okzim hy2011 interim results presentation

TRANSCRIPT

OK Zimbabwe Limited

PresentationTo

Analysts & Asset Managers

23 November 2011

Half Year Results to 30th September 2011

PRESENTATION FORMAT

Introduction Willard Zireva

Review of operating Environment Albert Katsande

Financials Alex Siyavora

Outlook Willard Zireva

Discussion All

Preamble

The company resultsfor the period ending30 September 2011 show good growth andperformance in the context of the prevailingoperating environment.

Between 60-65% of grocery products is imported mostly from South Africa with balance produced locally.In the other product categories the percentage of imports is higher.The foreign supply base remains a mix of direct sourcing and agencies/distributors. A significant increase has been achieved with direct sourcing at +/-60% of all imports Limitations still exist on importation of certain products & this affects supplies. Where licences are required the lead times are longer.Payment terms have improved towards 30 days with more foreign suppliers giving credit on longer terms. In addition to existing house brands, POG,OK Value & Premier Choice, we are introducing a group brand which will be sold through all our store formats. Direct sourcing mainly from Asia is being used to supply more competitively priced general merchandise particularly for OK Mart as well as some OK & Bon Marche’ stores.

Operating EnvironmentProduct Supply Situation

OK Zimbabwe Limited’s new private label

SHOPPERSCHOICE

3 SKU’s now in the stores

15 SKU’s now in the stores. Target is to cover most high volume lines

Low employment- A new middle class is emerging though still smallHigh level of dependency – compounded by HIV/AIDSCivil service average salaries and general market salaries have remained low affecting consumer spend (Govt still largest employer)Wage and salary expectations remain high with employers lacking capacity to meet them. These demands are a result of pressure from

-High levels of dependency-High cost of accommodation given shortages at the low end.-High cost of transport, electricity, water, rates & other services.-High cost of health services and medicines-High cost of education and related products-Diminished alternative sources of income- smaller

informal market -Diminished diaspora remittances post dollarisation.

Operating Environment

Disposable Income Challenges

Operating EnvironmentRisk & Security

Frauds, shoplifting and staff thefts continue to occur contributing to shrinkageacross the retail sector. This is driven by:

*The difficult economic environment*The high levels of unemployment*The culture of easy money and disrespect for ownership and others*General lawlessness and inadequate deterrent measures

For OK, effective use of CCTV at all stores and tighter controls which include monthly stock takes, engagement of external professional securityall combine to reduce and maintain the level of shrinkage to within acceptable levels.

The adoption of Enterprise Risk Management has ushered in a new dimensionto our risk management and risk mitigation across the company.

No Robberies have been experienced in our chains though a few break ins have occurred. Further physical store fortifications have been done with externally linked intruder alarm systems in place.

Operating EnvironmentPromotions

The environment remained very competitive with all major retailersvery active. Thus, to increase customer foot print, one had to have effective promotions and marketing activities.

OK Stores : OK Grand ChallengeWarm up this WinterSizzling Summer‘Bonus’ Basket Promotion

Bon Marche’ : Its Winter - Promotion Its Summer- PromotionGreen Power Walk (One Day event)Shape up for Summer (One Day event)

OK Mart : Multi Media Launch CampaignDirect Marketing & ExhibitionsGift Centre promotionOK Mart “Sportsline” - Radio program

Shop Easy : Shopping Voucher and Cash Card promotion

Operating Environment

Logistics & Central Distribution

The high level of imports have made our Central Warehousing and Distribution Centre a critical component of the Supply Chain into our store network.

To ensure we develop internal capacity for distribution, we have invested in additional distribution fleet for both dry goods and perishable products which includes 30 Tonne vehicles for the out of Harare Stores.

The opening of the new trading brand OK Mart ‘s two mega stores in Harare and Bulawayo gave us enhanced capacity in a different marketA number of Branches were refurbished during the period moving them into the new generation store category with world class ratings:

OK QueensdaleOK ChiredziOK Avonlea

A Bon Marche’ store with the new fresh image was opened at the Westgate shopping mall in August.Post September, we completed refurbishment of Bon Marche’ Mt Pleasant and partial refurbishment of Bon Marche’ Chisipite. Work to bring Bon Marche’ Borrowdale to the new image is almost completed.

Customer Response to the fresh new image stores has been tremendous across different markets.

Operating EnvironmentCapacity Development

OK OK KwekweKwekwe

OK Queensdale

OK CHIREDZI

OK Avonlea

OK AvonleaOK AvonleaBon Bon MarcheMarche WestgateWestgate

Bon Bon MarcheMarche BelgraviaBelgravia

Bon Marche- Chisipite

n n MarcheMarche ChisipiteChisipite

FINANCIAL HIGHLIGHTS

Revenue of $185.609 million compared to $115.061 million last year

Profit before tax $5.151 million from $0.615 million last year

EBITDA $7.279 compared to $2.293 in prior year

Attributable Profit of $3.863 million versus $0.322 million in prior year

Headline earnings per share of 0.38 US cents versus 0.04 US cents last

year

6 Months To 30 September 2011

$ millions 2011 2010 Variance %

RevenueNet salesCost of borrowingIncome before taxTaxation – currentTaxation - deferredIncome after tax

No of ordinary shares in issue (millions)

Attributable earnings basis US centsHead line earnings /share US cents Net asset value per share

185.609185.355

0.0025.151

(0.974)(0.314)

3.863

1 019.9660.380.384.02

115.061 114.956

0.1020.615

(0.093)(0.200)

0.322

970.7180.030.043.26

616198

738(947)

(57)1 099

Income Statement6 Months To 30 September 2011

2011 2010

Net sales ($ millions)

Gross margin %

Profit before tax %

Overheads %

Stock turn (times) historicDays stock against sales forecast

185.355

17.06

2.78

14.93

9.8836

114.956

16.04

0.53

15.96

11.0433

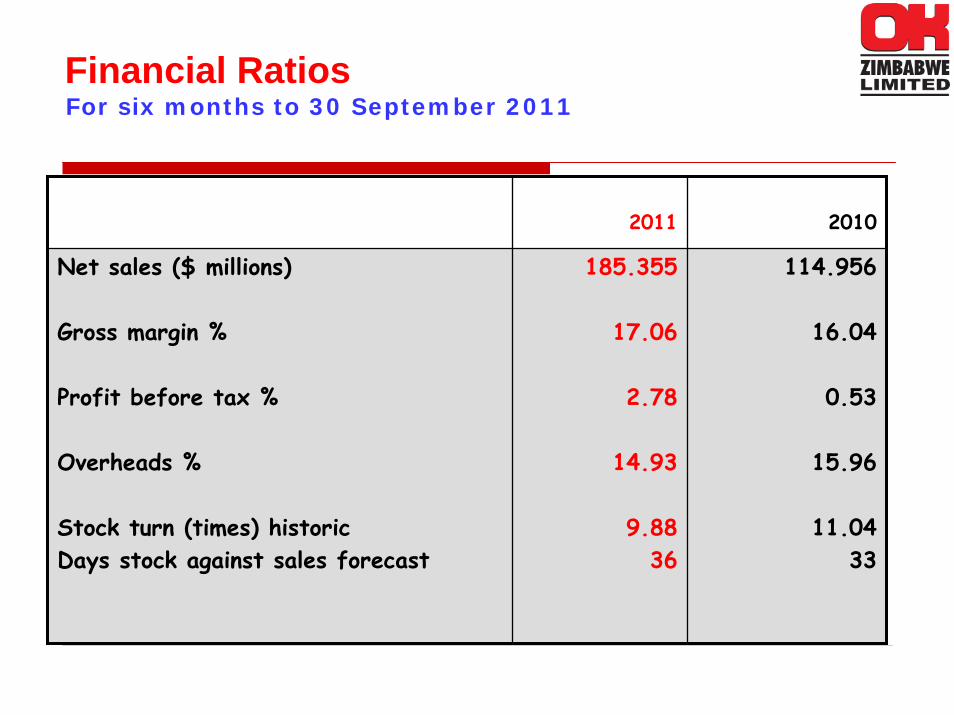

For six months to 30 September 2011Financial Ratios

Sales growth of 61% ahead of average internal inflation of 6.8%Increase in margin to 17.06% (2010 : 16.04%) due to better sourcing and improved mixOverheads up 50.84% :lower than sales growth(This is despite higher growth in Employee Benefits at 62%due to additional staff, Bon Marche Westgate & Refurbished Stores)Stock holding is balanced with forecast salesCapital expenditure $6.960 million (2010: $4.325 million)

REVIEW OF PERFORMANCE

Shrinkage% sales

Shrinkage$ million

6 months to 30 September 2011 0.70 0.957

6 months to 30 September 2010 1.48 1.391

12 months to 31 March 2011 1.00 2.160

Shrinkage Control

The macro environment is expected to remain stable.Inflation -.will remain low with the movement of the Rand being

the main factor. Liquidity - will remain tight, with low savings, exports and

foreign injection. May improve with diamond earnings.Exports - no major increases apart from mining Agricultural sector – no major improvement anticipated in the coming season

given limited facilities for farmers and no free inputs as well aslack of reliable power supply.

Donor support - Low - limited to humanitarian aid. Employment - No growth is anticipated given the low capacity

utilisation across the economy. Some retrenchments expected with company realignments. Mining resurgence may

seemore people employed

Price controls - No price controls are envisaged.Interest rates -With low liquidity expected to remain above regional

rates

Macro Environment

OUTLOOK

Will remain stable as long as there are no restrictions on imports

Strategic purchases will be used for both local & direct imports

with limited use of middleman :- efforts being directed more at

direct buys

Growth of own brand ranges using both local & foreign

manufacturers.

Continued efforts to push trade terms to above 30days

Improved margins through better sourcing

Product Supply

OUTLOOK

Unless there is an increase in employment and salary awards for both public & private sector employees, disposable incomes will remain constrained.

New generation stores, improved facilities and product offering will continue to draw more feet into our stores.

Price stability is expected to maintain with minor movements associated with firming or weakening of the Rand.

Availability of consumer credit through micro finance operations and banks will increase consumer spend particularly in the non-food areas, depending on the interest charged.

Consumer Spend

OUTLOOK

Major refurbishments planned for the remainder of the year- Avondale, Five Avenue, Marimba. Some may be moved to next financial year owing to delays in local authority approvals

Limited refurbishments planned for Machipisa & Mbare before March 2012.

Refurbishment programme to continue in next financial year

Continued focus on growing participation of high mark up product categories

across the three store brands- OK, Bon Marche’ & OK Mart.

Strategic Procurement to ensure consistent product supply including house brands

Competitive pricing strategy to be maintained

Total Quality Management & improved service delivery programs to continue

Organisational effectiveness initiatives and skills development on-going.

OUTLOOKTHE FUTURE

Timely re-alignment of the business model to better withstand Competition/grow customer support, allow growth, preserve capitaland grow shareholder Value!!!

WILL KEEP US AHEAD OF THE PECK

ProductBrandsQualityPackaging

PricePromotionDistributionKeeping pace with technology Customer focus StaffCorporate Social Responsibility