main street industry news - june 2013

DESCRIPTION

PIA of Nebraska and Iowa, Main Street Industry News. Politics, Insurance, News and more.TRANSCRIPT

June 2013 | Published Monthly

PIA Legislative Report »7

INSIDE

National Alliance Names 2013 Top »11

Will Americans Comply & Buy Health Insurance? »16

2013 Awarri Dunes Golf Outing »18

Poking Fun! Good Natured Fun of ObamaCare —

Diagnostic Codes »26

Cover Photo: University of Nebraska in Lincoln — Some rights reserved by Len “Doc” Radin

PIA Welcomes James Dobler,

CPCU as Legislative

Coordinator!

Did youknow?

National Association of Professional Insurance Agents400 N. Washington St., Alexandria, VA 22314-2353www.pianet.com | [email protected] | (703) 836-9340

Did you know that on April 10-11, 2013, PIA members from across the country came to Washington, DC to meet with their Members of Congress as part of PIA’s annual Federal Legislative Summit (www.piafls.com)?

These agents know that laws made in Congress can have devastating effects on their businesses. They also know that PIA has the tools, information and support materials to arm a grassroots movement.

Here are some of the important issues these agents were fighting for:

Crop Insurance•

Health Care Reform•

National Flood Insurance Program•

Regulation of Insurance•

Tax and Regulatory Reform•

To learn how you can become a PIA Grassroots Action Leader, visit www.piagrassroots.com.

PIA will continue to fight for the best interests of professional insurance agents. If you are not a PIA member, please join the fight. Contact us for a membership application or visit us online at www.pianet.com/joinpia

June 2013 | Main Street Industry News | www.pianeia.com | 4

Will Americans Comply & Buy Health Insurance? | 16In October Americans without insurance and small businesses will be required to go to their state health insurance exchange and purchase health insurance for themselves, and in the case of small business, for their employees.

2013 Awarri Dunes Golf Outing | 18The afternoon of June 4th was overcast, but the promise of fun and competition filled the air. Eighteen foursomes looked forward to testing their skills at Awarri Dunes in Kearney, NE.

2013 Evening of Comedy and Trade Fair | 21On the evening of June 4th, numerous businesses serving independent agents had the pleasure of connecting with convention delegates.

2013 Past Presidents Breakfast & Education | 23The morning of June 5th begin with a breakfast celebration for PIA Past Presidents. All convention delegates were welcome to join in recognizing and congratulating all of the past presidents.

2013 Achiever’s Luncheon | 24During the noon hour on June 5th, agents were treated to a delicious lunch buffet, sponsored by PIA Trust.

Poking Fun! Good Natured Fun of ObamaCare — Diagnostic Codes | 26Kentucky Senator Rand Paul is classified as a Republican but he’s really a Libertarian.

PIA Legislative Report | 7Senators passed LB 568 that will require individuals and entities applying for and acting as navigators for the state’s health benefit exchange to be registered with the Nebraska Department of Insurance.

MarketScout & May’s Rates | 8MarketScout said the increase for the month of May’s composite insurance rate for commercial lines is 5%.

Coastal Controversy — Homeowners Rates Rise | 9Nationwide the rates are rising for homeowners insurance.

Small Business & Cyber Attacks | 10Small businesses need to worry about cyber attacks and that isn’t happening.

National Alliance Names 2013 Top CSRs | 11Every year the National Alliance for Insurance Education & Research looks for the best customer service reps in the country.

FIO Reports — Late, Late, Late | 11PIA National reports that House Financial Services Committee staffers say they plan to continue to pressure the Federal Insurance Office (FIO) to release a series of long-overdue reports.

The Basics of Business Interruption Coverage and Having the Right Limit | 12Most commercial customers should have business interruption coverage, yet judging by some industry articles on Superstorm Sandy, that issue may be debatable.

PIA National & ObamaCare | 14PIA National focused on the Patient Protection and Affordable Care Act last week.

Top STorieS

piA Ne iA eveNTS

Upcoming Events Calendar 2013 | 27

AdverTiSemeNTS

Wanted, For Sale and Opportunities | 28Contact us to place a classified ad.

CINCINNATUSP A R T N E R S®

Cincinnatus Partners I, LP$30 Million of Committed Equity Capital

Focused on acquiring property-casualty independent insurance agencies with the following profile:

• Comprised predominately of personal lines, agriculture and small commercial coverage

• Annual commission income in the range of $500K - $5 Million

• Based in Nebraska, Iowa and surrounding states

Partners | Carey Bush, Brandon Perry, William Re., John Ward

6279 Tri-Ridge Boulevard, Suite 150, Loveland, Ohio 45140(513) 381-2500 • www.cincinnatuspartners.com

Retention Strategy #12LIFE INSURANCE SALES

Omaha Branch: 800.338.9735 | Home Office: Des Moines, IA www.emcins.com© Copyright Employers Mutual Casualty Company 2013. All rights reserved.

“ A life insurance sale can make a customer for life.”

The more coverages clients have with you, the less likely they are to switch agents. EMC National Life is committed to making life sales simple with easy-to-understand products and online services to speed the sales process. It’s just one of the many reasons policyholders Count on EMC®.

Lora Buske, EMC National Life Life Sales Representative

Professional Insurance Agents NE IAAttention: EditorialMain Street Industry News920 S 107 Avenue, Ste. 305Omaha, NE 68114

Email: [email protected]: 402-392-1611www.pianeia.com

The PIA NE IA, Main Street Industry News reserves the right to edit your comments to fit space available. We respectfully ask that you keep the comments to 200-300 words.

PIA Association for Nebraska and Iowa is committed to focusing its resources in ways that cast the most favorable light on its constituents. We are dedicated to providing the type of programs, the level of advocacy, and the dissemination of information that best supports the perpetuation and prosperity of our members. We pledge to always conduct ourselves in a manner that enhances the public image of PIA and adds real value to our members.

SUBSCriBe or CommeNT

piA for NeBrASkA ANd iowA

AdverTiSiNg QUeSTioNS

Cathy Klasi, Executive Director(402) 392-1611

This publication is designed by Strubel Studios.

Join Our Facebook Fan PageProfessional Insurance Agents of NE IA

IS YOUR E&OX-DATE HERE?

Consideringa change?

Let the piA quote your e&o

Phil Fried(402) 392-1611

E&O CoordinatorPhil Fried

June 2013 | Main Street Industry News |www.pianeia.com| 7

Top STorieS

PIA LegIsLAtIveRePoRt

Senators passed LB 568 that will require individuals and entities applying for and acting as navigators for the state’s health benefit exchange to be registered with the Nebraska Department of Insurance. The exchange will be established in Nebraska under the Federal Affordable Care Act which requires that all exchanges include programs and navigators to assist individuals in navigating the new system.

Navigators must be at least 18 years old and must certify to the Director that they have passed an examination to act as a navigator. The maximum registration fee will be $25 for an individual and $50 for an entity. Registration will be valid for one year and may be renewed for a fee.

Navigators will be prohibited from: engaging in any activities that would require an insurance • producer license;violating Nebraska insurance licensure law;• recommending or endorsing a particular health plan;• advising consumers about which health plan to choose;• accepting compensation dependent on whether a person enrolls • in or purchases a qualified health plan; orfailing to respond to an inquiry from the director.•

If the Navigator is in contact with an individual who says they have an insurance agent for their health insurance, the Navigator must make a reasonable effort to advise the individual that he/she may seek further assistance from their agent.

The bill is also important from the standpoint that it establishes Nebraska Department of Insurance regulatory authority over navigators. There will be some local control over the activities of navigators. This bill is effective June 5, 2013.

Other bills passed this session which might be of interest to PIA members include LB 105 which requires day care providers licensed under the state Child Care Licensing Act to maintain liability insurance in a minimum amount of $100,000 per occurrence. This bill is effective July 1, 2014. Also passed was LB 133 which changes how multiple auto policies apply in the case of an individual using a loaner vehicle provided by an auto dealer. This bill provides that the policy of the driver is primary and the dealer’s policy is excess if the loaner vehicle is provided at no charge. The bill is limited to car dealers. It is effective September 6, 2013. n

PIA Welcomes James Dobler, CPCU as Legislative Coordinator!

On June 1, Jim Dobler, CPCU, opened a new chapter as legislative coordinator/lobbyist for PIA. Many of you know Jim from the Farmers Mutual meetings and panel discussions. Jim recently retired from Farmers Mutual as Executive Vice President, Secretary, and General Counsel. He was also president of Nebraska Insurance Information Service from 1991-2012 and will continue to assist them with their endeavors. Jim looks forward to maintaining his many relationships with independent agents and keeping an eye on the legislation that affects them.

Top STorieS

MarketScout & May’s RatesMarketScout said the increase for the month of May’s composite insurance rate for commercial lines is 5%. Just like April, March and February. That is three straight months with increases of 5%.

MarketScout CEO Richard Kerr said this month’s results continue the steady trend of rate increases in commercial lines. “There is ample capacity but underwriters continue to increase rates as appropriate.”

Personal lines did well, too. The composite rate from April to May is 4%. April’s rate was 3%. “Regardless of the value of your home, most insureds had premium increases for renewals in May. Perhaps the numerous tornadoes or the pending hurricane season had an impact on pricing. We feel the increases are driven more by underwriter’s sentiment than actuarial projections,” Kerr said. n

Commercial Property Up 6%

Business Interruption Up 3%

BOP Up 4%

Inland Marine Up 3%

General Liability Up 6%

Umbrella/Excess Up 5%

Commercial Auto Up 5%

Workers’ Compensation Up 6%

Professional Liability Up 3%

HERE ARE THE SUMMARIES PER LINE:

Small Up 5%

Medium Up 5%

Large Up 4%

Jumbo Up 3%

FOR ACCOUNT SIzE:

Homes — All Values Up 4%

Automobile Rates Up 4%

Personal Articles Premiums Up 3%

D&O Up 4%

IFU Up 4%

June 2013 | Main Street Industry News |www.pianeia.com| 9

Top STorieS

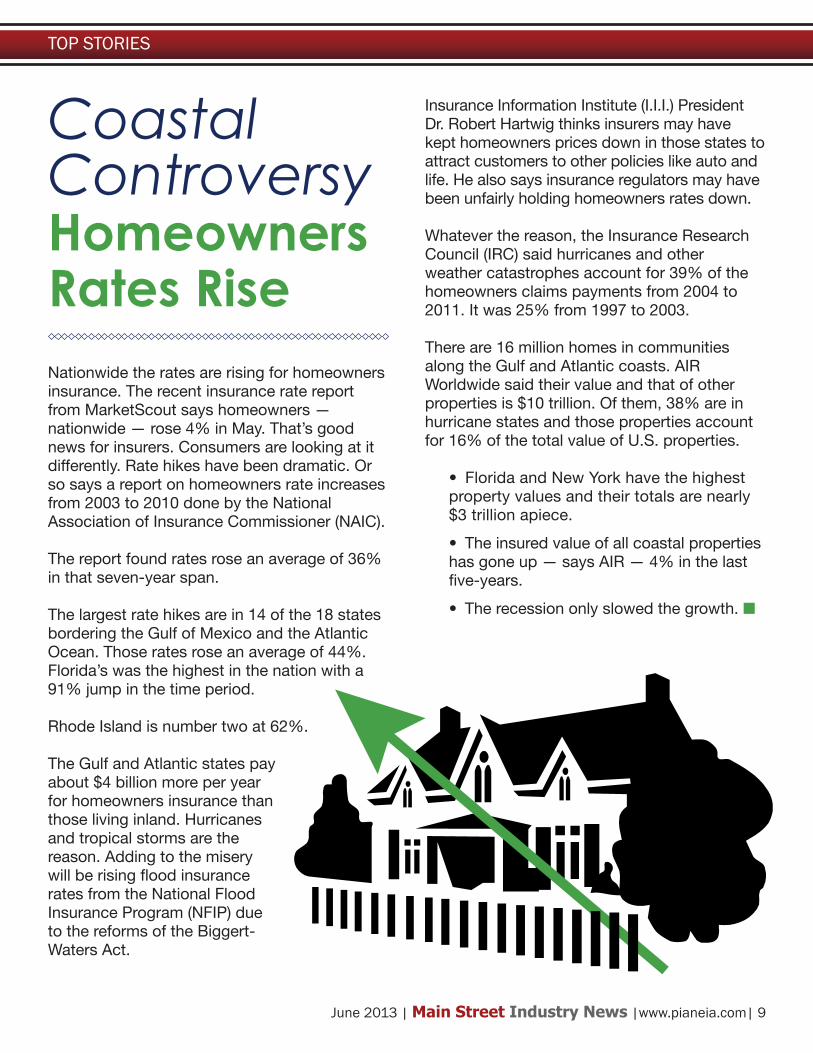

Coastal ControversyHomeowners Rates Rise Nationwide the rates are rising for homeowners insurance. The recent insurance rate report from MarketScout says homeowners — nationwide — rose 4% in May. That’s good news for insurers. Consumers are looking at it differently. Rate hikes have been dramatic. Or so says a report on homeowners rate increases from 2003 to 2010 done by the National Association of Insurance Commissioner (NAIC).

The report found rates rose an average of 36% in that seven-year span.

The largest rate hikes are in 14 of the 18 states bordering the Gulf of Mexico and the Atlantic Ocean. Those rates rose an average of 44%. Florida’s was the highest in the nation with a 91% jump in the time period.

Rhode Island is number two at 62%.

The Gulf and Atlantic states pay about $4 billion more per year for homeowners insurance than those living inland. Hurricanes and tropical storms are the reason. Adding to the misery will be rising flood insurance rates from the National Flood Insurance Program (NFIP) due to the reforms of the Biggert-Waters Act.

Insurance Information Institute (I.I.I.) President Dr. Robert Hartwig thinks insurers may have kept homeowners prices down in those states to attract customers to other policies like auto and life. He also says insurance regulators may have been unfairly holding homeowners rates down.

Whatever the reason, the Insurance Research Council (IRC) said hurricanes and other weather catastrophes account for 39% of the homeowners claims payments from 2004 to 2011. It was 25% from 1997 to 2003.

There are 16 million homes in communities along the Gulf and Atlantic coasts. AIR Worldwide said their value and that of other properties is $10 trillion. Of them, 38% are in hurricane states and those properties account for 16% of the total value of U.S. properties.

Florida and New York have the highest • property values and their totals are nearly $3 trillion apiece.

The insured value of all coastal properties • has gone up — says AIR — 4% in the last five-years.

The recession only slowed the growth.• n

June 2013 | Main Street Industry News | www.pianeia.com | 10

Small businesses need to worry about cyber attacks and that isn’t happening.

The Small Business Authority® looked at cyber security in its monthly SB Authority Market Sentiment Survey. The 100,000 member organization asked 2,100 of its members if they worry about cyber attacks. A majority — 56% — say they do not. Here are the survey results:

Do you have a fear of cyber-attacks?Yes: 44% No: 56%

Has your website been scanned for security vulnerabilities in the last 12 months?Yes: 40% No: 35%

The Small Business Authority CEO Barry Sloane said, “Despite the fact that cyber-attacks and the threat of this activity have

grown in recent years within the U.S. economy, a majority of our small

business owners are still not afraid. The concept of fear can be viewed in two ways: the actual fear of being attacked, or

the mere recognition that attacks are possible. There is an air of

complacency with business owners who think cyber-attacks will not happen or affect them.”

The Ponemon Institute said close to a third of the nation’s small business — according to its research — were exposed to a cyber attack last year. That number is expected to continue to grow. Ponemon did the study for The Harvard Steam Boiler Inspection and Insurance Company. Hartford Steam Vice President Timothy Zeilman said the study found that 75% of the businesses that were attacked were never able to completely restore their computer data.

“The Internet connects even the smallest businesses to data networks and computer systems around the world. This access also exposes companies to hackers, viruses and other computer attacks that can corrupt critical data, shut down their operations and make them liable for compromised information.”

Here’s what the survey found:29% of small businesses were cyber •

attacked last year. 59% suffered damage to their reputations. • 49% had business information stolen.• 48% reported angry or worried — or both — •

customers.48% experienced network and data center •

downtime.

The attacks were done with:Viruses, worms and Trojans — 61%.•

Malware — 22%. • n

SmallBusiness& Cyber Attacks

Top STorieS

June 2013 | Main Street Industry News |www.pianeia.com| 11

FIO ReportsLate, Late, Late

Every year the National Alliance for Insurance Education & Research looks for the best customer service reps in the country. Last week the National Alliance named each state’s winners for National Outstanding Customer Service Representative (CSR) of the Year.

The winners were picked based on an essay they did on this question: “Communication is one of the most important parts of building strong relationships with your clients, companies, and coworkers. Identify and explain the four greatest barriers to effective communication that you face (or have faced) and how you’ve worked to overcome these barriers.”

Each winner now competes for the National Customer Service Representative of the Year. It carries a prize of $2,000 cash and more.

Here are the top CSRs for 2013 from PIA NE IA: Iowa: Nicole L. Keck, CISRAW Welt Ambrisco Insurance, Inc.

Nebraska: Dianne L. MillerCIC, Western Insurers

Names 2013 Top CSRs

Top STorieS

PIA National reports that House Financial Services Committee staffers say they plan to continue to pressure the Federal Insurance Office (FIO) to release a series of long-overdue reports.

The most critical is on insurance regulation.

PIA has issued warnings that it may be used by the FIO as a vehicle for a power grab and propose that it take over some or all insurance regulatory functions from the states. PIA opposed this study from the outset due to the fact that the questions being asked and the basis of the report is biased in favor of federal regulation. It may not matter though. Committee chairman Rep. Jeb Hensarling — a Texas Republican — has strongly indicated to PIA he opposes federal insurance regulation. To provide a measure of balance that we expect will be lacking in the FIO report, last year PIA worked with then Insurance Subcommittee Chairwoman, Illinois Republican Rep. Judy Biggert and Rep. Steve Stivers — a Republican from Ohio — on requesting a study from the Government Accountability Office (GAO) that looks into the benefits of the state insurance regulatory structure. That study was accepted and is due out from the GAO this summer. Final review of the study will take place this week, with a release possible at the end of this month.

That said, the release date can be postponed up to 30 days. Shortly after becoming CEO of the National Association of Insurance Commissioners (NAIC) former Sen. Ben Nelson warned the FIO that it needs to stick to its assigned role. “We are determined to see that FIO does the job it was intended to do, but not our job,” Nelson declared during the spring meeting of the National Conference of Insurance Legislators (NCOIL).

During that speech, Nelson restated that the FIO is not a regulator. He then added, “I think they’re beginning to understand that.” n

June 2013 | Main Street Industry News | www.pianeia.com | 12

Most commercial customers should have business interruption coverage, yet judging by some industry articles on Superstorm Sandy, that issue may be debatable. One article cited a survey from a national carrier stating that only 30 percent of the small businesses in New Jersey had business interruption coverage, and only 10 percent had coverage for off-premises utility interruption.

Let’s Look at Three Key Questions:How many of your agency’s commercial •

lines customers have business interruption coverage?

For those that do, when was the last time the • limit was updated?

Do those customers know how the coverage • would respond in the event of a loss?

ComplexitiesEach year, the business-interruption line-of-business seems to generate a significant number of errors-and-omissions claims. This could be partly due to Mother Nature and the numerous weather-related catastrophes the United States has been experiencing. A common saying among errors-and-omissions carriers notes that “nothing brings out an agent’s mistake as quick as a catastrophe.”

Potential issues include a customer not having the coverage at all, not having the right type

by Curtis M. Pearsall, CPCU, AIAF, CPIA, President – Pearsall Associates, Inc., and Special Consultant to the Utica National E&O Program

The Basics of Business Interruption Coverage and Having the Right Limit

of coverage, not understanding the coverage he or she has, or not having the right amount. How well do professional agents understand the need and the value for a customer to have business interruption coverage? This coverage has complexities to it, so it is important that agents and agency staff understand the types and how they work.

Doesn’t Have the CoverageBusiness interruption coverage is designed to cover the loss of business income/profits if normal business operations are disrupted by a covered physical damage loss to property. An effective approach to handle this with a customer is by using an exposure analysis checklist. Most industry checklists will enable you, by SIC code, to get a firm handle on all the business interruption forms that might be applicable to a particular customer. Each of these forms is fully defined with extensive explanations regarding issues for you to consider.

After you recommend business interruption coverage, your customer might reject it. If so, document these discussions and decisions. It is best to either require the customer’s signature on the proposal noting the rejection or documenting back to the customer a recap of the discussion and decision in an e-mail or letter. This documentation is invaluable should an E&O claim arise in this area.

Doesn’t Have the Right Type of CoverageAs you will note from the exposure analysis checklists, there are many forms available, so it is important to ask the customer questions to better understand the exposure and which form and limit will achieve the desired result. Questions might include:

Can the business operate at a temporary • location rather than suspend operations?

Top STorieS

June 2013 | Main Street Industry News |www.pianeia.com| 13

Could your client’s business be interrupted • because of a loss at one of its suppliers?

What would happen if a key piece of • machinery was damaged – how long would it take to get a replacement? What if the manufacturer is overseas?

Would the customer suffer a loss if one of its • service providers – electrical, fuel, water, heat, refrigeration, communication, etc. – suffered a loss?

Is there a need for Extra Expense Insurance?•

Are there any new state Ordinance or Law • requirements or code upgrades that could delay the customer from getting back in business?

Doesn’t Understand the Current CoverageAgents should realize that after a loss, it is possible the customer will state that he or she was not truly aware of the business interruption coverage, what it covers and how a loss would be adjusted. To address this, an agency’s insurance proposals should include the industry definition of that specific type of business interruption and any unique terms/phrases, such as “waiting period” or “co-insurance.” When reviewing the proposal with the prospect/customer, dedicate the necessary time and attention to this line of business. If possible, include some real-life claim examples to help your clients/prospects understand the importance of this key coverage.

Here is an actual claim where the issue of co-insurance played a significant role:

The insured procured a boiler machinery policy with $884,000 of coverage for business interruption written with a 100% co-insurance provision. The client was a long-time customer of the agency. The limit in place had been the same for 10 years as the agent never asked for updated earnings information during that time. A loss occurred, which the carrier determined to total $250,000. However, the carrier also determined the annual income for the risk to be $2.2 million. Due to the 100% co-insurance provision, a 60% co-insurance penalty was

Top STorieS

assessed, resulting in a $150,000 shortfall. The case was settled with the E&O carrier paying $180,000 primarily due to 1) the agent telling the client the $884,000 limit was sufficient and 2) the agent not explaining or informing the client of the 100% co-insurance on the policy.

Imagine how including the definition of co-insurance could have altered the settlement of this claim. Agents should also look to provide, if applicable, explanations such as:

Waiting periods – These can be fairly common • with different duration periods. Losses incurred during the period directly following an event will not be covered. If possible, try securing coverage without a waiting period.

Specific clauses that could impact • the settlement of a claim – including any exclusions/limitations/war clauses, etc.

Is the Limit Adequate Today?Updating the limits is much easier with property coverage, especially building coverage. This assumes the current coverage was calculated correctly. However, with business interruption, determining the proper limit can be much more challenging. In many cases, the coverage and limit from last year may no longer be adequate. Many carriers have worksheets to help determine the proper limit. Using this worksheet, it is highly recommended that you work with the customer’s accountant to ensure calculation of the right coverage amount. As evidenced by the claim above, business interruption is definitely not a coverage you want to renew “as is.”

Having business interruption coverage is extremely important. Your customer must also understand where property coverage ends and business interruption coverage begins. Take the necessary time to ensure your customer know the importance of business interruption, how it works and what coverage form best fits them. This education will go a long way toward selling more insurance and minimizing the possibility of an errors-and-omissions claim being made against your agency. n

June 2013 | Main Street Industry News | www.pianeia.com | 14

Top STorieS

PIA National focused on the Patient Protection and Affordable Care Act last week.

At the end of the week, the association thanked California Republican Rep. Duncan Hunter for taking the lead in raising significant concerns regarding healthcare navigators with the Department of Health and Human Services (HHS).

In a June 7 letter to HHS Secretary Kathleen Sebelius, Rep. Hunter and 32 other members of Congress focused on the need for consumer protections for the navigators working within the health insurance exchanges of each state. The concern is that navigators are not required to be licensed or carry liability insurance to protect consumers against errors or omissions — like professional insurance agents — and the need for appropriate oversight. The letter notes that missing from HHS’s proposed rule governing navigators and non-navigator assisters is ensuring clients will receive information on the best possible plan that best suits their individual needs whether that plan is available in the marketplaces or through the traditional market. The letter mentions that navigators will not be allowed to assist with determining the appropriate plan.

PIA noted while it is appropriate that unlicensed navigators or assisters not be permitted to make plan recommendations, this puts the consumer in the position of lacking needed

PIA National& ObamaCare

ObamaCareinformation. “According to the National Association of Professional Insurance Agents, this scenario can be expected to be common and it is our position that the complexities of these plans is best handled by those who are trained and state-certified to sell such products — licensed insurance agents or brokers,” the letter to Secretary Sebelius notes. It goes on to say that navigators need no insurance of their own to protect consumers.

“...Insurance agents and brokers carry Errors and Omission (E&O) insurance to protect not just themselves, but consumers from any accidental wrongdoing. In the event that an error occurs, consumers have recourse to recoup any losses that they may have endured. It is our understanding that your Department will not recommend E&O coverage for Navigators, resulting in possible large gaps in consumer protections.” After that statement, the letter from Duncan and other members of Congress poses a series of questions to Sebelius. They also note that the ACA preserves state regulatory authority of insurance and that many state legislatures have passed legislation that will strengthen consumer protections, such as further defining the role of a navigator. PIA National’s Vice President of Federal Affairs Mike Becker said, “The letter prompts HHS to provide the Department’s perspective on key areas of consumer protection, including inquiries into background checks, training, and oversight. We greatly appreciate Congress’ recognition of the critical exposure to stringent consumer protections and the valued role agents and brokers provide. We look forward to continuing our work on this matter.”

June 2013 | Main Street Industry News |www.pianeia.com| 15

Top STorieS

Meanwhile, PIA National Senior Vice President Ted Besesparis wrote an article for American Agent & Broker. Besesparis’ angle is that even with the reelection of Barack Obama and the U.S. Supreme Court’s decision on the individual mandate, the fight to end ObamaCare is not over.

“Most of ACA’s provisions don’t kick in until 2014. The public’s experiences with the law will be grist for off-year Congressional election campaigns. It would be comforting to believe that because the major challenges to the new healthcare law have been adjudicated, everyone would just get about the task of making the best of the situation. That may be hoping for too much,” he wrote.

Besesparis said healthcare stirs intense passions on both ends of the political spectrum. He likens the controversy over ObamaCare to the battle over gun control and abortion. But the real difference between them is that not everyone owns guns, and not everyone will have an abortion. Healthcare — on the other hand — affects everyone.

“Most people are in the middle on most issues, but advocacy on issues of passion comes from activists on both the left and the right. And the money to fuel the activists, whose motives are usually ideologically pure, often comes from those with a vested monetary interest in the outcome and thus are anything but pure in their motivation.”

He also notes it is likely to become a mid-term election issue.

“If you want a preview of what could become one of the major issues of Campaign 2014, spend some time reading the latest news regarding ACA. Implementation of ACA could either go reasonably well, or be an unmitigated disaster. One thing is certain: Those who still dream of repealing ACA — despite being repudiated by the voters and the Supreme Court — will no doubt try to foster the impression that it has been the disaster they predicted.”

Then he explains what can go wrong with the implementation of the Patient Protection and Affordable Care Act. There are four issues but we are outlining two pointed out by Besesparis.

The first is rate shock. State insurance commissioners worry about this because the ACA has been sold — at least in part — as a way to make healthcare more affordable. He notes the problem with rate shock was outlined in a paper delivered at the latest meeting of the National Association of Insurance Commissioners.

“The paper indicates that state officials have serious concerns about possible rate increases, despite assurances from federal officials. It then laid out some options to mitigate rate increases, including regulating premiums more tightly; forcing insurers to cut costs or operate at a loss; financial assistance to consumers, above the subsidies that will already be provided; and programs to ensure that the costs of the sickest patients are shared by all insurers,” Besesparis wrote.

And Besesparis concludes, “If forcing insurers to operate at a loss is being raised as a serious option, it indicates that something is very wrong here.”

Another concern takes us full circle back to the beginning of this article. It is the navigators and where to get them. “In March, a controversy erupted regarding plans to check the backgrounds of some 20,000 unlicensed ‘assisters’ set to be recruited in California to help consumers enroll in health insurance plans. Inexplicably, there were howls of protest about the background checks from some California consumer activists. California Insurance Commissioner Dave Jones said he was ‘just shocked that groups that represent the consumer interest summarily dismiss what I think is a very real probability of immense consumer fraud.”

Jones is correct — Besesparis writes — it takes just one consumer being a fraud victim because of a navigator and public confidence will be

June 2013 | Main Street Industry News | www.pianeia.com | 16

Top STorieS

undermined. “PIA testified before the NAIC in April, saying people who work as navigators in health insurance exchanges should be subject to background checks and licensing, to protect consumers. The list of individuals that can become navigators is lengthy, which leads to an increased concern that many navigators will have little to no experience with insurance. As both the states and federal government establish navigator parameters, there is a better option for consumers: agents and brokers,” he wrote.

There are benefits — as we all know — to using agents and brokers as navigators.

“Agents and brokers are licensed, regulated, experienced professionals that educate consumers on complex insurance products and enroll them in policies that best fit their personal needs. Agents and brokers have a deep familiarity with insurance markets and products; they service plans throughout the year, assist with renewals, and are held to strict compliance standards,” Besesparis said.

And agents and brokers are required to do continuing education to maintain their licenses. From the HHS point of view, they are not.

“Rather than recruiting inexperienced, unlicensed people, it would make sense to rely more on professional independent insurance agents and brokers to help people navigate the ACA,” he concluded.

The HHS does — however — recognize the value of agents and brokers.

“In a proposed rule issued on April 3, HHS confirms that agents and brokers can act as navigators in a federally facilitated exchange, but not receive consideration directly or indirectly from an issuer. However, it notes that ‘agents and brokers who sell other lines of insurance would not be prohibited from receiving consideration from the sale of those other lines of insurance while serving as Navigators, provided they complied with the [new] disclosure requirement.” n

In October Americans without insurance and small businesses will be required to go to their state health insurance exchange and purchase health insurance for themselves, and in the case of small business, for their employees.

A new survey from InsuranceQuotes.com done by Princeton Survey Research Associates International says about two-thirds of us still aren’t sure whether we’ll comply with the new law.

64% haven’t decided yet whether to • purchase the insurance.

Just 19% say they’ll buy it by the January 1, • 2014 deadline.

10% are for sure that they won’t buy and will • pay the penalty instead.

Will Americans Comply & Buy Health Insurance?

The penalty is $95 or 1% of a person’s income whichever is greater. For children under 18, the penalty is half that of an adult. By 2016 the penalty will be the greater of $695 or 2.5% of an adult’s income. For a family it is $2,085 or 2.5% of family income.

Amy Back of the consumer advocacy group United Policyholders said people are in wait-and-see mode. “People are still in the dark about what their options are going to be — and they’re skeptical that the penalty for not buying insurance is going to be enforced, at least in the first couple of years.”

The survey still shows a large number of people unsure about how the law works. It also shows that many won’t purchase the insurance — subsidized or not — because they can’t afford the cost. n

FirstComp Fastball ®

A New Kind of Ballgame!

FirstComp Underwriters Group, Inc. is a servicing entity for Markel Insurance Company.FirstComp is a registered trademark of Markel Aspen, Inc. used under license by its affiliates including but not limited to those doing business as FirstComp Insurance Company, FirstComp Underwriters Group, Inc., FirstComp Group Inc., FirstComp Group, FirstComp Insurance Agency, and Risk Exchange Insurance Services, Inc., a subsidiary of REX, Inc. also doing business as Risk Exchange Insurance Agency Services, Inc. FC1140(0213)_PIA_NE_IA

Forget about March Madness ... FirstComp has Baseball Fever!

Step up to the plate!For every new account you request to bind starting 2/1/13 through 4/30/13, you will earn one shot at winning big-league prizes each week. The more accounts you request to bind, the more entries you earn into the weekly drawings. Weekly winners will be announced each Monday for 13 weeks.

We have 67 Prizes on Deck! • 10 Grand Slams: College World Series Trip to Omaha, NE for two, June 14-16 • 5 Home Runs: Round trip airfare for 2 anywhere in the continental U.S. ($800 value) • 15 Triple Plays: iPad 2 • 37 Steals: $100 Visa Gift Card

Remember, the more accounts you request to bind each week, the more new entries you get to win!

For more informationcontact your Sales Manager.

‘Like Us’ on Facebook to stay up-to-date on FirstComp

news and special promotions!

June 2013 | Main Street Industry News | www.pianeia.com | 18

piA Ne iA eveNTS

The afternoon of June 4th was overcast, but the promise of fun and competition filled the

air. Eighteen foursomes looked forward to testing their skills at Awarri Dunes in Kearney,

NE. They were met with challenging shots and unique course layouts as they played towards

winning best score, best shot and even best photo. Many golfers had the opportunity to team up with their loved ones and reconnect with old friends. Those new to this golf outing enjoyed networking and creating new business partnerships. This event was the perfect beginning to a memorable convention. n

1ST PLACE 1ST FLIGHTJR Johnson, Brent Walker, Doug Mitchell, Ed Wiltgen

1ST PLACE 2ND FLIGHTAdam Crowe, Colleen Olson,

Cody Fruin, John Kucera

1ST PLACE 3RD FLIGHTJustin Shavlik, Janet Barna,

Jim Barna, Terry Delp

Golf Outing2013 Awarri Dunes

June 2013 | Main Street Industry News |www.pianeia.com| 19

piA Ne iA eveNTS

2013 Awarri Dunes Golf Outing

June 2013 | Main Street Industry News | www.pianeia.com | 20

piA Ne iA eveNTS

2013 Awarri Dunes Golf Outing

June 2013 | Main Street Industry News |www.pianeia.com| 21

piA Ne iA eveNTS

On the evening of June 4th, numerous businesses serving independent agents had the pleasure of connecting with convention delegates. There were nine exhibitors in attendance and each of their booths offered a unique presentation of the services they have to offer. Hors d’oeuvres and a cash bar were available to all attendees as they explored the trade fair. PIA Marketing Director, Gary Baumann, awarded the golf prizes to the top players from the afternoon’s outing. True to the convention title, “Laugh and Learn” with PIA, this evening was filled with laughter, particularly when comedian Gayle Becwar took the stage. His humorous anecdotes and magic tricks regaled the crowd and created an enjoyable experience for all. n

Comedy and Trade Fair2013 Evening of

BOOTH: Armtech

BOOTH: Premier

BOOTH: Liberty Mutual

BOOTH: Safelite

BOOTH: Paul Davis

BOOTH: CRDN BOOTH: Yellow Van

June 2013 | Main Street Industry News | www.pianeia.com | 22

piA Ne iA eveNTS

2013 Evening of Comedy and Trade Fair

June 2013 | Main Street Industry News |www.pianeia.com| 23

piA Ne iA eveNTS

Breakfast & Education2013 Past Presidents The morning of June 5th begin with a breakfast celebration for PIA Past Presidents. All convention delegates were welcome to join in recognizing and congratulating all of the past presidents. Rick Sirek led the ceremony and presented 2012 President, Justin Shavlik of The Pinnacle Agency with a red past-presidents polo shirt. Following this special event, delegates had the opportunity to listen to two different education seminars and earn continuing education credit. The first session, “The Latest in E&O” was taught by Curt Pearsall and sponsored by Utica. This course gave participants the opportunity to earn credit toward their E&O premium. The afternoon session, entitled “Public Entities” was presented by Monte Giddings and sponsored by Farmers Mutual Insurance Co. of NE. Both courses were highly informative and participants left with a new understanding of these important topics. n

June 2013 | Main Street Industry News | www.pianeia.com | 24

piA Ne iA eveNTS

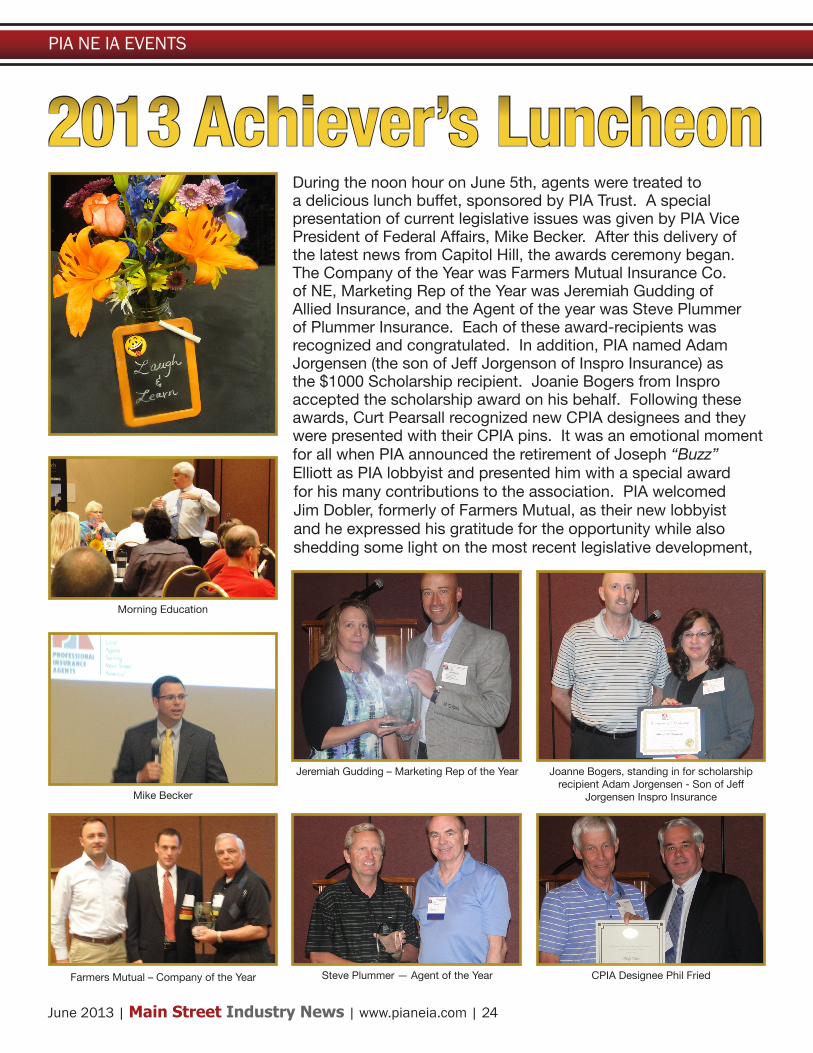

During the noon hour on June 5th, agents were treated to a delicious lunch buffet, sponsored by PIA Trust. A special presentation of current legislative issues was given by PIA Vice President of Federal Affairs, Mike Becker. After this delivery of the latest news from Capitol Hill, the awards ceremony began. The Company of the Year was Farmers Mutual Insurance Co. of NE, Marketing Rep of the Year was Jeremiah Gudding of Allied Insurance, and the Agent of the year was Steve Plummer of Plummer Insurance. Each of these award-recipients was recognized and congratulated. In addition, PIA named Adam Jorgensen (the son of Jeff Jorgenson of Inspro Insurance) as the $1000 Scholarship recipient. Joanie Bogers from Inspro accepted the scholarship award on his behalf. Following these awards, Curt Pearsall recognized new CPIA designees and they were presented with their CPIA pins. It was an emotional moment for all when PIA announced the retirement of Joseph “Buzz” Elliott as PIA lobbyist and presented him with a special award for his many contributions to the association. PIA welcomed Jim Dobler, formerly of Farmers Mutual, as their new lobbyist and he expressed his gratitude for the opportunity while also shedding some light on the most recent legislative development,

2013 Achiever’s Luncheon

Morning Education

Mike Becker

Jeremiah Gudding – Marketing Rep of the Year

Steve Plummer — Agent of the Year

Joanne Bogers, standing in for scholarship recipient Adam Jorgensen - Son of Jeff

Jorgensen Inspro Insurance

CPIA Designee Phil FriedFarmers Mutual – Company of the Year

June 2013 | Main Street Industry News |www.pianeia.com| 25

piA Ne iA eveNTS

CPIA Designee Peggy Holeman

Board Members taking oath of office

CPIA Designee Robert Clements

CPIA Designee Kathy Drake

CPIA Designee Robert Hansen, Jr. Education

Afternoon Education

Afternoon Education

PIA Lobbyist Jim Dobler

Justin Shavlik recieving past president plauque from President Amy Rademacher

CPIA Designee Amy Rademacher

the Navigator bill. At the conclusion of the ceremony, PIA board members were inducted by National Director, Rob Hansen, Jr. followed by Amy Rademacher of Loop Agency giving her inaugural address as the new PIA NE IA President. n

2013 Achiever’s Luncheon

JUST for fUN

PIA of NE IA 3.5x4.75 Prom.pdf 6/18/13 2:06:02 PM

Kentucky Senator Rand Paul is classified as a Republican but he’s really a Libertarian. Paul is also a doctor so his good-humored concern over the new diagnostic codes for the Patient Protection and Affordable Care Act (ObamaCare) come from experience.

Paul says some are very, very strange.

He’s also concerned about the addition of more codes to the system. Currently, Paul said, there are 18,000 diagnostic codes used in the U.S. That’s a lot but it pales in comparison to the 144,000 codes the medical professional will start using when ObamaCare goes into full swing in January of 2014.

For example, Paul said 312 of the new codes are for injuries from animals and 72 of those are for birds. “Nine new codes are for injuries from the macaw. The macaw?” he said.

Two of the codes are for turtle injuries. “Now, you might say, ‘Well, turtles can be dangerous.’” But why do you need two new codes? Your doctor needs to inform the government whether you’ve been struck by a turtle or bitten by a turtle,” Paul noted.

Other codes include walking into a lamppost and walking into a lamppost subsequent encounter. The second is if you didn’t learn not to walk into one from the first.

Rand Paul’s favorite? And one he notes, defies explanation: injuries sustained from burning water skis. n

Poking Fun!Good Natured Fun of ObamaCare — Diagnostic Codes

June 2013 | Main Street Industry News |www.pianeia.com| 27

For information and to register Click Hereor call (402) 392-1611.

UpcomingEvents Calendar 2013

Date Event City StateJune 26-28, 2013 CIC Commercial Property Institute Des Moines IA

June 26, 2013 CISR William T. Hold Seminar W Des Moines IA

July 10, 2013 CISR Personal Lines/Miscellaneous Marion IA

July 17, 2013 CISR Insuring Personal Residential Property Johnston IA

July 17-19, 2013 CIC Personal Lines Institute Omaha NE

July 24, 2013 CISR Commercial Casualty I Davenport IA

August 7, 2013 CISR Insuring Personal Auto Exposures Marion IA

August 21-23, 2013 CIC Personal Lines Institute Cedar Rapids IA

August 28, 2013 CISR Insuring Commercial Property W Des Moines IA

September 10, 2013 Scholarship Golf Outing Ashland NE

September 12, 2013 CISR Commercial Casualty II W Des Moines IA

September 18-20, 2013 CIC Commercial Casualty Institute Lincoln NE

September 19, 2013 CISR Dynamics of Service Seminar Johnston IA

September 26, 2013 CISR Agency Operations Davenport IA

October 3, 2013 CISR Insuring Personal Residential Property Marion IA

October 16, 2013 CISR Insuring Personal Auto Exposures Davenport IA

October 16-18, 2013 CIC Commercial Casualty Institute Des Moines IA

November 13-15, 2013 CIC Life & Health Institute Omaha NE

November 21, 2013 CISR William T. Hold Seminar Marion IA

December 5, 2013 Greater Omaha Committee Christmas Party Omaha NE

piA Ne iA eveNTS

ADvERTISEMENTSPost a classified ad!Your ad will stand out! Main Street Industry News is issued electronically to over 8,000 Professional Insurance Agents throughout NE & IA, PIA state and national associations and other organizations that provide products or services to insurance agencies.

To advertise contact PIA of Nebraska and Iowa – Executive Director, Cathy Klasi at (402) 392-1611.

Retention Strategy #19LOCAL SERVICE

Omaha Branch: 800.338.9735 | Home Office: Des Moines, IA www.emcins.com© Copyright Employers Mutual Casualty Company 2013. All rights reserved.

“ We’re here for you. I mean, really here!”

Your customers like working with a local agent to handle their insurance. We think you deserve the same kind of attention. That’s why EMC has a fully staffed branch office in your area—to respond quicker and with a greater understanding of your area’s needs. It’s just one of the many reasons you and your policyholders Count on EMC®.

Riley Tonkin, Omaha Branch Marketing Representative