poultry industry trends - astral foods : home results...poultry industry trends financial overview...

TRANSCRIPT

Interim Results Presentation

for the six months ended 31 March 2015

2

AGENDA

Business Overview

Poultry Industry Trends

Financial Overview

Industry Matters

Prospects

Q & A

2

3

BUSINESS OVERVIEW

4

THE PERIOD IN PERSPECTIVE

Revenue

Operating profit

Earnings per share

Headline earnings per share 159%

The period under review reflects an improved performance assisted by higher poultry and

feed volumes with increased poultry sales realisations

Financial

Indicators

4

166%

158%

22%

5

THE PERIOD IN PERSPECTIVE

Increase in poultry sales volumes, in particular from the expansion at County Fair in the

Western Cape which now processes broilers supplied by Tydstroom (550 000 bpw)

Good poultry sales realisations coupled with lower stock levels and the post-festive

season demand for poultry products exceeding seasonal expectations

Good poultry production efficiencies, in particular an improved mortality rate together

with no cutbacks versus the comparative period have supported poultry sales volumes

Expansion in feed volumes that now includes production of feed from the Standerton feed

mill previously supplied by Afgri in Kinross

Healthy global maize and soya crops which resulted in the softening of grain prices and

subsequently benefited feed prices and livestock production costs

5

6

THE PERIOD IN PERSPECTIVE

Poultry imports continued at high levels with little impact from the EU anti-dumping

remedies

Depreciation of the Rand against the US Dollar eroding some of the benefits of

lower CBOT corn prices

Load shedding, especially unplanned, had an impact and a direct cost to the Group

of approximately R4 million

Currency weakness in Zambia and Mozambique negatively impacting raw material

costs and profitability

6

7

POULTRY DIVISION

8

Operating profit - R million

Operating profit up 680%

• Net margin 7.8% 1H2014: 1.4%

• Feed costs down 2.3%

Revenue - R million

Revenue up 36%

• Broiler volumes up 20%

• Broiler selling prices up 13%

3 317

4 503

-

1 000

2 000

3 000

4 000

5 000

1H2014 1H2015

45

351

-

50

100

150

200

250

300

350

1H2014 1H2015

POULTRY DIVISION - OVERVIEW

8

9

Broiler sales volumes increased year-on-year by 19.9% (Slide 10)

Broiler selling prices increased year-on-year by 12.8%

Product mix improvement with fresh increasing by 2% and IQF reducing by 1%

Improved broiler production efficiencies – improved mortality rate

Average broiler feed price decreases year-on-year by 2.3%

Continued high level of poultry imports ≈ March 2015 @ 7.2 million bpw

POULTRY DIVISION - OVERVIEW

9

10

53%

5%

10%

7%

3%

22%

Product Mix

POULTRY DIVISION – SALES

53%

4%

12%

7%

4%

21%

239 534 Tons Volume increase ≈ 20%

199 838 Tons

1H2014 1H2015

10

11

Poultry Production Volume Growth

POULTRY DIVISION - PRODUCTION

11

Farm efficiencies = 62 000 bpw

Increased placements = 170 000 bpw

Average birds per week

(increase of 790 000 birds ≈ 18,9%)

Tydstroom = 558 000 bpw

1H

2014 =

4,1

71,0

00

1H

2015 =

4,9

61,0

00

13.3%

4.1%

1.5%

12

70%

75%

80%

85%

90%

95%

100%

105%

110%

115%

120%

F2009 F2010 F2011 F2012 F2013 F2014 F2015

Mortality Feed conversion (FCR) Efficiency factor (PEF)

BROILER PRODUCTION PERFORMANCES

Key indicators base-lined to 100% in 2009

12

13

95%

96%

97%

98%

99%

100%

101%

102%

103%

104%

105%

106%

F2009 F2010 F2011 F2012 F2013 F2014 F2015

Slaughter age Live weight Processing yield

BROILER PRODUCTION PERFORMANCES

Key indicators base-lined to 100% in 2009

13

14

Projected higher feed costs in the second half of the reporting period

Broiler production efficiencies should uphold current positive performance

Slaughter volumes of approximately 5 million birds per week

Favourable market conditions for poultry to continue into 2H2015

Improved product mix towards fresh as a result of “Tydstroom” volumes

Supply to KFC “now” commenced from mid-April 2015

POULTRY DIVISION - PROSPECTS

14

15

FEED DIVISION

16

Operating profit - R million

Operating profit up 18%

• Net margin at 6.3% 1H2014: 6.2%

• Benefit from increased volumes

Revenue - R million

Revenue up 16%

• Sales volumes up 17%

• Avg. realisation down

FEED DIVISION - OVERVIEW

2 550

2 961

-

1 000

2 000

3 000

1H2014 1H2015

157

186

-

50

100

150

200

1H2014 1H2015

16

17

FEED DIVISION - OVERVIEW

Feed volumes increased by 17.2% due to higher inter-group volumes (up 36.6%)

Rand per ton margin maintained on prior year despite a competitive landscape

Inflationary costs were successfully recovered from the market

Profitability in the livestock markets positively impacted feed sales

Standerton feed mill producing on average 23 000 tons of feed per month

(ex Afgri 15 200 tons)

17

18

60%

8%

20%

12%

Meadow Feeds - Sales Mix

FEED DIVISION – SALES

52%

10%

23%

15%

605 066 Tons

1H2014 1H2015

708 969 Tons Volume increase ≈ 17%

18

19

FEED DIVISION - PROSPECTS

Current maize crop estimate of 9,8 million tons – smallest crop since 2007

Maize import opportunities into the coastal regions

Increasing local maize prices with upward pressure on feed prices

Lower soya prices in 2H2015 will partly offset the impact of higher maize prices

International maize and soya balance sheets remain healthy

Focus on Rand per ton margins to continue

19

20

OTHER AFRICA DIVISION

21

OTHER AFRICA DIVISION - OVERVIEW

Operating profit - R million

Operating profit up 24%

• Net margin 5.3% 1H2014: 4.4%

• Exchange rate impact

Revenue - R million

Revenue up 3%

• Feed volumes up 5%

• Hatchery volumes up 36%

248 256

-

50

100

150

200

250

1H2014 1H2015

11

14

-

3

5

8

10

13

15

1H2014 1H2015

21

22

OTHER AFRICA DIVISION - OVERVIEW

Zambia

Profitability at Tiger Animal Feeds impacted negatively by currency exchange

movements

Improved earnings in 1H2015 at Tiger Animal Feeds versus 1H2014

Tiger Chicks sales volumes increased by 29% over comparative period

Mozambique & Swaziland

Profitability at Meadow Mozambique impacted negatively by currency exchange

movements

Good performance from National Chicks Swaziland due to lower hatching egg

costs and improved hatchability

22

23

INDUSTRY TRENDS

24 Source: CJA Strategic Risk Brokers

F2011 F2012 F2015 F2013 F2014

SAFEX YELLOW MAIZE PRICE

24

F2010

Refer Slide 50

25 Source: CJA Strategic Risk Brokers

SAFEX SOYA BEANS PRICE

25

F2011 F2012 F2015 F2013 F2014 F2010

Refer Slide 50

26

INDUSTRY BROILER SELLING PRICES

Source: SAPA 26

13.2

2

13.4

7

13.4

1

12.7

0

11.9

6

11.9

5

11.7

5

12.2

2

11.7

5

11.7

6

12.2

9

11.8

3

12.3

3

12.8

3 13.5

1

13.3

4

13.4

2

13.2

0

13.3

8

13.4

6

13.1

8

12.7

9

12.8

6 13.5

6

13.9

1

14.9

0

15.5

3

14.5

1

13.6

6

13.2

1

13.4

2

13.1

5

12.6

7

12.5

1 1

3.4

0

15.0

3 15.7

9

15.5

5

14.8

2

13.8

5

14.0

8

15.5

3

15.3

5

15.2

4

15.0

7

15.4

2

15.4

4

16.0

1

16.2

7

16.2

6 17.0

5

16.1

5

16.6

0

16.8

8

16.9

7

17.1

3

17.2

3

15.9

4 1

6.9

6

16.7

4

17.4

4

18.4

8

18.6

8

17.6

9

17.8

1

17.9

8

11.00

11.50

12.00

12.50

13.00

13.50

14.00

14.50

15.00

15.50

16.00

16.50

17.00

17.50

18.00

18.50

19.00

19.50

Oct-

09

Dec-0

9

Fe

b-1

0

Ap

r-10

Ju

n-1

0

Au

g-1

0

Oct-

10

De

c-1

0

Fe

b-1

1

Ap

r-11

Ju

n-1

1

Au

g-1

1

Oct-

11

Dec-1

1

Fe

b-1

2

Ap

r-12

Ju

n-1

2

Au

g-1

2

Oc

t-1

2

Dec-1

2

Fe

b-1

3

Ap

r-13

Ju

n-1

3

Au

g-1

3

Oct-

13

Dec-1

3

Fe

b-1

4

Ap

r-14

Ju

n-1

4

Au

g-1

4

Oct-

14

Dec-1

4

Fe

b-1

5

Broiler selling price Six month average

Rand per kilogram

27

Source: SAPA & CJA Strategic Risk Brokers

BROILER PRICE VS FOOD PRICE INFLATION

27

85

90

95

100

105

110

115

120

125

130

135

140

85

90

95

100

105

110

115

120

125

130

135

140

Oct-

09

Dec-0

9

Fe

b-1

0

Ap

r-10

Ju

n-1

0

Au

g-1

0

Oct-

10

Dec-1

0

Fe

b-1

1

Ap

r-11

Ju

n-1

1

Au

g-1

1

Oct-

11

Dec-1

1

Fe

b-1

2

Ap

r-12

Ju

n-1

2

Au

g-1

2

Oct-

12

Dec-1

2

Fe

b-1

3

Ap

r-13

Ju

n-1

3

Au

g-1

3

Oct-

13

Dec-1

3

Fe

b-1

4

Ap

r-14

Ju

n-1

4

Au

g-1

4

Oct-

14

Dec-1

4

Fe

b-1

5

Ind

ex

(O

ct

20

09

= 1

00

)

Poultry selling price index SA food price index

28

Source: SAPA & Own Data

CHANGE IN BROILER SELLING PRICE VS FEED PRICE

28

-30%

-20%

-10%

0%

10%

20%

30%

40%

Oct-

09

Dec-0

9

Fe

b-1

0

Ap

r-10

Ju

n-1

0

Au

g-1

0

Oct-

10

Dec-1

0

Fe

b-1

1

Ap

r-11

Ju

n-1

1

Au

g-1

1

Oct-

11

Dec-1

1

Fe

b-1

2

Ap

r-12

Ju

n-1

2

Au

g-1

2

Oct-

12

Dec-1

2

Fe

b-1

3

Ap

r-13

Ju

n-1

3

Au

g-1

3

Oct-

13

Dec-1

3

Fe

b-1

4

Ap

r-14

Ju

n-1

4

Au

g-1

4

Oct-

14

Dec-1

4

Fe

b-1

5

% Change in feed price % Change in broiler selling price

29

-

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

45 000

50 000

Oct-

09

Dec-0

9

Fe

b-1

0

Ap

r-10

Ju

n-1

0

Au

g-1

0

Oct-

10

Dec-1

0

Fe

b-1

1

Ap

r-11

Ju

n-1

1

Au

g-1

1

Oct-

11

Dec-1

1

Fe

b-1

2

Ap

r-12

Ju

n-1

2

Au

g-1

2

Oct-

12

Dec-1

2

Fe

b-1

3

Ap

r-13

Ju

n-1

3

Au

g-1

3

Oct-

13

Dec-1

3

Fe

b-1

4

Ap

r-14

Ju

n-1

4

Au

g-1

4

Oct-

14

Dec-1

4

Fe

b-1

5

Total poultry imports 6 per. Mov. Avg. (Total poultry imports)

Tons

Source: SAPA

POULTRY IMPORTS PER MONTH

29

30

FINANCIAL OVERVIEW

31

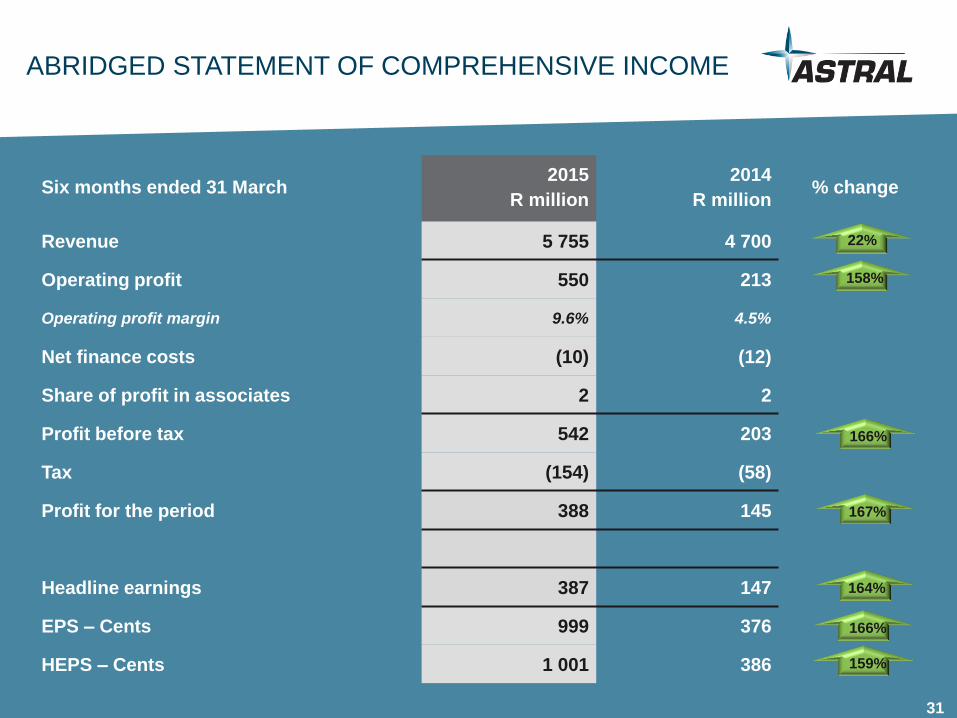

ABRIDGED STATEMENT OF COMPREHENSIVE INCOME

Six months ended 31 March 2015

R million

2014

R million % change

Revenue 5 755 4 700

Operating profit 550 213

Operating profit margin 9.6% 4.5%

Net finance costs (10) (12)

Share of profit in associates 2 2

Profit before tax 542 203

Tax (154) (58)

Profit for the period 388 145

Headline earnings 387 147

EPS – Cents 999 376

HEPS – Cents 1 001 386

22%

158%

166%

167%

164%

159%

166%

31

32

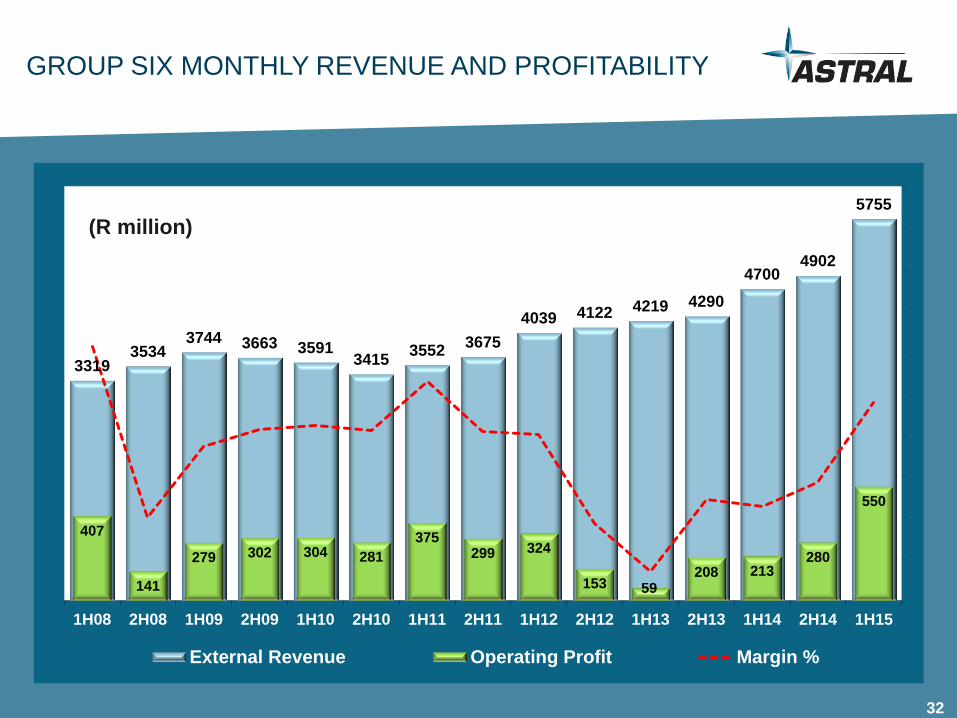

3319 3534

3744 3663 3591 3415

3552 3675

4039 4122 4219 4290

4700 4902

5755

407

141

279 302 304 281

375 299 324

153 59 208 213

280

550

0

200

400

600

800

1000

1200

1400

1600

1800

2000

0

1000

2000

3000

4000

5000

6000

1H08 2H08 1H09 2H09 1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14 2H14 1H15

External Revenue Operating Profit Margin %

GROUP SIX MONTHLY REVENUE AND PROFITABILITY

(R million)

32

33

2581 2449 2606 2652 2878 2956 2952 3049

3317 3650

4503

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

6000

1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14 2H14 1H15

Revenue Change in realisations (SAPA) Change in volumes

POULTRY – SIX MONTHLY REVENUE

33

(R million)

34

1847 1730 1708 1770

2175 2152 2397 2519 2550

2956 2961

0

0

0

1

1

1

1

1

2

1000

1500

2000

2500

3000

3500

4000

4500

1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14 2H14 1H15

Revenue Change in volumes Change in feed price

FEED – SIX MONTHLY REVENUE

34

(R million)

35

GROUP SIX MONTHLY OPERATING PROFIT

35

(R million)

134 128 229 124 140

-3 -117 5

45 59 351

151 130

133

149 154

135 156 173 157 197

186 304

281

375 299 324

153 59 203 213

280

550

-0.1

0.1

0.3

0.5

0.7

0.9

1.1

1.3

1.5

-120

-20

80

180

280

380

480

580

680

1H10 2H10 1H11 2H11 1H12 2H12 1H13 2H13 1H14 2H14 1H15

Poultry Feed Other Africa

Change in feed price Change in realisations (SAPA) Broiler volumes

Feed volumes

36

ABRIDGED STATEMENT OF FINANCIAL POSITION

March 2015

R million

September 2014

R million % change

Non-current assets 2 203 2 242

Net working capital 341 452

Current assets (excl. cash) 2 006 2 003

Current liabilities (excl. borrowings) (1 665) (1 551)

Non-current liabilities (excl. borrowings) (558) (575)

Net assets 1 986 2 119

Net (surplus) / debt (240) 174

Loans 183 206

Cash and cash equivalents (423) (32)

Equity 2 226 1 945

Total 1 986 2 119

2%

3%

6%

14%

6%

36

25%

7%

37

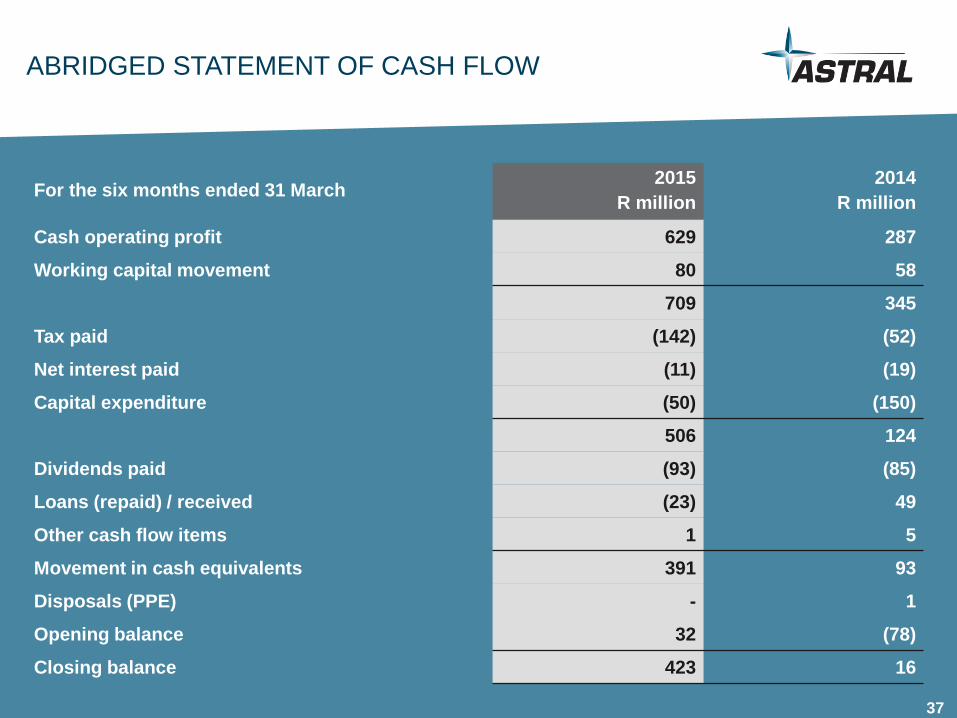

ABRIDGED STATEMENT OF CASH FLOW

For the six months ended 31 March 2015

R million

2014

R million

Cash operating profit 629 287

Working capital movement 80 58

709 345

Tax paid (142) (52)

Net interest paid (11) (19)

Capital expenditure (50) (150)

506 124

Dividends paid (93) (85)

Loans (repaid) / received (23) 49

Other cash flow items 1 5

Movement in cash equivalents 391 93

Disposals (PPE) - 1

Opening balance 32 (78)

Closing balance 423 16

37

38

CAPITAL EXPENDITURE

Six months ended 31 March 2015

R million

2014

R million

Depreciation 73 69

Replacement capex 41 74

Expansion capex 9 82

Total capex 50 156

Commitments 83

Total spent and committed 133

38

39

IN SUMMARY

39

Poultry division now at a more normalised profit margin level

Poultry division benefited from various volume growth initiatives

Feed division benefited from Standerton feed mill contribution

Cash flow for the period positive

Net surplus cash R240 million (30 Sep 2014: Net debt to equity ratio of 8.9%)

Interim dividend of 575 cents per share declared

40

INDUSTRY MATTERS

41

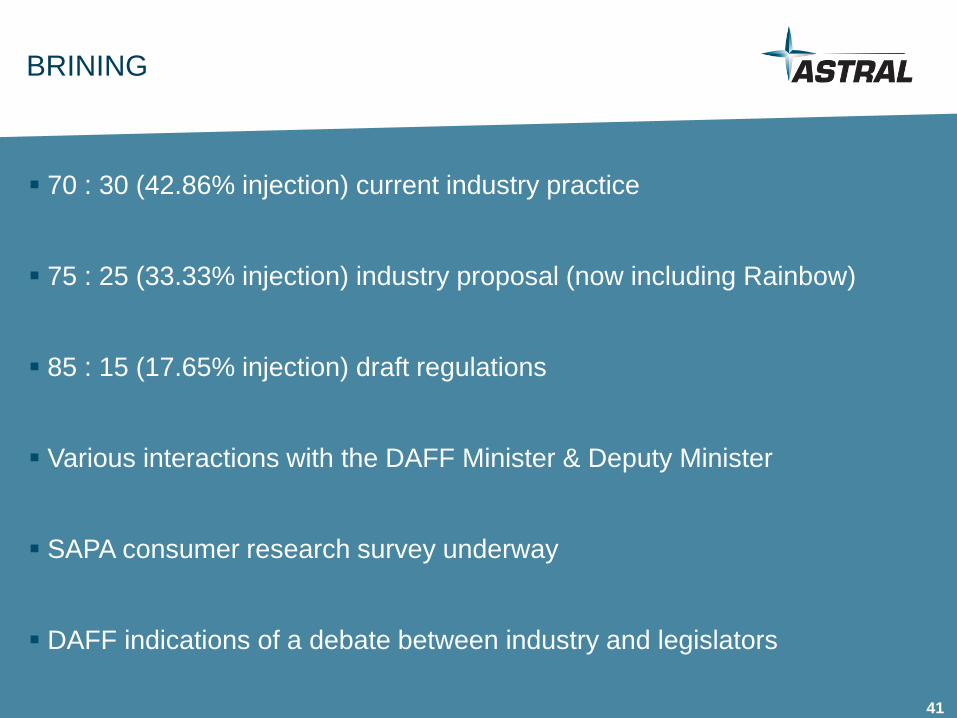

BRINING

70 : 30 (42.86% injection) current industry practice

75 : 25 (33.33% injection) industry proposal (now including Rainbow)

85 : 15 (17.65% injection) draft regulations

Various interactions with the DAFF Minister & Deputy Minister

SAPA consumer research survey underway

DAFF indications of a debate between industry and legislators

41

42

IMPORTS (EU & US)

On 27 Feb 2015 anti-dumping duties were imposed on Germany,

Netherlands and United Kingdom

Duties range from 3.86% to 73.33% on frozen bone in chicken portions

Outbreaks of AI in all three EU countries has interrupted imports into RSA

US demanding export leg quarter volumes to RSA duty free for AGOA

renewal

Poultry industry bodies of both countries not in agreement on quota

42

PROSPECTS

44

PROSPECTS

The slowing level of growth in the economy and higher unemployment levels

will continue to hamper an increase in the per capita consumption of poultry.

If a quota on US poultry imports is agreed to on the back of the AGOA

renewal this is likely to negatively impact local producers.

The South African maize crop currently being harvested is estimated to be

the lowest maize crop since 2007, which will negatively impact livestock

production costs due to higher feed prices in the second half of the current

reporting period and to the onset of the new maize crop in 2016.

The higher maize prices will be partly offset by more favourable soya prices

as global stock levels remain healthy.

Astral’s best cost integrated strategy has further strengthened on the back

of selective investments contributing to higher poultry volumes, improved

efficiencies and feeding costs into the future.

44

45 10 April 2015

46

ADDITIONAL INFORMATION

46

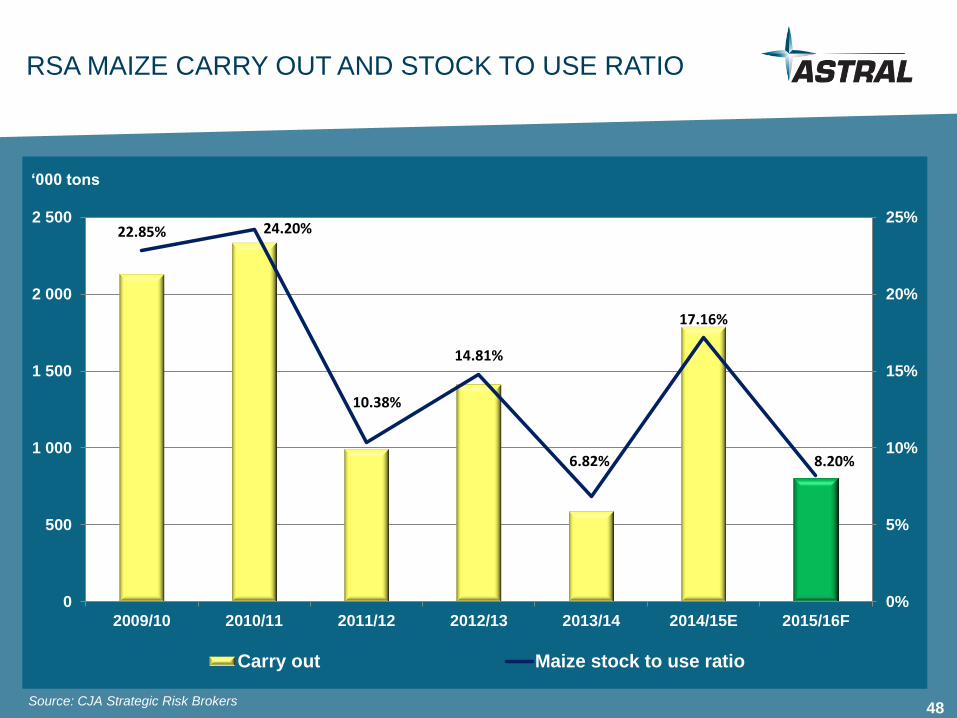

47 Source: CJA Strategic Risk Brokers

2009/10 2010/11 2011/12 2012/13 2013/14 2014/15E 2015/16F

Actual Actual Actual Actual Actual Estimate Forecast

Carry In (1 May) 1,581 2,131 2,336 991 1,414 590 1,790

Crop Estimate 12,050 12,815 10,360 12,121 11,811 14,250 9,763

Sagis Delivery 11,697 12,092 10,394 11,972 11,072 13,730 9,193

Minus early deliveries 0 0 0 0 0 0 0

Imports 27 0 421 11 80 50 450

Total Supply 13,305 14,224 13,151 12,973 12,566 14,371 11,434

Domestic Usage Food 4,471 4,513 4,512 4,499 4,583 5,087 4,663

Domestic Usage Feed 4,101 4,271 4,362 4,378 4,715 4,904 4,527

Gristing, withdrawn & released 755 866 693 674 480 441 612

Total Domestic Usage 9,327 9,650 9,567 9,551 9,777 10,431 9,802

Exports & Sundries 1,847 2,238 2,590 2,008 2,122 2,149 828

Plus early deliveries 0 0 0 0 0 0 0

Carry Out (30 Apr) 2,131 2,336 994 1,414 590 1,790 804

No of days usage 83 88 38 54 25 63 30

STU 22.85% 24.20% 10.38% 14.81% 6.82% 17.16% 8.20%

Marketing year (May to April)

'000 tons

SOUTH AFRICA - TOTAL MAIZE SUPPLY & DEMAND

47

48

22.85% 24.20%

10.38%

14.81%

6.82%

17.16%

8.20%

0%

5%

10%

15%

20%

25%

0

500

1 000

1 500

2 000

2 500

2009/10 2010/11 2011/12 2012/13 2013/14 2014/15E 2015/16F

Carry out Maize stock to use ratio

Source: CJA Strategic Risk Brokers

RSA MAIZE CARRY OUT AND STOCK TO USE RATIO

‘000 tons

48

49

F2010 F2011 F2014 F2012 F2013

Source: CJA Strategic Risk Brokers

SAFEX YELLOW MAIZE VS CBOT CORN IN RAND TERMS

49

F2015

50

BROILER FEED

INGREDIENT INCLUSION AND COST CONTRIBUTION

50

69.1 43.5 65.1 48.7 68.8 49.2 67.0 39.0 66.9 47.5 67.0 44.6 65.9 42.5 65.5 40.8

16.3

19.7

16.6

18.6

16.6

22.6

16.6

24.7

14.0

20.9

17.0

26.8

18.9

29.2

16.5

25.3

4.2

3.4

5.7

3.5

4.5

3.3

6.1

5.4

8.5

8.0

7.0

6.8

6.0

5.7

7.5

7.5

8.5

14.9

10.4

19.8

6.1

11.9

7.1

13.2

9.9

18.5

8.4

16.6

7.9

14.7

9.9

21.3

1.6

4.8

1.9

5.1

3.8

8.3

1.4 3.6

0.5 1.2

0.4

1.1 0.9

2.4 0.3

0.9

0.3

13.7

0.3 4.3

0.3 4.8

0.3 3.5

0.3 3.8

0.3

4.1

0.4 5.5

0.3

4.2

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2H11Incl.

2H11Contr.

1H12Incl.

1H12Contr.

2H12Incl.

2H12Contr.

1H13Incl.

1H13Contr.

2H13Incl.

2H13Contr.

1H14Incl.

1H14Contr.

2H14Incl.

2H14Contr.

1H15Incl.

1H15Contr.

Maize Soya o/c Sunfl. o/c Other Fish Vit and Med

51

F2014 28,250 38,397 32,403 25,144 23,898 31,719 37,136 36,543 40,612 26,501 25,979 37,128

F2015 42,363 38,807 27,504 28,896 31,305 40,372

% Var 49.9 1.1 -15.1 14.9 31.0 27,3

bpw* 7,5 6,9 4,9 5,1 5,6 7,2

Source: SAPA

TOTAL POULTRY IMPORTS (CHICKEN, TURKEY, MDM)

*bpw ≈ million birds per week

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

F2012 33 348 67 819 100 540 135 614 170 194 204 560 244 296 278 914 305 472 326 520 353 296 387 173

F2013 47 942 89 095 117 712 145 426 172 727 207 148 243 623 282 790 316 047 343 913 371 741 409 158

F2014 28 250 66 647 99 050 124 194 148 092 179 811 216 947 253 490 294 102 320 603 346 582 383 710

F2015 42 363 81 170 108 674 137 660 168 965 209 337

0

50 000

100 000

150 000

200 000

250 000

300 000

350 000

400 000

450 000

F2012 F2013 F2014 F2015

Tons

52 52

Ex BRAZIL – May 2015

FROZEN LEG QUARTERS BULK PACKED

CIF DBN US$ per ton TON 1 100.00 1 100.00 1 100.00 SA COST

R/$ exchange rate R$ 11.50 12.00 12.50

Rand per ton TON 12 650.00 13 200.00 13 750.00 20 800.00

Rand per kg KG 12.65 13.20 13.75 20.80

Duty per kg KG 37% 37% 37% -

Clearance costs KG 0.50 0.50 0.50 -

COST INTO STORAGE KG 17.83 18.58 19.34 20.80

Storage KG 0.50 0.50 0.50 -

Distribution KG 0.64 0.64 0.64 0.74

Marketing, Administration, Finance KG 0.78 0.78 0.78 0.85

TOTAL COST KG 19.75 20.50 21.26 22.39

Ex UNITED KINGDOM – May 2015

FROZEN LEG QUARTERS BULK PACKED

CIF DBN US$ per ton TON 1 400.00 1 400.00 1 400.00 SA COST

R/$ exchange rate R$ 11.50 12.00 12.50

Rand per ton TON 16 100.00 16 800.00 17 500.00 20 800.00

Rand per kg KG 16.10 16.80 17.50 20.80

Duty per kg KG 30.99% 30.99% 30.99% -

Clearance costs KG 0.50 0.50 0.50 -

COST INTO STORAGE KG 21.59 22.51 23.42 20.80

Storage KG 0.50 0.50 0.50 -

Distribution KG 0.64 0.64 0.64 0.74

Marketing, Administration, Finance KG 0.78 0.78 0.78 0.85

TOTAL COST KG 23.51 24.43 25.34 22.39

BRAZIL & EUROPE PRODUCT COST BENCHMARK

53

02468101214161820222426283032343638404244

5.0

10.0

15.0

20.0

25.0

30.0

Oc

t-0

9

De

c-0

9

Feb

-10

Ap

r-1

0

Ju

n-1

0

Au

g-1

0

Oct-

10

De

c-1

0

Feb

-11

Ap

r-1

1

Ju

n-1

1

Au

g-1

1

Oc

t-1

1

De

c-1

1

Feb

-12

Ap

r-1

2

Ju

n-1

2

Au

g-1

2

Oc

t-1

2

De

c-1

2

Feb

-13

Ap

r-1

3

Ju

n-1

3

Au

g-1

3

Oc

t-1

3

De

c-1

3

Feb

-14

Ap

r-1

4

Ju

n-1

4

Au

g-1

4

Oc

t-1

4

Dec-1

4

Feb

-15

RSA broilers (slaughtered / week) Poultry imports (birds / week)

Broiler selling price (Rand / kg) Per capita consumption (kg)

Million birds per week / Rand per kg kg

Source: SAPA

LOCAL BROILER PRODUCTION, IMPORTS & PER CAPITA CONSUMPTION

53

54

1000

1500

2000

2500

3000

3500

Beef

Pork

Chicken

Chicken Pork Beef Sheep

Feed Conversion Rate 1.7 2.2 5.5 5.0

Per Capita Consumption 37.9 kg 4.6kg 17.2kg 3.2kg

Source: SAPA & FNB

PRODUCER PRICE COMPARISON – RSA PROTEIN

Cents per kg

54

55

Tel: +27 (0) 12 667 5468

Fax: +27 (0) 86 504 2002

Astral Foods Corporate

Office

92 Koranna Avenue,

Doringkloof, Centurion,

0157, Gauteng, South Africa

Chris Schutte

Chief Executive Officer

Tel : +27 (0) 12 667 5468

Fax : +27 (0) 86 504 2002

Email: [email protected]

Website: www.astralfoods.com

Daan Ferreira

Group Financial Director

Tel : +27 (0) 12 667 5468

Fax : +27 (0) 86 504 1602

Email: [email protected]

CONTACTS

55