midmarket: opportunity, productivity & scale

TRANSCRIPT

Tim Frankcom, EVP Midmarket

Investor Day, September 2016

Midmarket:

Opportunity,

Productivity & Scale

2 | Copyright © 2016 Criteo

Safe Harbor Statement

This presentation contains “forward-looking” statements that are based on our management’s beliefs and assumptions and on information

currently available to management. Forward-looking statements include information concerning our possible or assumed future results of

operations, business strategies, financing plans, projections, competitive position, industry environment, potential growth opportunities,

potential market opportunities and the effects of competition.

Forward-looking statements include all statements that are not historical facts and can be identified by terms such as “anticipates,”

“believes,” “could,” “seeks,” “estimates,” “intends,” “may,” “plans,” “potential,” “predicts,” “projects,” “should,” “will,” “would” or similar

expressions and the negatives of those terms. Forward-looking statements involve known and unknown risks, uncertainties and other

factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or

achievements expressed or implied by the forward-looking statements. Forward-looking statements represent our management’s beliefs and

assumptions only as of the date of this presentation. You should read the Company’s most recent Annual Report as filed on Form 10-K, on

February 29, 2016, including the Risk Factors set forth therein and the exhibits thereto, completely and with the understanding that our

actual future results may be materially different from what we expect. Except as required by law, we assume no obligation to update these

forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in the forward-

looking statements, even if new information becomes available in the future.

This presentation includes certain non-GAAP financial measures as defined by SEC rules. As required by Regulation G, we have provided a

reconciliation of those measures to the most directly comparable GAAP measures, which is available in the Appendix slides to today’s

“Financial Update” presentation. In addition, certain financial information contained herein with respect to years ended prior to December 31,

2013 has been derived from our audited consolidated financial statements that were prepared in accordance with IFRS and presented in

Euros. Financial information contained herein with respect to quarterly periods has been derived from our unaudited condensed

consolidated financial statements.

3 | Copyright © 2016 Criteo

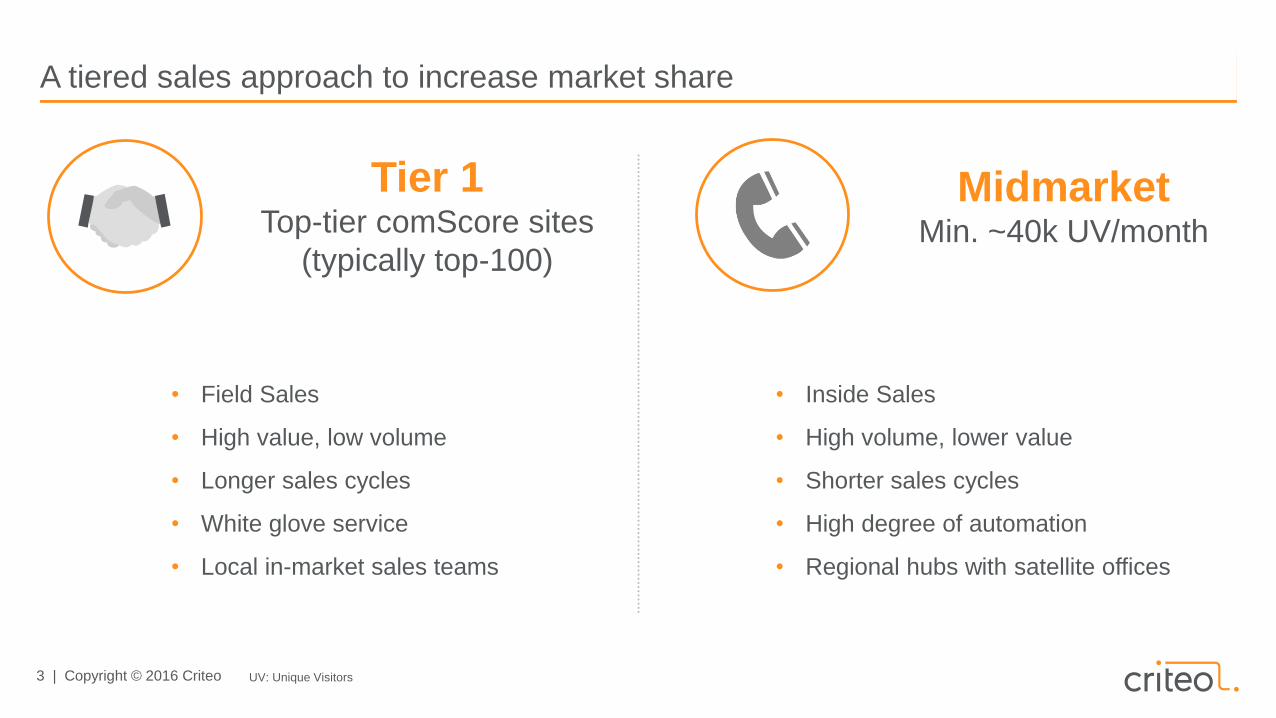

A tiered sales approach to increase market share

• Field Sales

• High value, low volume

• Longer sales cycles

• White glove service

• Local in-market sales teams

• Inside Sales

• High volume, lower value

• Shorter sales cycles

• High degree of automation

• Regional hubs with satellite offices

Tier 1Top-tier comScore sites

(typically top-100)

MidmarketMin. ~40k UV/month

UV: Unique Visitors

4 | Copyright © 2016 Criteo

Midmarket consists of thousands of advertisers, some of which are well-known

5 | Copyright © 2016 Criteo

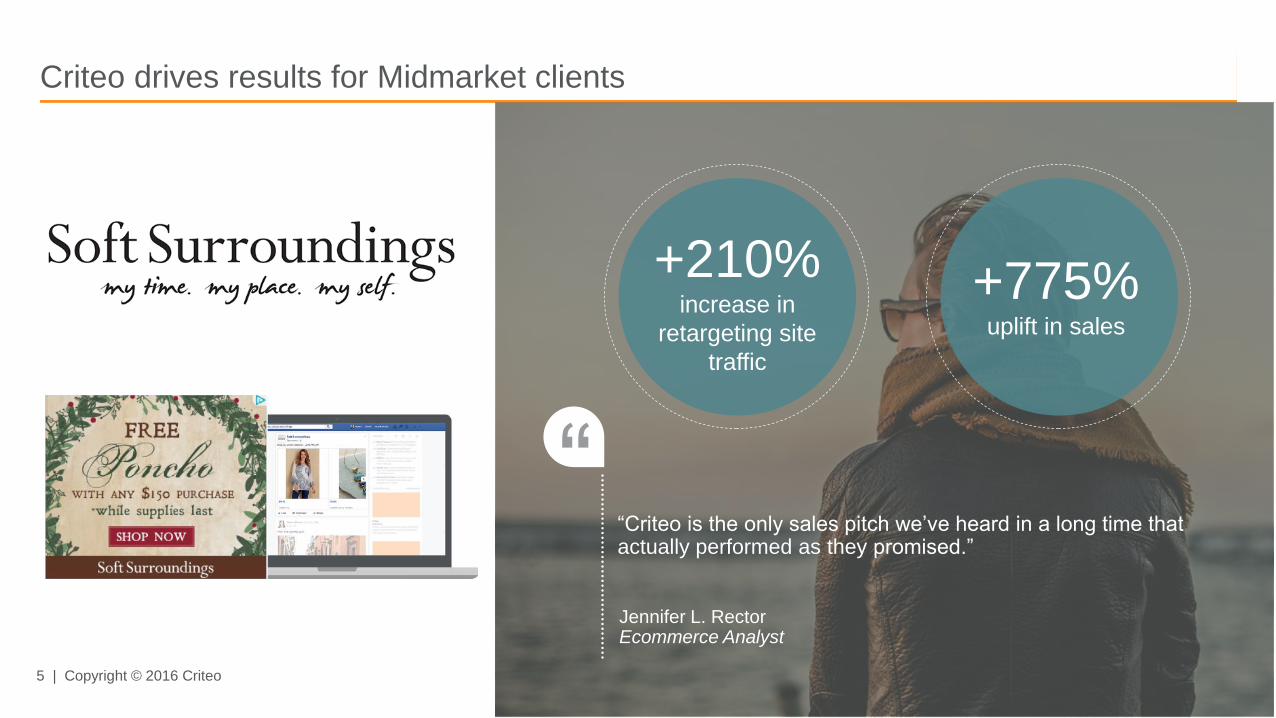

Criteo drives results for Midmarket clients

““Criteo is the only sales pitch we’ve heard in a long time that actually performed as they promised.”

Jennifer L. RectorEcommerce Analyst

+210%increase in

retargeting site

traffic

+775%uplift in sales

6 | Copyright © 2016 Criteo

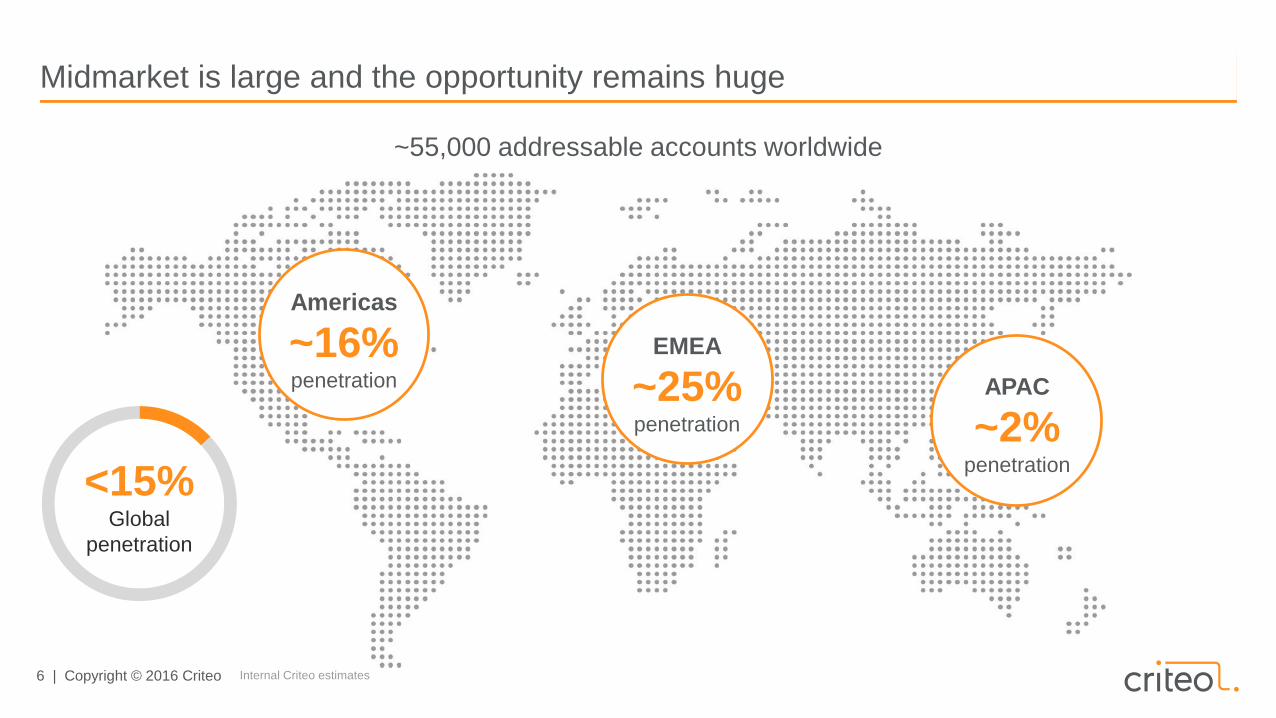

Midmarket is large and the opportunity remains huge

<15%Global

penetration

~55,000 addressable accounts worldwide

Americas

~16% penetration

EMEA

~25% penetration

APAC

~2% penetration

Internal Criteo estimates

7 | Copyright © 2016 Criteo

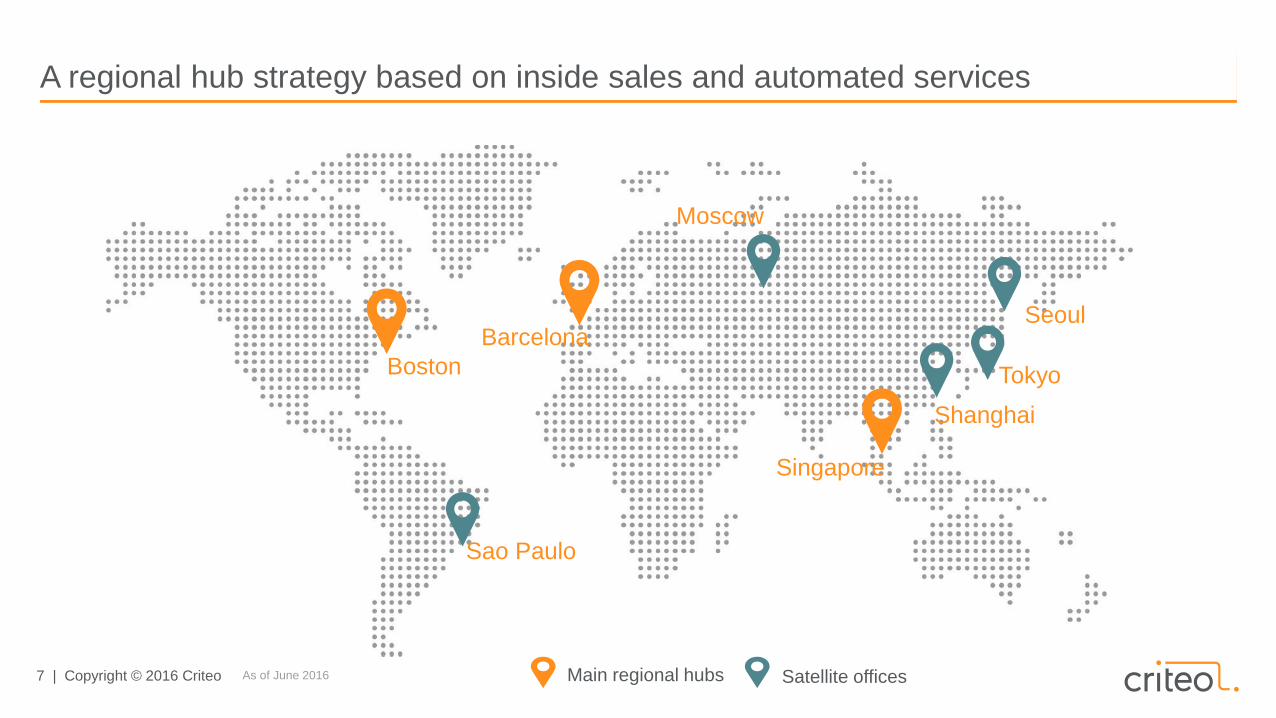

Boston

Barcelona

Tokyo

Singapore

Sao Paulo

Shanghai

A regional hub strategy based on inside sales and automated services

Main regional hubs Satellite offices

Seoul

Moscow

As of June 2016

8 | Copyright © 2016 Criteo

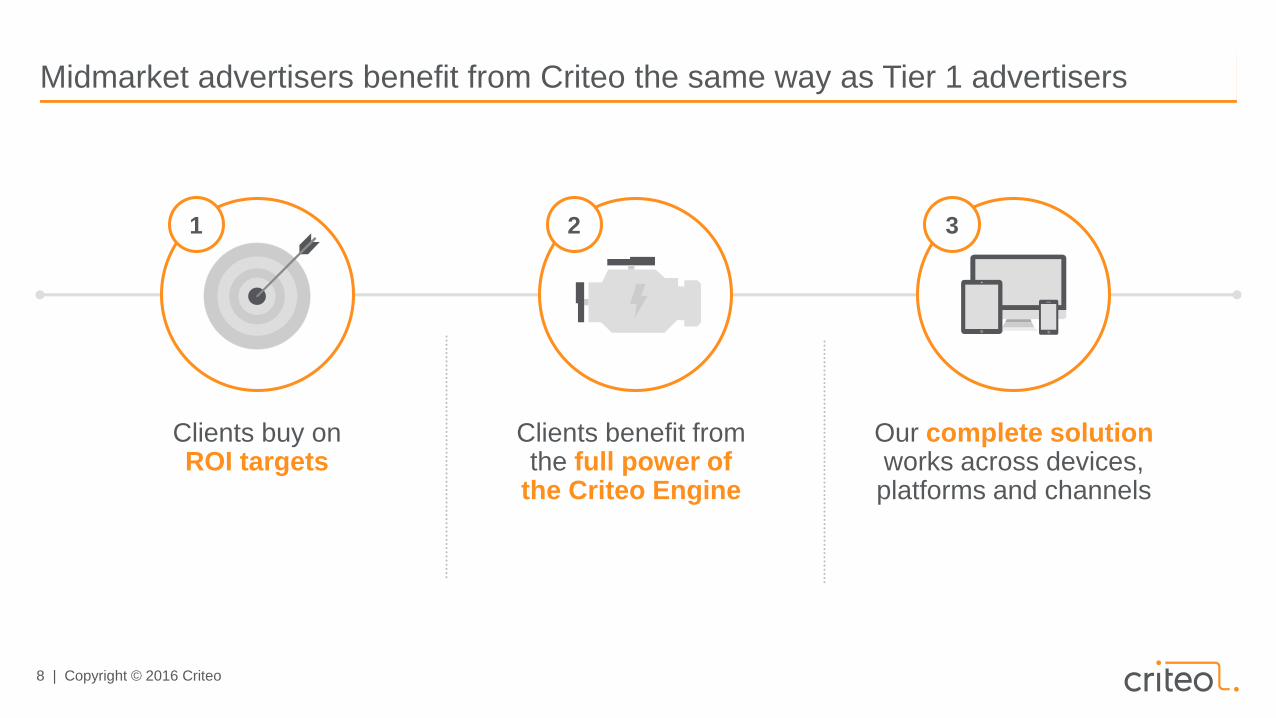

Midmarket advertisers benefit from Criteo the same way as Tier 1 advertisers

1 2 3

Clients benefit from the full power of

the Criteo Engine

Our complete solution works across devices, platforms and channels

Clients buy on ROI targets

9 | Copyright © 2016 Criteo

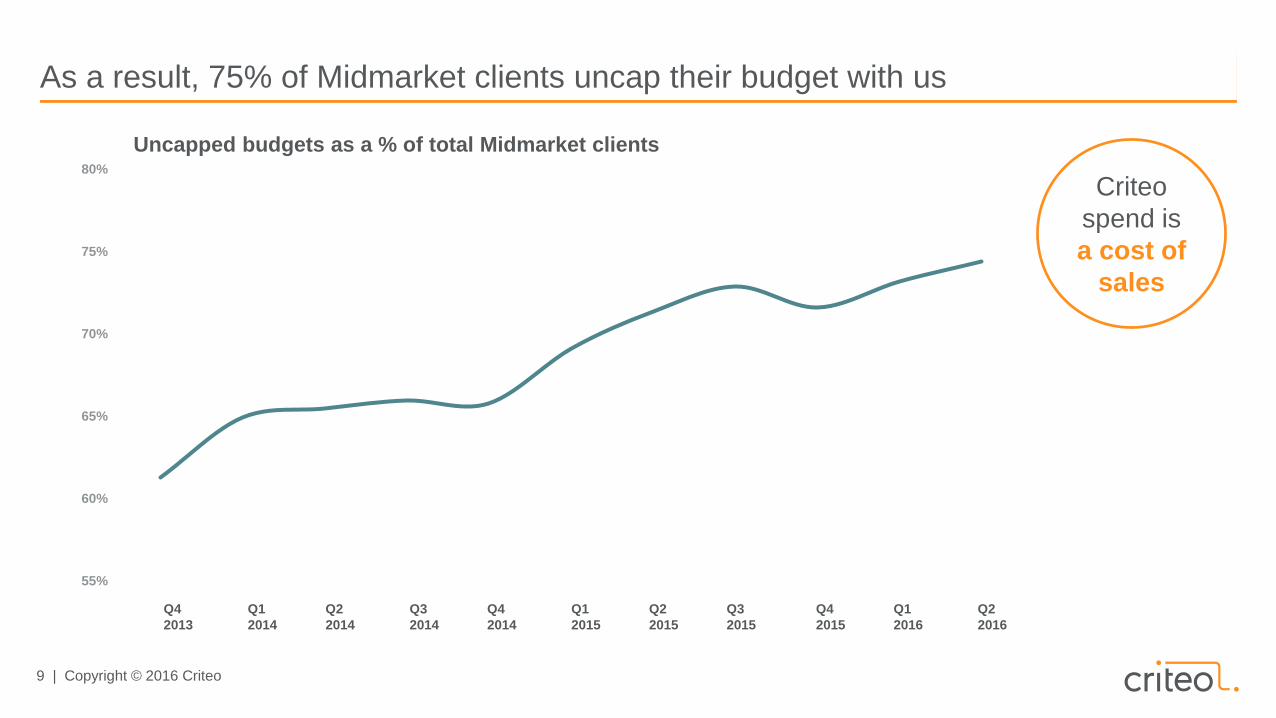

As a result, 75% of Midmarket clients uncap their budget with us

Criteo

spend is

a cost of

sales

55%

60%

65%

70%

75%

80%

Uncapped budgets as a % of total Midmarket clients

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2013 2014 2014 2014 2014 2015 2015 2015 2015 2016 2016

10 | Copyright © 2016 Criteo

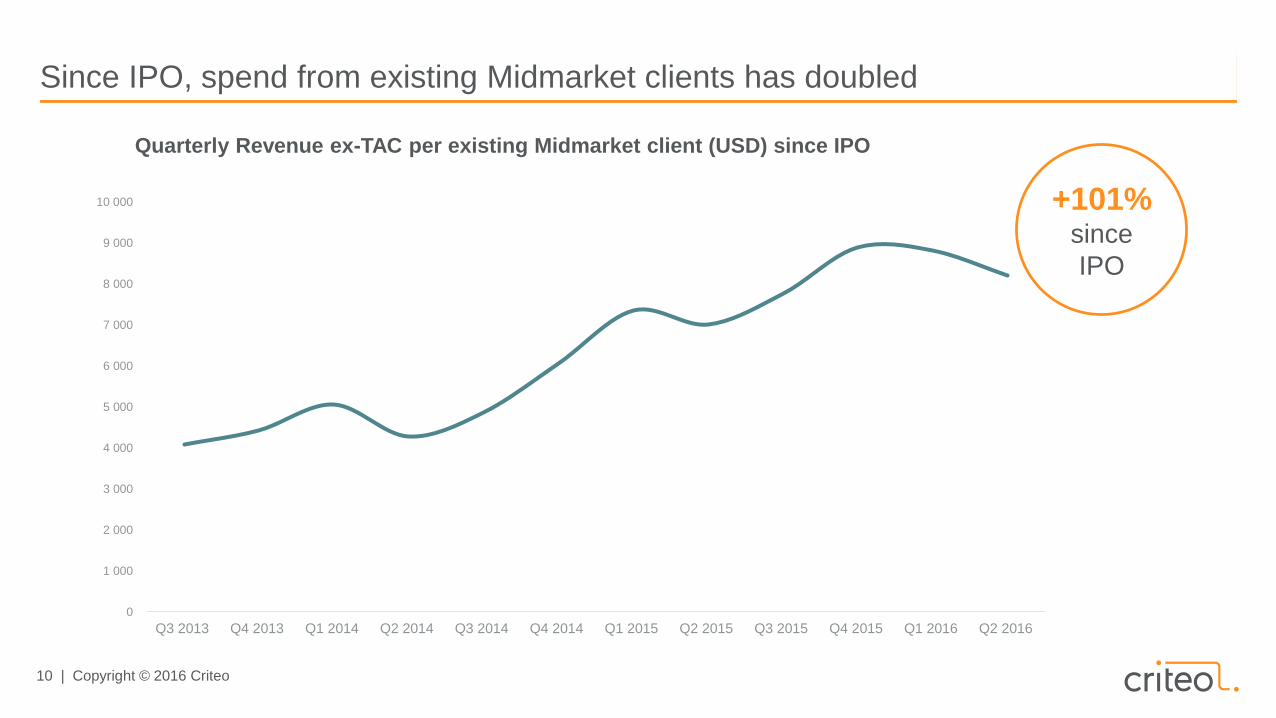

Since IPO, spend from existing Midmarket clients has doubled

Quarterly Revenue ex-TAC per existing Midmarket client (USD) since IPO

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

10 000

Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016

+101% since

IPO

11 | Copyright © 2016 Criteo

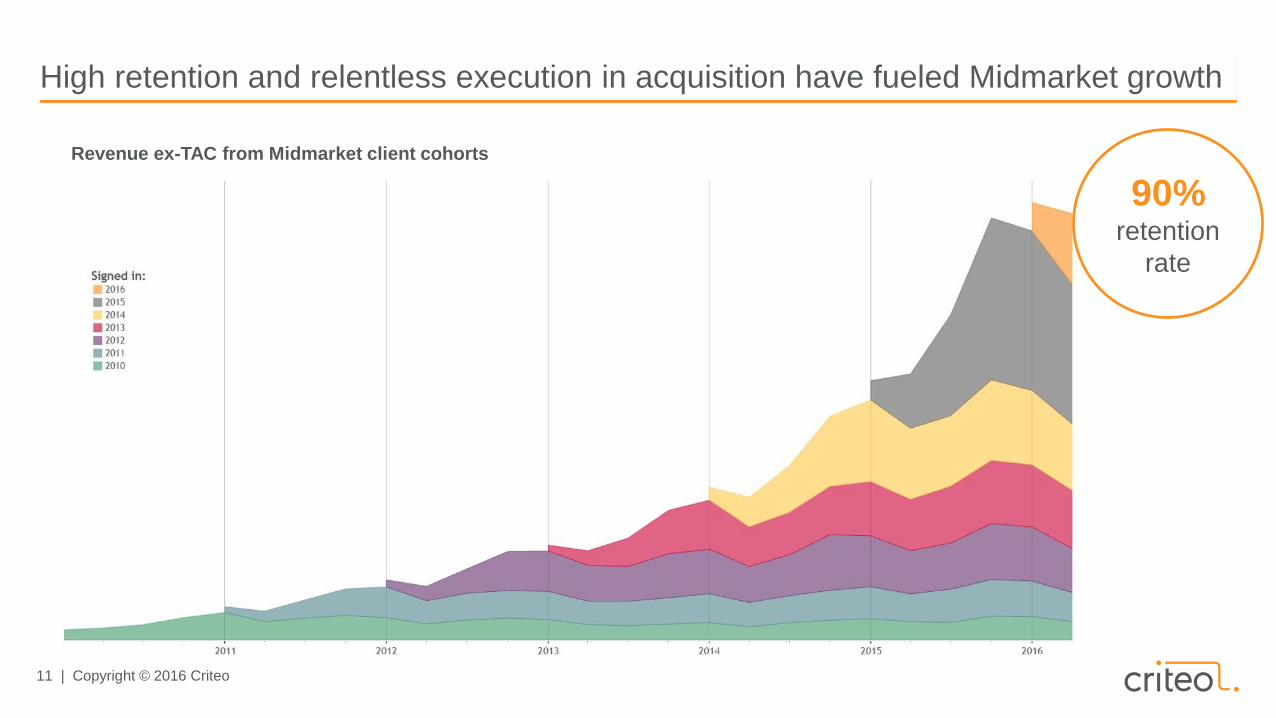

High retention and relentless execution in acquisition have fueled Midmarket growth

90% retention

rate

Revenue ex-TAC from Midmarket client cohorts

12 | Copyright © 2016 Criteo

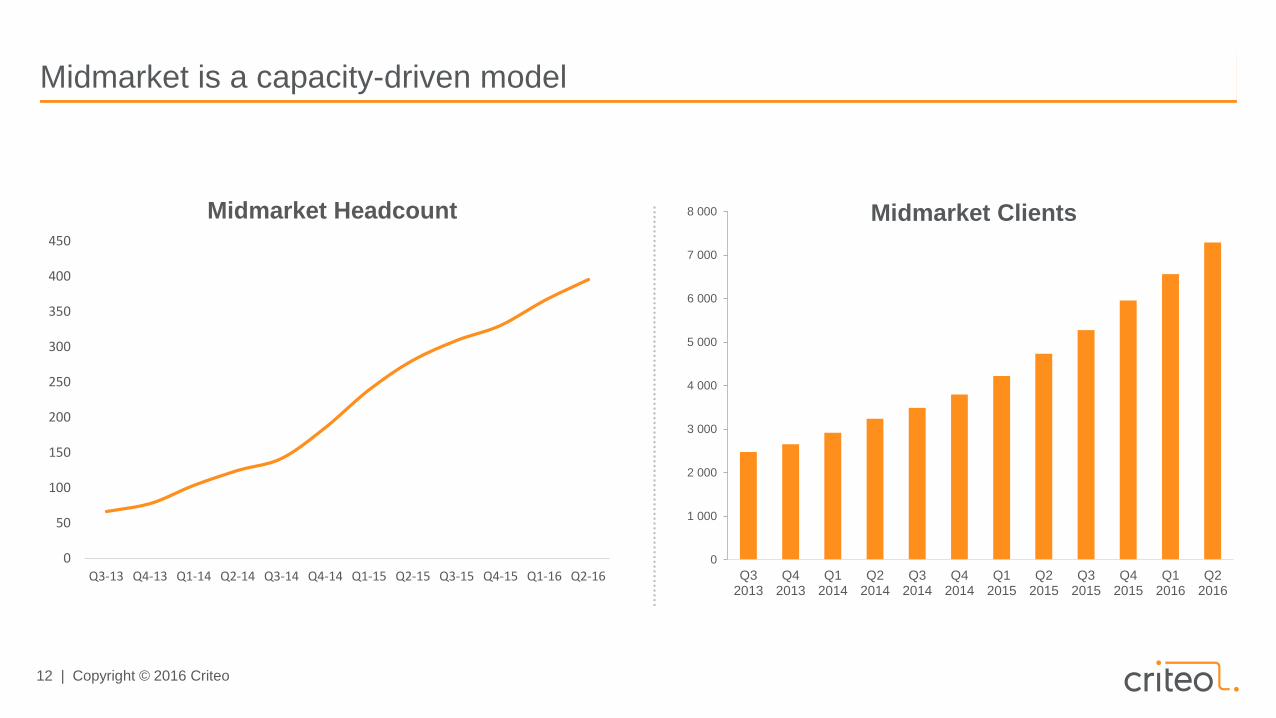

Midmarket is a capacity-driven model

0

50

100

150

200

250

300

350

400

450

Q3-13 Q4-13 Q1-14 Q2-14 Q3-14 Q4-14 Q1-15 Q2-15 Q3-15 Q4-15 Q1-16 Q2-16

Midmarket Headcount

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

Q12016

Q22016

Midmarket Clients

13 | Copyright © 2016 Criteo

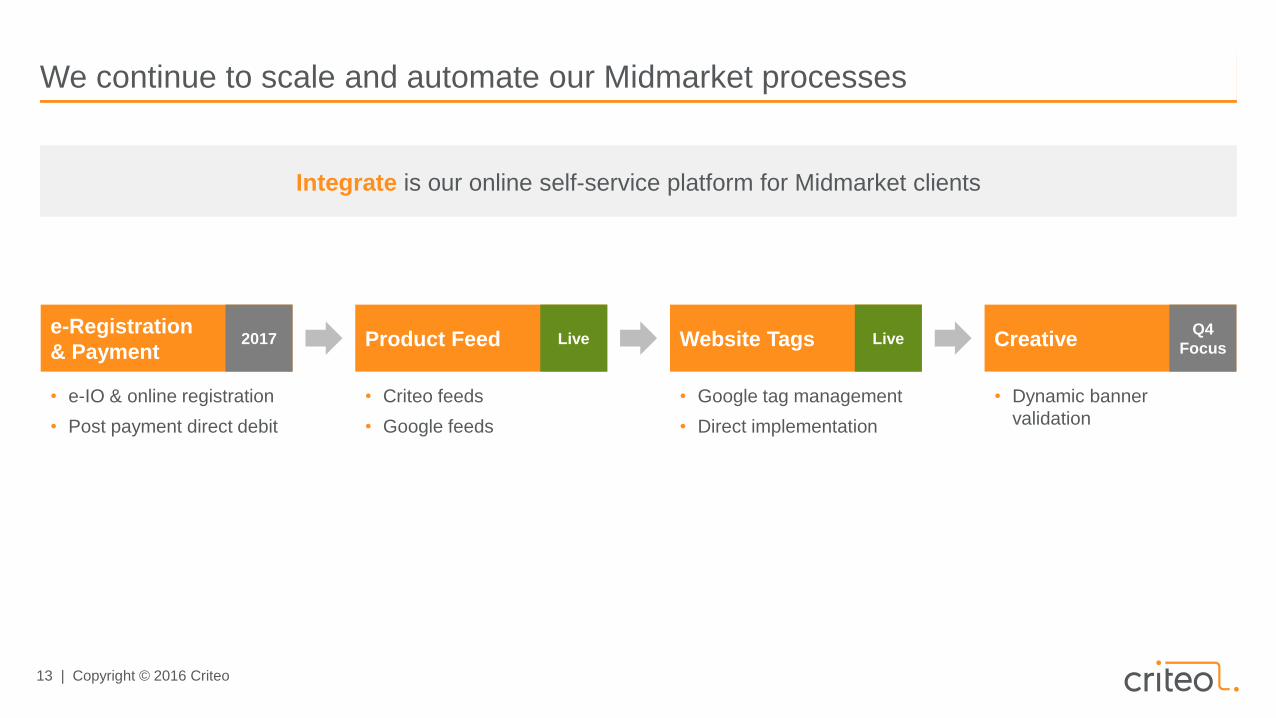

We continue to scale and automate our Midmarket processes

• e-IO & online registration

• Post payment direct debit

• Criteo feeds

• Google feeds

• Google tag management

• Direct implementation

• Dynamic banner

validation

Website Tags Live CreativeQ4

Focus

Integrate is our online self-service platform for Midmarket clients

Product Feed Livee-Registration

& Payment2017

14 | Copyright © 2016 Criteo

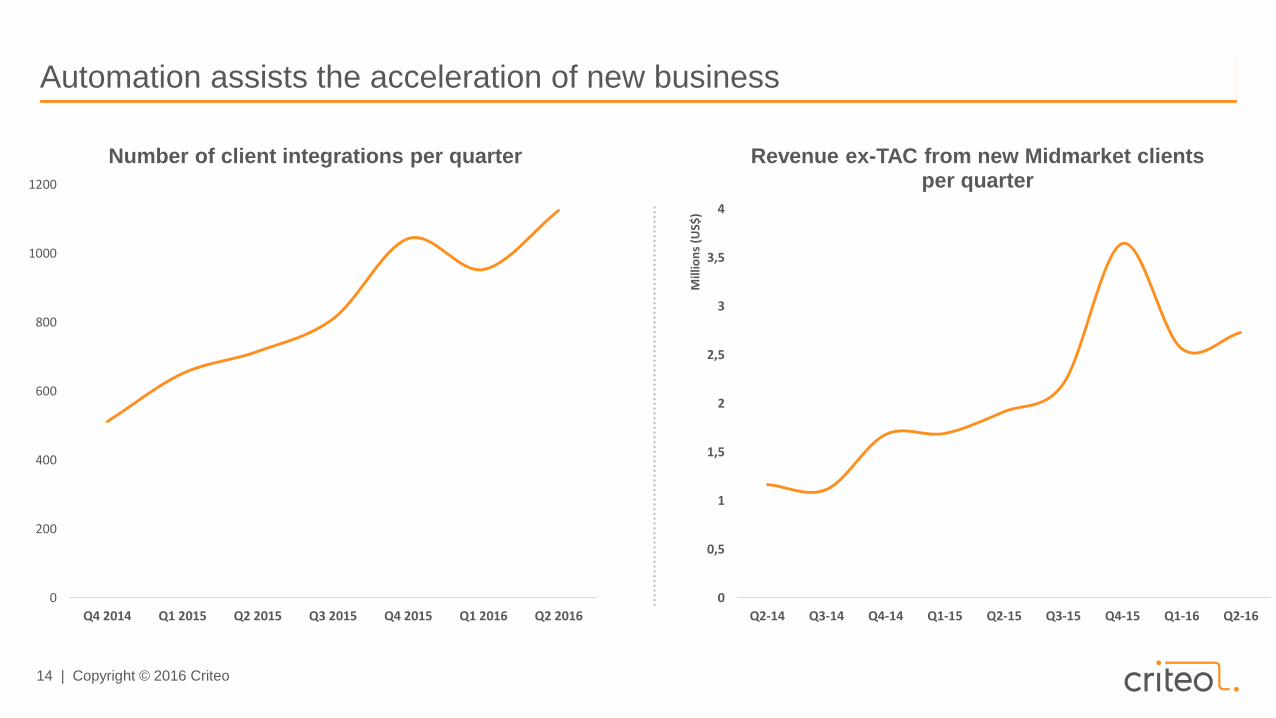

Automation assists the acceleration of new business

0

200

400

600

800

1000

1200

Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016

Number of client integrations per quarter

0

0,5

1

1,5

2

2,5

3

3,5

4

Q2-14 Q3-14 Q4-14 Q1-15 Q2-15 Q3-15 Q4-15 Q1-16 Q2-16

Mill

ion

s (U

S$)

Revenue ex-TAC from new Midmarket clients per quarter

15 | Copyright © 2016 Criteo

Conclusion

2Our multi-channel approach (Display, Email and Search)

further enhances the opportunity

3Continued investment in automation drives

improved productivity and scale

1 Midmarket is a huge opportunity

The World’s

Performance

Marketing Platform