices continues to go up…

9

Agenda

1. Macro Scenario

2. The Real Estate Market in Brazil

Residential

Office

Hospitality

Industrial

Shopping center

3. Sonae Sierra Brasil at a Glance

10

Real Estate Market in Brazil - Office Market

€0 €300 €600 €900 €1200 €1500

Occupancy Costs per m² per year

Most Expensive World Locations

Source: C&W

2010

São Paulo represents the largest office submarket of

Brazil accounting for 60% of the total class A buildings

Rio de Janeiro is the 2nd largest office submarket and

also the most expensive, recording R$142 per m² per

month in 3Q10, mainly due to both the lack of vacant

lands for future developments and growing demand

Rio de Janeiro is among the top 20 most expensive locations in the world but still has lower rental rates when compared to that of prime office markets such as Tokyo, London, Dubai, New York and Paris indicating potential for future appreciation

With an overall average of R$70 per m² per

month, in 3Q10 asking rental rates increased

about 23% yoy

Overall vacancy rate averaged 10% in 3Q10

Source: C&W 2010

Overall Asking Rental Rates (Class A)

-

15

30

45

60

75

90

105

120

135

150

São Paulo Rio de

Janeiro

Brasília Porto

Alegre

Salvador Vitória Curitiba

R$/s

qm

/mo

nth

3Q09 3Q10

Overall Vacancy Rates (Class A)

0%

5%

10%

15%

20%

25%

30%

São Paulo Rio de

Janeiro

Brasília Porto

Alegre

Salvador Vitória Curitiba

Vacan

cy R

ate

3Q09 3Q10

142

91

Average = 10%

Average = 70

11

Agenda

1. Macro Scenario

2. The Real Estate Market in Brazil

Residential

Office

Hospitality

Industrial

Shopping center

3. Sonae Sierra Brasil at a Glance

12

Real Estate Market in Brazil - Hospitality Market

Source: JLL Hotels

Since 2004 ADR and RevPAR grew 5.7% and 8.4% per year, respectively, as occupancy rates have

been going up. The southeast region represents almost half of the entire national supply with São

Paulo and Rio de Janeiro being the main submarkets

78 7583

87

97104

112

181

164158

152

140137

151

62%63%61%57%59%

55%52%

60

80

100

120

140

160

180

200

2003 2004 2005 2006 2007 2008 2009

0%

10%

20%

30%

40%

50%

60%

70%

Average Daily Rate (R$) RevPAR (R$) Room Occupancy

Brazil Lodging Performance

8%

21%

21%

47%

3%

Mid-west Northeast North Southeast South

Distribution of Rooms per Region

Source: JLL Hotels

440,857 Total Number of Rooms:

# Brands # Rooms % of Total

1 Accor 23,950 5%

2 Choice 9,158 2%

3 Golden Tulip 5,313 1%

4 Blue Tree 4,149 1%

5 Nacional inn 3,747 1%

6 Meliá 3,395 1%

7 IHG 3,247 1%

8 Transamérica 2,774 1%

9 Windsor 2,726 1%

10 Othon 2,717 1%

61,176 14%

Offered by national and

international brands

Top 10 Brands

Source: JLL Hotels

13

Agenda

1. Macro Scenario

2. The Real Estate Market in Brazil

Residential

Office

Hospitality

Industrial

Shopping center

3. Sonae Sierra Brasil at a Glance

14

Real Estate Market in Brazil - Industrial Market

Net Absorption

Gross Absorption

Vacancy Rate (prime properties)

Overall Vacancy Rate

Industrial Space Performance*

Va

ca

nc

y R

ate

(%)

Ab

so

rpti

on

(m

²)

(*) São Paulo & Campinas Region Source: CBRE

Industrial real estate market continues to experience strong net absorption with low vacancy rates

and escalating rents. The average vacancy rate is 6.3% with asking rents growing 7.8% per year

on average, and ranging from R$12 to R$25 per m² per month – the highest levels since 2007

13

14

19

16

17

19

2005 2006 2007 2008 2009 2010

Asking Rental Rates* (R$/ m² / month)

Growing direct investments on new plants are expected to lead cumulative absorption

(demand) to historic levels of 600 thousand m² in 2010

Coupled with rising construction costs, leasing prices may experience a new rising wave in

coming future, mainly for built-to-suit developments

Trends:

15

Agenda

1. Macro Scenario

2. The Real Estate Market in Brazil

Residential

Office

Hospitality

Industrial

Shopping center

3. Sonae Sierra Brasil at a Glance

16

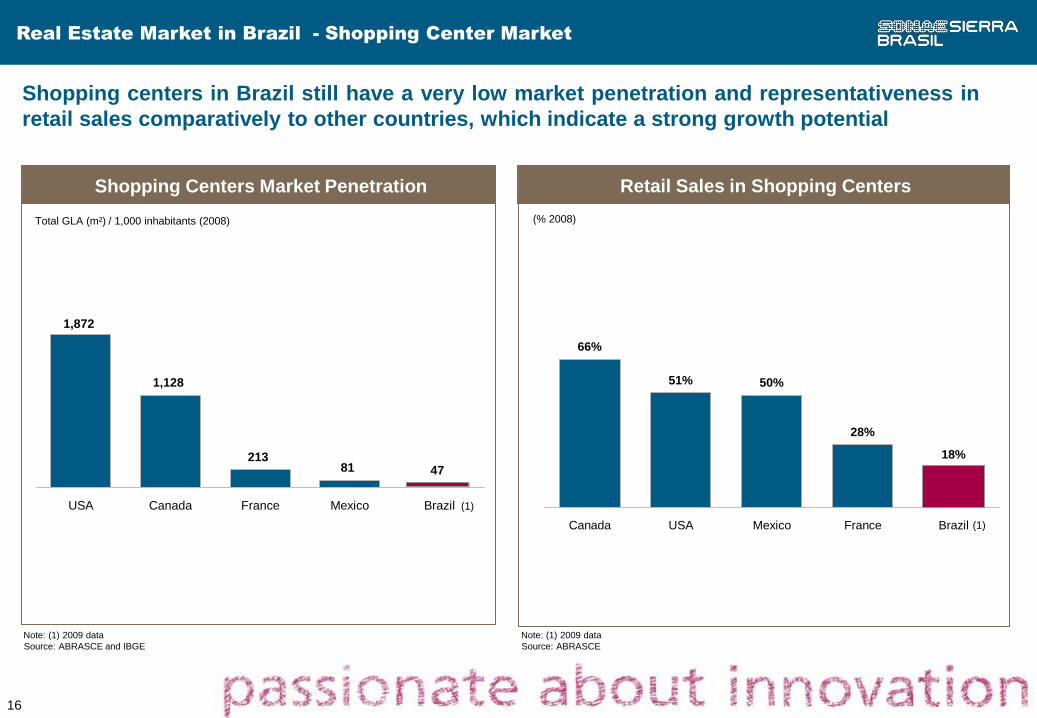

Retail Sales in Shopping Centers

Shopping centers in Brazil still have a very low market penetration and representativeness in

retail sales comparatively to other countries, which indicate a strong growth potential

Shopping Centers Market Penetration

Total GLA (m²) / 1,000 inhabitants (2008)

1,872

1,128

21381 47

USA Canada France Mexico Brazil

66%

51% 50%

28%

18%

Canada USA Mexico France Brazil

(% 2008)

(1)

(1)

Note: (1) 2009 data

Source: ABRASCE and IBGE

Note: (1) 2009 data

Source: ABRASCE

Real Estate Market in Brazil - Shopping Center Market

17

Total GLA

Source: ABRASCE (2010)

In the last 10 years, the number of shopping centers and GLA increased at annual rates of 3.8%

and 6.6%, respectively

Number of Operating Shopping Centers

Source: ABRASCE (2010)

2000 – 2009 CAGR: 3.8% 2000 – 2009 CAGR: 6.6%

280294

304316

325338

351365

377393

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

5.1 5.25.5 5.6

6.26.5

7.5

8.38.6

9.1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Real Estate Market in Brazil - Shopping Center Market

18

Geographic Distribution of GLA Geographic Distribution of Number of Malls

Geographic Distribution of Number of Shopping Centers Total number of shopping centers aff iliated to ABRASCE: 391

North

3% Northeast

14%

Mid-West

9%

Southeast

55%

South

19%

Geographic Distribution of Total GLA Total GLA of shopping centers aff iliated to ABRASCE: 96.9 million square feet

North

3% Northeast

14%

Mid-West

8%

Southeast

60%

South

15%

The Southeast Region – the most economically advanced in Brazil - holds more than half of

total malls and GLA in Brazil

Malls in operation: 393 Total GLA: 9.1 million m2

Source: ABRASCE (2010) Source: ABRASCE (2010)

Real Estate Market in Brazil - Shopping Center Market

19

Agenda

1. Macro Scenario

2. The Real Estate Market in Brazil

Residential

Office

Hospitality

Industrial

Shopping center

3. Sonae Sierra Brasil at a Glance

20

Portfolio Footprint

1

City: Campinas (SP)

GLA: 114.2 k m2

Ownership: 51.0%

2

City: São Paulo (SP)

GLA: 16.0 k m2

Ownership: 100.0%

City: Campinas (SP)

GLA1): 118.730 m2

Ownership1): 51.0%

Parque D. Pedro

Boavista Shopping

3

City: São Paulo (SP)

GLA: 29.5 k m2

Ownership: 73.2%

Shopping Penha

4 Franca Shopping

City: Franca (SP)

GLA: 18.1 k m2

Ownership: 67.4%

5 Tivoli Shopping

City: Sta. Barbara

d’Oeste (SP)

GLA: 22.1 k m2

Ownership: 30.0%

6 Shopping Metrópole

City: São Bernardo do

Campo (SP)

GLA1): 25.0 k m2

Ownership: 100.0%

7 Pátio Brasil

City: Brasília (DF)

GLA: 29.0 k m2

Ownership: 10.4%

8

Shopping Plaza Sul

City: São Paulo (SP)

GLA: 23.0 k m2

Ownership: 30.0%

9 Shopping Campo Limpo

City: São Paulo (SP)

GLA: 19.9 k m2

Ownership: 20.0%

10 Manaura Shopping

City: Manaus (AM)

GLA: 46.7 k m2

Ownership: 100.0%

12 Boulevard Londrina Shopping

City: Londrina (PR)

GLA2): 47.8 k m2

Ownership: 84.5%

Exp. Opening2): 2H 2012

11 Uberlândia Shopping

City: Uberlândia (MG)

GLA2): 43.6 k m2

Ownership: 100.0%

Exp. Opening2): 2H 2011

13 Passeio das Águas Shopping

City: Goiânia (GO)

GLA: 78.1 k m2

Ownership: 100.0%

Exp. Opening: 2013

Projects under development:

Centers # Stores Total GLA

(‘000 m²)¹

Operating Assets 1,934 347.7

Greenfields Projects 691 173.3

Total 2,625 521.0

8

1) Excludes GLA owned by third parties

2) Includes PDP 1 BV’s stake

21

Thank you!

22

Disclaimer

The material herein has been prepared based on data collected through our own research as well as information available to us from public

and other external sources. In respect to all external data, the sources are believed to be reliable and have been used in good faith.

However, Sonae Sierra Brasil can not accept responsability for their accuracy and completeness, nor for any undisclosed matters that would

affect the conclusions we have drawn. In addition, this presentation is provided for informational purposes only and It does not constitute an

offer or a solicitation of any kind or to participate in any particular trading strategy.