lesson 2 rules of accounting and financial reports li, jialong 2011-2-26

Post on 22-Dec-2015

217 views

TRANSCRIPT

Lesson 2 Rules of Accounting and

Financial Reports

Li, Jialong

2011-2-26

The need for financial reporting

• Information for the business operations

• Financial Management

• Social and environmental responsibility

• Corporate Governance

• Ethics

Financial Statements

What are the common ones?

• Income Statements

• Balance sheets

• Statement of Changes in Equity

• Cash Flow Statement

How often are Financial Statements

Prepared and what are the reporting periods?

• Annually

• Financial year normally 1 July to the following 30 June.

• Monthly, quarterly and six monthly are also prepared usually for internal users

Income Statement

• The Income Statement summarises the Revenue and expenses (running Costs) of your business operation for a given period

Income Statement

Revenue – Expenses = Profit/ (Loss) REVENUE Revenue or income is the earnings made fro

m the operations of the business; it mainly comes from sales, which the business makes.

EXPENSES Expense or cost is what is incurred or spent in making the sales and in running the business.

PROFIT/LOSS: If the total sales revenue is greater than the total expenses then the business makes a profit, which is added to the Owners Equity in the Balance Sheet.

If the total sales revenue is less than the total expenses then the business has made a loss, which is reported on the Balance Sheet in the Owners Equity.

The Balance Sheet

Definition: The Balance Sheet is a report which shows in statement form the relationship between Assets, Liabilities and Owners Equity at a point in time.

Statement of Changes in Equity

This Report shows the change in the amount owed to the owners of the business and how it has changed for a period

Cash Flow Statement

The Cash Flow Statement summarises the flow of CASH ONLY (not credit transactions) through the business for a given period of time

Samples

A Sample of the four financial Statements are below taken from the Australian Accounting Standards AASB no 101 which outlines the accounting standards for the financial reports completed by businesses. There are also international accounting standards that must be complied with when reporting for a business.

Income Statement Example

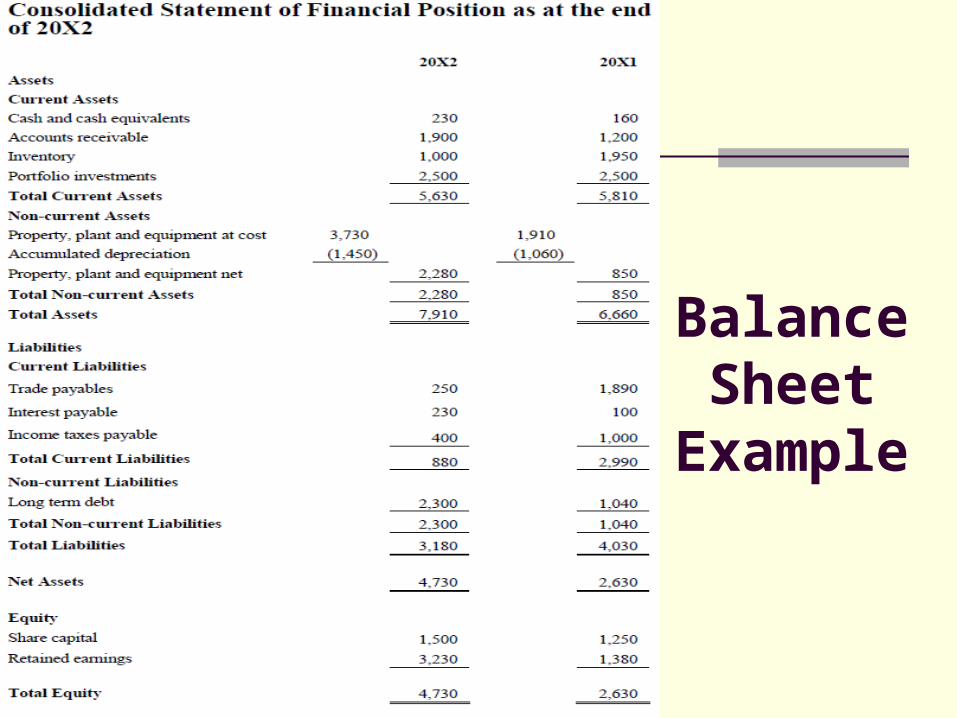

Balance Sheet

Example

Cash Flow Statement Example

Statement of Changes in Equity

Summary of Financial Statements

Items What to tell?Time

descriptionMetaphor

Investment ways

Balance sheet Lists of assets, liabilities, and owner’s equity

Specific date (end of a month or a year)

A snapshot

A pool with some water

Entrepreneur

Income statement Summary of the

revenues and expenses

Specific period (a month or a year)

A moving picture

Change of water amount in the pool

Shareholder or stockholder

Statement of cash flows

State of inflow and outflow of cash

Specific period (a month or a year)

Intake and outlet of the water

Loaner or lender

Statement of owner’s equity

Summary of changes in owner’s equity

Specific period (a month or a year)

The money get or made from the water

Opportunistic stockholder

Assets

These are items of value owned by the business. Examples are cars, cash, stock/inventory, accounts receivable and furniture and fittings.

An item may be an asset of the business even if the business has not paid for it. For example the business may have borrowed money from the bank to buy a motor vehicle. The accounting records show the motor vehicle as an asset.

Liabilities

These are the amounts of money OWED to others. Examples include accounts Payable, bank overdrafts, and mortgage loans. The money owed on the motor vehicle asset is recorded as a liability. Liability is another name for debt owed to anyone other than the owner of the business.

Owners Equity

This is the amount of money required by the OWNER of the business to invest in the business for it to be established and maintained. In large public companies it is the money from shareholders. It is increased when the owners contribute more funds to the business. This is called Capital.

It is reduced when the owner takes funds out of the business. This is called Drawings or dividends.

Revenue

A retail business normally earns revenue from selling its stock/inventory which has been specifically purchased for resale (Purchases). The total of the daily sales is the revenue for the day.

A service industry earns revenue from selling services, e.g. haircuts.

The other types of revenue that can be earned by a business include interest on cash in the bank, rental income, commissions, etc.

Revenue can be earned in cash or on the promise to pay at a later date (credit sales).

Not all money received is earned by a business. For example when a business receives money from a bank as a loan and when a debt is repaid (credit sale payment) and other loans lent by the business are repaid.

Expenses

A business incurs expenses as a result of supplying goods or services to a customer. For instance wages must be paid; there are bills for electricity, rates, telephone and taxes to be paid. These result in some spending of the money (cash payments) that was received from revenue (sales).

Accountants also recognise expenses that are not cash payments. Under an accrual-based accounting system, expenses are recognised when they are incurred. For example, depreciation of plant and equipment is recognised every year over the life of the asset as the asset deteriorates or erodes in value.

Some cash payments that aren’t expenses would include making loan repayments and the purchase of an asset e.g. motor car.

Chart of Accounts

Ledger accounts are used in the accounting system to summarise transactions. For instance, Cash at bank ledger account records all cash receipt and cash payments.

The chart of accounts is an index of ledger accounts designed to assist you to find a particular account. It is a listing that shows the arrangement of the accounts in the ledger and the number assigned to each account. Accounts of the same type are arranged together. For example all the assets are numbers 1xxx.

EXAMPLE OF CHART

OF ACCOUNTS

(Accounts

List)

Users of accounting information

Internal Users • Owners

• Managers • Employees

Internal users may ask the following questions from the financial information:

• .IS CASH SUFFICIENT TO PAY YOUR DEBTS? • What is the cost of manufacturing each unit of

product? • Can we afford to give employees pay raises this year? • Which product line is the most profitable?

Users of accounting information External Users

Investors Employees Contributors Members Tax payers ( Government businesses) Creditors (Suppliers of trading goods Lenders Recipients of Goods and Services Donors Resource Providers

Parties performing a review or oversight function

Parliaments state and federal Regulatory agencies Employer groups Media Special interest group Governments Trade unions Analysts

BUSINESS STRUCTURES

Sole Trader Partnerships Joint Ventures Company Cooperative Incorporated Association Trust

Sole Proprietorship

Advantages Simple to establish Owner controlled

Disadvantages Unlimited liability Limited cash Ability to expand is limited

Partnership

Advantages Simple to establish Shared control Broader skills and resources

Disadvantages All partners are legally bound to each other Unlimited liability

Company

Advantages

Easier to transfer ownership

Easier to raise funds

No personal liability

Proprietary Pty Ltd Limits ownership

Disadvantages

Under company law there are substantial reporting requirements.

Lack of personal decision making

Trusts

If you operate your business as a trust, you’re:

a trustee

responsible for holding property or income for

the benefit of others (the beneficiaries). The most common variety of trust is the discretionary

trust. If you’re the trustee of a discretionary trust,

you have the power to decide how the profit will be

distributed among the beneficiaries.

Trusts

Advantages A trust has a limited liability if the trust is a company. A trust has perpetual existence and does not cease with the death of a beneficiary. Increased asset protection. Things to consider Like a company, a trust is more expensive and potentially complicated to establish. It may be more expensive to complete the required tax and administrative paperwork each year. Profits distributed to children under 18 may be taxed at higher rates.

Review Questions

What are Financial Reports? Who uses financial reports? What information is contained in the Financial

Reports? Definitions of Assets, Liabilities, Owners

Equity, Revenue and Expenses. Types of Business Structures Discuss the advantages and disadvantages

of business structures

Exercises

Exercise 2.1 Put the following accounts for a Beauty Salon into a

chart of accounts organising the assets, liabilities, owner’s equity, revenue and expenses into sections and numbering the accounts to provide an index.

Exercise 2.2 In groups choose a business and develop a chart of

accounts for that business and explain the accounts that you have chosen to the class.

Exercise 2.3 Identify each of the following items as an asset, a

liability, owner’s equity, revenue or an expense. Use the letters A, L OE R or E

Reading and Resources

Choosing the right business structure (BUSINE_1)

Student Notes and Readings Lesson 2

The End of Lesson 2