marico management meet-210910

TRANSCRIPT

Please refer to important disclosures at the end of this report 1

Core brands to post steady growth: Management is confident of driving 7-8% volume growth in Parachute aided by strong push of recruiter packs (5/10/20ml SKUs) and increased focus on rural growth. Saffola is expected to sustain 14-15% volume growth driven by strong positioning as a good-for-heart brand.

Copra and rice bran oil rise, ~3-5% price hikes taken: On a yoy basis YTD, copra prices have risen by almost 12-15%. However, in 2QFY2011, copra prices witnessed a steep rise of ~20-25% and rice bran oil is up almost 10% yoy. Hence, Marico has initiated another price hike in the 200ml SKU of ~5% (Rs40 to Rs42) in August and Rs3/litre hike (~3% hike) in Saffola Gold/ Saffola Active.

International business on strong footing, we peg 22% CAGR over FY10-12E: Management is confident of sustaining 20-25% growth across geographies driven by better distribution reach and new product launches. Moreover, current OPMs at ~12% in the international business are likely to improve to ~14% over 2-3 years aided by supply chain re-engineering and price increases.

Kaya domestic under consolidation, 4-6 clinics to be opened in Middle East: Focus in Kaya has now shifted to improve consumer experience and pushing product revenues higher. In 2QFY2011, Marico opened one more clinic in the Middle East and Bangladesh respectively, taking the total tally to 101 clinics. In FY2011, Marico plans to open no new clinics in India and around 4-6 clinics in the Middle East. During 3QFY2011, management plans to introduce Derma-Rx products in India/Middle East.

No major capex, tax guidance of ~19-20% maintained: Capex for FY2011E includes Rs15-20cr maintenance capex, Rs25cr additional capex for Baddi plant and Rs4-6cr for Kaya clinics. Management has maintained its guidance of ~19-20% tax guidance due to rising contribution from tax-saving plants (Baddi and Ponta Sahib) and international operations (low tax rate).

Outlook and Valuation: We have marginally tweaked our estimates upwards to account for: 1) recent price hikes, 2) stronger growth in international business, and 3) better margins aided by price hikes and improving profitability in the international business. At the CMP of Rs131, the stock is trading at 22.4x FY2012E earnings, which is justified given 22% earnings CAGR over FY2010-12E. Hence, we upgrade the stock from Neutral to Accumulate with a Target Price of Rs135 (Rs124) based on P/E multiple of 23x FY2012E earnings.

Key Financials (Consolidated) Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E

Net Sales 2,388 2,661 3,133 3,598

% chg 25.4 11.4 17.7 14.8

Net Profit 203.8 241.5 296.6 359.2

% chg 28.6 18.5 22.8 21.1

EBITDA (%) 12.7 14.1 13.7 14.0

EPS (Rs) 3.3 3.9 4.8 5.8

P/E (x) 39.5 33.3 27.1 22.4

P/BV (x) 17.6 12.2 8.9 6.7

RoE (%) 53.0 43.6 38.2 34.0

RoCE (%) 35.7 32.5 30.8 30.9

EV/Sales (x) 3.4 3.1 2.6 2.3

EV/EBITDA (x) 27.2 22.2 19.1 15.8

Source: Company, Angel Research

ACCUMULATE CMP Rs131 Target Price Rs135

Investment Period 12 Months Stock Info Sector FMCG

Market Cap (Rs cr) 7,988

Beta 0.4

52 Week High / Low 136/84

Avg. Daily Volume 1,78,289

Face Value (Rs) 1

BSE Sensex 20,002

Nifty 6,000

Reuters Code MRCO.BO

Bloomberg Code MRCO@IN

Shareholding Pattern (%) Promoters 63.5

MF / Banks / Indian Fls 7.3

FII / NRIs / OCBs 23.2

Indian Public / Others 6.0

Abs. (%) 3m 1yr 3yr

Sensex 11.9 19.5 20.8

Marico 12.4 50.8 128.2

Anand Shah 022 – 4040 3800 Ext: 334

Chitrangda Kapur 022 – 4040 3800 Ext: 323

Sreekanth P.V.S 022 – 4040 3800 Ext: 331

Marico Management Meet Note

Management Meet Note | Media

September 21, 2010

Marico | Management Meet Note

September 21, 2010 2

Parachute volumes to grow 7-8%, price hikes to aid value growth

Parachute to post steady 7-8% volume growth: Management is confident of driving 7-8% volume growth (Parachute rigids grew 14% in 1QFY2011) in Parachute coconut oil (CNO), which constitutes 30% of consolidated revenues, through conversion from loose/unbranded CNO (Rs750cr market, 40% of CNO volumes) aided by: 1) price cuts taken in 3QFY2010 in 50ml SKU (Rs12 to Rs10) and 100ml SKU (Rs21 to Rs20), 2) strong push of recruiter packs (5/10/20ml SKUs), and 3) increased focus on rural growth led by initiatives to improve quality of coverage (cover most outlets directly). We note that recruiter packs account for 15-20% volumes of Parachute rigids (which is 75% of overall Parachute CNO volumes). However, flexi-packs (non-focus, high volumes, low-margin), which are largely used to enable conversion from loose oil, account for 25% of the remaining volumes and posted marginal decline in 1QFY2011 dragging overall growth of Parachute CNO to 11%.

Second round of price hikes initiated in August, more cannot be ruled out: Post the ~2.5% price hike (Rs39 to Rs40) in the Parachute 200ml SKU in 4QFY2010, Marico initiated another price hike in the 200ml SKU of ~5% (Rs40 to Rs42) in August along with reversing the price cut in the 100ml SKU (increased back to Rs21 from Rs20). However, the 500ml SKU prices, which were increased from Rs90-92 in 4QFY2010, have been left untouched. We note that the 200ml SKU constitutes 35%, 500ml SKU constitute 30% and 50/100ml SKU constitutes 15-20% of Parachute rigid volumes.

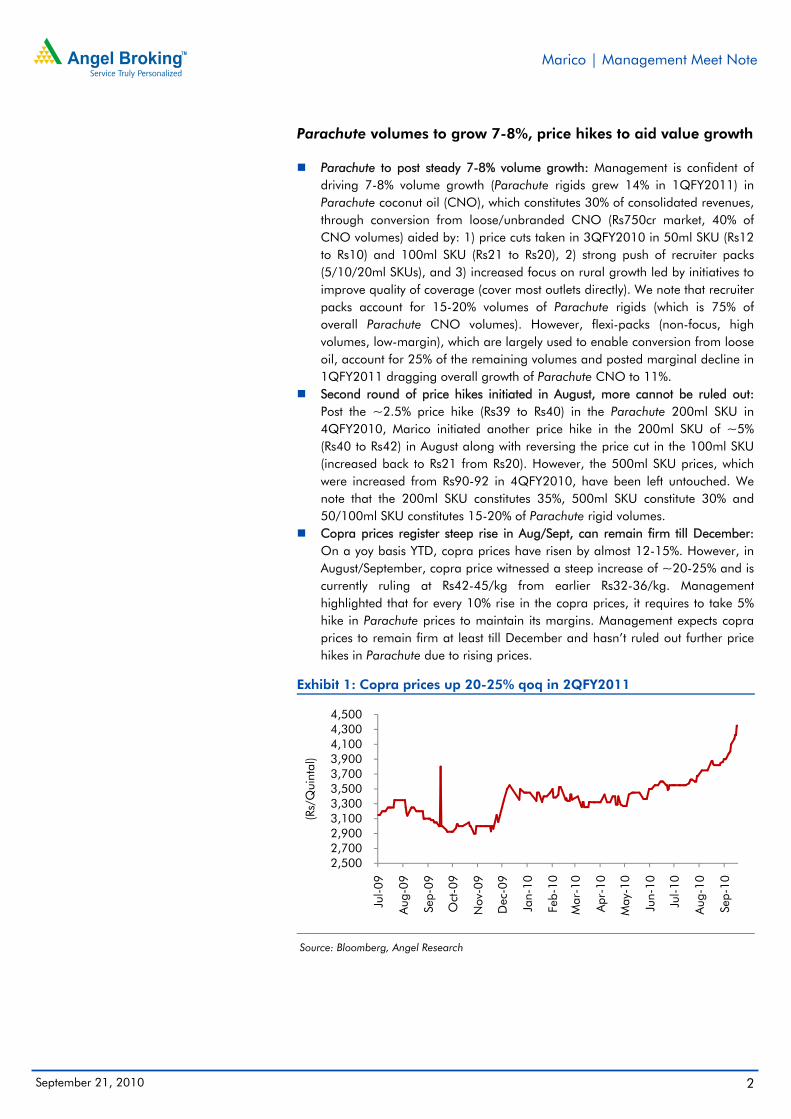

Copra prices register steep rise in Aug/Sept, can remain firm till December: On a yoy basis YTD, copra prices have risen by almost 12-15%. However, in August/September, copra price witnessed a steep increase of ~20-25% and is currently ruling at Rs42-45/kg from earlier Rs32-36/kg. Management highlighted that for every 10% rise in the copra prices, it requires to take 5% hike in Parachute prices to maintain its margins. Management expects copra prices to remain firm at least till December and hasn’t ruled out further price hikes in Parachute due to rising prices.

Exhibit 1: Copra prices up 20-25% qoq in 2QFY2011

Source: Bloomberg, Angel Research

2,500 2,700 2,900 3,100 3,300 3,500 3,700 3,900 4,100 4,300 4,500

Jul-

09

Aug

-09

Sep-

09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-

10

Aug

-10

Sep-

10

(Rs/

Qui

ntal

)

Marico | Management Meet Note

September 21, 2010 3

Saffola to grow 14-15%; focus on extension into foods to rise

Management confident of sustaining 14-15% volume growth in Saffola: Based on its strong positioning as a good-for-heart brand coupled with relatively zero competition in the premium ROCP category (97% market share in Safflower segment, 54% market share when Sundrop considered as a universe), management is confident of sustaining 14-15% volume growth in Saffola ROCP. During 1QFY2011, Saffola posted a strong growth of 17% yoy partially aided by the promotional offer (20% extra, 1kg pouch free with 5kg) on select SKUs. However, management re-iterated that quantum of promotional volume has reduced significantly yoy.

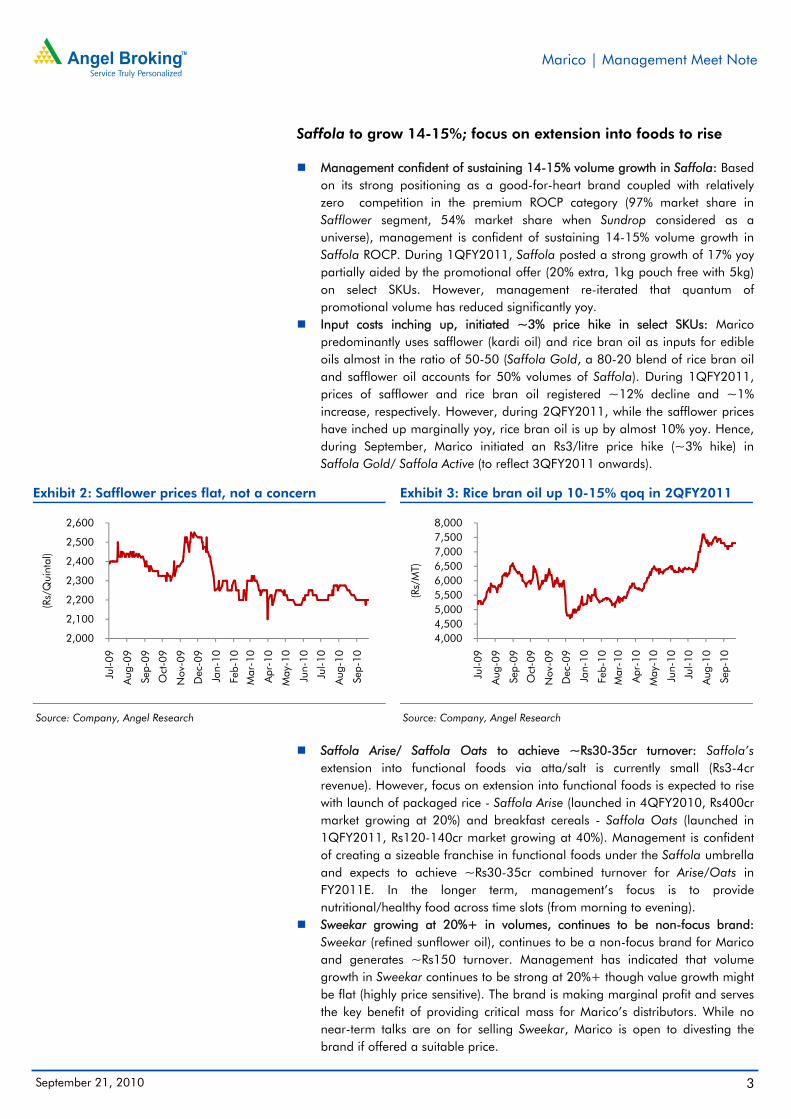

Input costs inching up, initiated ~3% price hike in select SKUs: Marico predominantly uses safflower (kardi oil) and rice bran oil as inputs for edible oils almost in the ratio of 50-50 (Saffola Gold, a 80-20 blend of rice bran oil and safflower oil accounts for 50% volumes of Saffola). During 1QFY2011, prices of safflower and rice bran oil registered ~12% decline and ~1% increase, respectively. However, during 2QFY2011, while the safflower prices have inched up marginally yoy, rice bran oil is up by almost 10% yoy. Hence, during September, Marico initiated an Rs3/litre price hike (~3% hike) in Saffola Gold/ Saffola Active (to reflect 3QFY2011 onwards).

Exhibit 2: Safflower prices flat, not a concern

Source: Company, Angel Research

Exhibit 3: Rice bran oil up 10-15% qoq in 2QFY2011

Source: Company, Angel Research

Saffola Arise/ Saffola Oats to achieve ~Rs30-35cr turnover: Saffola’s

extension into functional foods via atta/salt is currently small (Rs3-4cr revenue). However, focus on extension into functional foods is expected to rise with launch of packaged rice - Saffola Arise (launched in 4QFY2010, Rs400cr market growing at 20%) and breakfast cereals - Saffola Oats (launched in 1QFY2011, Rs120-140cr market growing at 40%). Management is confident of creating a sizeable franchise in functional foods under the Saffola umbrella and expects to achieve ~Rs30-35cr combined turnover for Arise/Oats in FY2011E. In the longer term, management’s focus is to provide nutritional/healthy food across time slots (from morning to evening).

Sweekar growing at 20%+ in volumes, continues to be non-focus brand: Sweekar (refined sunflower oil), continues to be a non-focus brand for Marico and generates ~Rs150 turnover. Management has indicated that volume growth in Sweekar continues to be strong at 20%+ though value growth might be flat (highly price sensitive). The brand is making marginal profit and serves the key benefit of providing critical mass for Marico’s distributors. While no near-term talks are on for selling Sweekar, Marico is open to divesting the brand if offered a suitable price.

2,000

2,100

2,200

2,300

2,400

2,500

2,600

Jul-

09

Aug

-09

Sep-

09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-

10

Aug

-10

Sep-

10

(Rs/

Qui

ntal

)

4,000 4,500 5,000 5,500 6,000 6,500 7,000 7,500 8,000

Jul-

09

Aug

-09

Sep-

09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-

10

Aug

-10

Sep-

10

(Rs/

MT)

Marico | Management Meet Note

September 21, 2010 4

Hair oils poised for robust growth, prototypes hold promise

Hair oils to grow in excess of 20%+ in FY2011E: Marico is a dominant player in the Rs2,600cr hair oils market with volume market share of 22% (Dabur stands at 30%). While management is confident of achieving 15-20% growth in hair oils over FY2010-12E, we believe FY2011E is likely to witness a stronger 22% yoy growth driven by robust 1QFY2011(27% yoy growth) led by market share gains (up 150bp yoy). Shanti Badam Amla, which accounts for ~15% of its hair oils portfolio, has gained significant market share (up from 8-9% in January to 13% in September) post the 20-25% price cut taken in January 2010. During 1QFY2011, Shanti Badam Amla recorded a strong growth of 92% yoy.

Cooling oil prototypes doing well, possible launch next summer: Marico’s plans to enter cooling oils (~18% of hair oils market in volume terms) are on track with its two prototypes – Nihar Natural Coconut Cooling Oil in Bihar and Parachute Advansed Coconut Cooling Oil in Andhra Pradesh doing well. Marico is confident of tasting success in cooling oils this time around due to the differentiated offerings (coconut oil based cooling oils) unlike its earlier prototype, Maha Thanda. Parachute Advansed Coconut Cooling Oil has already gained 5% market share in Andhra Pradesh and achieved Rs5cr turnover. Marico is looking to launch these products nationally next summer.

New prototype – Parachute Advansed Ayurvedic Hair Oil launched in South: Recently, Marico announced the launch of another prototype - Parachute Advansed Ayurvedic Hair Oil, a combination of ayurvedic herbs in coconut oil, which guarantees hair fall control. The prototype is being test marketed in the South and retails for Rs20 for 50ml SKU. According to management, the market for such products is around Rs200cr.

International business on strong footing, profitability to rise

Management confident of 20%+ growth, we peg 22% CAGR over FY10-12E: Marico’s international business grew a strong 22% in 1QFY2011 (17% volume growth, 12% pricing growth and 7% decline due to translation loss) and now contributes 23% to consolidated revenues (25% including Kaya’s Middle East business). Management is confident of sustaining 20-25% growth across geographies (Bangladesh, Gulf, Egypt and South Africa) driven by better distribution reach and new product launches. We have modeled in 22% CAGR in the international business over FY2010-12E.

Takeaways from different geographies: Bangladesh (contributes 50% of international business revenues) registered strong 45% CAGR over the last 3-4 years driven by Parachute (90% of business). Over the next few years, Marico plans to grow the Bangladesh market by leveraging its strong distribution network and new product launches (HairCode hair dye launched earlier has garnered 20% market share, Saffola launched in 1QFY2011). In Egypt, Fiancee and HairCode enjoy 57% market share. Marico plans to launch Parachute in Egypt (for women) and HairCode in the Middle East (for men). The Egypt facility is now fully stabilised. Hence, exports from India (reflected in standalone) are likely to drop as the Egypt facility ramps up to cater to GCC.

Margins to improve, low tax rates to boost overall profitability: Besides Bangladesh (27% tax rate), most other geographies are tax free (South Africa has accumulated losses) and will help consolidated group tax rate to remain below 20%. Moreover, current OPMs at ~12% in the international business are likely to improve to ~14% over the next 2-3 years aided by supply chain re-engineering and price increases.

Marico | Management Meet Note

September 21, 2010 5

Kaya domestic under consolidation, Derma-Rx to boost revenues

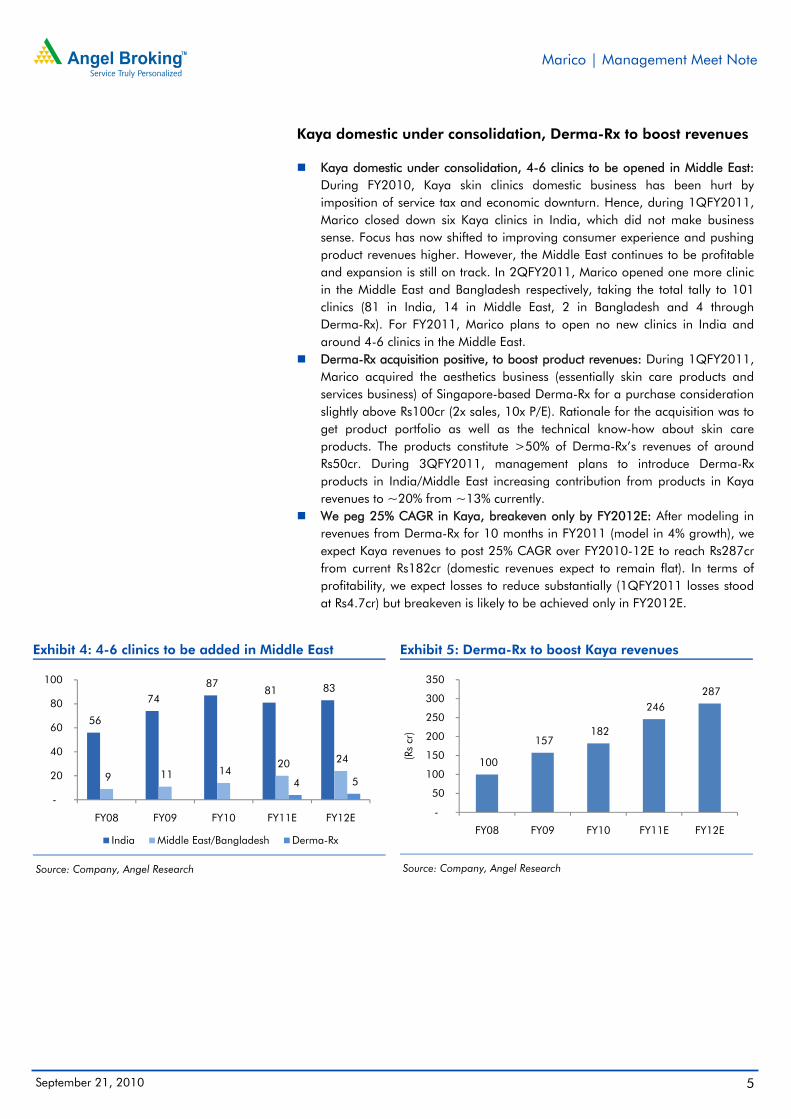

Kaya domestic under consolidation, 4-6 clinics to be opened in Middle East: During FY2010, Kaya skin clinics domestic business has been hurt by imposition of service tax and economic downturn. Hence, during 1QFY2011, Marico closed down six Kaya clinics in India, which did not make business sense. Focus has now shifted to improving consumer experience and pushing product revenues higher. However, the Middle East continues to be profitable and expansion is still on track. In 2QFY2011, Marico opened one more clinic in the Middle East and Bangladesh respectively, taking the total tally to 101 clinics (81 in India, 14 in Middle East, 2 in Bangladesh and 4 through Derma-Rx). For FY2011, Marico plans to open no new clinics in India and around 4-6 clinics in the Middle East.

Derma-Rx acquisition positive, to boost product revenues: During 1QFY2011, Marico acquired the aesthetics business (essentially skin care products and services business) of Singapore-based Derma-Rx for a purchase consideration slightly above Rs100cr (2x sales, 10x P/E). Rationale for the acquisition was to get product portfolio as well as the technical know-how about skin care products. The products constitute >50% of Derma-Rx’s revenues of around Rs50cr. During 3QFY2011, management plans to introduce Derma-Rx products in India/Middle East increasing contribution from products in Kaya revenues to ~20% from ~13% currently.

We peg 25% CAGR in Kaya, breakeven only by FY2012E: After modeling in revenues from Derma-Rx for 10 months in FY2011 (model in 4% growth), we expect Kaya revenues to post 25% CAGR over FY2010-12E to reach Rs287cr from current Rs182cr (domestic revenues expect to remain flat). In terms of profitability, we expect losses to reduce substantially (1QFY2011 losses stood at Rs4.7cr) but breakeven is likely to be achieved only in FY2012E.

Exhibit 4: 4-6 clinics to be added in Middle East

Source: Company, Angel Research

Exhibit 5: Derma-Rx to boost Kaya revenues

Source: Company, Angel Research

56

74 87

81 83

9 11 14 20 24

4 5

-

20

40

60

80

100

FY08 FY09 FY10 FY11E FY12E

India Middle East/Bangladesh Derma-Rx

100

157 182

246 287

-

50

100

150

200

250

300

350

FY08 FY09 FY10 FY11E FY12E

(Rs

cr)

Marico | Management Meet Note

September 21, 2010 6

Investment Rationale

Steady volumes in core brands, new prototypes promising: We expect Marico’s core brands, Parachute and Saffola, to deliver sustainable volume growth of 6-8% and 14-15% respectively, during FY2010-12E. Moreover, Marico’s entry into cooling oils (~18% of hair oils market in volume terms) via Nihar Natural Coconut Cooling Oil/Parachute Advansed Coconut Cooling Oil coupled with initial success of Saffola Arise and introduction of Soffola Oats (management expects Rs35cr revenues in FY2011E from rice and oats) looks promising.

Robust growth in international business: Strong presence in emerging markets coupled with series of acquisitions (Egypt, South Africa, Malaysia) have helped Marico post strong growth in its international business, which now contributes ~23% to consolidated revenues. We have modeled in a robust 22% CAGR in international revenues over FY2010-12E and expect high incremental contribution to overall profitability (better margins and lower tax rates).

Kaya’s long-term potential intact, near-term consolidation: Over the last

several quarters, Marico has consolidated its Kaya operations in India post the dip in same store sales growth due to service tax imposition and economic downturn. However, post consolidation (six clinics closed in India), we believe profitability is likely to improve in Kaya and revenue traction is likely to pick up on a low base. Moreover, acquisition of Derma Rx (Rs50cr revenue) is likely to be EPS accretive and holds synergistic benefits for Kaya in India (management expects the same to help product revenues increase from ~13% to 20% in Kaya). Over FY2010-12E, we have modeled in 13% CAGR in standalone Kaya revenues and 25% CAGR including Derma Rx revenues.

Outlook and Valuation Post management meet, we have marginally tweaked our estimates upwards to account for: 1) recent price hikes in Parachute and Saffola, 2) stronger growth in international business, and 3) better margins aided by price hikes and improving profitability in international business.

Exhibit 6: Change in Estimates

Old Estimate New Estimate % chg

(Rs cr) FY11E FY12E FY11E FY12E FY11E FY12E

Revenue 3,121 3,586 3,133 3,598 0.4 0.3

OPM (%) 13.7 13.8 13.7 14.0 (5) 15

EPS (Rs) 4.7 5.6 4.8 5.8 2.8 4.4

Source: Company, Angel Research

At the CMP of Rs131, the stock is trading at 22.4x FY2012E earnings, which is justified given the 22% earnings CAGR over FY2010-12E. Hence, we upgrade the stock from Neutral to Accumulate (modeling in our upgrade in estimates by ~3-4%) with a Target Price of Rs135 (Rs124) based on P/E multiple of 23x FY2012E earnings (at 10% premium to its historical valuations).

Marico | Management Meet Note

September 21, 2010 7

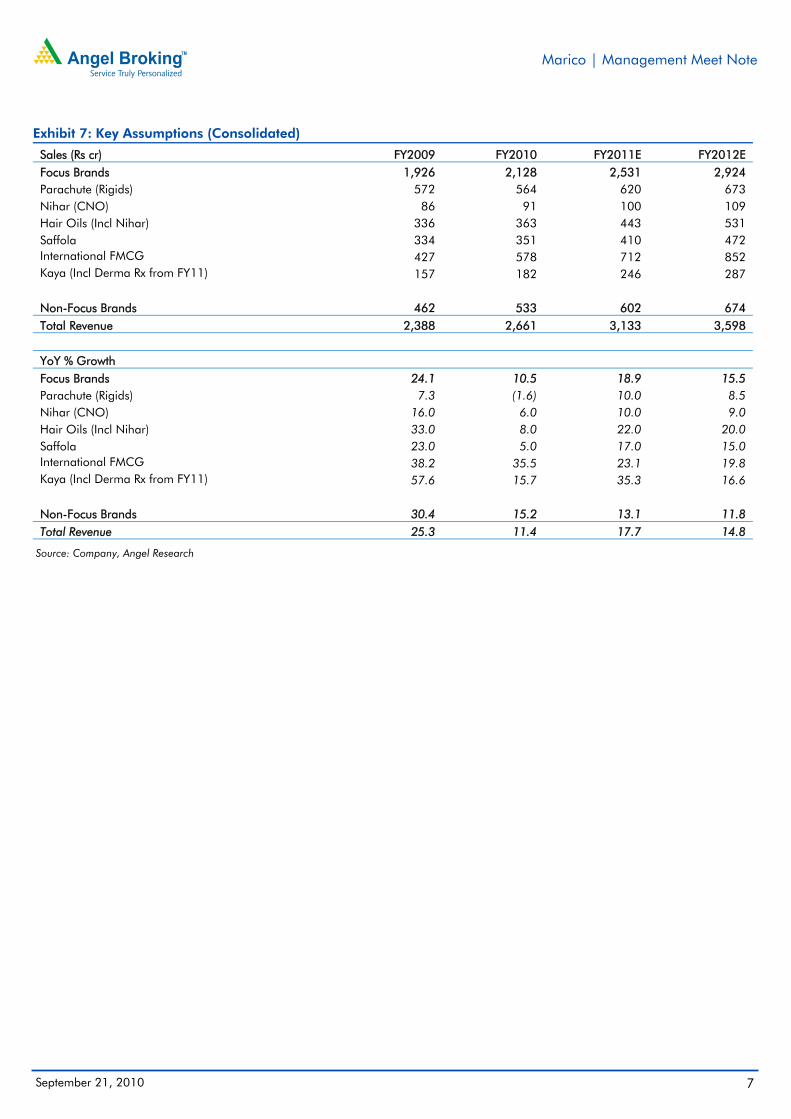

Exhibit 7: Key Assumptions (Consolidated)

Sales (Rs cr) FY2009 FY2010 FY2011E FY2012E Focus Brands 1,926 2,128 2,531 2,924 Parachute (Rigids) 572 564 620 673 Nihar (CNO) 86 91 100 109 Hair Oils (Incl Nihar) 336 363 443 531 Saffola 334 351 410 472 International FMCG 427 578 712 852 Kaya (Incl Derma Rx from FY11) 157 182 246 287

Non-Focus Brands 462 533 602 674 Total Revenue 2,388 2,661 3,133 3,598

YoY % Growth Focus Brands 24.1 10.5 18.9 15.5 Parachute (Rigids) 7.3 (1.6) 10.0 8.5 Nihar (CNO) 16.0 6.0 10.0 9.0 Hair Oils (Incl Nihar) 33.0 8.0 22.0 20.0 Saffola 23.0 5.0 17.0 15.0 International FMCG 38.2 35.5 23.1 19.8 Kaya (Incl Derma Rx from FY11) 57.6 15.7 35.3 16.6

Non-Focus Brands 30.4 15.2 13.1 11.8 Total Revenue 25.3 11.4 17.7 14.8

Source: Company, Angel Research

Marico | Management Meet Note

September 21, 2010 8

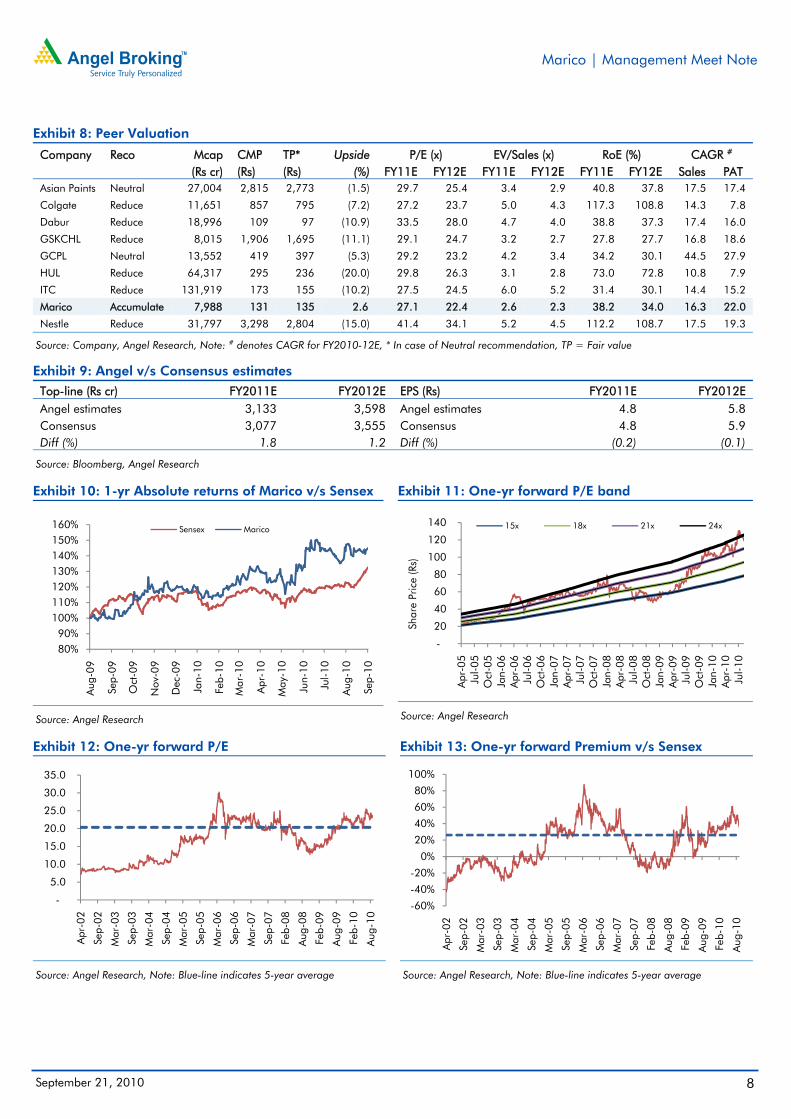

Exhibit 8: Peer Valuation

Company Reco Mcap CMP TP* Upside P/E (x) EV/Sales (x) RoE (%) CAGR # (Rs cr) (Rs) (Rs) (%) FY11E FY12E FY11E FY12E FY11E FY12E Sales PAT Asian Paints Neutral 27,004 2,815 2,773 (1.5) 29.7 25.4 3.4 2.9 40.8 37.8 17.5 17.4

Colgate Reduce 11,651 857 795 (7.2) 27.2 23.7 5.0 4.3 117.3 108.8 14.3 7.8

Dabur Reduce 18,996 109 97 (10.9) 33.5 28.0 4.7 4.0 38.8 37.3 17.4 16.0

GSKCHL Reduce 8,015 1,906 1,695 (11.1) 29.1 24.7 3.2 2.7 27.8 27.7 16.8 18.6

GCPL Neutral 13,552 419 397 (5.3) 29.2 23.2 4.2 3.4 34.2 30.1 44.5 27.9

HUL Reduce 64,317 295 236 (20.0) 29.8 26.3 3.1 2.8 73.0 72.8 10.8 7.9

ITC Reduce 131,919 173 155 (10.2) 27.5 24.5 6.0 5.2 31.4 30.1 14.4 15.2

Marico Accumulate 7,988 131 135 2.6 27.1 22.4 2.6 2.3 38.2 34.0 16.3 22.0

Nestle Reduce 31,797 3,298 2,804 (15.0) 41.4 34.1 5.2 4.5 112.2 108.7 17.5 19.3

Source: Company, Angel Research, Note: # denotes CAGR for FY2010-12E, * In case of Neutral recommendation, TP = Fair value

Exhibit 9: Angel v/s Consensus estimates Top-line (Rs cr) FY2011E FY2012E EPS (Rs) FY2011E FY2012E Angel estimates 3,133 3,598 Angel estimates 4.8 5.8 Consensus 3,077 3,555 Consensus 4.8 5.9 Diff (%) 1.8 1.2 Diff (%) (0.2) (0.1)

Source: Bloomberg, Angel Research

Exhibit 10: 1-yr Absolute returns of Marico v/s Sensex

Source: Angel Research

Exhibit 11: One-yr forward P/E band

Source: Angel Research

Exhibit 12: One-yr forward P/E

Source: Angel Research, Note: Blue-line indicates 5-year average

Exhibit 13: One-yr forward Premium v/s Sensex

Source: Angel Research, Note: Blue-line indicates 5-year average

80%90%

100%110%120%130%140%150%160%

Aug

-09

Sep-

09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-

10

Aug

-10

Sep-

10

Sensex Marico

-

20

40

60

80

100

120

140

Apr

-05

Jul-

05O

ct-0

5Ja

n-06

Apr

-06

Jul-

06O

ct-0

6Ja

n-07

Apr

-07

Jul-

07O

ct-0

7Ja

n-08

Apr

-08

Jul-

08O

ct-0

8Ja

n-09

Apr

-09

Jul-

09O

ct-0

9Ja

n-10

Apr

-10

Jul-

10

Shar

e Pr

ice

(Rs)

15x 18x 21x 24x

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Apr

-02

Sep-

02

Mar

-03

Sep-

03

Mar

-04

Sep-

04

Mar

-05

Sep-

05

Mar

-06

Sep-

06

Mar

-07

Sep-

07

Feb-

08

Aug

-08

Feb-

09

Aug

-09

Feb-

10

Aug

-10

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

Apr

-02

Sep-

02

Mar

-03

Sep-

03

Mar

-04

Sep-

04

Mar

-05

Sep-

05

Mar

-06

Sep-

06

Mar

-07

Sep-

07

Feb-

08

Aug

-08

Feb-

09

Aug

-09

Feb-

10

Aug

-10

Marico | Management Meet Note

September 21, 2010 9

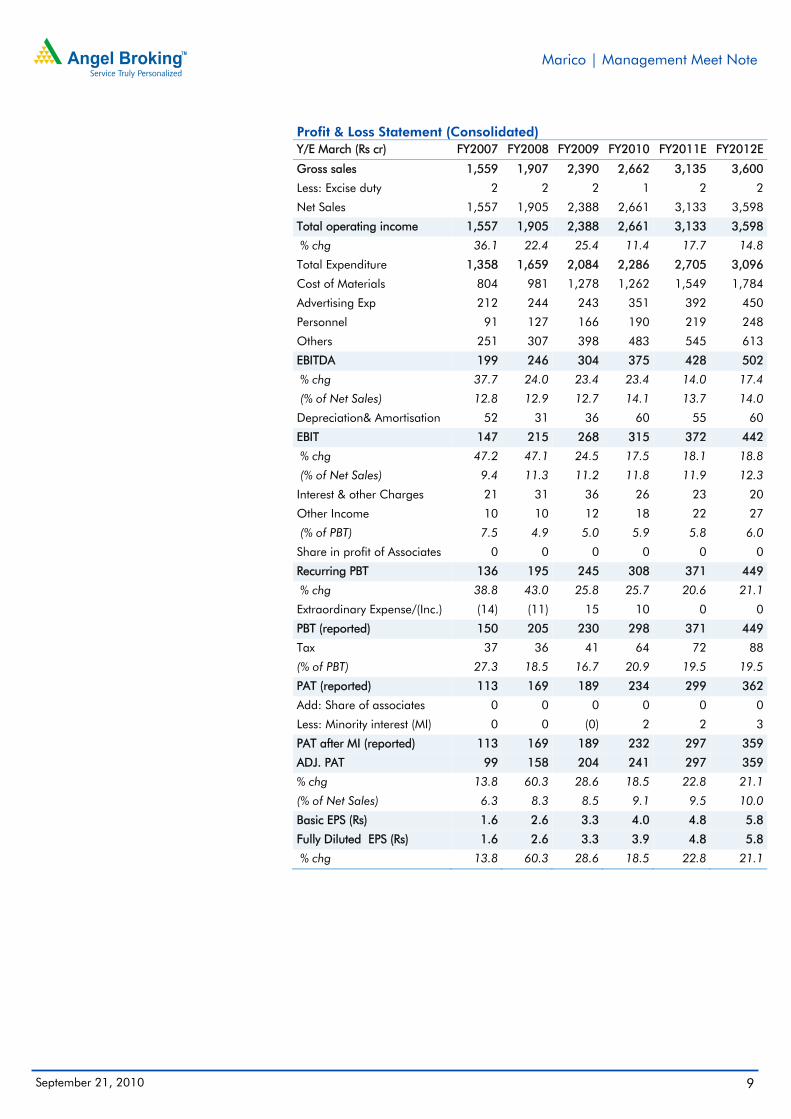

Profit & Loss Statement (Consolidated) Y/E March (Rs cr) FY2007 FY2008 FY2009 FY2010 FY2011E FY2012E

Gross sales 1,559 1,907 2,390 2,662 3,135 3,600

Less: Excise duty 2 2 2 1 2 2

Net Sales 1,557 1,905 2,388 2,661 3,133 3,598

Total operating income 1,557 1,905 2,388 2,661 3,133 3,598

% chg 36.1 22.4 25.4 11.4 17.7 14.8

Total Expenditure 1,358 1,659 2,084 2,286 2,705 3,096

Cost of Materials 804 981 1,278 1,262 1,549 1,784

Advertising Exp 212 244 243 351 392 450

Personnel 91 127 166 190 219 248

Others 251 307 398 483 545 613

EBITDA 199 246 304 375 428 502

% chg 37.7 24.0 23.4 23.4 14.0 17.4

(% of Net Sales) 12.8 12.9 12.7 14.1 13.7 14.0

Depreciation& Amortisation 52 31 36 60 55 60

EBIT 147 215 268 315 372 442

% chg 47.2 47.1 24.5 17.5 18.1 18.8

(% of Net Sales) 9.4 11.3 11.2 11.8 11.9 12.3

Interest & other Charges 21 31 36 26 23 20

Other Income 10 10 12 18 22 27

(% of PBT) 7.5 4.9 5.0 5.9 5.8 6.0

Share in profit of Associates 0 0 0 0 0 0

Recurring PBT 136 195 245 308 371 449

% chg 38.8 43.0 25.8 25.7 20.6 21.1

Extraordinary Expense/(Inc.) (14) (11) 15 10 0 0

PBT (reported) 150 205 230 298 371 449

Tax 37 36 41 64 72 88

(% of PBT) 27.3 18.5 16.7 20.9 19.5 19.5

PAT (reported) 113 169 189 234 299 362

Add: Share of associates 0 0 0 0 0 0

Less: Minority interest (MI) 0 0 (0) 2 2 3

PAT after MI (reported) 113 169 189 232 297 359

ADJ. PAT 99 158 204 241 297 359

% chg 13.8 60.3 28.6 18.5 22.8 21.1

(% of Net Sales) 6.3 8.3 8.5 9.1 9.5 10.0

Basic EPS (Rs) 1.6 2.6 3.3 4.0 4.8 5.8

Fully Diluted EPS (Rs) 1.6 2.6 3.3 3.9 4.8 5.8

% chg 13.8 60.3 28.6 18.5 22.8 21.1

Marico | Management Meet Note

September 21, 2010 10

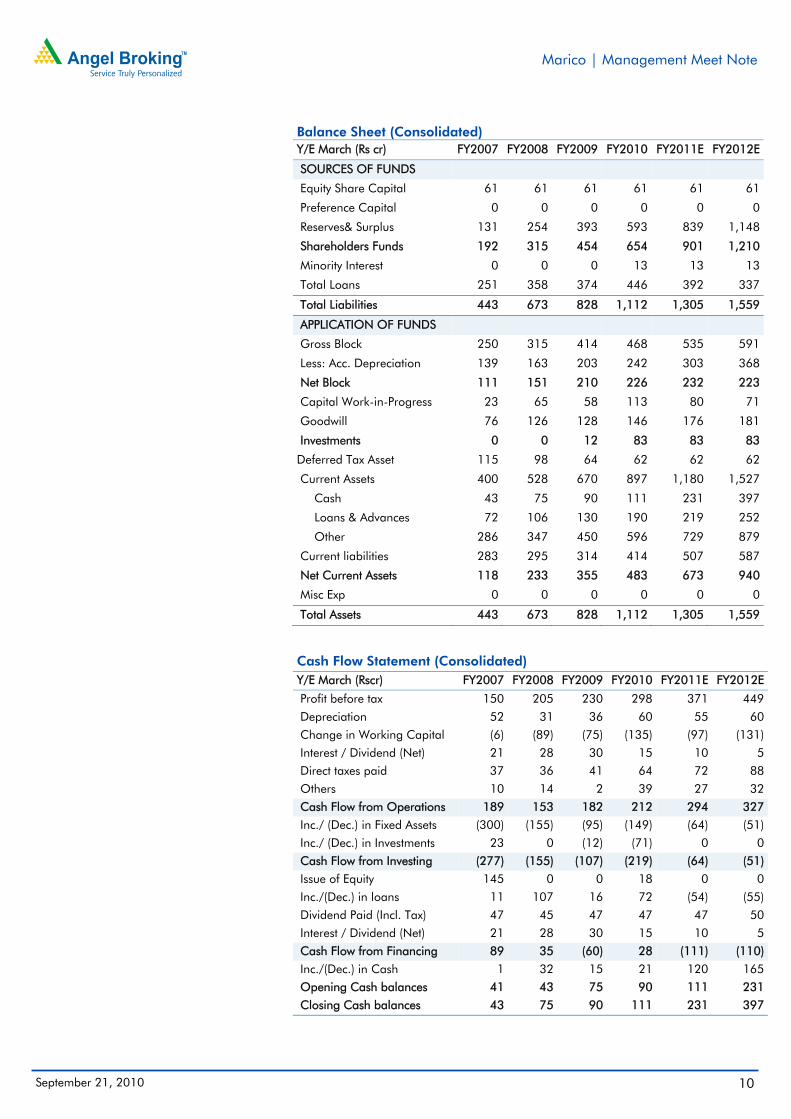

Balance Sheet (Consolidated) Y/E March (Rs cr) FY2007 FY2008 FY2009 FY2010 FY2011E FY2012E

SOURCES OF FUNDS

Equity Share Capital 61 61 61 61 61 61

Preference Capital 0 0 0 0 0 0

Reserves& Surplus 131 254 393 593 839 1,148

Shareholders Funds 192 315 454 654 901 1,210

Minority Interest 0 0 0 13 13 13

Total Loans 251 358 374 446 392 337

Total Liabilities 443 673 828 1,112 1,305 1,559

APPLICATION OF FUNDS

Gross Block 250 315 414 468 535 591

Less: Acc. Depreciation 139 163 203 242 303 368

Net Block 111 151 210 226 232 223

Capital Work-in-Progress 23 65 58 113 80 71

Goodwill 76 126 128 146 176 181

Investments 0 0 12 83 83 83

Deferred Tax Asset 115 98 64 62 62 62

Current Assets 400 528 670 897 1,180 1,527

Cash 43 75 90 111 231 397

Loans & Advances 72 106 130 190 219 252

Other 286 347 450 596 729 879

Current liabilities 283 295 314 414 507 587

Net Current Assets 118 233 355 483 673 940

Misc Exp 0 0 0 0 0 0

Total Assets 443 673 828 1,112 1,305 1,559

Cash Flow Statement (Consolidated) Y/E March (Rscr) FY2007 FY2008 FY2009 FY2010 FY2011E FY2012E

Profit before tax 150 205 230 298 371 449

Depreciation 52 31 36 60 55 60

Change in Working Capital (6) (89) (75) (135) (97) (131)

Interest / Dividend (Net) 21 28 30 15 10 5

Direct taxes paid 37 36 41 64 72 88

Others 10 14 2 39 27 32

Cash Flow from Operations 189 153 182 212 294 327

Inc./ (Dec.) in Fixed Assets (300) (155) (95) (149) (64) (51)

Inc./ (Dec.) in Investments 23 0 (12) (71) 0 0

Cash Flow from Investing (277) (155) (107) (219) (64) (51)

Issue of Equity 145 0 0 18 0 0

Inc./(Dec.) in loans 11 107 16 72 (54) (55)

Dividend Paid (Incl. Tax) 47 45 47 47 47 50

Interest / Dividend (Net) 21 28 30 15 10 5

Cash Flow from Financing 89 35 (60) 28 (111) (110)

Inc./(Dec.) in Cash 1 32 15 21 120 165

Opening Cash balances 41 43 75 90 111 231

Closing Cash balances 43 75 90 111 231 397

Marico | Management Meet Note

September 21, 2010 11

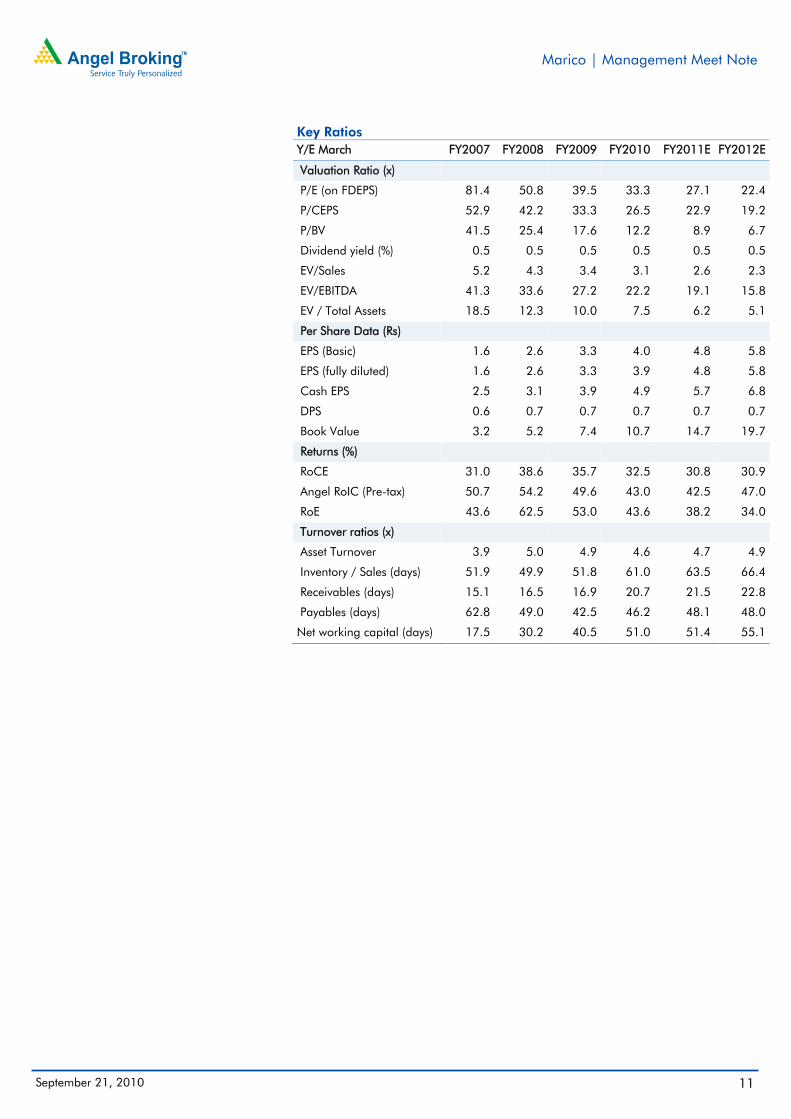

Key Ratios Y/E March FY2007 FY2008 FY2009 FY2010 FY2011E FY2012E

Valuation Ratio (x)

P/E (on FDEPS) 81.4 50.8 39.5 33.3 27.1 22.4

P/CEPS 52.9 42.2 33.3 26.5 22.9 19.2

P/BV 41.5 25.4 17.6 12.2 8.9 6.7

Dividend yield (%) 0.5 0.5 0.5 0.5 0.5 0.5

EV/Sales 5.2 4.3 3.4 3.1 2.6 2.3

EV/EBITDA 41.3 33.6 27.2 22.2 19.1 15.8

EV / Total Assets 18.5 12.3 10.0 7.5 6.2 5.1

Per Share Data (Rs)

EPS (Basic) 1.6 2.6 3.3 4.0 4.8 5.8

EPS (fully diluted) 1.6 2.6 3.3 3.9 4.8 5.8

Cash EPS 2.5 3.1 3.9 4.9 5.7 6.8

DPS 0.6 0.7 0.7 0.7 0.7 0.7

Book Value 3.2 5.2 7.4 10.7 14.7 19.7

Returns (%)

RoCE 31.0 38.6 35.7 32.5 30.8 30.9

Angel RoIC (Pre-tax) 50.7 54.2 49.6 43.0 42.5 47.0

RoE 43.6 62.5 53.0 43.6 38.2 34.0

Turnover ratios (x)

Asset Turnover 3.9 5.0 4.9 4.6 4.7 4.9

Inventory / Sales (days) 51.9 49.9 51.8 61.0 63.5 66.4

Receivables (days) 15.1 16.5 16.9 20.7 21.5 22.8

Payables (days) 62.8 49.0 42.5 46.2 48.1 48.0

Net working capital (days) 17.5 30.2 40.5 51.0 51.4 55.1

Marico | Management Meet Note

September 21, 2010 12

Research Team Tel: 022 - 4040 3800 E-mail: [email protected] Website: www.angeltrade.com DISCLAIMER This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other reasons that prevent us from doing so. This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement Marico 1. Analyst ownership of the stock No 2. Angel and its Group companies ownership of the stock No 3. Angel and its Group companies' Directors ownership of the stock No 4. Broking relationship with company covered No Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors. Ratings (Returns): Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%) Reduce (-5% to 15%) Sell (< -15%)

Marico | Management Meet Note

September 21, 2010 13

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel: (022) 3952 4568 / 4040 3800

Research Team

Fundamental:

Sarabjit Kour Nangra VP-Research, Pharmaceutical [email protected]

Vaibhav Agrawal VP-Research, Banking [email protected]

Vaishali Jajoo Automobile [email protected]

Shailesh Kanani Infrastructure, Real Estate [email protected]

Anand Shah FMCG, Media [email protected]

Deepak Pareek Oil & Gas [email protected]

Sushant Dalmia Pharmaceutical [email protected]

Rupesh Sankhe Cement, Power [email protected]

Param Desai Real Estate, Logistics, Shipping [email protected]

Sageraj Bariya Fertiliser, Mid-cap [email protected]

Viraj Nadkarni Retail, Hotels, Mid-cap [email protected]

Paresh Jain Metals & Mining [email protected]

Amit Rane Banking [email protected] Srishti Anand IT, Telecom [email protected] John Perinchery Capital Goods [email protected]

Jai Sharda Mid-cap [email protected]

Sharan Lillaney Mid-cap [email protected]

Amit Vora Research Associate (Oil & Gas) [email protected]

V Srinivasan Research Associate (Cement, Power) [email protected]

Mihir Salot Research Associate (Logistics, Shipping) [email protected]

Chitrangda Kapur Research Associate (FMCG, Media) [email protected]

Vibha Salvi Research Associate (IT, Telecom) [email protected]

Pooja Jain Research Associate (Metals & Mining) [email protected]

Yaresh Kothari Research Associate (Automobile) [email protected]

Shrinivas Bhutda Research Associate (Banking) [email protected]

Sreekanth P.V.S Research Associate (FMCG, Media) [email protected]

Hemang Thaker Research Associate (Capital Goods) [email protected] Nitin Arora Research Associate (Infra, Real Estate) [email protected]

Technicals:

Shardul Kulkarni Sr. Technical Analyst [email protected]

Mileen Vasudeo Technical Analyst [email protected]

Derivatives:

Siddarth Bhamre Head - Derivatives [email protected]

Jaya Agarwal Derivative Analyst [email protected]

Institutional Sales Team:

Mayuresh Joshi VP - Institutional Sales [email protected]

Abhimanyu Sofat AVP - Institutional Sales [email protected]

Nitesh Jalan Sr. Manager [email protected]

Pranav Modi Sr. Manager [email protected]

Sandeep Jangir Sr. Manager [email protected]

Ganesh Iyer Sr. Manager [email protected]

Jay Harsora Sr. Dealer [email protected]

Meenakshi Chavan Dealer [email protected]

Gaurang Tisani Dealer [email protected]

Production Team:

Bharathi Shetty Research Editor [email protected]

Simran Kaur Research Editor [email protected]

Bharat Patil Production [email protected]

Dilip Patel Production [email protected]

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Securities Ltd:BSE: INB010994639/INF010994639 NSE: INB230994635/INF230994635 Membership numbers: BSE 028/NSE:09946 Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM / CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302