newground reviable white paper 11011

TRANSCRIPT

Take a second look at existing branches to set your organization up for success

Is your branch network ready for the next growth opportunity?

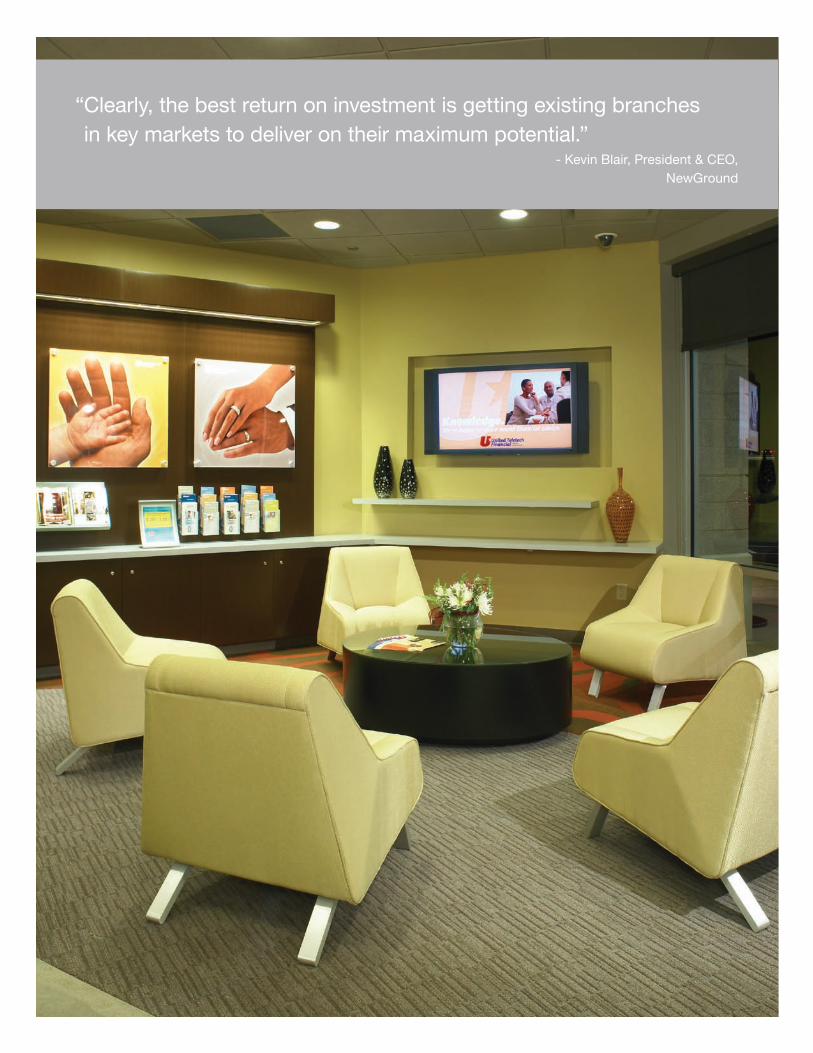

“ Clearly, the best return on investment is getting existing branches in key markets to deliver on their maximum potential.”

- Kevin Blair, President & CEO, NewGround

In the business world, it’s all about being ready to capitalize on the opportunities of today and those that will emerge tomorrow. Is your branch network set up for peak performance across markets to provide the greatest return on investment?

Until recently, a branch network expansion strategy helped many financial institutions fuel growth and conquer new geographic markets. According to the Federal Deposit Insurance Corporation, the total number of branches in the United States grew at a total rate of 28% with a total branch increase count of 18,990 between 1999 and 2009.

Future shock: the aftermath of the branch sonic boom

On the downside, it is estimated that nearly three-fourths of existing branches worldwide are inadequate to meet the needs of today’s customers because of the focus on new branches, according to an article in Talaris Interactive, Revitalizing Channel Distribution (Autumn 2009).

The 75 percent ratio holds true within the United States. Out of 120,000 total banking offices, including credit unions and savings banks, more than 80,000 locations are at least 10 years or older. New prototypes built within the past 10 years generally have not been integrated across entire branch distribution networks. Nor have new retail concepts been introduced into older, legacy branches, creating a jarring disconnect for customers.

How should legacy branches in the branch network be put to work for the organization? A cost containment-only branch network strategy has considerable down side. Closing under-performing branches during a time of economic contraction can spook already unsettled customers, sending an unintended message of instability. The opportune time to wield the hatchet is often best during times of prosperity and growth rather than during challenging times.

Given the current economic situation, the most attractive strategy is to create a higher return on investment within the existing branch network for today and ready the organization for opportunities that will emerge tomorrow.

Legacy branches have sat, often ignored, like Cinderella on the sidelines during recent periods of economic highs and lows. The capital invested in older branches is significant. Now is the time to dress up Cinderella.

“ Financial institutions worldwide that are taking steps to become more competitive across their entire retail distribution network will be positioned for success in the upcoming rebound,” said Kevin Blair, President and CEO, NewGround. “Clearly, the best return on investment is getting existing branches in key markets to deliver on their maximum potential.”

64

,33

0

68

,25

9

65

,66

9

73

,507

82

,88

9

64

,901

1999

55,000

2009

70

,89

0

79

,115

66

,941

76

,55

3

83

,32

0

Federal Deposit Insurance Corporation Number of Branches FDIC-Insured Commercial Banks

United States & Other Areas Balances at Year End, 1999-2009

1IS YOUr Br ANCH NET wOrK rE ADY FOr THE NEx T GrOw TH OPPOrTUNIT Y?

1 “The Next Growth Opportunity for Banks: How the Post-Crisis Financial Needs of Younger Consumers will Transform retail Banking Services,” by Philip Farah, James Macaulay and Jörgen Ericsson. Cisco Internet Business Solutions Group report Study.

Because of age, changing retail concepts, and evolving customer needs, legacy branches can easily move out of alignment with an organization’s current brand promise and value proposition. Most legacy branches are ten years or older, in many cases, considerably older, and may have been inherited during a merger or acquisition. As mentioned, new prototypes or retail concepts often have not been integrated across the branch network. In addition, many legacy branches have not been assessed in recent years to determine how well the location meets the needs of the current and future customer base.

Even little things, like scuffed-up walls and threadbare carpeting, communicate volumes to skittish customers in lean economic times. Branches begin to show their age quickly, and it’s often hard for those closest to the branch to recognize how tired a location can look to customers. More significantly, the branch may not be set up to facilitate banking today or designed to adapt nimbly to future trends.

Not every branch needs to look identical, but there should be a set of signature elements that convey a consistent image across the branch network and a branch readiness plan in place to respond to changing customer and market demands.

For example, a February 2010 report by Cisco Internet Business Solutions Group1 predicts that the technology preferences of younger consumers will have a profound impact on retail banking and will provide the next opportunity for revenue growth.

Cisco surveyed more than 1,000 U.S. Generation Y, Millennials (born between 1980 and 1992) and Generation x (born between 1960 and 1979) consumers and found younger customers want advice on personal financial management and look to banks as their primary providers of advice for issues like getting out of debt and saving for the future. Yet, to succeed with this emerging and powerful consumer block, retail banking needs a new approach. Younger consumers want financial solutions delivered via alternative channels like mobile devices, video and social networking and are willing to switch to financial organizations that offer these technologies.

Although not all answers are known today, financial institutions should plan how their branches can connect cost-effectively with these younger consumers, who do not have the net worth to validate the marketing spend currently devoted to older affluent consumers. This preparation should be part of a comprehensive branch optimization and readiness plan.

ready or not, the next growth opportunity is around the corner from your branch

2 IS YOUr Br ANCH NET wOrK rE ADY FOr THE NE x T GrOw TH OPPOrTUNIT Y?

1

3

Three critical reasons to revitalize existing branches

2Great place to work

Often, top performers are siphoned off to work at new high profile prototype retail branches. who’s left minding the store at legacy branches? And, how do employees feel about being left behind? It’s critical that the most important asset, the organization’s employees, are set up for success in legacy locations. Don’t forget, dissatisfied employees may jump to the competitor’s new branch down the street and take customer relationships with them. Studies have shown dynamic retail environments attract and retain employees and produce higher employee morale and greater customer satisfaction.

It makes good cents

The investment to acquire property and design, construct, furnish and staff a new branch can reach millions, before any payback is in sight. Take that same investment and apportion it strategically across the most promising legacy branches in high-growth markets. The returns are much greater than those resources invested in a single site. By adjusting the level of refurbishing to fit the potential of the branch and amount of maintenance required, an organization could easily touch as many as fifty sites. Think about the impact this diversification strategy would make across a branch network and how many customers would be touched.

Mind the gap

Financial institutions that have built new branches in the past 10 years and haven’t refurbished existing branches are facing a brand misalignment. Each new branch further widens this disconnect. Customers are probably visiting this mishmash of branches, either during their workday or on errands. The implied message to customers, who bank regularly at older branches that are tired and worn out, is that the institution doesn’t value those locations, and as a result, may not value its relationship with them.

3IS YOUr Br ANCH NET wOrK rE ADY FOr THE NEx T GrOw TH OPPOrTUNIT Y?

4 IS YOUr Br ANCH NET wOrK rE ADY FOr THE NE x T GrOw TH OPPOrTUNIT Y?

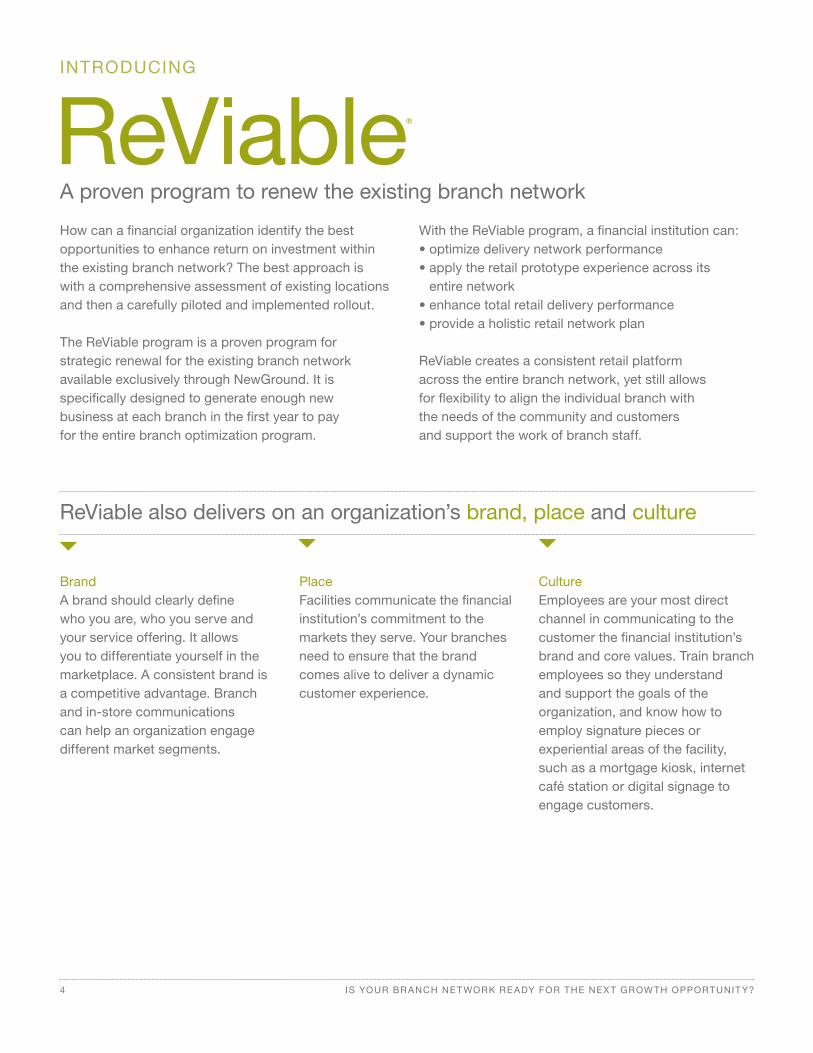

How can a financial organization identify the best opportunities to enhance return on investment within the existing branch network? The best approach is with a comprehensive assessment of existing locations and then a carefully piloted and implemented rollout.

The reViable program is a proven program for strategic renewal for the existing branch network available exclusively through NewGround. It is specifically designed to generate enough new business at each branch in the first year to pay for the entire branch optimization program.

with the reViable program, a financial institution can: • optimize delivery network performance• apply the retail prototype experience across its

entire network• enhance total retail delivery performance• provide a holistic retail network plan

reViable creates a consistent retail platform across the entire branch network, yet still allows for flexibility to align the individual branch with the needs of the community and customers and support the work of branch staff.

Brand A brand should clearly define who you are, who you serve and your service offering. It allows you to differentiate yourself in the marketplace. A consistent brand is a competitive advantage. Branch and in-store communications can help an organization engage different market segments.

PlaceFacilities communicate the financial institution’s commitment to the markets they serve. Your branches need to ensure that the brand comes alive to deliver a dynamic customer experience.

Culture Employees are your most direct channel in communicating to the customer the financial institution’s brand and core values. Train branch employees so they understand and support the goals of the organization, and know how to employ signature pieces or experiential areas of the facility, such as a mortgage kiosk, internet café station or digital signage to engage customers.

reViable also delivers on an organization’s brand, place and culture

A proven program to renew the existing branch network

reViable®

INTrODUCING

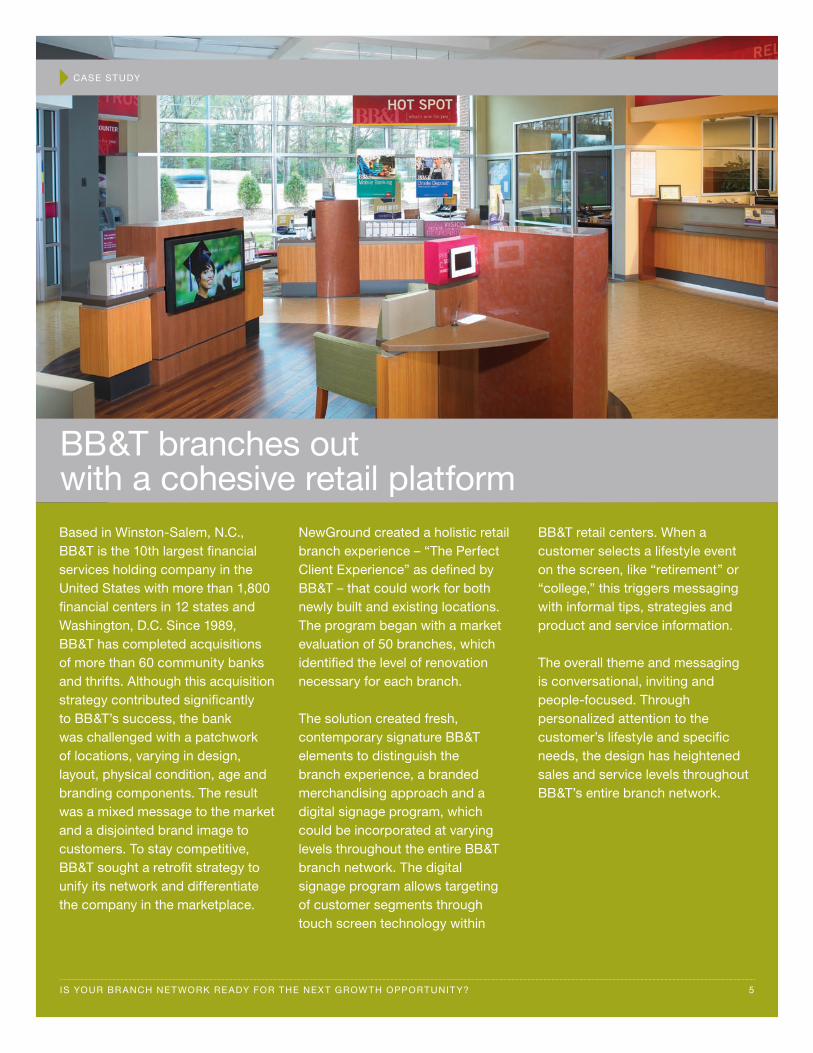

Based in winston-Salem, N.C., BB&T is the 10th largest financial services holding company in the United States with more than 1,800 financial centers in 12 states and washington, D.C. Since 1989, BB&T has completed acquisitions of more than 60 community banks and thrifts. Although this acquisition strategy contributed significantly to BB&T’s success, the bank was challenged with a patchwork of locations, varying in design, layout, physical condition, age and branding components. The result was a mixed message to the market and a disjointed brand image to customers. To stay competitive, BB&T sought a retrofit strategy to unify its network and differentiate the company in the marketplace.

NewGround created a holistic retail branch experience – “The Perfect Client Experience” as defined by BB&T – that could work for both newly built and existing locations. The program began with a market evaluation of 50 branches, which identified the level of renovation necessary for each branch.

The solution created fresh, contemporary signature BB&T elements to distinguish the branch experience, a branded merchandising approach and a digital signage program, which could be incorporated at varying levels throughout the entire BB&T branch network. The digital signage program allows targeting of customer segments through touch screen technology within

BB&T retail centers. when a customer selects a lifestyle event on the screen, like “retirement” or “college,” this triggers messaging with informal tips, strategies and product and service information.

The overall theme and messaging is conversational, inviting and people-focused. Through personalized attention to the customer’s lifestyle and specific needs, the design has heightened sales and service levels throughout BB&T’s entire branch network.

BB&T branches out with a cohesive retail platform

5IS YOUr Br ANCH NET wOrK rE ADY FOr THE NEx T GrOw TH OPPOrTUNIT Y?

CASE STUDY

7IS YOUr Br ANCH NET wOrK rE ADY FOr THE NEx T GrOw TH OPPOrTUNIT Y?

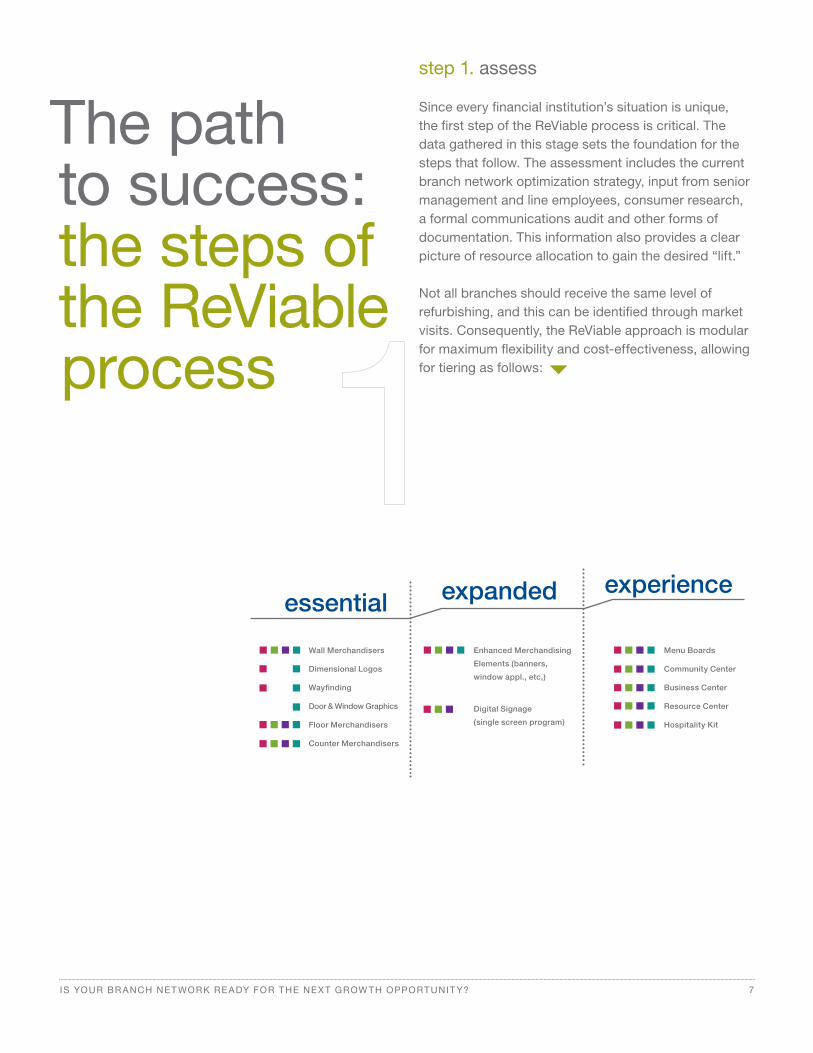

step 1. assess

Since every financial institution’s situation is unique, the first step of the reViable process is critical. The data gathered in this stage sets the foundation for the steps that follow. The assessment includes the current branch network optimization strategy, input from senior management and line employees, consumer research, a formal communications audit and other forms of documentation. This information also provides a clear picture of resource allocation to gain the desired “lift.”

Not all branches should receive the same level of refurbishing, and this can be identified through market visits. Consequently, the reViable approach is modular for maximum flexibility and cost-effectiveness, allowing for tiering as follows:

The path to success: the steps of the reViable process

essential expanded experience

Wall Merchandisers

Dimensional Logos

Wayfinding

Door & Window Graphics

Floor Merchandisers

Counter Merchandisers

Menu Boards

Community Center

Business Center

Resource Center

Hospitality Kit

Enhanced Merchandising

Elements (banners,

window appl., etc,)

Digital Signage

(single screen program)

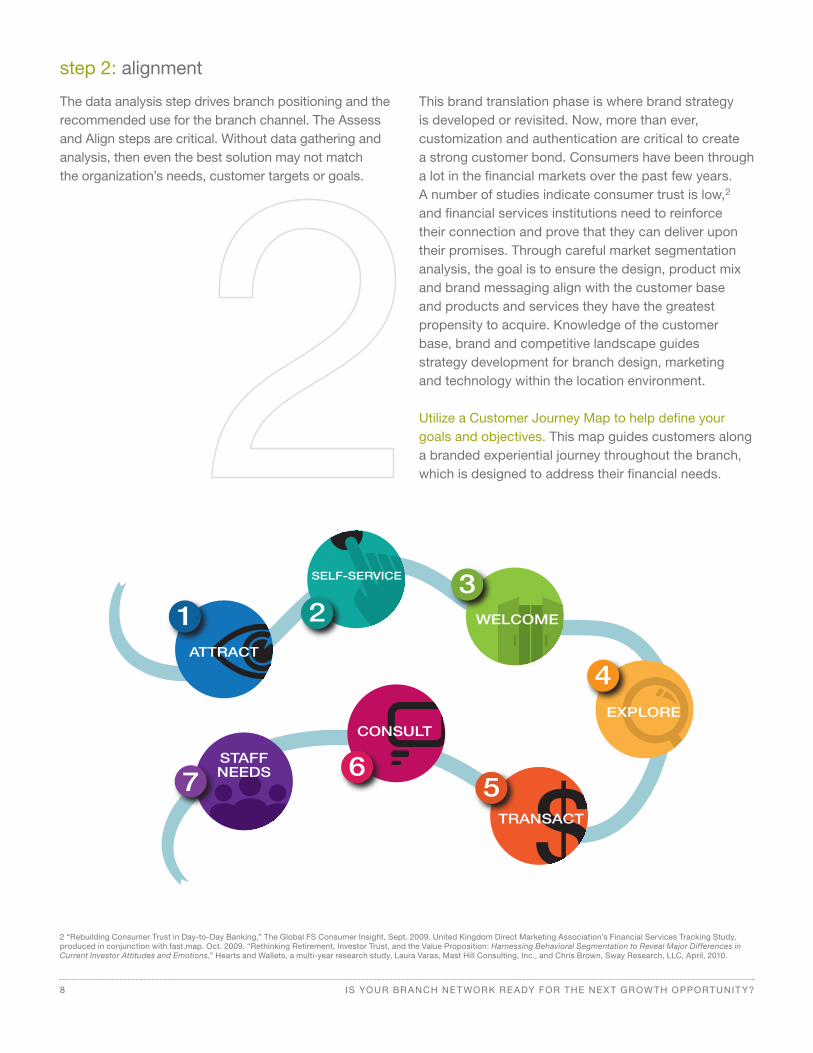

step 2: alignment

The data analysis step drives branch positioning and the recommended use for the branch channel. The Assess and Align steps are critical. without data gathering and analysis, then even the best solution may not match the organization’s needs, customer targets or goals.

This brand translation phase is where brand strategy is developed or revisited. Now, more than ever, customization and authentication are critical to create a strong customer bond. Consumers have been through a lot in the financial markets over the past few years. A number of studies indicate consumer trust is low,2 and financial services institutions need to reinforce their connection and prove that they can deliver upon their promises. Through careful market segmentation analysis, the goal is to ensure the design, product mix and brand messaging align with the customer base and products and services they have the greatest propensity to acquire. Knowledge of the customer base, brand and competitive landscape guides strategy development for branch design, marketing and technology within the location environment.

Utilize a Customer Journey Map to help define your goals and objectives. This map guides customers along a branded experiential journey throughout the branch, which is designed to address their financial needs.

2 “rebuilding Consumer Trust in Day-to-Day Banking,” The Global FS Consumer Insight, Sept. 2009. United Kingdom Direct Marketing Association’s Financial Services Tracking Study, produced in conjunction with fast.map. Oct. 2009. “rethinking retirement, Investor Trust, and the Value Proposition: Harnessing Behavioral Segmentation to Reveal Major Differences in Current Investor Attitudes and Emotions,” Hearts and wallets, a multi-year research study, Laura Varas, Mast Hill Consulting, Inc., and Chris Brown, Sway research, LLC, April, 2010.

SELF-SERVICE

2

4EXPLORE

$5

TRANSACT

6

CONSULT

7STAFFNEEDS

WELCOME

3

ATTRACT

1

8 IS YOUr Br ANCH NET wOrK rE ADY FOr THE NE x T GrOw TH OPPOrTUNIT Y?

9IS YOUr Br ANCH NET wOrK rE ADY FOr THE NEx T GrOw TH OPPOrTUNIT Y?

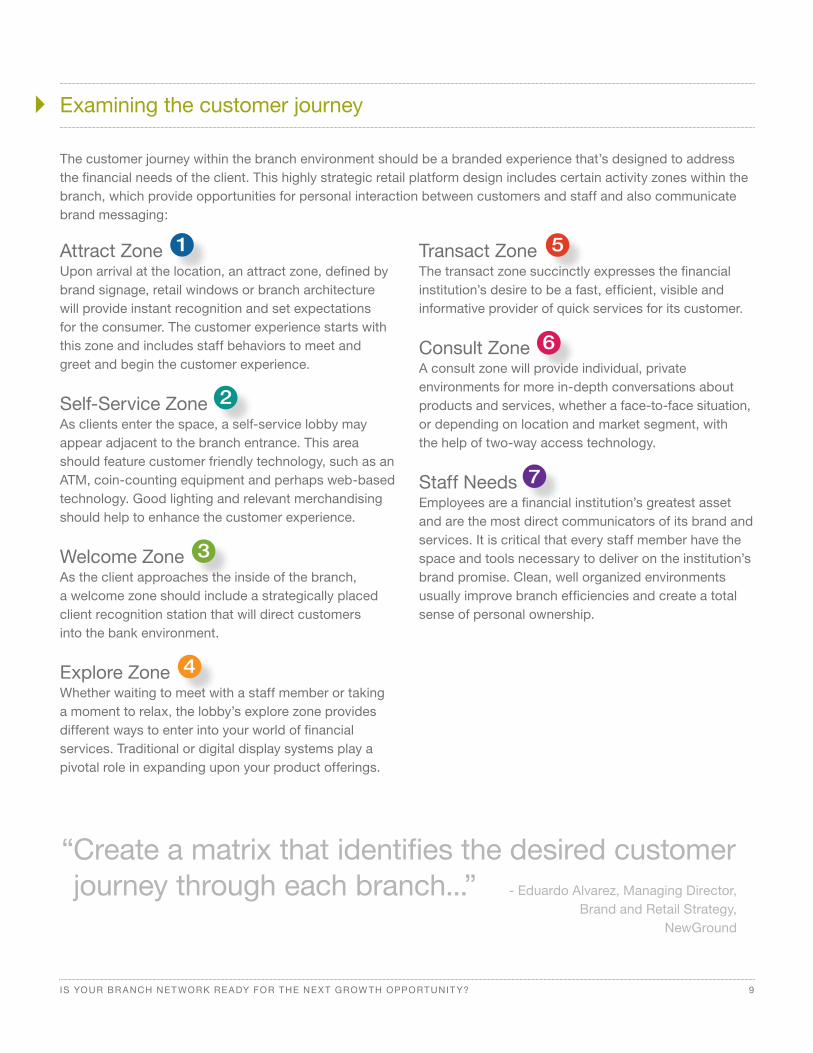

Attract ZoneUpon arrival at the location, an attract zone, defined by brand signage, retail windows or branch architecture will provide instant recognition and set expectations for the consumer. The customer experience starts with this zone and includes staff behaviors to meet and greet and begin the customer experience.

Self-Service ZoneAs clients enter the space, a self-service lobby may appear adjacent to the branch entrance. This area should feature customer friendly technology, such as an ATM, coin-counting equipment and perhaps web-based technology. Good lighting and relevant merchandising should help to enhance the customer experience.

welcome ZoneAs the client approaches the inside of the branch, a welcome zone should include a strategically placed client recognition station that will direct customers into the bank environment.

Explore Zonewhether waiting to meet with a staff member or taking a moment to relax, the lobby’s explore zone provides different ways to enter into your world of financial services. Traditional or digital display systems play a pivotal role in expanding upon your product offerings.

Transact ZoneThe transact zone succinctly expresses the financial institution’s desire to be a fast, efficient, visible and informative provider of quick services for its customer.

Consult ZoneA consult zone will provide individual, private environments for more in-depth conversations about products and services, whether a face-to-face situation, or depending on location and market segment, with the help of two-way access technology.

Staff NeedsEmployees are a financial institution’s greatest asset and are the most direct communicators of its brand and services. It is critical that every staff member have the space and tools necessary to deliver on the institution’s brand promise. Clean, well organized environments usually improve branch efficiencies and create a total sense of personal ownership.

The customer journey within the branch environment should be a branded experience that’s designed to address the financial needs of the client. This highly strategic retail platform design includes certain activity zones within the branch, which provide opportunities for personal interaction between customers and staff and also communicate brand messaging:

Examining the customer journey

“ Create a matrix that identifies the desired customer journey through each branch...” - Eduardo Alvarez, Managing Director,

Brand and retail Strategy, NewGround

10 IS YOUr Br ANCH NET wOrK rE ADY FOr THE NE x T GrOw TH OPPOrTUNIT Y?

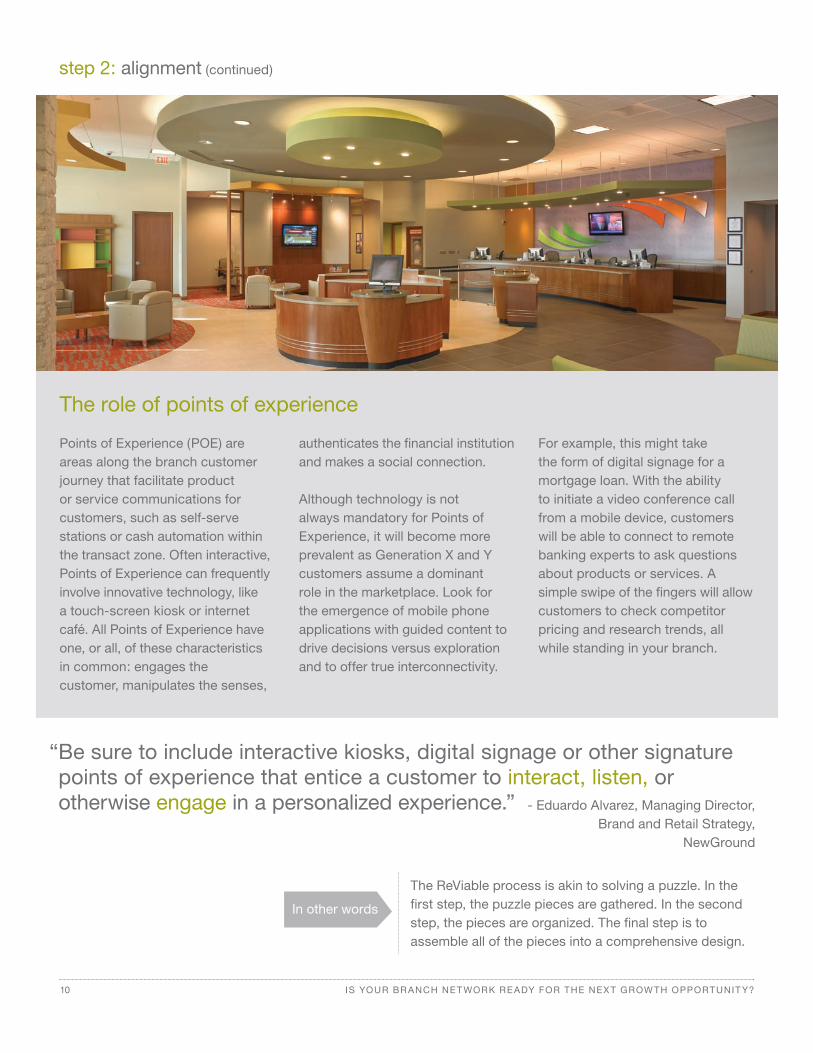

Points of Experience (POE) are areas along the branch customer journey that facilitate product or service communications for customers, such as self-serve stations or cash automation within the transact zone. Often interactive, Points of Experience can frequently involve innovative technology, like a touch-screen kiosk or internet café. All Points of Experience have one, or all, of these characteristics in common: engages the customer, manipulates the senses,

authenticates the financial institution and makes a social connection.

Although technology is not always mandatory for Points of Experience, it will become more prevalent as Generation x and Y customers assume a dominant role in the marketplace. Look for the emergence of mobile phone applications with guided content to drive decisions versus exploration and to offer true interconnectivity.

For example, this might take the form of digital signage for a mortgage loan. with the ability to initiate a video conference call from a mobile device, customers will be able to connect to remote banking experts to ask questions about products or services. A simple swipe of the fingers will allow customers to check competitor pricing and research trends, all while standing in your branch.

The role of points of experience

The reViable process is akin to solving a puzzle. In the first step, the puzzle pieces are gathered. In the second step, the pieces are organized. The final step is to assemble all of the pieces into a comprehensive design.

In other words

step 2: alignment (continued)

“ Be sure to include interactive kiosks, digital signage or other signature points of experience that entice a customer to interact, listen, or otherwise engage in a personalized experience.” - Eduardo Alvarez, Managing Director,

Brand and retail Strategy, NewGround

11IS YOUr Br ANCH NET wOrK rE ADY FOr THE NEx T GrOw TH OPPOrTUNIT Y?

step 4: implementation

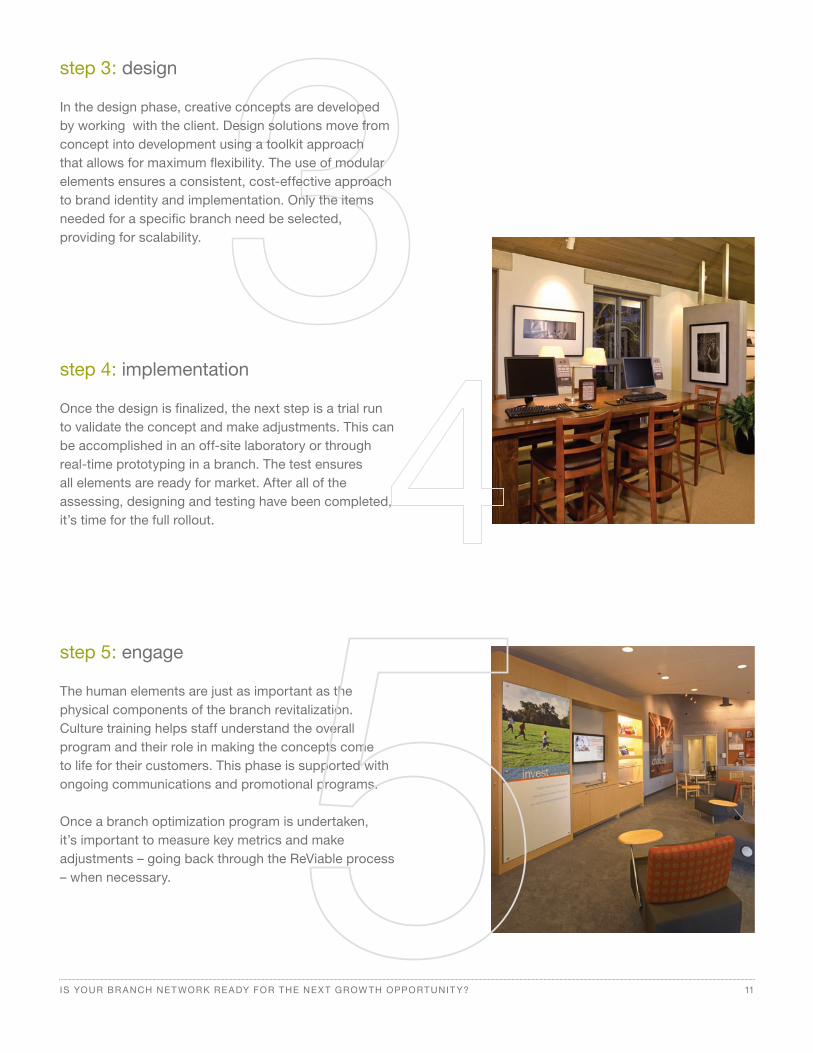

Once the design is finalized, the next step is a trial run to validate the concept and make adjustments. This can be accomplished in an off-site laboratory or through real-time prototyping in a branch. The test ensures all elements are ready for market. After all of the assessing, designing and testing have been completed, it’s time for the full rollout.

step 3: design

In the design phase, creative concepts are developed by working with the client. Design solutions move from concept into development using a toolkit approach that allows for maximum flexibility. The use of modular elements ensures a consistent, cost-effective approach to brand identity and implementation. Only the items needed for a specific branch need be selected, providing for scalability.

step 5: engage

The human elements are just as important as the physical components of the branch revitalization. Culture training helps staff understand the overall program and their role in making the concepts come to life for their customers. This phase is supported with ongoing communications and promotional programs.

Once a branch optimization program is undertaken, it’s important to measure key metrics and make adjustments – going back through the reViable process – when necessary.

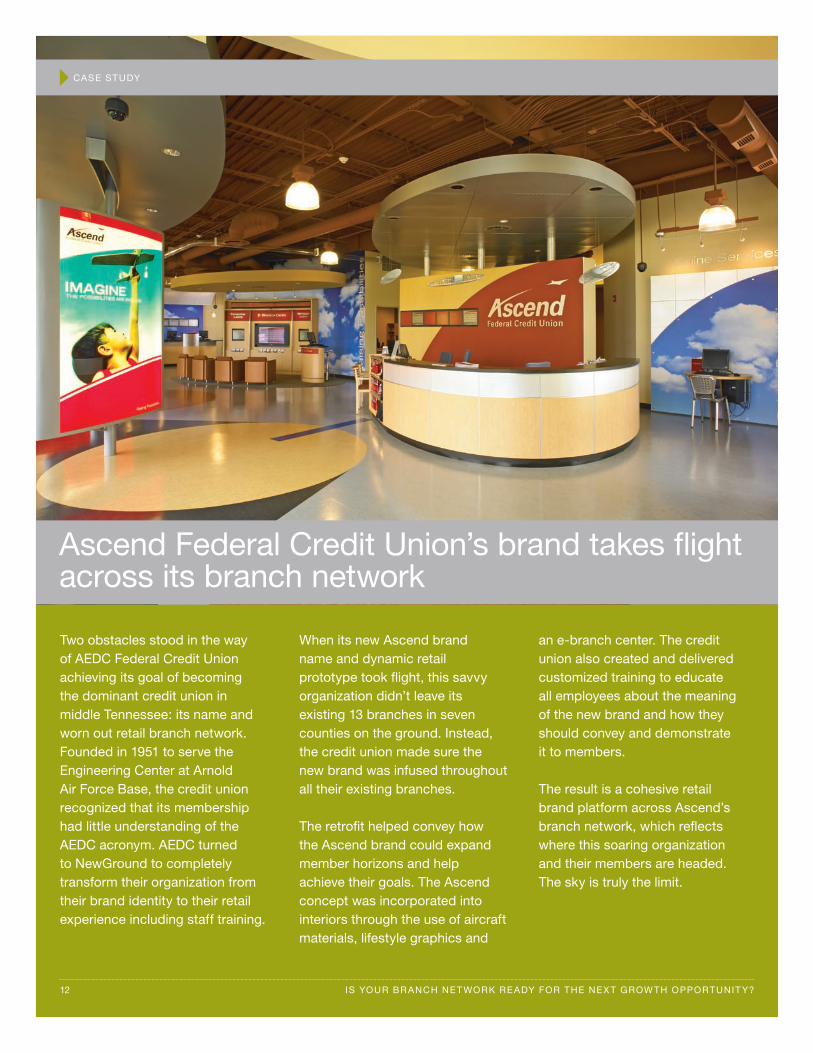

Two obstacles stood in the way of AEDC Federal Credit Union achieving its goal of becoming the dominant credit union in middle Tennessee: its name and worn out retail branch network. Founded in 1951 to serve the Engineering Center at Arnold Air Force Base, the credit union recognized that its membership had little understanding of the AEDC acronym. AEDC turned to NewGround to completely transform their organization from their brand identity to their retail experience including staff training.

when its new Ascend brand name and dynamic retail prototype took flight, this savvy organization didn’t leave its existing 13 branches in seven counties on the ground. Instead, the credit union made sure the new brand was infused throughout all their existing branches.

The retrofit helped convey how the Ascend brand could expand member horizons and help achieve their goals. The Ascend concept was incorporated into interiors through the use of aircraft materials, lifestyle graphics and

an e-branch center. The credit union also created and delivered customized training to educate all employees about the meaning of the new brand and how they should convey and demonstrate it to members.

The result is a cohesive retail brand platform across Ascend’s branch network, which reflects where this soaring organization and their members are headed. The sky is truly the limit.

Ascend Federal Credit Union’s brand takes flight across its branch network

12 IS YOUr Br ANCH NET wOrK rE ADY FOr THE NE x T GrOw TH OPPOrTUNIT Y?

CASE STUDY

13IS YOUr Br ANCH NET wOrK rE ADY FOr THE NEx T GrOw TH OPPOrTUNIT Y?

retailer revitalization programsThe financial services industry isn’t the only one looking to strengthen customer relationships and jump-start profits by revitalizing branch locations. retailers are launching extensive remodeling programs across their footprints, often on a more frequent cycle than the banking industry.

Burger King launched an extensive interior renovation of its 12,000 restaurants following the success of its innovative whopper Bar. The sleek, futuristic design is intended to create a cohesive style to visually link all Burger Kings. Burger King has found that remodeled restaurants consistently experience a 12 to 15 percent increase in sales.3

The design, which echoes the aggressive whopper Bar outlet look, is intended to attract young males, who make up the majority of the chain’s customers.

Holiday Inn has embarked on a $1 billion revamp across its hotel chain to attract business travelers. The holistic redesign includes increased quality inspections on all hotels with guidance to hotel owners on how to meet new standards, covering everything from entrance lighting, shower rods and lobby soundtrack to customer service training.

Joining the hotel chain in its refurbishing efforts is competitor Marriott International with a green sustainability redesign for its Courtyard sub-brand, which will be rolled out to sister brands, and a redesign of its SpringHill Suites brand, with environments that stimulate all the senses, creating a relaxing experience.

Target also jumped on the green bandwagon, rolling out new stores based on two prototypes developed in 2008, which have larger footprints with more space for food and electronics. Target unveils new prototypes every four to five years to freshen its look and better meet customer expectations.

3 “Burger King makeover: Fast food profits off franchisees’ whopping costs,” Daily Finance, Bruce watson, Oct. 8, 2009.

readiness is a constant, not a one-time event.

The reViable program allows a financial institution to get the most out of its existing retail distribution network. Set up correctly, the branch architecture allows for rapid deployment when customer needs and technology changes.

with the reViable program, your existing branch network can become a star performer. Each branch will be positioned to reach its full potential in today’s market and be ready to capitalize on emerging growth opportunities.

About NewGroundNewGround is a leading international design and implementation firm. For nearly a century, NewGround has been a premier provider of growth solutions, helping organizations advance by focusing on the design and delivery of customer and employee experiences. NewGround provides strategic solutions through the integration of their core offerings, which include: Brand, Consult, Design, Build, Retail and Culture.

The company’s headquarters are in St. Louis, MO, and corporate office in Chicago, IL; with principal offices in San Francisco, CA; Atlanta, GA; Portsmouth, NH; Cincinnati, OH; and Toronto, Canada.

To learn more about NewGround, call 888.613.0001, or visit www.newground.com.

©2011 NEwGrOUND. ALL rIGHTS PrOTECTED AND rESErVED.