r international natural gas market university developments...

TRANSCRIPT

1

RICEUNIVERSITY

IEEJ: January 2007

International Natural Gas Market Developments to 2030

Peter Hartley

Professor, Economics Department

Kenneth B Medlock III

Fellow in Energy Studies, James A Baker III Institute for Public Policy

Adjunct Assistant Professor, Economics Department

James A. Baker III Institute of Public PolicyRICE UNIVERSITY

2

RICEUNIVERSITY

IEEJ: January 2007

Global Trends in Natural GasWorld natural gas demand doubled from 1980-2004

Average annual growth of 2.5% is triple that of oil and double the coal growth rate

Key reasons for the increase in demand :

Environmental pressure, wholesale electricity market competition, technical change (combined cycle gas turbines) and economic growth in Asia

The gas share may continue to rise if gas supplies transportation fuel

Possible challenges to a gas future include:

Lack of investor confidence, political instability in supplier nations, local opposition to infrastructure, slowdown to electricity reforms, alternative energy technologies perhaps assisted by further improvements in long-distance electricity transmission

Petroleum (46%)

Natural Gas (19%)

Coal (25%)

Hydroelectric (6%)Nuclear (3%)

Renewables, waste (1%)

Petroleum (39%)

Natural Gas (22%)

Coal (26%)

Hydroelectric (6%)Nuclear (6%)

Renewables, waste (1%)

Petroleum (38%)

Natural Gas (23%)

Coal (26%)

Hydroelectric (6%)Nuclear (6%)

Renewables, waste (1%)

1980 1990 2004

283.65 1015

BTU 347.32 1015

BTU 446.45 1015

BTU

Source: EIA

3

RICEUNIVERSITY

IEEJ: January 2007

Prices 2015, 2030

J

J

J

J

JJ

J

JJ

Beijing Buenos Aires Delhi Henry Hub Seoul Sydney Tokyo UK - NBP Zeebrugge$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

2015 price ($2005/mmbtu)

J annual growth 2010-15

J

JJ

J J

J

J

J J

Beijing Buenos Aires Delhi Henry Hub Seoul Sydney Tokyo UK - NBP Zeebrugge$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

2030 price ($2005/mmbtu)

J annual growth 2025-30

4

RICEUNIVERSITY

IEEJ: January 2007

Supply 2015, 2030

Europe (10%)

Russia (19%)

Other FSU (7%)

North America (24%)

South America (5%)

Qatar (2%)

Iran (3%)

Saudi Arabia (2%)

Other Middle East (3%)

North Africa (6%)

Other Africa (3%)

Australia, NZ, PNG (3%)

ASEAN (7%)China (2%)

Other Asia (3%)

World total 128.51 Tcf

Supply 2015

Europe (6%)

Russia (20%)

Other FSU (7%)

North America (13%)

South America (8%)

Qatar (3%)

Iran (5%)

Saudi Arabia (4%)

Other Middle East (6%)

North Africa (6%)

Other Africa (5%)

Australia, NZ, PNG (5%)

ASEAN (7%)China (2%)

Other Asia (2%)

World total 159.80 Tcf

Supply 2030

5

RICEUNIVERSITY

IEEJ: January 2007

Demand 2015, 2030

Europe (18%)

Russia (14%)

Other FSU (7%)

North America (28%)

South America (4%)

Qatar (0%)

Iran (3%)

Saudi Arabia (2%)

Other Middle East (4%)

North Africa (2%)Other Africa (1%)

Australia, NZ, PNG (1%)

ASEAN (4%)

China (4%)

Other Asia (8%)

World total 126.00 Tcf

Demand 2015

Europe (16%)

Russia (13%)

Other FSU (7%)

North America (27%)

South America (5%)

Qatar (0%)Iran (3%)

Saudi Arabia (2%)

Other Middle East (4%)

North Africa (2%)Other Africa (1%)

Australia, NZ, PNG (1%)

ASEAN (5%)

China (5%)

Other Asia (9%)

World total 154.61 Tcf

Demand 2030

6

RICEUNIVERSITY

IEEJ: January 2007

Natural gas trade

Eu

rop

e

Ru

ssia

Oth

er F

SU

Nor

th A

mer

ica

Sou

th A

mer

ica

Qat

ar

Iran

Sau

di A

rabi

a

Oth

er M

idd

le E

ast

Nor

th A

fric

a

Oth

er A

fric

a

Au

stra

lia,

NZ

, PN

G

ASE

AN

Ch

ina

Oth

er A

sia-25

-20

-15

-10

-5

0

5

10

15

Tcf per year

2015

2030

Overall Exports (+) and Imports (-)

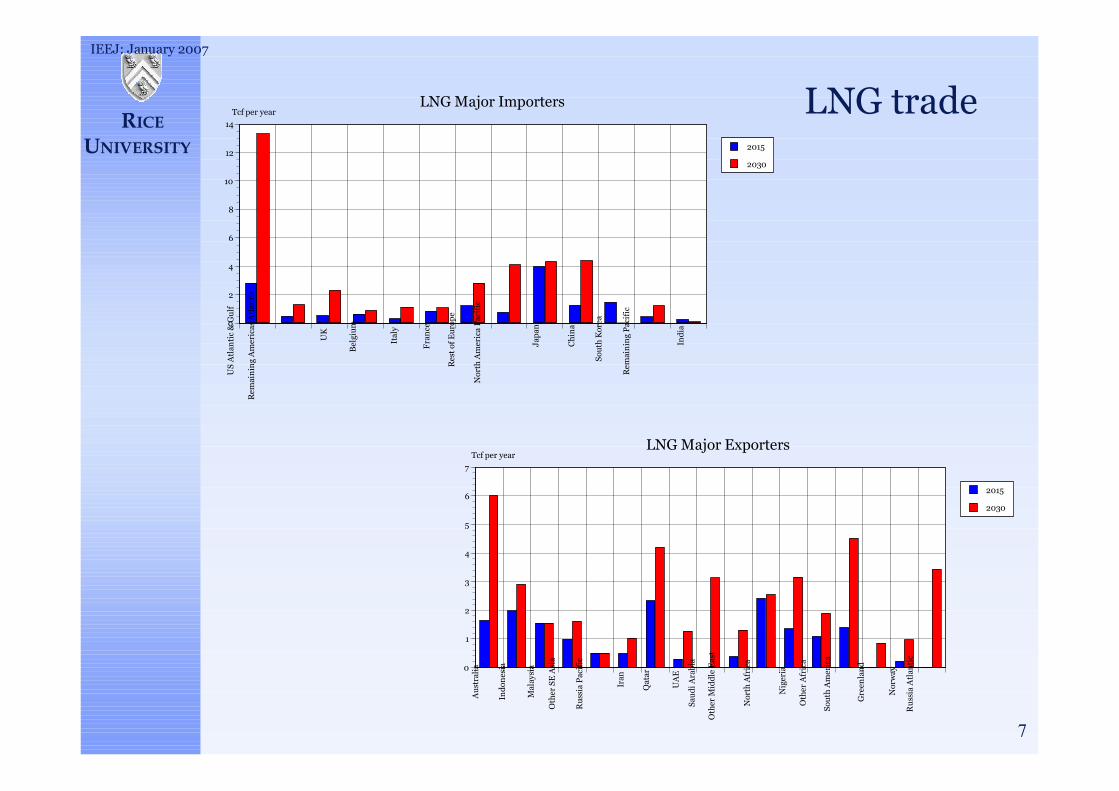

7

RICEUNIVERSITY

IEEJ: January 2007

LNG trade

US

Atl

anti

c &

Gu

lf

Rem

ain

ing

Am

eric

as A

tlan

tic

UK

Bel

giu

m

Ital

y

Fra

nce

Res

t of

Eu

rop

e

Nor

th A

mer

ica

Pac

ific

Jap

an

Ch

ina

Sou

th K

orea

Rem

ain

ing

Pac

ific

Ind

ia

0

2

4

6

8

10

12

14

Tcf per year

2015

2030

LNG Major Importers

Au

stra

lia

Ind

ones

ia

Mal

aysi

a

Oth

er S

E A

sia

Ru

ssia

Pac

ific

Iran

Qat

ar

UA

E

Sau

di A

rab

ia

Oth

er M

idd

le E

ast

Nor

th A

fric

a

Nig

eria

Oth

er A

fric

a

Sou

th A

mer

ica

Gre

enla

nd

Nor

way

Ru

ssia

Atl

anti

c

0

1

2

3

4

5

6

7

Tcf per year

2015

2030

LNG Major Exporters

8

RICEUNIVERSITY

IEEJ: January 2007

Natural Gas Demand: Short and Long Run Substitution

9

RICEUNIVERSITY

IEEJ: January 2007

US Natural Gas Demand: 1984-2005The US experience provides evidence of fuel switching

The demand driver has also changed from industrial activity and space heating to power generation

Average Annual Growth Rate approximately 1% per year

JJ

J

J J J JJ J J

JJ

JJ

J J

J

J

J

JJ

J19

84

198

5

198

6

198

7

198

8

198

9

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

200

0

200

1

200

2

200

3

200

4

200

50

5

10

15

20

25

$0

$1

$2

$3

$4

$5

$6

$7

$8

$9

US Natural Gas Consumptin (Tcf) J US City Gate Price ($2005/Tcf)

10

RICEUNIVERSITY

IEEJ: January 2007

Linkage of crude oil and natural gas prices

US markets show strong evidence of a link between natural gas and oil prices:

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$/mmbtu

Diesel Fuel Residual Fuel Oil Natural Gas Coal Refiner Acquisition Cost of Crude

11

RICEUNIVERSITY

IEEJ: January 2007

What links oil and gas prices?

Demand factors

Substitution in the generation of electricity

Substitution in industrial processes –refining, electricity cogeneration – but in sectors such as chemicals high gas prices cut demand without fuel switching

Substitution between gas and heating oil for space heating

Supply factors

Joint production of natural gas and oil can have positive or negative effectsIncreased oil production also yields additional associated gasHigher oil prices also raise the value of non-gas liquids often produced with gasHowever, gas can also be re-injected to enhance oil recovery

Unconventional oil, such as Canadian tar sands, requires natural gas as input

Gas-to-liquids (GTL) conversion (as in Qatar) can lead to direct competition between gas and oil for providing transportation fuel

Impediments to substitution

Environmental factors can affect demand side substitution of oil for gas

Short run capital costs can slow development of alternative supplies

Uncertainty about future energy prices limits willingness to invest

Economies of scale for GTL versus LNGGTL only makes economic sense for smaller scale projects or if oil prices are high

12

RICEUNIVERSITY

IEEJ: January 2007

RWGTM Price Forecast in Historical Context

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040$0

$2

$4

$6

$8

$10

$12

$14

$2005/mmbtu

Actual US RACC ($2005/mmbtu)

EIA World Oil Price Forecast ($2005/mmbtu)

Actual US Wellhead Prices ($2005/mmbtu)

Calculated US Gas Price ($2005/mmbtu)

Oil price forecast is from the US Energy Information Administration

Gas price forecast is the equilibrium calculated by the RWGTM

The generally rising ratio of gas to oil prices reflects the assumption that gas tends to supply more energy as economies develop

13

RICEUNIVERSITY

IEEJ: January 2007

Natural Gas Supply: Geography, Geology and Geopolitics

14

RICEUNIVERSITY

IEEJ: January 2007

Supply estimates

RegionProved

ReservesaUndiscovered

ResourcebShare of Total

ResourceMiddle East 2565.4 1294.7 34.4%

Qatar 910.5 41.1 8.5%Saudi Arabia 241.8 681.0 8.2%Iran 971.2 314.6 11.5%

Former Soviet Union 1952.6 1611.3 31.8%Russia 1680.0 1168.7 25.4%

Asia-Pacific 391.6 688.9 9.6%Indonesia 97.8 107.7 1.8%Australiac 27.6 338.4 3.3%

Africa 485.8 330.1 7.3%Nigeria 184.7 123.2 2.7%Algeria 160.5 49.0 1.9%

North Americac 265.1 451.5 6.4%Central and South America 250.8 421.0 6.0%

Venezuela 151.4 101.2 2.3%Europe 200.7 312.4 4.6%

Norway 84.3 183.0 2.4%World Totald 6112.1 5109.8

a - Oil and Gas Journal as of Jan. 1, 2006b - Compiled from USGS, ABARE, and other national sourcesc - Includes assessed non-conventional natural gas resourcesd - Does not include future growth in existing fields. USGS estimates the World Total at 3305 tcf.

15

RICEUNIVERSITY

IEEJ: January 2007

Linking supply with demand

16

RICEUNIVERSITY

IEEJ: January 2007

Concluding Remarks

17

RICEUNIVERSITY

IEEJ: January 2007

Concluding Remarks

Modeling illustrates the key roles Russia and the countries of the Middle East will play in the world gas market

Prices will be linked through global arbitrage

Trade need not actually occur, there simply needs to exist the ability to trade – LNG provides this capability

Long distance international gas trade provides opportunities forcountries to gain from cooperation, but also to lose from conflict

Absent political constraints, there appears to be substantial gas available to satisfy demand at a reasonable price

Political constraints may, however, present the largest impediment to globalization

Such political constraints may encourage alternative sources of supply and ultimately alternative sources of energy

The development of alternative energy sources later this century will likely mean that substantial natural gas resources will not be exploited for a very long time, if at all

Contact: [email protected]