peran bank syariah bagi sektor riil dan pengembangan ekonomi rifki ismal asisten direktur, departmen...

TRANSCRIPT

PERAN BANK SYARIAH BAGI SEKTOR RIIL DAN PERAN BANK SYARIAH BAGI SEKTOR RIIL DAN PENGEMBANGAN EKONOMIPENGEMBANGAN EKONOMI

Rifki IsmalAsisten Direktur, Departmen Perbankan Syariah

Bank Indonesia

Kuliah Tamu di Universitas Islam Negeri Malang14 Maret 2013

UIN Malang

Indonesian Indonesian Economy : Monetary Policy Economy : Monetary Policy and Financial Stabilityand Financial Stability – Recent – Recent

DevelopmentDevelopment

Indonesian Indonesian Economy : Monetary Policy Economy : Monetary Policy and Financial Stabilityand Financial Stability – Recent – Recent

DevelopmentDevelopment

3Executive SummaryExecutive Summary Indonesia’s economic growth remains robust in 2012 amidst the

continuation of global economic slowdown. Contributed by buoyant consumption and investment, economic growth in the Q4-2012 reached 6.11%, and charted 6.23% for the whole year of 2012.

Inflation in January 2013 remained subdued and arrive at 4.57%(yoy) which is within target range of 4.5%±1%. This inflation supported by the implementation of monetary and macroprudential policy mix, as well as policy coordination with the Government through national inflation control team (TPI) and regional inflation control team (TPID).

Financial system stability remained solid with intermediation function is improving within prudential manner as indicated by secure level of capital adequacy ratio (CAR) is well above minimum level of 8% and gross non-performing loan (NPL) below 5%. In December 2012, credit growth charted 23.1% (yoy). Considering the type of loan, investment loan recorded the highest growth of 27.4% (yoy), in line with the increased in investment.

In the Board of Governors' Meeting convened on 12 February 2013, Bank Indonesia decided to hold the BI rate steady at 5.75% in which considered consistent with low inflation forecast and contained within its target range of 4.5%±1% in 2013 and 2014. Bank Indonesia believes that the implementation of policy mix together with strengthen coordination with the Government will be able to maintain macroeconomic stability and sustainable economic growth.

4Executive SummaryExecutive SummaryMonetary policy Keep policy rate unchanged at 5.75% since March 2012, this level

considered to be consistent with inflation target Maintain IDR exchange rate stability Strengthen monetary policy by implementing monetary and

macroprudential policy mix Deepening of the foreign exchange market

Exchange RateOn January 2013, Rupiah depreciated by 0.22% (mtm) to Rp9.654 per USD, with a contained volatility. In the future, BI will continue to maintain the stability of Rupiah exchange rate consistent with its economic fundamentals. Furthermore, BI will support the formation of a reference to Rupiah exchange rate in the domestic spot market. This reference is expected to promote foreign exchange market efficiency, deepening the domestic financial market

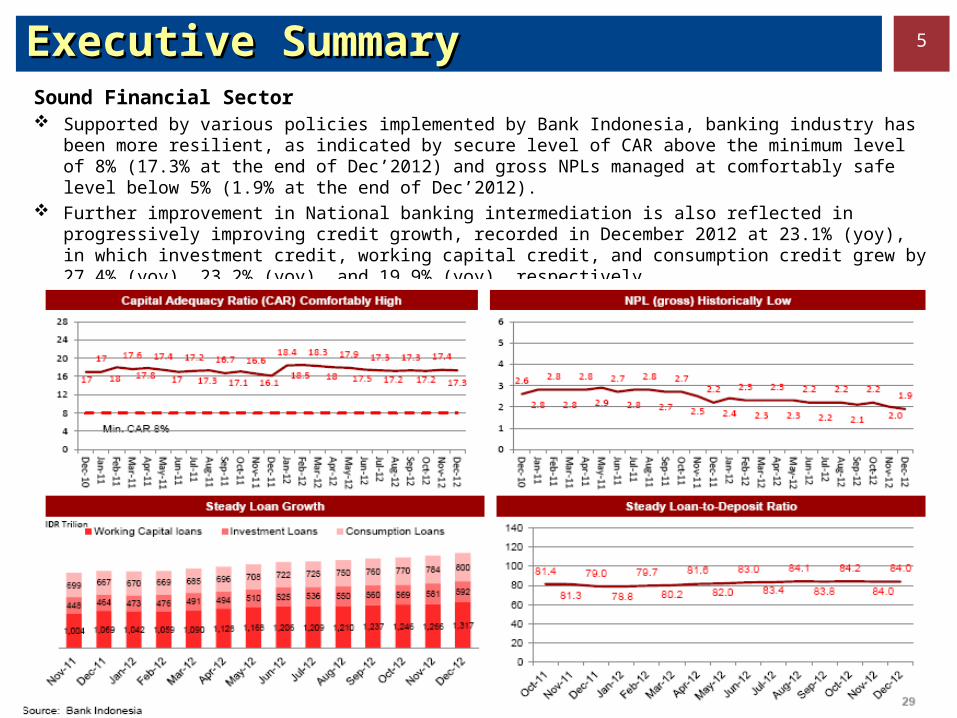

5Executive SummaryExecutive SummarySound Financial Sector Supported by various policies implemented by Bank Indonesia, banking industry has been

more resilient, as indicated by secure level of CAR above the minimum level of 8% (17.3% at the end of Dec’2012) and gross NPLs managed at comfortably safe level below 5% (1.9% at the end of Dec’2012).

Further improvement in National banking intermediation is also reflected in progressively improving credit growth, recorded in December 2012 at 23.1% (yoy), in which investment credit, working capital credit, and consumption credit grew by 27.4% (yoy), 23.2% (yoy), and 19.9% (yoy), respectively.

6Executive SummaryExecutive SummaryRoles of Banking in the Domestic Economy The role of the Indonesian banking is not yet optimal to support the real

sector. Credit to GDP ratio is relatively low compared to the ASEAN countries.

The Indonesian Credit to GDP ratio stands between 26%-32%, almost the same as Philippines and Brunei. While others, especially Thailand and Singapore has more than 100% credit to GDP ratio. Malaysia is following them with a growing ratio from 96% to 112%.

As such, the are more rooms to utilize the banking sector to boost the domestic economy.

0

20

40

60

80

100

120

140

160

Indonesia Singapore Malaysia Phillipines Brunei Thailand

2008

2009

2010

2011

%

2008 2009 2010 2011Indonesia 26.60 27.70 29.10 31.70Singapore 106.70 109.90 100.00 112.60Malaysia 96.70 111.60 110.70 112.20Phillipines 29.10 29.20 29.60 31.80Brunei 35.20 44.50 40.90 31.80Thailand 113.00 116.40 123.90 140.10

Indonesian Islamic Banks – Indonesian Islamic Banks – Sustainable Sustainable Growth and Role in Economic Growth and Role in Economic

Development & Financial Stability Development & Financial Stability

Indonesian Islamic Banks – Indonesian Islamic Banks – Sustainable Sustainable Growth and Role in Economic Growth and Role in Economic

Development & Financial Stability Development & Financial Stability

8Indonesia’s Islamic Bank (iB) DevelopmentIndonesia’s Islamic Bank (iB) Development

Indonesia’s IB (BUS+UUS) average growth in last 5 years reach 37% for asset then 36% for financing and 38% for deposits. Whereas in 2012, the growth for asset (±34%) value Rp. 195 T, financing (±44%) value Rp.147,5 T and deposit (±28%) value Rp.147,5 T. Indonesia’s iB aset ±98% dominated by Islamic Commercial Bank

(BUS) and Islamic Busines Unit (UUS). In year 2012, the IB’s (BUS+UUS) performance relatively good, reflected by : (i) optimum intermediation function with average FDR reach 97,16%; (ii) CAR beyond minimum regulation 8% with average CAR reach ±17%; and (iii) Non Performing Financing (NPF) under 5% with average 2.72% and even in December 2012 reach 2.22%.

Rp. Triliun

9Current Growth is in line with projectionsCurrent Growth is in line with projections

Islamic banks’ (BUS+UUS+BPRS) asset growing in 2012 reach Rp. 199,72 T and within BI’s previous projection scenarios between moderate scenario (Rp.187.2T) and optimistic scenario (Rp.206T).

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

Jan-

11

Mar

-11

May

-11

Jul-1

1

Sep-

11

Nov

-11

Jan-

12

Mar

-12

May

-12

Jul-1

2

Actual Projections

European CrisisEuropean Crisis

90,000,000

110,000,000

130,000,000

150,000,000

170,000,000

190,000,000

210,000,000

230,000,000

Jan-

11

Mar

-11

May

-11

Jul-1

1

Sep-

11

Nov

-11

Jan-

12

Mar

-12

May

-12

Jul-1

2

Sep-

12

Nov

-12

10Increasing number of Islamic Bank (iB) s Customer Increasing number of Islamic Bank (iB) s Customer

With 11 Islamic Commercial Bank (BUS), 24 Islamic Business Unit (UUS) and 156 Islamic Rural Bank (BPRS), the office network increased from 2.101 in year 2011 becoming into 2.663 (26,75%).

The increasing number of iB’s customer iB’s account number (financing + deposits) increases ± 4 million accounts from ± 10.4 mio year 2011 into ± 14.4 mio in Dec’12 (38%, yoy)

The significant increasing number of iB’s customer in last 4 years (average ± 31%), even growth in period 2011 – 2012 (± 38%) higher than previous period reflect the more trusted iB by Indonesia’s people for saving/invest fund

More broaden customer has been serviced by Islamic banks

11

The direction of more financing toward productive sector looks on the right track by the end of 2012

Decreasing growth of non productive financing share

Financing growth to Non productive sector (services and others) has decelerated from 8,4% (2010 - 2011) become 0,82% (2011 – 2012) or decreasing 7,59%.

The growth share of Non Productive financing type compare to productive (working capital + Investment) has decelerated from 30,09% (2010 - 2011) become 1,92% (2011 - 2012) or decreasing 28%.

The Decreasing Growth of Non Productive The Decreasing Growth of Non Productive Financing Share/SectorFinancing Share/Sector

Data :Sept’12

12Islamic BanksIslamic Banks (iB) (iB) : : Promote Financial StabilityPromote Financial Stability

Advantages as Islamic banks during current global uncertain periods:1. Profit and loss sharing system will be beneficial and provide fair return to all parties. With this system,

islamic banks will promote social welfare as the benefit receivers need to pay zakah as part of social contribution while complying to the shariah principle.

2. The products offered by islamic banks always use real sector transaction as its underlying; therefore, the impact of islamic financial transaction can be significant to promote economic growth

3. Reduce potential excessive speculation since islamic finance prohibits the speculative motive. Derivatives products are prohibited by islamic principles because of the existance of gharar

4. In the case of Indonesia: a. islamic banks nature is to focus on developing small and medium enterprises as the underlying, and there are

relatively small risks involvedb. Exposure to currency risk, financial sector is relatively small

Indonesian Islamic Banks – Indonesian Islamic Banks – Policy Policy Direction and ProspectDirection and Prospect

Indonesian Islamic Banks – Indonesian Islamic Banks – Policy Policy Direction and ProspectDirection and Prospect

14Maintaining Strong GrowthMaintaining Strong Growth

• Innovation of genuine sharia Products and services : support the people need ,more broaden customer base and more productive activities

• Strategic alliance and strong infrastructure support : i.e. Government support, Optimization synergy with iB’s holding/Grup companies.

• More professionals & qualified HRD• Intensified Education and socialization

This strategy will attract more broaden customers to use services from islamic banks, and in the end this will have an impact to strong growth

With Rp.199,72 trilion of iB (BUS+UUS+BPRS) asset in Dec’12 (eq $ 22 billion) we only account for 4.6% of Indonesian banking industry, or less than 2% of global islamic assets.

15BI Policy: Product InnovationBI Policy: Product Innovation

1. In the current highly competitive environment, islamic banks cannot rely on standard product to attract customers. Islamic financial institutions must act and able to offer pure and genuine Islamic products that bring up the uniqueness of sharia principles that can meet customers' and investors needs

2. BI will facilitate Working Group Discussions (with National Sharia Board and indonesia Accountant Association) to activate innovation and creativity regarding product development to attract more customers.

3. BI will consider to improve related regulations on Islamic banking products in order to increase the efficiency of the product licensing process.

4. In order to increase public awareness to Islamic banking products (iB financial literacy), socialization programs / public education and communication will be more focused on equality "parity" and the uniqueness of "distinctiveness" of the productIslamic banking.

Islamic banks are expected to strengthen the product development unit in order to accelerate the equalization of products and service levels with conventional banks, to increase service to meet customers needs

Islamic banks are expected to strengthen the product development unit in order to accelerate the equalization of products and service levels with conventional banks, to increase service to meet customers needs

16BI Policy: Emphasis Financing in Productive SectorBI Policy: Emphasis Financing in Productive Sector

1. Bank Indonesia in its capacity will facilitate link and match program between islamic banks and industry which is prioritized by the government, such as infrastructure, agriculture, as well as others.

2. Focus Group Discussions and business match will be the main forum to match supply and demand between banks and productive sectors.

BI have facilitated several FGDs and have received positive feedbacks.

In return, this will help promoting resilience of islamic banks, as well as generate higher asset growth, so that asset share of islamic banks compared to that of in conventional will gradually increase projection of 15-20% in the next decade

In return, this will help promoting resilience of islamic banks, as well as generate higher asset growth, so that asset share of islamic banks compared to that of in conventional will gradually increase projection of 15-20% in the next decade

17BI Policy: BI Policy: Support Adequate iBs Liquidity Framework Support Adequate iBs Liquidity Framework

• BI will support efforts to increase islamic money market transaction through enhancement the features of Interbank Mudharabah Certificate (SIMA) as underlying transactions,

• We are introducing sharia commodity trading scheme to add islamic money market instruments, and to increase the role of money broker in islamic money market transaction.

• Providing complete financial services to client, islamic banks can also provide financial services in the form of foreign currency , such as import payments or other foreign currency liabilities mitigate currency risks review the mechanisms and hedging instruments which comply with sharia principles.

• BI also support cross border liquidity instrument in foreign currency IILM initiatives issuing short term global sukuk in USD

Development in islamic financial market, especially money market instruments, will help banks to manage liquidity lower liquidity risk

Help Promoting Help Promoting Asset GrowthAsset Growth

18Projection of Indonesia’s iB (BUS+UUS+BPRS): 2013Projection of Indonesia’s iB (BUS+UUS+BPRS): 2013

Baseline Moderate Optimistic

(Rp.

Triliun)

(%) (Rp.

Triliun)

(%) (Rp.

Triliun)

(%)

Asset 255 36 % 269 44% 296 58%Deposit (DPK)

168 17% 177 23% 186 29%

Financing (PYD)

200 36% 211 43% 222 50%

0,00%

10,00%

20,00%

30,00%

40,00%

50,00%

60,00%

Aset DPK PYD

Pesimis

Moderat

Optimis

0

50

100

150

200

250

300

Aset DPK PYD

Pesimis

Moderat

Optimis

Growth (%) Growth (Rp. Triliun)

Baseline

Baseline

19..

TERIMA KASIH

20

Associate Prof. Dr. Rifki Ismal is both a central banker and lecturer. He earned bachelor degree in economics from University of Indonesia, master in economics from University of Michigan, ann arbor (USA) and PhD in Islamic economics and Finance from Durham University (England). An Associate Professor in Islamic Banking and Finance is from the Australian Government (Australian Center for Islamic Financial Studies)

SHORT BIO