matthew chan & celena chen -...

TRANSCRIPT

Healthcare Investing Team

Matthew Chan & Celena Chen

Healthcare Investing Team

Healthcare Investing Team

INVESTMENT THESIS

2

Glybera’s launch in the EU will kickstart product revenue, facilitating deleveraging and helping to drive uniQure’s equity value

Vanguard gene therapy program in Hemophilia B presents significant upside if it reaches market− uniQure’s strong manufacturing capabilities and chosen gene cassette de-risk impending clinical trials

Current lack of FDA approval in the United States is misunderstood− We believe that the market sentiment has misinterpreted lack of US presence as speaking to the inefficacy of

Glybera− Clinical trial data points against this

Undervaluation

Upcoming profitability catalyst and underappreciated technology platform make QURE a long-term buy

Healthcare Investing Team

TABLE OF CONTENTS

3

1. Background & Overview

2. LPL-D Program

3. Hemophilia Program

4. Other programs

5. Valuation

6. Summary

Healthcare Investing Team

COMPANY OVERVIEW

4

uniQure is currently the first and only commercial-stage gene therapy company in the western world

Business

FinancialsCurrent Price (4/25/14) $26.09

Market Cap $559.11M

52-Week Range $8.29 - $35.50

Excess Cash on Balance Sheet 20.0%

EV/LTM EBITDA 11.5x

Develops adeno-associated virus (AAV)-based gene therapies for metabolic orphan diseases and broader hematological, cardiac and CNS indications.

Advanced clinical programs in LPL-D, Hemophilia B

Commercial-stage product, Glybera, approved by European Commission in 2012 for the treatment of familial lipoprotein lipase deficiency (LPLD), remains to be the only approved gene therapy on the western market

Partnership with leading international pharmaceutical company, Chiesi for imminent product launch in 2015

Phase I/II trials underway for Hemophilia B (AMT-061)

Acquisition of InoCard GMBH and collaboration with Bristol-Myers Squibb to develop cardiac disease franchises

Partner with private and academic institutions

Chiesi for Glybera EU commercialization and co-development of AMT-061

4D Molecular Therapeutics and Protein Sciences Corp for technology licensing, vector optimization

Acquire strong IP portfolio

Investment in R&D, manufacturing capabilities

Strategy

Healthcare Investing Team

GENE THERAPY INDUSTRY

5

Gene therapy is a young but appealing market due to its potential to effectively treat a variety of genetic disorders

Market Conditions

Roch

J&J14

Uniqur

Abbot

Sieme

Dana

Other30

Increasingly favorable regulatory environment

As signaled by FDA granting [insert examples of accelerated approval designation] to gene therapeutics in past year in response to increased safety in clinical trials

EMA has already authorized Glybera

Strict governance on biologics manufacturing standards

Policy environment

Pricing is an issue, along with insurance reiumbursement – potential for pay-per-performance and annuity pricing models

Competitive environment

11 players in space that promises to offer fundamental cures at a promise of high-price treatments ~$1M

Currently firms generate revenue from upfront licensing and collaboration payments, as well as licensing royalties and milestone payments

Healthcare Investing Team

PIPELINE OVERVIEW

6

uniQure’s drug development focuses on orphan as well as larger-scale chronic & degenerative diseases

Pipeline

Clinical Trial Progress

Currently developing drugs for Orphan diseases: Acute Intermittent Porphyria (AIP), Sanfilippo B Syndrome, and LPLD Large-scale chronic and degenerative diseases: Hemophilia A, Hemophilia B, Parkinson’s, and Congestive Heart

Failure

Glybera has been approved by the European Medicines Agency (EMA) and is targeted to treat its first patient in mid-2015

Glybera EUGlybera US

Hem BHem A

CHFAIP

Sanfillippo BParkinson's

Preclinical Phase I Phase II Phase III Market

AMT-021 for Acute Intermittent Porphyria (AIP): AAV5 vector containing PBGD gene for treatment of severe liver disorder

S100A1 for Congestive Heart Failure (CHF): stabilizes heart function by restoring concentration of protein that regulates cardiomyocyte-calcium network

AMT-110 for Sanfilippo B Syndrome: intra-cerebral administration of naGLU-gene to combat lysosomal storage malfunction in the brain

Exclusive license to GDNF therapeutic gene in NIH-funded clinical trial to treat Parkinson’s

Indication Highlights

Healthcare Investing Team

TABLE OF CONTENTS

7

1. Background & Overview

2. LPL-D Program

3. Hemophilia Program

4. Valuation

5. Summary

Healthcare Investing Team

LPL-D FRANCHISE

8

LPL-D is an orphan disease that causes severe hypertriglyceridemia, for which Glybera is the only therapy

Market Conditions

Glybera Delivers functional LPL gene variant in

recombinant AAV1 vector

Administered once at multiple intramuscular injection sites at a dose of 1E12 gc/kg

1M EUR benchmark price as determined in Germany dossier submission

LPL is important for lipid uptake in the bloodstream; deficiency leads to chronic pancreatitis

LPLD is unresponsive to standard therapeutics as fibrates; as such the treatment standard of care (SOC) limited to restricting dietary intake of fat with minimal mitigation of pancreatitis risk

Prevalence of 1-2 per million worldwide

Granted orphan drug exclusivity by EU until 2022

FDA orphan drug status guarantee as well

Healthcare Investing Team

GLYBERA US

9

Market misinterprets lack of uniQure presence in US

Current sentiment has not been supportive due to initial rejections by EMA and the narrow margins by which Glybera has been approved in the EU in 2012

However, this was due to insufficient evidence from a limited number of data-points; mature long-term data collected in 6-year retrospective analysis should facilitate adoption into the U.S.:− Approximate 40-50% reduction in post-treatment pancreatitis − No severe pancreatitis up to 6 years after Glybera treatments − 50% decrease in hospitalization rate− Generally well-tolerated, with no identifiable long-term safety concerns

FDA requires additional data in addition to demonstrating changes in chylomicron metabolism

QURE will identify additional endpoints by which to evaluate Glybera and file an SPA in the first half of 2015− If approved, poised to initiate Phase III study in US beginning 2016

Healthcare Investing Team

TABLE OF CONTENTS

10

1. Background & Overview

2. LPL-D Program

3. Hemophilia Program

4. Other programs

5. Valuation

6. Summary

Healthcare Investing Team

HEMOPHILIA B FRANCHISE

11

uniQure is well-positioned to be the first to market for first-in-class treatment of high unmet need

Market Conditions

Gene therapy advantages Recombinant factors just incremental

improvements in efficacy; still require regular prophylaxis

Anticoagulant targeting therapies knockdown natural antithrombin levels; do not actually produce missing factor

Major gene therapy players include Spark, Baxter and uniQure

Spark has not yet initiated trial; BAX just released data; QURE expected release preliminary data in mid-2015

Hemophilia B presents a USD $1.8B market

Prevalence of 1 in 30,000 males worldwide

Current standard of care requires a minimum of 2 IV infusions per week with per-patient lifetime cost upwards of US $10M

Painful, time-consuming; does not eliminate bleed episodes; compliance an issue

Hemophilia B is an ideal target for gene therapy as patients are readily accessible, factor level in blood can be easily monitored, and treatment is a question of expression of a single gene

Healthcare Investing Team

AMT-061

12

QURE’s gene cassette is founded in successful initial proof-of-concept study

St. Jude’s Trial Outcomes With FIX transgene and AAV8 vector

Sustained dose dependent effect over > 4 years after a single intervention

4/6 high dose patients achieved FIX expression > 5% of normal; did not require further FIX treatment; 4/7 on prophylaxis could stop prophylaxis

Licenses FIX transgene from St. Jude’s, which was proven in 2011 to display reduced need for prophylactic treatment after a single intervention

Exclusively licenses AAV5 vector from NIH− Same vector as used in AIP Phase I trial demonstrating AAV5 safety− Serotype where percentage of population with pre-existing neutralizing antibodies is likely the lowest

› As opposed to at least 14% of population with NABs unable to use AAV8 vector-based therapies of SPK and BAX

Currently undergoing Phase I dose-escalation study that cross references St. Jude’s and AMT-021 trial results

AIP (AMT-021) Phase I Doses up to 2E13 gc/kg, with detected successful

liver transfection in 6/8 patient in one-year follow-up

No liver enzyme perturbations noted or corticosteroid administrtion required

Implications for efficacy of AAV5 in liver-directed gene therapy

Healthcare Investing Team

TABLE OF CONTENTS

13

1. Background & Overview

2. LPL-D Program

3. Hemophilia Program

4. Other programs

5. Valuation

6. Summary

Healthcare Investing Team

VALUE DRIVER 1: GLYBERA LAUNCH

14

Commencement of Glybera’s commercial sales in 2015 will generate positive cash flows, helping to drive down debt and boost equity value

Expect to launch in Germany, Italy, UK; later on Japan, Israel, ME, Korea, Australia− Partnership with Italian corporation Chiesi Pharmaceuticals group, with 80 years of experience

exporting to 70 countries and direct presence in 25 −Receive payments from Chiesi for quantities of Glybera manufactured and supplied to them

› Their estimates anticipate retaining range of 20% to 30% net sales

Seek FDA Approval in 2018− Planned Phase 4 trial to start mid-2015; initial issue was with insufficient data

› Builds off six year follow-up study demonstrated 40-50% lower pancreatitis events, none severe

− Approval does not seem to pose major issue as Phase II/III evidence indicates significant improved chylomicron metabolism post-injection despite return to baseline triglyceride levels

Healthcare Investing Team

VALUE DRIVER 2: HEM B TRIAL DATA

15

uniQure is well-positioned to become leader in lucrative Hemophilia B space, with clinical Phase I trial results to come out later in 2015 Potential for first mover advantage

− Even without, distinct AAV5 serotype ensures reasonable market share

Positive Phase I endpoints would significantly de-risk AAV5 technology platform, as dosage is 10x what was used in successful initial St. Jude’s proof-of-concept study

Follows competitor BAX lackluster recent clinical trial data release

Competitor Trials BAX 335

2 of 4 subjects receiving the 2 highest doses of BAX 335 had Factor IX activity at about 10% of normal.

Of these 2 best responders, 1 demonstrated immune response

Dose-limiting toxicities apparent

Should not cause elevate liver enzymes if safety profile is similar to AMT-021

SPK-FIX

Expect to initiate SPK-FIX trial in first half of 2015

Healthcare Investing Team

QURE’S TECHNOLOGY PLATFORM

16

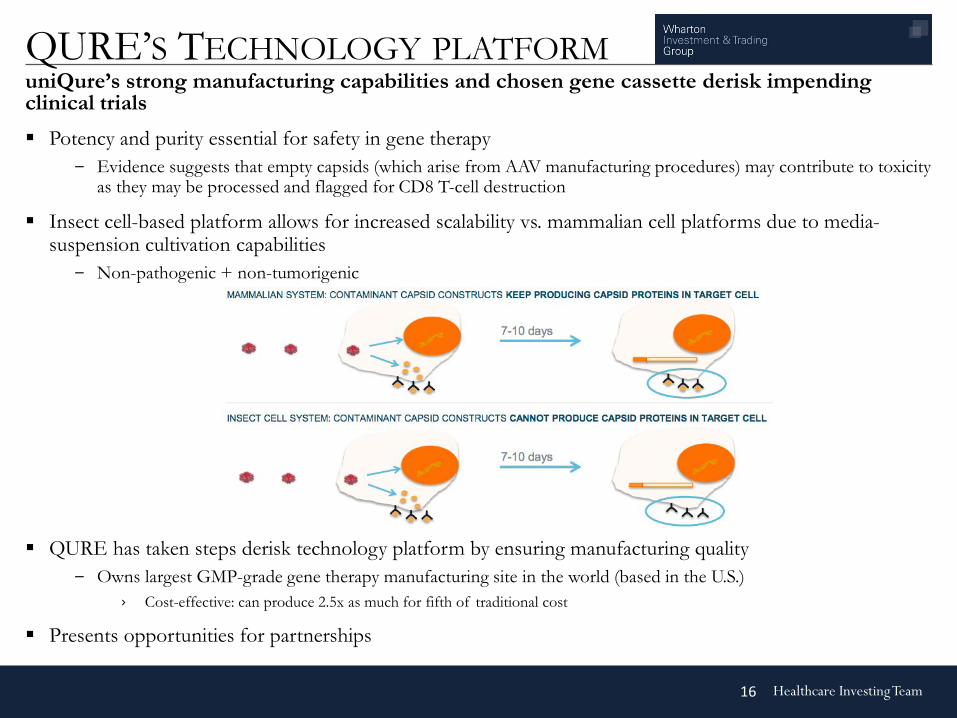

uniQure’s strong manufacturing capabilities and chosen gene cassette derisk impending clinical trials Potency and purity essential for safety in gene therapy

− Evidence suggests that empty capsids (which arise from AAV manufacturing procedures) may contribute to toxicity as they may be processed and flagged for CD8 T-cell destruction

Insect cell-based platform allows for increased scalability vs. mammalian cell platforms due to media-suspension cultivation capabilities− Non-pathogenic + non-tumorigenic

QURE has taken steps derisk technology platform by ensuring manufacturing quality − Owns largest GMP-grade gene therapy manufacturing site in the world (based in the U.S.)

› Cost-effective: can produce 2.5x as much for fifth of traditional cost

Presents opportunities for partnerships

Healthcare Investing Team

VALUATION

17

− Based on sum of parts analysis with primary pipeline programs in LPL-D and Hemophilia B, assuming 60 and 20 percent probability of approval in U.S., respectively

− 73% upside from current share price

Upside primarily in Hemophilia B franchise− LPL-D revenues marginal compared to Hemophilia B, even after conservative 20% probability weighting for AMT-

061

Estimated price per share: $45.66

Current price: $26.09

Upside: +%73

Healthcare Investing Team

REVENUE PROJECTIONS

18

Revenue Projections in ($mm)

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

450.0

500.0

2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E 2026E

Glybera

AMT-021

Healthcare Investing Team

SUMMARY

19

QURE is a long-term buy

Imminent revenue generation beginning this year to boost equity value

De-risking events have already occurred in manufacturing investment, vector serotype selection and demonstrated comparable clinical trials

Hemophilia B market indication and current progress relative to peers presents significant upside opportunity

Sentiment against Glybera is largely unfounded

Healthcare Investing Team

APPENDIX

Healthcare Investing Team

INCOME STATEMENT

21

Healthcare Investing Team

MODEL: DCF

22

Healthcare Investing Team

REVENUE BUILD

23

Healthcare Investing Team

REVENUE BUILD (CONT.)

24

Healthcare Investing Team

COGS & R&D

25