brazil real estate and land investors report 2011

TRANSCRIPT

1

Brazil 2011 Real Estate and Land

Investors Report

All material written in this guide is, unless otherwise stated, the property of the Brazil Real Estate Investment Guide (under the company name: ‘Brazil Real Estate Partners’). Copyright and other intellectual property laws protect these materials.

Reproduction or retransmission, in whole or in part, in any manner, without the prior written consent of the copyright holder, is a violation of copyright law.

This guide is intended for educational purposes only and the author has made every effort to ensure its accuracy and reliability. However, the author suggests that readers should, in addition, seek professional advice when conducting any kind of real estate

business in Brazil. The author shall in no event be held liable for any loss directly or indirectly arising from any material contained within this guide.

Should you wish to contact the author directly, please email:

For more information about who we are please click on the following link:

The Brazil Real Estate Investment Guide - Biography

2

Brazil 2011 Real Estate and Land Investors Report

CONTENTSPage

1 Welcome 4

2 Brazil Under the Rule of Dilma Rousseff 5

3 Brazil’s 2011 Economic Leadership Team 7

4 Brazil’s Involvement in the Currency Wars 9

5 Bringing Down Brazil’s National Interest Rate 10

6 Concerns Over Brazil’s Domestic Savings Levels 11

7 The Petrobras Phenomenon 12

8 The Brazil-China Relationship 13

9 House Price Inflation in Brazil 14

10 Brazil’s Real Estate Finance Market 15

11 Brazil’s Housing Deficit 17

12 Brazil State Housing Programme Examples 19

13 Brazil’s Construction Industry 20

14 Labour Supply in the Construction Industry 22

15 Low Income Housing / ‘Minha Casa, Minha Vida’ 23

16 The Regeneration of Brazil’s Favelas (Urban Slums) 24

3

Brazil 2011 Real Estate and Land Investors Report

CONTENTSPage

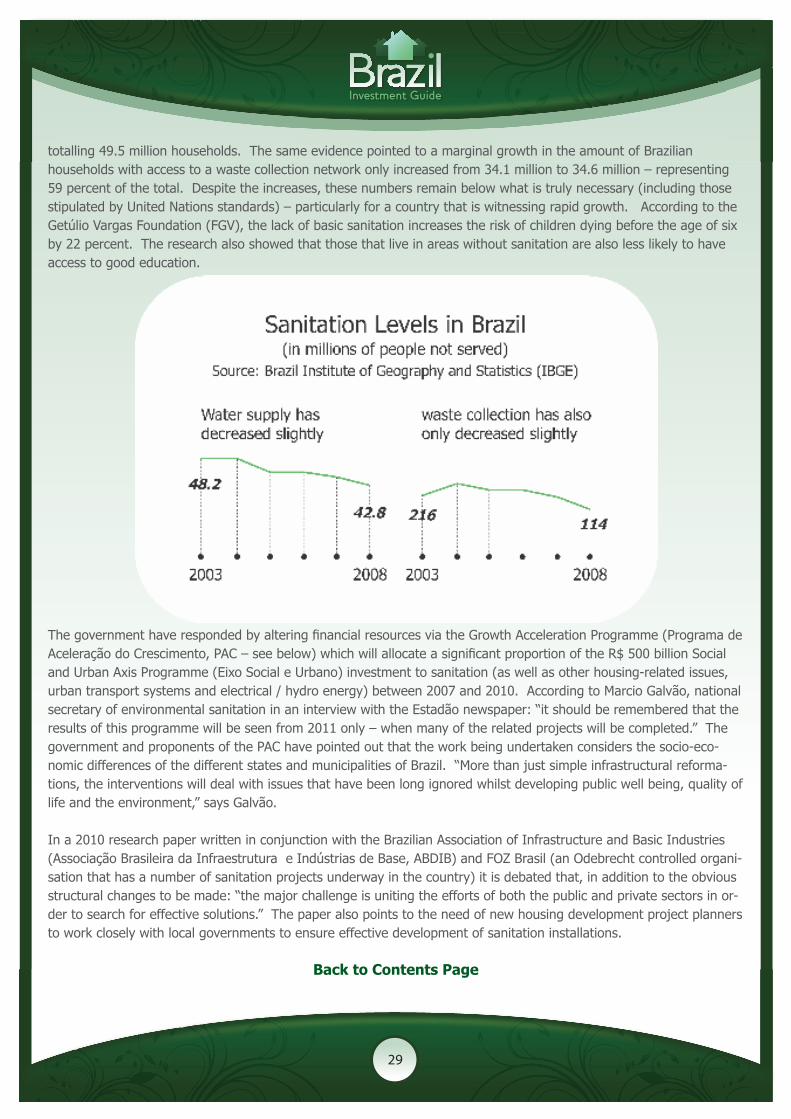

17 Brazil’s Low Sanitation Levels 28

18 Brazil’s Housing Industry Sustainability 30

19 Brazil’s Retail Real Estate Market 32

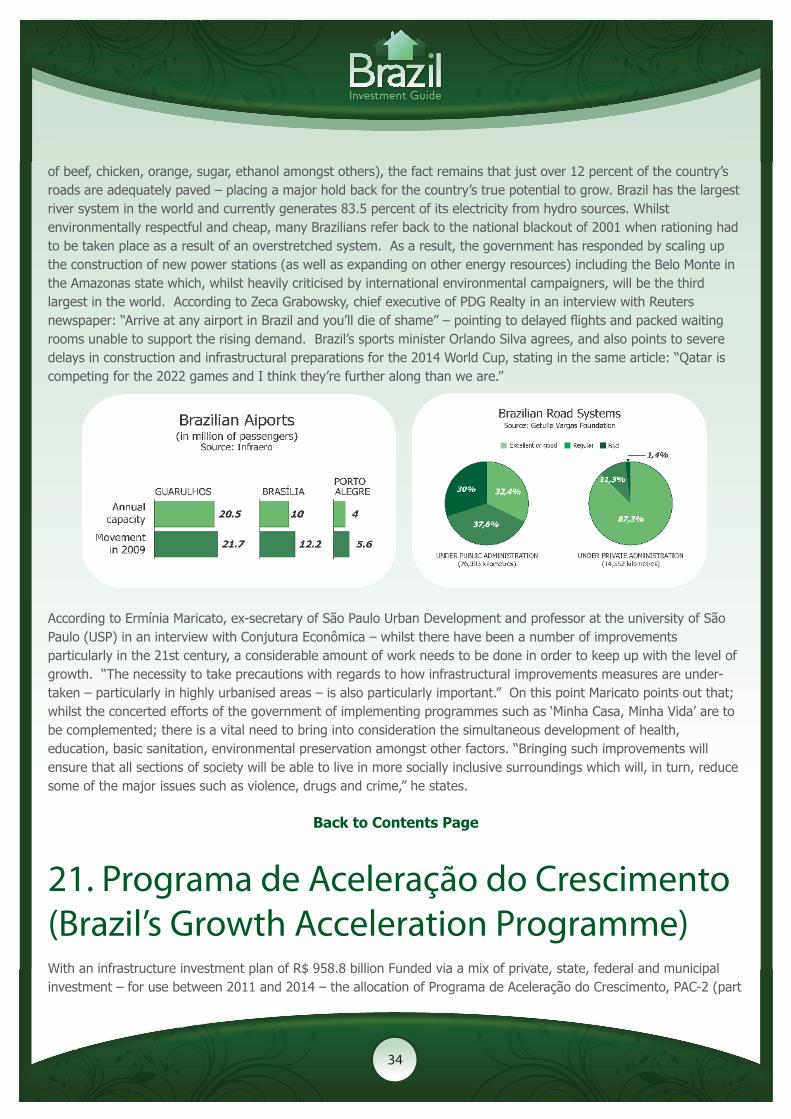

20 Brazil’s Other Infrastructural Challenges in 2011 33

21 Programa de Aceleração do Crescimento (Brazil’s Growth Acceleration Programme)

34

22 Relieving Congestion in Major Cities – Case Study: São Paulo

36

23 Brazil’s Demographic Movements 37

24 Removing Poverty in Brazil 38

25 Bolsa Família (Brazil’s Family Grant Programme) 39

26 Education in Brazil 39

27 Brazil’s Informal Economy 41

28 Bringing More Business Transparency into Brazil 42

4

1. WelcomeMany thanks for downloading this report. Written at the close of 2010, it is aimed at giving a detailed examination into the prominent issues related to Brazil’s property and land investment climate for the year ahead.

So what’s in store? The majority of international investors continue to remain bullish about Brazil – an entirely justified perspective for many reasons including rising incomes, lower unemployment, an asian-driven commodity boom, gigantic oil discoveries, up and coming major sporting / high profile events, oil findings, a vigilant banking system to name a few. However, as with any inflationary market, business risks need to be taken into account – from a macro-economic perspective, examples include a highly valued currency that is continuing to lose international competiveness (whilst weighing down the trade-weighted exchange rate and boosting consumer costs); a growing current account deficit; low comparative international savings levels; the ever rising need to improve infrastructure as well as low comparative innovatory and education levels. In 2010, perhaps more than ever before, it has become clear that the key to Brazil’s continued success is for the nation to not become complacent and take advantage of the wave of ‘feel good factors’ that have been sweeping the country in recent years.

For the real estate and land investor – despite possible issues related to over-supply, rising mortgage finance costs and ownership – industry professionals within the country remain positive that, for at least the next few years, the housing market will remain bouyant. In terms of overseas interest, 2010 events such as the financial turmoil in the Eurozone and the repercussions of the credit crisis in countries such as the USA and the UK have made property / land investing in Brazil a challenge – particularly combined with the fact that real estate finance for foreigners is not available (bar some development finance programmes are offered by some constructors). Other issues commonly noted include excessive bureaucracy, title protection, exchange rate issues, obtaining a sufficiently valid investment visa and acquiring real estate related assets transparently in accordance with international legal standards.

Nevertheless, as these issues are unlikely to disappear any time soon, investors – including an increasing amount from other so-called ‘emerging’ nations such as China, India and South Korea – have been striving to work through the complex system. We believe that it is a task that is well worth undertaking considering the wealth of opportunities available in a country with such strong medium to long term growth prospects.

What follows takes both macro and micro based outlooks on factors facing the Brazilian real estate and land industry at the close of 2010. As always, we have aimed the text to be written entirely objectively and welcome any comments to be sent to [email protected].

Thank you, Ruban SelvanayagamDirector, Brazil Real Estate Partners / Brazil Real Estate Investment [email protected]

Back to Contents Page

5

2. Brazil Under the Rule of Dilma Rousseff2010 saw the election of Brazil’s first female president – Dilma Rousseff – who took over the mantel of Lula da Silva’s unprecedented 81 percent approval rating with 56 percent of the public vote. Against punditry comments of being the ‘automatic pilot president’ and ‘Lula with a skirt’ she has appeared determined to establish her own impact on the country. The campaign that led up to her election on October 31st took an unusual trajectory due to the popularity of her predecessor – with her main opponent José Serra (current governor of São Paulo) even commending the achievements of the Workers Party government via using images of Lula in his presidential campaign, a rare site in Brazilian politics. Indeed, some argued that the campaign was far too ‘rosy’ without real and necessary debate on the relevant issues and, whilst Lula’s achievements are to be noted and indeed merited – Rousseff is entering leadership of a country at an historically important economic turning point. The achieved momentum thus far will need to be maintained and worked on in order for the country to maintain this position. Nevertheless, upon winning the election – accompanied by Fernando Pimentel (now minister of development, industry and external trade), Antônio Palocci (federal deputy), José Eduardo Dutra (president the Workers Party) and José Eduardo Cardozo (general secretary of the Workers Party) – Rousseff announced “I’ll be president of all Brazilians. I will honor the trust placed upon me.”

Her history is well-populated with political battles against the former military regime representing and leading left-wing organisations including the Workers Politics Party (Política Operária), the Command of National Liberation (Comando de Libertação Nacional), the Popular Revolutionary Vanguard (Vanguardhea Popular Revolucionária) and the Palmares Popular Revolutionary Vanguard (Vanguarda Popular Revolucionária Palmares). In the 1970s, she was arrested and brutally tortured which many state fortified her strong character.

A trained economist and a propensity to favour state-led industrial policy, most are expecting very few significant changes to occur. In her campaigning, the main pledges included: the continuation of social welfare and housing programmes such as the ‘Bolsa Família’ (Family Grant’) and the ‘Minha Casa, Minha Vida’ (‘My House, My Life’); a more flexible state sector, whilst actively supporting private enterprise (something of which has been questioned by economic commentators); reduce the country’s inflation level by half a percentage point to 4 percent by 2012 – although she has emphasised the need for this to be done in a careful and gradual manner; increase national savings levels; continuing the drive to improve the country’s infrastructure as well as ensuring solid preparation for the 2014 World Cup and the 2016 Olympics; reign in government spending including public sector wage levels; cut national interest rates to 2 percent by 2014 (by cutting state spending amongst others – see below); rid the country of extreme poverty by 2016 (see below); reduce the excessive appreciation of the currency whilst maintaining the country’s level of reserves (currently standing at US$ 280 million); fortify and closely monitor the financial system to ensure healthy and consistent growth (the country proudly operates well above the international Basel accord standards); maintain central bank autonomy, which has proven to be a success;

6

impose additional taxes on capital inflows, to limit currency overvaluation (something of which former Central Bank chief Henrique Meirelles stated as ‘a possibility’); a review of the tax system – although full details of what this will entail have yet to be announced; in what many have commented as maintaining the vote of Brazil’s ‘Landless Workers’ Movement’, she has stated that there is an ‘abundance’ of land to distribute; her team of economists have been analysing the feasibility of rising minimum wages by 20 percent.

She has confirmed that she will not be undertaking in any reforms of the public sector (which many debate is over weighted) as well as the highly restrictive labour laws (one of the main attributors that led to the 2010 ‘International Index of Business Freedom’ lowering Brazil’s overall score). Many are expecting President Lula’s presence to still be felt in the coming years and Rousseff herself stated to the press that she will ‘frequently knock’ on his door for advice.

For business leaders; whilst a significant proportion desired main election opponent José Serra to gain the presidential seat (largely due to his largely pro-private interest stance and success as governor of São Paulo); Rousseff has been largely welcomed. At the Brazil Investment Summit in late 2011, Edemir Pinto, chief executive of BM&F Bovespa said to reporters: “I’m just as happy that I can be with Brazil for the next few years.” Yet he warned that Brazil must increase its savings rates from the current level of 18 percent of GDP in order to match its BRIC counterparts stating: “that will have to be a priority for us to become the fifth or sixth biggest economy (in the world) by 2016” (see below). Other concerns highlighted by Pinto include the level of fiscal spending; inflationary risks; the high valued real (see below); high taxes and stringent rules in place when hiring / firing employees. Also at the Brazil Investment Summit, Zeca Grabowsky, CEO of PDG Realty (one of the largest developers in the country): “I think she’s going to surprise in a positive sense with the seriousness with which she’ll attack the housing deficit.” Below are some other comments from some real estate specialists in the country who we asked on their opinion as to how the market will behave as a result of her election:

“With the election of Rousseff, the Brazilian property market has at least another ten years of growth. The Workers Party government was the best thing that could have happened in the history of construction in the country since

7

it was the only ruling party that has created real incentives for the industry – with the main one being Minha Casa, Minha Vida (‘My House, My Life’) as well as other infrastructural programmes such as the Programa de Aceleração do Crescimento (‘Programme of Accelerated Growth’). It is certain that the scope of these programmes will continue to grow and assist the real estate market in a major way.” Flavio Cabrera, Lopes Real Estate Consultants, Porto Alegre, Rio Grande do Sul

“Even if Rousseff didn’t get elected, our sales volumes would not have stopped growing. I don’t think there is one person that is not confident about the housing market here in Rio. Credit is easier to obtain, prices are still reasonable and our local economy is looking its strongest in a long time – particularly as we look forward to the World Cup, Olympic Games and several other international events. Supply does also remain a major issue still and therefore there is still much room for the market to rise.” Roberto Pimenta, Patrimovel Real Estate, Rio de Janeiro

“The Paulista real estate market remained strong throughout the election build up – which doesn’t usually happen. We specialise in commercial / industrial real estate and we have been finding that, in 2010, there are more buyers than sellers which is due to the fact that São Paulo is the biggest economic city of a country that is witnessing rapid growth, hence the increased demand. Our quarter 3 sales statistics are 42 percent higher than that of the same pe-riod in 2009 – a trend of which we expect to continue.” Tânia Amorim, Tânia Amorim Real Estate Consultancy, São Paulo

Back to Contents Page

3. Brazil’s 2011 Economic Leadership TeamAlexandre Tombini – President of the Central Bank (Banco Central): Stated by Henrique Meirelles that Tombini ‘is the best prepared to take his place’ and was described by the FT as an ‘apolitical technocrat’; Some commentators have stated that he is less orthodox and more flexible than his predecessor – with Antonio Carlos Aidar of the Getúlio Vargas Foundation stating in late 2010 that there is a ‘radical change in the air’; Director of standards and financial system organisation of the Central Bank of Brazil since April 2006 (with other roles in the bank including international affairs director and director of special affairs); Senior advisor to the executive director of the Brazilian representation at the International Monetary Fund (IMF) from July 2001 to May 2005 (based in Washington DC) where he was heavily involved in the formulation, analysis and presentation of the Brazilian position on numerous policy issues to the IMF including the monitoring bilateral and multilateral programmes; Head of the department of studies and research at the Central Bank of Brazil from March 1999 to June 2001 focused on inflation targeting, banking microeconomics and financial sector regulation with emphasis on market risk as well as the relationship with the World Bank and the Bank for International Settlements (BIS); Special adviser at the Foreign Trade Chamber from February 1995 to May 1998; Area coordinator general of the External Economic Policy Secretariat, Ministry of Finance from December 1992 to January 1995:

8

Head of the technical group in the negotiation of the Common External Tariff (CET) of Mercosur; Visiting Professor, Department of Economics, University of Brasília from March 1993 to December 1994.

Guido Mantega – Minister of Finance Has been in the role since March 2006; the FT referred to him as a ‘developmental’ economist and he is widely credited with helping to steer Brazil’s quick recovery from the international financial crisis; Upon the announcement of his renewed position, he stated that he will aim to reduce the government’s expenses and public debt in the new administration saying that the goal is to reach a public debt of 30 percent of GDP by 2014 (currently 41 percent). “I want to reaffirm my commitment to consolidate the economic development, with high growth rates and a continuous improvement of the Brazilian population’s living conditions,” he stated to the Globo newspaper; President of the National Social and Economic Development Bank (BNDES) from November 2004 until March 2006; State minister of planning, budget and management from January 2003 to November 2004. Economic advisor to President Luiz Inácio Lula da Silva from 1993 to 2002 and one of the Worker Party economic program coordinators in the 2002 presidential campaign; Member of the Workers’ Party (PT) Economic Program Coordinating Group in the 1984, 1989 and 1998 presidential elections; Budget director and chief of staff of the São Paulo Municipal Planning Secretariat from 1989 to 1992; Former professor of economics at the Catholic University of São Paulo’s (PUC-SP) Master’s and PhD programs, from 1982 to 1987; PhD in development sociology from the Philosophy, Sciences and Liberal Arts School of the University of São Paulo, with specialisation studies at the Institute of Development Studies (IDS) of the University of Sussex, England in 1977; Former professor of economics at the School of Business Administration of the Getúlio Vargas Foundation Deputy dean of the Catholic University of São Paulo (PUC-SP) from 1984 to 1987; Books published include: “Monopolist Accumulation and Crises in Brazil” (1981); ”Brazilian Economic Policy “ (1984); “The Brazil Cost – Myth or Reality “ (1997) and “Talks with Brazilian Economists II” (1999).

Miriam Belchior – Minister of Planning Eight years of experience in government she was formerly coordinator of the Programme of Accelerated Growth (Programa de Aceleração do Crescimento, PAC); Former special advisor to President Lula and had a integral role in the development of the country’s social programmes; Between 2001 and 2008 she was professor of the development of administration, accounting and economics at the University of São Paulo (USP); From January 1997 to December 2000, she was head of administration and modernisation of the city of Santo André and from January 2001 to November 2002, municipal secretary of Housing and Social Inclusion (a region selected as being in the top 100 public practices in the world by the UN in 2000); Started a career as a social and political campaigner for São Paulo’s ABC party.

Back to Contents Page

9

4. Brazil’s Involvement in the Currency WarsBrazil’s participation in the debate over international exchange rate policy has been viewed as particularly important, particularly as – according to Financial Times statistics – the Real has risen by 33 percent since the start of 2009 which has had an effect on the country’s export levels. To place into context, in 2002 one US dollar would exchange for R$ 3.89 where as at November 2010 it is R$ 1.68. Whilst efforts were made by the finance ministry through the means of imposing a 6 percent tax on inflows, the medium term impacts are said to be negligible. As illustrated in the July 2010 Economist magazine’s novel methodology of analysing how far currencies are from their realistic value via the price of a McDonalds ‘Big Mac’, a 31 percent overvaluation was indicated for the country (although it should be noted that this measurement stated that several other developed world currencies, including the Euro, are also appreciated). Despite such international comments, as Lula prepared to move away from the presidency, he has nevertheless continued to exert much of the international political clout that he has gained in recent years – an example of this has been his public criticisms of China and the US for maintaining their currencies at artificially de-pressed levels. In one of her first world stage appearances at the G-20 summit in Seoul, Rousseff stated (perhaps a touch extremely): “the last time there was a series of competitive devaluations, it ended in the second world war.” For many reasons, Brazil’s rapid currency rise in recent years was to be expected as a result of its comparatively large economic success – including seeing 30 million people enter the middle class and 20 million being assisted under some kind of government social programme. To the country’s credit, this has been achieved whilst keeping inflation under control; organised expansion by the private and, to a certain extent, the public sector and a solid financial system. Such events have been in sharp contrast to many developed economies as a result of the crisis producing what is a seeming disequilibrium. According to Benjamin Steinbruch of the Federation of São Paulo State Industries (Federação das Indústrias do Estado de São Paulo: “China and Brazil have become the major targets of the world. China – seeing itself as a potential global leader has been witnessed protecting its own interests whilst advancing into others. Brazil, on the other hand, has remained open to imports – and, indeed, has reduced both prices and taxes (such as the ICMS value added tax which has been dropped from 12 to 3 percent for imported products in nine states). Brazil’s low savings rate also makes the country dependent on international capital flows such as via the capitalisation of Petrobras which attracted investment estimated at over $US 14.9 billion (see below). In an interview with City Wire Global Magazine, manager of the HSBC GIF Brazil Equity Fund José Cuervo states that the real issues occurring are as a result of wasteful public spending, stating: “the cause of the imbalance lies with the policies within Brazil, despite very strong economic growth the country has very loose fiscal policy. We hope after the election the government will sit down and become more conservative. Hopefully they will ask themselves, ‘How do we start this ad-ministration on the best footing?’ The view has to be that the government will take a slightly more cautious approach. Spending on subsidies and education is core to what the government stands for but it will have to take a stricter approach to fiscal policy going forwards.”

10

At an international press conference in late October 2010, Mantega firmly stated that Brazil had an ‘arsenal’ of curbing measures including the purchasing of US dollars to boost international reserves as well as discussions over reserve-swapping and increasing capital limits for banks in the country to ease the pressure in the futures and other derivative markets. Others include Central Bank (Banco Central) monetary control; utilising the Brazil Sovereign Fund (‘Fundo Soberano do Brasil’ which enables controls to be placed on foreign inflows); using fiscal instruments to control the situation – as was done in October and November 2010 when the Imposto sobre Operações Financeiras (IOF, Tax on Financial Operations) was increased from 2 to 6 percent (two hikes in the space of one month) as well as the promise to realign the ICMS (Imposto sobre Circulação de Mercadorias e Serviços) value added tax – but the execution of this has yet to be specified and will also have to be approved by the 27 members of the Council of Finance Policy (Conselho da Política Fazendaria, CONFAZ).

Whether such actions result in an improved equilibrium in the relationship between Brazil’s and other world currencies remains to be seen, however it is widely expected that it will also require the economic performance of the lead-ing economies (and Brazil’s trade partners) to also improve. Indeed, as several countries are initiating measures to devalue their currencies in order to boost exports, Brazil may well be forced into a position of following suit in order to remain competitive.

Back to Contents Page

5. Bringing Down Brazil’s National Interest RateAs Rousseff confidently announced in her pre-election campaign as having the ability to bring down Brazil’s interest rates in line with international standards, what many claimed as political rhetoric has now being increasingly debated as a potential reality – something that would be unprecedented in the economic history of the country. When President Lula was elected in November 2002 international investors required interest rates of 24 percent

11

per annum above the rate paid by U.S. Treasury securities to invest in Brazil; today this requirement has fallen to 2 percent. Many have attributed much of the excellent outcomes of monetary decisions to Henrique Meirelles which, in turn, has prompted Rousseff’s confidence in making such statements.

Nevertheless, opinions with regards to the realism of low interest rates remain clearly divided – a significant proportion believe monetary policy will remain relatively in line with how it operates today. Others are expecting increased restraints in public spending to lead to interest rates falling but point to the accompanying risk of spiralling inflation (which will need to be controlled); low unemployment levels as well as the concerns over the introduction of new and untested policy making. Another camp state that the key to lower interest rates is a rapid transformation of the onerous taxation system – according to Roberto Setubal, CEO of Itaú Unibanco: “there’s no free lunch. For interest rates to fall, fiscal policy has to help – but I’m confident from what I’ve heard from the president that she’ll address this issue.” Setubal also argues that should this policy be undertaken, the currency issues mentioned above will also come back under control.

In a blog post via the FT Tony Volpon, head of emerging market research for the Americas at Nomura pointed to Bra-zil’s increasing tendency to emulate China (one of its increasingly important trading partners) – one example illustrated with regards the substitution of rising interest rates was to place restraints on credit growth, which Brazil was witnessed doing at the end of 2010, a practice that Volpon expects to continue.

Back to Contents Page

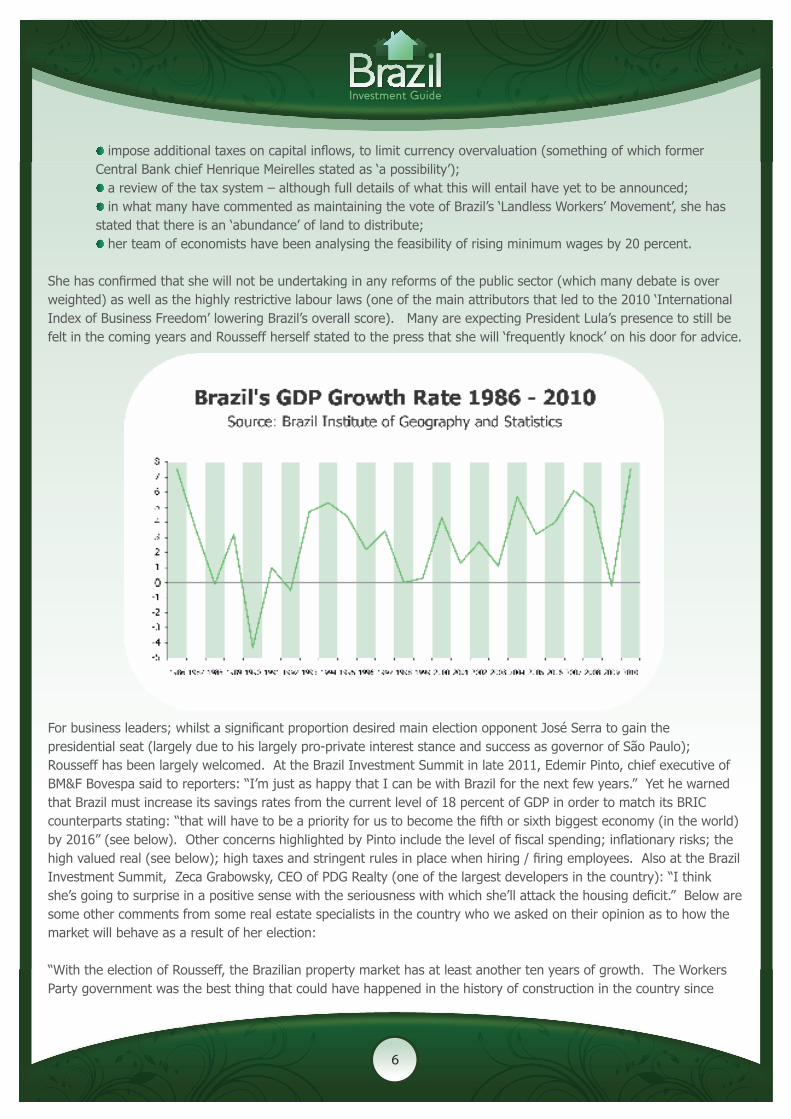

6. Concerns Over Brazil’s Domestic Savings LevelsThroughout 2010, Henrique Meirelles has stated the challenge that Brazil faces in terms of increasing its domestic savings. The Brazilian Institute of Geography and Statistics (Instituto Brasileiro de Geografia e Estatística, IBGE) at the close of 2010 showed a national savings rate of 4.71 percent of GDP compared to 20 percent in China.

Amongst the reasons stated is the country’s social security system which – whilst considered to have become increasingly generous – has resulted in lesser desire to save. Another is the lower average national income level when compared to developed countries which inhibits people’s ability to store money away. Brazil’s increasingly apparent goods and services consumption activity is also stated as an explanation: between 2004 and 2008 – con-trary to predictions of falls due to the economic crisis – goods and services sales increased from 59.7 percent to 62.8 percent of GDP. Luiz Guilherme Schymura – director of the Economic Institute of Brazil (Instituto Brasileiro Economia, IBRE) in a November 2010 interview with Epoca magazine stated: “despite increases in the minimum wage level, [which has increased from US$ 60 in 1994 to almost US$ 300 today] the level of savings still remain low due to the increase of consumer prices limiting people’s ability to store money away.” He also points to the fact that “the older generation of Brazil rarely save and the young, more often than not, do not often view the benefit of saving.” The high burden of tax is further attributed to be a cause of the issue – whilst it is argued that public money is being used improve the country’s infrastructure, analysts remain confused with regards to the altitude of the public deficit. According to the latest figures released by the Central Bank, between January and May, the public sector recorded a nominal deficit of 2.69% of GDP (the equivalent to R$ 37.6 billion). In contrast, the savings rate of many private companies in Brazil – as per IBGE statistics – remains close to 20 percent (a figure that is almost identical to China). It is argued that, as a result of this, an increased reliance will be required for production growth of this sector.

12

Whilst not public announcing that danger beckons as a result of these statistics, prior to his exit, Meirelles was seen actively encouraging banks to provide greater customer savings abilities – with the aim of allowing better financing activity and security in times of crisis. However, it is argued that the lack of clear policies is the true cause of the issue – Márcio Nakane professor of economics at the University of São Paulo (USP) stated in a late 2010 interview with Veja magazine that: “there is a clear need to raise awareness about the importance of private pensions.” Whilst investment in pension plans has witnessed steady growth in revenue levels over the last decade according to data from the National Federation of Private Pension and Life (FenaPrevi) – Nakane argues there remains much more room for growth. He also points to the need for financial education to be encouraged from a young age right through to the work place – illustrating some wage saving schemes that have been introduced by companies. Schymura states that the government’s focus needs to be placed on ensuring that economic growth remains stable – with the key route being through maintaining a sustainable level of consumer price control that does not get out of hand and impedes people’s ability to save.

Back to Contents Page

7. The Petrobras PhenomenonSeptember 2010 saw national oil company Petrobras announcing a stock offering to assist with the funding of a R$ 224 billion, five-year capital-spending plan – the majority of which was allocated to exploration of the so-called ‘pre-salt’ region that runs 800 kilometers along the south-east coast from the states of Espírito Santo to Santa Catarina at up to 7,000 metres below sea water, salt and hard rock as well as to bring up to date the shortfall of previous downstream spending. The fundraising was deemed a huge success with Theodore Helms, executive manager of in-vestor relations stating: “one of the remarkable aspects of the deal was how well it matched Petrobras’ expectations.” Brazil is now the 16th largest global oil producer and will be scaling up its production process in the coming years to reach 5 million barrels per day by 2020 (excelling it to be one of to be one of the world leaders).

13

However, the growth of the petroleum industry has raised a number of concerns – many of which accompany countries where large scale discoveries are found – including political corruption, efficiency control, an over-reliance on a volatile commodity and the so-called ‘Dutch Disease’ in addition to the practical issues of drilling (an issue was bought to prominence as a result of the Mexican oil spills). Whilst policies initiated by Lula to allocate funding to education and infrastructure have been commended, other concerns about royalty allocation have also been voiced – particularly by the main oil producing states such as Rio de Janeiro and São Paulo who believe these areas should be prioritised and awarded the most amount of funding. In December 2010, the government has said it would negotiate a more moderate redistribution of oil revenues amongst other states that do not produce oil.

Another issue is the pace of governmental management of the exploration and drilling being particularly slow. In an interview with the FT, Christopher Gar man of the Eurasia Group states: “the government is embarking on a route that will clearly lead to a slower pace of development. It is limiting development to the operational and financial constraints of a single company. There’s a big question as to whether they will be able to attract serious junior partners.” According to Helms: “what is crucial is that Brazil’s great discoveries are coming after economic development is well under way – if we assume exports in 2020 might be 2 million barrels a day, this is not huge relative to the overall economy and simply not enough.” Many analysts also agree that Brazil’s exposure to the overall oil sector remains low – with Diego Donadio from BNP Paribas in Brasil in an interview with Euro Money magazine stating: “Brazil’s oil trade balance is close to zero and the country is miles away from becoming an economy extremely dependent on oil like other OPEC members such as Norway.”

Back to Contents Page

8. The Brazil-China RelationshipBetween 2000 and 2009, trade between Brazil and China rose from just under US$ 1 billion to over US$ 37 billion – making it the country’s largest partner. According to Guido Mantega on a trip to China in mid 2010: “the two countries have much room to be able to grow together.” The arrival of Chinese investors and business leaders entering the country has also reached unprecedented levels and between January and September 2010 US$ 372 million came into the country – bringing the total to US$ 23 billion. In terms of exports, the main products received by China from Brazil include metal minerals (largely steel), petroleum, cellulose and sugar and vice versa are televisions, radios, IT / telephony and lighting. 2010 has also seen an increased interest on the part of Chinese exploring a range of new market sectors including vehicles, real estate and other metals.

Perhaps the most important export for China – due to the large-scale and ever increasing demand – is agriculture, namely soya (a staple food source for the country). In 2010, Chinese business leaders were acquiring large tracts of land to create and boost production facilities – particularly in the states of Bahia, Maranhão, Piauí and Tocantins. However, a legal ruling enacted in April 2010 stipulating that foreign land purchases are to be limited to 25 percent of any municipality in Brazil soon bought some control to what was (according to the legislators) a risk to the interests of the country. This ruling subsequently saw a reduction of the activity of the Chinese in Brazil who are now seeking further flexibility in the laws arguing that their activity creates win-win opportunities for both countries – an argument

14

that some see as somewhat hypocritical due to the highly protective laws of investment that operate in China.

Nevertheless, an example of the fact that expansion has continued was the cooperation term signed between the state of Goiás and the China National Agricultural Development Group in November 2010 – an agreement which is expected to bring an initial US$ 7.5 billion into the state. Operating more as a partnership between the two countries, (and thereby bypassing the land ownership laws) the investment will see the transformation of over 2.5 million hectares of grain productive land for export. According to Odécio Kieling, partner in a landownership company responsible for 1,800 hectares in the state in an interview with Exame magazine: “the Chinese have been particularly interested in grand-scale mechanisation and up-to-date technology in order to maximise productivity and efficiency. It will be an excellent opportunity for all producers in the region.” Kieling also points out that degraded land throughout the state is also being fertilised and transformed for livestock rearing, rice growing amongst other activities in line with the project.

Back to Contents Page

9. House Price Inflation in BrazilThe effects of the global economic crisis bought what was a real estate boom period in several developed countries to an abrupt end. Conversely, Brazil (along with a number of other so-called ‘emerging’ nations) has seen what many have termed as being at the start of a long term growth trajectory. Renowned real estate developer Donald Trump, for example, commented to the LA Times that: “it is one of the few places in this troubled world I feel confident to make an investment” and the modern day ‘sage’ of value investing Warren Buffett stating to Fox News: “Brazil has cleverly positioned itself to become one of the world’s greatest investment opportunities in modern times.”

Nevertheless, as property prices have continued to grow in 2010 on a general level across all of the country’s 26 states – a rising debate of the emergence of a bubble has become more apparent. In Rio de Janeiro, for example, some agencies reported a 50 percent increase in house price values in the space of just 9 months particularly after Olympic Games announcement. According to Globo, property values have increased by 100 percent in São Paulo in the space of 5 years; 50 percent in Brasília over 2 years and as much as 60 percent in Recife (Pernambuco, north east Brazil) between 2009 and 2010.

On the one hand, property price rises (as with the currency) are to be expected and viewed as a natural progression of the success of the economy – the housing market in Brazil is being well reinforced by a range of factors includ-ing lower unemployment levels (Ministry of Labour statistics have indicated that over 1 million new jobs have been created in 2010); rising wages (according to the registry of employment, average initial salaries have increased by 27 percent in the last seven years); a very lowly leveraged mortgage market which looks set to grow considerably in the coming years as well as the fact that many existing homeowners having a considerable amount of equity stored in property (a very different situation when compared to markets of many developed countries). However, despite these favourable factors, concerns nevertheless remain that house prices have become increasingly excessive within such a short space of time.

15

A report was thus published by Brazilian macroeconomic consultants – MP Associates – on behalf of the Brazilian Association of Real Estate Credit and Savings (ABECIP) entitled: “Are Brazil Real Estate Valuations Reaching Bubble Like Proportions, as Seen in the USA?” José Roberto Mendonca de Barros, author of the report and former Secretary of Economic Policy for the Ministry of Finance concludes: “there is a price rise in property values because there is increased demand and we therefore have no doubt in saying that there is no housing bubble in Brazil.”

The debate was somewhat quashed as the housing market began to cool off in the second half of 2010, when the effects of the SELIC rises were seen to take effect. Salomão Quadros, coordinator of the national index of prices (Índice Geral de Preços, IGP) in an interview with Conjutura Econômica, stated: “the contrary appeared to what was expected and the market did not become overheated” going on to illustrate that the fact that the rise in prices of real estate and housing finance has encouraged the industry to expand and meet the rising demand rather than main-tain existing stock levels and limit supply – this, in turn, has and will enable prices to be more controlled. Whilst the supply of property in the market place is increasing, many still see the actual number as insufficiently limited (for example, via the inefficiencies of the ‘Minha Casa, Minha Vida’ housing programme – see below). Others have also questioned the current indices of Brazilian house prices and state that such reports of rapid increases in values are a result of media hyperactivity without due regard to real economics.

It would therefore seem that, if a property bubble is emerging in Brazil, it is currently far too early to predict when it will happen. Investors should, however, be well aware of the fact that the country’s housing market should not always be viewed holistically and close attention is needed with local idiosyncrasies (such as supply /demand, rental figures, taxes and legal jurisdictional variations amongst others).

Back to Contents Page

10. Brazil’s Real Estate Finance Market It is the youth of housing finance market that is demonstrating the growth potential exciting the Brazilian banks and lending institutions. In 2002 and 2003, no more than one thousand houses were mortgaged and it was not until 2006 that the evolution really started to take place as housing loan terms were extended from periods of 12 to up to 30 years and repayment levels (whilst still internationally comparatively high) decreased from 12 to the 8-9 percent level. By 2004, 321,149 units were financed in Brazil – of which 53,787 were from via the Brazilian System of Savings and Loans (Sistema Brasileiro de Poupança e Empréstimo, SBPE – the constituted system of Brazilian lending institutions that offer housing finance) and the rest by means of the Fundo de Garantia do Tempo de Serviço (FGTS – click here to read our blog post). By 2009, the amount of units being financed by the SBPE comfortably increased by over five times to 302,680 and those financed by the FGTS increased to 396,367. This does not include the Minha Casa, Minha Vida allocation bringing the total for the year to 897 thousand properties. Banking figures have shown that in 2004, a total of R$ 6.849 billion was lent – of which R$ 3.9 billion was via the FGTS and the remainder from the SBPE. By 2007, this figure via the FGTS increased to R$ 24.464 billion. According to Ana Maria Castelo of the Getúlio

16

Vargas Foundation in an interview with the Conjutura Econômica magazine: “the growth of the market occurred in very little time both in quantitative and qualitative terms. By 2004, a significant proportion of middle class Brazilians earning over five and six times the minimum wage were able to access housing finance in addition to make use of the FGTS. Then, the introduction of the ‘Minha Casa, Minha Vida’ programme in 2009 enabled those who were previously excluded to enter the market. It was not too long ago that rates were so high that the total value of the finance package exceeded that of the property. Also, with the rise of the popularity of pre-construction real estate (where buyers are often unsure) – there exists many reasons that indicate that it is worth undertaking housing finance rather than pay down a whole lump sum.”

Furthermore, it was only in 2005 that a number of legal changes related to the housing market were made which bought increased security for investors and developers which reinforced confidence. The Brazilian Chamber of the Construction Industry (Câmara Brasileira da Indústria da Construção, CBIC) stated (in their 2010 annual report): “the governmental decision to make housing a priority was of fundamental importance for the finance industry. In addition to contributing approximately 40 percent of the fixed investments in the country, the sustainable growth of the market can be allowed to take its natural course and necessary progress on the country’s infrastructural, logistical, energy, social and urban issues can also be made complementarily. We will be able to therefore boost our economic output whilst also developing the country and improve existing systems.”

Yet at the same time, as the rise of the market continues, concerns with regards to source of funding to support the growth in demand for housing remain. Whilst the Fundo do Garantia do Tempo de Serviço (FGTS) complements the law that mandates that 65 percent of bank savings funds need to be allocated to housing finance – the recent rhythm is reaching higher than what is available in Brazil’s banks coffers. It is therefore fundamental that new short term residential property funding avenues are searched – such as via the secondary markets which are currently largely focused on commercial / industrial real estate in Brazil. Experts believe that the Minister of Public Finance (Ministério da Fazenda) and the Central Bank (Banco Central) will be initiating measures to encourage more funding resources for the real estate sector to maintain its sustainable growth. Ana Maria Castelo also points to the obligations made by the Banco Central for banks to allocate more financial resources into the SBPE, stating: “the changes in the rules with regards to regulation in the housing finance markets in turn bought a horizon of greater security and, for both

17

consumers and the banks themselves, opportunities to gain.”

Brazil property experts also criticise the lack of real incentives in the market place and whilst instruments such as Real Estate Receivable Certificates (Certificados de Recebíveis Imobiliários, CRI) have existed since the late 1970s, the take up has been insignificant due to their high associated interest rates (although commercial CRIs remain popular). However, one encouraging sign in recent years was the change of the credit securitisation law in 2008 that enabled borrowers to benefit from tax exemptions.

To add more transparency into the housing finance marketplace, there are also plans for legal obligations of lenders to clearly state their terms to borrowers including all potential costs, interest and penalties. A new law (currently being passed through the National Congress) is expected to provide more security and peace of mind for borrowers – particularly as many continue remain weary with regards to their rights and obligations when using housing finance.

Whilst there remains much work to be done in developing what remains a very immature housing finance environment, steps are being taken in the right direction. At the close of 2010, data has revealed that the amount of housing finance as a proportion of Brazil’s GDP has reached 4 percent. Nevertheless, according to Ana Maria Castelo, whilst the next few years are likely to witness growth – it will be difficult for the banks to increase their loans books rapidly (as what occurred in 2007 when aggregate Brazilian lending levels doubled compared to what they were in 2006): “in addition to sustaining the level already achieved, the housing finance sector need to ensure that growth can continue,” she stated.

Back to Contents Page

11. Brazil’s Housing DeficitThe fact that the provision of housing in Brazil has improved cannot be denied – particularly when comparing to the 1990s where there was very little housing credit and low income earner programmes as what exists today as well as the lesser security for homeowners as mentioned above. Nevertheless, the issue of an insufficient supply of housing remains. Deficit predictions vary with the João Pinheiro Foundation believing that there were 7.2 million units by the close of 2010 – of this total, 90.3 percent were of families earning between one and three of the Brazilian minimum wage (the organisation point out that this does not take into account favela community dwellings and those which are sub-habitable which would certainly push this figure upwards). According to a survey conducted by Sinduscon-SP (the Union of Construction Industry of the State of São Paulo) and the Getúlio Vargas Foundation, the Brazilian housing deficit has remained virtually unchanged between 2008 and 2009. Using data from the IBGE (Brazilian In-stitute of Geography and Statistics), it was concluded that the deficit for 2008 was 5,799,859 and 5,808,547 in 2009. The data also showed a decrease in the number of makeshift dwellings by 6.8 percent from 3,780,113 in 2008 to 3,521,089 in 2009. Prior to the onset of the global downturn (between 2007 and 2008), the IBGE data estimated that 450,000 units were delivered to the entire market place but with growing demand – not to mention the population (which between 2000 and 2010 increased from 169 million to 185.7 million and the number of people per household from 3.79 to 3.34 in the same period, according to the 2010 national census) – there continues to be less supply than demand. The João Pinheiro Foundation’s analysis (for statistics leading to the close of 2008) pointed the deficit

18

representing 9.7 percent of the total stock of the country with the south-east (composed of Espírito Santo, Minas Gerais, Rio de Janeiro and São Paulo) having the largest proportion at 36.9 percent; followed – in order – by the north east (Maranhão, Piauí, Ceará, Rio Grande do Norte, Paraíba, Pernambuco, Alagoas, Sergipe and Bahia) at 35.1 percent; the south (Paraná, Santa Catarina and Rio Grande do Sul) at 10.5 percent; the north (Acre, Amapá, Amazonas,Pará, Rondônia, Roraima and Tocantins) at 10 percent and the centre west Goiás, Mato Grosso, Mato Grosso do Sul and the Distrito Federal).

The government itself is well aware that it will take some time for the balance of Brazilian housing supply and demand to come into equilibrium. At the close of 2010, Dilma Resident presented a housing plan at the annual Congress of Brazilian Construction in conjunction with the Getúlio Vargas Foundation (FGV) and the Federation of Industries of the State of São Paulo (FIESP). With the aim of constructing an average 1.8 million housing units annually until 2022 – demanding an annual cost of R$ 86.2 billion as at 2010 increasing to R$ 152.7 billion by 2022 (accounting for housing inflation and improved social mobility) the housing deficit is expected to hit 1.5 percent should expectations be met.

According to Melvyn Fox of the Brazilian Association of the Construction Material Industry (Associação Brasileira das Indústrias de Materiais de Construção, ABRAMAT), present at the event: “if we continue at the rhythm witnessed in the second half of 2009 and 2010, the country will have the ability to substantially reduce the deficit by 2022.” The achievement of this, he states, will depend on the growth of the credit markets; the successful implementation of programmes such as ‘Minha Casa, Minha Vida’; more efficient practices being undertaken in the construction industry (including the sales process); streamlining processes in what remains a hugely bureaucratic system as well as general factors related to the economy. “Brazil’s housing deficit has remained an issue for the country for many years. Today, the growth of the middle class and the changing overall face of Brazilian society is contributing to encourage the market but the ultimate solution lies in maintaining and creating structural actions that will function in the long term,” said Danilo Garcia, CNI industrial policy analyst.

One of the main debates that remain is the issue of the need to encourage more state based housing programmes (see below) – which work to the idiosyncrasies of each of the regions of Brazil – as opposed to having solely the National Habitation Plan (Plano Nacional de Habitação) in operation. Another concern relates to the standard of

19

existing housing in the country – it is estimated that 12 million households do not have basic access to sanitation. According to Edward Zaidan, economic director at Sinduscon-SP (Sindicato da Indústria da Construção Civil do Estado de São Paulo, Civil Construction Industry Union of São Paulo State): “most people in Brazil want to improve their living conditions and, as a result, the amount of searching is increasing to levels that have not been witnessed before.”

According to the projections of the City Ministry (Ministério das Cidades) – the number of new housing units required throughout Brazil will reach a further 23 million units. This, of course, brings encouraging news for the country’s housing developers – but also a concern as for the need to effectively manage the scaling up process as well as to improve infrastructure to support such rises and ensure that the barriers that confront the construction industry (such as high costs, labour issues, bureaucracy etc.) are reduced as much as feasibly possible.

Back to Contents Page

12. Brazil State Housing Programme ExamplesIn addition to national housing development public initiatives such as ‘Minha Casa, Minha Vida’ (see below), a number of regional programmes have emerged which are serving to act complementarily whilst also benefitting local economies. An example is the ‘Creditcasa’ programme underway in the state of Pará administered and managed by COHAB (Companhia de Habitação do Estado do Pará, the Housing Company of the State of Pará) which according to Vando Vidal, state secretary of finance: “will leave a strong imprint and, in addition to reducing the housing deficit, will boost the sales of construction materials.” Using a process known as ‘given credit’ (‘crédito outorgado’) – the beneficent uses the funds to pass on to the constructor to be used to purchase materials. The constructor can also offset Brazil’s value added tax (Impostos Sobre Circulação de Mercadorias e Prestação de Serviços, ICMS) against the cost of construction.

The Nova Mutum municipality in the state of Mato Grosso which is witnessing massive growth levels – both in terms of economic achievements (24 percent rise in 2009) and population (22 percent rise in 2009) – due to the arrival of several agro-business, bio energy and grain multinationals also has an interesting housing programme in operation. As a result of the rapid increase in the demand for housing, the ‘Tô Feliz’ project serves to work alongside the ‘Minha Casa, Minha Vida’ – upon its launch in 2010, the construction of 1,300 units is already underway in line with other infrastructural developments including a new school, technical college and wide scale sanitation improvements.

The ‘Subsídio à Moradia’ (Housing Benefit) programme in Paraíba – where constructors receive a bonus correspondent to the level of ICMS paid with an allocated initial budget of R$ 100 million – is expected to assist with the development of over 6,300 housing units in 111 state municipalities. According to Fransisco de Assis Benevides Gadelha, president of the Federation of Paraíba State Industries (Federação das Indústrias do Estado da Paraíba, FIEPB): “such funding activities are serving to facilitate business development in this niche whilst assisting the impor-tant issue of reducing the housing deficit.”

In the Rio Grande do Sul interior, the second most populous municipality of state Erechim has also witnessed a rapid amount of housing growth facilitated – according to Joselito Onhate director of housing development – by the elimination of a number of bureaucratic processes as well as rising demand levels. According to Onhate, between

20

January 2009 and August 2010, the 1,500 units that are in the construction process under the ‘Minha Casa, Minha Vida’ programme are being assisted by further industry incentives such as the ‘Paióis’ which enables constructor tax to be offset in addition to other subsidies to facilitate the build process. The municipality is also using state funding to improve sanitation, water provision and waste disposal facilities.

Back to Contents Page

13. Brazil’s Construction Industry After falling patterns up until the year 2004, Brazil’s construction industry has witnessed a solid amount of growth – particularly encouraged by a range of broad based macro economic factors including the Minha Casa, Minha Vida housing programme for low income earners (see below); the Growth Acceleration Programme (Programa de Aceleração do Crescimento PAC); rising credit opportunities for both constructors and buyers; improvements in regulatory processes including title ownership and, perhaps most importantly, a growing economy accompanied by factors such as lower unemployment facilitating an increased demand for homeownership.

At the close of 2010, the growth of construction reached 13.3 percent – 5.8 percent higher than what has been stated by the OECD as the average for the economy. A consensus has now clearly been reached amongst experts operating in the sector that the mild panic that hit the industry through the course of 2008 and 2009 has disappeared. Accord-ing to Fabio Romão, economist at LCA Consultants, in an interview with Valor Magazine: “the perspectives are good for all the sectors related to the construction industry.

21

Indeed, there are a number of other related industries that have and will continue to be positively benefitted from cement to paint manufacturers as well as retailers who are operating close to developments amongst others. The Brazilian Association of the Construction Material Industry (Associação Brasileira das Indústrias de Materiais de Construção, ABRAMAT) stated that the growth of the foundation and finishing industry will close 2010 at 16.9 percent. According to president Melvyn Fox: “we will recoup the drop in sales in 2009 over the course of 2011 in addition to approximately 13 percent of growth”. Vice president of the Union of Cement Industry (Sindicato Nacional da Indústria do Cimento, SNIC) stated: “in 2009 and 2010, Brazil’s cement industry has operated in a manner very different to the rest of the world – 2011 will see an increased growth rate heading back on track after a slow period” illustrating that it has come to a point where cement supply has become an issue in certain parts of the country, witnessing heavy real estate development, such as he north east (see below). According to Ana Maria Castelo in an interview with Conjuntura Econômica: “in 2010, more companies have focused on becoming more industrialised and productive which has required investments in technological development as well as methodologies that encourage sustainability and the effective use of labour.” Complementing these factors was the decision made in late 2010 that the govern-ment will extend tax cuts for building materials for an additional year after they expire on December 31st with Guido Mantega stating: “the construction industry has been one of the chief engines of Brazilian economic growth this year.”

According to the Getúlio Vargas Foundation, the volume of investments has also come back to pre-downturn levels which the organisation states as reaching R$ 258.6 billion for 2010 (43 percent higher than what was invested in 2009). The industry is of the firm belief that the brief recessionary period that was experienced in 2008/9, whilst taking its toll on the industry, failed to have the same effect as what occurred in many of the world’s most developed housing markets. In their 2010 annual report, the Brazilian Chamber of Commerce for the Construction Industry (Câmara Brasileira da Indústria da Construção, CBIC) Paulo Safady Simão stated: “these numbers represent a notable performance that emanate clear signs of recovery. The coming years look set for clear growth – boosted by the PAC programmes, the pre-salt oil findings, the World Cup 2014 and the Olympics 2016.” The governmental programmes have been seen to act as a major springboard for the growth of the housing construction sector with the aim of cater-ing for the C and D sectors (lower income earners who previously had very little access to finance). The main lender for this sector is the Caixa Ecônomica Federal who have been able to offer increasingly affordable rates – making the purchase by people in these groups much more viable (although a number of difficulties this sector of the industry have also emerged – discussed below). It is also widely rumoured that other major Brazilian banks will enter the low cost housing market such as Banco Itaú, Santander and Banco Real.

Construction sector equipment and machinery prices have also been gaining pace gradually. For 2010, the National Index of the Civil Construction Market (Índice Nacional do Custo da Construção Civil-Mercado, INCC-M) – which takes into account all components including labour, machinery and related services – averaged at 6.19 percent between January and September, compared to 2.62 percent in the same period in 2008 and 9.05 percent in 2009. Looked at individually, materials costs increased by 4.29 percent, fell by 2.22 percent and increased by 10.70 percent respective-ly in 2010, 2009 and 2008; services increased 5.33 percent, 3.61 percent and 6.82 percent and labour costs also rose by 8.02 percent, 7.07 percent and 7.92 percent in the same respective years. According to Ana Maria Castelo of the Getulio Vargas Foundation: “increases in construction material should be viewed positively with regards to the sustain-able growth of the housing market but the risk of their rapid rise in recent years could spell difficulties for making real estate development projects viable.”

Back to Contents Page

22

14. Labour Supply in the Construction IndustryIn 2009, according to the Annual Report on Social Information (Relação Anual de Informações Socias, RAIS), the number of workers in the construction industry stood at 2.11 million compared to 1.88 million in 2008 and 1.60 million in 2007. 2010 estimates are pointing to a total of over 2.46 million as a result of 300,000 formal employment posi-tions created this year. It is widely believed that, as Brazil’s construction industry continues to mature, this pattern will continue.

Whilst the statistics above represent positive indicators, issues related to a lack of an adequately qualified level of labour still remains amongst the construction industry. This has a situation that has been of concern for many years with most professionals pointing to a general attitude by most people that a job on a building site is really a ‘stop gap’ – according to Melvin Fox – president of the Brazilian Association of the Construction Industry and Materials (As-sociação Brasileira da Indústria de Materiais de Construção, ABRAMAT): “many people see working in the sector as a temporary solution whilst they can find something with, usually speaking, better pay and working conditions.”Published in June 2010, a civil construction poll – published by the Brazilian Construction Industry Chamber of Com-merce (Câmara Brasileira da Indústria da Construção, CBIC) and the National Confederation of Industry (Confedera-ção Nacional da Indústria, CNI) – 62 percent of all developers remained concerned about the lack of adequate labour for their projects.

In an attempt to minimise the effects, a number of construction companies have begun to invest heavily in profes-sional qualification and related initiatives aimed at focusing on personal development and company loyalty. Several companies are also developing bonus schemes aimed at incentivising workers who can meet set targets. These steps are being viewed as worthwhile, particularly in light of the majority of companies expecting growth in the medium to long term to be strong bringing a need to retain key members of their building teams. Ana Maria Castelo states: “today constructors are finishing off one project and starting another – therefore staffing longevity is becoming increasingly important.”

In 2009 in the state of São Paulo, there were approximately 45,000 construction employees undertaking professional training programmes – considered under what is necessary given the growth levels of the market. In the organisation’s annual report Edward Zaidan, economic director at Sinduscon-SP (Sindicato da Indústria da Construção Civil do Estado de São Paulo, Civil Construction Industry Union of São Paulo State) stated: “contrary to what the government believes, it is not the sole responsibility of the construction industry to develop such training programmes; there is a clear need for greater national policy to support this sector.” His comments are supported by Danilo Garcia, industrial policy analyst at the CNI in an interview with Conjuntura Econômica: “a rationally focused construction labour training programme is needed in addition to incentives for companies to enable to develop the skills and abilities of their building site staff.”

At the same time, however, it is worth noting that some steps are being taken in the right direction with 2010 statistics from the Department of Statistics and Socioeconomic Studies (Departmento Intersindical de Estatística e Estudos Socioeconômicos, DIESSE) illustrating that the number of technical schools offering construction training programmes has doubled in the last decade to 354. Yet, this is still generally considered as being too low in relation to the growth of the industry and, in an attempt to put pressure on the government, a number pilot programmes have subsequently been developed by the industry itself. One example has been created by the Brazilian Association of the

23

Construction Material Industry (Associação Brasileira das Indústrias de Materiais de Construção, ABRAMAT) in con-junction with the Brazilian Association of Technical Norms (Associação Brasileira de Normas Técnicas, ABNT) and the National Institute of Metrology, Normalisation and Industry Quality (Instituto Nacional de Metrologia, Normalização e Qualidade Industrial, INMETRO) – the project aims to look at the role of the construction worker (as well as other professions), examining what exactly the needs are in order to develop ways in which the industry can adapt to meet them. Another notable project developed by the National Federation of Industries of São Paulo State (Federação Nacional das Indústrias do Estado de São Paulo, FIESP) is the country’s construction college which, according to vice-preident José Carlos de Oliveira Lima: “is intended to act as an incubator for the construction industry where we can look at ways to develop, unify and consolidate the key issues to boost production.” DIESSE also stated the need to improve the working conditions on some of Brazil’s building sites, noting that a general ambiance of informality does not encourage labour usage optimisation.

Back to Contents Page

15. Low Income Housing / ‘Minha Casa, Minha Vida’The role of state bank Caixa Econômica Federal (CEF) in the low income (‘baixa renda’) market place has and looks set to continue to reform a sector of the industry in most need. According to Inês Magalhães of the National Ministry of Housing (Nacional de Habitação do Ministério) in an interview with Conjuntora Econômica, the CEF’s involvement with ‘Minha Casa, Minha Vida’ programme: “really started to push the market into the spotlight – especially for those who would not be usually awarded credit in the eyes of most banks.”

Nevertheless, the strong presence of the government has also bought problems for those who fall into the low income category. As it is the CEF that has sole responsibility for the administration of the ‘Minha Casa, Minha Vida’ credit line – housing executives are experiencing several bureaucracy related problems particularly with getting loans released. The practical reality of the implementation of the programme has appeared in 2010 and, by the close of quarter three, the CEF had approved approximately 275,000 units whereas double the amount of proposal to engage in the programme had been received. Perhaps of more concern was the fact that only 3,600 units were delivered up until August – one and half years after the initiation of the programme. Whilst it was announced in November that there had been a rapid increase in the number of contracts being awarded, a number of construction companies have begun to move away from being involved in the programme. According to Eduardo Gorayeb, president of the Rodo-bens construction company in an interview with the Examen magazine: “the speed of doing business that we are ac-customed to is different to that of the public powers.” Related to this is the fact that many of the Brazil’s constructors have developed a growing reluctance to engage in the programme due to lower profitability levels – an issue that has been exacerbated by the rising construction costs witnessed throughout the country. The Jotanunes company from Sergipe, for example, with revenue levels reaching R$ 200 million between 2009-10 (growing 180 percent for the last 2 years), were formerly very active in the lower income market but announced its intention to move into the Class C bracket stating in an interview with Examen magazine: “today, to touch a low income project we have to consider twice, maybe three times. The risk is far greater and, as a company, we do not want to tread this fine line.” The viability of implementing the programme for those between 3 and 6 times the minimum wage is also proving diffi-cult. According to João Alberto Viol of the National Union of Architects and Engineering Companies and Consultancies (Sindicato Nacional das Empresas de Arquitetura e Engenharia Consultiva, SINAENCO), in an interview with Conjun-

24

tura Econômica, the aim was for the programme to naturally develop and progress to serve this sector of Brazilian society – but due to difficulties in the administration of the programme for those earning between 1 and 3 times the minimum wage, what was intended to run co-existently has failed to take off as originally expected.

A further issue has risen as a result of where to locate of the ‘Minha Casa, Minha Vida’ units – which, it is claimed, is being lost under the weight of local government red tape leading to many projects not progressing. According to Inês Magalhães of the National Ministry of Housing (Nacional de Habitação do Ministério) in an interview with Conjuntora Econômica: “80 percent of Brazil’s municipalities have statistics that demonstrate a housing deficit but, paradoxically, the amount of land available remains high – the federal government is therefore working with state and municipality authorities to resolve this issue.”

Back to Contents Page

16. The Regeneration of Brazil’s Favelas (Urban Slums)A common comment of visitors to all of the major cities of Brazil is the presence of ramshackle buildings – known as ‘favelas’ – that remain co-existent and juxtaposed with middle and upper class neighbourhoods: a phenomenon that is noticed throughout Latin America.

Throughout 20th century, Brazil saw a number of architects and engineers develop programmes in an attempt to resolve the issue with varying levels of success. An example of this was during 1937 and 1964, when urban housing units were designed and constructed by prominent architectural and engineering figures such as Max Bill, Nabil Bondukim, Lucio Costa, Gregori Warchavchik and Affonso Reidy. It is said that the effects of military rule over the country effectively paralysed the growth of urban housing and, much of the problems that remain today would have been removed would the momentum created during those years have continued.

Part of the problem that remained until the 1980s was a general nonchalance on the part of city authorities and indeed the federal government itself to attempt to integrate the favela communities and their inhabitants into mainstream society. It was during this time when the state authorities began to operate more autonomously together with a constitutional amendment of 1988 that the agenda of fevela reformation began moving to the forefront. In the early 1990s, the ‘Favela-Bairro’ project was launched in Rio de Janeiro which saw a significant amount of public funds injected into several communities which, whilst viewed as a success in its own right, failed to really make a noticeable impact in terms of widescale reform. It was debatably the elections of Henrique Cardoso and subse-quently Lula da Silva, that saw the favela urbanisation pushed further into the spotlight – particularly as the country became ever concerned about its reputation to international visitors (for example, as a result of the World Cup 2014 and Olympic Games 2016 being awarded to Brazil). For this reason, a number of programmes have been announced in some of the major cities of Brazil which – whilst being debated from various perspectives – are considered to be looked at as important steps in the reduction and, perhaps, eventual elimination of the issue:

São Paulo Towards the east of the city, in the Praça do Lajeado neighbourhood – architects are working closely with community groups to improve the organisation of space whilst keeping costs to an absolute minimum. The result has been the

25

creation of a park, leisure areas and a football field. To the south-west, in Paraisópolis – the city’s second largest favela (60,000 inhabitants) and a region with such poor infrastructure that flooding regularly remains a problem – construction specialists have been developing a project entitled ‘Urbano Córrego do Antonico’ which attempts to deal with the major issues. Despite confronting difficulties with regards to the stream cuts through the region, specialists have developed a technically viable solution which has visibly evolved the living conditions of all the residents. The main transformation has been improvements to the underground drainage system (water is now also biologically filtered to mitigate the effects of pollution and contamination); the creation of spaces that avoid the congestion issues that are apparent in many favela communities; increased mobilisation for vehicles of various sizes; a wide scale tree-planting programme and the creation of what has been termed as an ‘urban beach’ environment which, according to Fernando Fernando de Mello Franco of MMBB, chief architect on the project: “aims to conceptualise special awareness, community integration and the ordinary life of the city.”

Belo HorizonteWhat makes the capital of Minas Gerais interesting in terms of its urban reform is that fact that 22 percent of its population (over 400,000) lives within 5 percent of the area – creating an intensified situation between the lower and upper classes. However, since 1993 the city has seen massive changes largely due to funding allocated via the Programme of Accelerated Growth (Programa de Aceleração do Crescimento, PAC). In recent years, as well as the creation of areas for communal use such as parks and other public space, many of the lower class neighbourhoods have witnessed significant transformation. The Prado Lopes favela, for example, has seen the development of recreational areas to encourage community integration whilst being supported by installations that prevent flooding and ground levelling programmes. In the Serra favela – home to over 50,000 residents – some of the main changes include the relocation of over 700 dilapidated households as well as extensive land regeneration, planting programmes, leisure areas, a skate park and squares. These reformations have also assisted the local economy in the form of employment creation (the majority of the works were undertaken by community residents) as well as an increase in the amount of businesses attracted to the area.

Rio de Janeiro The most notable announcement this year a programme to be implemented until 2020 entitled ‘Morar Carioca’ (broadly translated in English to mean ‘to live as a resident of Rio de Janeiro’) which will seek to implement the radical urbanisation of the city’s favelas. The project essentially aims to urbanise all of the communities that exist in Brazil’s second largest metropolitan region. The city’s growing international presence was stained twice in 2010 with a hostage taking situation in the wealthy south zone as well as reappearance of violence between gangs and the police in Rio de Janeiro. Whilst some have debated that tougher law enforcement, arising middle class and more pro-active policy making may well be decreasing the problems (viewed as particularly important as the World Cup 2014 and Olympic Games of 2016 draw closer) – the issue continues to remain prominent. According to Sonia Lopes, project coordinator of ‘Morar Carioca’ the programme “will work to establish a well-planned pathway to be able to offer every resident of Rio de Janeiro a standard of living to be expected from a modern and developed international city.”

The project is set to benefit over 240,000 families by 2020 and the local government has confirmed its partnership with the Brazilian Institute of Architects (Instituto de Arquitetos do Brasil, IAB-RJ) who will be responsible for the registration of companies involved with the projects; logistical management / coordination; working with teams of

26

engineers to effectively realise the projects and, in conjunction with the Municipal Secretary of Habitation (Secretaria Municipal de Habitação), will publicise and promote the project whilst ensuring the highest technical standards are being adhered to. The table below is an outline of the project cost estimations.

The execution of urbanisation projects will be undertaken with respect to the individual characteristics of the individual unit classification: Small settlements with less than 100 domiciles – works on overhaul of water supply systems, sewage supply, rainwater drainage, public illumination and paving; Favelas with between 100 and 500 domiciles – urbanisation plans will incorporate wide scale improvements to water supply systems, sewage supply, rainwater drainage, road access, internal vehicle circulation, leisure areas, landscaping and the elimination of high risk / dangerous areas as well as the implementation of urban regulation processes; Favelas with more than 500 domiciles – these will fall under 2 categories: • Partially urbanised – complementary provisions to serve existing infrastructure, namely: water supply systems, sewage supply, rainwater drainage, improvements to road / paving access, internal vehicle circulation, leisure areas, landscaping, public equipment, elimination of high risk / dangerous areas and the implementation of urban regulation processes; • Non-urbanised – a considerable level of residential construction will be combined with a range urbanisation projects including water supply systems, sewage supply, rainwater drainage, improvements to road / paving access, internal vehicle circulation, leisure areas, landscaping, public equipment, elimination of high risk / dangerous areas, the implementation of urban regulation processes, the promotion of new work opportunities for residents and conservation projects; • Favelas which are impossible to urbanise – at 122, these settlements are deemed as extremely difficult to create feasible urbanisation and residential projects. Families living in these communities will be re-housed under the Minha Casa, Minha Vida (My House, My Life) projects.

To regulate and integrate the city’s favelas into the formal system, the Rio de Janeiro government have developed a system of rules which will define how the urbanisation projects will be carried out as well as the ongoing management procedures post-works. The essential aim is to create an environment where residents can benefit most from the new living conditions whilst offering increased security, community support and organisation. All the favelas that do not have such systems in place will therefore be obliged to adhere to the established rules under the auspices of POUSOs – Postos de Orientação Urbanística e Social, ligados à Secretaria de Urbanismo (Urban and Social Guidance, attached to the Secretariat of Urbanisation). Today, there are currently 30 in operation in Rio’s favelas – consisting of engineers,

27

architects, social workers and other service providers as well as community development workers from the favelas themselves – with another 100 to be in place by 2020. POUSOs essentially represent the presence of the municipal government within the favelas whilst also legally regulating all real estate; supervising compliance with rules; ensuring that public / conservational areas are well maintained and soliciting other public / private organisations to deal with day to day management issues.