presentation made by sana muqadas

TRANSCRIPT

Presentat ion ByPresentat ion ByAanalys i sn OfFinancial Statement

Presented ToPresented ToS ir Amir I lyas

Group Leader Naila Latif

(D1F13MCOM0009)Group Member

Qurat-ul-ain(D1F13MCOM0026)

Sana Muqadas(D1F13MCOM0004)

TOPIC IS INTRODUCTION TO LONG-TERM ASSETS

Long-term Assets:

Long-term assets are resources that are used to generate operating revenues (or reduce operating costs) for more than one period. Major long-term assets include property, plant, equipment, intangibles, investments, and deferred charges.

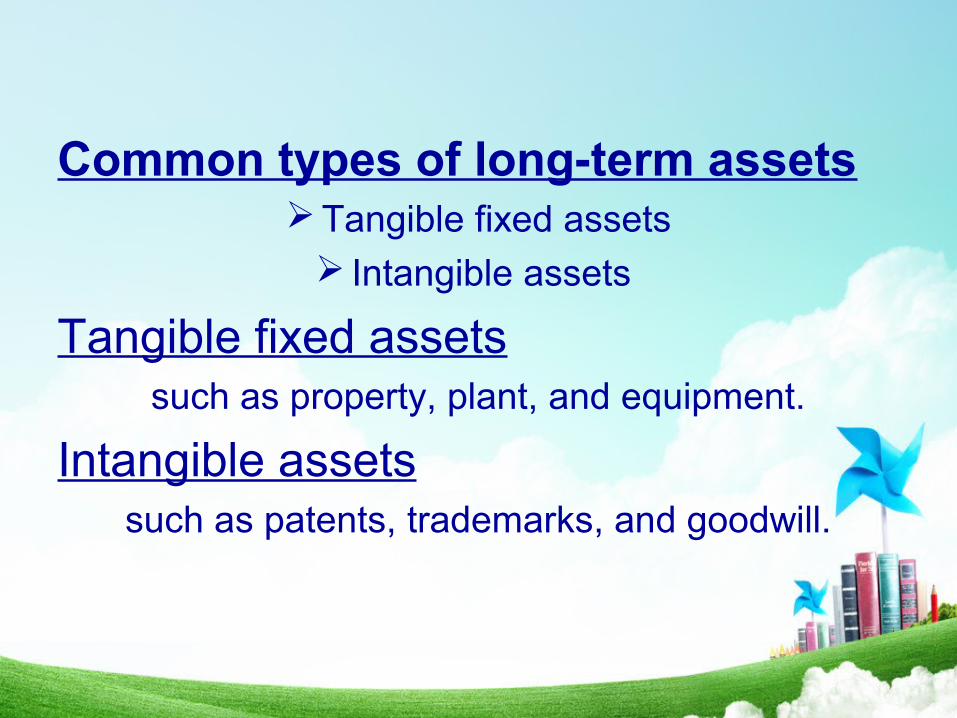

Common types of long-term assets Tangible fixed assets

Intangible assets

Tangible fixed assetssuch as property, plant, and equipment.

Intangible assetssuch as patents, trademarks, and goodwill.

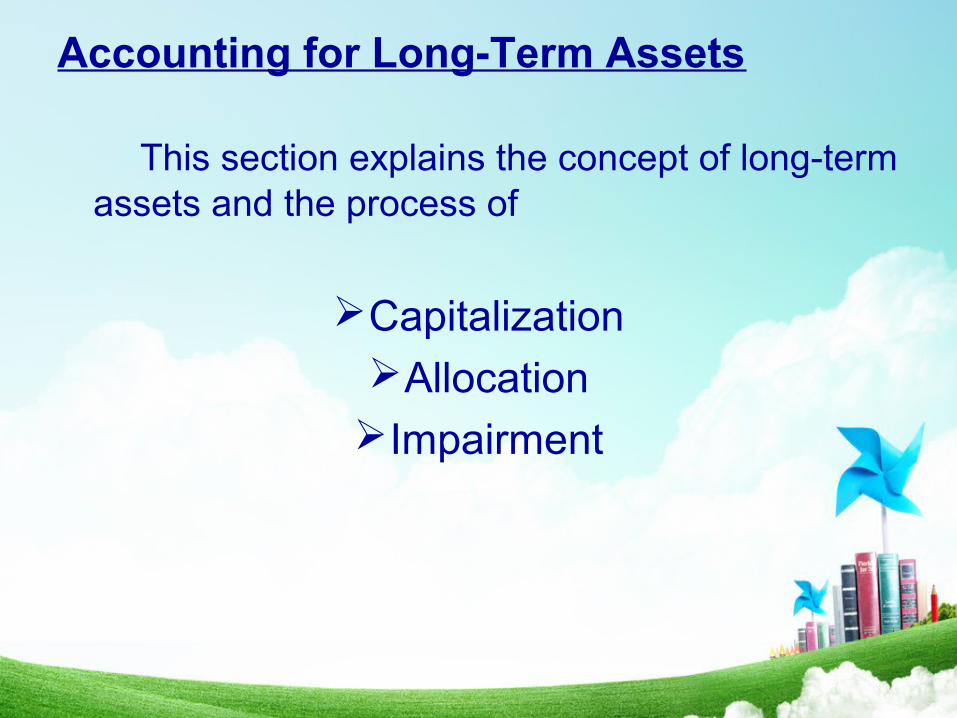

Accounting for Long-Term Assets

This section explains the concept of long-term assets and the process of

CapitalizationAllocationImpairment

Capitalization : capitalization is the process of deferring a

cost that incurred in the current period, but whose benefits are expected to extend to one or more future periods.Directly effect on balance sheet rather than immediate record in income statement.

• Soft assets: such as R&D and wages cost capitalization

is more problemetic.

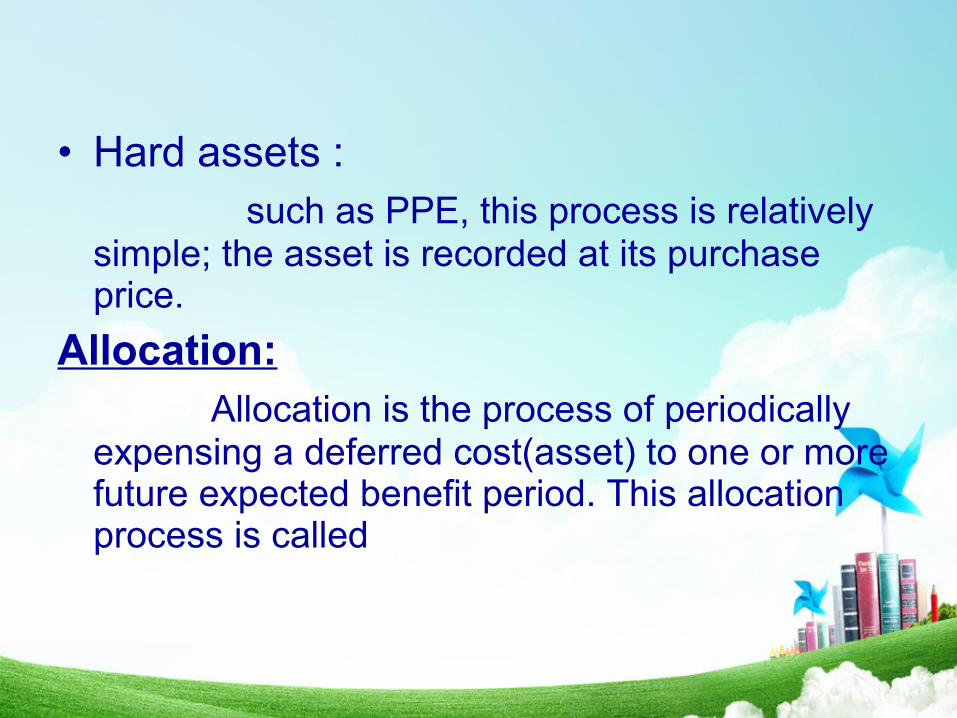

• Hard assets : such as PPE, this process is relatively

simple; the asset is recorded at its purchase price.

Allocation: Allocation is the process of periodically

expensing a deferred cost(asset) to one or more future expected benefit period. This allocation process is called

• Depreciation:Applied on tangible fixed assets.

• Amortization:Applied on intandible assets.

• Depletion: Applied on natural resources. such as gas, oil etc. Three factors determine the cost allocation

amount_1) useful life, 2) salvage value, 3) allocation method.each factors requires estimates-estimates that involve managerial discretion and effect of these estimates on financial statement, especially when estimates change.

Impairment : Impairment is the process of writing downthe book value of the asset when its expected cashflows are no longer sufficient to recover the remainingcost reported on the balance sheet.when the depreciated amount of an asset is estimated to be

higher than its current estimated value (often, its market value), then its amount on the balance sheet is written down to reflect its current value. Such a write-down (or write-off) is termed impairment.

Capitalizing vs Expensing:

Financial Statement and Ratio Effects: