lesson 10 gst on import & export business li, jialong 2011-2-26

Post on 20-Dec-2015

226 views

TRANSCRIPT

Lesson 10

GST on Import & Export Business

Li, Jialong

2011-2-26

GST on Exports

WHAT ARE THE RULES FOR GST-FREE EXPORTS?

If you export goods from Australia within 60 days of issuing an invoice or receiving some payment, the export will be GST-free.

For further information on GST on Exports please read the PDF file GST on Exports.

GST on Imports

Goods and services tax (GST) is payable on most goods imported into Australia.

GST is payable by businesses, organisations and private individuals, whether they are registered for GST or not. However, if you are a GST-registered business or organisation and you import goods as part of your activities, you may be able to claim a GST credit for any GST you pay on those goods.

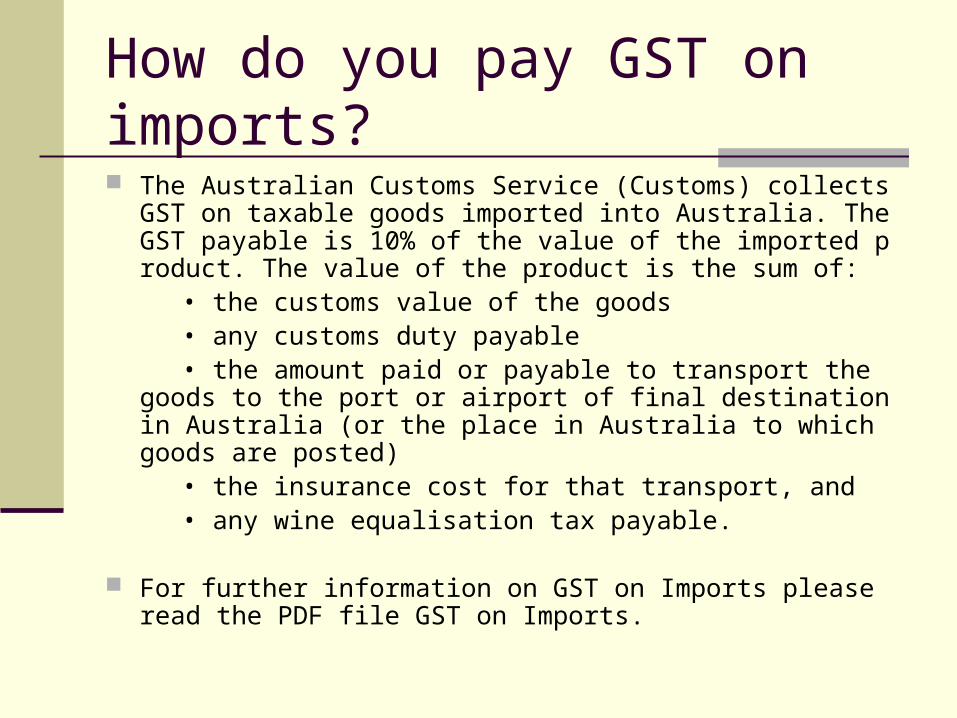

How do you pay GST on imports?

The Australian Customs Service (Customs) collects GST on taxable goods imported into Australia. The GST payable is 10% of the value of the imported product. The value of the product is the sum of:

• the customs value of the goods • any customs duty payable • the amount paid or payable to transport the goods to the port o

r airport of final destination in Australia (or the place in Australia to which goods are posted)

• the insurance cost for that transport, and • any wine equalisation tax payable.

For further information on GST on Imports please read the PDF file GST on Imports.

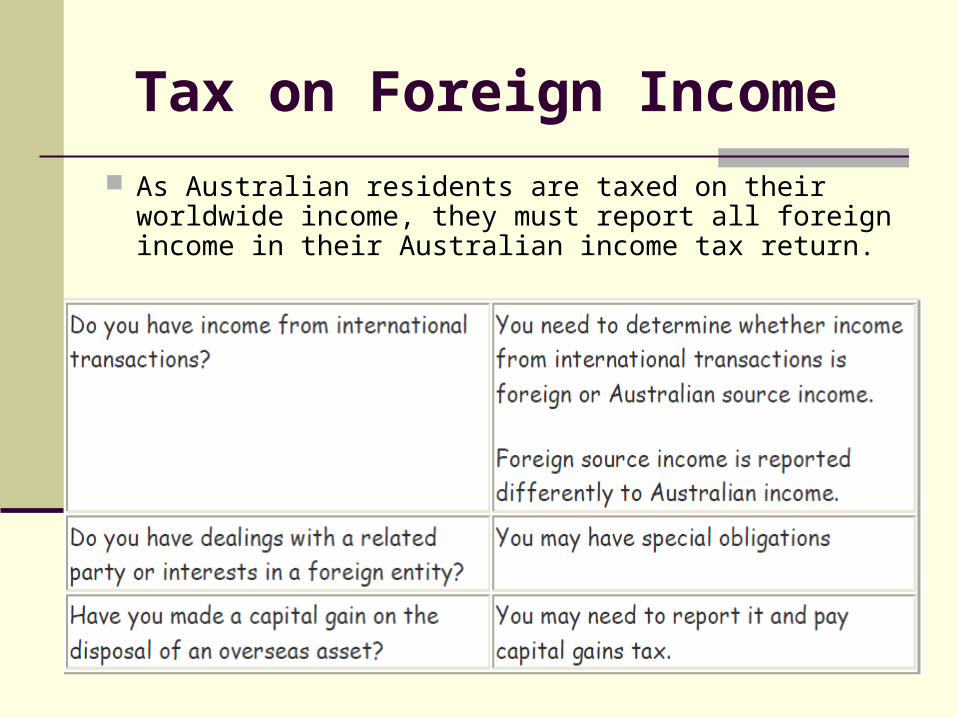

Tax on Foreign Income

As Australian residents are taxed on their worldwide income, they must report all foreign income in their Australian income tax return.

Reporting income from international transactions

If you have assessable income from overseas, you must declare it in your Australian income tax return.

You must also report foreign income that is exempt from Australian tax, as it may be taken into account to work out the amount of tax you have to pay on your assessable income, both Australian and foreign.

Before you calculate your net income, all foreign income, deductions and foreign tax paid must be converted to Australian dollars.

For more information on foreign income tax offset rules refer to Guide to foreign income tax offset rule

Foreign tax offset credit

If you have paid foreign tax in another country, you may be entitled to an Australian foreign income tax offset, which provides relief from double taxation.

These rules apply for income years that start on or after 1 July 2008. Different rules apply for income periods up to 30 June 2008 (refer to How to claim a foreign tax credit, NAT 2338).

You can claim a tax offset for the foreign tax you have paid on income, profits or gains (including gains of a capital nature), that are included in your Australian assessable income. In some circumstances, the offset is subject to a limit.

To be entitled to a foreign income tax offset:

• you must have actually paid an amount of foreign income tax. The income or gain on which you paid foreign income tax must be included in your assessable income for Australian income tax purposes.

Differences between the Australian and foreign tax systems may lead to you paying foreign income tax in a different income year from that in which the income or gain is included in your assessable income for Australian income tax purposes. You could have paid the foreign tax in an earlier or later income year. However, the offset can only be claimed after the foreign tax is paid.

The foreign income tax offset applies to foreign income tax imposed on all forms of income, profits and gains, (including gains of a capital nature) and to all taxpayers, whether individuals or other entity types.

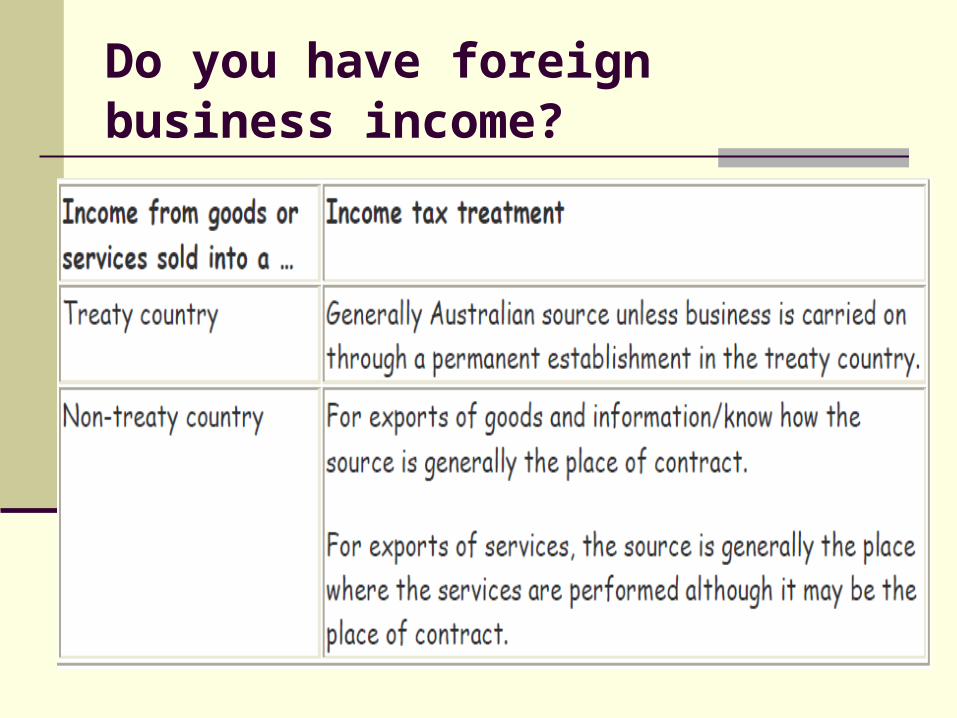

Do you have foreign business income?

To determine the tax treatment of income from international transactions, you must first determine the source of the income. This may depend on whether the transaction involves a country that has a tax treaty with Australia. Currently, Australia has tax treaties with more than 40 countries including all our major trade and investment partners.

Do you have foreign business income?

Do you have foreign business income?

A permanent establishment is a fixed place of business through which the business of an enterprise is wholly or partly carried on. It includes a sales outlet, a branch, place of management, a factory, a workshop, an office or a dependent agent (who has authority to enter into contracts on behalf of the enterprise and habitually exercises that authority). Generally, having a website that is hosted by an independent internet service provider in another country is not regarded as having a permanent establishment in that country.

Do you have foreign business income?

If you operate a subsidiary in another country, different arrangements may apply. A subsidiary incorporated overseas is treated as a foreign resident for the purposes of Australian tax law. Generally, a foreign-resident subsidiary will not be treated as constituting a permanent establishment of its Australian parent company.

Do you have foreign business income?

Australia has entered into taxation agreements with more than 40 countries. Tax treaties, which are also referred to as tax conventions or double tax agreements (DTA). They prevent double taxation and fiscal evasion and foster cooperation between Australia and other international tax authorities by enforcing their respective tax laws. You will only be affected by a tax treaty if you are a resident of Australia or the other treaty country.

Countries that have a tax treaty with Australia are contained in this table.

Countries that have a tax treaty with Australia

ArgentinaItalySlovakiaAustriaJapanSouth AfricaBelgiumKiribatiSouth KoreaCanadaMalaysiaSpainChinaMalta

Norway

Thailand

France

Papua New Guinea

United Kingdom

Germany

Philippines

United States

Hungary

Poland

Sri Lanka

Czech Republic

Mexico

Sweden

Denmark

Netherlands

Switzerland

Fiji

New Zealand

Taipei

Finland

Vietnam

India

Romania

Indonesia

Russia

Ireland

Singapore

Translation of overseas income and expenditure into Aust$ Translation (conversion) to Australian dollars – foreign curr

ency exchange rates to use All foreign income, deductions and foreign tax paid must be tran

slated (converted) to Australian dollars before including it in your return. From 1 July 2003, there are specific rules which tell you which exchange rate to use to convert these amounts. Generally, these require amounts to be converted at the exchange rate prevailing at the time of a transaction, or at an average rate. If you would like further information on the conversion rules, refer to the Tax Office publications:

• Foreign exchange (forex): the general translation rule, and • Foreign exchange (forex): general information on average rate

s

What is the general translation rule?

Translation is often referred to as ‘conversion’. In this fact sheet, the word ‘translation’ is used.

New legislation – ‘the general translation rule’ – applies to the translation of foreign income, expenses, and other tax-relevant amounts to Australian dollars. Generally speaking, the legislation applies from 1 July 2003.

Under the general translation rule, all tax-relevant amounts must be translated into Australian currency (unless falling within certain limited exceptions). This enables all gains and losses to be calculated using a common unit of measurement.

Tax-relevant amounts

Examples of tax-relevant amounts include an amount of:

• ordinary income • an expense • an obligation • a liability • a receipt • a payment • consideration, and • a value.

Tax-relevant amounts

These amounts may be on revenue account, capital account, or otherwise.

The general translation rule applies regardless of whether the foreign income is remitted to Australia or not. One significant change from the law as it applied before the operation of these measures is that foreign currency denominated liabilities on capital account are translated into Australian dollars (on a realisation basis) without the need for actual conversion into Australian currency.

Review Questions

GST on Exports

GST on Imports

Income Tax and international income

Tax treaties with other countries

Exercises

Build your skills of

Lesson 11 and Assessment 3

Assessment task 1 due

Reading and Resources

Student Notes Lesson 9-10

The End of Lesson 10