macroeconomics in the world economy: theory and applications topic … · 2014-12-09 ·...

TRANSCRIPT

Macroeconomics in the World Economy:Theory and ApplicationsTopic 2: The Supply Side

Dennis Plott

University of Illinois at ChicagoDepartment of Economics

http://blackboard.uic.edu

Spring 2014

Plott (ECON 221) Spring 2014 1 / 71

Outline

1 Topic 2: The Supply Side of the EconomyThe Production Market

The Labor MarketLabor Demand

Labor Supply

Long-Run Aggregate Supply

Long-Run Economic Growth

Plott (ECON 221) Spring 2014 2 / 71

Topic 2 Readings & Goals

Readings1 ABC 8e (2014) Chapter 32 ABC 8e (2014) Chapter 6

Goals1 Introduce the supply side of the macro economy.2 Discuss how countries grow and why some countries grow faster than

others.3 Determine how wages are set in the labor market.

Plott (ECON 221) Spring 2014 3 / 71

Outline

1 Topic 2: The Supply Side of the EconomyThe Production Market

The Labor MarketLabor Demand

Labor Supply

Long-Run Aggregate Supply

Long-Run Economic Growth

Plott (ECON 221) The Production Market Spring 2014 4 / 71

Factors of Production

Capital (K ): tools, machines, and structures used in production

Labor (N): the physical and mental efforts of workers

Others (raw materials, land, energy)

Productivity of factors depends on technology and management

Plott (ECON 221) The Production Market Spring 2014 5 / 71

The Production Function

It’s the mapping of inputs into output. GDP (Y ) is produced with

capital (K , price weighted) and labor (N , hours):

Y = AF(K ,N)

Sometimes, I will modify the production function such that:

Y = AF(K ,N ,other inputs)

where other inputs include energy/oil

Exhibits constant returns to scale (CRS).

A realistic example is the Cobb-Douglas function for F(K ,N):

Y = AK aN1−a

Y = AK 0.3N0.7

A is Total Factor Productivity (TFP), an index of efficiency in the use of

inputs (technology). 0 < a < 1 capital share.

Plott (ECON 221) The Production Market Spring 2014 6 / 71

Two Measures of Productivity

Labor Productivity = YN = A

( KN

)0.3

Driven by A and KN

Total Factor Productivity (TFP) = A = YF(K ,N)

Basically TFP is a "catch-all" for anything that effects output otherthan K and N .

Workweek of labor and capitalQuality of labor and capitalRegulationInfrastructureCompetitionSpecializationInnovationStrategy (Entrepreneurial methods/new management techniques)

Some components of TFP tend to be procyclical

Definition of procyclical: Variable increases when Y is high, decreases

when Y is lowPlott (ECON 221) The Production Market Spring 2014 7 / 71

Measurement

Y is GDP (it is measured in real dollars). As noted above, we want to

measure Y in "real" dollars.

For our Cobb-Douglas production function (previous slide), K ismeasured in real dollars and N in terms of hours worked.

K often is measured as the replacement cost of capitalN often is measured in number of workers time hours per worker

However, in practice, N can be measured in different ways (number ofworkers, number of effective workers, production workers).

Hours worked takes into account part-time and full-time. Number ofeffective workers adjustment are made by BLS.Unskilled vs.skilled workers: "skill" differentials.

Note: When we talk about standard of livings: income per capita is YPop

where Y is income and Pop is a population measure – sometimes we

assume Pop = N , labor force.

Plott (ECON 221) The Production Market Spring 2014 8 / 71

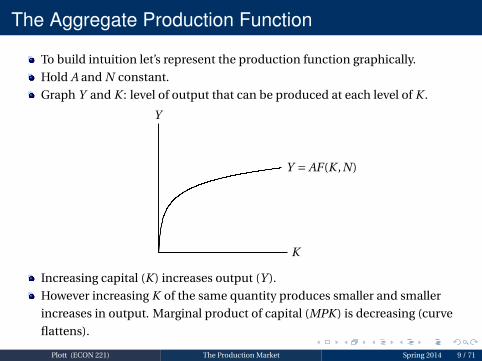

The Aggregate Production Function

To build intuition let’s represent the production function graphically.

Hold A and N constant.

Graph Y and K : level of output that can be produced at each level of K .

K

Y

Y = AF(K ,N)

Increasing capital (K ) increases output (Y ).

However increasing K of the same quantity produces smaller and smaller

increases in output. Marginal product of capital (MPK ) is decreasing (curve

flattens).

Plott (ECON 221) The Production Market Spring 2014 9 / 71

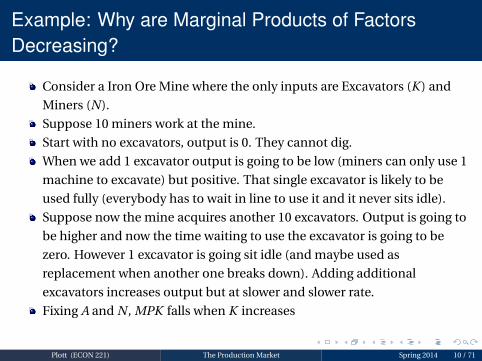

Example: Why are Marginal Products of FactorsDecreasing?

Consider a Iron Ore Mine where the only inputs are Excavators (K ) and

Miners (N).

Suppose 10 miners work at the mine.

Start with no excavators, output is 0. They cannot dig.

When we add 1 excavator output is going to be low (miners can only use 1

machine to excavate) but positive. That single excavator is likely to be

used fully (everybody has to wait in line to use it and it never sits idle).

Suppose now the mine acquires another 10 excavators. Output is going to

be higher and now the time waiting to use the excavator is going to be

zero. However 1 excavator is going sit idle (and maybe used as

replacement when another one breaks down). Adding additional

excavators increases output but at slower and slower rate.

Fixing A and N , MPK falls when K increases

Plott (ECON 221) The Production Market Spring 2014 10 / 71

The Aggregate Production Function (Continued)

Now hold A and K fixed.

Graph Y and N

A different slope than the previous graph (steeper because 1−a > a).

N

Y

Y = AF(K ,N)

Increasing labor (N) increases output (Y ).

Increasing N of the same quantity produces smaller and smaller increases

in output. Marginal product of labor (MPN) is decreasing (curve flattens).

Plott (ECON 221) The Production Market Spring 2014 11 / 71

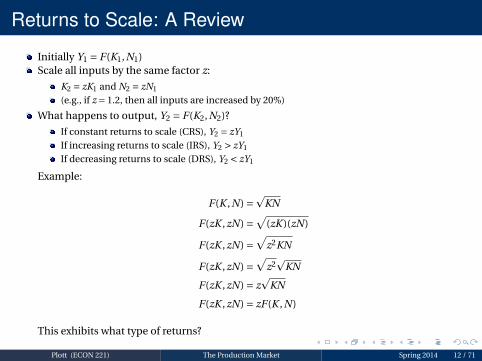

Returns to Scale: A Review

Initially Y1 = F(K1,N1)Scale all inputs by the same factor z:

K2 = zK1 and N2 = zN1

(e.g., if z = 1.2, then all inputs are increased by 20%)

What happens to output, Y2 = F(K2,N2)?

If constant returns to scale (CRS), Y2 = zY1

If increasing returns to scale (IRS), Y2 > zY1

If decreasing returns to scale (DRS), Y2 < zY1

Example:

F(K ,N) =pKN

F(zK ,zN) =√

(zK )(zN)

F(zK ,zN) =√

z2KN

F(zK ,zN) =√

z2p

KN

F(zK ,zN) = zp

KN

F(zK ,zN) = zF(K ,N)

This exhibits what type of returns?

Constant returns to scale (CRS) ∀z > 0

Plott (ECON 221) The Production Market Spring 2014 12 / 71

Returns to Scale: A Review

Initially Y1 = F(K1,N1)Scale all inputs by the same factor z:

K2 = zK1 and N2 = zN1

(e.g., if z = 1.2, then all inputs are increased by 20%)

What happens to output, Y2 = F(K2,N2)?

If constant returns to scale (CRS), Y2 = zY1

If increasing returns to scale (IRS), Y2 > zY1

If decreasing returns to scale (DRS), Y2 < zY1

Example:

F(K ,N) =pKN

F(zK ,zN) =√

(zK )(zN)

F(zK ,zN) =√

z2KN

F(zK ,zN) =√

z2p

KN

F(zK ,zN) = zp

KN

F(zK ,zN) = zF(K ,N)

This exhibits what type of returns? Constant returns to scale (CRS) ∀z > 0

Plott (ECON 221) The Production Market Spring 2014 12 / 71

Marginal Product of Labor

Plott (ECON 221) The Production Market Spring 2014 13 / 71

Marginal Product of Labor: a Decrease in TFP (A)

Plott (ECON 221) The Production Market Spring 2014 14 / 71

Outline

1 Topic 2: The Supply Side of the EconomyThe Production Market

The Labor MarketLabor Demand

Labor Supply

Long-Run Aggregate Supply

Long-Run Economic Growth

Plott (ECON 221) The Labor Market Spring 2014 15 / 71

Labor Market Roadmap: Demand and Supply

Three main concepts:1 Firms decide the optimal amount of labor to hire: Firm Labor Demand.

If you aggregate (i.e. add up) those decisions you obtain the AggregateLabor Demand.

2 Individual decision on optimal amount of leisure (= 1−N) to consume(and hence how much to work): Individual Labor Supply.If you aggregate those decisions you obtain the Aggregate Labor Supply.

3 Classical representation of the Labor Market Equilibrium:Aggregate Labor Demand = Aggregate Labor Supply

Note: no unemployment (real wages can adjust).

Plott (ECON 221) The Labor Market Spring 2014 16 / 71

Labor Demand: Firm’s Profit Maximizing Decision

In a competitive market, a firm can sell as much Y as it wants at the going price

P, and can hire as much N as it wants at the going nominal wage W .

Facing W and P, a profit maximizing firm will hire N to the point were MPN = WP

(the benefit from an additional worker (in terms of additional output) must equal

the cost which they are paid). This is straight from Microeconomics)

Why is this optimal? The MPN is decreasing in N , so:

If MPN > W /P then the firm can increase profits by increasing N . (Intuition: the

new worker adds more value than he costs, so profits increase).

If MPN < W /P then the firm can increase profits by decreasing N. (Intuition:

letting go a worker reduces the wage bill more than it cuts production, so profits

increase).

Example:

With Cobb-Douglas production function: MPN = 0.7Y

N= 0.7A

(K

N

)0.3

If firms maximize profits, then:W

P= 0.7

Y

N= 0.7A

(K

N

)0.3

Plott (ECON 221) The Labor Market Spring 2014 17 / 71

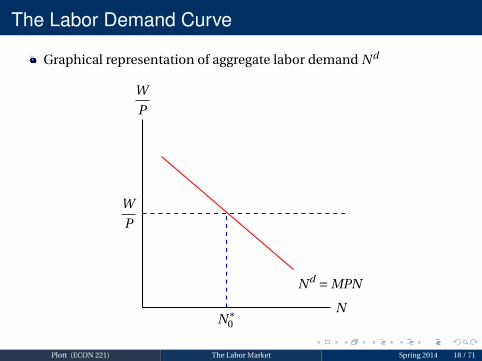

The Labor Demand Curve

Graphical representation of aggregate labor demand Nd

N

W

P

Nd = MPN

W

P

N∗0

Plott (ECON 221) The Labor Market Spring 2014 18 / 71

Notes on the Labor Demand Curve

Let us consider the level of K fixed for now.

Nd slopes downward: Nd = MPN = (1−a)A

(K

N

)a

= 0.7A

(K

N

)0.3

Nd rises with A and K .

When A increases, all my inputs are more productive, so the marginalproduct of one extra unit of labor input is higher.When K is higher, I have more capital to use with my labor (one extraunit of labor can work with more capital), hence the marginal productof labor is higher.

Note: labor demand shifts when the aggregate production changes (we

will see that the aggregate supply shifts).

Caveat: Who says that there is a demand for more Y ?

Need to look at the demand side of economy (introduced in Topic 1 –discussed in depth throughout the course).

Plott (ECON 221) The Labor Market Spring 2014 19 / 71

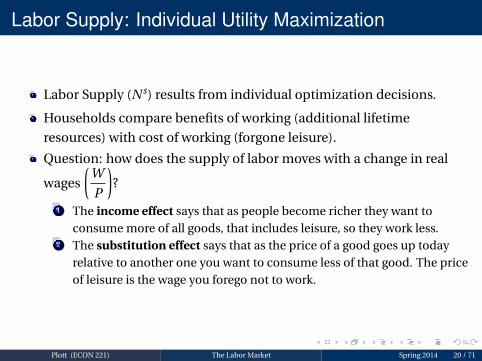

Labor Supply: Individual Utility Maximization

Labor Supply (N s) results from individual optimization decisions.

Households compare benefits of working (additional lifetime

resources) with cost of working (forgone leisure).

Question: how does the supply of labor moves with a change in real

wages

(W

P

)?

1 The income effect says that as people become richer they want toconsume more of all goods, that includes leisure, so they work less.

2 The substitution effect says that as the price of a good goes up todayrelative to another one you want to consume less of that good. The priceof leisure is the wage you forego not to work.

Plott (ECON 221) The Labor Market Spring 2014 20 / 71

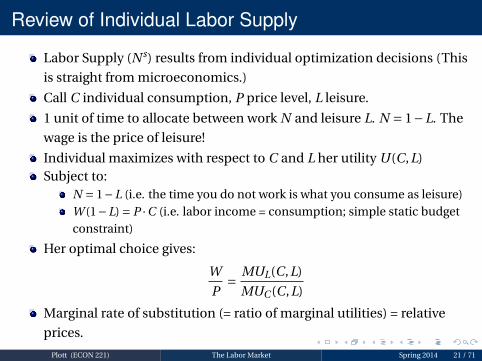

Review of Individual Labor Supply

Labor Supply (N s) results from individual optimization decisions (This

is straight from microeconomics.)

Call C individual consumption, P price level, L leisure.

1 unit of time to allocate between work N and leisure L. N = 1−L. The

wage is the price of leisure!

Individual maximizes with respect to C and L her utility U(C,L)Subject to:

N = 1−L (i.e. the time you do not work is what you consume as leisure)W (1−L) = P ·C (i.e. labor income = consumption; simple static budgetconstraint)

Her optimal choice gives:

W

P= MUL(C,L)

MUC(C,L)

Marginal rate of substitution (= ratio of marginal utilities) = relative

prices.

Plott (ECON 221) The Labor Market Spring 2014 21 / 71

Review of a Simple Individual Labor Supply

Her optimal choice is:

W

P= MUL(C,L)

MUC(C,L)

Marginal rate of substitution (= ratio of marginal utilities) = relative prices.

If WP goes up, then MUL(C,L)

MUC (C,L) has to go up.

QUESTION: Is N(= 1−L) going to increase or decrease?

Recall first that marginal utility of a good goes down with the amount

consumed (the 10th hamburger is not as satisfying as the 1st).

Substitution effect: if real wage goes up you work more. MUL(C,L)

increases – consume less leisure and MUC(C,L) decreases – consume more

goods).

Income effect: if real wage goes up you work less. MUL(C,L) decreases –

consume more leisure and MUC(C,L) decreases even more – consume

more goods).

Plott (ECON 221) The Labor Market Spring 2014 22 / 71

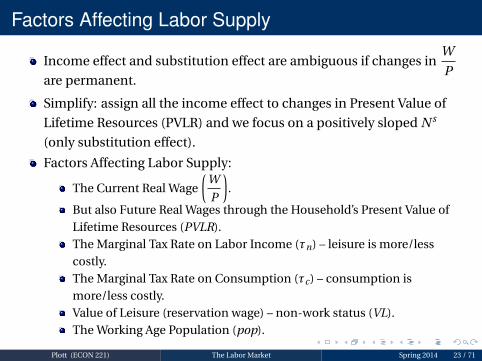

Factors Affecting Labor Supply

Income effect and substitution effect are ambiguous if changes inW

Pare permanent.

Simplify: assign all the income effect to changes in Present Value of

Lifetime Resources (PVLR) and we focus on a positively sloped N s

(only substitution effect).

Factors Affecting Labor Supply:

The Current Real Wage

(W

P

).

But also Future Real Wages through the Household’s Present Value ofLifetime Resources (PVLR).The Marginal Tax Rate on Labor Income (τn) – leisure is more/lesscostly.The Marginal Tax Rate on Consumption (τc) – consumption ismore/less costly.Value of Leisure (reservation wage) – non-work status (VL).The Working Age Population (pop).

Plott (ECON 221) The Labor Market Spring 2014 23 / 71

The Labor Supply Curve

Graphical representation of aggregate labor supply N s

NS(PVLR,τc,τn,population,Value of Leisure)

N

W

P

N s(·)

Ns slopes upward due to the substitution effect of before-tax wages

Plott (ECON 221) The Labor Market Spring 2014 24 / 71

Labor Supply Curve Notes

In terms of "wages and earnings", there is both an income and

substitution effect – we will look at them separately – in the real world,

they often occur jointly!The Real Wage – HOLDING PVLR fixed: A higher W

P encouragesindividuals to substitute away from leisure and toward work (leisurebecomes more expensive). This is a substitution effect. This is why thelabor supply curve slopes upwards!

Estimating this substitution effect is difficult since PVLR is not easilyheld constant. Estimates range from 0 - 2% (For a 1% increase inafter-tax W

P holding PVLR fixed, labor supply either increases by 0% or2%). Very Wide Range – little consensus.

PVLR = initial wealth + present discounted value of earningsA higher PVLR induces individuals to work less (lower N s) for a givenafter-tax wage, allowing them to enjoy more leisure (If leisure ispreferred to work – as I get richer, I can afford to work less).PVLR is net of taxes and non-work governmental transfers and inclusiveof all other transfers.

Plott (ECON 221) The Labor Market Spring 2014 25 / 71

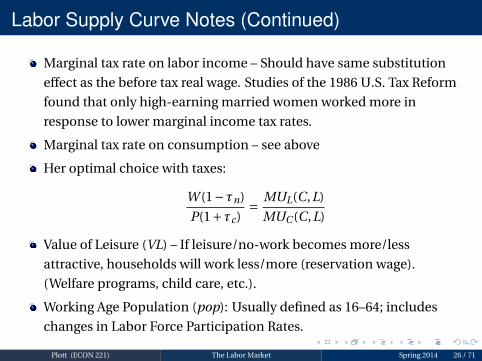

Labor Supply Curve Notes (Continued)

Marginal tax rate on labor income – Should have same substitution

effect as the before tax real wage. Studies of the 1986 U.S. Tax Reform

found that only high-earning married women worked more in

response to lower marginal income tax rates.

Marginal tax rate on consumption – see above

Her optimal choice with taxes:

W (1−τn)

P(1+τc)= MUL(C,L)

MUC(C,L)

Value of Leisure (VL) – If leisure/no-work becomes more/less

attractive, households will work less/more (reservation wage).

(Welfare programs, child care, etc.).

Working Age Population (pop): Usually defined as 16–64; includes

changes in Labor Force Participation Rates.

Plott (ECON 221) The Labor Market Spring 2014 26 / 71

Labor Market Equilibrium

N

W

P

N s(PVLR,τn,τc,pop,VL)

Nd(A,K )

N0

(W

P

)0

Plott (ECON 221) The Labor Market Spring 2014 27 / 71

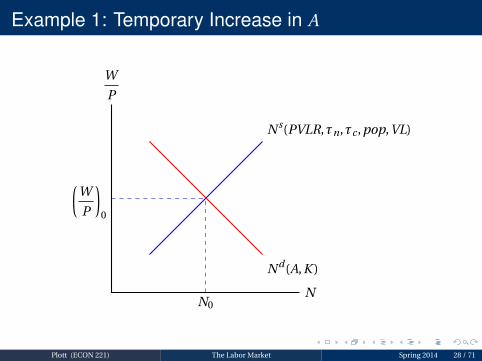

Example 1: Temporary Increase in A

N

W

P

N s(PVLR,τn,τc,pop,VL)

Nd(A,K )

N0

(W

P

)0

Plott (ECON 221) The Labor Market Spring 2014 28 / 71

Example 2: Permanent Increase in A

N

W

P

N s(PVLR,τn,τc,pop,VL)

Nd(A,K )

N0

(W

P

)0

Plott (ECON 221) The Labor Market Spring 2014 29 / 71

Interpretation

If firms become more productive they demand more labor. The Nd

curve shifts rightward. Real wages increase from the initial level since

workers become scarce. However PVLR stays the same so no

movement of N s. Then if the productivity shock is temporary,

everything reverts back.

If the shift is permanent people are also permanently "richer", so an

increase in PVLR will produce a consequent shift leftward of the N s

curve (income effect). This leaves the final result ambiguous.

Note: for any question involving the labor market I will specify

whether the income or substitution effect dominates.

Plott (ECON 221) The Labor Market Spring 2014 30 / 71

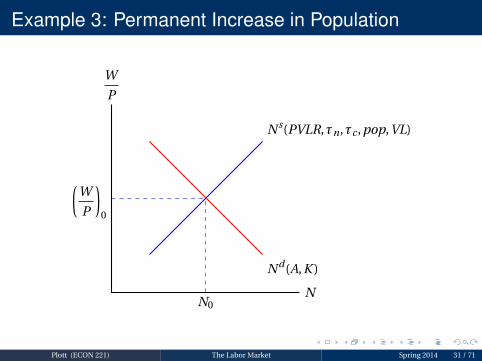

Example 3: Permanent Increase in Population

N

W

P

N s(PVLR,τn,τc,pop,VL)

Nd(A,K )

N0

(W

P

)0

Plott (ECON 221) The Labor Market Spring 2014 31 / 71

Consumption and Labor Taxes

Marginal tax rate on labor income – people care about after-tax wage

W (1−τn).

Consumption taxes – people care about after-tax price P(1+τC).

While the substitution effect of changing before-tax wage causes a

movement along the supply curve, the substitution effect of changing

taxes causes the labor supply curve to shift.

If leisure becomes relatively more inexpensive than consumption

(labor taxes or consumption taxes increase), the N s shifts to the left.

If the shift is permanent people are also permanently "poorer", so a

drop of PVLR will go down with consequent shift right of the N s curve

(income effect). This leaves the final result ambiguous.

Plott (ECON 221) The Labor Market Spring 2014 32 / 71

Example 4: Temporary Increase in Taxes (τc or τn)

N

W

P

N s(PVLR,τn,τc,pop,VL)

Nd(A,K )

N0

(W

P

)0

Plott (ECON 221) The Labor Market Spring 2014 33 / 71

Example 5: Permanent Increase in Taxes (τc or τn)

N

W

P

N s(PVLR,τn,τc,pop,VL)

Nd(A,K )

N0

(W

P

)0

Plott (ECON 221) The Labor Market Spring 2014 34 / 71

Recap on Labor Supply

Substitution Effect:For a given PVLR, a higher after-tax wage increases N s.

This is why Labor Supply Curve slopes upward

Income Effect:

For a given after-tax wage, higher PVLR decreases N s.Evidence:

Weak consensus is that, with equal (%) increase in PVLR and the after-tax

wage, Ns falls (income effect dominates).

A must read: Chapter 3 (on labor markets) in the text book.

Plott (ECON 221) The Labor Market Spring 2014 35 / 71

Labor Market Equilibrium (in the Long-Run)

We define Long-run Equilibrium in macroeconomics as occurring

when the labor market clears.

By definition, long-run macro equilibrium exists when N = N .

At N , labor demand = labor supply. So, by definition, all workers whowant a job (the suppliers) are able to find a firm looking for a worker(the demanders).

Implies that cyclical unemployment = zero at N .Long-run equilibrium is characterized by zero cyclical unemployment.

It is an equilibrium in that there is no incentive for real wages tochange at N .

Real wages( W

P

)has two components: nominal wages (W ) and the price

level (P).

Note: Y (by definition) = AK 0.3(N)0.7

Y = long-run equilibrium level of output (where labor market is in

equilibrium)

Plott (ECON 221) The Labor Market Spring 2014 36 / 71

Outline

1 Topic 2: The Supply Side of the EconomyThe Production Market

The Labor MarketLabor Demand

Labor Supply

Long-Run Aggregate Supply

Long-Run Economic Growth

Plott (ECON 221) Long-Run Aggregate Supply Spring 2014 37 / 71

Our First Aggregate Supply Curve

Suppose prices (P) increase. What happens in the labor market in thelong-run?

In terms of equilibrium, nothing happens!Increasing prices have no effect on labor demand (A and K do not change).Increasing prices have no effect on labor supply (VL, taxes, population, etc.do not change).

You may ask "Doesn’t PVLR change when prices increase?" No!

As long as nominal wages adjust, real wages will be unchanged when Pincreases.The % change in prices will be match exactly by the % change in nominalwages – real wages will not change (so PVLR will not change).No effect on labor supply.

Key: Because real wages will not change, changes in prices will have NO

effect on the labor market (i.e. it will have no effect on N) in the long-run.

Conclusion: changing prices will have NO effect on Y (since N is

constant) in the long-run.

Plott (ECON 221) Long-Run Aggregate Supply Spring 2014 38 / 71

Our First Aggregate Supply Curve

If the labor market clears, changes in prices will lead to equal changes in nominal wages. As aresult, there will be no change in N and hence, no change in Y .

This results in a vertical long-run aggregate supply (LRAS) curve. Prices do not affect productionin the long-run!

Y

P

LRAS

Y

Plott (ECON 221) Long-Run Aggregate Supply Spring 2014 39 / 71

What shifts Y ? (the LRAS)

Anything that affects the labor market will affect Y .

If N increases, Y will shift to the right.

If N decreases, Y will shift to the left.

Summary – Y will shift right if:

A, K increase (and income effect on N s is small relative to shift in Nd)population increaseslabor income taxes fall (and income effect is small relative tosubstitution effect)labor income taxes rise (and income effect is large relative tosubstitution effect)

Plott (ECON 221) Long-Run Aggregate Supply Spring 2014 40 / 71

Things to Remember!

The demand side of the economy is NOT important for determining Y .

All we need to know is A, K and N and we know Y .The demand side of the economy is not important for economic growth.Key: If I ever ask you about what determines Y (i.e.,output/income/expenditure in the long-run), you should think about A,K and the labor market.

As a rule, K will be fixed unless I tell you otherwise (for simplicity, you will

see why soon).

Why do we care about the demand side of the economy?

In the long-run, prices will be determined by demand.Also, LRAS is dependent on labor market being in equilibrium. In theshort-run, the labor market need not be in equilibrium.Demand will determine output in the short-run.

Plott (ECON 221) Long-Run Aggregate Supply Spring 2014 41 / 71

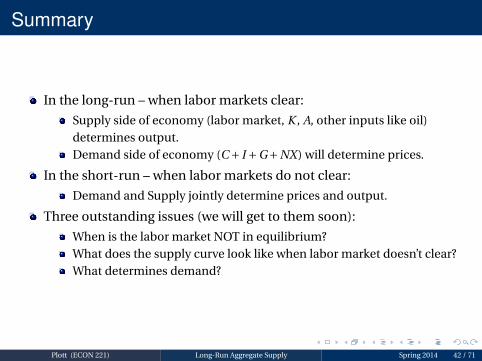

Summary

In the long-run – when labor markets clear:

Supply side of economy (labor market, K , A, other inputs like oil)determines output.Demand side of economy (C + I +G+NX) will determine prices.

In the short-run – when labor markets do not clear:

Demand and Supply jointly determine prices and output.

Three outstanding issues (we will get to them soon):

When is the labor market NOT in equilibrium?What does the supply curve look like when labor market doesn’t clear?What determines demand?

Plott (ECON 221) Long-Run Aggregate Supply Spring 2014 42 / 71

When Are Labor Markets in Dis-equilibrium?

The labor market is in disequilibrium when labor demand is not equal

to labor supply.

Nominal wages do not adjust to clear the labor market.

We refer to this as "sticky" or "rigid" wages.Because of wage contracts (and uncertainty), nominal wages no notalways adjust immediately.Need a model for short-run disequilibrium – we will do that in Topic 6.

Plott (ECON 221) Long-Run Aggregate Supply Spring 2014 43 / 71

Cyclical Unemployment in Labor Markets

When do we get cyclical unemployment in our models?

Cyclical unemployment occurs when there are no jobs available (labor demand) for those withthe skills and the desire to work (labor supply) at current wages.

Cyclical unemployment occurs only in disequilibrium (when desired labor demand less thandesired labor supply – at given wages)

N

W

P

Ns0

Nd0

N0

(W

P

)0

a

Plott (ECON 221) Long-Run Aggregate Supply Spring 2014 44 / 71

Outline

1 Topic 2: The Supply Side of the EconomyThe Production Market

The Labor MarketLabor Demand

Labor Supply

Long-Run Aggregate Supply

Long-Run Economic Growth

Plott (ECON 221) Long-Run Economic Growth Spring 2014 45 / 71

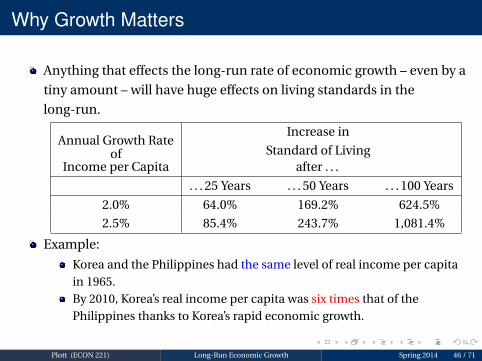

Why Growth Matters

Anything that effects the long-run rate of economic growth – even by a

tiny amount – will have huge effects on living standards in the

long-run.

Annual Growth Rateof

Income per Capita

Increase in

Standard of Livingafter . . .

. . . 25 Years . . . 50 Years . . . 100 Years

2.0% 64.0% 169.2% 624.5%

2.5% 85.4% 243.7% 1,081.4%

Example:

Korea and the Philippines had the same level of real income per capitain 1965.By 2010, Korea’s real income per capita was six times that of thePhilippines thanks to Korea’s rapid economic growth.

Plott (ECON 221) Long-Run Economic Growth Spring 2014 46 / 71

Sources of Economic Growth

We want to study what’s behind ∆YY .

Start from a stylized aggregate Cobb-Douglas production function for

F(K ,N):

Y = AK aN1−a

Suppose the only factor increasing is K . Jumps to K +∆K . Capital

growth rate is ∆KK .

How much does Y grow?

Rule of thumb for the proportional growth rate of a quantity raised to a

power:

∆Y

Y= a

∆K

K(1)

If all economic growth ∆YY was due to the capital stock growth we

would have (1).

Plott (ECON 221) Long-Run Economic Growth Spring 2014 47 / 71

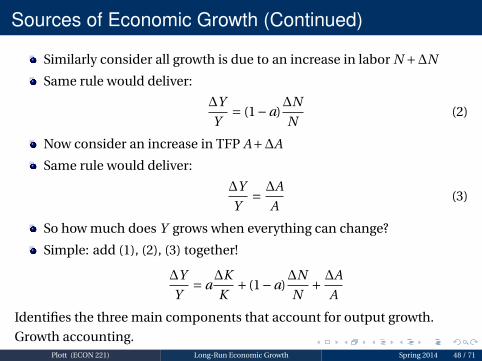

Sources of Economic Growth (Continued)

Similarly consider all growth is due to an increase in labor N +∆N

Same rule would deliver:

∆Y

Y= (1−a)

∆N

N(2)

Now consider an increase in TFP A+∆A

Same rule would deliver:

∆Y

Y= ∆A

A(3)

So how much does Y grows when everything can change?

Simple: add (1), (2), (3) together!

∆Y

Y= a

∆K

K+ (1−a)

∆N

N+ ∆A

A

Identifies the three main components that account for output growth.

Growth accounting.Plott (ECON 221) Long-Run Economic Growth Spring 2014 48 / 71

Growth Accounting

Y = AK 0.3N0.7 (US production function) implies:

∆Y

Y= 0.3

∆K

K+0.7

∆N

N+ ∆A

A

Output in a country can be decomposed in:

Growth in TFP (entrepreneurial ability, education, roads, technology,etc.)Growth in Capital (machines, equipment, plants, etc.)Growth in Labor (workforce, population, labor participation, etc.).

Note: For a general production function (i.e. not Cobb-Douglas)

∆Y

Y= aK

∆K

K+aN

∆N

N+ ∆A

A

where aK = elasticity of output with respect to capital (same definition

for labor).

Plott (ECON 221) Long-Run Economic Growth Spring 2014 49 / 71

Limits of Growth Accounting: Just Diagnostics

. . . these accounting exercises say nothing about causality, and so are

very hard to interpret.

Say you found it’s 50% efficiency and 50% factor endowments. What

conclusion do you draw from it? You could imagine a story where the

underlying cause of growth is factor accumulation, with

technological upgrading or enhanced allocative efficiency as the

by-product.

Or you could imagine a story whereby technological change is the

driver behind increased accumulation.

Both are compatible with the result from accounting decomposition.

Indeed, I have yet to see a sources-of-growth decomposition which

answers a useful and relevant economic or policy question.

Dani Rodrik (KSG, Harvard)

http://rodrik.typepad.com/dani_rodriks_weblog/2008/02/

what-use-is-sou.html

Plott (ECON 221) Long-Run Economic Growth Spring 2014 50 / 71

Long-Run Growth

Two basic questions about growth:1 What’s the relationship between the long-run standard of living and the

saving rate, population growth rate, and rate of technical progress?2 How does economic growth change over time? Will it speed up, slow

down, or stabilize?

We will use the Solow Growth model to explore these questions.

Plott (ECON 221) Long-Run Economic Growth Spring 2014 51 / 71

The Solow Growth Model: Assumptions

A worker is a worker. Assume equal qualifications (homogeneous labor)

A unit of capital is a unit of capital, no matter what it actually is (homogeneous

capital).

K is no longer fixed: investment causes it to grow, depreciation causes it to

shrink.

Technology is just the function that connects K and N to Y . An engineering

blueprint.

There’s no unemployment (or it doesn’t change)

Constant returns to scale (CRS)

The economy is closed (i.e. NX = 0) and the asset market clears, so It = St ; i.e.

national saving equals investment.

G = T = 0 only to simplify presentation; we can still do fiscal policy experiments.

Population and work force grow at same rate∆Nt

Nt= n (exogenous)

Example: Suppose N = 1,000 in year 1 and the population is growing at 2% per year(n = 0.02).Then ∆N = nN = 0.02×1,000 = 20, so N = 1,020 in year 2.

Plott (ECON 221) Long-Run Economic Growth Spring 2014 52 / 71

The Solow Model

Due to Robert Solow (1924 – ), won Nobel Prize (1987) for

contributions to the study of economic growth.A major paradigm:

widely used in policy makingbenchmark against which most recent growth theories are compared

Looks at the determinants of economic growth and the standard of

living in the long-runhttp://www.nobelprize.org/nobel_prizes/economic-sciences/laureates/1987/solow-facts.html

Plott (ECON 221) Long-Run Economic Growth Spring 2014 53 / 71

The Solow Growth Model: Production Function

Labor productivity is the key determinant of real GDP per capita and thestandard of living in a country. This model explains how the long-run growthrate of the economy depends on saving, population growth, andtechnological change. The model begins with the per capita productionfunction where y is real GDP per worker, k is capital per worker, or thecapital-labor ratio. For simplicity, assume total factor productivity (TFP)equals one; i.e. A = 1:

Yt = F(Kt ,Nt ) = K at N1−a

t Aggregate Production Function (Cobb-Douglas)

Yt

Nt= F(Kt ,Nt )

Nt= K a

t N1−at

NtDivide by Nt

Yt

Nt= F

(Kt

Nt,

Nt

Nt

)= K a

t N1−at

Nat N1−a

t

Nt = N1t = Na+(1−a)

t = Nat N1−a

t

yt = F(kt ,1) = kat

yt = f (kt ) = kat Per Capita Production Function (Cobb-Douglas)

Plott (ECON 221) Long-Run Economic Growth Spring 2014 54 / 71

The Solow Growth Model: Capital Accumulation

Capital accumulation is the change over time in the capital stock. The capitalstock increases because of investment in new capital, but it also decreasesbecause of depreciation and dilution. Under the simplifying assumption of aclosed economy with no government sector, all output is either consumed orinvested in new capital goods. Real GDP per worker, y, can be divided intoconsumption per worker, c, and investment per worker, i:

Yt = Ct + It +Gt +NXt Aggregate Income-Expenditure Equation

Yt = Ct + It G = T = 0 and NX = 0 (Assumed)

Yt

Nt= Ct

Nt+ It

NtDivide by Nt

yt = ct + it Per Capita Form

Note: it is investment per capita NOT the nominal interest rate!

Plott (ECON 221) Long-Run Economic Growth Spring 2014 55 / 71

The Solow Growth Model: Saving

Saving is proportional to current income where s is the saving rate,

which is between 0 and 1:

St = sYt

s = St

Yt

Note: s is the only lowercase variable that is NOT equal to its uppercase

version divided by N .

We assume that s, the fraction of total output saved, or the national

saving rate, is a constant fraction of real GDP per worker, y.

Plott (ECON 221) Long-Run Economic Growth Spring 2014 56 / 71

The Solow Growth Model: Capital Accumulation

The capital-labor ratio, k, increases when the stock of investment goodsincreases faster than the number of workers. Because saving and investmentare equal, investment per worker, i, equals:

It = St

it = syt plug in St = sYt

ct = (1− s)yt substitute into yt = ct + it

Substituting the production function into the equation for investment, wehave the investment function: it = syt = sf (kt )

As the capital-labor ratio increases, real GDP per worker increases, causinginvestment per worker to increase. Because of diminishing marginal returns,increasing the capital-labor ratio causes smaller and smaller increases in realGDP per worker. Investment per worker equals the constant saving ratemultiplied by real GDP per worker, so the increase in investment per workergets smaller and smaller as the capital-labor ratio increases.

Plott (ECON 221) Long-Run Economic Growth Spring 2014 57 / 71

The Solow Growth Model: Depreciation and Dilution

The depreciation rate is the rate at which the capital stock declines due toeither capital goods becoming worn out by use or becoming obsolete.Assume that the deprecation rate, d, is a constant fraction of the capital-laborratio and is between zero and one:

Depreciation = dk

Investment and depreciation affect the numerator of the capital-labor ratio.Changes in the labor force affect the denominator of the capital-labor ratio.We can think of the effect of the labor force increasing faster than the capitalstock as spreading out-diluting-the capital stock over more workers. Theamount of dilution equals the labor force growth rate, n, multiplied by thecapital-labor ratio:

Dilution = nk

Note: both depreciation and the population growth rate are greater than

zero; i.e. d > 0 and n > 0Plott (ECON 221) Long-Run Economic Growth Spring 2014 58 / 71

The Solow Growth Model: Equation of Motion

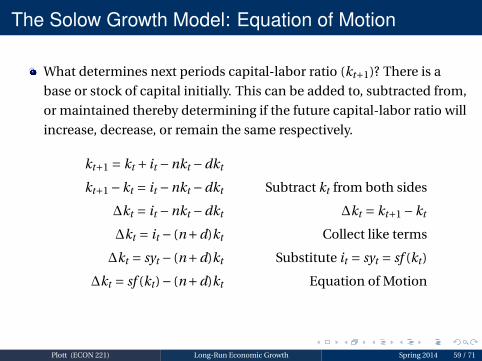

What determines next periods capital-labor ratio (kt+1)? There is a

base or stock of capital initially. This can be added to, subtracted from,

or maintained thereby determining if the future capital-labor ratio will

increase, decrease, or remain the same respectively.

kt+1 = kt + it −nkt −dkt

kt+1 −kt = it −nkt −dkt Subtract kt from both sides

∆kt = it −nkt −dkt ∆kt = kt+1 −kt

∆kt = it − (n+d)kt Collect like terms

∆kt = syt − (n+d)kt Substitute it = syt = sf (kt)

∆kt = sf (kt)− (n+d)kt Equation of Motion

Plott (ECON 221) Long-Run Economic Growth Spring 2014 59 / 71

The Solow Growth Model: Steady State

In the Solow growth model, equilibrium occurs when the capital-labor

ratio is constant; real GDP is also constant. An equilibrium in the

Solow growth model in which the capital-labor ratio and real GDP per

worker are constant, but capital, labor and output are growing, is

called a steady state.

∆kt = sf (kt)− (n+d)kt Equation of Motion

∆kt = 0 = sf (kt)− (n+d)kt In steady state

sf (k∗) = (n+d)k∗ An asterisk denotes steady state

Plott (ECON 221) Long-Run Economic Growth Spring 2014 60 / 71

The Solow Growth Model: Determinants – Saving

Higher saving rate means higher capital-labor ratio, higher output per

worker, and higher consumption per worker

Should a policy goal be to raise the saving rate?

Not necessarily, since the cost is lower consumption in the short-runThere is a trade-off between present and future consumption

Steady state values differ across countries. Government policies that

change the saving rate have a level effect – that is, the policies can raise

real GDP per capita and the standard of living to a higher level, but do

not have a growth effect: The policies will not result in a sustained

increase in the standard of living over time. Only policies that change

the steady-state growth rate of real GDP per worker have a growth

effect that will bring about sustained increases in the standard of

living.

Plott (ECON 221) Long-Run Economic Growth Spring 2014 61 / 71

The Solow Growth Model: The Golden Rule

While a higher capital stock implies higher output, this does not mean

that a higher capital stock is necessarily desirable. To sustain a high

level of the capital stock, a lot of output may have to be devoted to

replacement investment, so it will not be available for consumption.

We now compare steady states in terms of consumption. The steady

state with the highest possible level of consumption is known as the

golden rule level of capital accumulation. The golden rule can be

analyzed without reference to people’s behavior (that is, without

reference to the saving rate).Transition to the golden rule steady state:

The economy does NOT have a tendency to move toward the goldenrule steady state.Achieving the golden rule requires that policymakers adjust s.This adjustment leads to a new steady state with higher consumption.But what happens to consumption during the transition to the goldenrule?

Plott (ECON 221) Long-Run Economic Growth Spring 2014 62 / 71

Edmund Phelps (1933 – )

Nobel Prize (2006)

Developed golden rule level of capital accumulation.

Edmund Phelps helped change the way we think about

macroeconomic theory and policy, by introducing imperfect

information and costly communication into the theory, and deriving

their implications for the dynamics of inflation and unemployment.http://www.nobelprize.org/nobel_prizes/economic-sciences/laureates/2006/phelps-facts.html

Plott (ECON 221) Long-Run Economic Growth Spring 2014 63 / 71

The Solow Growth Model: Determinants – PopulationGrowth

Higher population growth means a lower capital-labor ratio, lower

output per worker, and lower consumption per worker .

Should a policy goal be to reduce population growth?

Doing so will raise consumption per workerBut it will reduce total output and consumption, affecting a nation’sability to defend itself or influence world events

The Solow model also assumes that the proportion of the populationof working age is fixed

But when population growth changes dramatically this may not be trueChanges in cohort sizes may cause problems for social security systemsand areas like health care

Plott (ECON 221) Long-Run Economic Growth Spring 2014 64 / 71

The Malthusian Model (1798)

Thomas Robert Malthus (1766–1834) argued in his book An Essay on the

Principle of Population as It Affects the Future Improvement of Society that

an ever-increasing population would continually strain society’s ability to

provide for itself. Mankind, he predicted, would forever live in poverty.

Malthus began by noting that "food is necessary to the existence of man"

and that "the passion between the sexes is necessary and will remain

nearly in its present state". He concluded that "the power of population is

infinitely greater than the power in the earth to produce subsistence for

man". According to Malthus, the only check on population growth was

"misery and vice".

Malthus neglected the effects of technological progress; e.g. birth control.

Since Malthus, world population has increased sixfold, yet living standards

are higher than ever.

http://www.econlib.org/library/Malthus/malPopCover.html

Plott (ECON 221) Long-Run Economic Growth Spring 2014 65 / 71

The Dismal Science

. . . the dismal science

– Thomas Carlyle

Plott (ECON 221) Long-Run Economic Growth Spring 2014 66 / 71

The Kremerian Model (1993)

While Malthus saw population growth as a threat to rising living

standards, economist Michael Kremer (1964 – ) has suggested that

world population growth is a key driver of advancing economic

prosperity.

If there are more people, Kremer argues, then there are more

scientists, inventors, and engineers to contribute to innovation and

technological progress.

Evidence, from very long historical periods:1 As world population growth rate increased, so did rate of growth in

living standards2 Historically, regions with larger populations have enjoyed faster growth

Plott (ECON 221) Long-Run Economic Growth Spring 2014 67 / 71

Economic Growth as "Creative Destruction"

In his 1942 book Capitalism, Socialism, and Democracy, economist Joseph

Schumpeter (1883 – 1950) suggested that economic progress comes through a

process of creative destruction.

According to Schumpeter, the driving force behind progress is the entrepreneur with

an idea for a new product, a new way to produce an old product, or some other

innovation. When the entrepreneur’s firm enters the market, it has some degree of

monopoly power over its innovation; indeed, it is the prospect of monopoly profits

that motivates the entrepreneur.

An example of creative destruction involves the retailing giant Walmart. Although

retailing may seem like a relatively static activity, in fact it is a sector that has seen

sizable rates of technological progress over the past several decades. Through better

inventory-control, marketing, and personnel-management techniques, for example,

Walmart has found ways to bring goods to consumers at lower cost than traditional

retailers. These changes benefit consumers, who can buy goods at lower prices, and

the stockholders of Walmart, who share in its profitability. But they adversely affect

small mom-and-pop stores, which find it hard to compete when a Walmart opens

nearby.

Plott (ECON 221) Long-Run Economic Growth Spring 2014 68 / 71

The Solow Growth Model: Balanced Growth

Solow model’s steady state exhibits balanced growth – many variablesgrow at the same rate.

Solow model predicts y and k grow at the same rate (g), so KY should be

constant. This is true in the real world.Solow model predicts real wage grows at same rate as y, while real rentalprice is constant. Also true in the real world.

Solow model predicts that, other things equal, poor countries (withlower y and k) should grow faster than rich ones.

If true, then the income gap between rich and poor countries wouldshrink over time, causing living standards to converge.In real world, many poor countries do NOT grow faster than rich ones.

Plott (ECON 221) Long-Run Economic Growth Spring 2014 69 / 71

The Solow Growth Model: Convergence

Does this mean the Solow model fails?

No, because "other things" aren’t equal:

In samples of countries with similar savings and population growthrates, income gaps shrink about 2% per year.In larger samples, after controlling for differences in saving, populationgrowth, and human capital, incomes converge by about 2% per year.

The Solow growth model predicts that countries will converge

provided that they have the same steady state. However, steady states

can differ among countries as a result of differences in saving rates,

labor force growth rates, or the rates of labor-augmenting

technological change. Countries exhibit conditional convergence,

where each country converges to its own steady state.

Plott (ECON 221) Long-Run Economic Growth Spring 2014 70 / 71

Additional Topics

A chemist, a physicist, and an economist are all trapped on a desert island,trying to figure out how to open a can of food. "Let’s heat the can over the fireuntil it explodes," says the chemist. "No, no," says the physicist, "let’s drop thecan onto the rocks from the top of a high tree." "I have an idea," says theeconomist. "First, we assume a can opener. . . "

Endogenous growth theory: models of economic growth that try to

explain the rate of technological change; rejects the Solow model’s

assumption of exogenous technological change.

Poverty traps: a self-perpetuating condition where an economy, caught in

a vicious cycle, suffers from persistent underdevelopment.

Esther Duflo won the John Bates Clark Medal in 2010 for her work in

development economics (a branch of economics which deals with

economic aspects of the development process in low-income countries).

http://www.ted.com/talks/lang/en/esther_duflo_social_

experiments_to_fight_poverty.html

Plott (ECON 221) Long-Run Economic Growth Spring 2014 71 / 71