michael a. golemi william w. pugh - willis group pugh.pdf · michael a. golemi. william w. pugh....

TRANSCRIPT

New Orleans | Lafayette | Houston | 1A Professional Law Corporation

Michael A. GolemiWilliam W. Pugh

Willis 2012 North America Energy Conference May 16, 2012

Contractual Risk Allocation in a Post- Macondo Environment

Overview

Significant Macondo decisions

Setting up a risk allocation program

Basic indemnity and insurance issues

Restrictions on indemnity and insurance in the oilfield

Texas Construction Anti‐indemnity Act

Survey: Top 4 Texas Country and Western Songs

from Texas Risk Managers

4.

How Can I Miss You . . .

If You Won't Go Away?

3.

You Got The Ring . . .

And I Got The Finger

2.

I Still Miss You Baby . . .

But My Aim's Gettin' Better

And the # 1 song is . . .

1.

If I Had Shot You When I First Wanted To . . .

I'd Be Out Of Prison By Now

Significant Macondo Decisions – Insurance and Indemnity

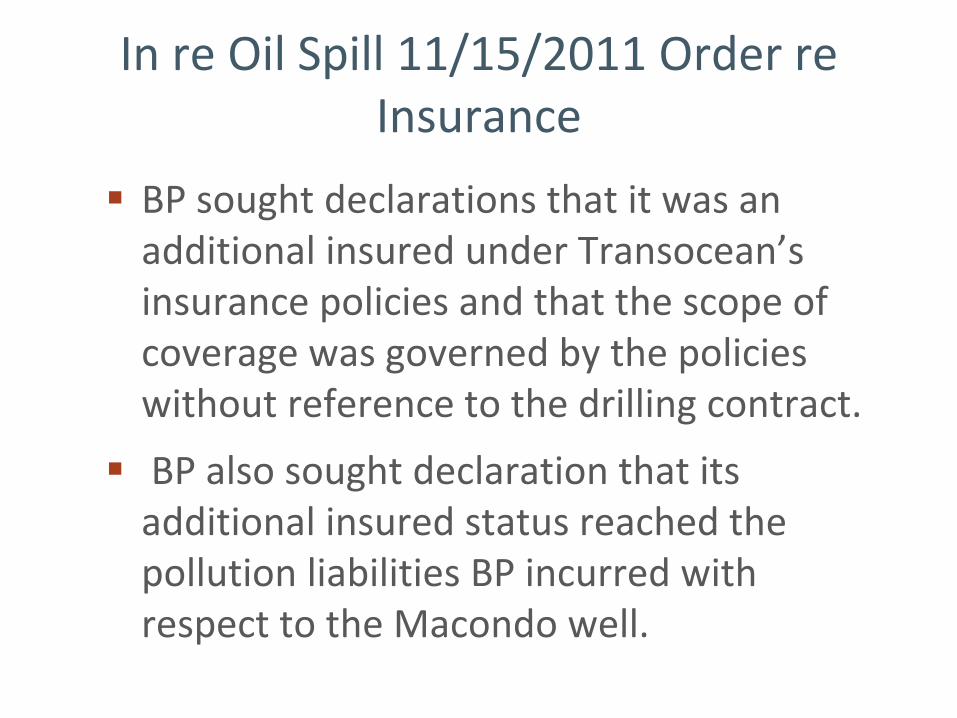

In re Oil Spill 11/15/2011 Order re Insurance

BP sought declarations that it was an additional insured under Transocean’s

insurance policies and that the scope of coverage was governed by the policies

without reference to the drilling contract.

BP also sought declaration that its additional insured status reached the

pollution liabilities BP incurred with respect to the Macondo well.

In re Oil Spill 11/15/2011 Order re Insurance

Court distinguished cases refusing to consider underlying contract because policy at issue referenced

“Insured Contract”

in the additional insured provision.

Court also distinguished cases invalidating limitations found in additional insured provisions of underlying

contract because additional insured provision at issue referenced indemnities within the contract as opposed to extra‐contractual indemnity provisions.

Court also reasoned that additional insured provision was not separate from and in addition to indemnities because it limited the additional insured coverage

requirement to liabilities assumed in the contract.

In re Oil Spill 11/15/2011 Order re Insurance

Court held that BP is an additional insured under Transocean’s policies;

however, the scope of BP’s additional insured status is limited to the risks

assumed by Transocean in the drilling contract.

Pollution risks were allocated to BP, so BP does not have insurance coverage under

Transocean’s policies.

In re Oil Spill 1/26/2012 Order re Indemnity

BP argued:

• indemnification for Transocean’s gross negligence is against public policy

indemnity for punitive damages and civil fines/penalties under CWA is also against public

policy

Transocean’s breach of drilling contract invalidates indemnity

no attorney’s fees for pursuit of indemnity

no duty to assume defense of Transocean

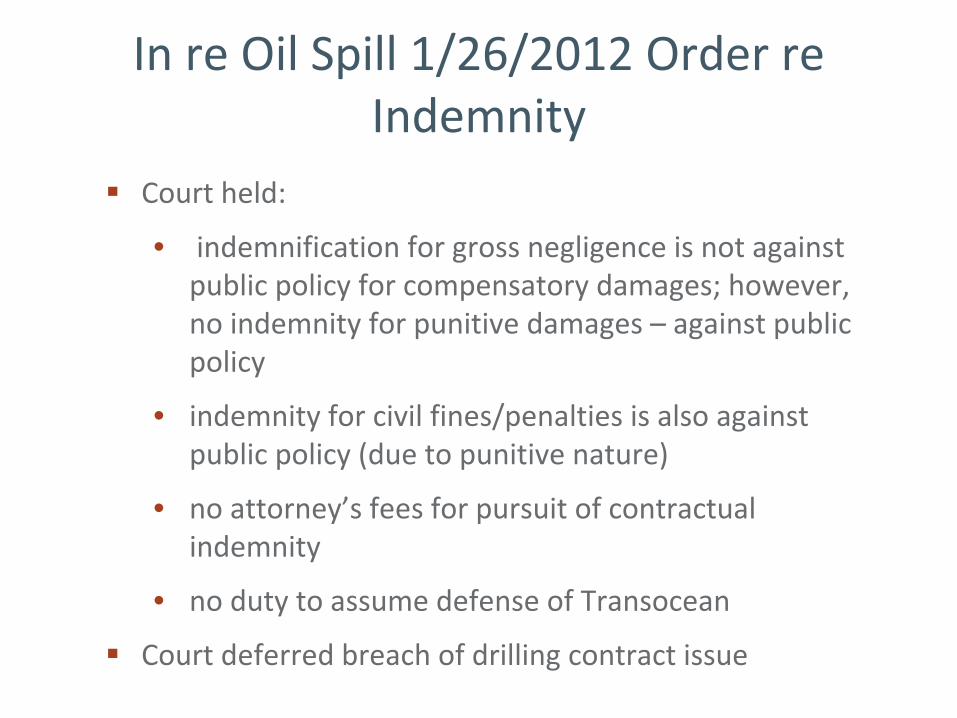

In re Oil Spill 1/26/2012 Order re Indemnity

Court held:

• indemnification for gross negligence is not against public policy for compensatory damages; however, no indemnity for punitive damages – against public policy

• indemnity for civil fines/penalties is also against public policy (due to punitive nature)

• no attorney’s fees for pursuit of contractual indemnity

• no duty to assume defense of Transocean

Court deferred breach of drilling contract issue

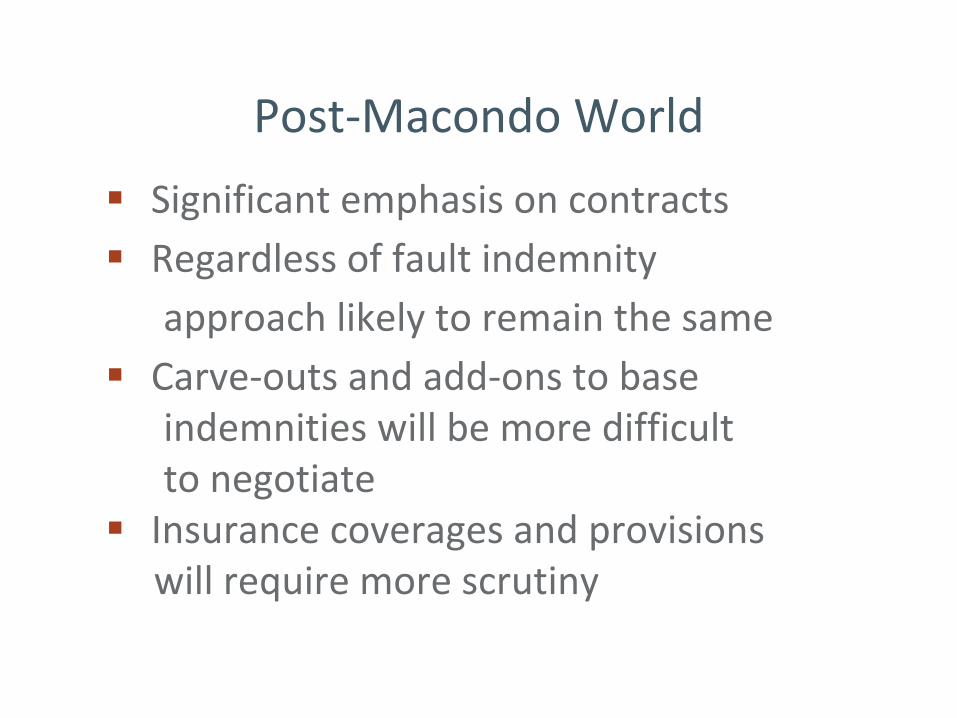

Post‐Macondo World

Significant emphasis on contracts

Regardless of fault indemnityapproach likely to remain the same

Carve‐outs and add‐ons to baseindemnities will be more difficultto negotiate

Insurance coverages and provisionswill require more scrutiny

Developing a Risk Allocation Program

Keys to Contractual Risk Allocation

Understand the big picture

• Recognize the impact of drilling contracts

• Consider different reciprocal indemnity approaches

Prepare your “pass‐through”

protection plan

Develop your master service agreements (MSAs) and analyze how other contracts will

come into play

Coordinate with your risk management department and insurance broker

Anticipating the Broad Reciprocal Indemnity

In a common workplace, indemnities will generally apply regardless of fault

Drilling contract or other major contract is often the key contract

Drilling contractor will want indemnity for Operator’s people and property and

people and property of

Operator’s other contractors (Broad Group)

Operator will owe indemnity to drilling contractor every time there is an accident involving anyone

other than the drilling contractor

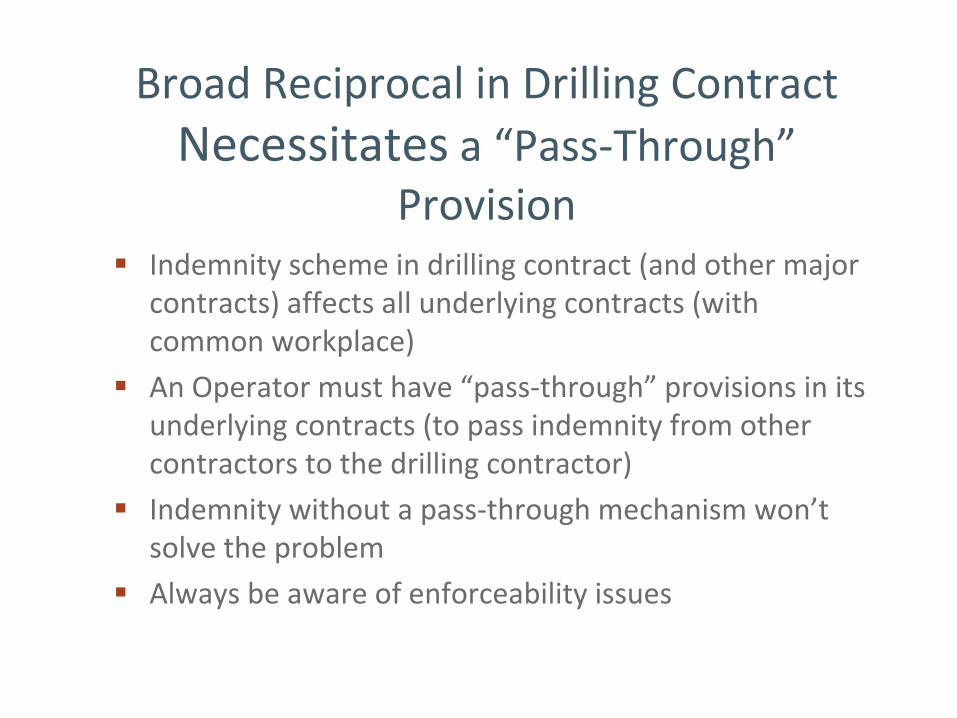

Broad Reciprocal in Drilling Contract Necessitates

a “Pass‐Through”

Provision

Indemnity scheme in drilling contract (and other major

contracts) affects all underlying contracts (with common workplace)

An Operator must have “pass‐through”

provisions in its underlying contracts (to pass indemnity from other

contractors to the drilling contractor)

Indemnity without a pass‐through mechanism won’t solve the problem

Always be aware of enforceability issues

Contractor’s View

COMPANY CONTRACTOR

OTHER CONTRACTORS SUBCONTRACTOR

Company

Drilling Wireline Vessel Casing Helicopter

Mud LoggingContractor

Subs, if any

Operator’s View

16 2/3 %

16 2/3 %

16 2/3 %

16 2/3 %

16 2/3 %

16 2/3 %

Drilling

Wireline

Helicopter

Casing

Mud Logging

Vessel

Company

What Happens Without a Pass‐ Through Provision

For every instance in which an Operator owes a broad reciprocal

indemnity, but the underlying

contract has no pass‐through

provision, the Operator will have no recourse!!!!

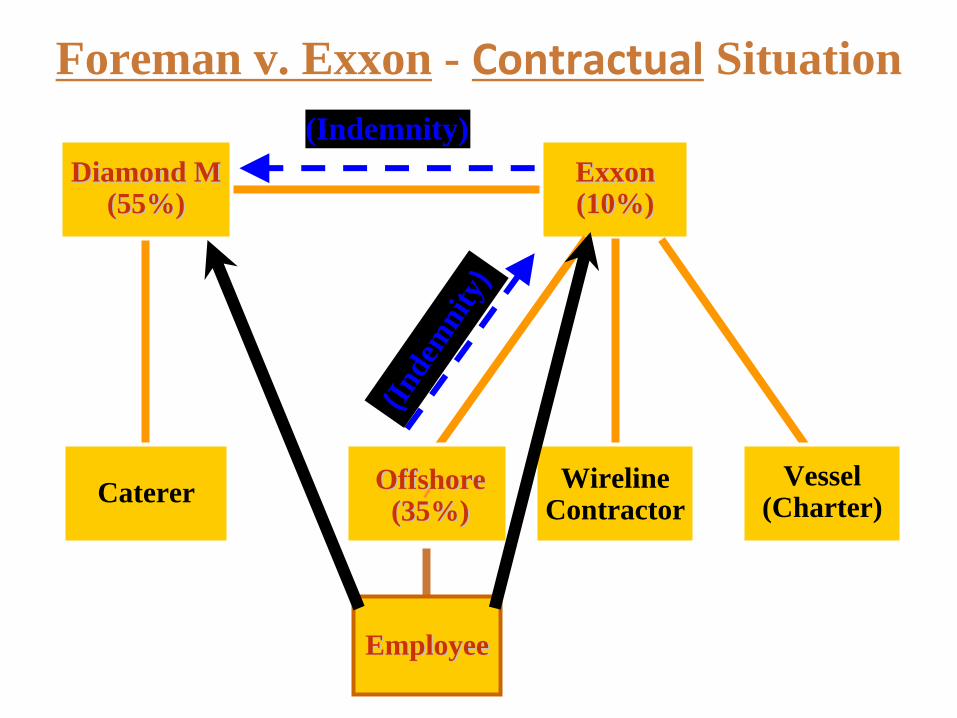

Foreman v. Exxon ‐

Contractual Situation

ExxonExxon(Indemnity)

EmployeeEmployee

Caterer Vessel(Charter)

OffshoreOffshore WirelineContractor

(Inde

mni

ty)

Diamond MDiamond M

Foreman v. Exxon - Contractual

Situation

ExxonExxon(10%)(10%)

(Indemnity)

EmployeeEmployee

Caterer Vessel(Charter)

OffshoreOffshore(35%)(35%)

WirelineContractor

Diamond MDiamond M(55%)(55%)

(Inde

mni

ty)

Foreman v. Exxon ‐

Result

Exxon Exxon (15%)(15%)(10%)(10%)

(Indemnity)

EmployeeEmployee

Caterer Vessel(Charter)

OffshoreOffshore(35%)(35%)

WirelineContractor

(Inde

mni

ty)

Diamond M Diamond M (85%)(85%)(55%)(55%)

Foreman v. Exxon - ResultOffshoreOffshore (15%)(15%)(10%)(10%)

(Indemnity)

EmployeeEmployee

Caterer Vessel(Charter)

OffshoreOffshore(35%)(35%)

WirelineContractor

(Inde

mni

ty)

ExxonExxon(85%)(85%)(55%)(55%)

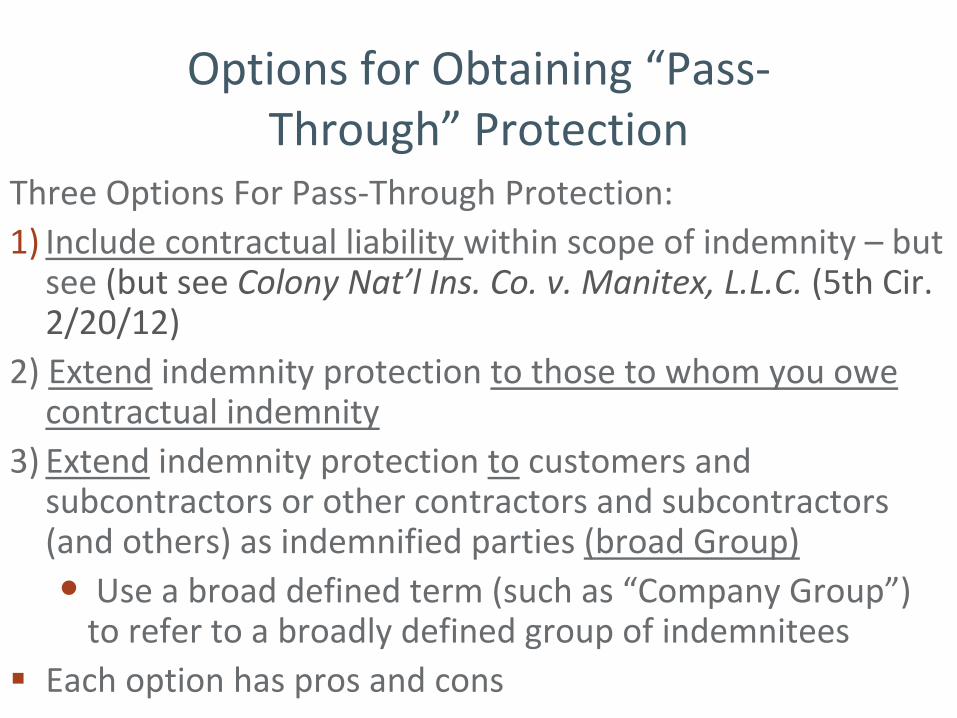

Options for Obtaining “Pass‐ Through”

Protection

Three Options For Pass‐Through Protection:1)

Include contractual liability within scope of indemnity –

but

see (but see Colony Nat’l Ins. Co. v. Manitex, L.L.C. (5th Cir. 2/20/12)

2) Extend

indemnity protection to those to whom you owe contractual indemnity

3)

Extend

indemnity protection to

customers and subcontractors or other contractors and subcontractors

(and others) as indemnified parties (broad Group)• Use a broad defined term (such as “Company Group”)

to refer to a broadly defined group of indemnitees

Each option has pros and cons

Basic Indemnity and Insurance Protections

Indemnity Basics

• MSA is a building block for most operations

• Must have valid “magic language”

to obtain indemnity for one’s own negligence

• Indemnity (and “magic language”) must be broad enough to extend to all intended beneficiaries

• Anticipate and address possible restrictions on indemnity

• Be aware of any issues relating to the scope of the indemnity or the scope of the MSA

• Deepwater Horizon ‐

indemnity for gross negligence (as opposed to release) is not against public policy under

maritime law ‐

indemnity for punitive damages is

Carefully Consider Who Should be the Indemnitees

Use defined term such as “Company Group”

Consider all parties you may want protected

Include contractors and subcontractors or use another approach to provide pass through protection

Expand use of “Company Group”• Allows consistent and uniform risk allocation scheme• Use same definition in insurance requirements and

certificate of insurance• Use same definition in other contracts if at all

possible

Anticipating Carve‐Outs, Add‐ons, and Other Exceptions

Avoid carve‐outs and add‐ons if possible

Limit carve‐outs to the actual risk intended (such as

well control costs) as opposed to “all claims arising out of . . . [a blowout]”

Well Control

Pollution

Loss of Reservoir

Gross Negligence

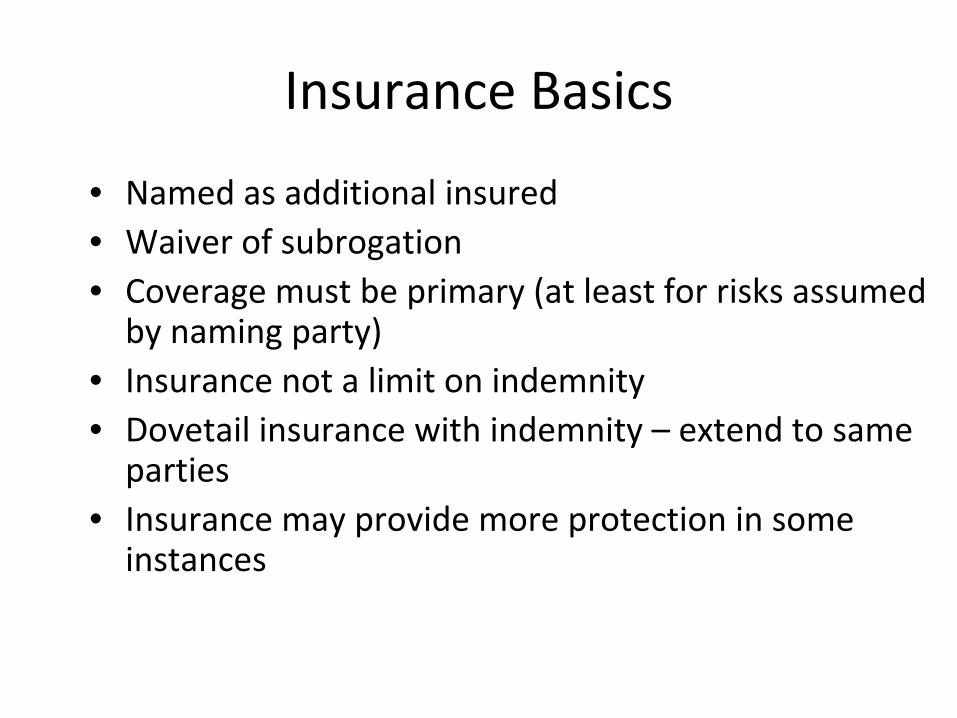

Insurance Basics

• Named as additional insured• Waiver of subrogation• Coverage must be primary (at least for risks assumed

by naming party)• Insurance not a limit on indemnity• Dovetail insurance with indemnity –

extend to same

parties• Insurance may provide more protection in some

instances

Insurance may provide more protection than indemnities

Insurance may provide more protection in some instances due to anti indemnity laws

Texas ‐

Getty

and Oryx

• Comply with Texas insurance language

• Include Getty

language

Insurance may provide more protection than indemnities (cont’d)

Louisiana‐consider application of Marcel

LHWCA ‐

insurance protection is

enforceable even if indemnity is invalid

under §

905(b)

State that minimum limits are not a

limitation or restriction on indemnity

Critical Maritime Endorsements

Endorse P&I Insurance:

• To provide full protection to Company Group additional insureds without limitation as to liability as

owner of the vessel (and delete any “as owner” restrictions)

• To prohibit reduction of limits for Company Group in the event of limitation of liability

Restrictions on Indemnity and Insurance

Effect of Applicable Law

Maritime law ‐

indemnity and insurance generally fully

enforceable

• Drilling contract for jack‐up is maritime

• Be aware of § 905(b) of LHWCA

Determining applicable law is complicated and important in view of anti‐indemnity laws

Oilfield Anti‐Indemnity Acts

• Texas

• Louisiana

•New Mexico

•Wyoming

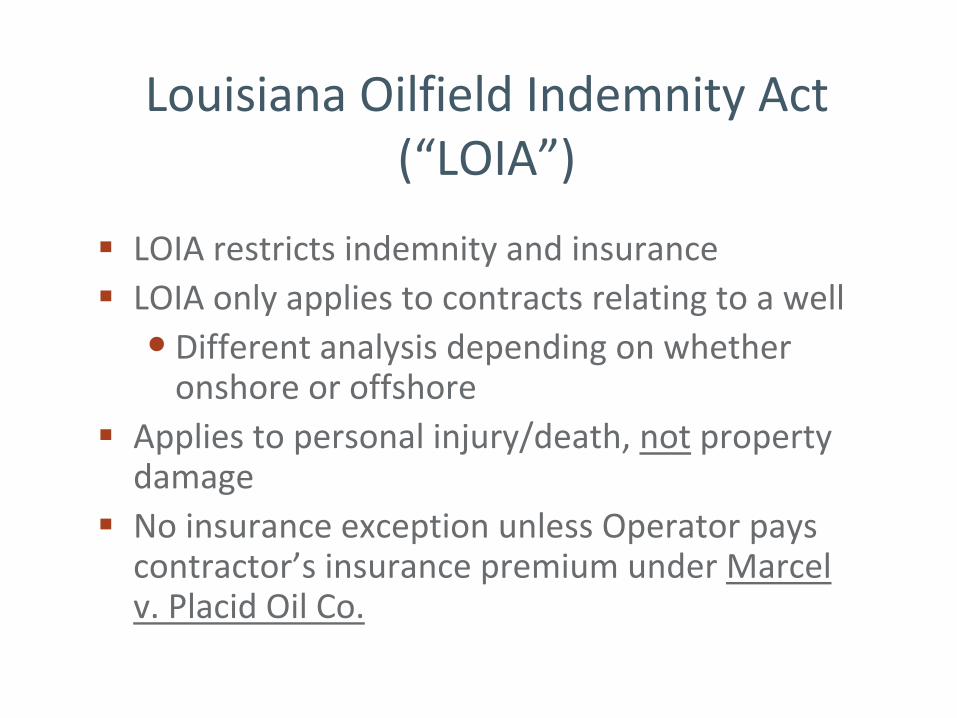

Louisiana Oilfield Indemnity Act (“LOIA”)

LOIA restricts indemnity and insurance

LOIA only applies to contracts relating to a well• Different analysis depending on whether

onshore or offshore

Applies to personal injury/death, not

property

damage

No insurance exception unless Operator pays

contractor’s insurance premium under Marcel v. Placid Oil Co.

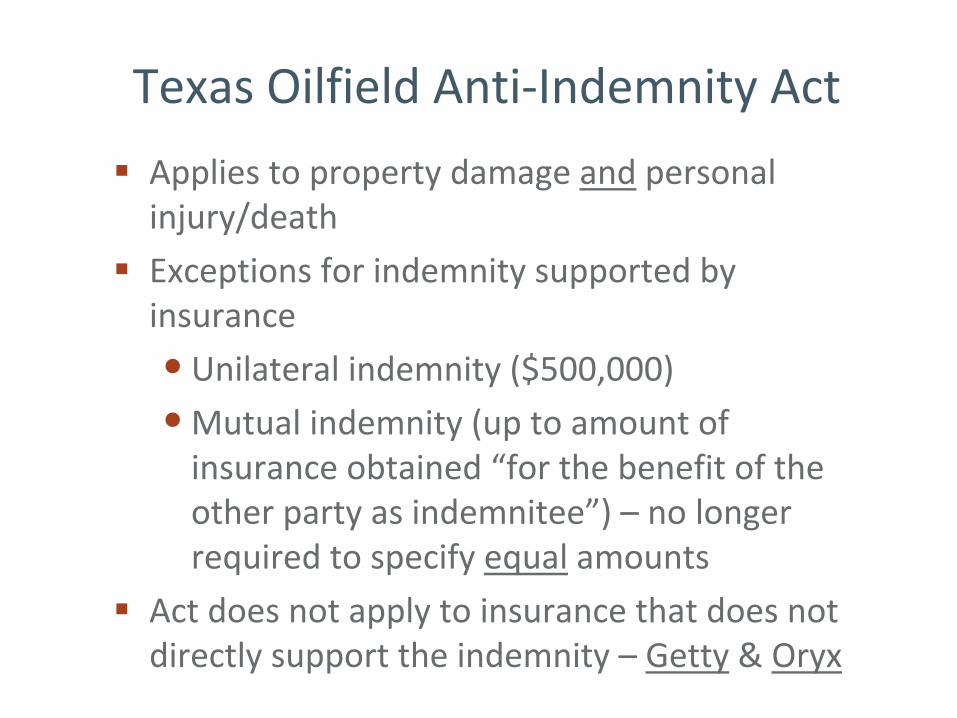

Texas Oilfield Anti‐Indemnity Act

Applies to property damage and

personal injury/death

Exceptions for indemnity supported by insurance

• Unilateral indemnity ($500,000)

•Mutual indemnity (up to amount of insurance obtained “for the benefit of the

other party as indemnitee”) – no longer required to specify equal

amounts

Act does not apply to insurance that does not directly support the indemnity –

Getty

& Oryx

Texas Construction Anti‐Indemnity Act

• Bill submitted to address problem for Owner Controlled Insurance Programs (“OCIPs”)

• Wanted to make sure OCIP policy would provide insurance protection for some

minimum period of time beyond performance

Legislative History

• All that remains of original bill is Section 151.051– requires OCIP policy that provides general

liability insurance coverage to provide completed operations insurance coverage for a

minimum period of three years• Section 151.151 added to prohibit indemnity

provisions and certain insurance protection

OCIP Bill was Hijacked

SUBCHAPTER A. GENERAL PROVISIONS

Sec. 151.001.

DEFINITIONS.

In this chapter:(1)

"Consolidated insurance program”

means a

program under which a principal

provides general liability insurance coverage, workers' compensation

insurance coverage, or both that are incorporated into an insurance program for a . . . construction

project.

(8)

"Principal" means the person who procures the insurance policy under a consolidated insurance

program.

Sec. 151.001

DEFINITIONS (cont’d)

(2)

"Construction project" means construction, remodeling, maintenance, or repair of improvements

to real property.

The term includes the immediate construction location and areas incidental and

necessary to the work . . . .

(3)

"Contractor" means any person who has entered into a construction contract or a professional services contract and

is enrolled in the consolidated insurance

program.

Sec. 151.001

DEFINITIONS (cont’d)(5)

"Construction contract" means a contract, subcontract, . .

. entered into or made by an owner, architect, engineer, contractor, . . . for the design, construction, alteration, . . .

repair, or maintenance of, or for the furnishing of material or equipment for, a building, structure, . . . or other

improvement to or on . . . real property, including moving, demolition, and excavation connected with the real property.

(6)

"Indemnitor" means a party to a construction contract that is required to provide indemnification or additional

insured status to another party to the construction contract or to a third party.

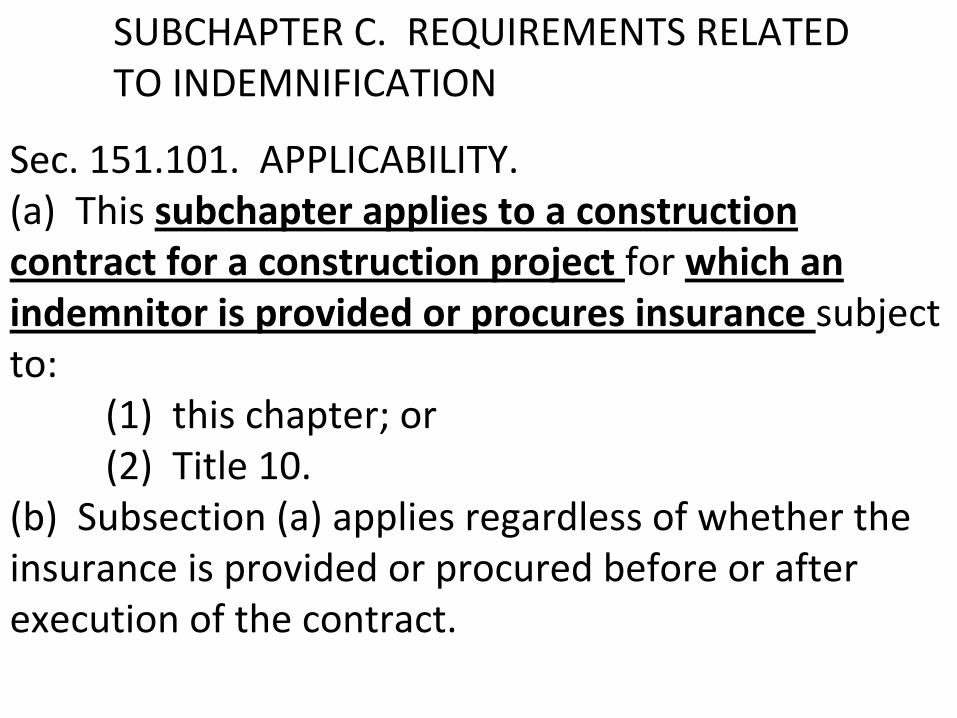

SUBCHAPTER C. REQUIREMENTS RELATED TO INDEMNIFICATION

Sec. 151.101.

APPLICABILITY. (a)

This subchapter applies to a construction

contract for a construction project for which an indemnitor is provided or procures insurance subject

to:(1)

this chapter; or

(2)

Title 10.(b)

Subsection (a) applies regardless of whether the

insurance is provided or procured before or after execution of the contract.

Sec. 151.102.

AGREEMENT VOID AND

UNENFORCEABLE.

Except . . . 151.103, a provision in a construction contract,

or in an agreement collateral to . . . , is void and unenforceable as against public policy

to the extent that it

requires an indemnitor to indemnify, hold harmless, or defend a party, including a third party, against a claim

caused by the negligence or fault, the breach or violation of a statute, ordinance, governmental regulation,

standard, or rule, or the breach of contract of the indemnitee, its agent or employee, or any third party

under the control or supervision of the indemnitee . . . .

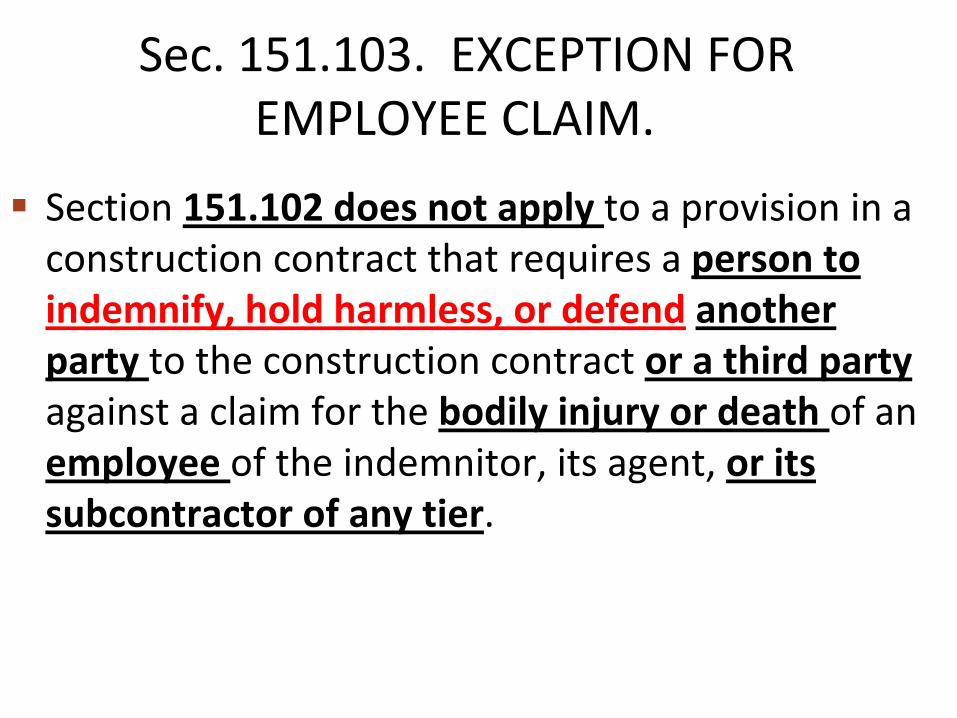

Sec. 151.103.

EXCEPTION FOR EMPLOYEE CLAIM.

Section 151.102 does not apply to a provision in a construction contract that requires a person to

indemnify, hold harmless, or defend

another party to the construction contract or a third party

against a claim for the bodily injury or death of an employee of the indemnitor, its agent, or its

subcontractor of any tier.

Sec. 151.104.

UNENFORCEABLE ADDITIONAL

INSURANCE PROVISION.(a)

Except as provided by Subsection (b), a provision in a

construction contract that requires the purchase of additional insured coverage, or any coverage endorsement,

or provision within an insurance policy providing additional insured coverage, is void and unenforceable

to the extent

that it requires or provides coverage the scope of which is prohibited under this subchapter for an agreement to

indemnify, hold harmless, or defend.(b)

This section does not apply to [an OCIP policy]

Sec. 151.105.

EXCLUSIONS.This subchapter does not affect:(1)

an [OCIP] insurance policy . . . ;

(3)

indemnity provisions contained in loan and financing documents, other than construction contracts to which the

contractor and owner's lender are parties . . . ;

(7)

agreements subject to [TOAIA];

Where Are We Now?

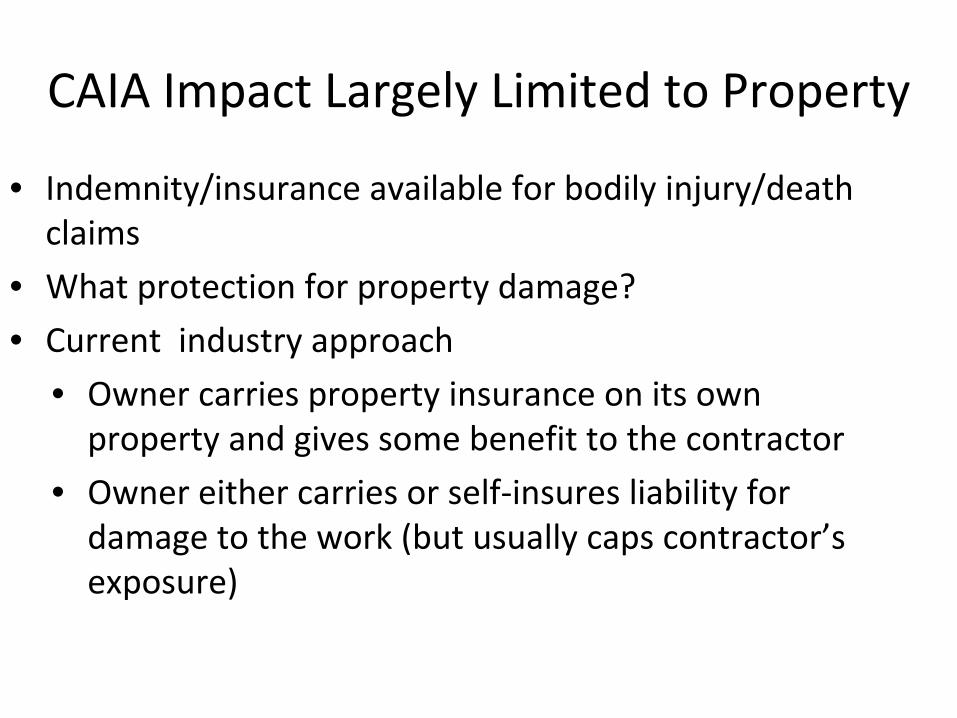

CAIA Impact Largely Limited to Property

• Indemnity/insurance available for bodily injury/death claims

• What protection for property damage?

• Current industry approach• Owner carries property insurance on its own

property and gives some benefit to the contractor

• Owner either carries or self‐insures liability for damage to the work (but usually caps contractor’s

exposure)

Best Case Argument

• CAIA does not prohibit owner of property from insuring its property and releasing its claim against

the other party

– “Releases”

are not prohibited

–No prohibition of “waivers of subrogation”

–Arguably nothing to prevent property owner from releasing all claims, regardless of fault, and

requiring its insurers to waive subrogation

Rationale

Statute only prohibits indemnity and additional insured, which address liability

claims

An owner should always be able to release

his own claim and require his insurer to do the same

Consistent with standard practice

Avoids duplicate insurance

Conclusion

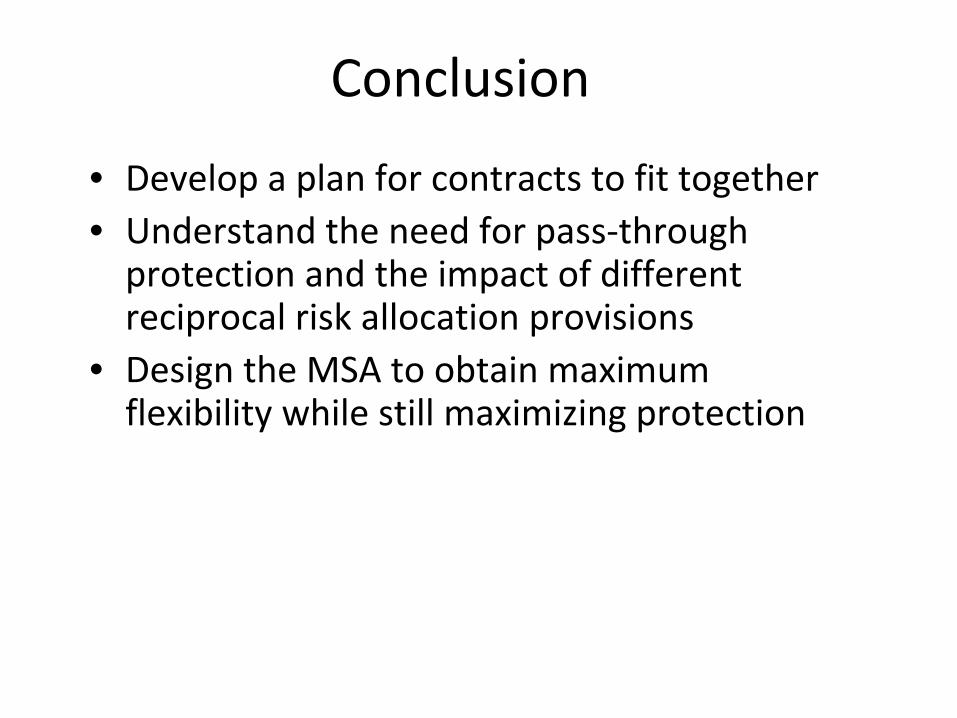

Conclusion

• Develop a plan for contracts to fit together• Understand the need for pass‐through

protection and the impact of different reciprocal risk allocation provisions

• Design the MSA to obtain maximum flexibility while still maximizing protection

Conclusion (cont’d)

• Try to anticipate and guard against carve‐ outs, gaps, and enforceability issues

• Indemnity and insurance are important risk allocation tools, but they must fit with an

overall plan to be effective

• Contracts may be more difficult to negotiate in a post‐Macondo world

• Texas CAIA raises some difficult questions

Conclusion (cont’d)

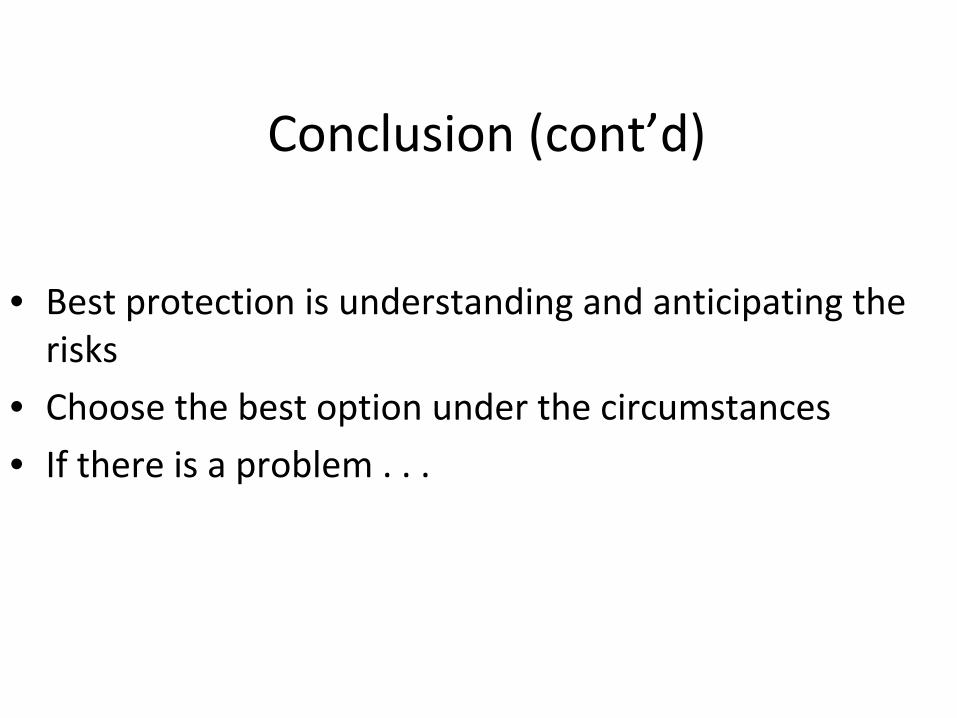

• Best protection is understanding and anticipating the risks

• Choose the best option under the circumstances

• If there is a problem . . .

55

If Problems do Occur – Learn to Cope

Flooding in Ireland