national tax policy draft updated)

DESCRIPTION

Nigeria National Tax PolicyTRANSCRIPT

Draft Document on the National Tax Policy

DRAFT 1.1

(Revision Date: July 16, 2008)

Updated as at 16th July, 2008 ii

Presentation by the Presidential Committee on National Tax Policy

Updated as at 16th July, 2008 iii

Draft National Tax Policy

Executive Summary The National Tax Policy provides direction for the future of the Nigerian tax system in

order to help stimulate the economy in a way that will be of benefit to all Nigerians. In

achieving this goal, this document provides a set of guiding principles for all taxation in

Nigeria. It shall provide a stable point of reference for all stakeholders in the system and

a standard on which they would be held accountable. The following points are the

highlights of this document.

• The overriding objective of the National Tax Policy is to provide a stable point

of reference for all Stakeholders in the country on which they shall be held

accountable as this will facilitate economic growth and development.

• The taxes in the Nigerian tax system shall be few in number, broad-based

and high revenue-yielding.

• The overall Nigerian Tax System shall be fair, so that similar cases are

treated equally while different cases are handled based on their respective

peculiarity.

• There shall be a shift in the focus of the tax system from direct taxation to

indirect taxation. Nigeria should seek to have low rates of Companies Income

Tax and Personal Income Tax by international comparison. This would then

be accompanied by a gradual increase in the rate of Value Added Tax (VAT).

An increase in the emphasis on VAT and Customs duties should have an

upward effect on the country’s stable revenue base, at least from the

perspective of the ease of collection and yield.

Updated as at 16th July, 2008 iv

• Internal multiple taxation by the various tiers of Government on income,

property, imports, production and turnover should be avoided.

• The Nigerian tax system should minimise and streamline the number of tax

incentives and restrict their use to instances where they can help to achieve

the national objective of building an efficient tax system that encourages

voluntary compliance that cannot be achieved more efficiently in any other

way.

• The Ministry of Finance should be the body charged with providing oversight

function over the activities of the Tax/Revenue Authorities in Nigeria, as well

as being the sole authority responsible for Coordination of all inputs into

national tax policies, including the drafting of any amendments to laws or

legislations on taxation and revenues. Tax policy formulation must be the joint

responsibility of FIRS, Customs, NPC, NNPC and other Agencies.

• The power to impose, increase, reduce, vary or cancel any rate of tax should

be vested on the National Assembly with respect to all tax laws from the

Executive.

• The Joint Tax Board (JTB) should be strengthened as an Institution for the coordination of Personal Income Tax administration across Nigeria. By giving it legal powers to function as a policy making body for those taxes for which the administration is split across States, rather than merely an advisory body, will ensure an increase in collection efficiency.

• The Nigerian Tax System shall be subject to comprehensive review every

three (3) years. This review should not only be restricted to the existing tax

legislations i.e. CITA, PPTA, PITA, VATA, CGT etc; but cover all aspects in

relation to tax policy, administration and laws.

Updated as at 16th July, 2008 v

• Nigeria shall ensure that all the international tax obligations contracted by it

are respected. Nigeria shall also continue to pursue and expand its frontiers

on international tax treaties.

• Tax shall be collected only by career tax administrators, who are public

servants, and not by Consultants or Agents in ad-hoc capacity.

It is expected that the National Assembly shall be the guardian of Nigeria’s National

Tax Policy. Furthermore, after the approval of Nigeria’s National Tax Policy by the

Federal Executive Council, following consultations with the National Economic

Council (NEC), the Policy shall be implemented administratively, pending enactment

by the National Assembly and eventual inclusion in the constitution

Updated as at 16th July, 2008 vi

Sections Pages

1. Introduction 1-2

2. Objectives of the Nigerian Tax System and the features of a Good Tax 3-7 2.1 Objectives of the Nigerian Tax System 2.2 Features of a Good Tax System in Nigeria

3. Stakeholders in the Nigerian Tax System 8-13 3.1 Interrelationship between the Stakeholders in the

Development of a Good Tax System. 3.2 The Roles of the Stakeholders

in Developing a Good Tax Culture in Nigeria 3.3 Guiding Principles for all Stakeholders in the

Administration of Taxes in Nigeria

4. Policy and Administration 14-20 4.1 Funding of the Tax and Revenue Authorities 4.2 Capacity Building and Staff Training 4.3 Operation and Funding for Tax Refunds 4.4 Taxpayer Education 4.5 Self-Assessment 4.6 Tax Registration 4.7 Periodic Review of Existing Tax Laws and Legislations 4.8 Introduction of additional taxation 4.9 Power to vary the rates of tax 4.10 A shift away from direct taxation to indirect taxation 4.11 Centralisation of Revenue Authorities and the

Derivation Principle

5. Using the Tax System to Create Competitive Advantage 21-24 5.1 Reduction in the number of Effective Taxes 5.2 Internal Multiple Taxation 5.3 International Obligations and Double Taxation

Negotiations 5.4 Tax Incentives

6. Conclusions 25-26

Updated as at 16th July, 2008 vii

Appendices Appendix 1: Comparative Tax Rates in selected African Economies 27 Appendix 2: Strategy for Implementation of the Proposed Tax Policy 28-42 Appendix 3: Assessment of Tax Incentives 43-51 Appendix 4: Linkages for Effective Tax Policy 49

Updated as at 16th July, 2008 1

CHAPTER ONE

INTRODUCTION The National Tax Policy provides a set of rules, modus operandi and guidance to which all stakeholders in the tax system will subscribe. In line with the Federal Government’s economic reform agenda, the Federal Ministry of Finance, in collaboration with the Federal Inland Revenue Service has commenced the process of reform in the system of taxation in Nigeria. The development of the National Tax Policy is a crucial aspect of the reform process. The current reform process of the Nigerian Tax System commenced on 6th August 2002 when the Federal Ministry of Finance inaugurated a Study Group which examined the Tax system and made appropriate recommendations to entrench a better Tax Policy and improve Tax Administration in the country. The Study Group submitted its report in July 2003. Thereafter, a private sector-driven Working Group was constituted on 12 January 2004 to review the recommendations of the Study Group. Both the Study and Working Groups’ recommendations were further reviewed and commented upon by various stakeholders. Both groups addressed macro and micro issues in tax policy and administration. Among the macro issues discussed were the drafting of a National Tax Policy, Taxation and Federalism, Tax Incentives and Tax Administration generally. A clear outcome of the various meetings and consultations was a general agreement

that Nigeria is in urgent need of a National Tax Policy which will prescribe a set of

guiding principles and also provide a stable point of reference for all stakeholders in the

country and on which they shall be held accountable.

Updated as at 16th July, 2008 2

To this end, a sub-committee was commissioned to provide a blue-print of the National Tax Policy document for onward transmission to the Federal Ministry of Finance. It is expected that the National Assembly shall be the guardian of Nigeria’s National Tax Policy. Furthermore, after the approval of Nigeria’s National Tax Policy by the Federal Executive Council, following consultations with the National Economic Council (NEC), the Policy shall be implemented administratively, pending enactment by the National Assembly and eventual inclusion in the constitution.

Updated as at 16th July, 2008 3

CHAPTER TWO OBJECTIVES OF THE NIGERIAN TAX SYSTEM AND THE CHARACTERISTICS OF A GOOD TAX 2.1 Objectives of the Nigerian Tax System

The Nigerian Tax system should contribute to the well-being of all Nigerians. This can be accomplished both directly through improvements in the tax policy making process, and also indirectly through the utilisation of the revenues collected in judicious government spending.

Below are the stated objectives of a good Tax system which collectively should achieve the objective of stability and efficiency.

2.1.1 To enable economic growth and development.

The overriding objective of the Nigerian Tax system is to achieve economic growth and development. As such, the system should allow for stimulation of the economy and should not stifle economic growth. It is through sustained economic growth that the potential ability to offer improvements in the well-being of Nigerians will arise. However, where tax rates distort incentives for individuals to work or to save, or where the investment decisions of firms are distorted, then economic growth and development could be slowed down.

One of the objectives of the Nigerian Tax system shall be to cause as little disruption as possible to potential growth and development, whist meeting its revenue requirement.

Updated as at 16th July, 2008 4

2.1.2 To provide the government with stable resources that it shall invest in well-judged expenditures.

For Nigeria to pursue an active development agenda, or to even carry out the basic functions of government. Its tax system should be able to generate resources for government to provide basic public goods and services e.g. education, healthcare, infrastructure, security etc. The only sustainable way to achieve this is through the continual raising of revenues through taxation. It is therefore a primary objective of taxation to provide the government with such resources that it may invest in judicious expenditures that will ultimately improve the well-being of all Nigerians.

2.1.3 To provide economic stabilisation

Nigeria must seek to use its tax system to help in minimising the negative impacts of volatile booms and recessions in the economy and also to help complement the efforts of monetary policy in order to achieve economic stability.

2.1.4 To pursue fairness and distributive equity

Nigeria’s Tax system both in the present and future must be fair and concerned with pursuing both horizontal and vertical equity.

For Nigeria to focus on horizontal equity is to be concerned with equal treatment of equal individuals. The Nigerian Tax system should seek to avoid discrimination against economically similar entities to the fullest possible extent, in any new taxation policies and in the ways in which they are administered. Vertical equity will also address the issue of fairness among different income categories. The Nigerian Tax System shall recognise the ability-to-pay principle, in that individuals should be taxed according to their ability to bear the tax burden. Those with the highest absolute income should pay the highest absolute tax.

Updated as at 16th July, 2008 5

The overall Tax system shall be fair, so that similar cases are treated in similarly manner while different cases are handled differently.

2.1.5 To correct Market Failures or Imperfections

One of the objectives the Nigerian Tax System is the ability to correct market failures in cases where it is the most efficient device to employ. Market failures which the Nigerian Tax system may address are those that are as a result of externalities and those of natural monopolies.

2.2 Features of a Good Tax System in Nigeria

The following section provides the fundamental features for all taxes, which the Nigerian Tax system must exhibit. Where any of the criteria are not met in current or proposed tax legislations, serious debate should take place as to the desirability of such policies. In addition, any tax that violates several of these fundamental features shall not be part of the Tax System of Nigeria.

2.2.1 Simplicity, Certainty and Clarity.

Every person carrying out business in Nigeria must begin to truly trust the Tax system, and this can only be achieved if tax policy, at every level of Nigeria’s federal structure, endeavours to keep all taxes simple, creates certainty through considerable restrictions on the need for discretionary judgements, and produces clarity by educating the public on how the relevant tax laws impact on their lives.

It is therefore imperative that the Nigerian Tax system must be simple

(easy to understand by all), certain (its administration must be consistent) and clear (stakeholders must understand the basis of its imposition).

Updated as at 16th July, 2008 6

2.2.2 High Compliance Cost

To enable high compliance, the economic costs of time required, and the expense which a tax payer may incur during the procedures for compliance, shall be kept to the absolute minimum at all times. Furthermore, tax administrators shall be focused on treating taxpayer as a client who has a right to be treated well.

The convenience of the tax payer and minimal compliance cost shall guide the design and implementation of every tax in Nigeria.

2.2.3 Low cost of administration

A key feature of a good Tax system should be that the cost of administration must be relatively low when compared to the benefits derived from its imposition. The simpler the processes of a tax administration, the easier it will be for taxpayers to comply and the better for compliance. The more time and money spent on the collection of taxes, the greater the revenue expectation and the more potentials to cause distortion to economic growth. Therefore, the whole machinery of Nigerian Tax Administration should be efficient and cost-effective.

2.2.4 Fairness

All of Nigeria’s taxes should strive to observe the objective of horizontal and vertical equity as mentioned in section 2.1.4. The overall Nigerian Tax system shall be fair, so that similar cases are treated similarly, and different cases are handled differently.

Based on the foregoing, there must be overwhelming reasons for extending tax incentives and concessions to some preferred sectors over some other Sectors within the economy.

Updated as at 16th July, 2008 7

Where overwhelming reasons are presented for the exemption of any sector from the main provisions of the general tax law, it must serve to benefit the overall economy and not just the sector concerned.

2.2.5 Flexibility

Taxes in Nigeria should be flexible enough to respond to changing circumstances. Not only does this require pursuing new policies that are reflective of well-grounded economic reasoning, but it also requires the flexibility to change out-dated or inappropriate rates, or penalties for non-compliance, so as to establish and maintain the required incentives.

2.2.6 Economic Efficiency

Economic growth and development can be damaged where marginal tax rates distort incentives for individuals to work or to save, or where the investment decisions of firms are altered. Whilst many of the distortions are unavoidable, the extent to which they impact on the economy can be minimised. The Nigerian Tax System shall at all times strive to minimise the negative impacts of taxes on economic efficiency.

Updated as at 16th July, 2008 8

CHAPTER THREE STAKEHOLDERS IN THE NIGERIAN TAX SYSTEM Stakeholders include entities that contribute to and derive benefits from the country’s Tax system. This broad definition makes it difficult to imagine any individual, corporate entity or government agency as not being a stakeholder in the country’s tax administration. The relevant stakeholders in the Tax system of Nigeria can be broadly categorized into the: 1 Three Arms of Government

• Executives of the Federal, State and Local Government • The Legislature • The Judiciary

2 Tax and Revenue Authorities • Federal Ministry of Finance • FIRS, SBIR, JTB, State and Local Governments Revenue Committee and

Nigerian Custom Service

3 Tax Payers and Consultants • Nigerian Public (tax paying and non tax paying) • Corporate Organisations • Organised Private Sector • Trade Unions • Tax Consultants and Other Professionals

Updated as at 16th July, 2008 9

3.1 Interrelationship between the Stakeholders in the Development of a good tax system

The Ministry of Finance should be the body charged with providing the oversight function over the activities of Revenue Authorities in Nigeria, as well as being the sole organisation responsible for tax policy matters, including drafting any amendments to laws or legislations on taxation. All levels of Tax/Revenue Authorities which include FIRS and NCS shall account to the Federal Ministry of Finance and take directive from the Ministry. Also, no Government Ministry or organisation or persons will have the laxity to introduce new taxes without following due process i.e. through the Federal Ministry of Finance. There are of course specific Agencies of Government with responsibility for advising Government on Tax Policy direction. Some of these organisation include the National Planning Commission (NPC) and Nigerian Petroleum Corporation (NNPC). The NPC has a coordinating role on economic policy formulation of which National Tax Policy is a component. The respective States’ Tax and Revenue Authorities are also required to report to the State Government as represented by the States’ Ministry of Finance. The relationship between the Federal Tax Authorities as represented by the FIRS and the respective State Revenue Boards on tax related matters should be moderated through the Joint Tax Board (JTB). In addition, the JTB should in addition continue to play an advisory role to government whenever its opinion is sought. The Tax and Revenue Authorities should establish formal inter-agency cooperation with various Law Enforcement Agencies, such as the Nigerian Police. This becomes necessary in order to assist Tax Authorities to acquire skill, training and competences on investigation and enforcement activities in relation to the provisions of the enabling legislations, with respect to the problems of tax defaulters and recalcitrant taxpayers. Revenue authorities may also conclude information sharing agreements with EFCC, ICPC and SSS, in order that proper assessment can be made on taxpayers. Also, a more structured information-sharing arrangement shall be established between the Tax and Revenue Authorities on the one hand and government

Updated as at 16th July, 2008 10

bodies such as the Central Bank of Nigeria, Consultants, Nigerian Customs Service, Banks, NNPC, DPR, NDLEA, NAFDAC and the Ministry of Finance on the other hand. Finally, the different levels of government as well as the Tax and Revenue Authorities are expected to provide guidance and information to the tax paying public. This will elicit higher compliance and cooperation from the tax paying public.

A Pictorial Inter-relationship between all the Stakeholders in the Administration of taxes in Nigeria

Federal Ministry of

Finance

Office of the Accountant General of the Federation

Revenue Authorities

CBN, Tax Consultants, Professionals, Nigerian Customs Service, Banks

etc

Tax Paying Public

Law Enforcement Agencies e.g. Economic

& Financial Crime Commission, Nig Police

Joint Tax Board

NNPC

Tax Proceeds

NPC

Updated as at 16th July, 2008 11

3.2 The Roles of the Stakeholders in developing a Good Tax Culture in Nigeria

All the stakeholders in the Nigeria Tax System have critical roles to play in the

development of an efficient Tax administration in Nigeria. We state hereunder the respective roles that each of these stakeholders have

to play. 3.2.1 The Role of the Executive arm of Government

The executive arm of government; be it at the Federal, State and Local levels, plays an indirect yet crucial role in the development of a good tax culture in Nigeria. This is because they are not empowered to directly legislate on tax matters (The Legislature is the only law making body in Nigeria). However, the Ministry of Finance shall have the sole responsibility to propose to the Legislature any amendment or addition to existing and new Tax Legislation. This centralisation of the system for proposing tax policy by the Ministry of Finance will enable sustained co-ordination in the number and thrust of tax legislations being passed to the legislature for ratification.

The executive arm of government at the respective levels, are also saddled with the function of encouraging voluntary tax compliance by the tax payers. An effective mechanism for achieving this high compliance by the respective government level is by making the most efficient use of the tax revenue collected by them.

3.2.2 Role of Federal and State Legislatures / Judiciary

The Constitution of the Federal Republic of Nigeria vests the powers to make laws on the taxation of income or profits on the legislative arm of the government comprised of the Senate and the House of Representatives. It shall therefore be the constitutional responsibility of the National Assembly to make tax laws or amend existing laws, after

Updated as at 16th July, 2008 12

obtaining the recommendations from the Federal Ministry of Finance. Item 7 of the concurrent Legislative List restricts the states to the assessment and collection functions only.

The Judiciary on the other hand is saddled with the responsibility of interpreting and adjudicating on tax matters.

3.2.3 Role of the Tax / Revenue Authorities

The administration of the various tax laws is under the care and management of the Tax and Revenue Authorities as represented by the FIRS, the respective States Internal Revenue Service, the JTB etc. Apart from the general administration of taxes (assessment and collection of taxes), including accounting for the taxes collected. Revenue authorities are also saddled with the responsibility for advising government on treaty negotiation isues. In the Nigerian Tax System, tax shall be collected only by career tax administrators, who are Civil Servants, and not by ad hoc consultants or agents. Similarly, only self assessments or assessments by tax administrators shall be allowed in Nigeria.

In addition, the Tax Authorities also ensure that in carrying out its tax assessments and collection role, every claim, objection, appeal, representation or the like made by any tax payer are sufficiently considered by it. This will ensure that tax payers have confidence in the tax administration system in the country.

Finally, the Tax and Revenue Authorities at all levels are expected to provide guidance to the taxable public. This guidance could come in the form of information circulars, bulletins and newsletters.

3.2.4 Role of the Taxpayers

The taxpayers have a very significant role to play in the administration of tax in Nigeria. Apart from making the correct tax returns and

Updated as at 16th July, 2008 13

payments, as required under the law, they are expected to, from time to time provide the Tax/Revenue Authorities with useful information and suggestions that could assist in improving tax practices in the country.

3.3 Guiding Principles for all Stakeholders in the Administration

of Taxes in Nigeria.

There are certain universal principles which are necessary to ensure a convivial interaction between the stakeholders in the administration of taxes in Nigeria. These principles are:

• affirmation and acknowledgement of all stakeholders’ importance and

contributions; • provision of specific and general proactive feedback on issues and

developments that are relevant to tax administration; • ensuring that the principle of good faith is enshrined by all stakeholders,

especially between the tax payer and the Tax / Revenue Authorities on the one hand and the government and the tax authorities on the other hand;

• fairness in the treatment of all stakeholders by each other. This is especially so in the area of respecting each party’s viewpoints and in the allocation of resources.

3.4 Linkages for Effective Tax Policy

There should be solid linkages between the various Stakeholders in the tax system. These are persons, organisations and associations whose responsibilities are mainly to influence the achievement of voluntary tax compliance generally. A suggested linkage relationship is demonstrated in appendix 4.

Updated as at 16th July, 2008 14

CHAPTER 4 POLICY AND ADMINISTRATION Tax administration in Nigeria is shared across the three-tiers of government. One of the core success factors for any policy is enshrined in its position on policy and administrative issues. An effective tax policy document should be one that establishes a flawless position on crucial tax administration and policy issues. In the context of the Nigerian Tax Policy, the important administration and policy issues and the official position and recommendation on such issues are stated below: 4.1 Funding of the Tax and Revenue Authorities 4.1.1 It shall be the responsibility of the Government to provide adequate funding

arrangement for Tax and Revenue Authorities in Nigeria. In order to ensure that the Tax and Revenue Authorities in the country are well funded, Government at all levels shall ensure the following:

(i) That a sufficient proportion of revenue collected by any Revenue Authority,

as judged by international comparisons with well-funded, efficient tax systems, shall be provided to cater for its administration;

(ii) That any unspent portion of such fund allocation in any year shall be returned back to Government.

(iii) That all other government revenue-generating establishments shall receive a commensurate sum of money which will be adequate to administer their operations effectively.

(iv) That not less than 10% of total revenue collection by Tax/Revenue Authorities shall be appropriated each year by the NASS to FIRS in order to cater for refund requests from taxpayers.

It is believed that if all tax and revenue organs receive adequate funding as enunciated above, the administration of taxes by these organs will be greatly enhanced.

Updated as at 16th July, 2008 15

There is therefore the need to institutionalise this arrangement in the Federal tax statutes, as well as replicate it at the State Revenue authority level.

4.2 Capacity Building and Staff Training

The Government is committed to achieving high level of technical training and capacity building of all the tax and Revenue officials in the country.

In furtherance of this commitment, Government shall pursue the following policies: (i) Develop an adequately funded Tax Academy which will be established

for the primary purpose of capacity building of all revenue officials. (ii) Every revenue official (at least from middle management level and

above) shall be adequately exposed to international training on taxation, revenue administration and practice.

(iii) Provide a framework that ensures that every Revenue official is fully

acquainted with the global best practice of taxation. 4.3 Operation and Funding for Tax Refunds

4.3.1 Tax Refund Mechanism

Taxpayers are required to apply for refunds in respect of any excess tax paid to the Government. To be eligible for such refund, a genuine case of overpayment must be established by the taxpayer.

The Revenue authority is required to subject all claims for refund to sufficient verification and must honour ALL genuine refunds within 90 days of the decision of the Service.

4.3.2 Source of Funding for Tax Refund

All Tax and Revenue Authorities who are saddled with tax refund obligations shall meet these obligations both diligently and efficiently. Therefore, all Tax Authorities shall request sufficient funding from the

Updated as at 16th July, 2008 16

National Assembly or State House of Assembly (whichever is relevant) in their budgetary allocation, in order to meet these expected refund obligations.

4.4 Taxpayer Services and Education 4.4.1 It is the responsibility of the Tax Authority to constantly educate taxpayers on the

relevant aspects of the Tax System. This is based on the knowledge that once the taxpayer is sufficiently educated and enlightened, the cost of tax administration would be significantly reduced. Therefore, all Tax and Revenue Authorities will take responsibility for explaining their taxes and making them clear to all. There is a need for each of the Tax and Revenue Authorities to develop a comprehensive strategy on taxpayer services of which taxpayer education will be a key component, these strategies must then be reviewed and approved by the Joint Tax Board (JTB) on a yearly basis.

4.5 Self-Assessment

All the Tax and Revenue Authorities in Nigeria shall embrace Self-Assessment, and should put in place structures that will guarantee the realisation of true Self-Assessment. A successful self-assessment scheme can be achieved on the condition of existence of a reliable tax-data bank, on which tax authority can rely upon for the determination of taxpayers’ claims. Government should devote resources for data bank development.

4.6 Tax Registration

Every company and taxable persons shall be registered for tax purposes. The Federal Revenue Authority is required to issue a Tax Identification Number (TIN) upon the registration by taxpayers for taxes. This TIN, via Information Communication Technology will guide and provide insights into all the tax activities of the tax payers. This will ultimately reduce the cost of administration and supervision while enhancing higher compliance.

4.7 Periodic Review of Existing Tax Laws and Legislations

Updated as at 16th July, 2008 17

The Nigerian Taxation System shall be subject to a general review every year and subject to a comprehensive review every three years. The comprehensive review will not only be restricted to all the existing tax legislations i.e. CITA, PPTA, PITA, VATA, CGT etc; but would cover all aspects of tax administration and tax policy matters. The recommended five (5) yearly review of the tax administration system shall ensure conformity with the dictates of economic and business trends as well as with international trend. The comprehensive review shall set out plans and time-frames for any recommended reforms, as well as establishing the persons responsible for their implementation. This review exercise shall bring up tax matters requiring reform to the attention of the Minister of Finance.

4.7.1 To create an environment conducive for trade and investment, the tax laws and

regulations must be predictable and certain in their interpretation and applications. Tax Authorities must ensure that they comply with tax laws and regulations in their determination of tax cases.

4.8 Introduction of Additional Taxation

The Ministry of Finance is the sole body saddled with the responsibility of proposing amendments to all tax and revenue laws and legislations for consideration by the legislators. Therefore, it is the Minister’s responsibility to see that any additions to the existing tax laws and legislations shall meet as closely as possible with the criteria for good taxation as highlighted in this document. Any tax that violates several of the features of a good tax will not be part of the Tax system of Nigeria. Before any significant alteration is made to the Tax System, there shall be broad and detailed consideration on the potential economic impact of the proposed alteration(s). As part of this, the Ministry of Finance shall commission a study on the potential economic impact of any proposed alteration to the existing tax laws seeking recommendations from the relevant Revenue Authorities and stakeholders with the ultimate aim of assessing the extent to which the tax meets the criteria of the National Tax Policy.

Updated as at 16th July, 2008 18

4.9 Power to vary the tax rates Tax rates must be responsive to fiscal developments within the economy, and it is the Executive arm of government that is charged with the responsibility for managing the fiscal affairs of the nation. The Presidency or Finance Ministry may propose tax rate variation, but this will not become law until such proposal is supported and approved by the National Assembly. This is important and aims at checking any possible arbitrariness on the part of the Executive in matters of tax rates variation. It is therefore recommended that the power to vary tax rates should be vested only in the National Assembly with respect to all taxes.

4.10 A shift away from Direct taxation to Indirect taxation.

The current policy of shifting away from direct taxation to indirect taxation with respect to non-oil taxes is to pursue the goal of encouraging economic growth by decreasing direct taxes, whilst still meeting revenue requirements. Nigeria should therefore seek to have low rates of Companies Income and Personal Income taxes by all international comparison. This will be accompanied by a gradual increase in the rate of Value Added Tax VAT). An increase in the emphasis on VAT will have an upward effect on the country’s stable revenue base. The tax system should regularly look at the consumption side in order to strike a balance between savings investment and consumption. This is because VAT offers a more regular revenue flow and has huge prospects for improve tax compliance. Table1: VAT rates in selected ECOWAS countries

Country Benin Cote

D'Ivoire Ghana Mali Niger Nigeria Senegal Togo VAT Rate (%) 18 18 15 18 19 5 18 18

There is great demand for harmonisation in VAT legislations across the ECOWAS sub-region. This is part of a fiscal transition strategy by ECOWAS countries to achieve: (i) a more efficient inland tax collection system based more heavily on

indirect taxation. (ii) A reduction in economic distortions in sub-regional integration policies and

international conventions on trade liberalisation.

Updated as at 16th July, 2008 19

For Nigeria to be in the middle level of the ECOWAS group, it should look towards having an average VAT rate in a way that will not affect aggregate consumption. Many economists are quick to point out the inequitable and inflationary nature of indirect taxes, but they nevertheless always admit that it is a programatic solution to the problem of tax evasion and avoidance.

4.11 Coordination of Tax Authorities by the Joint Tax Board

The Nigerian Constitution is clear on the role of the Federal Government in matters pertaining to tax legislation. The Constitution grants the Federal Government through the National Assembly, the powers to impose any tax or duty on:

(a) Capital Gains, Incomes or profits of persons and companies; and (b) Documents or Transactions by way of Stamp Duties However, for efficient tax administration and by virtue of the concurrent legislative provisions, States were given administrative and collecting powers in regards to certain taxes, the most significant of which is Personal Income Tax. The Joint Tax Board (JTB) should be a strong and effective regulatory institution over the shared activities of all the Federal and States Tax authorities. This is in order to allow greater coordination of Personal Income Tax, and which will make compliance easier for taxpayers, as well as increase future tax collections. The JTB should be able to provide technical assistance and support to the State Boards of Internal Revenue, as well as providing standardised processes for the filing and collection of Personal Income Tax across the whole of Nigeria. This requires that the JTB should have extended authority to be more than just an advisory Board and should have the authority to make decisions on the administrative processes of Personal Income Tax. All decisions of Joint Tax Board must necessarily be subject to the final approval of the Minister of Finance in order to comply with due process requirement.

Updated as at 16th July, 2008 20

This process of empowering the JTB may require updating the relevant section in the Personal Income Tax Act so that the objective of achieving an efficiently administered Personal Income Tax across the whole of Nigeria is attained.

4.12 Tax Appeal Process

The appeal process must be strengthened so that an aggrieved taxpayer can have an avenue for redress and thereby have confidence in the fairness of the Tax System. Dispute Resolution function should be established in support of the appeal process as a way of reducing court delays and avoiding exorbitant legal costs.

4.13 Ratification of International Treaties

In order to improve the image or the economic interests of Nigeria, tax treaty matters must be taken more seriously by all Government Agencies having responsibilities for the function. The Foreign Affairs must facilitate the process of negotiation through official channels; ratification process is normally handled by FMF to the Council Secretariat for FEC approval before the submission to National Assembly for domestication. The whole process should be smooth and devoid of delay, particularly by the National Assembly.

Updated as at 16th July, 2008 21

CHAPTER 5 USING TAX SYSTEM AS A TOOL IN CREATING COMPETITIVE ADVANTAGE The Nigerian Tax System’s central objective as enunciated in Chapter Two is to encourage economic growth and development. This implies that the Tax System must also focus on growth facilitation in both foreign and domestic investment. Nigeria should therefore use the Tax System as one of the many tools for achieving a competitive advantage for investment. This competitive advantage will emerge if the business climate in Nigeria becomes superior to the business climate in other countries. The concern of businessmen over multiplicity of taxation must be addressed properly. The Joint Tax Board needs to re-double efforts in this regard. Below are the ways that taxes can be utilised as a means of fostering competitive advantage. 5.1 Reduction in the Number of Effective Taxes

The taxes in the Nigerian Tax System shall be few in number, broad-based and high revenue-yielding. This will enable the emergence of a far superior Tax System than an overly-complicated one with many relatively low revenue-yielding taxes. This will also in no small way enable easier monitoring and supervision.

5.2 Internal Multiple Taxation

Internal multiple taxation by the various tiers of Government on income, property, imports, production and turnover shall be avoided. The Joint Tax Board (JTB) shall ensure the coordination of taxation across Nigeria to avoid the multiplicity of taxes.

5.3 Liberalisation of Import Duty Regime With the adoption of the Common External Tariff (CET), sanity shall be restored to Customs administration. Government will purse the Port Reform programme to conclusion.

Updated as at 16th July, 2008 22

5.3 Strengthening of the Oil and Gas Sector Government shall encourage the Production Sharing Contracts in the Oil and Gas Sector in order to reduce the demand for cash calls. More transparency and accountability will be the guiding rules in the industry.

5.4 International Obligations and Double Taxation Negotiations

Nigeria shall ensure that all the international tax obligations contracted by it are respected. Nigeria shall also continue to pursue and expand on international tax treaties. Nigeria is committed to contributing to the goal of expanding trade within the Economic Community of West African States (ECOWAS). Therefore, the Tax System should strive to actualise this commitment by realising a common trade and competition policy in West Africa. Imposing tax on income which has been subjected to tax in another jurisdiction (Double Taxation) is harmful to economic growth. Therefore, Nigeria shall avoid fully taxing the incomes of companies, enterprises or individuals whose income has already been taxed in another country. Nigeria shall expand on the number of tax treaties it has with new countries in order to alleviate the problems of double taxation. This expansion will lead to greater certainty for firms and individuals operating both inside and outside of Nigeria and will improve the inflow of Foreign Direct Investment into the country.

5.5 Tax Incentives

Nigeria, like many other countries, has tried to make use of a plethora of tax incentives to try and nurture specific sectors that are regarded as key sectors. However, tax incentives, by their nature, on several occasions, come in conflict with the principles of good taxation because they; (i) Discriminate in favour of a particular sector thus violating horizontal equity

considerations;

(ii) Require a heavier tax burden from the other sectors in order to maintain a given revenue requirement, undermining fairness; and

Updated as at 16th July, 2008 23

(iii) Over-complicate the tax system, making it more expensive to monitor the beneficiaries of such incentives, therefore increasing the possibilities for tax evasion.

There is an urgent need to review the entire process of granting tax waivers/concessions with respect to custom duties, Value Added Tax, Pioneer Exemption status etc. The law at present requires that an Order must be issued by the present requires that an order must be issued by the President to make such waivers/exemptions valid. The Federal Ministry of Finance, working with the Justice Ministry should always ensure that the applicable Orders are issued and gazetted in support of any tax waivers/exemptions. This is not to say that the use of tax incentives to attract investment is not recognised. An efficient tax system must be capable of providing such incentives, which should provide benefits to all, rather than few. Also, as a matter of policy, a Technical Committee of Government, comprising of all relevant Ministries, Departments and Agencies should have responsibility for making recommendation to the Federal Executive Council (FEC) on Waivers/Exemption. The pertinent issue for discussion are the terms of reference of the Waiver/Exemption Technical Committee, location of its secretariat and funding sources. There had been a few instances where, corporate entities engaged in business and paying taxes to Government were suddenly granted Pioneer tax exemption status. This kind of concession should be frowned upon and discouraged. The Nigerian Tax System will minimise and streamline the number of tax incentives and restrict their use to instances where they help achieve a national objective that cannot be achieved more efficiently in any other way. Without prejudice to the stand of NIPC and NEPC, Government should se-emphasise tax incentives and should rather place more emphasis on the creation of enabling environment for trade, business and investment. Tax incentives should be comprehensively reviewed and those which create a greater burden on the economy than their benefit or, serve to unnecessarily complicate the Tax System, should be removed.

Updated as at 16th July, 2008 24

Included in appendix three is a comprehensive list of tax incentives in the Nigerian Tax System, some of which are difficult to implement and monitor. They complicate the Tax System and often investors are not aware of their existence. Therefore some of them are recommended to be removed or altered.

Updated as at 16th July, 2008 25

CHAPTER SIX CONCLUSION This National Tax Policy document has set out the fundamental objectives of the

Nigerian Tax System and has prescribed the qualities that must be embedded within all

future tax laws. That the Tax System must currently be focused on the main objective of

enabling economic growth and development is a reflection of the deep-rooted need for

improving the per capita income of Nigerians.

This document has stated the roles of stakeholders in the Tax System and the

interactions between them. The issue of high compliance by the taxpayers for all taxes

is of vital importance. The Tax Authority can encourage higher compliance if the

taxpayers are treated as clients and if the whole system of taxation is made simpler and

clearer. The need for mutual respect between all stakeholders in the Tax System is also

a crucial element in providing a modern functioning Tax System.

A major impact of this document should be the further empowerment of the Ministry of

Finance to take oversight of the administrative aspect of the Tax System. The links

between Tax Administration and Tax Policy are so interwoven that considering either

one of these in isolation of the other will risk great policy errors. For a successful and

coordinated mass reform of the Tax System, the Federal Ministry of Finance shall

assume a pivotal role.

Another policy thrust of this document is the need for greater administrative coordination

of the collection of revenues from Personal Income Tax by the JTB. The benefits of the

improved coordination are in terms of both higher compliance and increased efficiency.

Updated as at 16th July, 2008 26

A major policy outcome of this document is the commitment of Nigeria to increase the

role of indirect tax. The increased focus on VAT should be intrinsically linked to

decreases in the rates of Personal Income Tax (PIT) and Companies’ Income Tax (CIT)

because of its ease in administration. This policy change, in addition to the overall

simplification of the Tax System, will encourage the establishment of a good business

environment in Nigeria.

Finally, this document has highlighted various tax related issues in creating a good

business environment within the country. In particular, with tax incentives it has shown

the need for a restrained approach to allowing well-intended incentives into the Tax

System. The process of reducing the number of different incentives in the system and

coordinating and harmonising the remaining incentives to common rates shall be an

ongoing process of government.

Overall, this document has provided a set of guiding principles for all taxation in Nigeria.

It shall provide a stable point of reference for all stakeholders in the Tax System to refer

to, and a standard on which stakeholders shall be held accountable.

Updated as at 16th July, 2008 27

Appendix One Comparative Tax Rates in Selected African Economies Table 1: Value-Added Tax Rates in selected ECOWAS countries

Table 2 Income Tax Rates of Key African Economies

Nigeria Ghana Kenya South Africa

COMPANIES/ CORPORATE INCOME TAX

Tax rate 30% (20% for

manufactures, mining, agric, export)

25% 30% 29%

PERSONAL INCOME TAX

Personal allowance =N=5,000 + 20% $5,634

Top rate of tax 25% 25% 30% 40%

Threshold (US$)

1,260

960 5,500

40,000

Country Benin Cote

D'Ivoire Ghana Mali Niger Nigeria Senegal Togo VAT Rate (%) 18 18 15 18 19 5 18 18

Updated as at 16th July, 2008 28

Appendix Two

STRATEGY FOR IMPLEMENTATION OF THE PROPOSED TAX POLICY

Executive Summary

The Tax Strategy for Nigeria is a document mapping out the way the Federal Government of

Nigeria (FGN) intends to achieve a tax system that will significantly encourage investment

within the Nigerian economy, leading to more jobs and higher economic growth. This will be

achieved through the following measures;

Using revenues from Nigeria’s Oil wealth to alleviate the tax burden on companies, in order to diversify the economy.

Gradually decreasing Companies Income Tax to 20 percent by 2009.

Decreasing the top-rate of Personal Income Tax to 17.5 percent by 2009.

Shifting towards greater reliance on indirect taxation through gradually increasing Value-Added Tax to a rate that will not affect aggregate consumption by 2009, in line with achieving stable non-oil revenue flows and to achieve high compliance in the tax system .Also fulfilling commitments to ECOWAS.

Restricting Tax Holidays to sectors key to Nigeria’s development of basic infrastructure.

Decreasing the cost of compliance with tax obligations through simplification of tax laws, regular review process, improving taxpayer services and developing specific taxation regimes for effectively dealing with Small and Medium Enterprises i.e. Presumptive Income Taxation and prescription of a turnover threshold in Value-Added Tax operation.

Eliminating multiple taxation through improved collaboration between FIRS and Joint Tax Board (JTB), and empowering the JTB to have coordinating powers for taxation.

All these strategies should be pursued by the FGN, and where necessary, the appropriate

amendments to the tax laws should be pursued.

Updated as at 16th July, 2008 29

Table of Contents

Section

1.0 Introduction

2.0 Objectives 2.1 Domestic Investment 2.2 Foreign Investment 2.3 Employment

3.0 Creating a Competitive Advantage in Nigeria’s Tax System 3.1 Adjusting rates to Encourage Investment 3.2 Decreases in Income Tax Rates 3.3 Deliberate Policy Shift towards Indirect Taxation 3.4 Simplifying the Tax Laws to Encourage investment 3.5 Pioneer Status/ Tax Holidays for Developing Infrastructure 3.6 Export Processing Zones (EPZs) 3.7 Import and Excise Duties – CET

3.8 Strengthening the Oil and Gas Tax Regime

4.0 Taxation of Small and Medium Enterprises

4.1 Presumptive Income Taxation 4.2 Value-Added Tax (VAT) Threshold

5.0 Large Taxpayers

6.0 Elimination of Multiple Taxation

7.0 Conclusion

PPTRoyalty

Updated as at 16th July, 2008 30

List of Tables and Charts

Table/ Chart Page No.

Chart 1: Foreign Direct Investment inflows in

ECOWAS countries as at 2004 - 2

Table 1: Components of Total Revenue in Key

African Economies - 4

Table 2: Income Tax Rates in Key African

Economies - 4

Table 3: Rates of VAT in selected ECOWAS

Countries - 5

Updated as at 16th July, 2008 31

1.0 Introduction

The Tax Strategy for Nigeria is an accompanying document to the National Tax Policy.

Whilst the National Tax Policy highlights crucial rules, principles and specifies the

destination to which the tax system should be moving towards, the Tax Strategy for

Nigeria maps out the way in which the country will get there.

The tax system in any country is the key link between the private and the public sector in

growing and shaping the economy. There is no single tax system that can be said to be of

universal ‘best practice’, so the optimal public/ private sector mix of an economy will

depend on the differing circumstances of each country. However, there are general

principles of best practice that should be applied in the context of each country even

though they may require different paths to be taken. The Tax Strategy for Nigeria is an

attempt to do exactly that; to apply good principles of taxation that are tailor made to

Nigeria’s particular circumstance.

2.0 Objectives

The objective of the Tax Strategy for Nigeria is to use the tax system to help grow

investment and create employment; this is part of the intention of Government to grow

the Nigerian economy by an average of at least 10% per annum. All this must be

achieved whilst maintaining stable revenues to enable sustainable Government

expenditure.

2.1 Domestic Investment

Investment arises when companies and enterprises are able to see a likelihood of

future profits through sinking their money into projects at the present time. There

are many costs involved in any investment project which makes the project less

profitable and will impact on whether a firm takes the decision to proceed with it.

Nigeria's poor infrastructure makes investment projects costly, and will make

many investment decisions less likely to be taken than they would in other

countries with better infrastructure.

Updated as at 16th July, 2008 32

High taxation on any income will also make a project less likely to be undertaken as overall profits will be lower and companies will be more reluctant to take the investment risk. In the short to medium term, in order to try and compensate for poor infrastructure, the tax system should allow companies and enterprises higher post tax profits to increase the likely benefits of taking investment risks. This will lead to higher domestic investment from companies and result in higher economic growth.

2.2 Foreign Investment

As a member of ECOWAS, Nigeria is faced with the prospect that in the not too distant future, firms will, on a tariff free basis, have access to selling their products in Nigeria's market without having to actually locate in Nigeria.

When the free-trade zone and common external tariff are established, companies may choose to locate in any of the other ECOWAS countries, and will choose the country in which it is most profitable for them to do so. Foreign Direct Investment (FDI) has many benefits, compared to those derived from merely importing goods and services. Greater FDI can lead to higher employment, transfer of knowledge and skills (which will lead to further economic growth), as well as various other positive multiplier effects from the investment. Nigeria must strive to be competitive and therefore attractive for foreign firms to invest in. Chart 1 below, demonstrates the FDI inflow that the current ECOWAS member States had in 2004. As can be seen, Nigeria stands out by far the highest. However, the overwhelming majority of this is likely to be linked to the Oil and Gas sector. Nigeria needs to focus on being an attractive place for investment in the real sector.

Updated as at 16th July, 2008 33

For those foreign companies investing in natural resource extraction, there is little choice where they will locate. If the infrastructure is poor they are forced to adapt to it in order to locate where the resources are; however for foreign companies in the real sector, this is not a constraint. Nigeria's poor infrastructure will put the country at a significant disadvantage compared with ECOWAS countries that are in better infrastructural positions. To try and counter this disadvantage, Nigeria should make use of the tax system to make it more beneficial than other countries for investment.

2.3 Employment

Through policies that encourage increases in both domestic and foreign investment, will come greater employment opportunities in Nigeria. This will help distribute the benefits of economic growth. It is therefore through creating a Tax Strategy that encourages investment that higher employment will be achieved.

3.0 Creating a Competitive Advantage in Nigeria's Tax System

In order to achieve the objectives stated under Section 2, Nigeria must have a long-term objective of providing a good level of infrastructure as a significant way of creating a good business environment. In the short to medium term, where it may not be possible for the Government to provide the quality of infrastructure on the scale needed, it should seek to achieve the objective by making good use of the tax system. This can be done by decreasing the burden of taxation on companies and enterprises.

3.1 Adjusting Rates to Encourage Investment

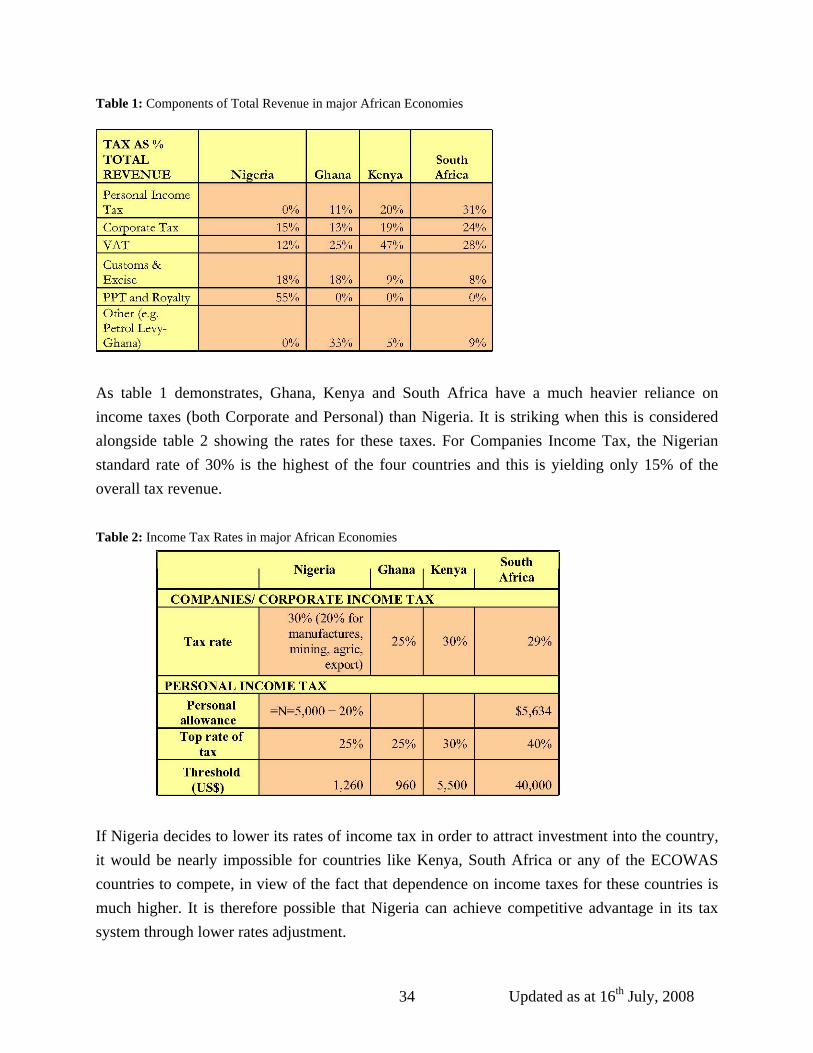

Nigeria has immense Oil and Gas resources which give the country a great opportunity to create fewer burdens on the real sector of the economy and still be able to finance the Government's expenditure budget. By comparing the proportion of revenues which Nigeria receives from Oil and Gas with those received by other African economies, it is clear that Nigeria can achieve competitive advantage for the real sector through its tax system.

Updated as at 16th July, 2008 34

Table 1: Components of Total Revenue in major African Economies

As table 1 demonstrates, Ghana, Kenya and South Africa have a much heavier reliance on income taxes (both Corporate and Personal) than Nigeria. It is striking when this is considered alongside table 2 showing the rates for these taxes. For Companies Income Tax, the Nigerian standard rate of 30% is the highest of the four countries and this is yielding only 15% of the overall tax revenue.

Table 2: Income Tax Rates in major African Economies

If Nigeria decides to lower its rates of income tax in order to attract investment into the country, it would be nearly impossible for countries like Kenya, South Africa or any of the ECOWAS countries to compete, in view of the fact that dependence on income taxes for these countries is much higher. It is therefore possible that Nigeria can achieve competitive advantage in its tax system through lower rates adjustment.

Updated as at 16th July, 2008 35

3.2 Decrease in Income Tax Rates

Based on the reasons stated so far, the strategy of Government is to reduce the rate of Companies Income Tax to 20% by 2009.

For Personal Income Tax, the strategy will be to eventually bring the top rate down to 17.5% of taxable income by 2009.

By lowering the rates of income taxes, not only will investment be encouraged, there will also be significant benefits in improving compliance from companies and individuals. The tendency for non-compliance will be significantly reduced if the tax required is smaller and the penalties for non-compliance are reasonable and not punitive.

Furthermore, it is important that there are not big differences in the rates of Companies Income Tax and Personal Income Tax in order to limit opportunities for tax avoidance.

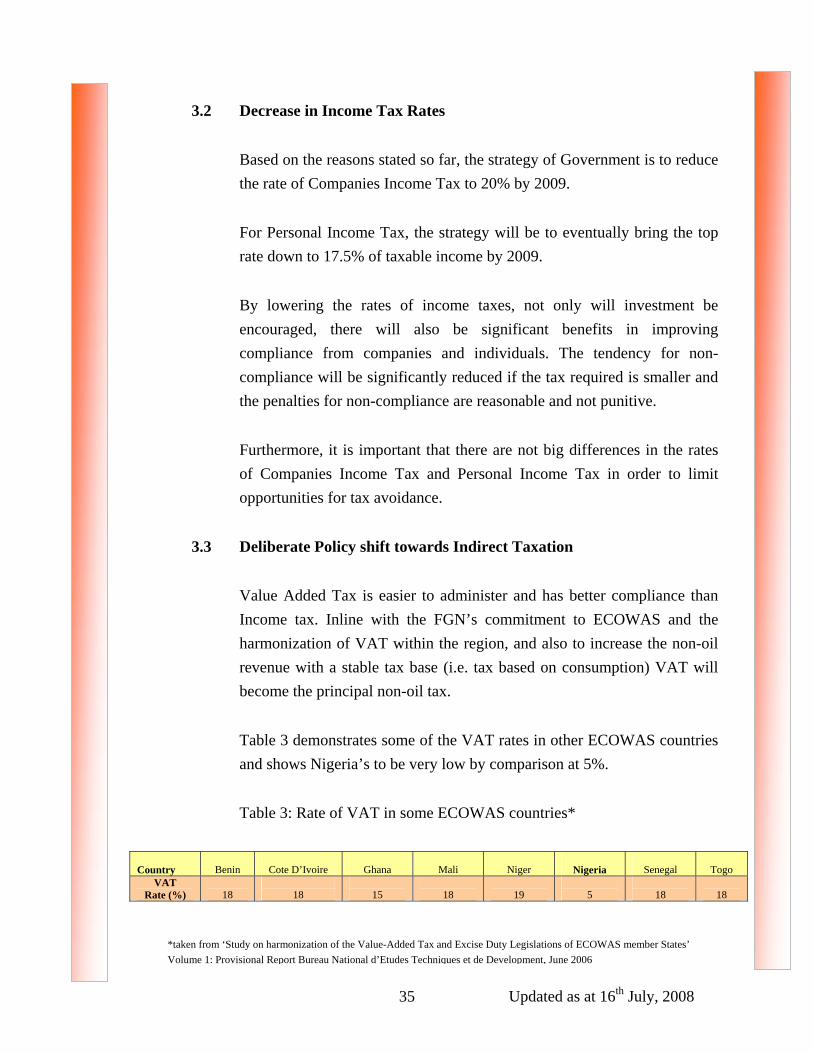

3.3 Deliberate Policy shift towards Indirect Taxation

Value Added Tax is easier to administer and has better compliance than Income tax. Inline with the FGN’s commitment to ECOWAS and the harmonization of VAT within the region, and also to increase the non-oil revenue with a stable tax base (i.e. tax based on consumption) VAT will become the principal non-oil tax.

Table 3 demonstrates some of the VAT rates in other ECOWAS countries and shows Nigeria’s to be very low by comparison at 5%.

Table 3: Rate of VAT in some ECOWAS countries*

Country Benin Cote D’Ivoire Ghana Mali Niger Nigeria Senegal Togo VAT

Rate (%)

18

18

15

18

19 5

18

18

*taken from ‘Study on harmonization of the Value-Added Tax and Excise Duty Legislations of ECOWAS member States’ Volume 1: Provisional Report Bureau National d’Etudes Techniques et de Development, June 2006

Updated as at 16th July, 2008 36

In order to start addressing the issues stated above, Government should begin to embark on a gradual increase in the rate of VAT in such a way that it will not affect aggregate consumption by 2009. This will make the revenues accruing from Companies and Personal Income Tax even less important than they currently are, and further goes to provide opportunities for using the tax system in order to increase both domestic and foreign investment.

With these increases in VAT, it is important to adhere to the principle of vertical equity (as articulated in the National Tax Policy document) which implies that those on the lowest incomes should not be impacted on by VAT increases as much as those on higher incomes. In order to achieve this, it is crucial to maintain a relevant list of basic necessity goods which should remain VAT-exempt or zero-rated, such as basic foods, health goods and services, educational materials etc.

3.4 Simplifying the Tax Laws To Encourage Investment

In order to encourage investment, it is necessary but not sufficient to lower the overall rates of key taxes. Part of the tax burden that falls on taxpayers is the administrative duties that are necessary to comply with the tax laws. Complicated tax laws increase the cost for taxpayers to comply with their tax obligations, many may have to employ special tax consultants at a cost to their business, and others may have to spend a lot of time trying to work out what the law is requiring from them. The tax laws must be very clear to taxpayers, and this is achieved through good taxpayer education, and having a system which is simple enough for most people to understand. As a result, the FGN is striving to make the tax system simpler by removing out-dated or under-utilised tax incentives (this is addressed comprehensively in the National Tax Policy). Furthermore, all Tax and Revenue collecting authorities in Nigeria should adopt wide-spread Taxpayer Education Strategies.

3.5 Pioneer Status / Tax Holidays for Developing Infrastructure

Horizontal equity is a key condition for fairness in a tax system. Under this concept, similar companies are treated similarly through the provisions of the tax laws. A Tax Holiday (or Pioneer Status) violates horizontal equity because it involves treating a

Updated as at 16th July, 2008 37

company or sector with preferential treatment over other companies or sectors.

This goes to both complicate and undermine confidence in the tax system, as well as

foregoing potentially substantial revenues. In general, any such provision is not

compatible with an ideal tax system.

However, whilst these type of tax incentives should generally be avoided; there are some

specific sectors involved with key infrastructure development that the FGN should make

an exception to. The justification for this is that they are involved in sectors that have

potentially large benefits to society at large, such as Public goods that are usually

provided by the Government. Where the FGN has not made sufficient provision for

certain infrastructures, it will be of immense benefits to provide Pioneer Status to help

facilitate the private sector to bridge these gaps. This fulfils the requirements stated in the

National Tax Policy Document that tax holidays must only be provided where there is no

other more efficient way to achieve the particular national objective.

By targeting infrastructure sectors, this will reinforce the policy to encourage investment

in Nigeria, as through improved infrastructure the cost of investments in general shall

decrease.

The following key infrastructure sectors should be provided with tax holidays under

Companies Income Tax;

• Power Sector • Railways/Roads Development • Education • Health • Aviation • Gas

Furthermore, there are sectors which should be given tax holidays because of the

competition they face in heavily competitive global markets;

• Exports • Agriculture

A key feature of all these tax holidays should be that they are not unlimited. They should

be time bound. The current situation has been to allow pioneer status for three years with

Updated as at 16th July, 2008 38

the potential for them to be extended for another two years if deemed appropriate by the

FGN. This policy should be retained as adequate for almost all sectors, and will provide a

realistic time-period for reappraisal.

Careful checks and balances must be in place to make the obtaining of tax holidays a

rigorous process. It should be restricted purely to those companies and sectors where

there is overwhelming evidence that no other policy would be as effective in achieving

substantial investment in that sector.

3.6 Export Processing Zones (EPZs)

In order to sustain the FGN’s policy which is directed at to encouraging export-oriented

industry, and to address some of the major administrative concerns that are associated

with the Export Processing Zones (EPZs), the following suggestions should be looked

into:

1) The FGN should provide a special tax holiday of seven years from Companies

Income Tax as opposed to the usual maximum of five years, this will allow

companies to be able to commit significant investment in Nigeria. Where

Withholding Tax is paid on dividends and interest, this should represents the final

tax payment.

2) Value-Added Tax on products produced in these zones for export will remain

zero-rated in order to allow these companies to claim back the input VAT from

Federal Inland Revenue Service (FIRS).

3) All companies located within the EPZ should continue to file Companies Income

Tax returns even where no tax is payable.

4) There should be no import or export levy or any form of taxation within these

zones, except where the entities transact business outside the EPZ.

5) Contrary to Decree 63 (of 1992) no percentage of EPZ production shall be

allowed into the country. Any firms located in EPZ but desirous of wanting to sell

to the domestic market should be made suffer tax on the profit realized from sales

outside the EPZ.

The fifth provision for the EPZs is due to the great difficulties in taxing those elements of

Updated as at 16th July, 2008 39

production that are sold in the domestic market but are produced in the EPZs. This will

make the EPZs fully effective and straight-forward to administer. It is recognized that

there are firms who may have been attracted to the EPZ due to servicing the Nigerian

Market, they will have to relocate, however the FGN should ensure a suitable

compensation package is made available to them.

3.7 Import and Excise Duties

In order to reduce costs of Nigerian manufacturers, and therefore to help make them more

competitive and cheaper for Nigerian consumers, the FGN should make moves (where

not contradictory to ECOWAS commitments) to reduce Import Duties on raw materials

to zero percent. This will encourage the production of both intermediate and finished

goods, which will develop the Nigerian economy further.

Furthermore, in order to encourage the Aviation Industry, the import duties on Aircraft

needs to be made competitively low.

3.8 Strengthening Oil and Gas Tax Regime

The fiscal regime for oil and gas, particularly the Petroleum Profit Tax (PPT), which

applies to Oil producers under Joint Venture contracts (JV) or the more recent Production

Sharing Contracts (PSC) require proper strengthening in view of its growing importance.

As a matter of necessity to ensure transparency and accountability, all Agencies of

Government charged with administration and collection of Oil & Gas revenues e.g.

NNPC, FIRS, NAPIMS and DPR should share information on regular basis in order to

optimize PPT collection. In addition, steps should be taken towards the codification of all

legislations applicable in the Oil and Gas Sector. This will prevent the continued reliance

on unilateral Ministerial orders or presidential side letters which often override the

statutes. As a matter of oil administration policy, all matters affecting taxation, deductible

costs and revenues should by commonly agreed between Government and all the

Agencies charged with responsibility for PPT collection.

4.0 Taxation of Small and Medium Enterprises

Compliance has been a great problem in the Nigerian Tax System, and this largely stems

Updated as at 16th July, 2008 40

from the large scale of Nigeria’s informal economy. The administrative burden of the

provisions of general tax laws may be too much for these companies, and therefore

efforts should be made to deal effectively and efficiently with them. This involves

strategies to increase both compliance and revenues whilst keeping the cost of

administration as low as possible.

4.1 Presumptive Income Tax

For those Small and Medium Enterprises that have historically failed to comply with the

tax laws, possibly due to their size and lack of a fixed business address, a simplified

Income Tax shall be applicable. This tax, known as a Presumptive Tax, will require much

less of an informational burden on the taxpayer, and will result in a quick and effective

method of providing an assessment. The method for such Income Taxation will be tightly

controlled and clear guidelines will be issued so that there is limited room for discretion

on the tax inspector’s part.

4.2 Value-Added Tax (VAT) Threshold

In order to establish effective administration of VAT, the Federal Inland Revenue Service

(FIRS) shall operate a threshold of company and enterprise turnover, below which there

will be no obligation to charge or remit VAT. The appropriate turnover threshold level

will be decided by the FIRS and will eventually be introduced.

Any entity with turnover level above the decided threshold should be fully complying

with the provisions of the VAT Act, and this will be strongly enforced.

This threshold level does not oblige these companies and enterprises to not collect VAT

if they wish to recoup their input VAT. However, if they do wish to receive their input

VAT they must be fully registered and complying with the regular monthly returns to

their Integrated Tax Office.

5.0 Large Taxpayers

Good progress has been made in taxing Large Taxpayers with the establishment of the

FIRS Large Tax Offices (LTOs). These LTOs have enabled the development of

specialists in dealing with the biggest contributors to Income Tax Revenues. The FGN

Updated as at 16th July, 2008 41

will ensure that even closer relationships are established with the largest taxpayers in

order to ensure full compliance and to minimise tax avoidance and evasion. The

simplification of the tax laws and better taxpayer services as expressed in section 4.2,

together with a strong and effective tax enforcement programs will all help ensure that

biggest taxpayers are maximizing their role in the Nations development.

6.0 Elimination of Multiple Taxation

Multiple taxation from Federal, State and Local Government has been very harmful to

the investment climate of Nigeria. Much of this is attributable to the political system and

is the result of the current inability to coordinate between the various Government levels.

In order to correct these failures, there is need for the relationship between the Federal

Inland Revenue Service (FIRS) and the Joint Tax Board (JTB) to be strengthened.

Furthermore, legislation should be pursued that empowers the JTB to have coordinating

powers for taxation across Nigeria rather than only acting as an information sharing

body. This will help minimize the harmful circumstances where businesses are forced to

pay multiple taxes on the same income, or where consumers will have to pay multiple

taxes on the same expenditure. 7.0 Conclusion

Through the strategies developed in this document, Nigeria will be making the most

effective use of its tax system given the particular situation of the economy i.e. Large oil

revenues and inadequate infrastructure. Through strategies such as reducing both

Companies and Personal Income Tax, the tax climate in Nigeria will be substantially

better for encouraging both domestic and foreign investment, and this will go someway to

compensate for some of the deficiencies in infrastructure that companies operating in

Nigeria are currently facing.

The strategy is focused at pushing Nigeria forward as a competitive economy in Africa

and will help ensure that the country will not lose out on inward investment with the

establishment of the free-trade zone and customs union of ECOWAS.

Finally, it is a sustainable strategy in the sense that it is making use of an unsustainable

Updated as at 16th July, 2008 42

resource (i.e. Oil reserves) in order to build up a sustainable real sector of the economy.

The FGN should now start the process to begin reflecting these strategies in the various

legislations, and seek to quickly pass the appropriate amendments. Investment is needed

not for its own sake, but for the sake of improving the living standards of Nigerians.

Through this investment will come more jobs, higher wages and competitive prices. All

this should hopefully provide for a more promising and prosperous future for all

Nigerians.

Updated as at 16th July, 2008 43

Appendix Three

Appraisal of Existing Tax Incentives Category 1

S/N Description of Concessions

Relevance/Application Rates of Concessions / Comments

Relevant Tax Section in Statute

i. In-Plant Training Applicable to industrial establishments that have set up in-plant facilities

2% of cost incurred is deductible

Not Available

ii. Investment in Infrastructure

Applicable to industries that provide facilities which should have been provided by Government e.g. pipe-borne water supply and electricity

20% of the cost of providing the facilities is deductible

iii. Investment in Economically Disadvantaged areas

Applicable to industries sited in economically disadvantaged Local Government areas.

Tax holiday of 7 years in addition to 5% capital allowances over and above the initial capital allowances

iv. Labour intensive mode of production

Applicable to industries with high labour/capital ratio. Such industries should employ more persons than plants to qualify.

Employment of 1,000 persons or more enjoys 15% of cost of plant. Graduated rates apply

v. Local Value Content Aimed at encouraging local fabrications rather than the mere assembly of completely knocked down parts (CKD)

10% cost of assets for a period of five (5) years

vi. Utilisation of Minimum Local Raw Materials

Applicable to industries that attain the minimum level of local raw materials sourcing and utilization as follows: Agro-Allied - 70% Engineering- 60% Chemicals- 60% Petro-chemicals- 70%

Tax credit of 20% of cost is granted for a period of five (5) years.

All the concessions described above are difficult to implement and monitor. They are cosmetic in nature and investors are often not aware of their existence.

Updated as at 16th July, 2008 44

Category 2

Manufacturing Companies S/N Description of

Concessions Relevance/Application Rates of Concessions /

Comments Relevant Tax Section

i. Incentive for Manufacturing Companies

Small Companies Relief

1. Companies with less than N1.0m annual turnover to pay tax at the rate of 20% during the first five years.

Comment: Distortionary concession to be abrogated from the status. All companies should pay at the same tax rate. 2. Dividends from small

manufacturing companies are exempted from income tax during the first 5 years.

Comment: From experience, small companies distribute dividends to their owners. To be abrogated from the status.

CITA – S19(1)(O)

ii. Research & Development expenses

Research & Development expenses are now deducted for tax purposes in the relevant year. The cost is to be treated as capital.

Research & Development expenses should be treated as normal operational expenses rather than accorded the status of capital assets in addition.

CITA – S22(1-2)

iii. Cement Producers For Cement producers in order to encourage them to increase production and reduce prices.

Two (2) years exemption from Income tax Comment: To be abrogated. Difficult to implement and monitor.

Budgetary IDA – S10

Updated as at 16th July, 2008 45

iv. Locally made spare parts

Manufacturers of locally made spare parts, tools and equipment

The 25% investment tax credit on equipment purchased. Comment: to be repealed.

CITA – S28(F)(1-2)

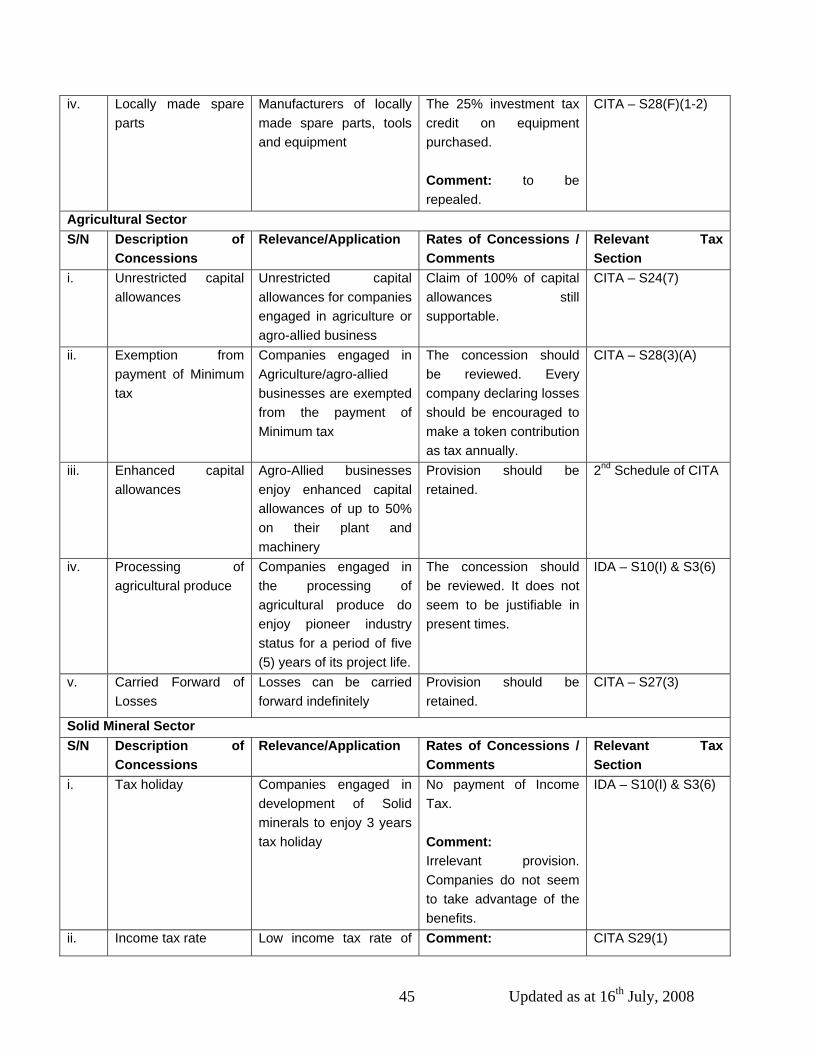

Agricultural Sector S/N Description of

Concessions Relevance/Application Rates of Concessions /

Comments Relevant Tax Section

i. Unrestricted capital allowances

Unrestricted capital allowances for companies engaged in agriculture or agro-allied business

Claim of 100% of capital allowances still supportable.

CITA – S24(7)

ii. Exemption from payment of Minimum tax

Companies engaged in Agriculture/agro-allied businesses are exempted from the payment of Minimum tax

The concession should be reviewed. Every company declaring losses should be encouraged to make a token contribution as tax annually.

CITA – S28(3)(A)

iii. Enhanced capital allowances

Agro-Allied businesses enjoy enhanced capital allowances of up to 50% on their plant and machinery

Provision should be retained.

2nd Schedule of CITA

iv. Processing of agricultural produce

Companies engaged in the processing of agricultural produce do enjoy pioneer industry status for a period of five (5) years of its project life.

The concession should be reviewed. It does not seem to be justifiable in present times.

IDA – S10(I) & S3(6)

v. Carried Forward of Losses

Losses can be carried forward indefinitely

Provision should be retained.

CITA – S27(3)

Solid Mineral Sector S/N Description of

Concessions Relevance/Application Rates of Concessions /

Comments Relevant Tax Section

i. Tax holiday Companies engaged in development of Solid minerals to enjoy 3 years tax holiday

No payment of Income Tax. Comment: Irrelevant provision. Companies do not seem to take advantage of the benefits.

IDA – S10(I) & S3(6)

ii. Income tax rate Low income tax rate of Comment: CITA S29(1)

Updated as at 16th July, 2008 46

between 20% - 30% The provision is distortionary and should be abrogated. All companies should be assessed to tax at a single of 30%.

iii. Deferred royalty payment

Deferred royalty payment depending on the magnitude of investment for companies engaged in solid mineral development.

Comment: Provision should be reviewed. Level of investment to be achieved before qualifying for the benefit not specified.