potashcorp.com yao manager, market research january 2015 fertilizer market update

TRANSCRIPT

PotashCorp.com

Click icon to add picture

Yao Yao

Manager, Market Research

January 2015

FertilizerMarket Update

This presentation contains forward-looking statements or forward-looking information (forward-looking statements). These statements can be identified by expressions of belief, expectation or intention, as well as those statements that are not historical fact. These statements often contain words such as “should,” “could,” “expect,” “may,” “anticipate,” “believe,” “intend,” “estimates,” “plans” and similar expressions. These statements are based on certain factors and assumptions including with respect to: foreign exchange rates, expected growth, results of operations, performance, business prospects and opportunities and effective tax rates. While the company considers these factors and assumptions to be reasonable based on information currently available, they may prove to be incorrect. Forward-looking statements are subject to risks and uncertainties that are difficult to predict. The results or events set forth in forward-looking statements may differ materially from actual results or events. Several factors could cause actual results or events to differ materially from those expressed in the forward-looking statements, including, but not limited to the following: variations from our assumptions with respect to foreign exchange rates, expected growth, results of operations, performance, business prospects and opportunities, and effective tax rates; risks and uncertainties related to operating and workforce changes made in response to our industry and the markets we serve; changes in competitive pressures, including pricing pressures; risks and uncertainties related to our international operations and assets; fluctuations in supply and demand in the fertilizer, sulfur, transportation and petrochemical markets; costs and availability of transportation and distribution for our raw materials and products, including railcars and ocean freight; adverse or uncertain economic conditions and changes in credit and financial markets; the results of sales contract negotiations within major markets; unexpected geological or environmental conditions, including water inflows; economic and political uncertainty around the world; risks associated with natural gas and other hedging activities; changes in capital markets; unexpected or adverse weather conditions; changes in currency and exchange rates; imprecision in reserve estimates; adverse developments in new and pending legal proceedings or government investigations; acquisitions we may undertake; increases in the price or reduced availability of the raw materials that we use; strikes or other forms of work stoppage or slowdowns; timing and impact of capital expenditures; rates of return on, and the risks associated with, our investments and capital expenditures; changes in, and the effects of, government policies and regulations; security risks related to our information technology systems; risks related to reputational loss; and earnings, and the decisions of taxing authorities, which could affect our effective tax rates. Additional risks and uncertainties can be found in our Form 10-K for the fiscal year ended December 31, 2013 under the captions “Forward-Looking Statements” and “Item 1A – Risk Factors” and in our other filings with the US Securities and Exchange Commission and the Canadian provincial securities commissions. Forward-looking statements are given only as at the date of this release and the company disclaims any obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Forward-looking Statements

PotashCorp Overview

Agriculture Market Overview

1. Crop prices supported in the first half by strong demand, unrest in Ukraine/Russia and delayed US planting.

2. Robust planting and yields in the US led to record corn and soybean production.

3. Global crop stocks increased following two years of above-trend yields, weighing on prices.

4. Significant improvement in livestock economics and healthy ethanol sector margins.

5. Delayed planting in Brazil created some yield risk and could impact Safrinha planting prospects.

Strong Global Production Softens Crop Prices

World Crop Market Update

Source: Bloomberg

Jan-

06

Sep-0

6

Jun-

07

Mar

-08

Dec-0

8

Aug-0

9

May

-10

Feb-1

1

Nov-1

1

Jul-1

2

Apr-1

3

Jan-

14

Oct-1

40

50

100

150

200

250

300

350

400

* Based on corn, soybean and wheat prices (weighted by global consumption).

World Crop Price Index* 2014 Highlights

Price Index (2005 Average = 100)

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014F1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

0%

5%

10%

15%

20%

25%

30%Consumption Production Stocks-to-Use Ratio

2014F refers to the 2014/15 crop year.

Stocks-to-Use RatioMillion Tonnes

Stocks Rise but Remain Well Below Historical Highs

World Grain and Oilseed Supply/Demand

Source: USDA

Soybean Corn Rice Wheat-4000

-2000

0

2000

4000

6000

8000

10000

12000

14000

Asia FSU EU

Latin America North America Others

Source: USDA

MT/HectareMillion Hectares

Record Production Driven by Acreage Expansion and Strong Yields

World Grain and Oilseed Acreage and Yield

Harvested Area Change: 2014 vs 5-Year Average Yield

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

F

2.00

2.25

2.50

2.75

3.00

3.25

3.50

Yield Linear (Yield)

Jan-0

6

Jul-0

6

Feb-07

Sep-07

Mar-0

8

Oct

-08

May-

09

Nov-09

Jun-1

0

Jan-1

1

Jul-1

1

Feb-12

Sep-12

Mar-1

3

Oct

-13

May-

14

Nov-14

0

50

100

150

200

250

300

350

400

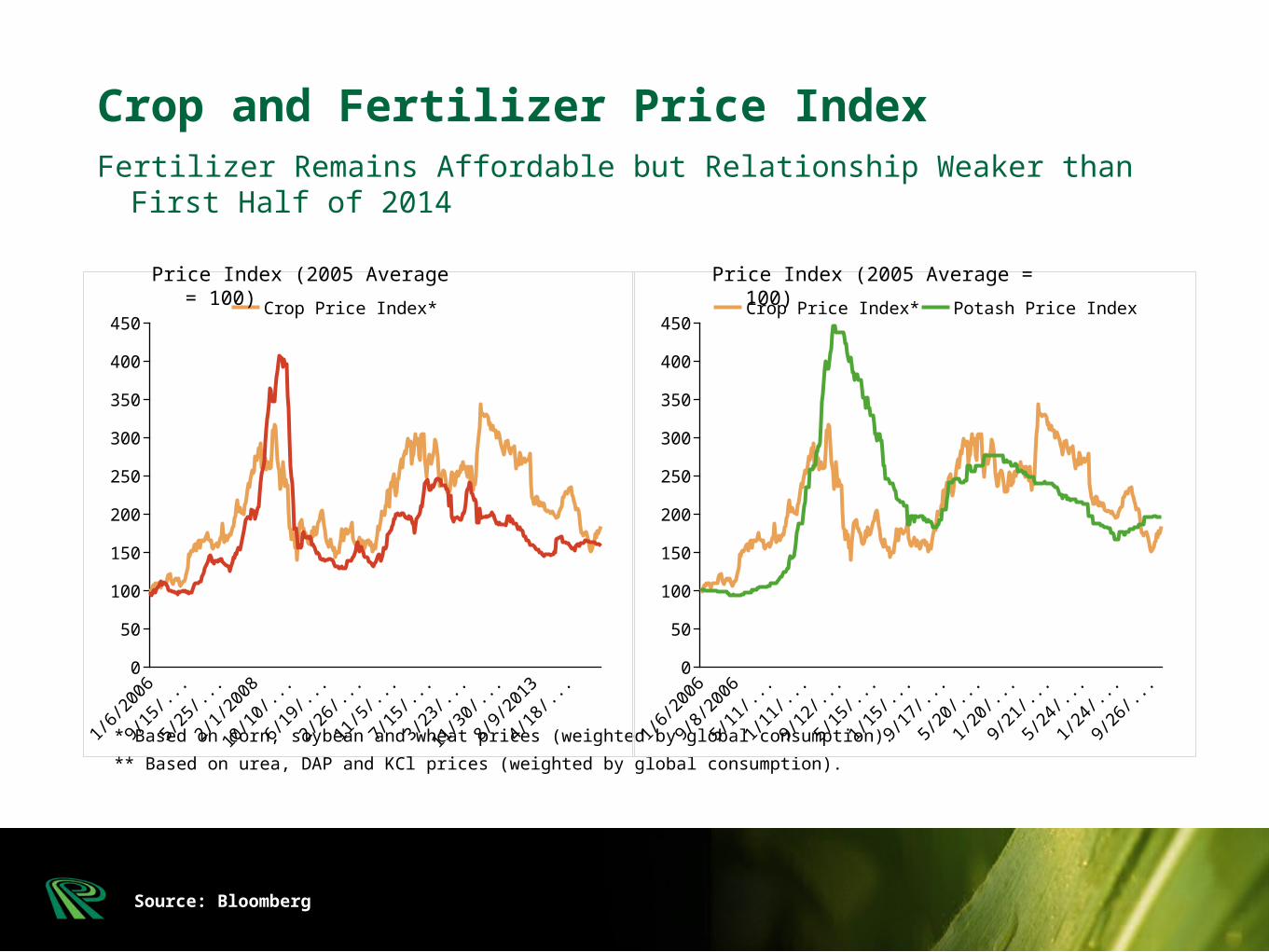

450Crop Price Index* Fertilizer Price Index**

* Based on corn, soybean and wheat prices (weighted by global consumption).

** Based on urea, DAP and KCl prices (weighted by global consumption).

Price Index (2005 Average = 100)

Crop and Fertilizer Price Index

Source: Bloomberg

Jan-0

6

Jul-0

6

Feb-07

Aug-07

Feb-08

Sep-08

Mar-0

9

Oct

-09

Apr-10

Nov-10

May-

11

Dec-11

Jun-1

2

Dec-12

Jul-1

3

Jan-1

4

Aug-14

0

50

100

150

200

250

300

350

400

450Crop Price Index* Potash Price Index

Price Index (2005 Average = 100)

Fertilizer Remains Affordable but Relationship Weaker than First Half of 2014

Source: USDA, PotashCorp

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

F0

1

2

3

4

5

6

7Seed Fertilizer Chemical Other VCLand Rent Other FC Corn Price

US$/Bushel

Margins Reset in 2014 After Multiple Years of Robust Returns

US Corn Economics

• Brazilian crop progress and safrinha planted area

• US crop acreage changes

• Expect less corn and cotton acreage

• Potential for more soybean based on current economics

• Chinese import demand and policy changes

• Macro factors (FX, oil prices, geopolitical events)

2015 Factors to Watch

Fertilizer Market Overview

KCl Ammonia Phosphoric Acid0

10

20

30

40

50

60

70

80

90

100

North America FSU Europe China India

Other Asia Africa/Middle East Latin AmericaPercent*

Capacity Typically Located Near Low-Cost/High-Quality Raw Material Source

World Fertilizer Capacity Percentage by Region

* Based on 2013 year-end nameplate capacity.

Source: CRU, Fertecon

Source: Fertilizer Week, PotashCorp

Potash Prices Strengthened in 2014

World Potash Market Update

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4200

300

400

500

600

700

Brazil CFR NOLA FOB

US$/tonne1. Potash prices increased in 2014,

particularly in major markets for granular product.

2. Record potash shipments expected,

3. Estimated global operating rates above 90 percent.

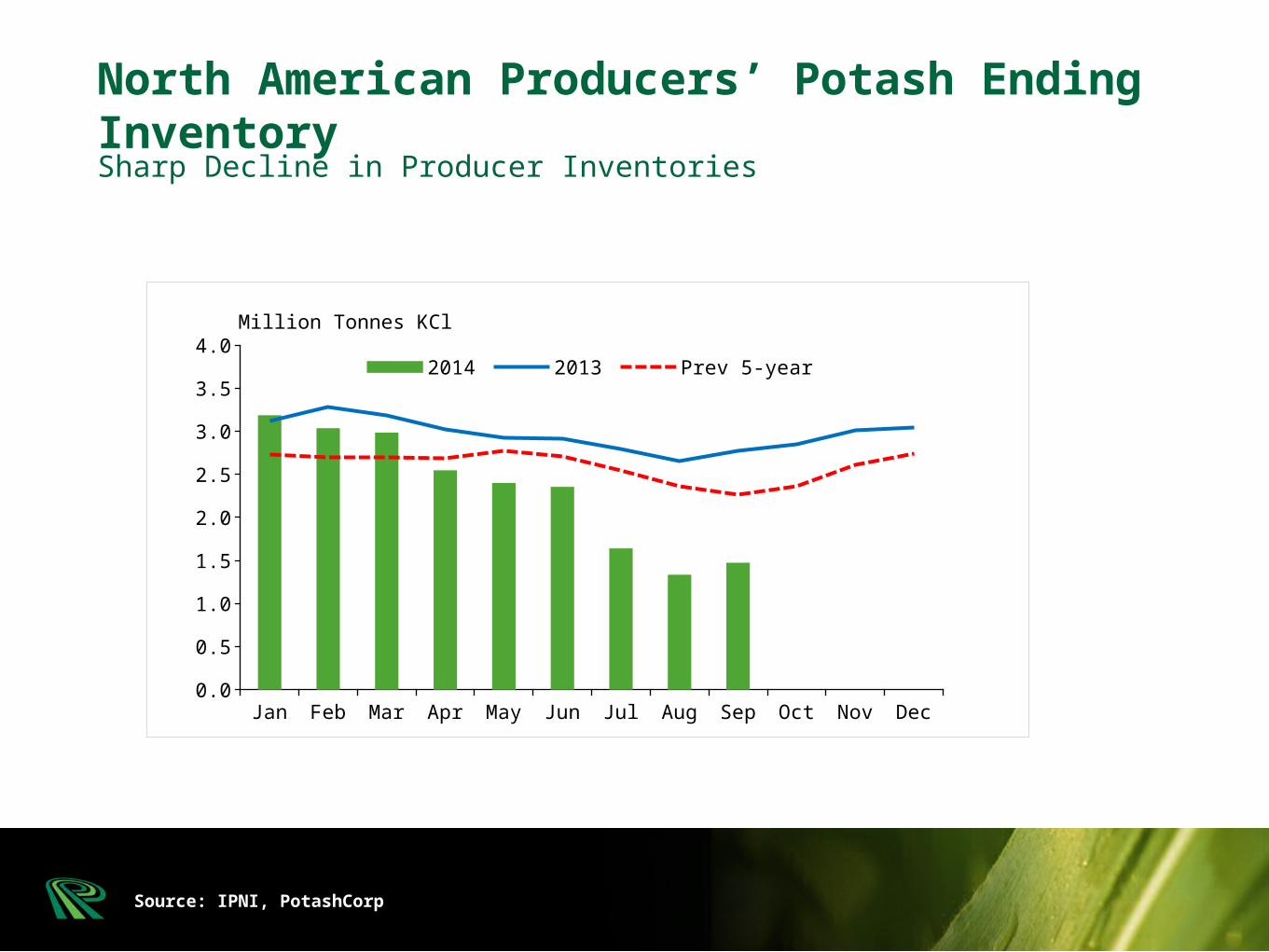

4. Producer inventory levels down significantly compared to the beginning of the year.

World Potash Prices 2014 Highlights

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

E0

10

20

30

40

50

60 Shipments Consumption Production

Million Tonnes KCl

World Potash S&D

Source: Fertecon, CRU, IFA, Industry Publications, PotashCorp

Record Potash Shipments in 2014

Source: IPNI, PotashCorp

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.02014 2013 Prev 5-year

Million Tonnes KCl

North American Producers’ Potash Ending InventorySharp Decline in Producer Inventories

12 13 14E

12 13 14E

12 13 14E

12 13 14E

12 13 14E

0

2

4

6

8

10

12

14

16Million Tonnes KCl

World Potash Shipments by Markets

Source: Fertecon, CRU, Industry Publications, PotashCorp

ChinaIndia L. AmericaOther Asia N. America

Strong Growth in Demand in All Major Potash Markets

Source: USDOC, Fertecon, IPNI, PotashCorp

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014E0.0

2.0

4.0

6.0

8.0

10.0

12.0 Domestic Producer Shipments Offshore Imports

Million tonnes KCl

North America’s Potash Shipment ProfileSignificantly Improved Demand in 2014

Source: USDA, AAPFCO, PotashCorp

Calculation based on commercial fertilizer application data, estimated nutrients available from manure and crop removal rates for all major crops grown in the US.

Central P

lains

Mountain

Lake States

MidwestOther

WestDelta

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

3.7

1.4

0.7 0.7 0.6 0.60.4

Million Short Tons KCl Equivalent

1975 1980 1985 1990 1995 2000 2005 20100

2

4

6

8

10

12

14

16Crop removal Fertilizer applied

Million Short Tons KCl Equivalent

Application Rates Have Not Kept Pace With Higher Crop Removal

US Potassium Application and Crop Removal

US Total Regional Application Deficit – 2010

~ 8.0 million

st

Source: Fertecon, CRU, Industry Publications

Potash Mines Could be Closed Due to Water Inflows or Ore Depletion

Historical Potash Mine Closures

1986

Berezniki - 3 mine in Russia (1.8 MMT)

was abandoned due to flooding

1988

Patience Lake SK mine (1.0 MMT) was converted to a

solution mine after flooding

1998

Cassidy Lake NB mine (1.3 MMT) was lost due to

flooding

1990-2003

Potash mines in US, Germany and France

closed due to depleting ore and high cost position

2006

Berezniki -1 mine in Russia (1.4 MMT) was closed due to

flooding

2014

Solikamsk - 2 mine in Russia (2.4 MMT) shut down due to elevated

brine inflow.

2018-2020

Mines to be closed due to reserve depletion:

Sigmundshall (Germany) and Taquari (Brazil)

2015

Mosaic to discontinue MOP production at

Carlsbad, NM mine (0.5 MMT)

Jan-

10

May

-10

Sep-1

0

Jan-

11

May

-11

Sep-1

1

Jan-

12

Jun-

12

Oct-1

2

Feb-1

3

Jun-

13

Oct-1

3

Feb-1

4

Jun-

14

Oct-1

40

100

200

300

400

500

600

700

800Tampa cfr Black Sea fob

Source: Fertilizer Week, PotashCorp

1. Weak fundamentals in the second half of 2013 impacted first-quarter 2014 ammonia prices.

2. Healthy demand and global plant outages supported ammonia prices following the first quarter.

3. Natural gas curtailments and plant reliability issues limited production in Egypt, Algeria, Libya, Trinidad and Pakistan.

4. Political tension in Ukraine/Russia constrained production and exports from this region.

US$/Tonne

Prices Were Firm Through Most of 2014

World Ammonia Market Update

World Ammonia Prices 2014 Highlights

Ukraine Trinidad Pakistan Egypt Algeria Libya0

1,000

2,000

3,000

4,000

5,000

6,000

7,000Production Curtailed Capacity

Million Tonnes - NH3

Significant Production Outages in Key Regions

Regional Ammonia Production Profile

Source: Fertecon, PotashCorp

Jan-

10

May

-10

Sep-1

0

Jan-

11

May

-11

Sep-1

1

Jan-

12

Jun-

12

Oct-1

2

Feb-1

3

Jun-

13

Oct-1

3

Feb-1

4

Jun-

14

Oct-1

40

100

200

300

400

500

600

700

800NOLA Middle East

Source: Fertilizer Week, PotashCorp

1. Strong demand in key import markets.

2. Tight supply contributed to a price premium in the US compared to global markets in the first half of 2014.

3. Record Chinese exports pressured global urea prices.

4. Middle East export volumes remained at elevated levels.

US$/MT

Prices Soften Due to Record Chinese Exports

World Urea Market Update

World Urea Prices 2014 Highlights

30,000

35,000

40,000

45,000

50,000

Source: Fertecon, CRU, PotashCorp

30,000

35,000

40,000

45,000

50,000Million Tonnes

Increased Demand Met by a Few Key Exporting Regions

Global Urea Trade Changes

World Urea Imports World Urea Exports

Million Tonnes

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,0002014

2013

Prev. 5-Year Avg.

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,00020142013Prev. 5-Year Avg.

Source: USDOC, Potafertz, FAI, Fertecon, PotashCorp

Million Tonnes

India Imports

Million Tonnes

Brazil ImportsUS Imports

Strong Imports in the Western Hemisphere; India to Catch Up

Cumulative Urea Imports for Key Regions

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

20142013Prev. 5-Year Avg.

Million Tonnes

Many Proposed Projects; Some Under Construction and Several Deferred

Potential North American Nitrogen Project Locations

High Probability Projects

Medium Probability Projects

More Speculative Projects

Projects under Construction

Expected Product Mix (million tons)

Ammonia Urea UAN

UC/High 1.3 5.0 3.8

Medium 0.9 0.7 0

Low 1.1 5.7 3.6

Source: Company Reports, Fertecon, CRU, PotashCorp

Announced Project Cancelations/Deferrals

1. Northern Hemisphere logistics and production issues tighten availability in first quarter.

2. India monsoon uncertainty and low importer margins limited import volumes.

3. Record demand from Latin America.

4. China exported record volumes with greater geographic diversity. Morocco and Saudi Arabia provided incremental supply.

5. Rising non-rock input costs.

Demand Strength and Supply Challenges Support Phosphate Market

World Phosphate Market Update

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

40

100

200

300

400

500

600

700

0

200

400

600

800

1,000

1,200 Tampa DAP CFR India Phosphoric Acid

US$/tonne - Phosphoric AcidUS$/tonne - DAP

Source: Fertilizer Week

World Phosphate Prices 2014 Highlights

Mar

-13

May

-13

Jul-1

3

Sep-1

3

Nov-1

3

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep-1

4

Nov-1

4

Jan-

15

Mar

-15

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Million Tonnes

Significant Shifts in the Supply/Demand Balance

Global DAP/MAP Trade Balance

Source: Profercy

Trade Surplus

Trade Deficit

Source: FAI, Potafertz, CRU, PotashCorp

14E

12

14E

12

14E

12

14E

12

14E

12

0 1 2 3 4 5 6

USA

Morocco

China

Saudi Arabia

Russia

Million Tonnes

Higher Exports From Morocco, Saudi Arabia and China

DAP/MAP Exports By Major Region

Global DAP/MAP trade: 2012 – 20.5 MMT, 2013 – 20.6 MMT, 2014E– 22.0 MMT

Source: FAI, Potafertz, CRU, PotashCorp

14E

12

14E

12

14E

12

14E

12

14E

12

0 1 2 3 4 5 6 7

Other Asia

Brazil

India

Other Latin America

US

Million Tonnes

Record Latin America and US Imports in 2014

DAP/MAP Imports by Major Region

Global DAP/MAP trade: ~21.0 MMT

• Impact of lower crop prices on global fertilizer consumption?

• US fertilizer demand in spring and logistics capability

• Impact of shortened fall application season?

• Potential nitrogen product mix changes?

• Macro factors and Geopolitical events

• Impact of changing FX, oil prices?

• Potential for new global fertilizer capacity?

2015 Factors to Watch

There’s more online:

PotashCorp.comVisit us online

Facebook.com/PotashCorpFind us on Facebook

Twitter.com/PotashCorpFollow us on Twitter

Thank you

Click icon to add picture