london central residential: a class apart its potential as a viable asset class in a diversified...

TRANSCRIPT

London Central Residential:London Central Residential:A class apart A class apart

Its potential as a viable asset class in a diversified portfolioIts potential as a viable asset class in a diversified portfolio

London Central Portfolio LimitedLondon Central Portfolio Limited

Who are LCP?Who are LCP?

What is London Central?What is London Central?

What makes it an attractive asset class? What makes it an attractive asset class?

How has it performed vs. other asset classes?How has it performed vs. other asset classes?

The impact of the credit crunchThe impact of the credit crunch

What now – possible scenariosWhat now – possible scenarios

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

For 20 years LCP have approached London Central as an alternative asset class

LCP do not LCP do not SELLSELL residential real estate but enable investors to residential real estate but enable investors to maximise their profit opportunity through sound business modelling maximise their profit opportunity through sound business modelling

Offering a full service solution: property finding, refurbishment and furnishing, letting and rental management

Launched the only two closed end residential funds targeting London Central

Based on financial criteria(income/expenditure and return targets)

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

Who are LCP?Who are LCP?

International market with low correlation to the UKInternational market with low correlation to the UK

Only 440,000 people in 6 square miles

What is London Central…What is London Central…

The Royal Borough of Kensington & Chelsea

City of Westminster

Just 2 boroughs out of 33

Average price almost £1 million

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

Prime London Central Prime London Central

The The bullseyebullseye of the capital of the capital

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

Globally desirable: the best real estate in the world…

International centre: geography, culture, finance, education

Scarcity of stock (215,000 units)

Lack of new supply (500 new units per annum)

What makes London Central an What makes London Central an attractive investment class?attractive investment class?

Low transaction levels (Ave. sales p.m. 600, 3.4% turnover p.a.)

High levels of rental occupancy (97%)

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

Average price is 1/4 of London Central (£230,562)

...and Docklands & Canary Wharf...and Docklands & Canary Wharf

30,000 units developed since 2000: oversupply of rental units

42 major developments approved ’08/’09 vs 17 in London Central

Differentiated from the rest of the UKDifferentiated from the rest of the UK

More impacted by Credit Crunch

Average price 1/3 of London Central

Affected by domestic factors: unemployment & mortgage availability

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

““The Simplified Map of London”The Simplified Map of London”Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

How has London Central performed?How has London Central performed?

““Past performance is not a guide to the Past performance is not a guide to the future”future”

““Lies, damned lies and statistics”Lies, damned lies and statistics”

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

A Strong PerformerA Strong Performer

Capital values have increased more than 12 fold since 1980, 4 times in real terms

Representing 8.7% compound growth and a doubling of values Representing 8.7% compound growth and a doubling of values approximately every 8 yearsapproximately every 8 years

Capital growth in London residential (1980 = 100) Capital growth in London residential (1980 = 100)

London Capital GrowthIndex = 1,292

RPIIndex = 312

Source: CML/ODPM/Office for Communities & Local Government/Office of National Statistics/LCP In-house

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

A Competitive PerformerA Competitive PerformerDemonstrates significantly less volatility and outperforms UK

commercial property and the UK stock market

Source: HM Land Registry, IPD, Reuters, LCP In house research

Comparative performance 1970 = 100Comparative performance 1970 = 100

UK Commercial Capital Growth Index = 506

FTSE 100 Index = 1,646

London Central Residential Capital GrowthIndex = 5,069

UK CommercialTotal Return Index = 5,532

London Central Residential Total ReturnIndex = 7,132

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

A Consistent PerformerA Consistent Performer

IRR over 10 year period (total return)IRR over 10 year period (total return)

Despite adverse conditions (1989 and the credit crunch) a 10 year hold has always shown real growth

Source: CML/ODPM/Office for Communities & Local Government/Office of National Statistics/LCP In-house

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

10 year IRR shows a spread of 5-12%.

Investment returns can be further enhancedInvestment returns can be further enhanced

Every case differs & you should seek specialist tax adviceEvery case differs & you should seek specialist tax advice

Net residential yields allow 60-70% gearing

Income tax mitigation

CGT exemption for non-res and non-doms

Inheritance tax mitigation through offshore holding vehicles

Significantly increasing returns over an 8 year period

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

The impact of the credit crunchThe impact of the credit crunch

London Central has shown a resilient performanceLondon Central has shown a resilient performance

Sector % Drop Peak to Trough % Change peak to date

London Central - 15% +3%

FTSE 100 - 47.75% -27%

UK commercial - 40% -22%(total return)

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

Source: HM Land Registry, IPD, Reuters, LCP In house research

What has underpinned London Central’s resilience? What has underpinned London Central’s resilience?

Desire for transparency: retrenchment into tangible assets

Opportunistic buying

Belief in long term desirability & longevity

High dependence on international vs domestic economy (investors & tenants)

Diversification

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

Weakness in sterling increased affordabilityWeakness in sterling increased affordabilityLondon Central pricing relative to different currenciesLondon Central pricing relative to different currencies

London Central Residential Capital Growth

Exchange RateUS$ : £

26% Drop from Peak

Exchange RateSingapore $ : £

28% Drop From Peak

Exchange RateMYR : £

28% Drop From Peak

Source: HM Land Registry (RBKC &CoW)/xrates.com

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

Reduced borrowing costs increased accessibility Reduced borrowing costs increased accessibility

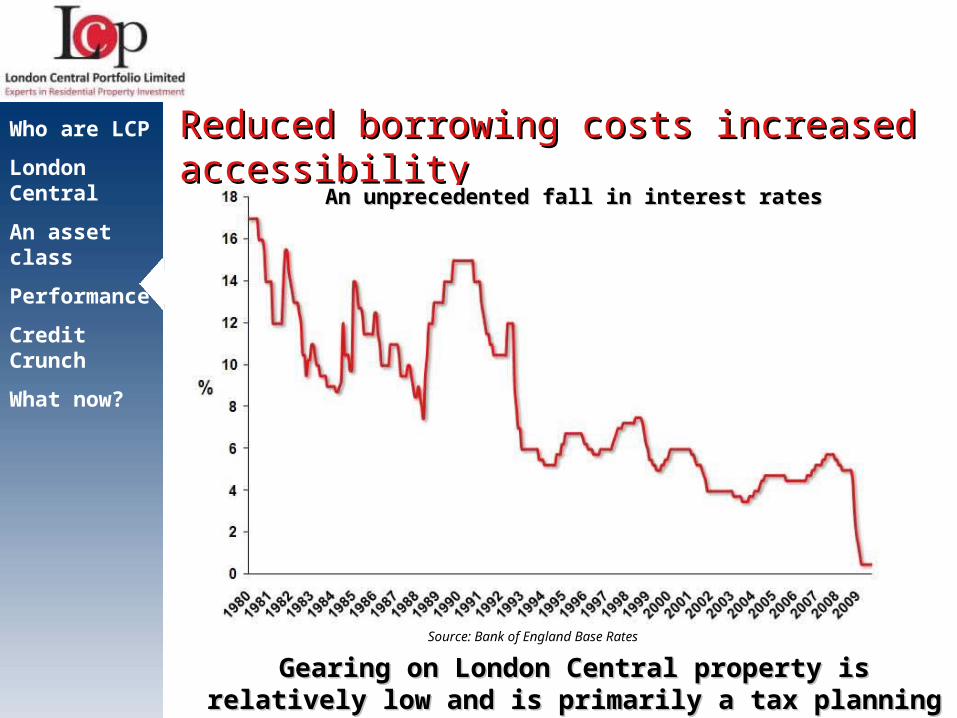

Source: Bank of England Base Rates

An unprecedented fall in interest ratesAn unprecedented fall in interest rates

Gearing on London Central property is relatively low and is Gearing on London Central property is relatively low and is primarily a tax planning mechanism primarily a tax planning mechanism

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

Press reporting on UK property market should be handled with care…Press reporting on UK property market should be handled with care…

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

What now? – Possible scenarios What now? – Possible scenarios

Factors affecting London Central performance Factors affecting London Central performance differ from the UK differ from the UK

Different price trends London Central vs England & WalesDifferent price trends London Central vs England & Wales 2003 = 1002003 = 100

Source: HM Land Registry HPI (RBKC &CoW)

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

Continued weak UK economy (low interest rates/weak sterling):Incentivises the foreign investor

High levels of inflation: historically reflected in property prices

Increase in base rates: already factored in at about 4% for 5 year fix

London loses its allure: not convincing (10m HNW, $39 trillion)

Lack of buyers leads to major price reductions: evidence suggests a floor to price falls

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

Despite risk of double-dip or triple-tumble, past Despite risk of double-dip or triple-tumble, past performance is probably our best predictorperformance is probably our best predictor

Major falls in transactional activity result in limited Major falls in transactional activity result in limited falls in pricesfalls in prices

Transaction falls peak to trough vs price falls Transaction falls peak to trough vs price falls

Source: HM Land Registry (RBKC &CoW)

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

Source: CML/ODPM/Office for Communities & Local Government/LCP In-house. Assumes 7.5% day 1 uplift and 3.5% net rental yield

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

Historic data shows lowest 10yr IRR at 3%, Historic data shows lowest 10yr IRR at 3%, average capital growth at 8.7%average capital growth at 8.7%

Capital Appreciation OnlyUngeared 3% Ave. Cap.App.

3.8% IRR & 44.5% RoE

Total ReturnUngeared 3% Ave. Cap.App.

6.6% IRR & 88.9% RoE

Capital Appreciation OnlyGeared (60% LTV) 3% Ave. Cap.App.

7.8% IRR & 111.2% RoE

Capital Appreciation OnlyUngeared 8.5% Ave. Cap.App.

9.3% IRR & 143.1% RoE

Total ReturnUngeared 8.5% Ave. Cap.App.

11.8% IRR & 203.6% RoE

Capital Appreciation OnlyGeared (60% LTV) 8.5% Ave. Cap.App.

16.4% IRR & 357.6% RoE

Using these as downside and upside parameters projections, Using these as downside and upside parameters projections, un-geared and geared growth can be assessedun-geared and geared growth can be assessed

SummarySummary

Shown robust performance outperforming conventional asset classes

Potential spread of returns makes London Central a strong candidate Potential spread of returns makes London Central a strong candidate for inclusion in a balanced portfoliofor inclusion in a balanced portfolio

London Central is a unique market benefiting from:

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?

Scarcity of stock

Increasing global demand

Consistent returns

Upside potential due to inherent market desirability

Downside possibility due to uncertain economic future

10 year ungeared IRR shows a spread of 5%-12%, ave. growth 8.7%

Who are LCP

London Central

An asset class

Performance

Credit Crunch

What now?