long-term debt-paying ability copyright ©2007 thomson south-western, a part of the thomson...

Post on 19-Dec-2015

216 views

TRANSCRIPT

Long-TermDebt-Paying Ability

COPYRIGHT ©2007 Thomson South-Western, a part of the Thomson Corporation. Thomson, the Star logo, and South-Western are trademarks used herein under license.

L 7 - Chapter 7

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #2

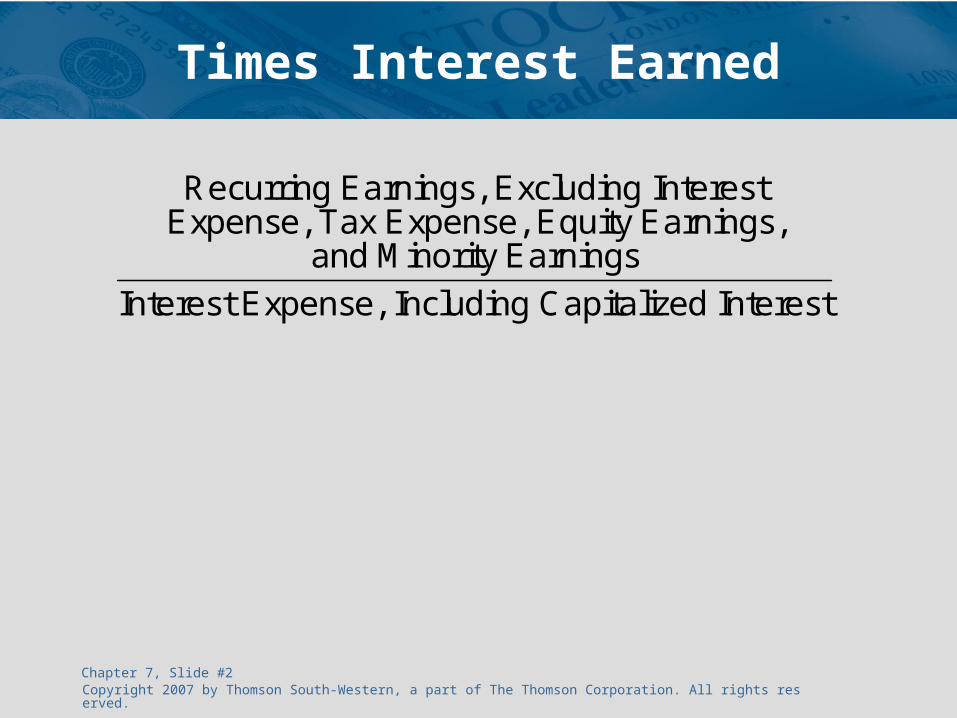

Times Interest Earned

Recurring Earnings, Excluding InterestExpense, Tax Expense, Equity Earnings,

and Minority Earnings

Interest Expense, Including Capitalized Interest

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #3

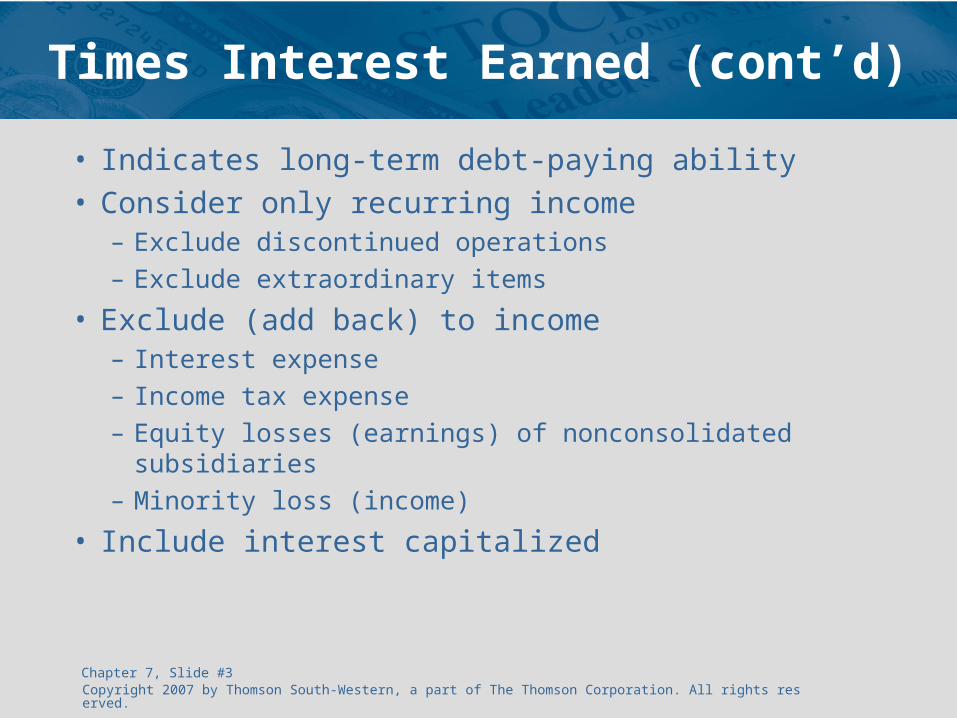

Times Interest Earned (cont’d)

• Indicates long-term debt-paying ability• Consider only recurring income

– Exclude discontinued operations– Exclude extraordinary items

• Exclude (add back) to income– Interest expense– Income tax expense– Equity losses (earnings) of nonconsolidated subsidiaries– Minority loss (income)

• Include interest capitalized

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #4

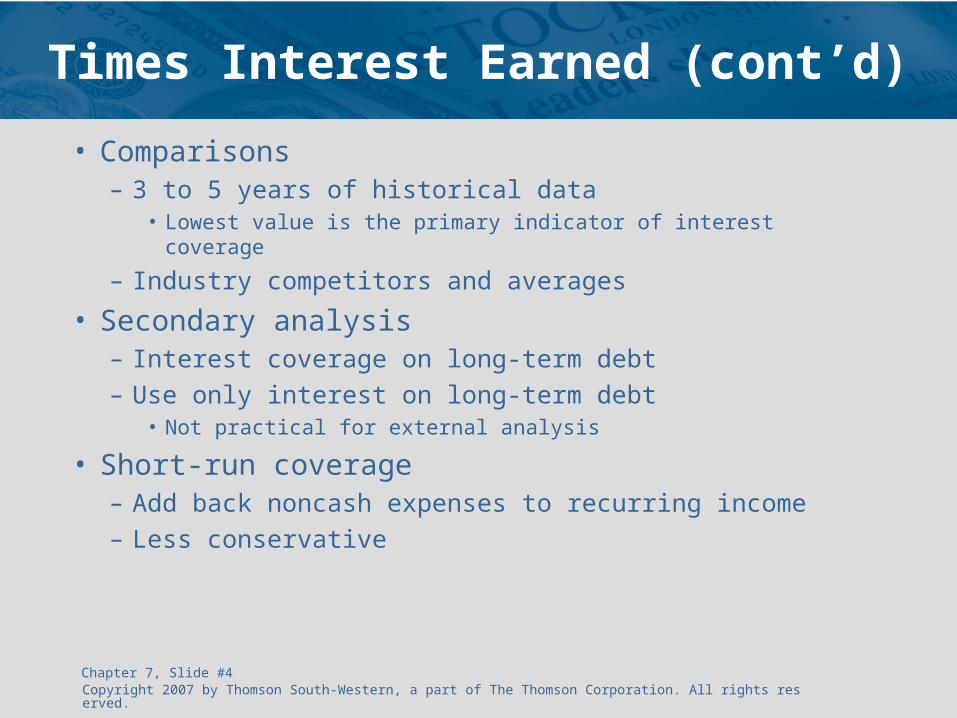

Times Interest Earned (cont’d)

• Comparisons– 3 to 5 years of historical data

• Lowest value is the primary indicator of interest coverage

– Industry competitors and averages

• Secondary analysis– Interest coverage on long-term debt– Use only interest on long-term debt

• Not practical for external analysis

• Short-run coverage– Add back noncash expenses to recurring income– Less conservative

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #5

(Recurring Earnings + Noncash Expenses)Excluding Interest Expense, Tax Expense,

Equity Earnings, and Minority Earnings

Interest Expense, Including Capitalized Interest

Times Interest EarnedShort-Run Variation

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #6

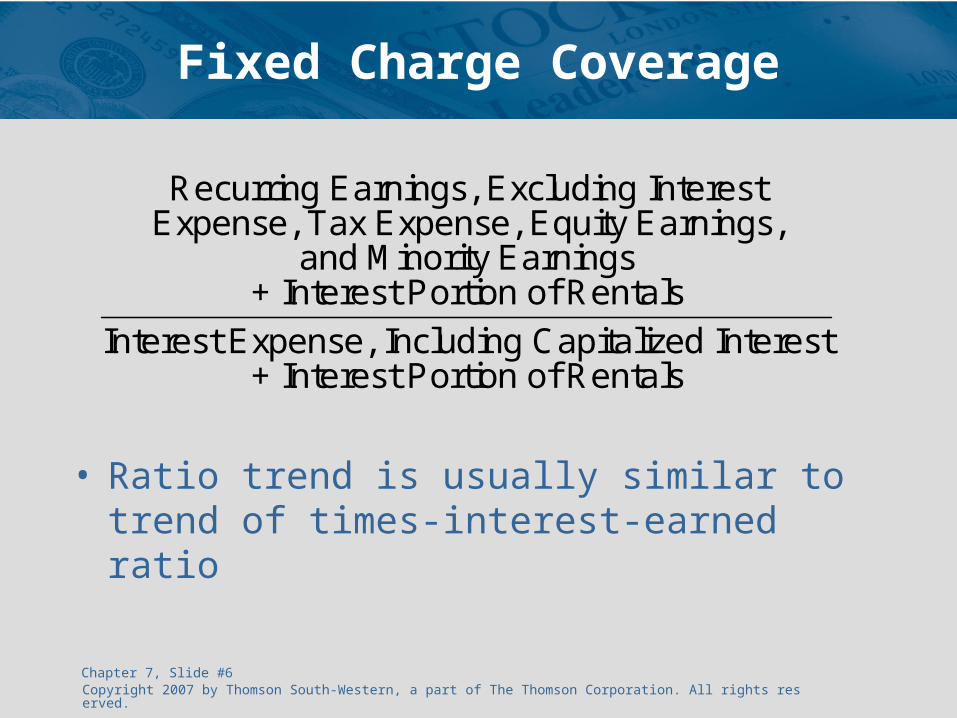

Fixed Charge Coverage

• Ratio trend is usually similar to trend of times-interest-earned ratio

Recurring Earnings, Excluding InterestExpense, Tax Expense, Equity Earnings,

and Minority Earnings+ Interest Portion of Rentals

Interest Expense, Including Capitalized Interest+ Interest Portion of Rentals

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #7

Fixed Charge Coverage (cont’d)

• Fixed charges include– Interest portion of operating lease payments

• General approximation: 1/3 of payments• SEC requires specific calculation using lease terms

– May also include• Depreciation, depletion, and amortization• Debt principal payments• Pension payments• Substantial preferred stock dividends

• The more items included as “fixed charges,” the more conservative the ratio

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #8

Debt Ratio

• Indicates the percentage of assets financed by creditors• Comparisons

– Industry competitors and averages

• Variations in application– Short-term liabilities

• Not part of long-term source of funds: exclude

• Part of the total source of funds: include

– Liabilities that do not necessarily represent a commitment to pay out funds in the future

Total Liabilities

Total Assets

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #9

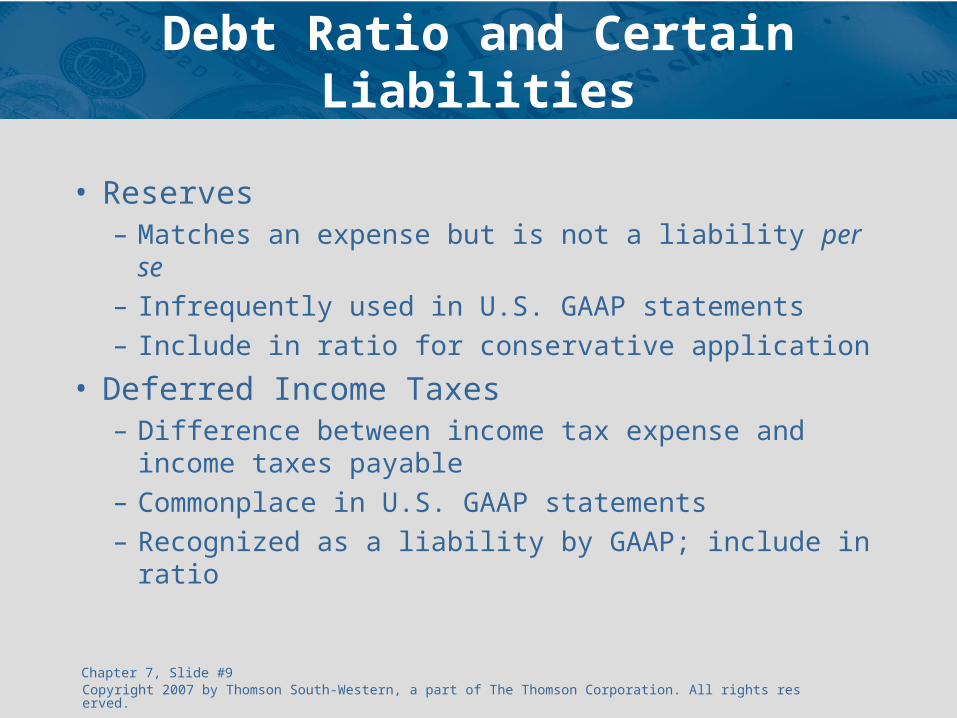

Debt Ratio and Certain Liabilities

• Reserves– Matches an expense but is not a liability per se– Infrequently used in U.S. GAAP statements– Include in ratio for conservative application

• Deferred Income Taxes– Difference between income tax expense and income

taxes payable– Commonplace in U.S. GAAP statements– Recognized as a liability by GAAP; include in ratio

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #10

Debt Ratio and Certain Liabilities (cont’d)

• Minority Shareholders’ Interest– Proportion of a consolidated entity that is not owned

by the controlling parent company– Not a liability per se– Include in ratio for conservative application

• Redeemable Preferred Stock– Exclude from ratio; does not present a normal debt

relationship– Include in ratio for conservative application

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #11

Debt/Equity Ratio

• Helps determine how well creditors are protected in case of insolvency

• Comparisons– Industry competitors and averages

Total Liabilities

Shareholders' Equity

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #12

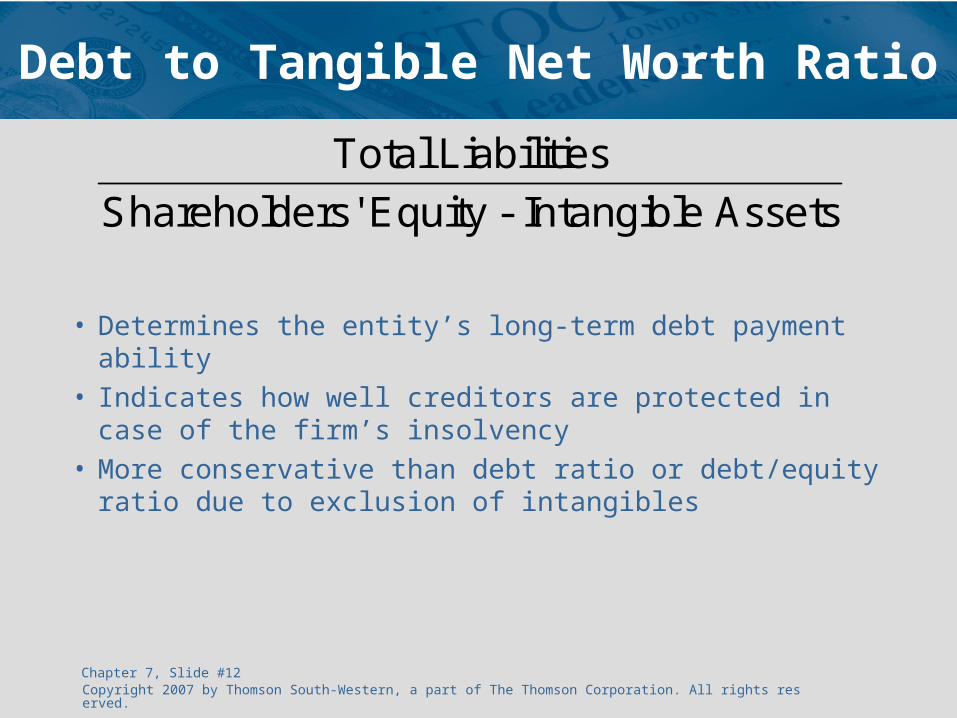

Debt to Tangible Net Worth Ratio

• Determines the entity’s long-term debt payment ability• Indicates how well creditors are protected in case of

the firm’s insolvency• More conservative than debt ratio or debt/equity ratio

due to exclusion of intangibles

Total Liabilities

Shareholders' Equity - Intangible Assets

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #13

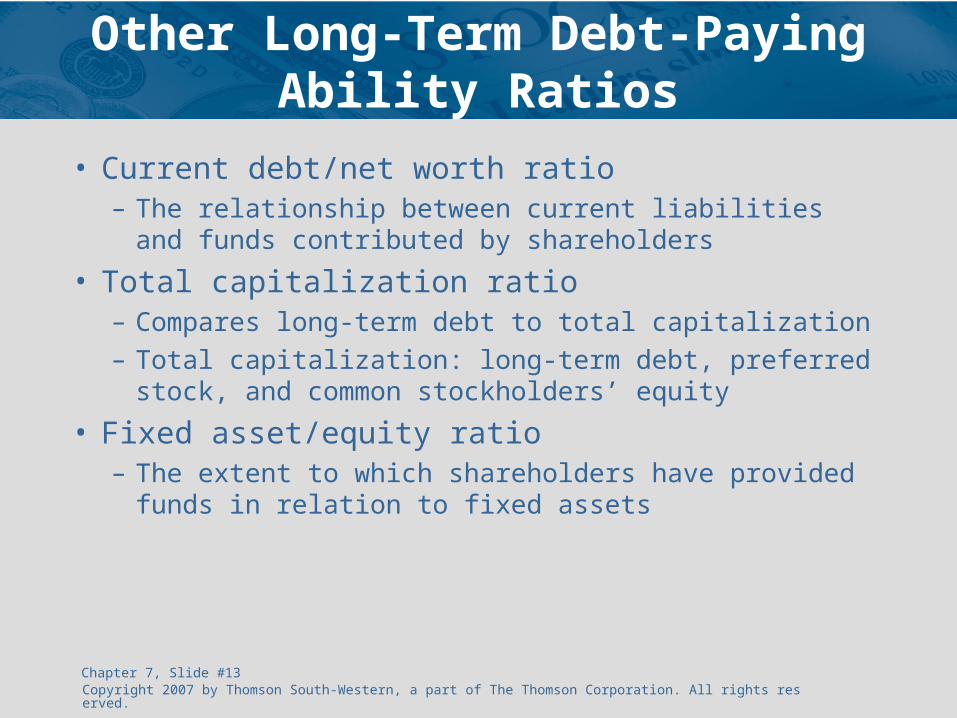

Other Long-Term Debt-Paying Ability Ratios

• Current debt/net worth ratio– The relationship between current liabilities and funds

contributed by shareholders

• Total capitalization ratio– Compares long-term debt to total capitalization– Total capitalization: long-term debt, preferred stock,

and common stockholders’ equity

• Fixed asset/equity ratio– The extent to which shareholders have provided

funds in relation to fixed assets

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #14

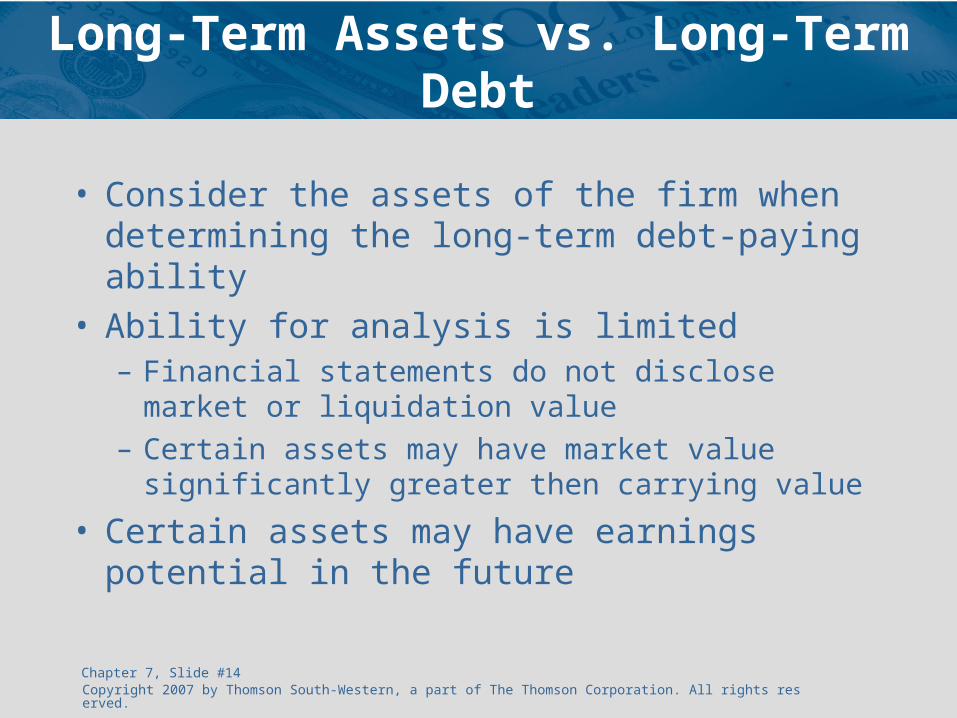

Long-Term Assets vs. Long-Term Debt

• Consider the assets of the firm when determining the long-term debt-paying ability

• Ability for analysis is limited– Financial statements do not disclose market or

liquidation value– Certain assets may have market value significantly

greater then carrying value

• Certain assets may have earnings potential in the future

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #15

Long-Term Leasing

• Capital leases– Asset and liability are reported on the balance sheet

• Operating leases– Reported as expense on the income statement– Supplemental analysis using future payments

• One-third can be estimated as interest• Two-thirds can be added to the fixed assets and long-term

liabilities for debt ratio analyses

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #16

Pension Plans

• Employee Retirement Income Security Act (ERISA)– Includes provisions requiring

• Minimum funding of plans• Minimum rights to employees upon termination of their

employment• Creation of the Pension Benefit Guaranty Corporation

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #17

Defined Contribution Plan

• Contributions to the plan are specified• Employer bears no risk for future growth of

plan• No complex expense or liability issues• 401K is a type of defined contribution plan• Trend analysis

– Compare three years of pension expense in relationship to operating revenue and income before income taxes

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #18

Defined Benefit Plan

• Defines the benefits to be received• Employer must fund sufficiently to achieve

benefit• Note actuarial assumptions inherent in the plan

– Interest (discount) rates– Employee turnover– Mortality rates– Compensation– Pension benefits

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #19

Defined Benefit Plan (cont’d)

• Compare three years of– Pension expense in relationship to operating

revenue and income before income taxes

• Compare benefit obligations to plan assets– Underfunded: a potential liability– Overfunded: potential opportunities to reduce future

pension expense and/or reduce related costs

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #20

Defined Benefit Plan (cont’d)

• Consider employer’s pension-related assumptions and the effect that changes in the assumptions will have on recognized and off-balance-sheet pension accounts– Interest (discount) rate– Rate of compensation increase– Expected return on plan assets

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #21

Postretirement BenefitsOther than Pensions

• Prior to 1993, accrual was not required• Transition costs may be

– Amortized over 20 years or– Expensed in the year of adopting the new

recognition practice

• Analysis is similar to defined benefit pension– Exception: no rate of compensation increase

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #22

Joint Ventures

• An association of two or more businesses established for a special purpose

• Consolidation– Parent firm has control

• Carry as an investment– Parent firm has significant influence

• Analysis– Review footnote for commitments relating to the joint venture– Off-balance sheet commitments represent potential liabilities

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #23

Contingencies

• Loss contingencies that are not accrued are footnoted if it is reasonably possible that an asset has been impaired or a liability has been incurred– Review contingency note for possible liabilities not

disclosed on the balance sheet

• Gain contingencies are not accrued

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #24

Financial Instruments withOff-Balance-Sheet Risk

• Disclosure is required of– Contract face amount– Nature and terms of the instrument– Amount of the potential loss– Entity’s collateral policy and description of the

collateral

• Risk: Potential loss if– The co-party fails to perform– Changes in market make instrument less valuable

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #25

Financial Instruments with Concentrations of Credit Risk

• Disclosure is required of– The extent of risk from exposures to individuals or

groups of counterparties in the same industry or region

• Small companies are particularly susceptible to concentration risk

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 7, Slide #26

Disclosures About Fair Value of Financial Instruments

• Disclosure of financial instrument fair value is required– On-balance sheet assets and liabilities– Off-balance sheet assets and liabilities

• If estimation of fair value is not practicable– Descriptive information pertinent to estimating fair

value is provided