pension presentation ian metcalf

TRANSCRIPT

Pensions and Auto-Enrolment

Ian Metcalf

Haymarket Associates Ltd

What is a pension?

“A pension is a fixed sum, to be paid regularly to a person, typically following retirement”

But pension income can be derived from a number of sources

So, why the need for change?

Before we can look forward, we have to look backwards

• Once upon a time…• Only the bigger companies had pensions• Pensions were based upon service and final salary• Employees had to stay with the employer to benefit• Protected Rights• This led to more ‘job mobility’

• With Job Mobility came the burden of maintaining a pension scheme for staff who no longer contributed

• Successive pensions ‘scandals’ (Maxwell) tightened the rules governing the funding and administration of pension schemes making the running of a Final Salary scheme administratively burdensome and expensive

• Gradually, Final Salary pensions have died out and have been replaced by ‘Personal’ or ‘Money Purchase’ pension schemes

Demographics and the Baby Boom

• People are generally living longer and retiring earlier• We’re starting work later, too• The Baby Boomers are coming to retirement now and there

is a major demographic shift in the UK• There are now more people in Britain over State Retirement

age than Children (DWP April 2013)• By 2020 the over 50s will represent 48% of the working age

population (DWP April 2013)

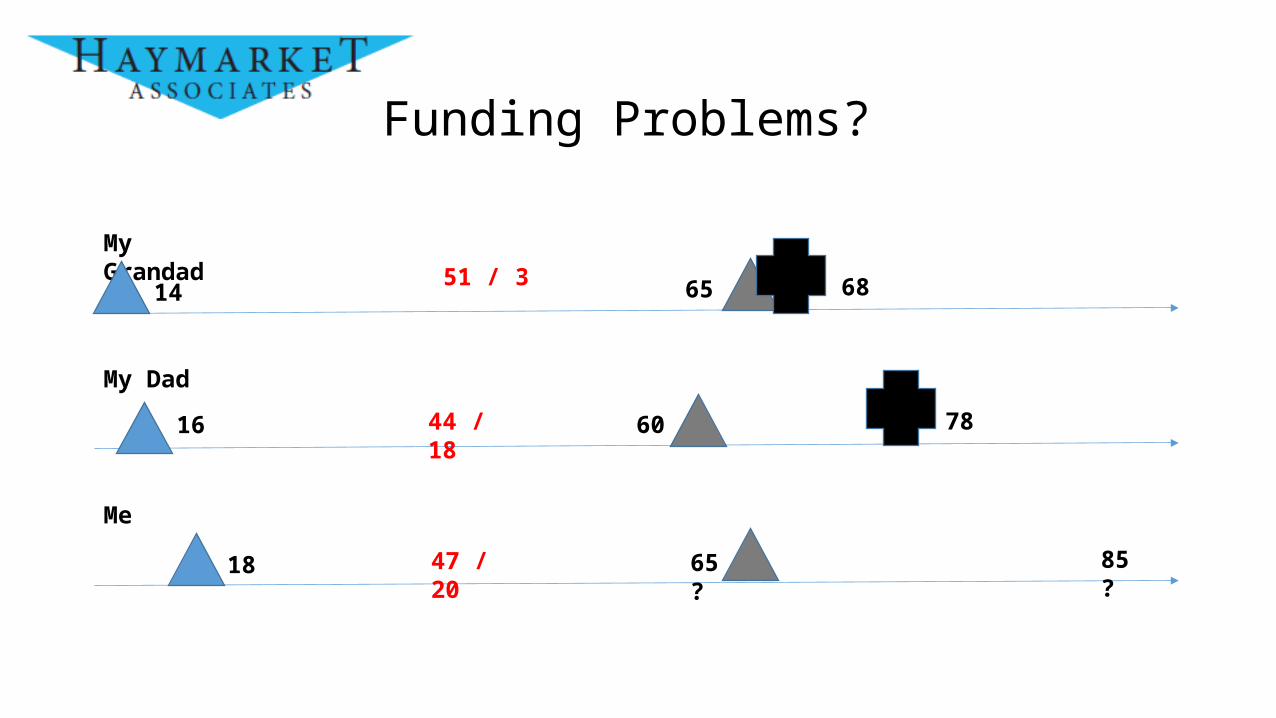

My Grandad

My Dad

Me

14

16

18

65

60

65?

68

78

85?

51 / 3

44 / 18

47 / 20

Funding Problems?

So what can a poor government do?

• Raise the State Retirement Age• Means Test Benefits• Raise taxes and National Insurance to pay pensions• Or…..

•Force people to contribute to pension schemes of their own

Why Now?

• This pensions ‘Time Bomb’ has been ticking for decades• Making these changes is politically dangerous and unpopular• If it’s in a manifesto it would be a vote loser• If it’s not in a manifesto it can’t be implemented early in a

term of office• Closer to elections would mean a danger of not being re-

elected• So successive Governments have kicked this particular can

down the road until changes are absolutely necessary

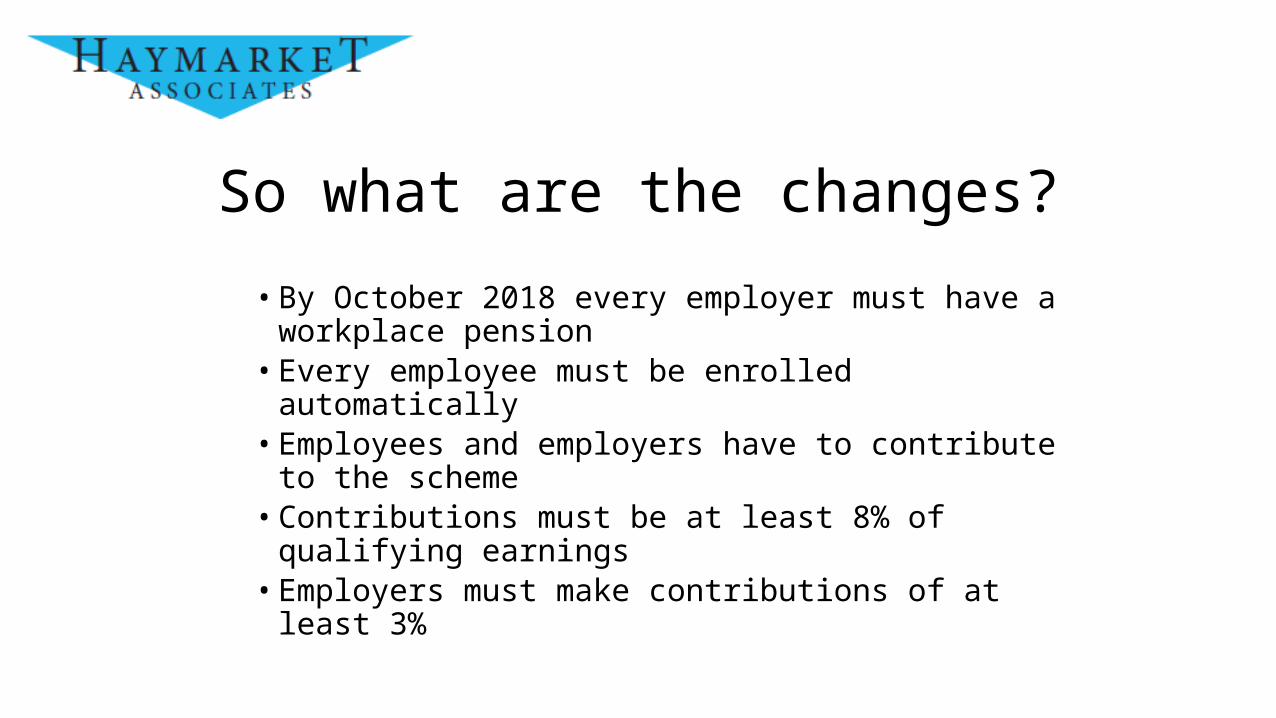

So what are the changes?

• By October 2018 every employer must have a workplace pension• Every employee must be enrolled automatically• Employees and employers have to contribute to the scheme• Contributions must be at least 8% of qualifying earnings• Employers must make contributions of at least 3%

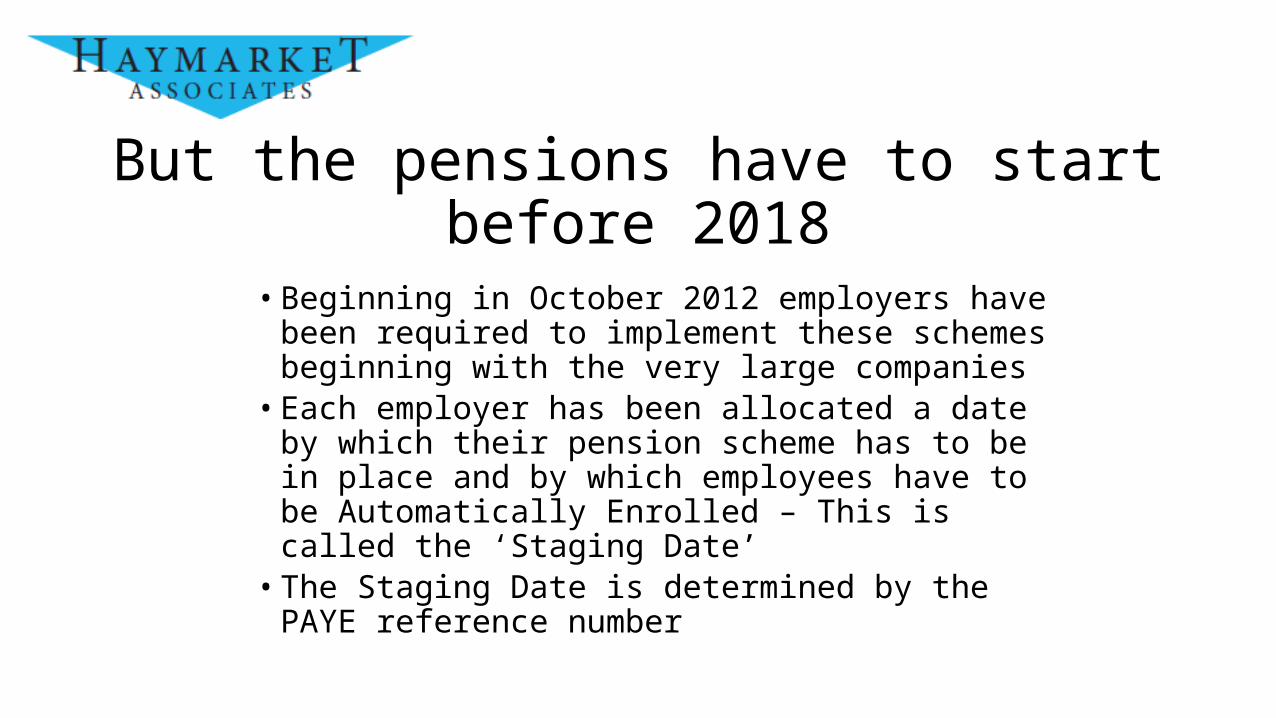

But the pensions have to start before 2018

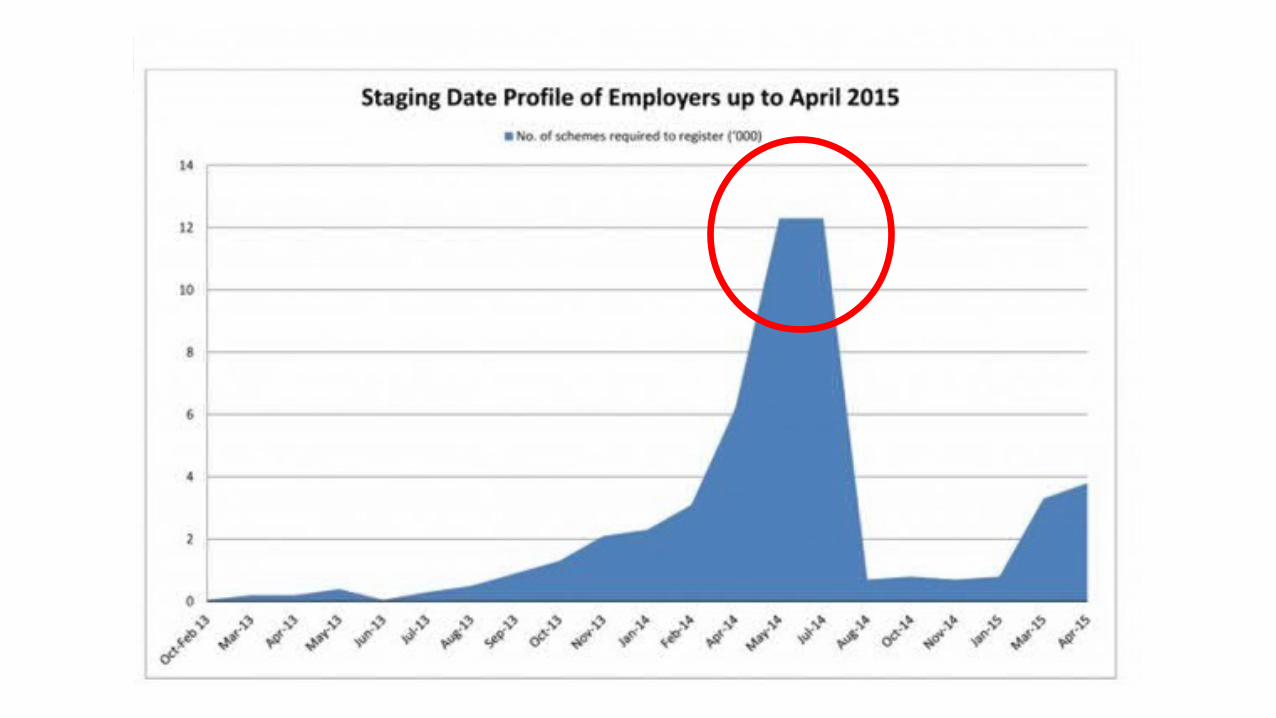

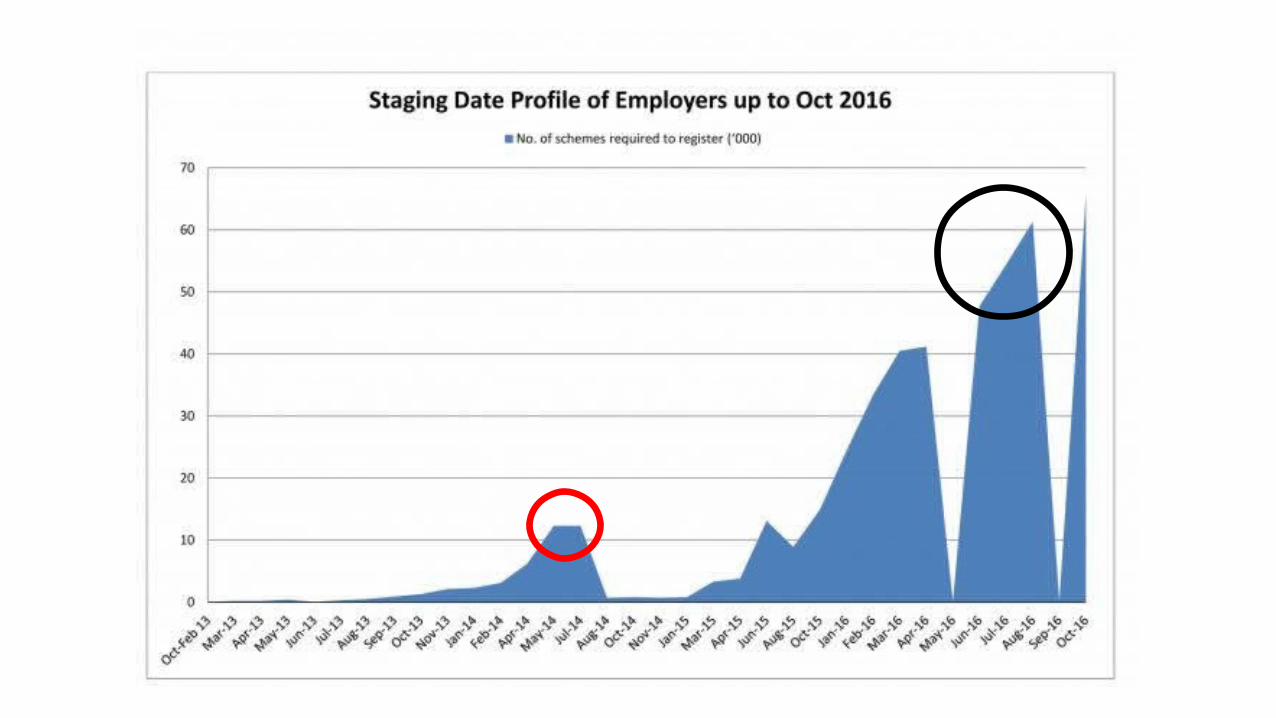

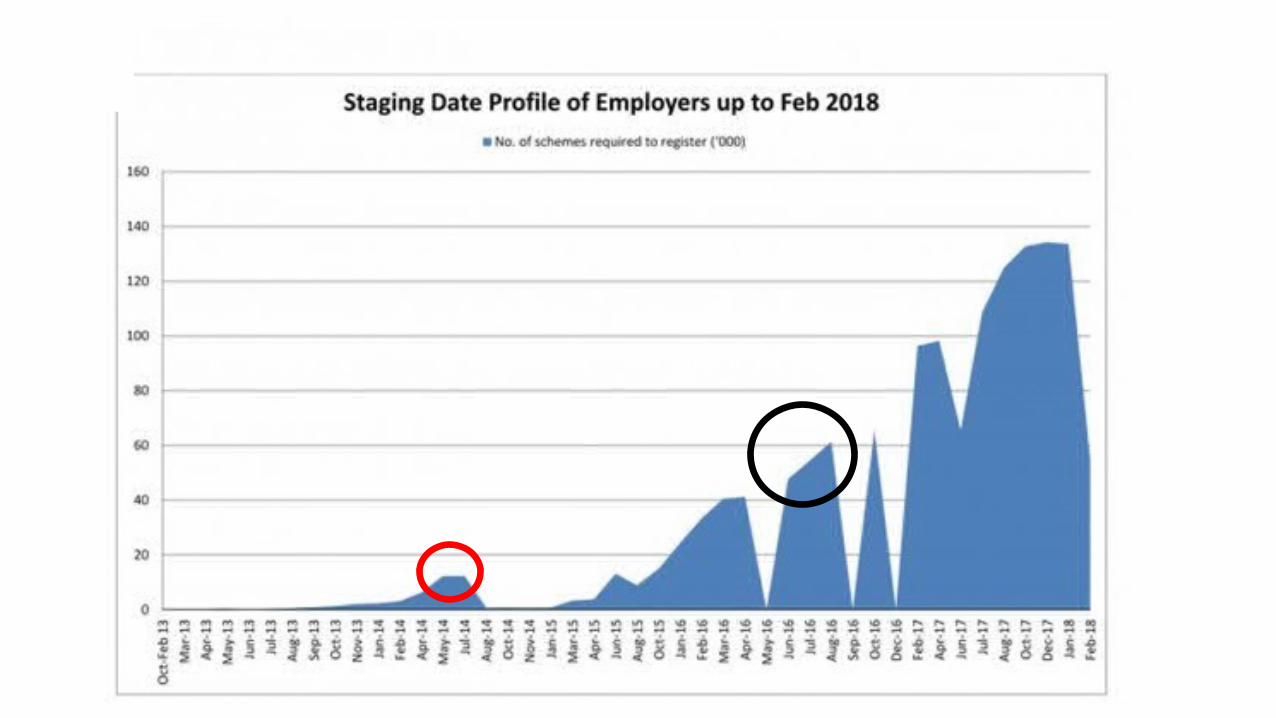

• Beginning in October 2012 employers have been required to implement these schemes beginning with the very large companies• Each employer has been allocated a date by which their

pension scheme has to be in place and by which employees have to be Automatically Enrolled – This is called the ‘Staging Date’• The Staging Date is determined by the PAYE reference

number

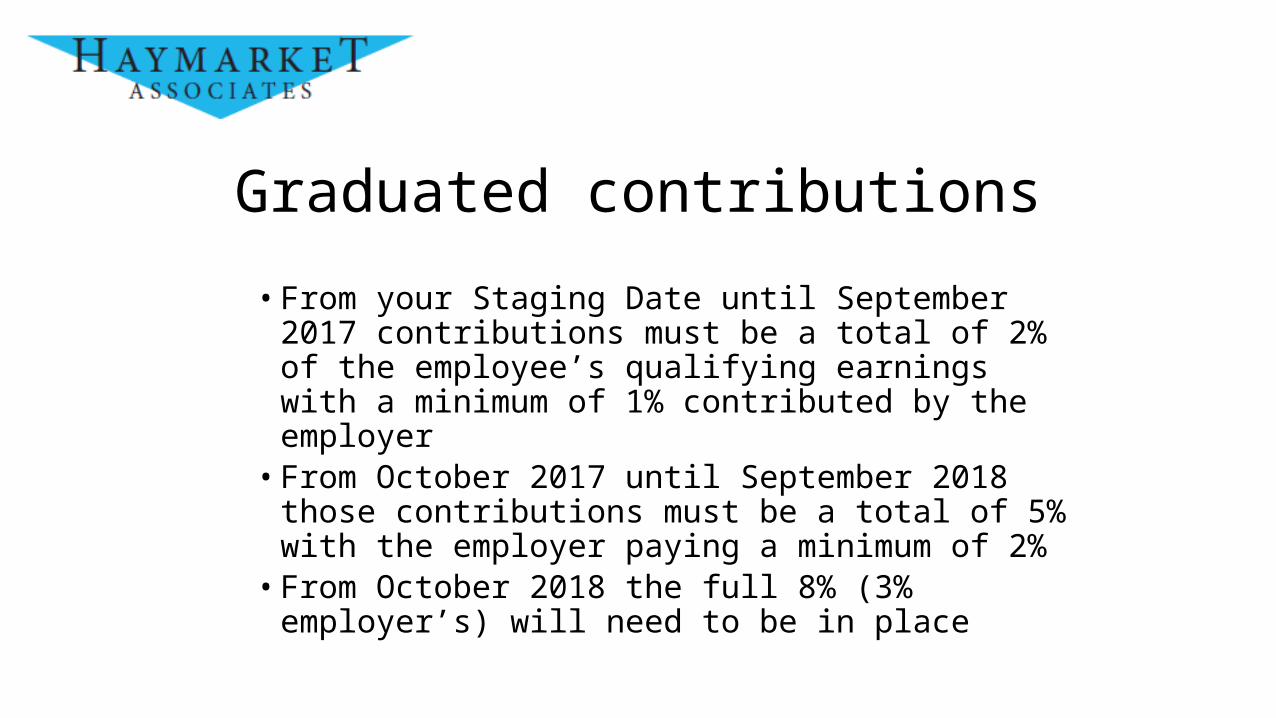

Graduated contributions

• From your Staging Date until September 2017 contributions must be a total of 2% of the employee’s qualifying earnings with a minimum of 1% contributed by the employer• From October 2017 until September 2018 those

contributions must be a total of 5% with the employer paying a minimum of 2%• From October 2018 the full 8% (3% employer’s) will need to

be in place

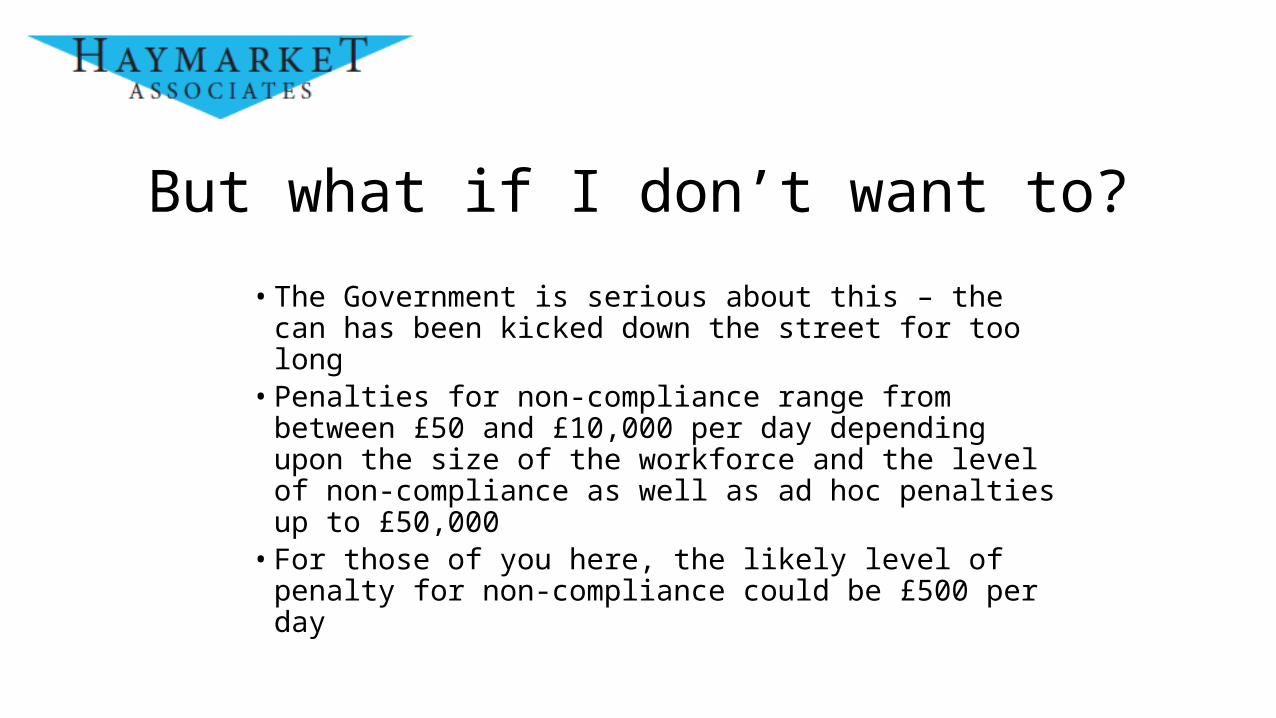

But what if I don’t want to?

• The Government is serious about this – the can has been kicked down the street for too long• Penalties for non-compliance range from between £50 and

£10,000 per day depending upon the size of the workforce and the level of non-compliance as well as ad hoc penalties up to £50,000• For those of you here, the likely level of penalty for non-

compliance could be £500 per day

Fines? I remember Stakeholder!

The Government is serious about this – up to the end of 2014 169 employers have already been fined

What you have to do next

• Firstly, you will need to determine your staging date• Then, assess your workforce for eligibility to the scheme• Choose a pension scheme provider• Communicate with the workforce• Review your contracts of employment• Organise payroll systems to ensure compliance• Implement the pension scheme• Continually monitor and assess the eligibility of employees

What employees have to be enrolled?

• Eligible Job Holders – aged between 16 and State Retirement Age and earning more than £10,000 per annum

• These members have to be enrolled• Members are entitled to ‘opt out’ if they wish but you, as an employer, are

forbidden to persuade them not to join or to opt out• Non-Eligible Job Holders – aged between 16 and State Retirement Age and

earning between £5,824 / a and £10,000 per annum or earn above £10,000 / a and are under 22 or over State Retirement Age

• These members do not have to be enrolled unless they specifically wish to join and you will have to allow this

• Other Entitled workers outside these categories have a right to join a pension scheme but the employer can choose a different scheme

Choosing a Pension Scheme

• Is Cheapest Best?

What do you want from a pension?

Do you simply want to get past the legislation and do the minimum possible?

Isn’t that a little like learning enough to pass your driving test but not really learning how to drive properly?

Or do you want to ensure that your employees have a pension that is worthwhile and one that will go someway towards helping provide properly for them in retirement?

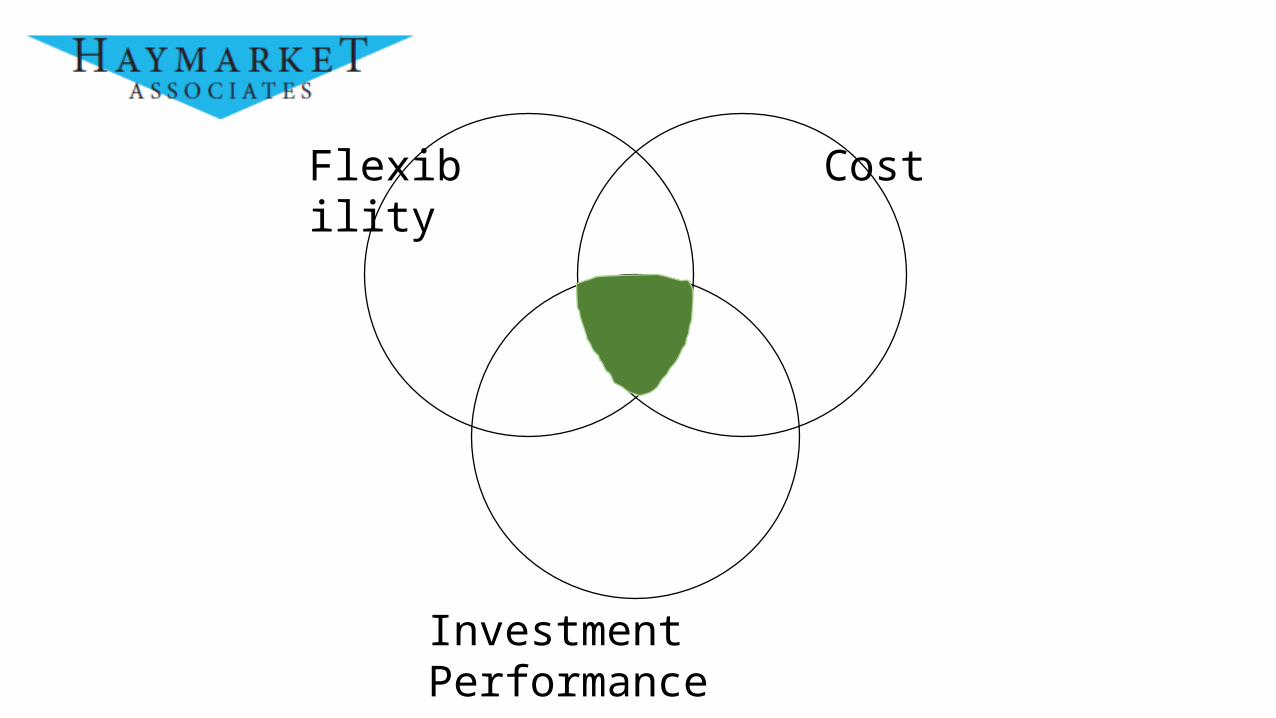

If you were to choose a pension scheme on merit, there are three main factors to take into

consideration …

Flexibility Cost

Investment Performance

Let’s take a closer look at why performance is so important …

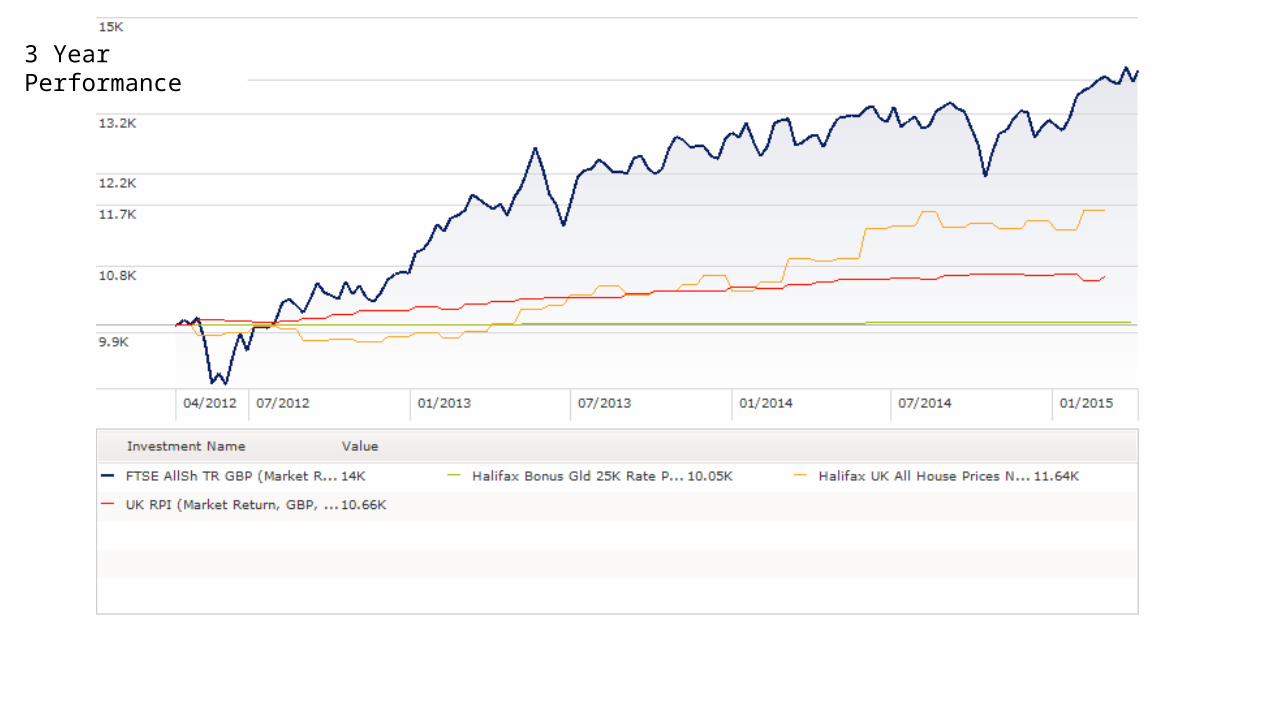

Why do most long term investments such as pension funds invest in equities (Stocks and Shares)? The following graphs show the performance of Stocks and Shares (the FTSE All Share Index) compared with Savings, Inflation and Property.

3 Year Performance

5 Year Performance

10 Year Performance

15 Year Performance

20 Year Performance

Diversifying not only protects but enhances

Diversification – Non Correlation

20 Year Performance

The Performance of a good pension fund can outweigh the costs

You would only pay for higher investment fund costs if the performance was justifying it

Is cheap really cheap anyway?

• NEST, NOW Pension, Peoples Pension• Limited Investment Range – no track record or poor approach• High Initial Charges • Nest – 1.8% of contributions and 0.3% of the value of the fund• Now - £3.60 - £18 per annum and 0.3% of the value of the fund• Limited Flexibility• Other drawbacks

• Not in Trust• No Transfers in or out

It has been said that the definition of an ‘expert’ is someone who knows when to call an expert in

If you are really looking to provide a worthwhile solution for your staff and not simply ‘pass your driving test’ then it’s worth seeking expert advice to choose the correct pension scheme

But hurry!

Leaving this to the very last minute before your Staging Date would be a ‘very brave’ thing to do

Find out your staging date immediately and seek advice as soon as possible

Questions

Ian Metcalf

Haymarket Associates Ltd