palmyra area school district 1125 park drive … area school district 1125 park drive palmyra, 17078...

TRANSCRIPT

Palmyra Area School District1125 Park DrivePalmyra, 17078

Planned Instruction for:

Accounting II

Grade Levels:

11, 12

Authors:

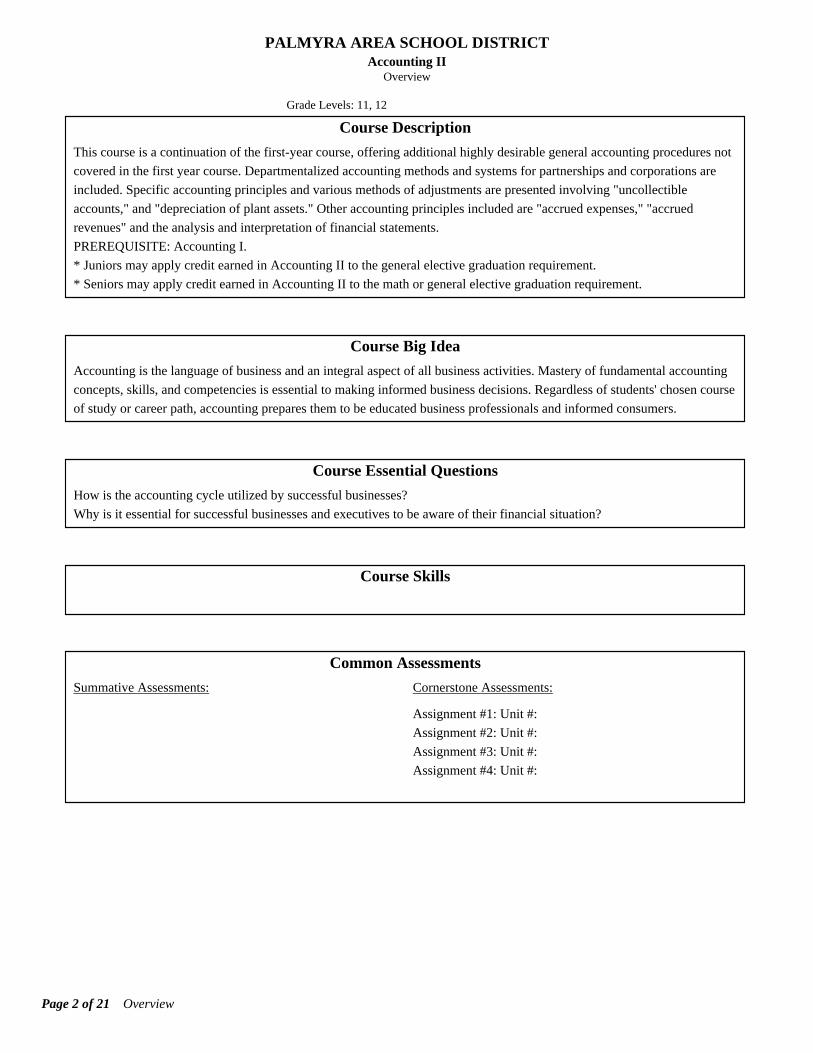

PALMYRA AREA SCHOOL DISTRICTAccounting II

Overview

Grade Levels: 11, 12

Course Description

This course is a continuation of the first-year course, offering additional highly desirable general accounting procedures not

covered in the first year course. Departmentalized accounting methods and systems for partnerships and corporations are

included. Specific accounting principles and various methods of adjustments are presented involving "uncollectible

accounts," and "depreciation of plant assets." Other accounting principles included are "accrued expenses," "accrued

revenues" and the analysis and interpretation of financial statements.

PREREQUISITE: Accounting I.

* Juniors may apply credit earned in Accounting II to the general elective graduation requirement.

* Seniors may apply credit earned in Accounting II to the math or general elective graduation requirement.

Course Big Idea

Accounting is the language of business and an integral aspect of all business activities. Mastery of fundamental accounting

concepts, skills, and competencies is essential to making informed business decisions. Regardless of students' chosen course

of study or career path, accounting prepares them to be educated business professionals and informed consumers.

Course Essential Questions

How is the accounting cycle utilized by successful businesses?

Why is it essential for successful businesses and executives to be aware of their financial situation?

Course Skills

Common Assessments

Summative Assessments: Cornerstone Assessments:

Assignment #1: Unit #:

Assignment #2: Unit #:

Assignment #3: Unit #:

Assignment #4: Unit #:

Page 2 of 21 Overview

PALMYRA AREA SCHOOL DISTRICTAccounting II

Curriculum Map Planning Chart

Grade Levels: 11, 12

Curricular Concepts Pacing Resources

Unit #1: Adjustments and

Valuation44 Day(s)

Century 21 Accounting, Multicolumn Journal, 9th Edition Textbook and

Workbook

Whiteboard

Overhead Transparencies (as needed)

Document Camera

PowerPoint Presentations

Projector

Ruler

Calculator

Chapter Handouts

Excel/Laptop

Moodle

Unit #2: Additional Accounting

Procedures7 Day(s)

Century 21 Accounting, Multicolumn Journal, 9th Edition Textbook and

Workbook

Whiteboard

Overhead Transparencies (as needed)

Document Camera

PowerPoint Presentations

Projector

Ruler

Calculator

Chapter Handouts

Excel/Laptop

Moodle

Unit #3: Departmental

Accounting

Century 21 Accounting, Multicolumn Journal, 9th Edition Textbook and

Workbook

Whiteboard

Overhead Transparencies (as needed)

Document Camera

PowerPoint Presentations

Projector

Ruler

Calculator

Chapter Handouts

Excel/Laptop

Moodle

Unit #4: Business Operating

Activities

Whiteboard

Document Camera

PowerPoint Presentations

Projector

Ruler

Calculator

Chapter Handouts

Page 3 of 21 Curriculum Map Planning Chart

Curricular Concepts Pacing Resources

Laptop/Excel/Word

Moodle

Page 4 of 21 Curriculum Map Planning Chart

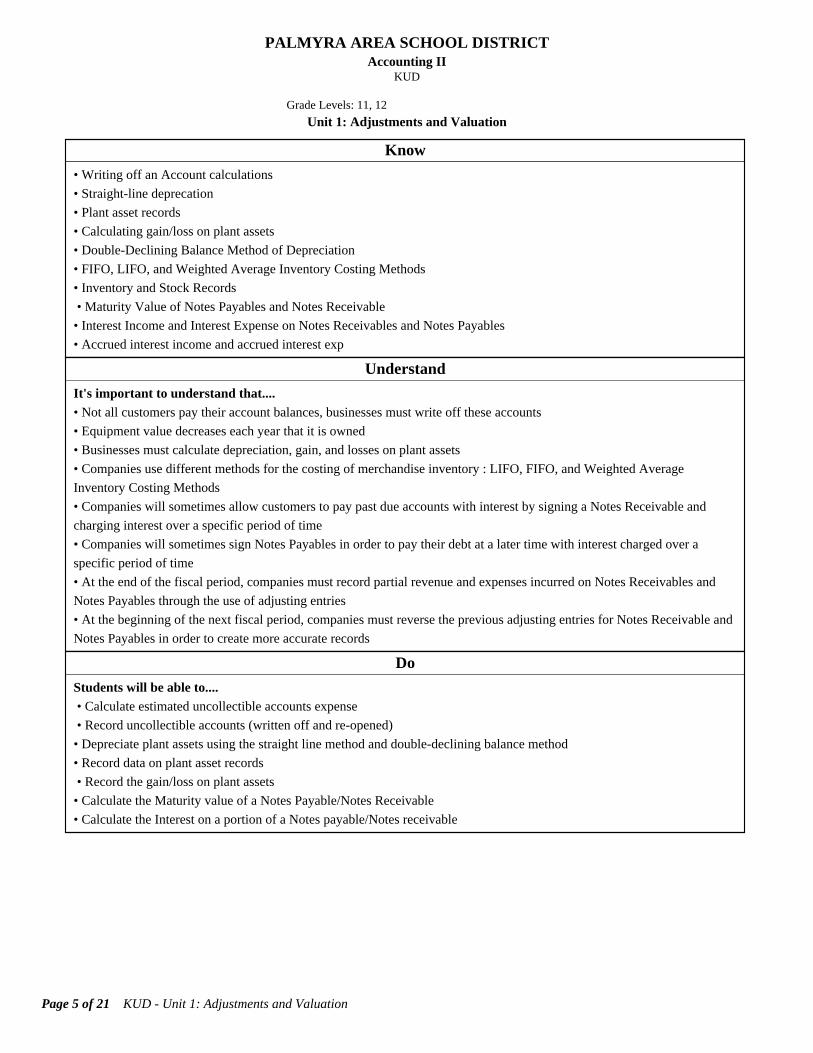

PALMYRA AREA SCHOOL DISTRICTAccounting II

KUD

Grade Levels: 11, 12

Unit 1: Adjustments and Valuation

Know

• Writing off an Account calculations

• Straight-line deprecation

• Plant asset records

• Calculating gain/loss on plant assets

• Double-Declining Balance Method of Depreciation

• FIFO, LIFO, and Weighted Average Inventory Costing Methods

• Inventory and Stock Records

• Maturity Value of Notes Payables and Notes Receivable

• Interest Income and Interest Expense on Notes Receivables and Notes Payables

• Accrued interest income and accrued interest exp

Understand

It's important to understand that.... • Not all customers pay their account balances, businesses must write off these accounts

• Equipment value decreases each year that it is owned

• Businesses must calculate depreciation, gain, and losses on plant assets

• Companies use different methods for the costing of merchandise inventory : LIFO, FIFO, and Weighted Average

Inventory Costing Methods

• Companies will sometimes allow customers to pay past due accounts with interest by signing a Notes Receivable and

charging interest over a specific period of time

• Companies will sometimes sign Notes Payables in order to pay their debt at a later time with interest charged over a

specific period of time

• At the end of the fiscal period, companies must record partial revenue and expenses incurred on Notes Receivables and

Notes Payables through the use of adjusting entries

• At the beginning of the next fiscal period, companies must reverse the previous adjusting entries for Notes Receivable and

Notes Payables in order to create more accurate records

Do

Students will be able to.... • Calculate estimated uncollectible accounts expense

• Record uncollectible accounts (written off and re-opened)

• Depreciate plant assets using the straight line method and double-declining balance method

• Record data on plant asset records

• Record the gain/loss on plant assets

• Calculate the Maturity value of a Notes Payable/Notes Receivable

• Calculate the Interest on a portion of a Notes payable/Notes receivable

Page 5 of 21 KUD - Unit 1: Adjustments and Valuation

PALMYRA AREA SCHOOL DISTRICTAccounting II

Unit Map

Grade Levels: 11, 12

Unit 1: Adjustments and Valuation

Day(s): 44

Unit Essential Question(s)

How does a corporation calculate and record entries for uncollectible accounts, plant assets and depreciation, inventory, notes and interest, and accruedrevenue and expenses?

Materials/Resources

Century 21 Accounting, Multicolumn Journal, 9th Edition Textbook and Workbook

Whiteboard

Overhead Transparencies (as needed)

Document Camera

PowerPoint Presentations

Projector

Ruler

Calculator

Chapter Handouts

Excel/Laptop

Moodle

Vocabulary

Writing off an Account

Real Property, Personal Property, Assessed Value, Plant asset record, Gain on plant assets, Loss on plant assets, Declining-balance method ofdepreciation

Periodic inventory, Perpetual inventory, Inventory record, Stock record, Stock ledger, Last-in first out inventory costing method, First-in first-outinventory costing method, Weighted-average inventory costing method, Gross-profit method of estimating inventory

Number of a note, Date of a note, Payee of a note, Time of a note, Principal of a note, Interest rate of a note, Maturity date of a note, Maker of a note,Promissory note, Creditor, Notes payable, Interest, Maturity value, Current liabilities, Interest expense, Notes receivable, Interest income, Dishonorednote

Accrued revenue, Intellectual property, Accrued interest income, Reversing entry, Accrued expenses, Accrued interest expense

Long-term liabilities, Working Capital, Current Ratio

Unit Assessment(s)

Reinforcement Activity 3 Parts A and B

Launch Activities

Review of Basic Accounting Concepts

• Students will review the Chart of Accounts, Debits and Credits, transactions, posting, and basic definitions

Students should complete the following: (teacher created materials for review)

• Review of Debits and Credits Worksheet

Page 6 of 21 Unit Map - Unit 1: Adjustments and Valuation

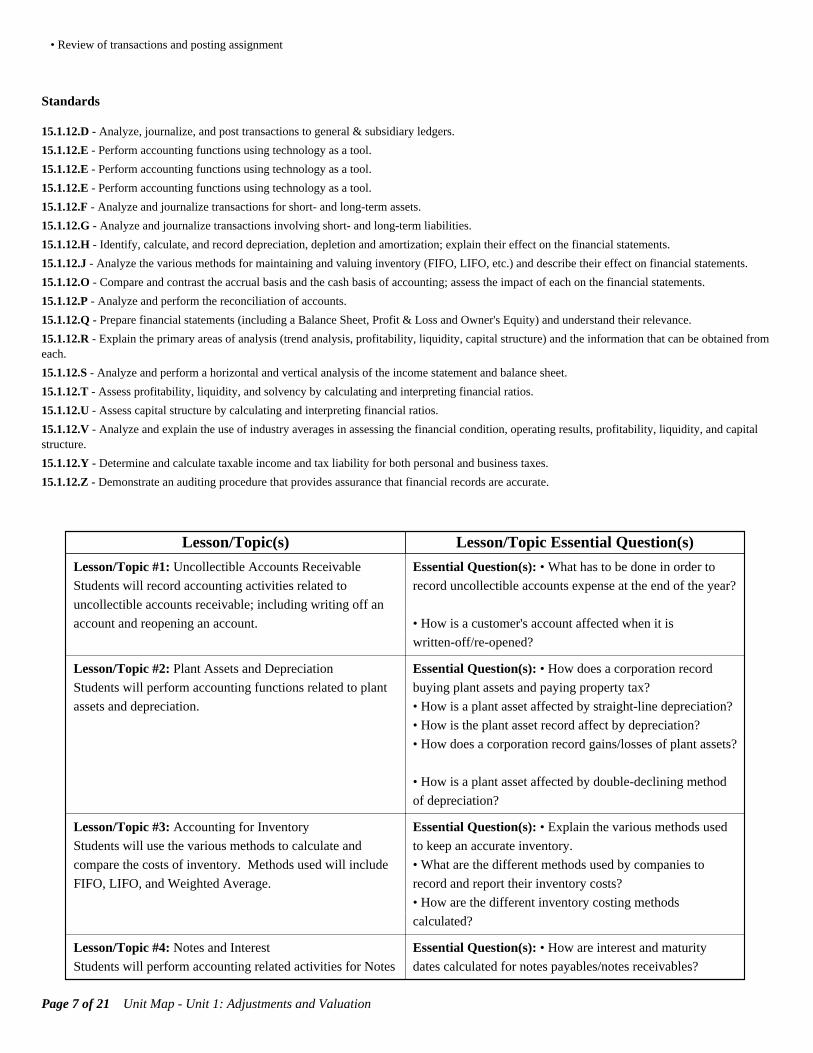

• Review of transactions and posting assignment

Standards

15.1.12.D - Analyze, journalize, and post transactions to general & subsidiary ledgers.

15.1.12.E - Perform accounting functions using technology as a tool.

15.1.12.E - Perform accounting functions using technology as a tool.

15.1.12.E - Perform accounting functions using technology as a tool.

15.1.12.F - Analyze and journalize transactions for short- and long-term assets.

15.1.12.G - Analyze and journalize transactions involving short- and long-term liabilities.

15.1.12.H - Identify, calculate, and record depreciation, depletion and amortization; explain their effect on the financial statements.

15.1.12.J - Analyze the various methods for maintaining and valuing inventory (FIFO, LIFO, etc.) and describe their effect on financial statements.

15.1.12.O - Compare and contrast the accrual basis and the cash basis of accounting; assess the impact of each on the financial statements.

15.1.12.P - Analyze and perform the reconciliation of accounts.

15.1.12.Q - Prepare financial statements (including a Balance Sheet, Profit & Loss and Owner's Equity) and understand their relevance.

15.1.12.R - Explain the primary areas of analysis (trend analysis, profitability, liquidity, capital structure) and the information that can be obtained fromeach.

15.1.12.S - Analyze and perform a horizontal and vertical analysis of the income statement and balance sheet.

15.1.12.T - Assess profitability, liquidity, and solvency by calculating and interpreting financial ratios.

15.1.12.U - Assess capital structure by calculating and interpreting financial ratios.

15.1.12.V - Analyze and explain the use of industry averages in assessing the financial condition, operating results, profitability, liquidity, and capitalstructure.

15.1.12.Y - Determine and calculate taxable income and tax liability for both personal and business taxes.

15.1.12.Z - Demonstrate an auditing procedure that provides assurance that financial records are accurate.

Lesson/Topic(s) Lesson/Topic Essential Question(s)

Lesson/Topic #1: Uncollectible Accounts Receivable

Students will record accounting activities related to

uncollectible accounts receivable; including writing off an

account and reopening an account.

Essential Question(s): • What has to be done in order to

record uncollectible accounts expense at the end of the year?

• How is a customer's account affected when it is

written-off/re-opened?

Lesson/Topic #2: Plant Assets and Depreciation

Students will perform accounting functions related to plant

assets and depreciation.

Essential Question(s): • How does a corporation record

buying plant assets and paying property tax?

• How is a plant asset affected by straight-line depreciation?

• How is the plant asset record affect by depreciation?

• How does a corporation record gains/losses of plant assets?

• How is a plant asset affected by double-declining method

of depreciation?

Lesson/Topic #3: Accounting for Inventory

Students will use the various methods to calculate and

compare the costs of inventory. Methods used will include

FIFO, LIFO, and Weighted Average.

Essential Question(s): • Explain the various methods used

to keep an accurate inventory.

• What are the different methods used by companies to

record and report their inventory costs?

• How are the different inventory costing methods

calculated?

Lesson/Topic #4: Notes and Interest

Students will perform accounting related activities for Notes

Essential Question(s): • How are interest and maturity

dates calculated for notes payables/notes receivables?

Page 7 of 21 Unit Map - Unit 1: Adjustments and Valuation

Lesson/Topic(s) Lesson/Topic Essential Question(s)

Receivables and Notes Payables. • How are transactions for notes payable recorded in the

journals?

• How are transactions for notes receivable recorded in the

journals?

Lesson/Topic #5: Accrued Revenue and Expenses

Students will record adjusting, closing, and reversing entries

for accrued revenue and expenses.

Essential Question(s): • How do companies record

adjusting, closing, and reversing entries for accrued

revenue?

• How do companies record adjusting, closing, and reversing

entries for accrued expenses?

Lesson/Topic #6: End of Fiscal Period Work

Students will complete a Work Sheet, Income Statement,

Statement of Stockholders Equity, Balance Sheet, and

complete the Adjusting, Closing, and Reversing entries.

Essential Question(s): • How are adjustments planned on

the worksheet?

• What information is recorded on an Income Statement?

How is it prepared?

• How is the Statement of Stockholder's Equity prepared?

• How is the Balance Sheet prepared? What information is

recorded on it?

• How do companies record adjusting, closing, and reversing

entries at the end-of-fiscal period?

Page 8 of 21 Unit Map - Unit 1: Adjustments and Valuation

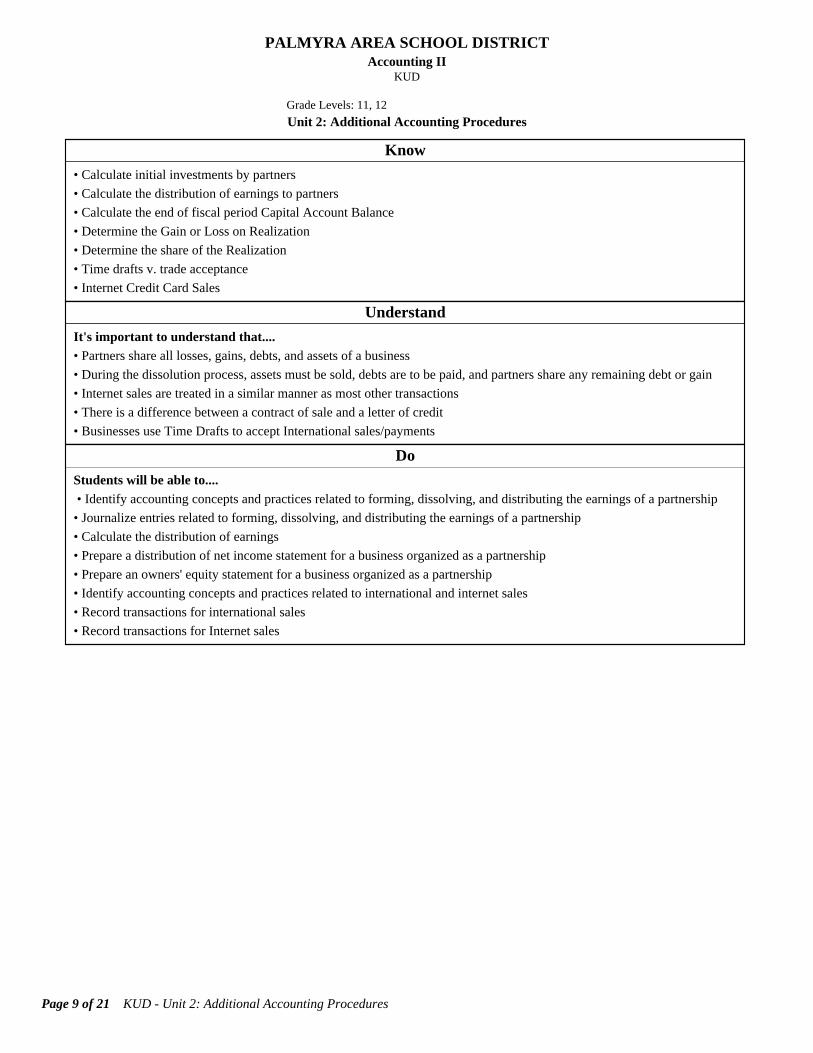

PALMYRA AREA SCHOOL DISTRICTAccounting II

KUD

Grade Levels: 11, 12

Unit 2: Additional Accounting Procedures

Know

• Calculate initial investments by partners

• Calculate the distribution of earnings to partners

• Calculate the end of fiscal period Capital Account Balance

• Determine the Gain or Loss on Realization

• Determine the share of the Realization

• Time drafts v. trade acceptance

• Internet Credit Card Sales

Understand

It's important to understand that.... • Partners share all losses, gains, debts, and assets of a business

• During the dissolution process, assets must be sold, debts are to be paid, and partners share any remaining debt or gain

• Internet sales are treated in a similar manner as most other transactions

• There is a difference between a contract of sale and a letter of credit

• Businesses use Time Drafts to accept International sales/payments

Do

Students will be able to.... • Identify accounting concepts and practices related to forming, dissolving, and distributing the earnings of a partnership

• Journalize entries related to forming, dissolving, and distributing the earnings of a partnership

• Calculate the distribution of earnings

• Prepare a distribution of net income statement for a business organized as a partnership

• Prepare an owners' equity statement for a business organized as a partnership

• Identify accounting concepts and practices related to international and internet sales

• Record transactions for international sales

• Record transactions for Internet sales

Page 9 of 21 KUD - Unit 2: Additional Accounting Procedures

PALMYRA AREA SCHOOL DISTRICTAccounting II

Unit Map

Grade Levels: 11, 12

Unit 2: Additional Accounting Procedures

Day(s): 7

Unit Essential Question(s)

What accounting procedures are used in partnerships, international, and Internet sales?

Materials/Resources

Century 21 Accounting, Multicolumn Journal, 9th Edition Textbook and Workbook

Whiteboard

Overhead Transparencies (as needed)

Document Camera

PowerPoint Presentations

Projector

Ruler

Calculator

Chapter Handouts

Excel/Laptop

Moodle

Vocabulary

Partnership, Partner, Partnership agreement, Distribution of Net Income Statement, Owners' Equity Statement, Liquidation of a partnership, Realization,Limited Liability Partnerships

Exports, Imports, Contact of sales, Letter of Credit, Bill of Lading, Commercial invoice, Draft, Sight draft, Time draft, Trade acceptance

Unit Assessment(s)

Unit Exam

Launch Activities

Have students pair with a partner and look through the chapters in the new unit and make a chart listing the following: Familiar Concepts v. NewConcepts

Discuss the various student created lists.

Standards

15.1.12.D - Analyze, journalize, and post transactions to general & subsidiary ledgers.

15.1.12.E - Perform accounting functions using technology as a tool.

15.1.12.K - Describe, calculate, and journalize the sales and cost of sales including purchases, transportation costs, sales taxes, and trade discounts.

15.1.12.N - Explain how the different forms of business ownership and business operations are reported on financial statements.

Lesson/Topic(s) Lesson/Topic Essential Question(s)

Lesson/Topic #1: Accounting for Partnerships

Students will perform accounting activities for the

formation, dissolution, and distribution of partnership

earnings as well as create financial statements for a

Essential Question(s): • How are forming, dissolving, and

distributing the earnings of a partnership recorded in the

journals?

• How is the distribution of partnership earnings calculated?

Page 10 of 21 Unit Map - Unit 2: Additional Accounting Procedures

Lesson/Topic(s) Lesson/Topic Essential Question(s)

partnership. • How are the financial statements for a business organized

as a partnership prepared?

Lesson/Topic #2: International and Internet Sales

Students will record international and internet sales.

Essential Question(s): • How does a company record

transactions for international sales?

• How are Internet Sales recorded by businesses?

Page 11 of 21 Unit Map - Unit 2: Additional Accounting Procedures

PALMYRA AREA SCHOOL DISTRICTAccounting II

KUD

Grade Levels: 11, 12

Unit 3: Departmental Accounting

Know

•Accounting Equation

•Normal Balances of Accounts

•Posting to General and Subsidiary Ledgers

•Journalizing to Special Journals (Sales Journal, Purchases Journal, General Journal, Cash Receipts Journal, Cash Payments

Journal)

•Calculate Sales Tax

•Calculate Sales Discounts

•Calculate Taxes and Deductions associated with Payroll

•Calculate Commission

•Calculate Component Percentages

•The relationship of accounts on financial statements (Worksheet, Interim Departmental Statement of Gross Profit,

Departmental Margin Statements, Income Statement, Statement of Stockholders' Equity, Balance Sheet)

•Accounting Cycle

Understand

It's important to understand that....

•Transactions are journalized in various Special Journals

•Businesses and customers will take advantage of discounts in order to save money

•Businesses and customers return merchandise when it is damaged

•Businesses with departments must separate departmental functions from company functions

•Not all employees are paid just a salary: commission + salary

•Benefits and taxes affect employee pay

•Employees and Employers pay taxes; employers have additional taxes to pay

Page 12 of 21 KUD - Unit 3: Departmental Accounting

Understand

•Businesses with various departments have to prepare additional financial statements for each different department

•There are different type of expenses: direct and indirect and they have different affects on the various departments in a

business

Do

Students will be able to....

•Journalize and post departmental: purchases and purchases returns/allowances, cash payments, sales on account and sales

returns/allowances, cash receipts

•Prepare a commission record and calculate commission on net sales

•Complete payroll records (Payroll Register, Employee Earnings Records)

•Journalize payroll transactions

•Distinguish between direct and indirect expenses

•Prepare an interim departmental statement of gross profit

•Prepare a work sheet for a departmentalized merchandising business

•Prepare financial statements for a departmentalized merchandising business

•Analyze financial statements using selected component percentages

•Complete end-of-period work for a departmentalized merchandising business

Page 13 of 21 KUD - Unit 3: Departmental Accounting

PALMYRA AREA SCHOOL DISTRICTAccounting II

Unit Map

Grade Levels: 11, 12

Unit 3: Departmental Accounting

Day(s):

Unit Essential Question(s)

What are the various differences of a departmental accounting system to that of a regular accounting system?

Materials/Resources

Century 21 Accounting, Multicolumn Journal, 9th Edition Textbook and Workbook

Whiteboard

Overhead Transparencies (as needed)

Document Camera

PowerPoint Presentations

Projector

Ruler

Calculator

Chapter Handouts

Excel/Laptop

Moodle

Vocabulary

Asset, Liability, Equities, Owners' equity, Stockholders' equity, Accounting equation, Source documents, Double-entry accounting, Journal, Specialjournal, Account, Ledger, General ledger, Subsidiary ledger, Controlling account, File maintenance, Departmental accounting system, Merchandisingbusiness, Posting, Debit memorandum, Contra account, Cash discount, Purchases discount, Petty cash

Credit memorandum, Sales discount, Point-of-sale terminal, Terminal summary

Salary, Pay period, Payroll, Payroll taxes, Withholding allowance, Tax base, Payroll register, Employee earnings record, Automatic check deposit,Electronic funds transfer

Fiscal period, Responsibility accounting, Direct expense, Indirect expense, Departmental margin, Departmental margin statement, Gross profit,Departmental statement of gross profit, Periodic inventory, Perpetual inventory, Gross profit method of estimating an inventory, Component percentage,Schedule of accounts receivable, Schedule of accounts payable, Work sheet, Trial balance, Plant assets, Depreciation expense, Responsibilitystatements, Income statement, Statement of stockholders' equity, Capital stock, Retained earnings, Dividends, Balance sheet, Adjusting entries, Closingentries, Post-closing trial balance, Accounting cycle

Unit Assessment(s)

Unit Exam

Launch Activities

Have students compare the Chart of Accounts to see the similarities/differences. Discuss.

Standards

15.1.12.D - Analyze, journalize, and post transactions to general & subsidiary ledgers.

15.1.12.E - Perform accounting functions using technology as a tool.

15.1.12.F - Analyze and journalize transactions for short- and long-term assets.

15.1.12.G - Analyze and journalize transactions involving short- and long-term liabilities.

15.1.12.K - Describe, calculate, and journalize the sales and cost of sales including purchases, transportation costs, sales taxes, and trade discounts.

Page 14 of 21 Unit Map - Unit 3: Departmental Accounting

15.1.12.L - Describe and explain the criteria used to determine expenses and journalize the expense transactions.

15.1.12.M - Analyze and calculate gross pay and net pay, including regular and overtime wages, commission, and piece rate.

15.1.12.P - Analyze and perform the reconciliation of accounts.

15.1.12.Q - Prepare financial statements (including a Balance Sheet, Profit & Loss and Owner's Equity) and understand their relevance.

15.1.12.R - Explain the primary areas of analysis (trend analysis, profitability, liquidity, capital structure) and the information that can be obtained fromeach.

15.1.12.S - Analyze and perform a horizontal and vertical analysis of the income statement and balance sheet.

15.1.12.T - Assess profitability, liquidity, and solvency by calculating and interpreting financial ratios.

15.1.12.U - Assess capital structure by calculating and interpreting financial ratios.

15.1.12.V - Analyze and explain the use of industry averages in assessing the financial condition, operating results, profitability, liquidity, and capitalstructure.

15.1.12.Y - Determine and calculate taxable income and tax liability for both personal and business taxes.

Lesson/Topic(s) Lesson/Topic Essential Question(s)

Lesson/Topic #1: Departmental Purchases and Cash

Payments

Students will record departmentalized transactions in the

purchases, cash payments, and general journals and then

post to the appropriate ledgers.

Essential Question(s): •Explain the importance of file maintenance.

•Identify and explain how to journalize and post purchases

and purchases returns.

•Identify and explain how to journalize and post payments

of cash.

Lesson/Topic #2: Departmental Sales and Cash Receipts

Students will record departmentalized transactions in the

sales, cash receipts, and general journals and then post to the

appropriate ledgers.

Essential Question(s): •Identify and explain how to journalize and post

departmental sales on account and sales returns and

allowances.

•Identify and explain how to journalize and post cash

receipts.

Lesson/Topic #3: Departmental Payroll

Students will calculate and record departmental payroll data

for both the employee and employer.

Essential Question(s): •How are payroll records and deductions recorded and

calculated for a departmental business?

•What journal entries are made in order to record payroll

and payroll taxes?

Lesson/Topic #4: Departmental Financial Reporting

Students will complete financial statements for the

departmental business.

Essential Question(s): •What features are required if responsibility accounting is to

be successful?

•What are the two principal methods for determining

amounts of merchandise on hand?

•What purpose do adjusting entries serve?

Page 15 of 21 Unit Map - Unit 3: Departmental Accounting

Lesson/Topic(s) Lesson/Topic Essential Question(s)

•What two reports are prepared to prove the accuracy of

posting to subsidiary ledgers?

•What conclusions can be obtained from an Income

Statement?

•What function do Adjusting and Closing entries serve?

How are they prepared?

Page 16 of 21 Unit Map - Unit 3: Departmental Accounting

PALMYRA AREA SCHOOL DISTRICTAccounting II

KUD

Grade Levels: 11, 12

Unit 4: Business Operating Activities

Know

•The basic functions of business (marketing, human resources, production and operations, finance, accounting and

information systems)

•The evolution of accounting in business

•The basic accounting concepts (business entity, monetary unit, going concern, periodicity)

•The elements of accounting

•The differences between GAAP and IFRS

•The information that belongs to each financial statement

•How to calculate the various financial ratios

•The four basic business processes (business organization and strategy process, operating process, capital resources process,

performance measurement and management process)

•The perspectives of the balance scorecard

•Various types of internal control (proper authorization, separating incompatible duties, maintaining adequate

documentation, physically controlling assets and documents, providing independent checks on performance)

•The elements of a bank reconciliation

•The goals of the revenue process and the expenditure process

•The differences between FOB destination and FOB shipping point

Understand

•Accounting exists only because it is needed by businesses

•Accounting terms and concepts evolve over time as the needs of users change

•The relationship, organization, and importance of financial statements.

•The relationship between the four financial statements

•The need/interpretation of financial ratios

Page 17 of 21 KUD - Unit 4: Business Operating Activities

Understand

•The basic business process and the importance of financial and non-financial performance measurement

•The importance of internal control and of a bank reconciliation

•The decisions to be made during the operating processes and the sources of information to be used to make these decisions

•The cost/revenue behavior and the two cost estimation methods

Do

•Explain the basic functions of business and identify how each function uses accounting

•Explain and identify the basic elements of accounting (assets, liabilities, owners' equity, revenues, expenses)

•Calculate the following ratios: current ratio, debt to equity ratio, return on sales ratio

•Explain the similarities and differences between GAAP and IFRS

•Calculate a bank reconciliation

•Determine the functions of each of the business processes

•Explain/Identify the perspectives of the balanced scorecard

•Provide examples for each type of internal control

•Differentiate between FOB shipping point and FOB destination and the affects on income

•Calculate Fixed, Mixed, and Variable Costs/Revenue

•Use the high/low method to separate a mixed cost/revenue into its fixed and variable components

Page 18 of 21 KUD - Unit 4: Business Operating Activities

PALMYRA AREA SCHOOL DISTRICTAccounting II

Unit Map

Grade Levels: 11, 12

Unit 4: Business Operating Activities

Day(s):

Unit Essential Question(s)

How is accounting used by businesses and individuals?

Materials/Resources

Whiteboard

Document Camera

PowerPoint Presentations

Projector

Ruler

Calculator

Chapter Handouts

Laptop/Excel/Word

Moodle

Vocabulary

Assets, Balance sheet, Business, Business entity concept, cash basis accounting, corporation, current asset, current liability, current ratio, debt-to-equityratio, double taxation, expense, finance function, Financial Accounting Standards Board, financial statements, generally accepted accounting principles,going concern concept, human resources function, income statement, international financial reporting standards, just-in-time, liability, limited liability,limited liability company, limited liability partnership, limited partnership, long-term asset, long-term liability, manufacturing firm, marketing function,merchandising company, monetary unit concept, mutual agency, net assets, net income, noncurrent asset, noncurrent liability, owners' equity,partnership, partnership agreement, periodicity concept, product life cycle, production and operations function, return on sales ratio, revenue, Scorporation, service firm, sole proprietorship, stakeholders, statement of cash flows, statement of owners' equity, unlimited liability, XBRL (eXtensiblebusiness reporting language)

appraisal cost, accounts payable turnover, accounts receivable turnover, balanced scorecard approach, bank reconciliation, bank statements, businessprocess, customer response time, deposits in transit, efficiency strategy, external failure cost, financing processes/activities, flexibility strategy, grossmargin ratio, internal control systems, internal failure cost, inventory turnover, investing processes/activities, lockbox system, mechanisticorganizational structure, nonsufficient funds check, nonvalue-added time, operating processes/activities, organic oranizational structure, organizationalstrategy, outstanding checks, prevention cost, quick ratio, return on investment ratio, return on owners' equtiy ratio, service charge, value-added time

activity drivers, bill of lading, conversion process, cost behavior, dependent variable, expenditure process, fixed cost, fixed revenue, FOB destination,FOB shipping point, independent variable, manufacturing overhead, mixed cost, mixed revenue, purchase allowances, purchase discounts, purchaseorder, purchase requisition, purchase return, relevant range, revenue behavior, revenue process, sales allowances, sales discounts, sales invoice salesreturns, variable cost, variable revenue, X variable, Y Variable

Unit Assessment(s)

Launch Activities

Standards

15.1.12.A - Summarize professional designations, careers, and organizations within the field of accounting, including education and certification

Page 19 of 21 Unit Map - Unit 4: Business Operating Activities

requirements.

15.1.12.E - Perform accounting functions using technology as a tool.

15.1.12.O - Compare and contrast the accrual basis and the cash basis of accounting; assess the impact of each on the financial statements.

15.1.12.P - Analyze and perform the reconciliation of accounts.

15.1.12.R - Explain the primary areas of analysis (trend analysis, profitability, liquidity, capital structure) and the information that can be obtained fromeach.

15.1.12.T - Assess profitability, liquidity, and solvency by calculating and interpreting financial ratios.

15.1.12.T - Assess profitability, liquidity, and solvency by calculating and interpreting financial ratios.

15.1.12.U - Assess capital structure by calculating and interpreting financial ratios.

15.1.12.U - Assess capital structure by calculating and interpreting financial ratios.

15.1.12.V - Analyze and explain the use of industry averages in assessing the financial condition, operating results, profitability, liquidity, and capitalstructure.

15.1.12.V - Analyze and explain the use of industry averages in assessing the financial condition, operating results, profitability, liquidity, and capitalstructure.

15.1.12.X - Analyze and perform breakeven and cost benefit analyses to support financial decisions.

ACC.VI.I - Use planning and control principles to evaluate the performance of an organization and apply differential analysis and present-valueconcepts to make decision.

Lesson/Topic(s) Lesson/Topic Essential Question(s)

Lesson/Topic #1: Accounting and Business

Students will be introduced to the history of business and

accounting. They will learn about the basic concepts in

accounting, various types of businesses and business

organizations, and will learn to identify between the four

financial statements and the report of the independent

accountant.

Essential Question(s): •How did business and accounting develop?

•What are the elements of accounting?

•Explain the differences between the basic types of

businesses and business organization structures.

•Identify the purpose and relationship among the four

financial statements and the report of the independent

accountant.

Lesson/Topic #2: Business Processes and Accounting

Information

This chapter explores the business processes and the role of

internal control. The four basic business processes will be

studied, focusing on the business organization and strategy

process and the performance measurement and management

process. In addition, we will apply internal control

principles to cash receipts and cash payments.

Essential Question(s): •What are the four basic business processes and the

management cycle?

•What is the balanced scorecard approach and what are its

four perspectives?

•What are internal controls and why are they important?

Lesson/Topic #3: Operating Processes: Planning and

Control

The activities involved in each of the three sub-processes

will be examined (1) marketing/sales/collection/customer

service [revenue], (2) conversion, and (3) purchasing/human

resources/payment [expenditure]. The relationship between

activities and costs/revenues and defines this relationship as

fixed, variable, or mixed will also be introduced/discussed.

Essential Question(s): •Explain the activities in three different operating

subprocesses.

•Explain the differences between fixed, mixed, and variable

costs and revenues.

•How is the linear regression method used to determine

Page 20 of 21 Unit Map - Unit 4: Business Operating Activities

Lesson/Topic(s) Lesson/Topic Essential Question(s)

Finally, methods that companies use to separate mixed

costs/revenues into their fixed and variable components will

be covered.

fixed and variable costs and revenues?

•How is the high/low method used to determine fixed and

variable costs and revenues?

Page 21 of 21 Unit Map - Unit 4: Business Operating Activities