overview of malaysian taxation by: associate professor dr. gholamreza zandi [email protected]

TRANSCRIPT

Masters of Financial PlanningTaxation Planning

Overview of Malaysian Taxation

By: Associate Professor Dr. GholamReza Zandi

Main Objectives of Taxation

• Taxes are used to fund government development and social

expenditure.

• Taxes are to be collected efficiently and at minimum cost to

government and to taxpayers.

• Taxes can be used as a fiscal tool to maintain the desired level of

employment and increase economic development and growth.

• Taxes are used as policy measures to encourage activities

beneficial to the country and to discourage those which are not

(for example smoking and consuming alcohol)2

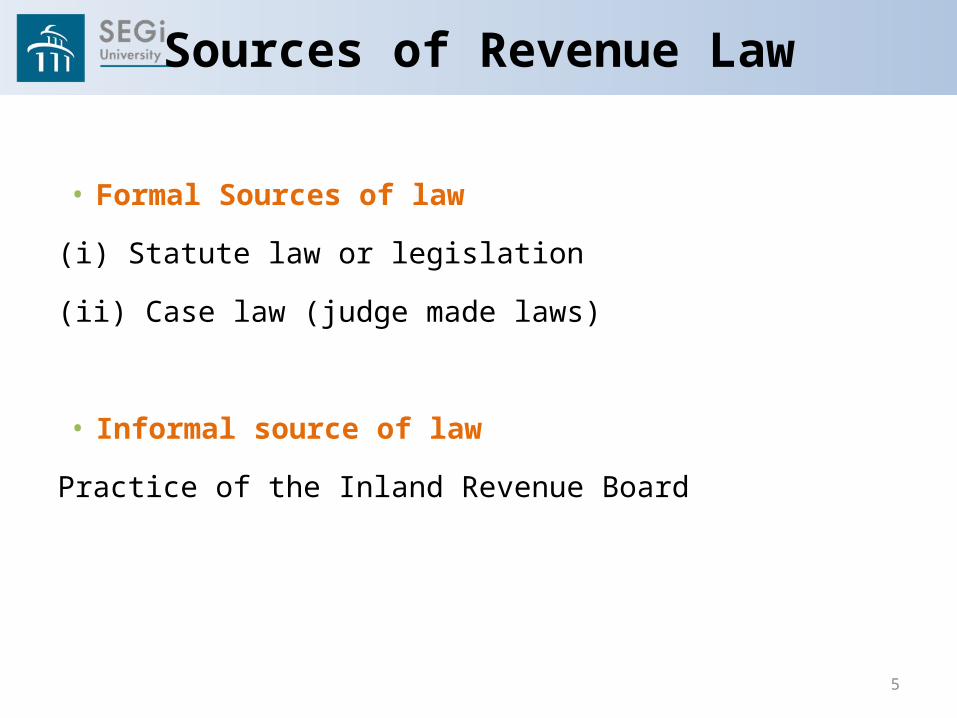

Sources of Revenue Law

• Formal Sources of law

(i) Statute law or legislation

(ii) Case law (judge made laws)

• Informal source of law

Practice of the Inland Revenue Board

5

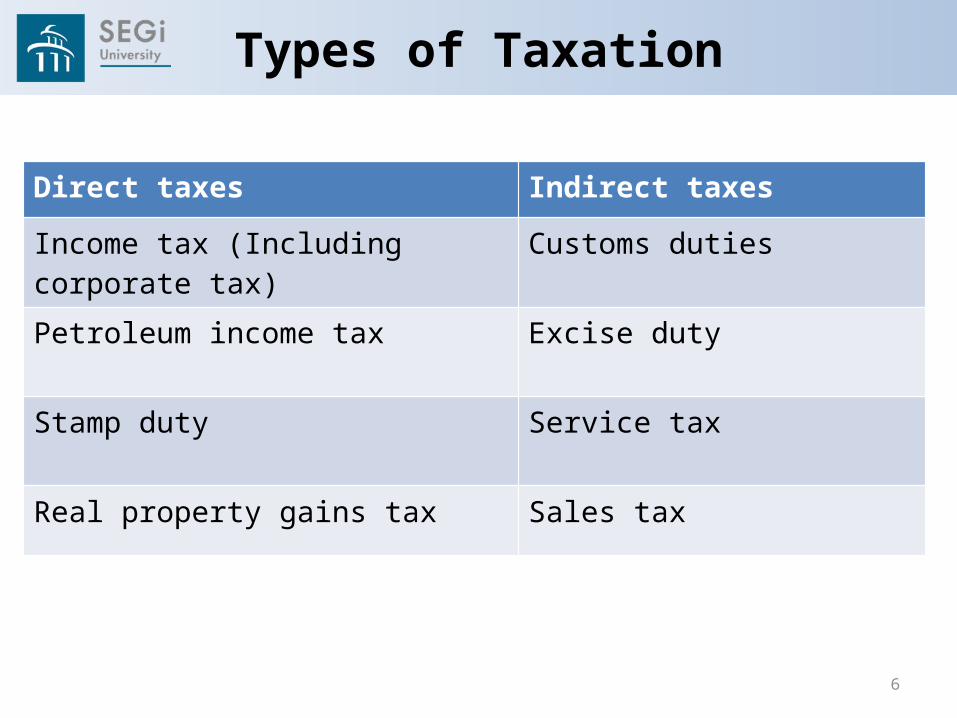

Types of Taxation

6

Direct taxes Indirect taxes

Income tax (Including corporate tax) Customs duties

Petroleum income tax Excise duty

Stamp duty Service tax

Real property gains tax Sales tax

Self Assessment System

• Self-assessment system (SAS) was implemented on

companies from year of assessment 2001 and on individuals

and other taxpayers from the YA 2004.

• Under the SAS, taxpayers determine their taxable income,

compute tax liability and submit tax returns.

7

Self Assessment System (cont’d)

Companies under the SAS

• Provide estimate of the tax payable one month prior to the

commencement of the business

• Estimates shall not be less than 85% of its previous year’s

estimate

• May revise estimates in the sixth and ninth month of the

relevant basis period

• File tax return within seven months of the close of the

financial year end

8

Tax Rates

•Resident individual taxpayers

Graduated scale of rates from 0% (on the first RM2,500) to a

maximum of 26% (for income exceeding RM100,000)

•Non-resident individual taxpayer

Flat rate of 26% with no personal reliefs

9

Tax Rates (cont’d)

• Companies

Paid-up capital ≤ RM2.5 million

- 20% on the 1st RM500,000 chargeable income

- 25% on the subsequent chargeable income exceeding

RM500,000

Paid-up capital > RM2.5m

- Fixed rate of 25%

10

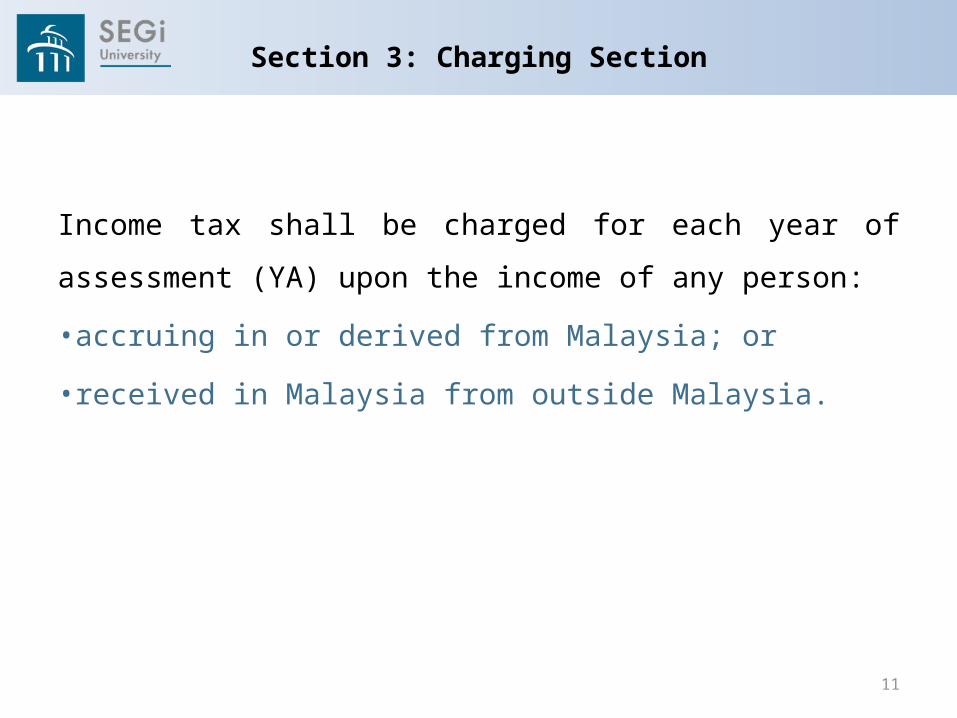

Section 3: Charging Section

Income tax shall be charged for each year of assessment (YA)

upon the income of any person:

•accruing in or derived from Malaysia; or

•received in Malaysia from outside Malaysia.

11

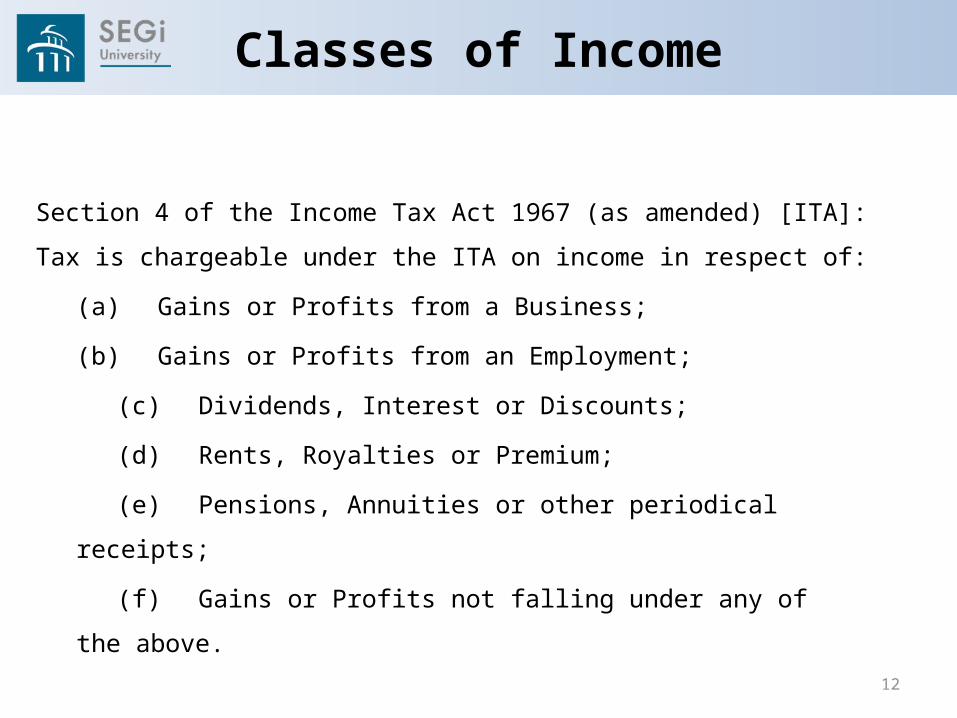

Classes of Income

Section 4 of the Income Tax Act 1967 (as amended) [ITA]: Tax is chargeable

under the ITA on income in respect of:

(a) Gains or Profits from a Business;

(b) Gains or Profits from an Employment;

(c) Dividends, Interest or Discounts;

(d) Rents, Royalties or Premium;

(e) Pensions, Annuities or other periodical

receipts;

(f) Gains or Profits not falling under any of

the above. 12

According to sec 5 ITA, ‘chargeable income’ of a person is

ascertained in 6 stages:

(i) Determine Basis Period

(ii) Compute Gross Income from each source

(ii) Compute Adjusted Income

(iv) Statutory Income

(v) Aggregate Income

(vi) Chargeable Income

13

Determination of Chargeable Income

Hierarchy of Malaysian Courts

• Federal Court

• Court of Appeal

• High Court

• Sessions Court

• Magistrates Court

14

Hierarchy of Income Tax Appeal Process

• The Director General of Inland Revenue

• Special Commissioners of Income Tax

• High Court

• Federal Court

15

The End