1 cornerstones of managerial accounting, 2e copyright © 2008 thomson south-western, a part of the...

TRANSCRIPT

1

Cornerstones of Managerial Accounting, 2e

Cornerstones of Managerial Accounting, 2e

Copyright © 2008 Thomson South-Western, a part of the Thomson Corporation. Thomson, the Star logo, and South-Western are trademarks used herein under

license.

Mowen/Hansen

Cost BehaviorChapter Three

2

Cost Behavior

The way costs change as the related activity changes

Fixed Cost A cost that does not change in total as output changes

---

3

Cost Behavior

The way costs change as the related activity changes

Variable Cost Increases in total with an increase in output and decreases in total with a decrease in output

---

4

Measures of Output

“What causes the cost of this particular activity to go up (or down)?”

To determine if a cost is fixed or variable, we must first determine the underlying business activity and ask ourselves….

In other words, we are trying to identify its driver.

5

Relevant Range

The range of output over which the assumed cost relationship is valid for the normal

operations of a firm.

Let’s take a closer look at fixed, variable and mixed

costs in light of the relevant range.

• Avoids extremely high levels of activity• Avoids extremely low levels of activity

6

Fixed Costs

Costs that in total are constant within the relevant range as the level of output increases or decreases.

7

Example

• It process up to 50,000 computers per year. • The production-line manager (supervisor) is paid

$32,000 per year.• The company was established 5 years ago.• Currently the factory produces 40,000 – 50,000

computers per year. • Production has never fallen below 20,000

computers in a year.

Colley Computers Inc. wants to look at the cost relationship between supervision cost and the number of computers processed.

Let’s look at the cost of supervision at several

production levels.

8

# of Computers Produced

20,000

30,000

40,000

50,000

Total Cost of Supervision

$32,000

$32,000

$32,000

$32,000We know the total cost of supervision, but what about per computer?

Unit Cost

Example

9

# of Computers Produced

20,000

30,000

40,000

50,000

Total Cost of Supervision

$32,000

$32,000

$32,000

$32,000

Unit Cost

Example

$1.60

1.07

0.80

0.64Unit cost changes! As production increases, the per

unit amount of a fixed cost decreases.

10

Discretionary Fixed Costs

Fixed costs that can be changed relatively easily at management

discretion

11

Committed Fixed Costs

A fixed cost that cannot be easily changed. Often these involve a long-

term contract

12

Variable Costs

Costs that in total vary in direct proportion to changes in output within

the relevant range

13

Variable Cost Behavior Example

• Each computer requires one DVD-ROM drive costing $40.

• The cost of DVD-ROM drives for various levels of production is as follows:

Expanding our Colley Computers example….

Let’s look at the cost of DVD-ROM’s at several

production levels.

14

# of Computers Produced

20,000

30,000

40,000

50,000

Total Cost of DVD-ROM Drives

$800,000

$1,200,000

$1,600,000

$2,000,000

Unit Cost

We know the total cost increases as production

increases. But what about the cost per computer?

Variable Cost Behavior Example

15

# of Computers Produced

20,000

30,000

40,000

50,000

Total Cost of DVD-ROM Drives

$800,000

$1,200,000

$1,600,000

$2,000,000

Unit Cost

Example:

$40

40

40

40Unit Cost stays the same! The per unit variable cost of DVD-ROM drives is always

$40 per computer.

16

Total Variable Cost

Variable Rate

x Amount of Output=

Variable Cost Relationship

Let’s look at the DVD-ROM costs for 50,000 computers.

17

Total Variable Cost

Variable Rate

x Amount of Output=

50,000 computers

$40 per computer x=$2,000,000

Variable Cost Relationship

18

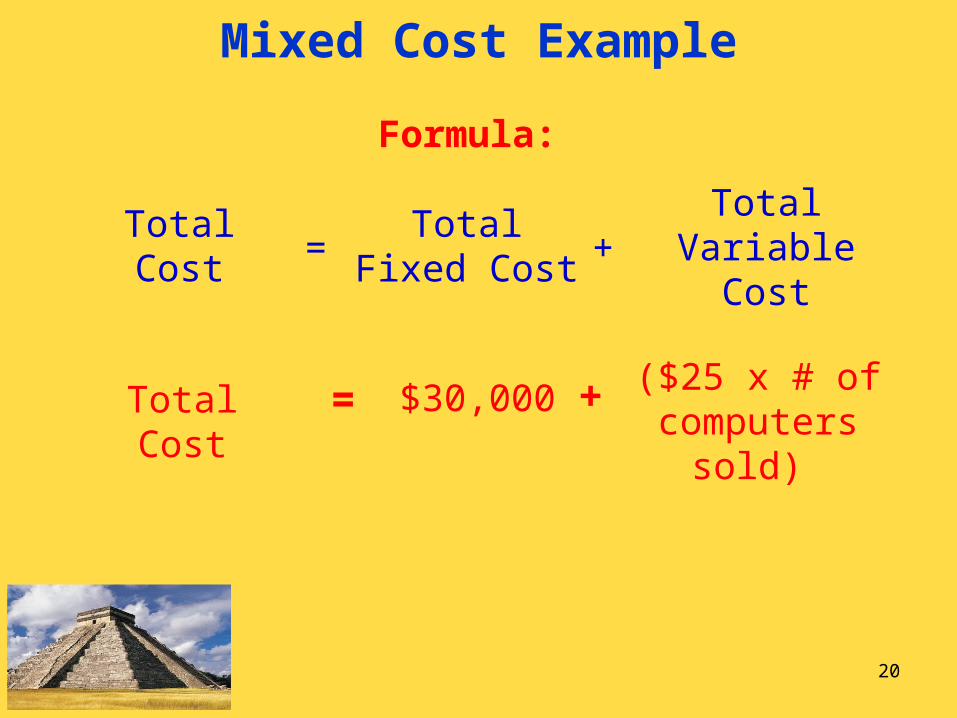

Mixed Costs

Costs that have both a fixed and a variable component.

Formula:

Total Cost =Total Fixed

Cost+

Total Variable Cost

Let’s look at an example from the Colley Computers

19

Example:

Colley Computers has 10 sales representatives.

Let’s plug this into our mixed cost formula.

• Each earns a salary of $30,000 per year.• And a commission of $25 per computer sold.• Each sales rep sells up to 50,000 computers

per year.

20

Mixed Cost Example

Formula:

Total Cost =Total Fixed

Cost+

Total Variable Cost

($25 x # of computers sold)

$30,000 +=Total Cost

21

Step Costs

Displays a constant level of cost for a range of output and then jumps to a

higher level of cost at some point, where it remains for a similar range of output

22

Separating Costs

Accounting records typically show only the total cost and the associated amount of

activity of a mixed cost item.

Therefore, it is necessary to separate the total cost into its fixed and variable

components.

How do we separate the costs?

23

1.High-Low method

2.Scattergraph method

3.Method of Least Squares

Separating Costs

Three methods:

24

Dependent Variable in the Cost Formula

Total Cost

= Total Fixed Cost

+ Total Variable Cost

Variable Rate x OutputTotal Cost

= Total Fixed Cost

+ Variable Rate

x Output

Dependent Variable

25

Dependent Variable

A variable whose value depends on the value of another variable

26

Independent Variable in the Cost Formula

Total Cost

= Total Fixed Cost

+ Total Variable Cost

Total Cost

= Total Fixed Cost

+ Variable Rate

x Output

Independent Variable

27

Independent Variable

A variable that measures output and explains changes in the cost

28

Intercept

Graphically, the intercept is the point at which the cost line intercepts the cost

(vertical) axis

Intercept

29

Intercept in the Cost Formula

Total Cost

= Total Fixed Cost

+ Total Variable Cost

Total Cost

= Total Fixed Cost

+ Variable Rate

x Output

Intercept

30

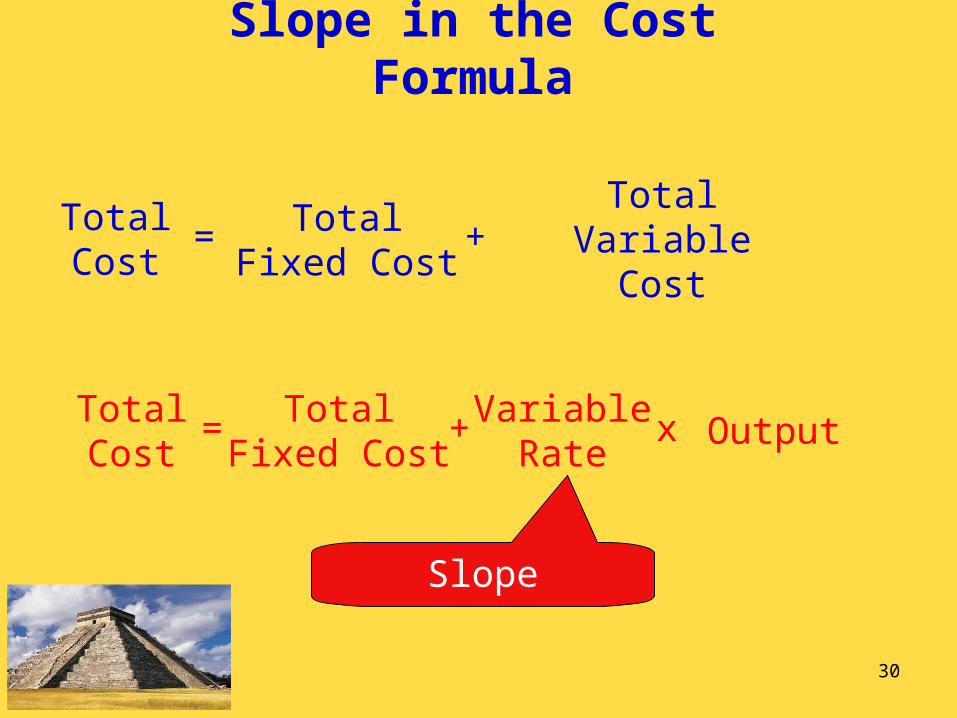

Slope in the Cost Formula

Total Cost

= Total Fixed Cost

+ Total Variable Cost

Total Cost

= Total Fixed Cost

+ Variable Rate

x Output

Slope

31

Slope

Corresponds to the variable rate (the variable cost per unit of output). It is

the slope of the cost line.

Let’s work through an example.

32

High-Low Method

A method of separating mixed costs into fixed and variable components by using just the high and low data points

Step #1 Find the high point and low point.

33

High-Low Method

Step #2 Using the high and low points, calculate the variable rate.

Variable rate =High point cost – Low point cost

High point output – Low point output

34

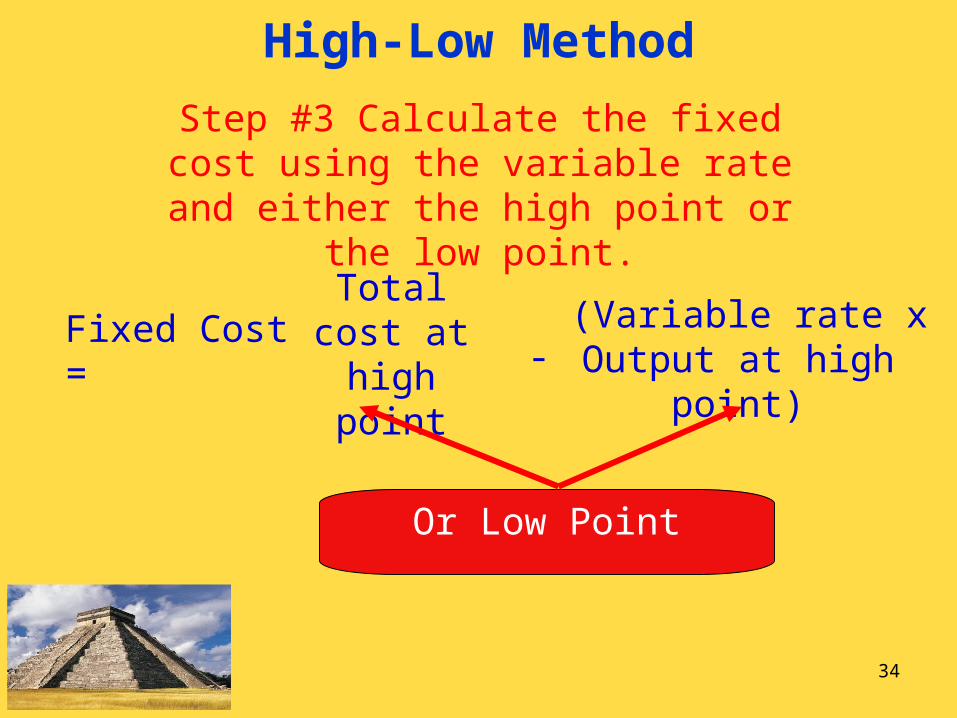

High-Low Method

Step #3 Calculate the fixed cost using the variable rate and either the high point or

the low point.

Fixed Cost = Total cost at high point

(Variable rate x Output at high point)

-

Or Low Point

35

High-Low Method

Step #4 Form the cost formula based on the high-low method.

Cornerstone 3-2 will walk us through an example of the

High-Low Method

36

Scattergraph Method

Purpose of this method:• To see whether or not a straight line

reasonably describes the cost relationship

• To reveal one or more points that do not seem to fit the general pattern of behavior

37

Scattergraph Method

Applying the method:• Draw a graph with units on the x-axis

and cost on the y-axis• Plot the data points on the graph• Visually fit a line to the data points on

the graph.• The intercept is the fixed cost.• Use the high-low method to determine

the variable rate.

38

Scattergraph Method

Disadvantage:

Lack of any objective criterion for choosing the best-fitting line.

We need a method that is objective and produces the

best-fitting line.

39

Method of Least Squares

A statistical way to find the best-fitting line through a set of data points.

What does best-fitting mean?

The line is one in which the data points are closer to the line than to any other line.

40

Method of Least Squares

▪▪▪

▪▪

▪ ▪▪

Measure distance from points to line.

Then square the differences. Add up

all the squared differences.

41

Method of Least Squares

Spreadsheet programs have packages to calculate the best-fitting line (called

regression line).

42

Managerial Judgment

Instead of the three methods previously discussed, many managers simply use their experience and past observation of cost relationships to

determine fixed and variable costs.

The appeal of this method is its simplicity.

43

Managerial Judgment with Estimation

Managers may use experience and judgment to refine statistical estimation

results.

Statistical techniques are highly accurate in depicting

the past, but they cannot foresee the future.