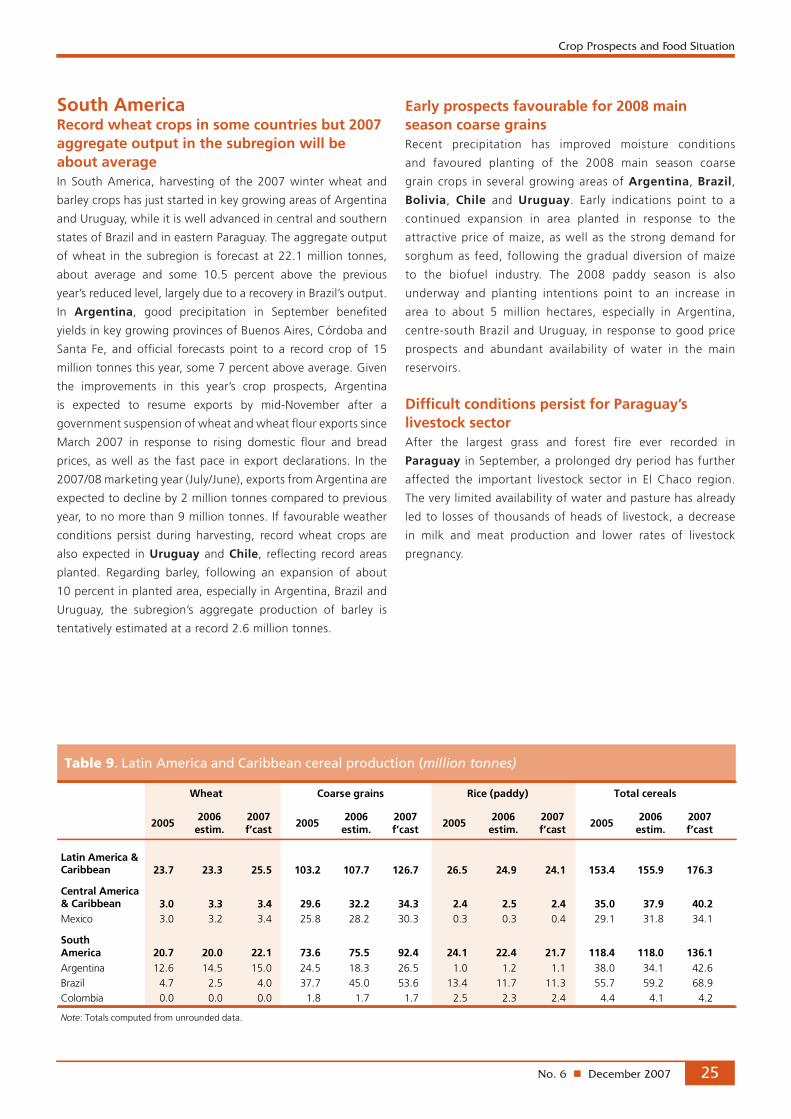

no. 6 december 2007 crop prospects and food situation

TRANSCRIPT

Crop Prospects and Food Situation

global information and early warning system on food and agricultureGIEWS

HIGHLIGHTS CONTENTS

No. 6 n December 2007

Countries in crisis requiring external assistance 2

Food emergencies update 3

Global cereal supply and demand brief 4

FAO global cereal supply and demand indicators 8

LIFDCs food situation overview11

Regional reviewsAfrica 13Asia 19LatinAmericaandtheCaribbean 24NorthAmerica,EuropeandOceania 26

Statistical appendix 29

nEarly prospects for the 2008 wheat crop are favourable.Withthewinterwheatplantingvirtuallycompleteinthenorthernhemisphere,latestestimatespointtoasignificantincreaseintheglobalwheatarea,inresponsetocurrenthighpricesandtheremovalofthecompulsorylandset-asidefor2008intheEU,theworld’slargestproducer.

nFAO’s latest forecast of the 2007 world cereal production has been revised downwards to 2 101 million tonnes,whichisstillrecordandsubstantiallyhigherthanlastyear.Mostoftheincreaseisincoarsegrains,especiallymaizeintheUnitedStates.

nIn the LIFDCs, as a group, 2008 cereal production is forecast to increase only marginally.However,ifthelargestcountries,ChinaandIndia,areexcluded,theaggregatecerealoutputoftheremainingcountriesisseentoregisterasignificantdecline.

nInternational cereal export prices remain high and volatile reflecting sustained demand,inparticularfromthefastgrowingbio-fuelsindustry,coupledwithhistoricallylowlevelsofstocksandinsufficientincreasesinthe2007production,mainlyforwheat,inexportercountries.

nIn spite of an anticipated reduction in quantities imported, the cereal food import bill of LIFDCs in 2007/08 is forecast to increase sharply for the second consecutive year.Risesininternationalpriceshavetranslatedintohigherretailpricesofbasicfoodinmanycountriesacrosstheworld.

nThe per caput food and feed consumption of cereals is forecast to decline in 2007/08 in LIFDCs.Mostaffectedbythereductionwillbelow-incomepopulationgroups.

nGood cereal harvests, although slightly lower than last year’s bumper crops, are being gathered in most of the Sahel and Eastern Africa, with the exceptions of Senegal, Cape Verde and Somalia.ElsewhereinWesternAfrica,productionisalsoanticipatedtodeclinesignificantlyinNigeria,whichcanaffectcerealpricesinthesubregion.

nIn Far East Asia, despite floods, landslides and cyclones during the growing season in several countries, a record 2007 cereal output has been obtained.InBangladesh,thelivelihoodofover8.5millionpeoplewasadverselyaffectedbydamagecausedbyCycloneSidrinmid-November.

50

100

150

200

250

300

350

400

NOSAJJMAMFJDNOSAJJMAMFJDN2005 20072006

Wheat

Rice

US$/tonne

Maize

Prices of cereals remain high and volatile

No. 6 n December 2007�

Crop Prospects and Food Situation

Countries in crisis requiring external assistance1 (37 countries)

Terminology1 Countries in crisis requiring external assistance are expected to lack

the resources to deal with reported critical problems of food insecurity. Food

crisesarenearlyalwaysdue toacombinationof factors,but for thepurposeof

responseplanning, it is important toestablishwhether thenatureof foodcrises

is predominantly related to lack of food availability, limited access to food, or

severebutlocalizedproblems.Accordingly,thelistofcountriesrequiringexternal

assistanceisorganizedintothreebroad,notmutuallyexclusive,categories:

•Countriesfacinganexceptional shortfall in aggregate food production/

suppliesasaresultofcropfailure,naturaldisasters,interruptionofimports,

disruption of distribution, excessive post-harvest losses, or other supply

bottlenecks.

•Countrieswithwidespread lack of access,whereamajorityofthepopulation

isconsideredtobeunabletoprocurefoodfromlocalmarkets,duetoverylow

incomes,exceptionallyhighfoodprices,ortheinabilitytocirculatewithinthe

country.

•Countrieswithsevere localized food insecurityduetotheinfluxofrefugees,

aconcentrationofinternallydisplacedpersons,orareaswithcombinationsof

cropfailureanddeeppoverty.� Countries facing unfavourable prospects for current crops are countries

whereprospectspointtoashortfall inproductionofcurrentcropsasaresultof

theareaplantedand/oradverseweatherconditions,plantpests,diseasesandother

calamities,whichindicateaneedforclosemonitoringofthecropfortheremainder

ofthegrowingseason.

Countries with unfavourable prospects for current crops2

AFRICA (�0 countries)

Exceptional shortfall in aggregate food production/supplies Lesotho Multipleyeardroughts,HIV/AIDSimpactSomalia Conflict,drought,highfoodpricesSwaziland Multipleyeardroughts,HIV/AIDSimpactZimbabwe Deepeningeconomiccrisis,drought

Widespread lack of accessEritrea IDPs,returnees,highfoodpricesEthiopia Lowincomes,highfoodprices,insecurityin

partsLiberia Post-conflictrecoveryperiod,IDPsMauritania Multipleyeardroughts,floodsinpartsSierraLeone Post-conflictrecoveryperiod,refugees

Severe localized food insecurityBurundi Civilstrife,IDPs,returneesandrecentdry

spellsCentralAfricanRepublic Civilstrife,IDPsChad Refugees,insecurityCongo,Dem.Rep.Civilstrife,IDPsandrefugeesCongo,Rep.of IDPs,refugeesCôted’Ivoire Civilstrife,IDPsGhana FloodsGuinea IDPs,refugeesGuinea-Bissau Localizedinsecurity,marketingproblemsSudan Civilstrife,returneesUganda Civilstrifeinthenorth,IDPs,floodsinparts

ASIA (9 countries)

Exceptional shortfall in aggregate food production/supplies Iraq Conflictandinsecurity,IDPs

Widespread lack of access Afghanistan Conflict,IDPsandreturnees,floodsKorea,DPR Economicconstraints,floodsTimor-Leste IDPs,drought/floods,marketaccess

Severe localized food insecurity Bangladesh FloodsandcycloneIndonesia EarthquakesNepal Marketaccessandeffectsofconflictand

floodsPakistan AftereffectsoftheKashmirearthquake,

floods,cycloneSriLanka AftereffectsoftheTsunami,deepeningcon-

flictsandfloods

AFRICASomalia Conflict,droughtinparts

LATIN AMERICA (6 countries)

Exceptional shortfall in aggregate food production/supplies Dominica HurricaneJamaica HurricaneSt.Lucia Hurricane

Severe localized food insecurity DominicanRep. FloodsHaiti FloodsNicaragua Floods

Europe (� countries)

Exceptional shortfall in aggregate food production/suppliesMoldova Droughtandlackofaccesstoinputsfor

wintercropping

Severe localized food insecurity

Russian Federation

(Chechnya) Civil conflict

No. 6 n December 2007 �

Crop Prospects and Food Situation

Emergency update

InWestern Africa,arelativelygoodcropisexpectedintheSahel (with the exception of Senegal and Cape Verde) butcropprospectsarelessfavourableinthecountriesalongtheGulf of Guinea, notably in northern Nigeria and northernGhana, which may have a significant impact on regionalcerealmarketsandpushupprices.Insomelocalizedareasofthesubregion,whereyieldswereseverelyreducedbydelayedrainsorfloods,populationsmaybeatriskoffoodshortages,andmayrequireassistance.InGhana,thehardesthitcountry,thefoodsecuritysituationofseveralnorthernareasaffectedbyfloodswasalreadyprecariousafterpoorrainfallandreducedharvestsduringthe2006croppingseason.Inthewesternpartof theSahel, lowdomesticproduction inacontextof tightinternationalmarketshasgeneratedhighinflationistpressureonthedomesticfoodmarket,erodingthepurchasingpowerof urban and rural consumers. This situation has alreadycausedsocialunrestinMauritaniaandSenegalwhichrelyheavilyoncerealimportsfromtheinternationalmarket.

InEastern Africa,followingtwoyearsofabove-averageharvestsinmanycountries,theoverallfoodsecuritysituationhasimprovedsomewhat.Thenumberofpeopleidentifiedinmid-2006ashighlyandextremelyfoodinsecureandneedinghumanitarianassistance,havedecreasedbysome7milliontoabout6millioncurrently,withthebiggestdeclinesinKenyaand Ethiopia. By contrast, in Somalia, after a temporaryreduction, a poor main season crop, renewed conflicts anddisplacements have again raised the affected populationfigure to some 1.5 million people. In Eritrea, cereal pricesremainhighaffecting the food securityof large sectionsofthepopulation.InEthiopia,despiteaneasingofrestrictionson trade in the Somali Region, households in vast areas oftheregionwillremainfoodinsecure.Inmostotherareastheanticipated good harvest is expected to improve the foodsupplyposition.However,thesecuritysituationofthepoorerhouseholdscontinuestobethreatenedbyhighfoodprices.In Kenya, for the first time in more than 45 years, severalsmallswarmsofadultDesertLocusthaveinvadedareasinthenortheastcausingdamagetocropsneartheDawaRiverontheEthiopianborder.Foodassistancecontinuestobeprovidedtoalargenumberofpeopleinthepastoralareasaffectedbyearlierdroughtandcontinuedpastoralconflicts.InSudan,asaresultofcontinuinginsecurity inDarfur,displacementandlossoflivelihoodsareexpectedtocontinueandmalnutritionratesarelikelytodeteriorateinthecomingmonthsbecauseoflackofproperaccesstofood.InsouthSudan,despiteanoverall adequate supplyof cereals, an inadequate transportandmarketingsystemwillpreventanysignificantmovementsfromsurplusestodeficitareas.InUganda,thepopulationatrisk, estimatedat some1.5million,will remainhighly foodinsecureandlargelydependantonhumanitariansupport.

In Southern Africa, owing to reduced harvests andsignificantincreasesincerealdomesticandimportprices,foodinsecurityhasworsened inseveralcountries. InZimbabwe,

with the latest inflation at a world record level of 7983percent,extremelyhighunemploymentandshortagesoffoodandnon-foodgoods,theeconomiccrisiscontinuestodeepen,affecting theestimated4.1million food insecurepeople. InLesotho andSwaziland,poorcerealharvests for the thirdyearinsuccessionduetodroughts,precludeanimprovementinthefoodsecurityofthesecountries,afflictedbyproblemsofpovertyandtheimpactofHIV/AIDS.

IntheGreat Lakesregion,thecontinuingconflictinthenorth-eastern parts of the Democratic Republic of the Congo, has affected large numbers of people who needfoodassistance.FoodaidisalsoneededinBurundifollowingthe poor 2007 total food crops harvest, combined withresettlementofreturneesandIDPs.

In Far East Asia, emergency food aid is needed inBangladeshafterasupercyclonicstorm(category4)inmid-November, caused extensive damage and affected close to8.5millionpeople in30districts.LocalizedfoodemergencyassistanceisalsoneededinViet Nam,Philippines,andNepalasaresultofthefloodsand landslides.Afterreceivingoverhalfamilliontonnesoffoodaid inthe lastseveralmonths,the food security situation in the Democratic People’s Republic of Korea has improved. However, a large gapbetweendomesticcerealsupplyandrequirementsisexpectedfor 2007/08 (November/October) as a result of long-termeconomicconstrainsandseverefloodsinJulyandSeptember.InMongolia,thefoodsecurityprospectsthiswinterfortherural populationshavebeennegatively affectedby reducedwheatandhayoutputin2007.InSri Lanka,thefoodsecuritysituationofvulnerablepopulationhasdeterioratedduetotheresurgenceofcivilconflict,thereductionofthisyear’scerealproductionandrisingcerealimportprices.ThefoodsecuritysituationinTimor-Lestehasrecentlydeterioratedduetohighcerealworldmarketprices,reducedcerealproductionduetoadverseweatherandanoutbreakoflocusts.

IntheNear East, inIraq,reflectingsomeslightimprovementinthesecuritysituation,afewhundredIraqirefugeesinSyrianArabRepublichaverecentlyjoinedthesteadymodestflowofrefugeeswhohavereturnedtotheirhomesinIraqinrecentmonths.Theexpatriateswhosoughtasyluminneighbouringcountriesareestimatedatabouttwomillionwhileasimilarnumberofpeoplehavebeeninternallydisplaced.

In Central America and the Caribbean, precipitationshave been well above normal levels during September andOctober.MajorfloodingandmudslidesoccurredinNicaragua,theDominican Republic,Haitiandthesouth-easternstatesofTabascoandChiapasinMexico,withlocalizedseverelossesofcashandfoodcropsaswellasdeathsofthousandsofheadof cattle. Food security situation appears to be particularlydifficultintheNorthernAutonomousAtlanticRegion(RAAN)of Nicaragua where the fragile livelihood systems of localpopulation have already been disrupted by the passage ofpowerfulhurricaneFelixinSeptember.

InSouth America,afterthemostseverefireofParaguay’shistory that destroyed in September almost one millionhectares of forest, pasture and cropland, a prolonged dryweatherperiodhasseriouslyaffectedtheimportantlivestocksectorofElChacoregion.

No. 6 n December 2007�

Crop Prospects and Food Situation

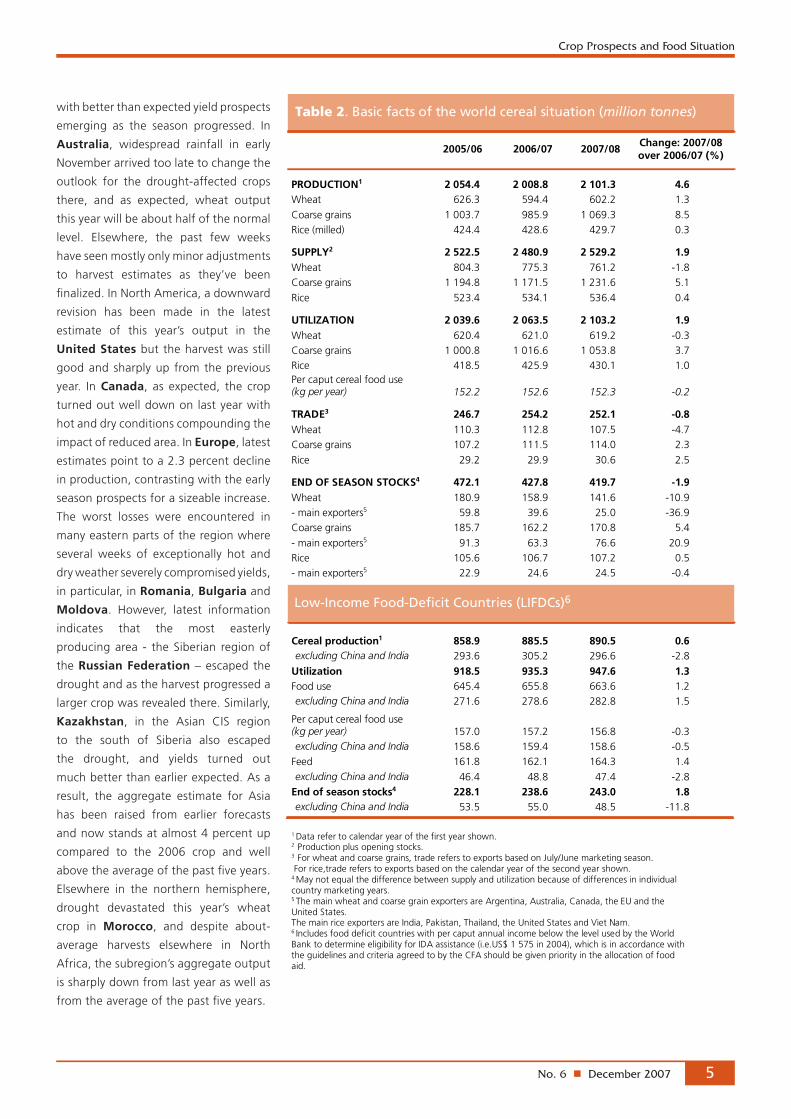

Global cereal supply and demand brief

Tight cereal supplies keep prices at high levelsFAO’s latest forecast for world cereal

production in 2007 has been revised

downwardfurtherinthepastfewweeks

and now stands at 2101 million tonnes

(including rice inmilled terms), although

still a record level and significantly (4.6

percent)upfromthepreviousyear.With

the last of the 2007 wheat harvests

underway in the southern hemisphere,

the estimate of world wheat production

fortheyearismorefirmnowandstands

at about1.3percent above theprevious

year’s about-average level. Prospects

at the start of the year had pointed to

a much larger harvest but as the year

progressedsomeoftheworld’smaincrops

were severely compromised by drought,

especially ineasternpartsofEuropeand

Australia.Whilecoarsegraincropsinthese

drought-affected areas have also turned

out less than early potential suggested,

generally good to bumper crops have

beenconfirmedelsewhere,particularlyfor

maize in the United States, contributing

to a better overall coarse grain harvest

at the world level than was expected

earlier in the year. Regarding rice, latest

indicationscontinuetopointtoanoutput

close to the previous year’s level. World

cerealutilizationin2007/08isforecastto

expandto2103milliontonnes,ornearly2

percentabovethepreviousseason.Based

onthelatestforecastsforworldproduction

and utilization, global cereal stocks by

the closeof the seasonsending in2008

areexpectedtofall toabout420million

tonnes,nearly2percentdownfromtheir

alreadyreducedopeninglevelandstillthe

lowest since1983.Worldcereal trade in

2007/08iscurrentlyforecastataround252

milliontonnes,about1percent,belowthe

volumein2006/07.However,atthislevel,

worldcereal trade in2007/08wouldstill

be the secondhighestafter last season’s

record. International prices for all major

cereals remain high and some registered

considerable gains from the previous

season.Tightsupplyamidstrongdemand

istheunderlyingfactorforthecontinuing

strength in prices of most cereals. This

is particularly the case for wheat, the

price ofwhich soared to recordhighs in

September and October and remained

highandvolatileinNovember.

The 2007 wheat seasons approach conclusion with an output close to last year’s about-average level FAO’s latest forecast puts aggregate

world wheat production in 2007 at

602 million tonnes, significantly below

expectations earlier in the season and

representing an increase of just over 1

percent from 2006. Harvesting of the

last of the 2007 wheat crops is well

underway in the southern hemisphere

withfewsurprises.SouthAmerica’smain

producers – Argentina and Brazil – are

reaping largercrops thanayearago:a

strongrecoveryinBrazil,afterareduced

crop in 2006, was already predicted

early in the season but the increase in

Argentina materialized more recently

No. 6 n December 2007 �

Crop Prospects and Food Situation

withbetterthanexpectedyieldprospects

emerging as the season progressed. In

Australia, widespread rainfall in early

Novemberarrivedtoolatetochangethe

outlook for the drought-affected crops

there, and as expected, wheat output

thisyearwillbeabouthalfofthenormal

level. Elsewhere, the past few weeks

haveseenmostlyonlyminoradjustments

to harvest estimates as they’ve been

finalized.InNorthAmerica,adownward

revision has been made in the latest

estimate of this year’s output in the

United Statesbuttheharvestwasstill

goodandsharplyup fromtheprevious

year. InCanada, as expected, the crop

turnedoutwelldownonlastyearwith

hotanddryconditionscompoundingthe

impactofreducedarea.InEurope,latest

estimatespointtoa2.3percentdecline

inproduction,contrastingwiththeearly

seasonprospectsforasizeableincrease.

The worst losses were encountered in

manyeasternpartsoftheregionwhere

several weeks of exceptionally hot and

dryweatherseverelycompromisedyields,

inparticular,inRomania,Bulgariaand

Moldova. However, latest information

indicates that the most easterly

producingarea - theSiberian regionof

theRussian Federation–escapedthe

droughtandastheharvestprogresseda

largercropwasrevealedthere.Similarly,

Kazakhstan, in the Asian CIS region

to the south of Siberia also escaped

the drought, and yields turned out

muchbetterthanearlierexpected.Asa

result, the aggregate estimate for Asia

has been raised from earlier forecasts

andnowstandsatalmost4percentup

compared to the 2006 crop and well

abovetheaverageofthepastfiveyears.

Elsewhere in the northern hemisphere,

drought devastated this year’s wheat

crop in Morocco, and despite about-

average harvests elsewhere in North

Africa,thesubregion’saggregateoutput

issharplydownfromlastyearaswellas

fromtheaverageofthepastfiveyears.

Low-Income Food-Deficit Countries (LIFDCs)6

No. 6 n December 20076

Crop Prospects and Food Situation

Favourable outlook for 2008 wheat cropsWith the winter wheat sowing in the

northern hemisphere virtually complete,

thelatestindicationspointtoasignificant

increaseintheworldwheatareafor2008.

In the United States, early tentative

estimatesputthewinterwheatareaupby

about3.5to4percentfromtheprevious

year,inresponsetohighprices.Thespring

wheatareamayalsoincreaseiftheprice

incentives for this crop at planting time

nextyearremainrelativelybetterthanfor

competingspring-sowncrops.InCanada

the wheat is predominantly spring sown

but early indications suggest plantings

mayincreasebysome10percentaftera

reducedarea this year.Theminorwinter

crophasalreadybeensownandplantings

aretentativelyestimatedtohaveincreased

byabout5percent. ThroughoutEurope,

conditions have been mostly favourable

for winter wheat planting and early

growth.ThewheatareaintheEUisseen

to rise by some 6 percent following the

removalofthe10percentcompulsoryset-

asidefor2008,combinedwiththecurrent

high price incentive to plant wheat. In

theCIS regionofEurope, theareasown

to winter grains (mostly wheat) in the

Russian Federation has increased by

about5percent,tothehighestlevelsince

2001,whileinUkraine,anincreaseofat

least9percentisexpected.InNorthAfrica,

widespreadrainsinnorthernAlgeriaand

easternMoroccoandhavefavouredwinter

wheatplanting.However,precipitationhas

notbeensufficientsofarinsouthwestern

parts of Morocco where, following the

past season’sdrought, conditions remain

too dry for widespread sowing. Planting

normallycontinues throughDecember in

thesubregionsothereisstilltimeforcrops

tobesownshouldadequateprecipitation

arrive. In Asia, planting conditions are

generally favourable in the main winter

wheat producing areas. The wheat

area in China is expected to match the

previous year’s good level. In India, the

previous year’s large area is expected to

berepeated,withtheincentiveofa17.6

percentriseinthewheatsupportpricefor

2008.InPakistanconditionsforplanting

are reported to be generally favourable

withadequate soilmoisture. In theNear

East,plantingconditionsarefavourablein

Turkey but dry conditions prevail in the

Islamic Republic of Iran.

Downward revisions for some 2007 coarse grain harvests but still record cropDespite some recent slight downward

revision, FAO’s latest estimate of world

coarse grains production in 2007, at

1069milliontonnes,wouldstillrepresent

an increaseof8.5percentfromlastyear

and a record high crop. Most of the

recent revision has been on account of

adjustmentsfortheUnitedStates,where

themaizeharvesthasrecentlyconcluded

with slightly lower output than earlier

predicted. However, the United States

crop is still estimated at its highest ever

level,inresponsetohighpricesandstrong

demand from the biofuel industry and

the huge increase in this crop accounts

forthebulkoftheincreaseintheglobal

coarse grains harvest this year. Bumper

cropshavealsobeenharvested inSouth

America, reflecting increased plantings

andfavourablegrowingconditionsthatled

toexceptionalhighyields.Thesecondary

cropjustgatheredinBrazilwasestimated

at 25 percent above last year’s already

goodlevel.Arecordcropisalsoexpected

in Central America, where plantings

expandedinMexico,themajorproducer.

Elsewhere, the 2007 coarse grain crops

are seen to remain relatively unchanged

inAsiaandAfrica,whileunfavourabledry

andhotconditionscompromisedthecrops

in Europe and Australia, reducing 2007

productionintheseparts.Withregardto

thefirst of themajor2008maize crops,

plantingoftheimportantsummercropis

alreadyunderwayinSouthAmerica.Early

indicationspointtoacontinuedexpansion

in area because of the incentive of

attractivereturnsrelativetoothercrops.

Global rice production to change little in 2007, remaining close to last year’s above average outputAccording to the latest FAO estimates,

global rice production (milled terms) is

set to reach about 430 million tonnes,

onlymarginallyabovethelatestestimate

for 2006. Generally, the 2007 outlook

is positive in Asia, where production

is expected to increase by 3.7 million

tonnes, to about 585 million tonnes

driven by sizeable gains in China and

Indonesia, two of the leading rice

producing countries. Large increases

are expected in India and Myanmar

as well, although the final outturn of

the season in these countries is still

uncertain,asitwillmuchdependonthe

secondary winter crops, which are just

beingplanted.Theseasonisanticipated

to end positively also in the Islamic

Republic of Iran,Japan,Lao People’s

Democratic Republic, Malaysia,

Nepal and Thailand. By contrast,

crop prospects have deteriorated in

Bangladesh andCambodia,whichare

nowexpectedtoharvestamuchsmaller

crop than last season, reflecting in the

firstcase large losses incurredtofloods

1750

1850

1950

2050

2150

200720052003200119991997

Million tonnes

UtilizationProduction

Figure 1. World cereal productionand utilization (1997-2007)

forecast

No. 6 n December 2007 �

Crop Prospects and Food Situation

and, in the second, pest and diseases

whichdepressedyields.

Most of the other producers in the

region are anticipated to face a drop in

production.Althoughstillsubjecttosome

uncertainty,theoutlookinAfricapointsto

aslightoverallcontractionofproduction,

largely reflecting expectations of poor

cropsinCôte d’Ivoire,MaliandNigeria,

more than offsetting positive crop

prospects in Guinea and Madagascar.

Indeed, although precipitation over the

continent was particularly abundant this

season,therainfallwasill-distributedover

time, depressing rice yields and eroding

prior expectations of production gains.

Bycontrast, theearly seasonoutlook for

reduced output in the United States has

beenreversedinthelightofrecordyields

that are forecast to boost production by

2 percent this year. Elsewhere, paddy

production is likely to change little in

Europe,whileitissettofallinLatinAmerica

andtheCaribbeanandinOceania.

Prices of cereals remain high and volatile International wheat export prices that

have been increasing since June remain

at high levels. In November, the United

States wheat No 2 (HRW, fob) averaged

US$332per tonne, a slight decline from

itspeak inOctober,but stillUS$113per

tonne, or 52 percent, above the price a

year earlier. Firmer estimates for 2007

production, and less possibility of any

majorchangesregardingtheremainderof

the crops that are now being harvested,

coupled with indications of a larger

2008 wheat area planted, prompted

the downward movement of prices in

November. However, the tight supply/

demand situation following a second

consecutive reduced global wheat crop,

particularlyinexportercountries,andthe

verylowlevelsofstocks,havekeptwheat

prices athistorically elevated levels.High

wheat prices and soaring freight rates

have resulted in sharp increases in retail

prices of bread and other basic food in

large number of importing countries all

overtheworld,particularlyaffectinglow-

incomesectionsofthepopulation.

Export prices of maize that have

remained volatile since February, when

they reached a ten-year highofUS$177

per tonne, have risen in the past two

months. The United States yellow maize

No 2 (Gulf, f.o.b) averaged US$171 per

tonneinNovember,US$5pertonnemore

thaninthesameperiodayearago.Prices

of maize reacted to recent downward

revisionsofthe2007worldcoarsegrains

output,followingcompletionofthemaize

harvestintheUnitedStates,whichhowever

isstillarecordcrop.Despitethishighlevel

of production, the market remains tight

mainlyreflectingthecontinuingexpansion

of demand from the bio-fuel industry in

the United States. Strong maize prices,

combinedwithshortagesof feedwheat,

havepushedupthevaluesofmostother

feedgrains.

Consistent with the general trend

that has dominated since the beginning

of the year, international rice price have

strengthen in the past two months,

notwithstandingthearrivalinthemarkets

of the bulk of the 2007 season paddy

cropsinceNovember.Sustainedbylimited

supply availability in major exporting

countries and strong import demand

around theworld, thefirmnessofprices

was generalized, affecting rice of all

qualitiesandfromallorigins.SinceAugust,

the imposition of export restrictions by

Egypt,IndiaandVietNaminjectedfurther

strengthtothemarket,whichwasalready

buoyed by the weakening of the US

Dollar.

No. 6 n December 2007�

Crop Prospects and Food Situation

% %

10

14

18

22

26

30

10

14

18

22

26

30

07/0806/0705/0604/0503/04

Total cereals

Rice

Coarse grains

Wheat

f’castestim.

1. Ratio of world cerealstocks to utilization

% %

100

110

120

130

140

150

100

110

120

130

140

150

07/0806/0705/0604/0503/04f’castestim.

2. Ratio of major grain exporters supplies tonormal market requirements

% %

5

10

15

20

25

5

10

15

20

25

07/0806/0705/0604/0503/04

Total cereals

Rice

Coarse grains

Wheat

f’castestim.

3. Ratio of major exportsstocks to their total disappearance

nTheratioofworldcerealendingstocks

in 2007/08 to the trend world cereal

utilizationinthefollowingseasonisforecast

tofallto19.9percent,thelowestlevelof

the past five years. Surging utilization is

likely to absorb most of the anticipated

gain in world 2007 cereal production,

hencekeepingworldendingstocksatvery

lowlevels.Theratioforwheatisforecast

toplummetfurtherto22.3percent,well

under34percentobservedduringthefirst

half of the decade. However, for coarse

grains, the ratio isexpected to registera

small recovery from2006/07,whichwas

one of the lowest levels since the early

80s, to 16.4 percent. The ratio for rice

shouldremainvirtuallyunchanged.

FAO’s global cereal supply and demand Indicators

1 Thefirst indicatoristheratioofworldcerealendingstocksinanygivenseasontoworldcerealutilizationinthefollowingseason.Utilizationin2008/09isatrendvaluebasedonextrapolationfromthe1997/98-2006/07period.

nBased on the latest production

estimates, and assuming no further

significantrevisionsforimportantsouthern

hemisphereharvestsstilltobecompleted,

aggregate supplies of the major grain

exporters in 2007/08 are expected to

exceedtheirnormalmarketrequirements

byjust18percent,marginallyupfromthe

previous season, but still a relatively low

level,considering thefigurewasover30

percent in the mid-2000s. This indicates

onlyasmallimprovementintheabilityof

theseexporterstomeettheglobaldemand

forwheatandcoarsegrains importsand

points to a likely continuation of a tight

marketsituationinthenewseason.

2 Thesecond indicatoristheratiooftheexporters’grain(wheatandcoarsegrains)supplies(i.e.asumofproduction,openingstocks,andimports)totheirnormalmarketrequirements(definedasdomesticutilizationplusexportsofthethreeprecedingyears).ThemajorgrainexportersareArgentina,Australia,Canada,theEUandtheUnitedStates.

nThe ratio of the major exporters’

ending wheat stocks to their total

disappearance is forecast precariously

lowat just10percentat theendof the

2007/08 seasons. High wheat prices on

internationalmarketsarealready leading

to increased import bills for the low-

incomefood-deficitcountriesandshould

production not increase significantly in

2008 there could be major implications

forthesupply/demandoutlook.Forcoarse

grains,theratioisexpectedtoincreasefrom

thepreviousyear’s low.Thefastgrowing

demand forbiofuels is expected tokeep

maizeexportablesuppliesatexceptionally

tight levels even with a record harvest.

The ratio for rice is expected to change

relatively little remaining at just over 16

percent.

3 Thethird indicatoristheratioofthemajorexporters’endingstocks,bycerealtype,totheirtotaldisappearance(i.e.domesticconsumptionplusexports).Themajorwheatand coarse grainexportersareArgentina,Australia,Canada,theEUandtheUnitedStates.ThemajorriceexportersareIndia,Pakistan,Thailand,theUnitedStates,andVietnam.

No. 6 n December 2007 �

Crop Prospects and Food Situation

-4

-2

0

2

4

6

8

10

20072006200520042003estim. f’cast

4. Year-to-year changein world cereal production

Percentage

-4 -2 0 2 4 6 8 10

2003

2004

2005

2006

2007

LIFDCs

LIFDCs less China and India

Percentage

5 & 6. Year-to-year change incereal production in the LIFDCs

estim.

f’cast

-20 -10 0 10 20 30 40 50 60 70 80

2003/04

2004/05

2005/06

2006/07

2007/08

Wheat (July/June)

Maize (July/June)

Rice (Jan./Dec., first year shown)

Percentage

7. Year-to year changein selected cereal price indices

nWorldcerealproductionisforecastto

increase4.6percentin2007,whichwould

representarelativelystrongreboundafter

two consecutive years of contraction.

However, in viewof the tightlybalanced

situation demonstrated by the first 3

indicators,anothergoodyearisneededin

2008,especiallyforwheat.

4 Thefourth indicatorshowstheaggregatecerealproductionvariationfromoneyeartothenextatthegloballevel.

nFollowing four years of sustained

growth, the cereal production of LIFDCs

in 2007 is forecast to increase only

marginallyfrom2006,whichmeansaless

comfortable supply situation in the new

2007/08season.ExcludingChinaandIndia,

whichaccountforsometwo-thirdsofthe

aggregate cereal output, production in

therestofLIFDCswoulddeclinebynearly

3percent after twoconsecutive yearsof

substantial increases. This, coupled with

population increases, is likely to result in

several LIFDCs having to resort to larger

importstocovertheirconsumptionneeds,

which,atatimewheninternationalcereal

prices are at very high levels, will put a

heavyburdenonthefinancialresourcesof

thesecountries.

5&6 InviewofthefactthattheLow-IncomeFood-DeficitCountries(LIFDCs)aremostvulnerabletochangesintheirownproductionandthereforesupplies,theFAO’sfifth indicatormeasuresthevariationinproductionoftheLIFDCs.Thesixth indicatorshowstheannualproductionchangeintheLIFDCsexcludingChinaandIndia,thetwolargestproducersinthegroup.

nThe tightening of the global cereal

balancein2007/08haspushedupprices

ofallcereals.Themostsignificantincrease

has been forwheat, forwhich theprice

index during the first 5 months of the

current marketing year (July 2007 to

November2007),hasaveraged63percent

abovetheaveragefor2006/07.Formaize,

theprice surgehasbeen less significant,

withtheindexrisingbynearly27percent,

but this followsan increaseofnearly45

percentalsointhepreviousyear.Forrice,

amodest16.4percentincreasehasbeen

registeredin2007sofar.Theseincreases

arecontributingtoasignificantriseinthe

cerealimportbilloftheLIFDCsin2007/08,

which is forecast to jump 27 percent to

reach some US$31 billion. Following a

sharply increased cereal import bill also

in the previous year, makes the current

situation all the more burdensome for

theLIFDCs,especially for thosecountries

needinglargerimportstocoverdomestic

productionshortfalls.

7 Theseventh indicatordemonstratescerealpricedevelopmentsinworldmarketsbasedonchangesobservedinselectedpriceindices.

No. 6 n December 200710

Crop Prospects and Food Situation

High cereal prices are hurting vulnerable populations in developing countries

Prevailing high international cereal prices, coupled with

soaring freight rates and record world fuel prices, have

resulted in substantial rises in retailpricesof cerealbased

foodstaples, suchasbread,pastaandtortillas,aswellas

milk and meat, in countries across the world, generating

inflationarypressureondomesticfoodmarketsandfuelling

social unrest. In the past months, food riots have broken

out in such countries asMexico,Morocco,Uzbekistan,

Yemen,Guinea,MauritaniaandSenegal.

Most affected by the higher cereal prices are those

developing countries that depend heavily on imports

from theworldmarket to cover their cereal consumption

requirements.Poorpopulationsareanticipatedtobearthe

heaviestburden,becausetheirdietsconsistofaveryhigh

proportionofcereals.Inaddition,thepoorspendahigher

shareoftheirincomeonfoodthandowealthiersectionsof

populations: themost vulnerablegroupscan spendup to

80percentoftheirtotalexpendituresonbasicfoodsalone.

As a result, the higher cereal prices are not only leading

tothedeteriorationoftheirdietsintermsofquantityand

quality,butalsosignificantlyerodingtheiroverallpurchasing

power.

Governments around the world have implemented a

seriesofpolicymeasures to limit the increaseofdomestic

foodpricesandpreventconsumptionfromfalling,including

pricecontrols,subsidies,reduction/waivingofimportbarriers

and impositionofexport restrictions.The impactof these

measuresonthefoodsecurityofvulnerablehouseholdswill

varywidelyandisyettobeassessed.

In North Africa, in Algeria, Egypt and Morocco,

whichhave importedonaverage66percent,50percent

and36percentrespectivelyoftheirtotalwheatutilization

over the past 5 years, soaring international prices have

pushed up domestic prices of bread, the main staple,

seriouslyaffectingfoodsecurityofvulnerablehouseholds.

The Government of Morocco recently cut wheat import

tariffstothelowestlevelever,whileEgypthassignificantly

raisedfoodsubsidies.

In the CIS countries, there is concern about wheat

suppliesinTajikistanandKyrgyzstan.Inthelattercountry,

wherepoorpeoplespendover70percentoftheirincomes

on foodalone, thepriceof bread in the capital, Bishkek,

hasincreasedby50percent.Salariesandpensions,onthe

otherhand,haveincreasedonlyby10percentthisyear.It

is roughly estimated that 500000 people in the poorest

strataofthepopulationaredirectlyaffectedbytheincrease

inbread andother basic products. In an attempt to ease

the situation, the Government has released wheat from

the emergency reserve in the poorest areas but without

any effect on inflation. With spiralling food costs, the

Governmenthasrevisedthecountry’s2007annualinflation

estimatefrom5-6percentupto9percent.

In Central America, production of the main food

staple, tortilla, depends on large imports of maize, retail

pricesforwhicharewellabovethepreviousyear’slevel in

mostmarketsofthesubregion.InGuatemala,thepriceof

maize inSeptemberwasalmost50percenthigher thana

yearearlier.Breadfromwheatflour(fullyimportedexceptin

Mexico),anotherimportantcomponentofthefoodbasket

inCentralAmerica,hasalsoincreasedsharply,erodingthe

purchasingpowerofthepooresthouseholdsandhampering

theiraccesstofood.

In Andean countries of South America, where

production of the basic staple bread heavily depends on

importedwheatflour,thecurrenthighlevelofinternational

wheatpricesisalsoraisingconcernaboutthefoodsecurity

of low-incomehouseholds. InPeru,thepriceof imported

wheathasincreasedby50percentsincethebeginningofthe

yearwithresultingincreasesinthepriceofbread;thelocal

BakersAssociationhasproposed theadoptionof“bread-

coupons”inordertosubsidizebreadforthepoorestfamilies.

InEcuador, theGovernmenthasauthorized importswith

nolevyforwheatandwheatflourfromArgentinainorder

to control local bread prices. In Bolivia, the Government

has empowered the national army to run some industrial

bakeriestoproducebreadataffordablepricesforthemost

vulnerablepopulationgroups.

Elsewhere in the world, cereal import dependent

countries such as Cape Verde, the Gambia, Eritrea,

Somalia,LesothoandSwazilandinAfrica,orMongolia,

Sri Lanka andTimor-Leste inAsia,which,even ingood

agricultural years import at least50percentof their total

cerealconsumption,areamongthosemoreaffectedbythe

highlevelsofinternationalcerealprices.

No. 6 n December 2007 11

Crop Prospects and Food Situation

Low-Income Food-Deficit Countries food situation overview1

1The Low-Income Food-Deficit (LIFDC) group of countriesincludesfooddeficitcountrieswithpercaputannualincomebelowthelevelusedbytheWorldBanktodetermineeligibilityforIDAassistance(i.e.US$1575in2004),whichisinaccordancewiththeguidelinesandcriteriaagreedtobytheCFAshouldbegivenpriorityintheallocationoffoodaid.

Bumper 2007 cereal harvests in China and India but aggregate production to decline in the rest of LIFDCsWiththe2007cerealharvestscompleteor

nearcompletioninallregionsoftheword,

FAO’s latest forecast of the LIFDCs’ total

output still points to a marginal growth

of less than1percent from2006,which

followsincreasesof5.1and3.1percentin

theprevioustwoyears.Whenthelargest

countries China and India are excluded,

the aggregate production of the rest of

countries declined by about 2.8 percent

to297milliontonnes.Thismainlyreflects

a sharply reduced production in North

Africa,wheredroughtinMoroccocaused

adropof76percentincerealoutputthis

year,butalsodeclinesintheotherAfrican

subregions,withtheexceptionofSouthern

Africa where an aggregate bumper

cereal crop was obtained. Elsewhere,

LIFDCsgathered largerharvests in2007,

particularlyinAsia.

Cereal import bill goes up by over one-quarterTheaggregatecereal importrequirement

of the LIFDCs, as a group, in marketing

year 2007/08 is estimated at 81.6

milliontonnes,slightlybelowthelevelof

2006/07.MostofthedeclineisinFarEast

Asia, notably in India that is forecast to

import4.7milliontonneslesscerealsthan

in 2006/07. By contrast, larger imports

areforecastinNorthAfrica,asMoroccois

expectedtoincreaseimportsthisseasonby

over2milliontonnes.InSouthernAfrica,

despitethegoodaggregatecerealharvest

ofthisyear,higherimportsin2007/08are

projected mainly reflecting requirements

fromZimbabwe,wheremaizeproduction

declined by 43 percent from 2006. In

otherLIFDCsintheworld,cereal imports

are anticipated to remain around the

levels of 2006/07. Notwithstanding the

reduction in quantities to be imported,

the cereal import bill of the LIFDCs is

forecast to increase by 27 percent to

US$31.2 millions, after having increased

by35percentinthepreviousseason.This

reflects the prevailing high cereal export

prices,aswellassoaringfreightratesthat

havedoubledsincelastyear.

Cereal food consumption to decline, vulnerable populations most affectedHigher international cereal prices have

already translated into substantial rises

in retail prices of basic food, such as

bread,pasta,maizebasedproducts,milk

andmeat, inLIFDCs thatdependheavily

on imports to meet their consumption

requirements.Mostaffectedby the food

priceinflationarethelow-incomegroups

of population, as their daily energy

intake depends more on cereal based

products and the share of food in their

total expenditures is higher than that of

wealthiersectionsofpopulation.

No. 6 n December 20071�

Crop Prospects and Food Situation

Asaresultofthemoreexpensivecereal

importsand lowerdomesticproductions,

theaggregateconsumptionoftheLIFDCs

(excludingChinaandIndia)isprojectedto

increaseata rate lower than thatof the

populationgrowth,whichwould lead to

aslightreductioninthepercaputcereal

foodconsumption,adeclineinthequality

of the diet of the vulnerable population

and to a significant decline in the per

caput cereal feed use. The reduction in

the aggregate consumption of LIFDCs

(excludingChinaandIndia)couldbemore

pronounced than forecast if the price

increases prompt further reduction in

demandforcerealbasedfoodproducts.

Cereal stocks to decline in 2008Atthecurrent2007productionestimates

andprojectedimportsin2007/08,cereal

stocksofthegroupofLIFDCs(excluding

China and India) by the close of their

cropseasonsin2008areforecasttodrop

by12percentfromtheiropeninglevels,

after steadily increasing in the past few

years.

No. 6 n December 2007 1�

Crop Prospects and Food Situation

Regional reviews

North Africa • coarse grains: harvesting• winter grains: planting

Southern Africa: • main season (summer cereals): planting

Note:CommentsrefertosituationasofNovember.

Kenya, Somalia: • main season cereals: harvested• secondary season: plantings

Uganda• secondary cereal crop: harvesting

Western Africa Sahel• harvestingcoastal countries: • secondary crop: harvesting Central Africa

- northern parts• secondary crop:harvesting

Eritrea, Ethiopia Sudan:• main season grains: harvesting

Burundi, Rwanda• cereals (secondary season): growing

Tanzania, U.R.• main season cereals: plantings• secondary season cereals: establishment

Africa

North AfricaWinter grain planting underway but conditions remain too dry in MoroccoPlanting of the 2008 winter wheat and coarse grains is

underway throughout the subregion. In northeastern growing

areas, adequate rainfall combined with cool temperatures has

beenfavourableforplanting. InMorocco,however,wheresoil

moisturereservesareseriouslydepletedafterdroughtinthepast

season,precipitationhasnotbeensufficientsofar,andconditions

stillremaintoodryforwidespreadsowing.Thesubregion’s2007

wheatcropisestimatedat13.5milliontonnes,28percentdown

from the good crop of 2006 and below average, largely due

drought. In Morocco, worst hit by the dry conditions, wheat

outputwassharplyreducedby76percentfromthepreviousyear,

to the lowest levelof thepastfiveyears. InEgypt, the largest

producerinthesubregion,wheremostofthewheatisirrigated,

production returned to an average level of about 7.4 million

tonnes,afterabumpercropin2006.Alsoreflectingthedrought,

the subregion’s 2007 coarse grains crop is estimated at 10.8

milliontonnes,about8percentbelowthefive-yearaverage.

Governments in the subregion move to counter rising food pricesNorthAfricancountriesrelyheavilyonwheat importsfromthe

internationalmarkettocovertheirconsumptionneeds.Overthe

past 5 years, Algeria, Egypt and Morocco imported about 66

percent,50percentand36percentoftheirtotalwheatutilization

respectively.Soaring internationalpriceshave increased imports

bills and pushed up domestic prices of bread and other basic

food causing social unrest in most countries of the subregion.

The problem was compounded in Morocco by the extremely

low level of domestic production in 2007. Governments have

implementedaseriesofmeasuresaimedatoffsettingthesharp

increase in world prices, including the waiving of tariffs, price

controlsandsubsidies.Moroccorecentlycutwheatimporttariffs

tothelowestlevelever,whileEgypthassignificantlyincreased

foodsubsidies.Theimpactofthesemeasuresonhouseholdfood

securityisyettobeassessed.

Western AfricaJoint CILSS/FewsNet Crop Assessment Missions to the nine

Saheliancountries(Burkina-Faso,CapeVerde,Chad,TheGambia,

Guinea-Bissau, Mali, Mauritania, Niger and Senegal) have

recentlybeencompleted. TheMissionsreviewedtheevolution

ofthe2007croppingseasonandpreliminarycerealproduction

estimatespreparedbythenationalagriculturalstatisticsservices.

This year, the exercisewas extended to three coastal countries

-Benin,GhanaandNigeria.FAOparticipated insomeofthese

missions.

Another good cereal output in most of the Sahel in 2007 but less favourable prospects in the coastal countriesAccordingtopreliminary findings,a relativelygoodcrop is

being gathered in the Sahel in spite of this year’s erratic

rains. The 2007 aggregate cereal production in the nine

countries is provisionally estimated at about 14.9 millions

tonnes, mostly millet and sorghum (see Figure 2), which

is slightly lower than last year’s bumper output, but still

some 12 percent above the average of the last five years.

Atnationallevel,above-averageharvestsareforecastinall

Sahelian countries with the exception of Cape Verde and

Senegal,where,comparedtotheaverageofthepastfive

years,output is expected todeclineby46percentand11

percentrespectively(seebox).

In the countries along the Gulf of Guinea, generally

less favourable harvest outcomes are expected, notably

in northern Nigeria, where coarse grain production is

anticipated to decline significantly due to late and poorly

distributedrains,andinGhanawherealongdryspellwas

followed by floods negatively affecting crops during the

No. 6 n December 20071�

Crop Prospects and Food Situation

%2

Burkina Faso 25.1%

Senegal 6.7%

Niger 26.6%

Mauritania 1.2%

Mali 23.6%Guinea-Bissau 1.4%

Gambia 1.5%

Chad 13.9%

Cape Verde <1%

Figure 6. Maize prices in selected Eastern Africamarkets

Figure 2. Sahel - 2007 cereal production bycountry

season. Nigeria is the largest producer in Western Africa

and given the high level of market integration in the

subregion, a reduction in this country’s cereal production

can push up cereal prices in some other poorer and more

vulnerableoftheWesternAfricannations.Therearealready

reportsofrisingfoodpricesinnorthernNigeriaandGIEWS

willcontinuetomonitorcloselypricetrendsinneighbouring

countries.Anotherimportanttradeflowinthesubregionis

that between Burkina Faso and Ghana, thus, the reduced

production in thenorthernGhana isexpected tobeoffset

withinflowsfromBurkinaFaso.

Central AfricaInCameroonandtheCentral African Republic,harvesting

ofthesecond2007maizecrop(plantedfromMarch-April) is

abouttostartinthesouthandoverallprospectsarefavourable

reflectingadequaterainsthroughoutthecroppingseason. In

thenorth,characterizedbyonlyonerainyseason,harvesting

ofmilletandsorghumisunderwayandoutput is forecast to

be about average. While the overall food supply situation is

expected to be satisfactory in Cameroon, any improvement

in the foodsecurity situation in theCentralAfricanRepublic

continues to be hampered by persistent insecurity and

inadequate availability of agricultural inputs, notably in

northernparts.

Eastern AfricaGood cereal crops in 2007 throughout most of the subregionIn Eastern Africa, harvesting of the 2007 main season

cereal crops has ended or is about to be completed in all

No. 6 n December 2007 1�

Crop Prospects and Food Situation

countries of the subregion. Notwithstanding floods earlier

intheseasoninsomeareasofSudan,Eritrea,Ethiopiaand

Uganda, which resulted in casualties and serious localized

food shortages, crop prospects in most countries are

favourable and above-average crops have been gathered,

or are being gathered, in most countries. The subregion’s

aggregate cereal production in 2007 is provisionally

estimated at 34 million tonnes, slightly lower than the

record2006outputbut about17percenthigher than the

averageofthepreviousfiveyears.

The main exception to the otherwise generally satisfactory

foodoutlookinthesubregionisSomalia,whereoutputfromthe

main“Gu”crop,harvestedearlierintheseason,wasestimated

atabout49000tonnes,onlyone-thirdofthepost-waraverage

1995-2006, and the worst in thirteen years. The reduction is

largelytheresultofdroughtconditions,coupledwithconflictand

intenseinsecuritysincethebeginningof2007.Thesecombined

factors have led to the worst humanitarian crises in Africa at

present.Currently,atotal1.5millionpeopleinthecountryneed

urgent humanitarian assistance. The humanitarian situation is

Successive poor harvests and high prices threaten food security in the western part of the Sahel

InCape Verde, productionofmaize (virtually theonly

cereal grown in the country) has been severely limited by

reducedandirregularrainfallforthethirdyearinsuccession.

Productionofharicotbeans,anotherimportantfood,which

arenormally intercroppedwithmaize,hasalsobeenbadly

affectedbytheadversegrowingconditions.

Although Cape Verde is a food-deficit country and

usually imports the bulk of its consumption requirements,

anyshortfalls in thedomesticproductioncanhaveserious

implicationsfor thefoodsecurityofsmall-scaleproducers,

whonormallyconsumetheirentirecropathome,and for

whom it forms an important part of the diet. After three

yearsofreducedproductionalargeproportionoffarmersare

findingthemselvesinasituationofincreasedvulnerability.

Moreover,theimplementationofthecountry’ssafetynet

programmaynowbeconstrainedbythereducedallocations

of foodaid.Until recently, foodaidplayedamajor role in

Cape Verde’s food policy, accounting for over 50 percent

of total cereal consumption in some years. Monetisation

of foodaid tofinance“cash-for-work”activitieshasbeen

the main instrument used by the Government to deal

with foodemergencies.However, theamountof foodaid

receivedhasdeclinedsharplyinrecentyearsduetovarious

factors,includingtheupgradingofCapeVerdetomedium-

developed country status from least-developed country,

andtheshiftofseveraldonors’aidpolicytodirectbudget

support. As of late September the country had received

only3500tonnesoffoodaidin2007comparedto22000

tonnesbythesameperiodlastyear.Moreover,foodimports

anddistribution,whichwerehandledbyaparastatal food

supplyagency,havebeencompletelyliberalized,increasing

theexposureofthedomesticfoodmarkettothevariability

of international commodity markets. Therefore, the food

situationduringthe2007/08marketingyearwilldependon

two major factors: (i) The capacity of the Government to

finance and implement an effective safetynetprogram in

the short term, to assist affected populations and restore

their production capacity for the next agricultural season,

and(ii)theevolutionofinternationalfoodpricesandactions

the Government may take to mitigate their impact on

consumers’purchasingpower.

InSenegal,anotherpoorharvestisgatheredand2007

cereal production is estimated to have declined by 11

percentcomparedtothefive-yearaverage.Largesegments

oftheruralpopulation,alreadysufferingfromtheeffectsof

lastyear’slowproduction,haveyetagainhadpoorharvests

becauseofadverseweather.Theirfoodsecuritystatuswill

remainprecariousandmayevendeterioratefurther in the

2007/08marketingyearduetohighandrisinginternational

food prices. Senegal is a food-deficit country whose

domesticproductioncoversonlyabouthalfofthecountry’s

cereal utilization requirements, so it relies heavily on rice

and wheat imports, amounting to and average of about

900000tonnesperannum,fromtheinternationalmarket.

Foodpricesarethusakeydeterminantofaccesstofoodfor

themajorityofthepopulation.Lowerdomesticproduction

inacontextoftightinternationalmarketislikelytoleadto

highinflationarypressureonthedomesticfoodmarketand

erodethepurchasingpowerofurbanandruralconsumers.

Mauritania is also likely to be seriously affected

by increased international prices due to its high import

dependenceandlowpercaputincomelevels.

No. 6 n December 200716

Crop Prospects and Food Situation

furtheraggravatedbycontinued increases instaplefoodprices

thatlimitfoodaccessfordisplacedandpoorfamilieswhohave

lostincome-earningopportunitiesandhavelimitedfoodstocks.

These rising prices mainly reflect disruption of markets and

depreciationoftheSomalishillingagainsttheUSdollarwhichin

theShabelleValley--thecentreofthecurrenthumanitariancrisis

--hasdepreciatedby50percentsinceJanuary.Prospectsforthe

“deyr”secondarycerealcroptobeharvestedfromFebruary2008

arefavourable.Afteralatestart,rainfallinsouthernSomaliahas

beenincreasingbenefitingdevelopingcrops.Asuccessful“deyr”

harvestisneededtoimprovefoodsecurityintheregion.Cereal

import requirement in the current marketing year (ending July

2008) isestimated to increasebysome10percent to480000

tonnes.

In Sudan, the outlook for the 2007 coarse grain harvest,

currently underway, is good reflecting favourable growing

conditions. Rainfall was above-normal and availability of

agricultural inputs is reported to have been normal to above

normal. However, after a bumper crop in the previous year,

plantingsreturnedtomorenormallevelsthisseasonandoutput

isexpectedtodecreaseslightly,althoughremainingwellabove

theaverageforthepreviousfiveyears.Thetargetedareaforthe

wheatcrop,nowbeingsownandforharvestfromMarch2008,

hasbeenincreasedbyabout13percentto347000hectares.

As a result of continuing violence in Darfur, insecurity,

displacement and loss of livelihoods are expected to continue

over thenextmonthsand, concomitantwith this,malnutrition

ratesare likelytodeterioratedueto lackofaccesstofood.An

FAO/WFPPost-HarvestAssessmentMission is scheduled tovisit

northern Sudan early next year to review the estimates of the

2007coarsegrainsharvest,the2008wheatcropandreviewthe

cerealsupply/demandsituationin2008.

Overall cereal surplus in southern Sudan but internal trade possibilities limitedAnFAO/WFPCropandFoodSecurityAssessmentMissionwhich

visited south Sudan recently, has estimated cereal production

in 2007 in the south to be fractionally higher than last year

withhigher thannormal yields.However, since theanticipated

increaseinoutputwillnotentirelymeettherequirementofthe

spontaneousandorganizedreturnees,the2007/08foodsupply

positioninsouthernSudanisexpectedtoshowagenerallynegative

balance.Moreover,lackofinfrastructureandofadevelopedtrade

network,will limit themovementof largequantitiesof cereals

fromsomeofthesurplusareastothedeficitonesinUpperNile,

Jonglei,Unity,EastEquatoriaandBahrelGhazal.

InEthiopia,theprospectsforthe2007main“meher”crop

now being harvested remain favourable. Output is estimated

somewhatlowerthanlastyearbutabout20percenthigherthan

thefive-yearaverage.Notwithstandinganeasingofrestrictions

ontrade intheSomaliRegion,households invastareasofthis

regionwillremainfoodinsecureduetocivilconflict.Inmostof

therestofthecountrytheanticipatedgoodharvestisexpected

toimprovefoodsecurity.However,thefoodsecurityofthepoorer

households continue tobe affectedbyhigh foodpriceswhich

have increased in the last two years despite three consecutive

yearsofgoodharvests.

InUganda,theoutlookforthesecondaryseasoncoarsegrain

cropsnowbeingharvested is favourable.Theaggregatecereal

outputin2007isestimatedtoremainsimilartolastyear’scrop

andmarginallyabove theaverageof thepastfiveyears.Good

main crop harvests earlier in the year have generally increased

food supply to markets and prices remain within the reach of

mosthouseholds.However, ineasternparts,whereheavyrains

earlierintheyearcauseddamageanddisplacementofhundreds

offamilies,theaffectedpopulation,especiallyinTesoRegion,will

facemoderatefood insecurity inearly2008.Thepopulationat

risk, including internallydisplacedpeople, isestimatedatsome

1.4million,continuetoremainhighlyfoodinsecureandlargely

dependantonhumanitariansupport.

InKenya, theharvestingofthe2007long-rainsseasongrain

cropsiscompleted.Reflectingfavourableweatherconditionsand

increasedplantingsproductionisexpectedtoincreasebyabout

200000 tonnes, to 2.6million tonnes. Prospects for the short

rainsseasoncrop,whichnormallyaccountsforabout20percent

oftotalcerealoutputandisdueforharvestfromFebruarynext

year,arealsofavourable.Asaresultofexpectedabove-average

cerealcropsthenationalfoodsupplysituationisgoodandmaize

pricesareexpectedtodeclineinearly2008.Thefoodsecurityof

drought-affectedpastoralistshas improved inseveralareasand

itisexpectedtogetbetteraslongasseasonalrainfallcontinues.

However, food assistance continues to be assured to a large

number of people in the pastoral areas affected by previous

droughtandcontinuedpastoralconflicts.

In theUnited Republic of Tanzania, theoutput from the

2007maincoarsegrainscropharvestedearlier intheyearwas

estimatedsimilartolastyear’scropofsome4milliontonnesand

aboveaverage.Thesowingofthesecondarycropdueforharvest

early next year has been completed under overall favourable

weather conditions and pasture and water availability remains

above normal. The food supply situation is therefore generally

satisfactory.Marketsarewellsuppliedandon-farmstocksinrural

areasareadequateexcept in localizedareasof the22districts

thatwereaffectedbyfloodsoranearlyendofrains.However,

despite the overall good availability, wholesale market prices

for many foodstuffs are higher than last year reflecting rising

transport costs following fuel price increases and government

campaigns tobuycropsusingstandardizedweightmethodsat

thefarmgate.Thesehighpricesarelikelytolimitfoodaccessfor

low-incomehouseholdsinurbanareas.

No. 6 n December 2007 1�

Crop Prospects and Food Situation

100

150

200

250

NOSAJJMAMFJDN

US$ per tonne

UgandaKampala

Tanzania U.R.Dar-es-Salaam

KenyaMombasa

KenyaNairobi

2006 2007

Source: Eastern AFrica Regional Agricultural Trade Intelligence Network

Figure 3. Maize prices in selected Eastern Africamarkets

100

200

300

400

500

US$ per tonne

Maize

Wheat

Teff

Source: Ethiopian Grain Traders

Figure 4. Selected cereal prices in Addis Ababa, Ethiopia

Nov.

InEritrea,theprospectsforthemaincerealcrop,nowbeing

harvested,aregoodreflectingoneofthebestgrowingconditions

in the last eight seasons. Theoutput is estimated to reach the

leveloflastyear’scropofsome230000tonnes,sharplyhigher

thantheaverageforthepreviousfiveyears.However,thecountry

depends largely on imports - mostly commercial - to cover its

totalcerealconsumptionrequirementsofabout550000tonnes.

Despite good domestic production, cereal prices remain high

affectingfoodsecurityoflargesectionsofthepopulation.

Cereal prices show mixed trends in the subregionInKenyathepriceofmaize(Figure3),whichhadremainedstable

in recent months, fluctuated in the Nairobi market between

US$199pertonneandUS$202pertonneintheperiodMayto

September, increasedinOctoberandNovembertoUS$210per

tonneandUS$211pertonne,respectively.Pricesreactedtothe

Government’s announcement of a purchase price of US$215

per tonne for the crop recently harvested. Spillover effects of

higherimportpricesalsoinfluencedthemarket.However,prices

have started to drop in the main maize producing areas and

areexpectedtodeclinealsoinNairobireflectingthefavourable

supplysituation.

IntheUnited Republic of Tanzania,wholesalemaizeprices

in Dar-es-Salam - quite low since the beginning of the year

averagingUS$123per tonne - began to increase sharply since

August,toreachUS$237pertonneinNovember.Thisincrease

is explainedbyhighdemand fromneighbouring countries and

increasedtransportationcostsattributedtotherisinginternational

fuel prices. Moreover, the decision of the Government of the

UnitedRepublicofTanzaniatobuyatargeted30000tonnesof

food-grainsforstatereservesfromfarmersintheremotesurplus

productionarea,alsogavesupporttoprices.However,priceshave

droppedinthemarketsofsouthernhighlandsmaizeproduction

areasandareexpected to fall in thecapital city in thecoming

monthsreflectingthegoodharvestthisyear.

InUganda, thathadbeendecliningsince thebeginningof

the year and at low levels in September, increased sharply in

Octoberdespiteabundantsupplies.Thishasbeenattributedto

reducedmaizepurchasesfromhumanitarianagencies.

In Ethiopia, prices of cereals and other commodities have

beenunusuallyhighsinceearly2004despiteconsecutiveseasons

ofbumperharvests.Notwithstandingthemeasurestakenbythe

GovernmentinMarch2006tostabilizeprices,includingsalesat

subsidizedpricestotheneedyinselectedurbanareas,banongrain

exportsandvariousfinancialmeasures,priceshavecontinuedto

increase.Therateofincreasehasbeenextraordinarilyhighpriorto

theharvestofthe2007mainseasoncropfromNovemberwhen

thewholesalemaizeandwheatprices in thecapital reacheda

recordUS$248pertonneandUS$326pertonne,respectively(see

Figure4).Possiblereasonsfortherecentpricetrendinclude:rise

inearnings-beinghelpedbytherapidincreaseingovernment

expenditure - commercial credits, export receipts and transfers

in the form of remittances, withholding of cereal supplies by

smallholderfarmersandthedeclineoffoodaiddistributedinthe

country. In contrast to 2006, when no significant post-harvest

reduction of prices were observed, this year maize wholesale

priceinAddisAbabainthefirstweeksofNovemberhasshown

No. 6 n December 20071�

Crop Prospects and Food Situation

areductionofabout20percentcomparedtothepreviousthree-

monthaverageofUS$243pertonne.

Southern AfricaGood start of the 2008 cereal seasonPlantingofthe2007/08mainseasoncerealcrops,mainlymaize,

isunderway.Rains inthe lastdekadofOctoberandNovember

have been generally favourable for planting operations, with

heavyprecipitationinAngolaandlocalizedareasofSouthAfrica

andZimbabwe.Maizeandothercerealsplantinginthesubregion

willcontinuetillendofDecember.Thelong-rangerainfallforecast

for the 2008 main crop growing season is overall positive for

SouthernAfrica.

While it is still too early to estimate the sub-region’s area

plantedthisyear,inSouthAfrica,afarmer’splantingintentions

surveyindicatesthatthemaizeareacouldexpandfromlastyear’s

belowaveragelevelof2.55millionhectarestosome2.67million

hectares,encouragedbycurrenthighdomesticandinternational

prices.

Higher cereal import requirements in 2007/08 with large deficit in ZimbabweThe2007aggregateproductionofcerealsinthesubregionwas

estimatedonlysomewhathigherthantheabout-averagelevelof

thepreviousyear.Thisreflectsasecondconsecutivepoorcropin

SouthAfrica,byfarthelargestproducer,andagoodaggregate

outputoftherestofcountries.However,whilebumpercropswere

gatheredinseveralcountries,particularlyinMalawi,production

was reduced in net-importing countries, namely Zimbabwe,

Namibia,Lesotho,SwazilandandBotswana.Asaresult,inspite

ofthe increase intheaggregateproductionofcerealsthisyear

(excludingSouthAfrica),thetotalcerealimportrequirementfor

the2007/08marketingyear(April/Marchinmostcases)hasbeen

estimatedtobesome15percenthigherthaninthepreviousyear

at4.36milliontonnes,whichincludessome614000tonnesof

foodaid(Figure5).Zimbabweaccountsforalmostaquarterof

theanticipatedaggregate imports, followingasharpdecline in

cerealoutputthisyear.

Against total food aid cereal import requirements for

2007/08(April/March),pledgesordeliveriesuntilearlyNovember

are estimated at 394000 tonnes or some 64 percent of the

requirement.Thetotalcerealfoodaidneed,calculatedat614000

tonnes,islowerthantheaverageannualfoodaidoftheprevious

fiveyearsofabout708000tonnes.

Satisfactory regional food supplyOverall,maize supply in SouthernAfrica thismarketing year is

quitesatisfactory.Asizeableexportablesurplusisestimatedfrom

Malawi(around1milliontonnes),South Africa (around1million

tonnes), Zambia (about 250 000 tonnes) and Mozambique

(about 150000 tonnes). This compares with the subregion’s

aggregatemaizeimportrequirements(commercialandfoodaid

for both white and yellow) of 2.6 million tonnes. Hence local

andregionalpurchasesoffoodaid,directorthroughtriangular

arrangementsarehighlyrecommended.

Reflectinghighinternationalprices,areducedharvestinthe

majorproducerSouthAfricaandbelow-averageharvestsinseveral

countries,quotationsofmaizepricesareabovetheirlevelsofa

0

500

1000

1500

2000

2500

3000

3500

-60

-30

0

30

60

90

120

150

000 tonnes

Mau

ritius

Botsw

ana

Moz

ambiq

ue

Angola

Sout

h Afri

ca

Zimba

bwe

Import requirements 2007/08

% Change from 2006/07

Mala

wi

Swaz

iland

Leso

tho

Mad

agas

car

Zam

bia

Namibi

a

Figure 5. Southern Africa - Total cereal importrequirements for 2007/08 and percent changefrom 2006/07

%

500

1000

1500

2000

4

6

8

10

2005/06

2005/06

2006/07

2007/08

2007/08

2006/07

Figure 6. Southern Africa: wholesale prices of white maize in selected markets

South Africa, Randfontein Rand/tonne

Mozambique, MaputoMtk/kg

MFJDNOSAJJMA

Sources: South Africa: Randfontein spot price (www.safex.co.za). Mozambique: SIMA, Monthly average wholesale prices in Maputo.

MFJDNOSAJJMA

No. 6 n December 2007 1�

Crop Prospects and Food Situation

Note:CommentsrefertosituationasofNovember.

Southeastern Asia: • rice (main): reproductive to maturing to harvesting• maize: planting

Near East: • winter grains: planting to establishment

China: • late double-crop rice (south): harvesting• winter wheat: planting

South Asia: • rice (main): harvesting• coarse grains: harvesting

India: • rice (Kharif): harvesting• maize (Kharif): harvesting• millet (Kharif): harvesting• wheat (Rabi): planting• maize (Rabi): planting

Asia (CIS): • small grains: harvested• maize: harvested• winter crops: planting underway or completed

yearearlierinmostcountriesofthesubregion,withtheexception

ofMalawi,(Figure6)andcontinuingthegeneralupwardtrend

startedduringthepost-harvestmonthsofApril-May.InSouth

AfricatheRandfonteinspotpriceofwhitemaize,hasrisenfrom

R1652/tonne(US$235/tonne)inMay2007toahighofR1862/

tonne(US$253/t)inSeptember2007showingaslight,andmost

likelyatemporary,declineinOctoberatR1820.SAFEXfuture’s

pricesshowcontinuationofthispositivetrenduntilMarch2008.

HighpricesinSouthAfrica,theregion’smainexportingcountry,

haveaffecteddomesticpricesinotherimportingcountriesinthe

region,especiallySwaziland, Lesotho andZimbabwe.

Bycontrast,inMalawi,abumpermaizeharvesthasresulted

inpost-harvestpricesbeingconsiderablylowerthaninthepast

twoyears.

In Madagascar prices of rice, the main staple food, need

watching carefully as the current levels have remained much

higher than the year before, despite an increase in the 2007

production, and are potentially heading upwards to the levels

which caused serious crisis last year. Increased rice importation

wouldberequiredtoavoidfurtherescalationofthisprice.

Asia

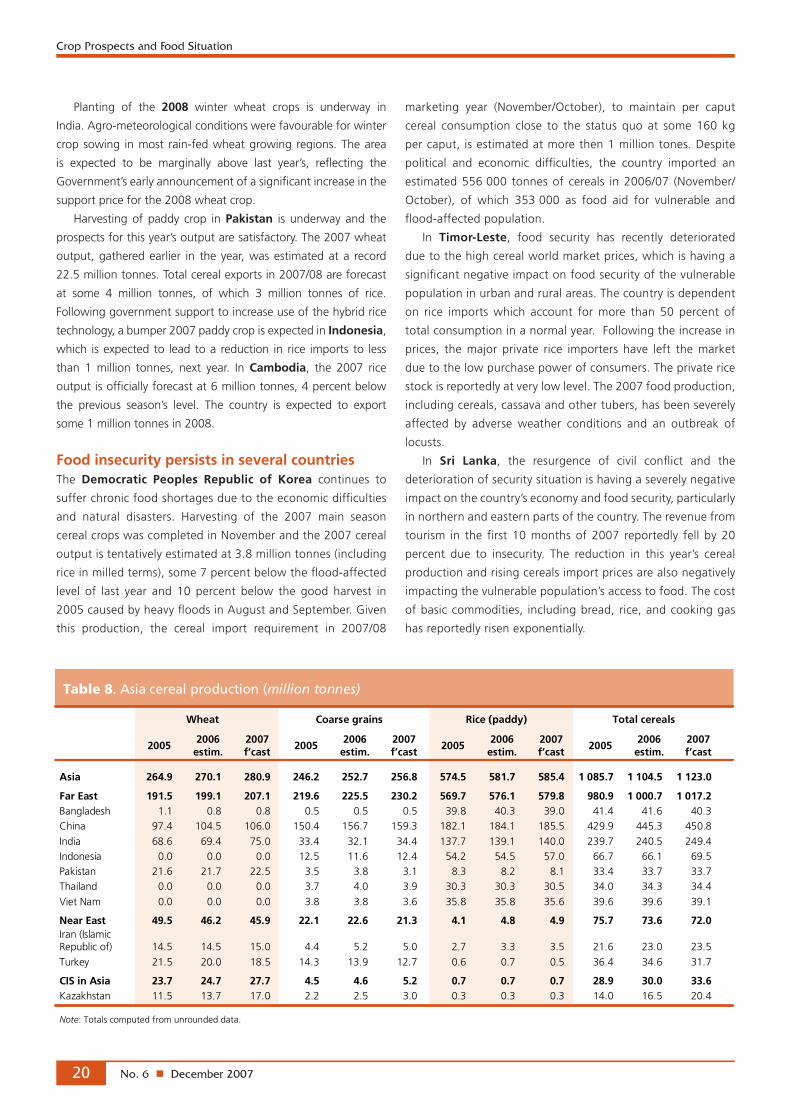

Far EastRecord 2007 cereal harvest with bumper crops in China and IndiaHarvestingofthemainriceandcoarsegrainscropsiscomplete

or drawing to a close. Based on latest information, the 2007

aggregate output of paddy is forecast at a record 580 million

tonnes, slightly above the previous year’s high. The aggregate

maizeoutput isforecastat198.1milliontonnes,marginallyup

from last year’s already bumper crop. Harvesting of the 2007

secondaryspring/summerwheatcrophas justbeencompleted,

whilethemainwintercropwasgatheredearlierintheyear.The

2007aggregatewheatoutputofthesubregion isestimatedat

207milliontonnes,4percentupfromlastyear’shighproduction

and 10 percent above the average of the previous five years.

Most of the increase comes from India. Planting of the 2008

winterwheatcropsisunderwayorcompleteinthemajorwheat

producingcountriesofthesubregionunderfavourableconditions

sofar,andalargeroverallareaisexpectedinresponsetohigh

prices.

In China (Mainland), harvesting of the

late riceandcoarsegrainshasbeencomplete.

The estimate of the 2007 aggregate paddy

production remains unchanged at 184 million

tonnes,about1percentupfromlastyear’slevel.

Harvestingofmaize is completeand the2007

maizeoutputisestimatedat148milliontonnes,

some2.5milliontonnesabovetherecordhigh

of2006,reflectinganincreaseinareaplanted,

due to relative higher profit, and favorable

weather. The aggregated 2007 wheat output

was estimated at a record 106 million tonnes.

Overall,China’s2007cerealoutputisestimated

at some 449 million tonnes, an increase of

about1.2percentfromlastyearand9percent

comparedtothefive-yearaverage.Asaresult,

thecountryisexpectedtoincreaseitsnetcereal

exportin2007,whileclosingstocksareexpectedtoincreasein

2007/08.

Planting of the 2008 winter wheat crop is complete in the

majorwheatproducingregionsofChina.Theareaisestimated

marginallyabovelastyear’salreadylargeareaduetotheincentive

ofhighwheatpricesandcontinuedgovernmentsupportforgrain

production.Thegrowingconditioninthemajorwheatproducing

provincesisclosetonormalandthesoilmoistureisadequate.

InIndia,the2007paddyproductionisforecastatabout140

milliontonnes,closetolastyear’sgoodharvest,whilethe2007

maize is forecastat15.5milliontonnes,some2milliontonnes

abovelastyear’sreducedoutput.Basedonthelatestinformation,

the2007wheatoutputisestimatedat75milliontonneswhich

issome5milliontonneshigherthan in2006andthefive-year

average.As a result of this goodoutturn, the country’swheat

importsin2007/08(April/March)hasbeenreviseddownfrom3

milliontonnes to2milliontonnes.Thecountry importedsome

6.7milliontonnesofwheatin2006/07.

No. 6 n December 2007�0

Crop Prospects and Food Situation

marketing year (November/October), to maintain per caput

cereal consumption close to the status quo at some 160 kg

percaput, isestimatedatmorethen1milliontones.Despite

political and economic difficulties, the country imported an

estimated556000 tonnesof cereals in2006/07 (November/

October), of which 353000 as food aid for vulnerable and

flood-affectedpopulation.

In Timor-Leste, food security has recently deteriorated

duetothehighcerealworldmarketprices,whichishavinga

significantnegativeimpactonfoodsecurityofthevulnerable

populationinurbanandruralareas.Thecountryisdependent

on rice imports which account for more than 50 percent of

totalconsumptioninanormalyear.Followingtheincreasein

prices, the major private rice importers have left the market

duetothelowpurchasepowerofconsumers.Theprivaterice

stockisreportedlyatverylowlevel.The2007foodproduction,

includingcereals,cassavaandothertubers,hasbeenseverely

affected by adverse weather conditions and an outbreak of

locusts.

In Sri Lanka, the resurgence of civil conflict and the

deteriorationofsecuritysituationishavingaseverelynegative

impactonthecountry’seconomyandfoodsecurity,particularly

innorthernandeasternpartsofthecountry.Therevenuefrom

tourism in thefirst10monthsof2007 reportedly fell by20

percent due to insecurity. The reduction in this year’s cereal

productionandrisingcerealsimportpricesarealsonegatively

impactingthevulnerablepopulation’saccesstofood.Thecost

ofbasiccommodities, includingbread,rice,andcookinggas

hasreportedlyrisenexponentially.

Planting of the 2008 winter wheat crops is underway in

India.Agro-meteorologicalconditionswerefavourableforwinter

cropsowing inmost rain-fedwheatgrowingregions.Thearea

is expected to be marginally above last year’s, reflecting the

Government’searlyannouncementofasignificantincreaseinthe

supportpriceforthe2008wheatcrop.

Harvestingofpaddy crop inPakistan is underwayand the

prospectsforthisyear’soutputaresatisfactory.The2007wheat

output,gatheredearlier in theyear,wasestimatedata record

22.5milliontonnes.Totalcerealexportsin2007/08areforecast

at some 4 million tonnes, of which 3 million tonnes of rice.

Followinggovernmentsupporttoincreaseuseofthehybridrice

technology,abumper2007paddycropisexpectedinIndonesia,

which isexpectedto leadtoa reduction in rice imports to less

than 1 million tonnes, next year. In Cambodia, the 2007 rice

outputisofficiallyforecastat6milliontonnes,4percentbelow

the previous season’s level. The country is expected to export

some1milliontonnesin2008.

Food insecurity persists in several countriesThe Democratic Peoples Republic of Korea continues to

sufferchronicfoodshortagesduetotheeconomicdifficulties

and natural disasters. Harvesting of the 2007 main season

cerealcropswascompletedinNovemberandthe2007cereal

outputistentativelyestimatedat3.8milliontonnes(including

riceinmilledterms),some7percentbelowtheflood-affected

level of last year and 10 percent below the good harvest in

2005causedbyheavyfloodsinAugustandSeptember.Given

this production, the cereal import requirement in 2007/08

No. 6 n December 2007 �1

Crop Prospects and Food Situation

Several countries in Far East suffer from floods/landslides and cyclones

In Bangladesh, a super cyclonic storm (category 4)

on 15 November caused extensive damage, affecting

closeto8.5 million8.5million peoplein30districts.Latestofficial

estimates(dated28November)indicatemorethan3 2563256

people were killed and 880 missing. More than 1.43

million houses were completely or partially destroyed.

The impact on agriculture is also severe, with 823 000

hectares of paddy and other crops damaged and 1.2

million animals, mostly cattle, killed. Already in June-

July this year, the country suffered from severe floods

and landslides which affected some 10 million persons

across 39 districts. http://www.fao.org/giews/english/

index.htm

In early November, Viet Nam suffered the fifth