monetary policy and sovereign debt vulnerability€¦ · government renounces the ability to...

TRANSCRIPT

Monetary Policy and Sovereign Debt Vulnerability1

Galo Nuño & Carlos Thomas

Banco de España

XVII Annual Inflation Targeting Seminar, Banco Central do BrasilMay 21 2015

1These slides represent the authors’views and does not necessarily represent those ofBanco de España

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 1

/ 26

Motivation: European debt crisis

Legacy of 2007-9 financial crisis: large fiscal deficits and soaringgovernment debt

Before summer 2012, sovereign yields rose sharply in EMU periphery(GR, IR, IT, PT, SP) ...

... but not in other highly indebted countries (US, UK, etc.)

Many argue a key difference is: US-UK can deflate debt away, EMUperiphery countries cannot

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 2

/ 26

Motivation: role of monetary policy

What role, if any, should monetary policy play in guaranteeingsovereign debt sustainability?

Arguments for and against monetary policy involvement:

provide ’monetary backstop’against default fearscreating inflation also entails costseffect on inflation expectations (and yields) if low monetary credibility

This paper: analyze trade-offs between price stability and sovereigndebt sustainability...

... when gov’t cannot make credible commitments

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 3

/ 26

Framework of analysis

Small open-economy, continuous-time model

Benevolent government issues nominal defaultable debt to foreigninvestors

Gov’t may default on debt at any time

costs of default: exclusion from capital markets + output loss

Government chooses fiscal (primary deficit) and monetary policy(inflation) under discretion

Benefits and costs of inflation:

debt can be deflated awaydirect welfare losses

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 4

/ 26

Preview of results

Calibrate to average peripheral EMU economy

Analyze two monetary regimes:1 inflationary regime: benevolent gov’t chooses inflation discretionarily2 no inflation regime: zero inflation at all times

In (2), government gives up option to deflate debt away

issue foreign currency debtjoin monetary union with strong anti-inflation mandate

Main result: Welfare is higher in no inflation regime, for any debtratio and on average

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 5

/ 26

Literature review

Links between sovereign debt vulnerability and monetary policy

Aguiar et al. (2013, 2015), Corsetti and Dedola (2013): self-fulfillingdebt crises (à la Calvo,1988; Cole and Kehoe, 2000)

Optimal fundamental sovereign default in quantitative models

Aguiar and Gopinath (2006), Arellano (2008), etc.

Extend literature on continuous-time models of default to the pricingof defaultable nominal sovereign debt

Merton (1974), Leland (1994)

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 6

/ 26

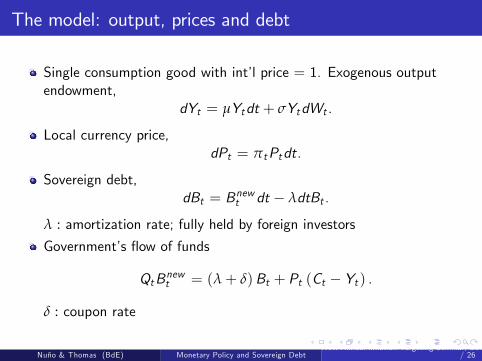

The model: output, prices and debt

Single consumption good with int’l price = 1. Exogenous outputendowment,

dYt = µYtdt + σYtdWt .

Local currency price,dPt = πtPtdt.

Sovereign debt,dBt = Bnewt dt − λdtBt .

λ : amortization rate; fully held by foreign investorsGovernment’s flow of funds

QtBnewt = (λ+ δ)Bt + Pt (Ct − Yt ) .

δ : coupon rate

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 7

/ 26

The model: output, prices and debt

Single consumption good with int’l price = 1. Exogenous outputendowment,

dYt = µYtdt + σYtdWt .

Local currency price,dPt = πtPtdt.

Sovereign debt,dBt = Bnewt dt − λdtBt .

λ : amortization rate; fully held by foreign investorsGovernment’s flow of funds

QtBnewt = (λ+ δ)Bt + Pt (Ct − Yt ) .

δ : coupon rate

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 7

/ 26

The model: output, prices and debt

Single consumption good with int’l price = 1. Exogenous outputendowment,

dYt = µYtdt + σYtdWt .

Local currency price,dPt = πtPtdt.

Sovereign debt,dBt = Bnewt dt − λdtBt .

λ : amortization rate; fully held by foreign investors

Government’s flow of funds

QtBnewt = (λ+ δ)Bt + Pt (Ct − Yt ) .

δ : coupon rate

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 7

/ 26

The model: output, prices and debt

Single consumption good with int’l price = 1. Exogenous outputendowment,

dYt = µYtdt + σYtdWt .

Local currency price,dPt = πtPtdt.

Sovereign debt,dBt = Bnewt dt − λdtBt .

λ : amortization rate; fully held by foreign investorsGovernment’s flow of funds

QtBnewt = (λ+ δ)Bt + Pt (Ct − Yt ) .

δ : coupon rate

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 7

/ 26

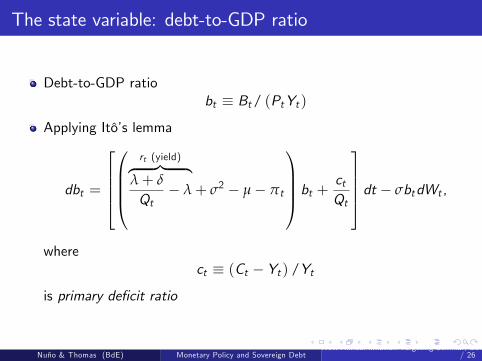

The state variable: debt-to-GDP ratio

Debt-to-GDP ratiobt ≡ Bt/ (PtYt )

Applying Itô’s lemma

dbt =

rt (yield)︷ ︸︸ ︷λ+ δ

Qt− λ+ σ2 − µ− πt

bt + ctQt

dt − σbtdWt ,

wherect ≡ (Ct − Yt ) /Yt

is primary deficit ratio

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 8

/ 26

The state variable: debt-to-GDP ratio

Debt-to-GDP ratiobt ≡ Bt/ (PtYt )

Applying Itô’s lemma

dbt =

rt (yield)︷ ︸︸ ︷λ+ δ

Qt− λ+ σ2 − µ− πt

bt + ctQt

dt − σbtdWt ,

wherect ≡ (Ct − Yt ) /Yt

is primary deficit ratio

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 8

/ 26

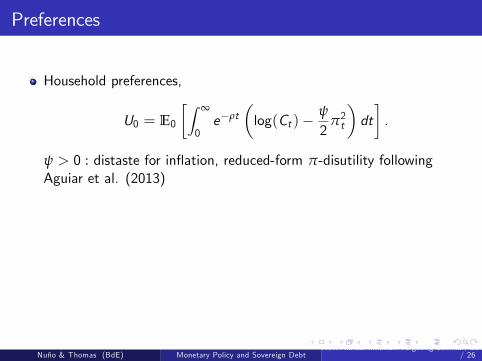

Preferences

Household preferences,

U0 = E0

[∫ ∞

0e−ρt

(log(Ct )−

ψ

2π2t

)dt].

ψ > 0 : distaste for inflation, reduced-form π-disutility followingAguiar et al. (2013)

Using Ct = (1+ ct )Yt ,

U0 = E0

[∫ ∞

0e−ρt

(log(1+ ct )−

ψ

2π2t

)dt]+ V aut0 ,

where V aut0 = E0[∫ ∞0 e

−ρt log(Yt )dt]is the (exogenous) autarky

value

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 9

/ 26

Preferences

Household preferences,

U0 = E0

[∫ ∞

0e−ρt

(log(Ct )−

ψ

2π2t

)dt].

ψ > 0 : distaste for inflation, reduced-form π-disutility followingAguiar et al. (2013)

Using Ct = (1+ ct )Yt ,

U0 = E0

[∫ ∞

0e−ρt

(log(1+ ct )−

ψ

2π2t

)dt]+ V aut0 ,

where V aut0 = E0[∫ ∞0 e

−ρt log(Yt )dt]is the (exogenous) autarky

value

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 9

/ 26

Fiscal and monetary policy

At each point in time, choose

default or continue repaying debt ⇔ optimal default threshold b∗

primary deficit ratio (ct ), inflation rate (πt )

under discretion (take investor’s pricing scheme Q (b) as given)

First analyze default scenario

Then lay out general optimization problem

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 10

/ 26

The default scenario

Default (at a debt ratio b) implies

exclusion from capital markets (reenter at rate χ)and contraction in output endowment (in logs, εmax{0, b− b})

At end of exclusion period, gov’t reenters markets with debt ratio θb

Value of defaulting (net of autarky value),

V def (b) = −εmax{0, b− b}ρ+ χ

+χ

ρ+ χV (θb) .

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 11

/ 26

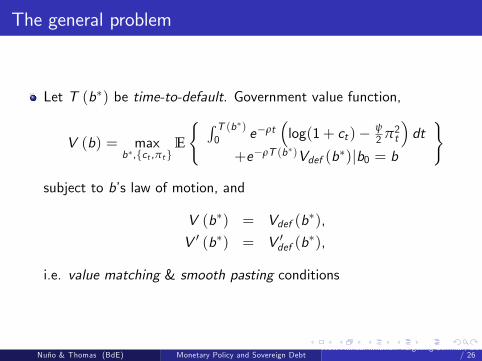

The general problem

Let T (b∗) be time-to-default. Government value function,

V (b) = maxb∗,{ct ,πt}

E

{ ∫ T (b∗)0 e−ρt

(log(1+ ct )− ψ

2π2t

)dt

+e−ρT (b∗)Vdef (b∗)|b0 = b

}

subject to b’s law of motion, and

V (b∗) = Vdef (b∗),

V ′ (b∗) = V ′def (b∗),

i.e. value matching & smooth pasting conditions

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 12

/ 26

The ’no inflation’regime

Consider an alternative scenario where

π (b) = 0

for all b.

Government renounces the ability to deflate debt away

Possible interpretations:

Issue foreign currency debtJoin a monetary union with a strong anti-inflationary stance(Appoint extremely conservative central banker)

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 13

/ 26

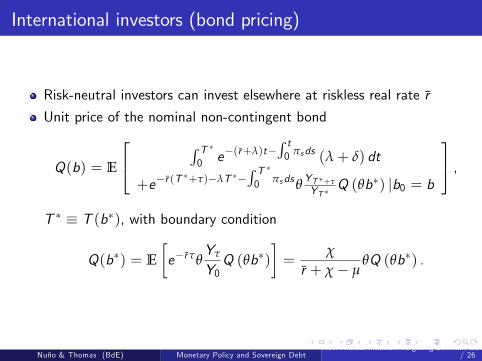

International investors (bond pricing)

Risk-neutral investors can invest elsewhere at riskless real rate r

Unit price of the nominal non-contingent bond

Q(b) = E

∫ T ∗0 e−(r+λ)t−

∫ t0 πsds (λ+ δ) dt

+e−r (T∗+τ)−λT ∗−

∫ T ∗0 πsdsθ

YT ∗+τ

YT ∗Q (θb∗) |b0 = b

,T ∗ ≡ T (b∗), with boundary condition

Q(b∗) = E

[e−rτθ

Yτ

Y0Q (θb∗)

]=

χ

r + χ− µθQ (θb∗) .

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 14

/ 26

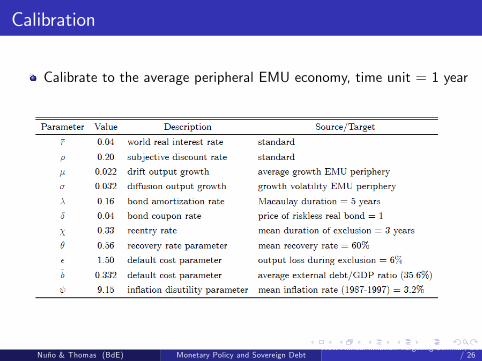

Calibration

Calibrate to the average peripheral EMU economy, time unit = 1 year

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 15

/ 26

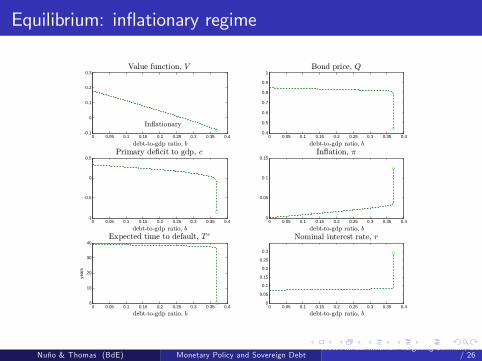

Equilibrium: inflationary regime

0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.40.1

0

0.1

0.2

0.3

debttogdp ratio, b

Value function, V

In.ationary

0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.40.4

0.5

0.6

0.7

0.8

0.9

1

debttogdp ratio, b

Bond price, Q

0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.41

0.5

0

0.5

debttogdp ratio, b

Primary decit to gdp, c

0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.40

0.05

0.1

0.15

debttogdp ratio, b

In.ation, :

0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.40

10

20

30

40

debttogdp ratio, b

Expected time to default, T e

year

s

0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.40

0.05

0.1

0.15

0.2

0.25

0.3

debttogdp ratio, b

Nominal interest rate, r

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 16

/ 26

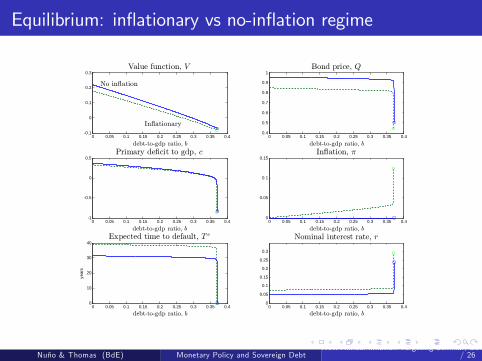

Equilibrium: inflationary vs no-inflation regime

0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.40.1

0

0.1

0.2

0.3

debttogdp ratio, b

Value function, V

No in.ation

In.ationary

0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.40.4

0.5

0.6

0.7

0.8

0.9

1

debttogdp ratio, b

Bond price, Q

0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.41

0.5

0

0.5

debttogdp ratio, b

Primary decit to gdp, c

0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.40

0.05

0.1

0.15

debttogdp ratio, b

In.ation, :

0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.40

10

20

30

40

debttogdp ratio, b

Expected time to default, T e

year

s

0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.40

0.05

0.1

0.15

0.2

0.25

0.3

debttogdp ratio, b

Nominal interest rate, r

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 17

/ 26

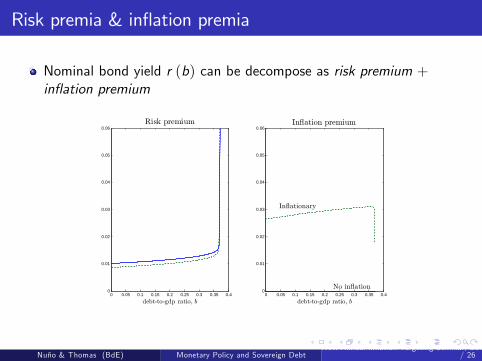

Risk premia & inflation premia

Nominal bond yield r (b) can be decompose as risk premium +inflation premium

0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.40

0.01

0.02

0.03

0.04

0.05

0.06

debttogdp ratio, b

Risk premium

In.ationary

0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.40

0.01

0.02

0.03

0.04

0.05

0.06

debttogdp ratio, b

In.ation premium

No in.ation

In.ationary

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 18

/ 26

Average performance

Inflationary regime yields lower value function V (b) at any debtratio, but...

... If it delivers suffi ciently lower debt ratio most of the time, averagewelfare could be higher

Compute stationary debt distribution so as to calculate unconditionalaverage values

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 19

/ 26

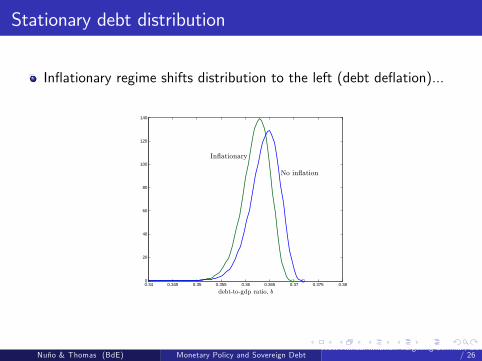

Stationary debt distribution

Inflationary regime shifts distribution to the left (debt deflation)...

0.34 0.345 0.35 0.355 0.36 0.365 0.37 0.375 0.380

20

40

60

80

100

120

140

debttogdp ratio, b

No in.ation

In.ationary

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 20

/ 26

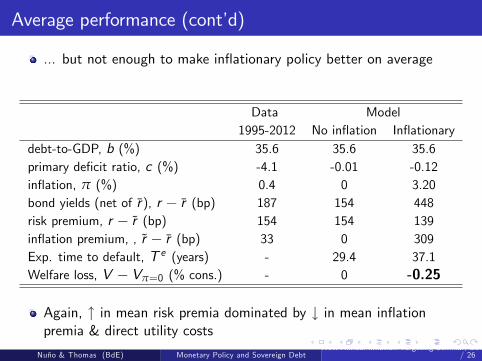

Average performance (cont’d)

... but not enough to make inflationary policy better on average

Data Model1995-2012 No inflation Inflationary

debt-to-GDP, b (%) 35.6 35.6 35.6primary deficit ratio, c (%) -4.1 -0.01 -0.12inflation, π (%) 0.4 0 3.20bond yields (net of r ), r − r (bp) 187 154 448risk premium, r − r (bp) 154 154 139inflation premium, , r − r (bp) 33 0 309Exp. time to default, T e (years) - 29.4 37.1Welfare loss, V − Vπ=0 (% cons.) - 0 -0.25

Again, ↑ in mean risk premia dominated by ↓ in mean inflationpremia & direct utility costs

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 21

/ 26

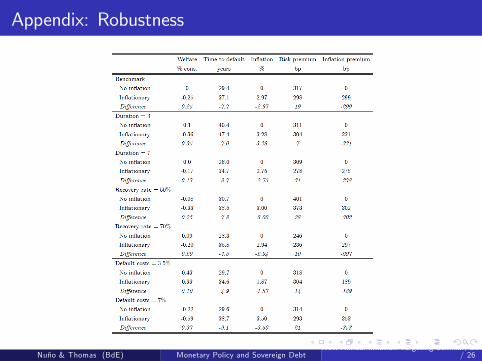

Robustness

Investigate robustness to alternative calibrations of:

bond amortization rate (λ)bond recovery parameter (θ)output loss from default (b)

For all parameter values, we continue to find higher average welfare inno-inflation regime

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 22

/ 26

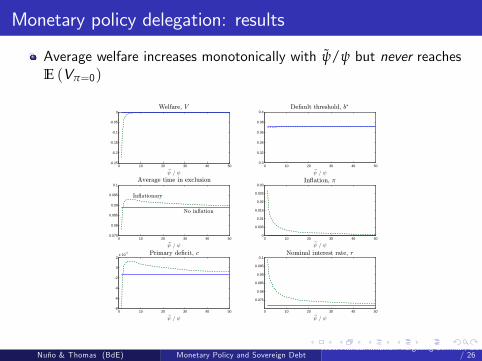

Monetary policy delegation

’No inflation’regime equivalent to appointing an extremelyconservative central banker

Consider intermediate arrangement: appoint a central banker...

who dislikes inflation more than society...... but not so much as to set π = 0 at all times

Given government’s c (b) and b∗, central banker chooses π ...

to maximize its value function V , defined similarly to V , but withψ ≥ ψ

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 23

/ 26

Monetary policy delegation: results

Average welfare increases monotonically with ψ/ψ but never reachesE (Vπ=0)

0 10 20 30 40 500.25

0.2

0.15

0.1

0.05

0

eA / A

Welfare, V

0 10 20 30 40 500.3

0.32

0.34

0.36

0.38

0.4

eA / A

Default threshold, b$

0 10 20 30 40 500.075

0.08

0.085

0.09

0.095

0.1

eA / A

Average time in exclusion

No in.ation

In.ationary

0 10 20 30 40 500

0.005

0.01

0.015

0.02

0.025

0.03

eA / A

In.ation, :

0 10 20 30 40 508

6

4

2

0

2x 104

eA / A

Primary decit, c

0 10 20 30 40 50

0.075

0.08

0.085

0.09

0.095

0.1

eA / A

Nominal interest rate, r

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 24

/ 26

Conclusions

Analyzed trade-offs between price stability and sovereign debtsustainability...

... in an open-economy model with nominal debt and optimal default

Welfare is higher if gov’t renounces the option to deflate debt away,e.g. by

issuing foreign currency debtjoining an anti-inflationary monetary union

Intuition: benefits (lower inflation premia, no direct welfare costs)outweigh costs (higher risk premia)

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 25

/ 26

Appendix: Robustness

Nuño & Thomas (BdE) Monetary Policy and Sovereign DebtXVII Annual Inflation Targeting Seminar, Banco Central do Brasil May 21 2015 26

/ 26