payments plus q1 2021 - oliver wyman

TRANSCRIPT

Q1 2021

Best wishes, Davin ChowPartner

A FRESH START FOR PAYMENTSAs we begin 2021, having navigated almost a year of global crisis, it is clear that payments is a dynamic and innovative industry that has been accelerated, not slowed, by the pandemic. The drivers of change are numerous, from evolving consumer needs and industry consolidation to government and regulatory action and technology development. While we may have seen shifts in the mix of global economic activity, the underlying need for payments to facilitate domestic and international commerce persists.

One recent area of note has been the establishment of new, innovative payment schemes, either by individual providers or by cooperative groups of industry participants. In Europe, a group of 21 major players (banks, acquirers, and industry consortia) from five countries has come together to launch the European Payments Initiative (EPI), intended to deliver an innovative pan-European payment solution providing greater choice and sovereignty for banks, merchants, payment processors, and consumers. We are pleased to announce that Martina Weimert, a partner in our European Financial Services Practice based in Paris, has been appointed chief executive of the EPI Interim Company.

In the following pages, you will see profiles of the work we are doing with clients to develop new propositions, capture market opportunities, and organize effectively for the long term.

As always, we welcome your feedback and thoughts.

PAYMENTS PLUS / MARKET DEVELOPMENTS

INVESTING IN PAYMENTS

Q1 2021

+FINANCIAL SPONSORS+DUE DILIGENCE

Investors have long loved the payments industry. And why not? It is a large, growing market with a healthy cycle of disruption and innovation. Leading players earn attractive returns with capital-efficient business models. Perhaps most important, payments businesses sell for very attractive multiples.

The past year has been an active one for payments M&A, with many willing buyers combing through a rich and diverse set of targets. Transactions have spanned a range of segments and models: issuing, acquiring, fraud prevention services, technology enablement, infrastructure, and so on. All are angling to separate themselves from the field with the help of the right financial sponsor.

Oliver Wyman has recently worked with several leading private equity firms to evaluate financial investments in payments companies. Specifically, we have conducted commercial due diligence

analyses that inform investment hypotheses across digital payments and wallet providers, prepaid cards, payroll, cross-border payments, card features, and many more. This work has included defining the total addressable market, detailing the basis of competition in the relevant segments, evaluating the targets’ right to play and right to win, understanding customer perspectives, and examining the long-term defensibility of competitive moats. Through these processes we work collaboratively with our private equity clients, iteratively sharing and testing ideas with a focus on answering the most important questions.

Our assistance with due diligence has contributed to the completion of prominent industry transactions this year. And our work does not stop there — we are now collaborating with several portfolio companies to realize their full potential in this dynamic market.

PAYMENTS PLUS / MARKET DEVELOPMENTS

NEW CREDIT CARD PROPOSITIONS

Q1 2021

+PRODUCT DEVELOPMENT +RAPID PROTOTYPING

Credit card issuers face a unique set of challenges in markets around the globe. Credit growth in many markets has declined through the course of the pandemic. Competition is increasingly intense, and while fintechs in many markets have historically been debit-centric, their product suites are expanding to include credit card propositions. We see a rise in “greenfield” credit card product launches from fintechs coming to market with their first products. On top of that, there is a tremendous explosion in buy now, pay later (BNPL) volumes. In select global markets, BNPL is already accounting for more than 10 percent of e-commerce volume, from almost nothing five to 10 years ago. The combination of pandemic pressures and new competition has prompted issuers to re-examine their current credit card value propositions.

Oliver Wyman has been working with a number of issuers globally to develop new propositions that are significantly different from their current offerings. In one instance, Oliver Wyman worked in a rapid, collaborative, co-creation format to develop a new credit card proposition and deliver a technology implementation roadmap to get the product quickly into the market. The work included defining the competitive landscape, customer-testing, and rapidly iterating wireframes to refine the proposition. We also facilitated engagement with product and technology to design a plan to bring the proposition in at budget and capable of delivering a unique solution.

PAYMENTS PLUS / MARKET DEVELOPMENTS

ESTABLISHING A NEW PAYMENTS ASSOCIATION

Q1 2021

+GUIDING PRINCIPLES+OPERATING MODEL

Many payments organizations are structured as associations of members. Think of the card networks before they became public companies, national payment schemes such as Interac, or international providers like SWIFT. Systemic payments endeavors usually require a degree of mutual cooperation between participants in areas such as setting the direction and mission of the organization, deciding on the scope of what the endeavor will and won’t do, and creating the rules and governance for participation. This mutual nature is fundamentally different from ordinary, profit-seeking commercial entities.

Of course, the association structure comes with its own challenges. These organizations are often created around a motivating mission, but stakeholders can have disparate views of how the mission should be pursued. This goes beyond the association’s members and can also affect the leadership and employees who come to the organization with their own views of mission and vision.

Oliver Wyman recently worked with a newly established payments association. The organization had developed a clear mission and vision, but there was a desire to drive more convergence among employees and other stakeholders on how this was to be pursued. We helped the association’s leadership develop a set of guiding principles and articulate a target operating model consistent with the mission and vision. We did this through deep engagement with staff and a series of focused workshops. The outcomes of these efforts have been used to give clear direction and guidance to employees, and to articulate to the membership how the association was pursuing its mission on their behalf.

PAYMENTS PLUS / MARKET DEVELOPMENTS

TRANSFORMING WHOLESALE PAYMENTS

Q1 2021

+COMMERCIAL EFFECTIVENESS+FEE INCOME

Wholesale payments and cash management businesses had a challenging year, with global revenue pools down 16 percent in the first nine months of 2020. Despite growing cash balances as corporates have built up cash reserves, declining commercial payment volumes and net interest margin compression have weighed on business performance. The gloomy outlook, combined with competitive pressure from new entrants, has put the commercial model in focus. In the near-term, banks are looking to increase fee income any way they can in order to plug the gap in interest income. In the medium term, they are looking to reset their commercial models away from interest income in favor of recurring fee income.

Oliver Wyman has been working with global transaction banks to help them generate more fee income in 2021 as well as lay the foundations for a broader shift in their commercial models in favor of recurring fee income. The levers

are broad, ranging from housekeeping such as addressing billing leakage (gaps between contractual entitlements and actual billed fees) to resetting standard price tariffs and better aligning discounting with customer value. Beyond the basics, we have developed plans to deliver a step-change in the commercial models to better align pricing to client value, including the introduction of packaged and subscription pricing for smaller clients, holistic relationship-based pricing for larger clients, and monetization of channels and APIs.

In a representative case we identified a 25 to 30 percent increase in fee income. Across the industry, the level of pricing maturity in wholesale banks is relatively low compared with nonbank payments providers, but as the old net-interest-income-centric model breaks down, we believe pricing and commercial effectiveness will become key differentiators for wholesale banks in the coming years.

PAYMENTS PLUS / MARKET DEVELOPMENTS

DELIVERING MERCHANT SERVICES DIFFERENTLY

Q1 2021

+DISTRIBUTION+ECONOMICS

The US merchant services market is large, complex, and highly competitive. A wide variety of providers help millions of merchant clients around the world, from micro-businesses to the largest retailers, to accept cards and other forms of payment. These merchants collectively generate $7.2 trillion in payment volume and $17 billion in merchant services revenue a year.

The market has specific needs driven by history and regulation (for example the compulsory co-badging of debit cards), and the means of delivering payment services is rapidly evolving, as payments are integrated into broader software and business solutions. Large direct acquirers as well as banks have traditionally dominated, but new entrants such as Square, Stripe, PayPal, and others have experienced significant growth in recent years.

Oliver Wyman recently worked with a financial institution looking to change the way it serves merchants. Historically, the institution partnered with a large merchant services provider in a referral arrangement. This allowed it to serve its clients’ needs and generated a recurring stream of revenue, but it resulted in an arrangement that was nonstrategic and lacked differentiation and focus. We helped the client assess what it would take to win in the market with a proprietary offering. We also analyzed the different distribution options and the corresponding economics. The work has helped the client shape its decisions on whether and how to invest to win.

PAYMENTS PLUS / PERSPECTIVES

QR CODE PAYMENTS

Alipay and Walgreens announce US partnership

Walmart makes checkout completely contact free with QR code

PayPal and Venmo payments enabled in-store at CVS using QR code

Restaurants enhance touchless dining experience with Clover’s “scan to order”

If you follow payments news, you have likely come across a number of press releases announcing new ways to pay. A common thread in many of these releases is the QR code as the base technology. QR code has long been the standard for payments in many parts of Asia but has failed to catch on in North America given the prevalence of card payments, among other factors. In 2020, COVID-19 enabled a rapid shift toward digital and touchless transactions and QR code has been a natural choice to enable them.

Perspectives

Oliver Wyman works closely with industry leaders, regulators, and academic experts to develop and deliver breakthrough solutions based on our deep understanding of issues and developments on the ground and across businesses.

February2019

March2020

August 2020

October 2020

Oliver Wyman has been at the forefront of helping clients understand the drivers of QR code adoption in North America and navigate the landscape. Fundamentally, QR code is a fairly simple technology that already works with most scanners and point-of-sale systems. It is much more flexible than other transaction protocols and better able to carry incremental data such as loyalty and offer information. It provides merchants with an ability to exercise more control over payments and loyalty relative to traditional mechanisms. Most important, it can deliver a single experience across mobile device platforms, while other near field communication (NFC)-based transaction methods are affected by device manufacturer limitations (for example, Apple's restrictions on access to the secure element of NFC hardware, meaning iOS and Android experiences are not consistent).

Select Examples

Q1 2021

Building a full-service customer mobile experience is critical for many retailers these days. To do so, a provider must fulfill three core roles: (A) manage the customer platform, incorporating loyalty and payments; (B) develop the app with in-store mobile checkout capabilities; and (C) process and settle in-app transactions. An indicative payment transaction flow based on QR codes that highlights these three roles is depicted below:

Other technologies are increasing consumers' familiarity with QR codes. Some restaurants have placed QR codes at the table so patrons can pull up a menu. Many curbside delivery systems are using QR codes to identify customers and match orders. As these types of everyday transactions increase, we anticipate the growth of QR codes into other areas, accounting for more than $50 billion in payments volumes by 2024 in the United States.

AC

POS System

Stored Value ProgramManager

Loyalty PlatformSponsor

BankIssuing

ProcessorNetwork

QR CodeCustomer

BApp Developer

PAYMENTS PLUS / INSIGHTS

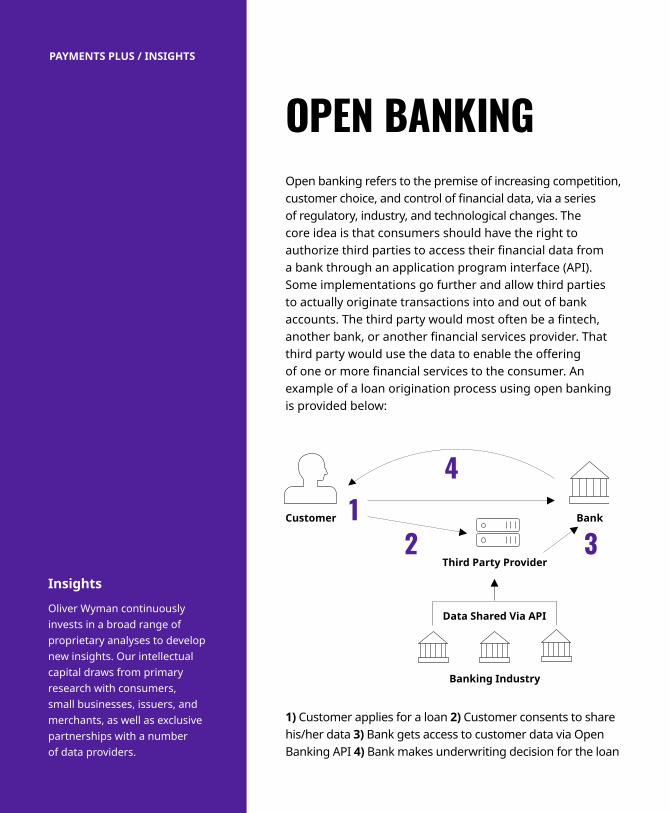

Open banking refers to the premise of increasing competition, customer choice, and control of financial data, via a series of regulatory, industry, and technological changes. The core idea is that consumers should have the right to authorize third parties to access their financial data from a bank through an application program interface (API). Some implementations go further and allow third parties to actually originate transactions into and out of bank accounts. The third party would most often be a fintech, another bank, or another financial services provider. That third party would use the data to enable the offering of one or more financial services to the consumer. An example of a loan origination process using open banking is provided below:

OPEN BANKING

Insights

Oliver Wyman continuously invests in a broad range of proprietary analyses to develop new insights. Our intellectual capital draws from primary research with consumers, small businesses, issuers, and merchants, as well as exclusive partnerships with a number of data providers.

132

4

Banking Industry

BankCustomer

Third Party Provider

Data Shared Via API

1) Customer applies for a loan 2) Customer consents to share his/her data 3) Bank gets access to customer data via Open Banking API 4) Bank makes underwriting decision for the loan

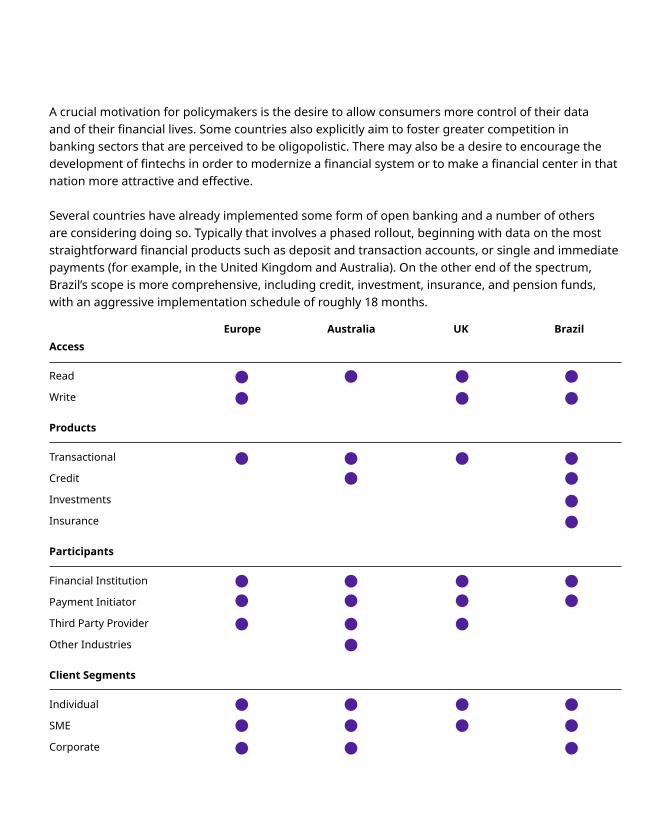

A crucial motivation for policymakers is the desire to allow consumers more control of their data and of their financial lives. Some countries also explicitly aim to foster greater competition in banking sectors that are perceived to be oligopolistic. There may also be a desire to encourage the development of fintechs in order to modernize a financial system or to make a financial center in that nation more attractive and effective.

Several countries have already implemented some form of open banking and a number of others are considering doing so. Typically that involves a phased rollout, beginning with data on the most straightforward financial products such as deposit and transaction accounts, or single and immediate payments (for example, in the United Kingdom and Australia). On the other end of the spectrum, Brazil’s scope is more comprehensive, including credit, investment, insurance, and pension funds, with an aggressive implementation schedule of roughly 18 months.

Access

Read

Write

Products

Transactional

Credit

Investments

Insurance

Participants

Financial Institution

Payment Initiator

Third Party Provider

Other Industries

Client Segments

Individual

SME

Corporate

UKEurope Australia Brazil

PAYMENTS PLUS / OLIVER WYMAN REPORTS

Oliver Wyman publishes a broad range of points-of-view across industries. A sample of our recently released intellectual capital is shown here.

The report images are hyperlinked. Please click to view or download the document.

Making The Invisible Visible Anticipating The Travel Recovery

Manufacturing Industries 2030

Financial Regulation Under Biden

OLIVER WYMAN REPORTS

Q1 2021

Ready Food Open Data Is Essential For Small Business Recovery

Rethink. Reboot. Recoup.

Time To Look At Costs The Post-COVID Opportunity For Banks

AI For Governments

OLIVER WYMAN REPORTS

PAYMENTS PLUS / CELENT REPORTS

Celent, a division of Oliver Wyman, is the leading subscription research and advisory firm focused on financial services technology.

Rethinking The Role Of QR Codes In Payments

Open Banking Enables New Retail Banking Propositions In Europe

The Evolution Of Europe’s TPP Ecosytem

Protecting Payments In The Cloud

CELENT REPORTS

Q1 2021

The Digital Journey In Life And Health Insurance

Request To Pay: A Payments Revolution?

Top Technology Trends In KYC-AML: Transforming AML Operations In The Digital Era

Investment Recommendation Engines: Using Ml To Automate Investment Advice

Keeping A Grip On Employee Conduct And Conflicts Of Interest

Health And Insurance: Health Informatics, Internet Of Things, And Integrated Electronic Health Records

INVESTMENT RECOMMENDATION ENGINES: USING ML TO AUTOMATE INVESTMENT ADVICE

THE DIGITAL JOURNEY IN LIFE AND HEALTH INSURANCE

KEEPING A GRIP ON EMPLOYEE CONDUCT AND CONFLICTS OF INTEREST

TOP TECHNOLOGY TRENDS IN KYC-AML: TRANSFORMING AML OPERATIONS IN THE DIGITAL ERA

HEALTH AND INSURANCE: HEALTH INFORMATICS, INTERNET OF THINGS, AND INTEGRATED ELECTRONIC HEALTH RECORDS

The Merchant Advisory Group (MAG) is the leading payments-focused association for merchants in the United States. In February we will be virtually attending the MAG 2021 Mid-Year Conference.

Beth Costa will moderate a panel titled “Emerging Checkout Experiences That Consumers Are Watching.” The panel will explore how merchants should think about and plan for upgrading their shopping experiences to meet consumer expectations in 2021.

Rob Mau will serve as a panelist on the topic “Cybersecurity: Identify Good Transactions.” The session will center on merchant strategies to distinguish between good transactions and risky ones to optimize authorization rates.

PAYMENTS PLUS / EVENTS

EVENTS

PAYMENTS + BRAND

PAYMENTS + DIGITAL

PAYMENTS + STRATEGY

PAYMENTS + OPERATIONS

PAYMENTS + TECHNOLOGY

PAYMENTS + PARTNERSHIPS

PAYMENTS + DUE DILIGENCE

PAYMENTS + DATA & ANALYTICS

PAYMENTS + RISK MANAGEMENT

PAYMENTS + CUSTOMER EXPERIENCE

PAYMENTS + ORGANIZATIONAL EFFECTIVENESS

Oliver Wyman is a wholly owned subsidiary of Marsh & McLennan Companies [NYSE: MMC].

Oliver Wyman is a global leader in management consulting with offices in 60 cities across 29 countries