long term care trends in the united states choices for independence summit lisa alecxih vice...

TRANSCRIPT

Long Term Care Trendsin the United States

Choices for Independence SummitLisa Alecxih

Vice President

December 5, 2006

Posted 12/8/06

2

Overview

Review of the Basics

Major Trends Demographics Delivery Financing

Implications for the Future

3

What is Long Term Care?

Services and supports needed when one’s ability to care for self has been reduced by a chronic illness, disability, or frailty.

Services usually provided: by family and friends at home through home and community-based services, such

as home health care, personal care, and adult day services

in institutional settings, such as nursing homes or residential care facilities

4

Who Might Need Long Term Services and Supports?

1.1% 1.6% 2.2% 3.7% 4.8% 6.5% 9.7%15.0%

27.1%

43.2%

66.7%

80.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

18-2

9

30-3

9

40-4

9

50-5

9

60-6

4

65-6

9

70-7

4

75-7

9

80-8

4

85-8

9

90-9

4

95+

Age

% o

f In

div

idu

als

wit

h a

Dis

abil

ity

Source: 1999 National Long Term Care Survey and the 1994 National Health Interview Survey Disability Supplement.

5

Most Seniors with Disabilities Supported by Unpaid Care in the Community

Source: 1999 National Long Term Care Survey, 2002 Medicare Current Beneficiary Survey, and 2005 CMS Minimum Data Set.

Alternative Residential

NursingFacility

Community

Community Paid Only

Community Unpaid Only

Community Paid and Unpaid

8%

21% 71%

25%

42%

4%

6

Who Uses Any Paid Services?

14.2%

7.5%

17.4%

31.3%

Source: 2003 Medical Expenditure Panel Survey, 2002 Medicare Current Beneficiary Survey, and 2005 CMS Minimum Data Set.

3.3% 3.5%

11.5%

5.9%

9.6%

6.2%

12.7%

14.0%

1.0%

1.3%1.3%

0.3%0%

5%

10%

15%

20%

25%

30%

35%

Age 65+ 65-74 75-84 85+

Per

cen

t U

sin

g P

aid

LT

C

Nursing Facilities Alternative Residential Paid HCBS

7

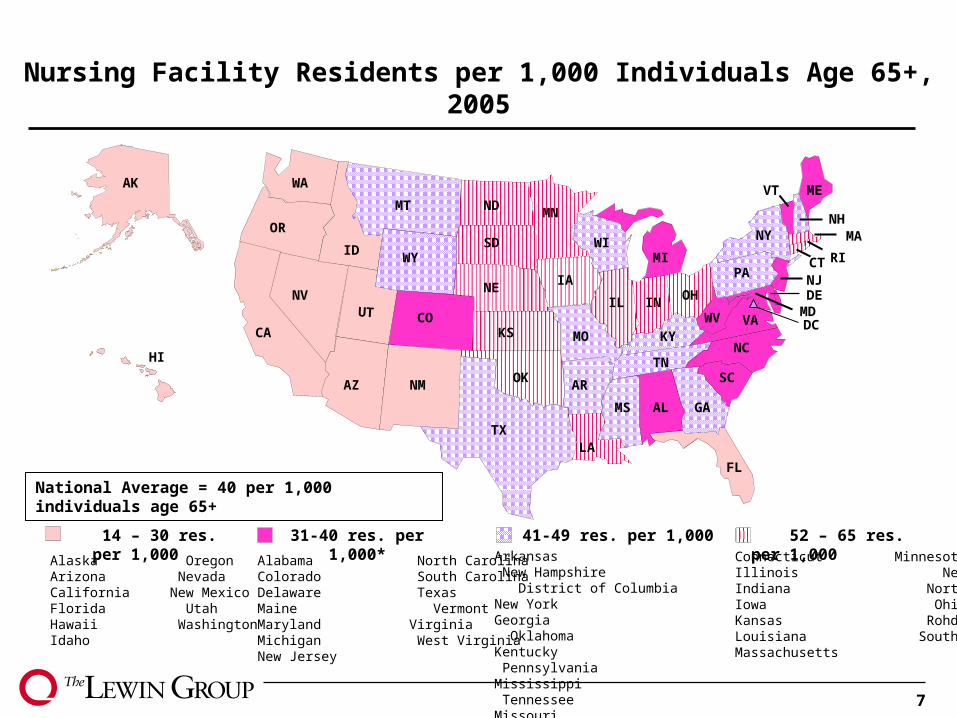

31-40 res. per 1,000* 14 – 30 res. per 1,000 41-49 res. per 1,000Connecticut MinnesotaIllinois NebraskaIndiana North DakotaIowa Ohio Kansas Rohde IslandLouisiana South Dakota Massachusetts

Alabama North CarolinaColorado South CarolinaDelaware TexasMaine Vermont Maryland VirginiaMichigan West VirginiaNew Jersey

Alaska OregonArizona Nevada California New MexicoFlorida UtahHawaii WashingtonIdaho

Nursing Facility Residents per 1,000 Individuals Age 65+, 2005

Arkansas New Hampshire District of Columbia New York Georgia Oklahoma Kentucky PennsylvaniaMississippi Tennessee Missouri WisconsinMontana Wyoming

52 – 65 res. per 1,000

HI

AK

MT

ID

WA

CO

WY

NV

CA

NMAZ

MN

KS

TX

IA

WI

IL

KY

TN

INOH

MI

ALMS

AR

LA

GA

FL

SC

WV VA

NC

MDDE

PANJ

VT

RI

ME

NHOR

UT

SD

ND

MO

OK

NE

NY

CT

DC

MA

National Average = 40 per 1,000 individuals age 65+

8

How Much Does Long Term Care Cost?

Nursing Home Care Average annual cost -- $74,095 $41,975 in Shreveport, Louisiana to $193,815 in Alaska

Assisted Living Average annual cost -- $34,860 $19,740 in Jackson, MS to $55,548 in Boston, MA

Home Care Average rate for home health aide -- $19/hour $12/hr in Shreveport, LA to $26/hr in Colorado Springs,

Co Average rate for homemaker/companion -- $17/hour $12/hr in Shreveport, LA to $23/hr in Minneapolis/St.

Paul, MNSource: The MetLife Market Survey of Nursing Home & Home Care Costs in 2005 and Assisted Living in 2005 which

includes private pay rates and services provided by home health agencies.

9

Medicare Covers Limited LTC Benefits Primarily post-acute care Home health services

Beneficiaries who are homebound Need part-time skilled nursing or therapy services,

and Under the care of a physician 27 visits per user on average in 2005

Skilled nursing facility care Up to 100 days for those recently discharged from a

hospital 35 days covered on average in 2005

10

Eligibility Criteria Among LTC Users Makes Medicaid the Payer of Last Resort

Pathway Income EligibilityAsset Limit

Individual/Couple

Mandatory Population

SSI Cash Assistance < 74% of poverty(SSI income eligibility)

$2,000$3,000

Optional Populations

Medically Needy* Spend income down to a specified level ($100-$825; $416 on average)

$2,000$3,000

Poverty Level < 100% of poverty $2,000$3,000

Special Income Rule for Nursing Home Residents

Income < 300% of the SSI level (1,809/month)

$2,000Spousal Impoverishment

HCBS Waivers Income up to 300% SSI level (37 states);

8 states at poverty level; some states allow spousal impoverishment

$2,000$3,000 or Spousal Impoverishment

*Medicaid benefits may be more limited than for SSI.

11

HCBS 20-32%* HCBS 35-54% HCBS 10-19% Alabama ConnecticutDelaware DCFlorida Georgia Indiana KentuckyMaryland Mississippi New Hampshire North DakotaPennsylvania South Dakota Tennessee Utah

Arkansas KansasMaine MassachusettsMissouri MontanaNevada New Jersey New York Oklahoma Vermont Virginia

Alaska CaliforniaIdaho MinnesotaNew Mexico North CarolinaOregon TexasWashington Wisconsin

Percent HCBS of Medicaid LTC Among Aged/Disabled, 2005

Colorado HawaiiIllinois IowaLouisiana MichiganNebraska OhioRhode Island South CarolinaWest Virginia Wyoming

HCBS <10%

National Average = 22.9%

HI

AK

MT

ID

WA

CO

WY

NV

CA

NMAZ

MN

KS

TX

IA

WI

IL

KY

TN

INOH

MI

ALMS

AR

LA

GA

FL

SC

WV VA

NC

MDDE

PANJ

VT

RI

ME

NHOR

UT

SD

ND

MO

OK

NE

NY

CT

DC

MA

12

Out-of-Pocket Covers A Significant Portion Some individuals pay for LTC on their own

Those who qualify for Medicaid also pay out-of-pocket Nursing facility residents with Medicaid financing contribute

all of their income with the exception of a personal needs allowance ($30-$100/month)

– On average, Medicaid nursing facility residents contribute 20% of their cost

Many states also require cost-sharing for their HCBS waiver

Medicaid rules protect the primary residence while the individual or their spouse is alive

– OBRA ’93 mandated estate recovery

– In 2003, states recovered a total of $347.4 million – on average 0.5% of Medicaid LTC costs, however, Oregon recovered 2.2% (AARP, 2005)

13

Long Term Care Insurance (LTCI) Plays a Limited Role LTCI market emerged during the 1980s 9.2 million total policies sold through 2002 However, only approximately 10 percent of those

age 65+ own LTCI policies because of: Complicated and expensive policies -- $1,337 to $2,862 at age

65 Consumer lack of awareness and denial of need Most policies must be “sold” by agents

Limited benefit payouts Early policies offered limited benefits – nursing home only and

often no inflation protection Benefits based on daily amount purchased and may not cover

full cost of care Many people lapse their policy prior to benefits

Source: American Health Insurance Plans (AHIP) (2004) Long Term Care Insurance in 2002 for number of policies sold and average premium.

14

LTC Sources of Financing Among Seniors

Medcaid38%

Medicare20%

Other Public3%

LTCI3%

Family Resources

36%

Source: The Lewin Group based on the Long Term Care Financing Model.

Total in 2005 =$140.8B

15

Major U.S. Long Term Care System Trends

Demographics

Delivery

Financing

Demographic Trends

17

Disability Rates Declined Between 3.0 and 6.5 percentage points or 10.5 to 25 percent

12.2%

29.1%

62.0%

9.2%

23.4%

55.5%

0%

10%

20%

30%

40%

50%

60%

70%

65-74 75-85 85+Pe

rce

nt

of

Ag

e G

rou

p w

ith

Dis

ab

ilit

y

1984

1989

1994

1999

Disability Rates Among Individuals Age 65 and Over by Age

Source: Brenda C. Spillman (2003) Changes in Elderly Disability Rates and the Implications for Health Care Utilization and Cost for the Office of the Assistant Secretary for Planning and Evaluation at http://aspe.hhs.gov/daltcp/reports/hcutlcst.htm.

18

Poverty Rates Among Oldest Old Declined by More Than 1/3rd

8.9

13.4

21.2

10.9

17.4

12.4

10.1

14.6

7

9

11

13

15

17

19

21

23

Perc

en

t o

f In

div

idu

als

with

Inco

me

Belo

w P

overt

y T

hre

sh

old

85+ 75-84 65-74 65 or Older

Elderly Poverty Rates Over Time

Source: Current Population Survey, Annual Supplement, 1983-2006.

19

Dip in Childless Women & Spike in Average Number of Children Among Mothers

Source: Bureau of the Census data..

Status at Age 40-44 and Year When Age 85-89

0%

5%

10%

15%

20%

25%

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

0.00.51.01.52.02.53.03.54.04.5

Percent Childless

Women

Average # of Children

Among those with

Children

Delivery Trends

21

Significant Declines in the Use of Nursing Facilities Among Oldest Old

Source: 1973-4, 1997, 1985, 1995, 1997, 1999 and 2004 National Nursing Home Survey.

3.8%

1.1%

5.0%

21.1%

3.6%

0.9%

3.6%

13.9%

0%

5%

10%

15%

20%

25%

65+ 65-74 75-84 85+

Pe

rce

nt

of

Po

pu

lati

on

Wh

o A

reR

es

ide

nts

of

Nu

rsin

g F

ac

ilit

ies

1973-74

1977

1985

1995

1997

1999

2004

22

Much of Decline From Growth in Alternative Residential Settings

Source: 1985 and 2004 National Nursing Home Survey and 2002 Medicare Current Beneficiary Survey.

13.9%

4.1%

0.9%

4.9%

0.3%0.2%

0%

5%

10%

15%

20%

25%

65-74

Alt. Residential - Community

Alt. Residential - Facility

Certified Nursing Home

2004

18.8%

22.9%

1.4%

5.9%

3.6%

1.2%1.1%

75-84 85+

4.7%

1.0%

5.2%

21.1%

1.8%

0.6%

0.2%0%

5%

10%

15%

20%

25%

65-74 75-84 85+

Non-Certified Nursing Home

Certified Nursing Home

1985

1.2%

5.8%

22.9%

Financing Trends

24

Medicaid LTC Devoted to HCBS for Aged and Disabled Grew Significantly Since 2000

11.1%11.9%

13.0%

14.6%

19.0%18.0%

17.0%

14.3%13.7%

11.8%11.1%

20.6%

12.3%

22.6%

10%

12%

14%

16%

18%

20%

22%

24%

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005P

rop

ort

ion

of

Med

icai

d L

TC

Sp

end

ing

for

HC

BS

Am

on

g A

ged

an

d D

isab

led

Source: 2005 MedStat LTC Data, Lewin Analysis. Long term care includes nursing facility, state plan personal care and home and community-based waivers for the aged and disabled.

25

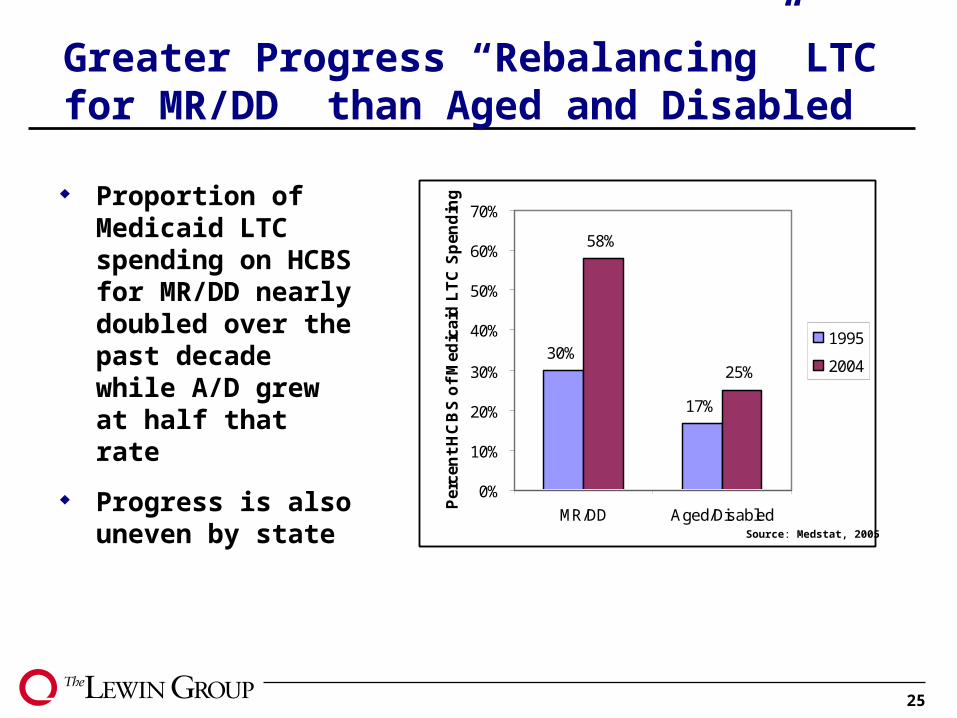

Greater Progress “Rebalancing” LTC for MR/DD than Aged and Disabled

30%

17%

58%

25%

0%

10%

20%

30%

40%

50%

60%

70%

MR/DD Aged/DisabledPer

cen

t H

CB

S o

f M

edic

aid

LT

C S

pen

din

g

1995

2004

Proportion of Medicaid LTC spending on HCBS for MR/DD nearly doubled over the past decade while A/D grew at half that rate

Progress is also uneven by state Source: Medstat, 2005

26

Change in Per Capita Medicaid Nursing Facility Residents, 1995-2005

HI

AK

MT

ID

WA

CO

WY

NV

CA

NMAZ

MN

KS

TX

IA

WI

IL

KY

TN

INOH

MI

ALMS

AR

LA

GA

FL

SC

WV VA

NC

MDDE

PANJ

VT

RI

ME

NHOR

UT

SD

ND

MO

OK

NE

NY

CT

DC

MA

National Average = 15.2% Decline

20% to 30% Decline 30% or More Decline 10% to 20% Decline

Alabama Mississippi District of Columbia New JerseyFlorida New YorkHawaii OhioIowa PennsylvaniaKentucky South CarolinaMichigan West Virginia

Alaska Washington Maine UtahOregon

Arizona Massachusetts California Missouri Connecticut NebraskaDelaware New Hampshire Idaho North CarolinaIllinois North DakotaKansas Rhode IslandMaryland South Dakota

Less than 10% Decline

Arkansas New MexicoColorado OklahomaGeorgia TennesseeIndiana TexasLouisiana VermontMinnesota VirginiaMontana WisconsinNevada Wyoming

27

A few well established programs and numerous start-ups.

Top Managed Care Programs:

Arizona – 42,125 lives (8/2006)New York – 16,224 lives (4/2006)Florida – 13,600 lives (8/2006)Wisconsin – 12,545 lives (8/2006)

Remaining Programs:

Massachusetts – 3,700 lives (2/2006)Texas – 3,300 lives (4/2006)Minnesota – 2,100 lives (1/2006)California -- unknown

New Programs:

Kentucky HawaiiIdaho MarylandNew Mexico North CarolinaSouth Carolina WashingtonVermont

Active & Pending Programs

Potential Expansions/Pilots

LTC Programs

Many States Looking to Managed Long Term Care to Rebalance Medicaid

28

Implications of Financing System

Financing silos and institutional bias of Medicaid eligibility make rebalancing difficult

Olmstead Decision and President’s New Freedom Initiative focus on individual choice and shifting the balance

Lack of insurance to spread risk means individuals responsible for paying for much of their care

Medicaid managed care re-emerging as states seek to eliminate institutional bias, improve service provision, and control costs May stand in contrast to consumer direction movement

Preparing for the Future

30

Aging of Baby Boomers Will More than Double the Number of Older Adults Age 65+ with Disabilities

0

2

4

6

8

10

12

14

16

1996

-00

2000

-04

2005

-09

2010

-14

2015

-19

2020

-24

2025

-29

2030

-34

2035

-39

2040

-44

2045

-49

Nu

mb

er o

f E

lder

ly w

ith

Dis

abili

ties

(i

n m

illio

ns)

2+ ADLs

1 ADL

IADL Only

Source: The Lewin Group based on the Long Term Care Financing Model.

31

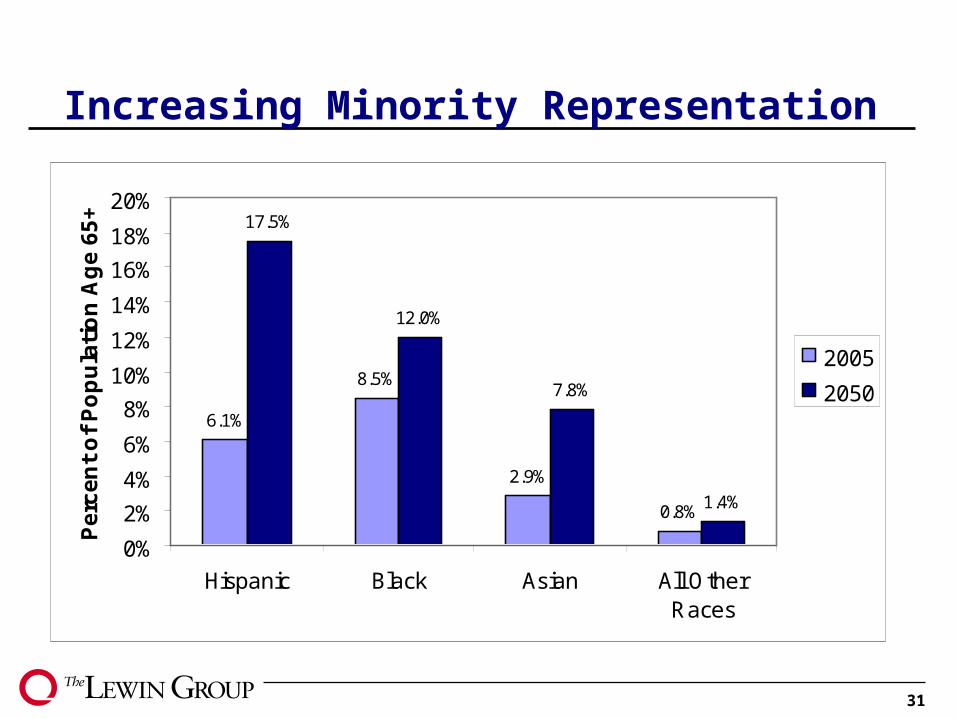

Increasing Minority Representation

6.1%

8.5%

2.9%

0.8%

17.5%

12.0%

7.8%

1.4%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Hispanic Black Asian All OtherRaces

Pe

rce

nt

of

Po

pu

lati

on

Ag

e 6

5+

2005

2050

32

Remaining Lifetime Use of LTC by People Turning 65 in 2005

Type of CareAverage Years of

Care% of People Using

Type of Care

All LTC need 3.0 69

At home

Informal care only 1.4 59

Formal care 0.5 42

Any care at home 1.9 65

In facilities

Nursing facilities 0.8 35

Assisted living 0.3 13

Any care in facilities 1.1 37Source: Kemper, Komisar & Alecxih; Inquiry; Vol. 42, Winter 2005/2006.

33

While Most Could Save Enough, Over 25% Face Expenses Over $100,000 2000 median net worth among elderly was

$110,000, but only $25,000 excluding home equity

Average lifetime per capita at age 65 =

$47,000

Distribution of Lifetime Expenditures After Age 65

No expenditures

(family and friendssupport)

42%

$1-$9,999

19%

$10,000-$24,999

8%

$25,000- $99,999

5%

$100,000+

Source: Kemper, Komisar & Alecxih; Inquiry; Vol. 42, Winter 2005/2006.

26%

34

Few Americans Plan Ahead for LTC Needs

Less than 10% of those age 65+ own a long term care insurance policy

Long term care insurance policies can be expensive and may be unaffordable for many middle-income Americans.

Baby boomers had children later than any previous generation and worry more about college tuition than financing future LTC needs

Older adults own nearly $3 trillion in home equity, yet few take advantage of methods to tap this resource.

35

Lifestyle Choices Affect Nursing Home Use

Source: Valiyeva E, et al. Lifestyle-Related Risk Factors and Risk of Future Nursing Home Admission. Archives of Internal Medicine. 2006; 166:985-90. May 8, 2006.

Relative Risk for Nursing Home Admission Over the Next 20 Years at Age 45-64

1.001.35

1.89

3.25

4.55

0.0

1.0

2.0

3.0

4.0

5.0

Normal BloodPressure

High BP High BP +inactivity

Diabetic Diabetic +inactive

36

Conclusions Consumers need trusted and reliable information

about their options to make informed decision Expect support options to continue to evolve:

Respond to market demand Role of technology States interests in lower cost alternatives

Encouraging purchase at younger ages would be the most effective policy for increasing the role of LTC insurance.

Standardizing the reverse mortgage process could promote the use and/or access to assistance for care planning when using personal assets.