employment income by: associate professor dr. gholamreza zandi [email protected]

TRANSCRIPT

Masters of Financial PlanningTaxation Planning

EMPLOYMENT INCOME

By: Associate Professor Dr. GholamReza Zandi

Employment

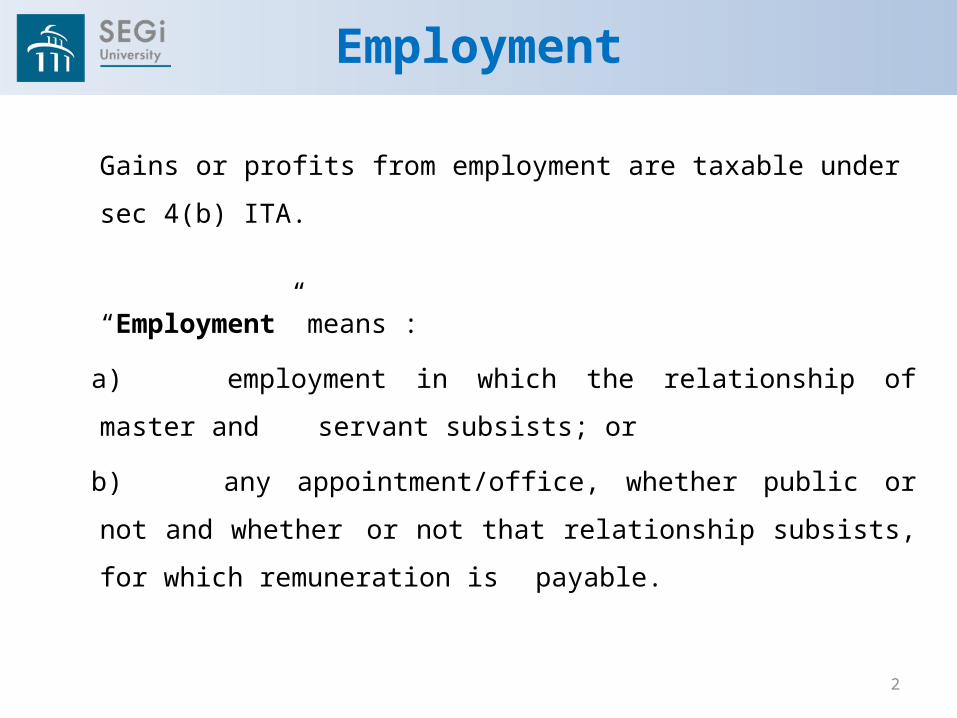

Gains or profits from employment are taxable under

sec 4(b) ITA.

“Employment” means :

a) employment in which the relationship of master and

servant subsists; or

b) any appointment/office, whether public or not and

whether or not that relationship subsists, for which

remuneration is payable.

2

Employment (cont’d)

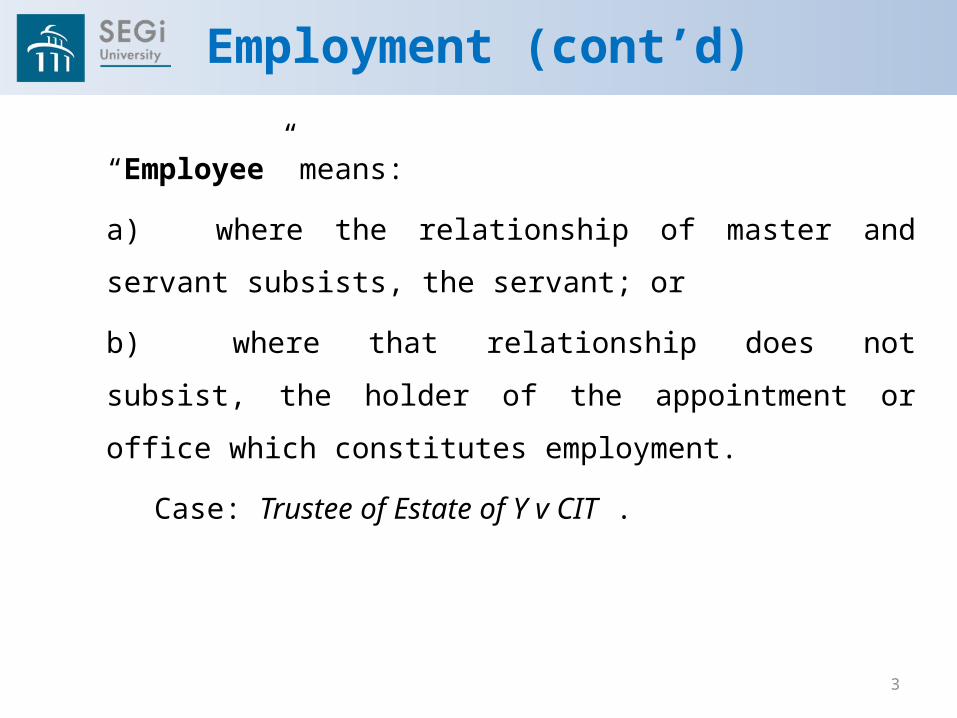

“Employee” means:

a) where the relationship of master and servant subsists,

the servant; or

b) where that relationship does not subsist, the holder of

the appointment or office which constitutes employment.

Case: Trustee of Estate of Y v CIT .

3

Sec 13(1)(a)

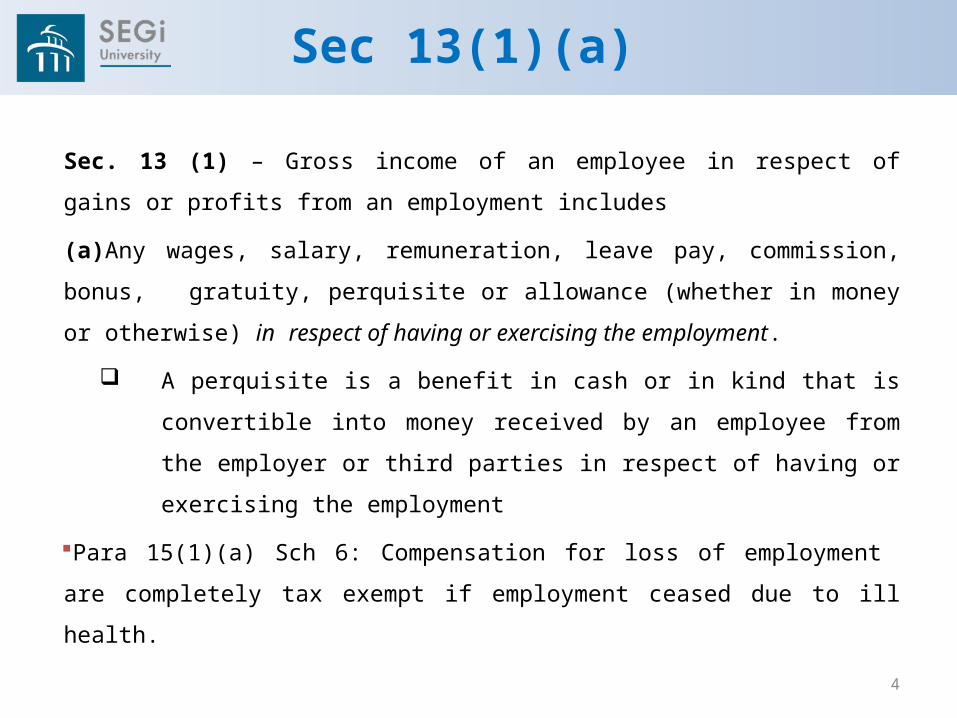

Sec. 13 (1) – Gross income of an employee in respect of gains or profits

from an employment includes

(a) Any wages, salary, remuneration, leave pay, commission,

bonus, gratuity, perquisite or allowance (whether in money or

otherwise) in respect of having or exercising the employment.

A perquisite is a benefit in cash or in kind that is convertible

into money received by an employee from the employer or

third parties in respect of having or exercising the employment

Para 15(1)(a) Sch 6: Compensation for loss of employment are

completely tax exempt if employment ceased due to ill health.

4

Sec 13(1)(a) (cont’d)

Para 15(1)(b) Sch 6: If payment is for loss of employment or for

entering into a restrictive covenant, then a sum of RM10,000

multiplied by the employee’s number of years of service with that

employer is tax exempt.

Gratuity is a gift of money in addition to salary to a retiring/ resigning

employee for services rendered. Taxable.

The manner in which it is paid does not alter the nature of the

gratuity

5

Sec 13(1)(a) (cont’d)

Case law: DGIR v Leong Ngoh Sang

A ‘ retirement gratuity ’ is exempt from tax under Sch 6 provided it is

due to ill health [Para 25(1)(a)] or he is 50 years and above and has

been employed by the same employer for at least 10 years [Para 25(1)

(b)].

6

Sec 13(1)(b)

a. Sec 13(1)(b) – Employment income includes the value of the

use or enjoyment by the employee of any benefit or amenity

provided for the employee by or on behalf of the employer.

b. Note: Income taxed under Sec. 13(1)(b) include:

Car benefit (private use)

Fuel

Furnishing

Driver/ Gardener/Maid

Utilities/Bills

7

Benefit in Kind

• A benefit in kind is a benefit provided for the employee by or on

behalf of the employer which is not convertible into money.

• Benefit in kind (BIK) is valued in one of the 3 following ways:

Where scale rates are provided by the IRB in the IRB Guidelines for

valuation of benefits in kind provided to employees.

Where special valuation rules are provided by the ITA’67

such as Sec. 32: Value is the cost to employer on just and

reasonable basis.

Where not covered by (i) or (ii), value on money’s worth basis if

convertible to money (i.e. its market value) or otherwise,

what it costs the employer to provide it to the employee. 8

Exempt Benefits

Exempt BIKs : Sec. 13(1)(b)

Medical, dental treatment and childcare benefits provided by

employer.

Medical benefits extended to include maternity and traditional

medicine.

Leave passage within Malaysia not exceeding 3 times per

annum or one overseas leave passage p.a. up to a maximum of

RM3,000 for employee and immediate family members.

Petrol/travel allowance for official duties up to RM6,000.

Allowance/subsidy for childcare up to RM2,400 p.a.

9

Sec 13(1)(c)

Accommodation [sec 13(1)(c)]

Sec. 13(1)(c ) – Employment income includes an amount in respect

of the use / enjoyment by the employee of living accommodation in

Malaysia provided for the employee by or on behalf of the employer

rent free or otherwise subsidized.

2 Categories

Sec. 32(3): Non Service Directors of a Controlled company.

Sec. 32(2): Other Employees.

Public Ruling No. 3/2005 explains the tax treatment of value of living

accommodation .

10

Sec 13(1)(c) (cont’d)

• Defined Value means (sec 18):

i. the rent on the unfurnished accommodation if it is rented leased from an independent lessor dealing at arm’s length (provided not under rent control); or

ii. in any other case, the annual value or in its absence the ‘economic rent’.

iii. Other Employees

Section 32(2): Assessable value of living accommodation provided for an employee is

(a) the defined value of the accommodation OR 30% of the gross employment income from the employment falling within sec 13(1)(a), whichever is LOWER; OR

11

Sections 13(1)(c), (d), (e)

(b) 3% of the gross employment income within Sec. 13(1)(a) if the

living accommodation is a hostel, hotel or any premises on a

plantation and forest.

• Section 13 (1)(d): Receipts from unapproved provident funds

• Section 13(1)(e): Compensation from loss of employment. But

exemptions are given for each completed year of service.

12

Deductions from Employment Income

Deduction of expenses from gross employment income is governed

by:

i. Section 33 [Deductions in general] ;

ii. Expenses only deductible if incurred in production of

employment income, i.e. must be ‘incurred in the performance of

employment duties’. Example: fees paid to professional bodies.

iii. Sec 38 – [Deductions against benefits in kind on furnishing and

living expenses]; and

iv. Sec 38 A – [Deduction for entertainment expense]

Deduction for entertainment expenses so long as they are taxed on

the entertainment allowance under sec 13(1)(a). 13

The End