kaiser medicaid commission on - kaiser family foundation ... · the state treasury via an igt. in...

TRANSCRIPT

February 2005

Medicaid Financing Issues: Intergovernmental Transfers and Fiscal Integrity

IGTs made by localities from their own tax revenues to help fund a state’s Medicaid program are a legal way for a state to pay its share of Medicaid spending. States use of intergovernmental transfers have been a part of the program since 1965.

Since its enactment in 1965, Medicaid has been a joint financing partnership between the states and the federal government. While each state administers its own Medicaid program within broad federal guidelines, the federal government provides over half of the program’s financing. As a result, Medicaid is both a federal and state budget item, and it is also the single largest source of federal revenue to the states. This shared financing structure, provides a guarantee of federal matching funds for state expenditures for health and long-term care services for our nation’s low-income population.

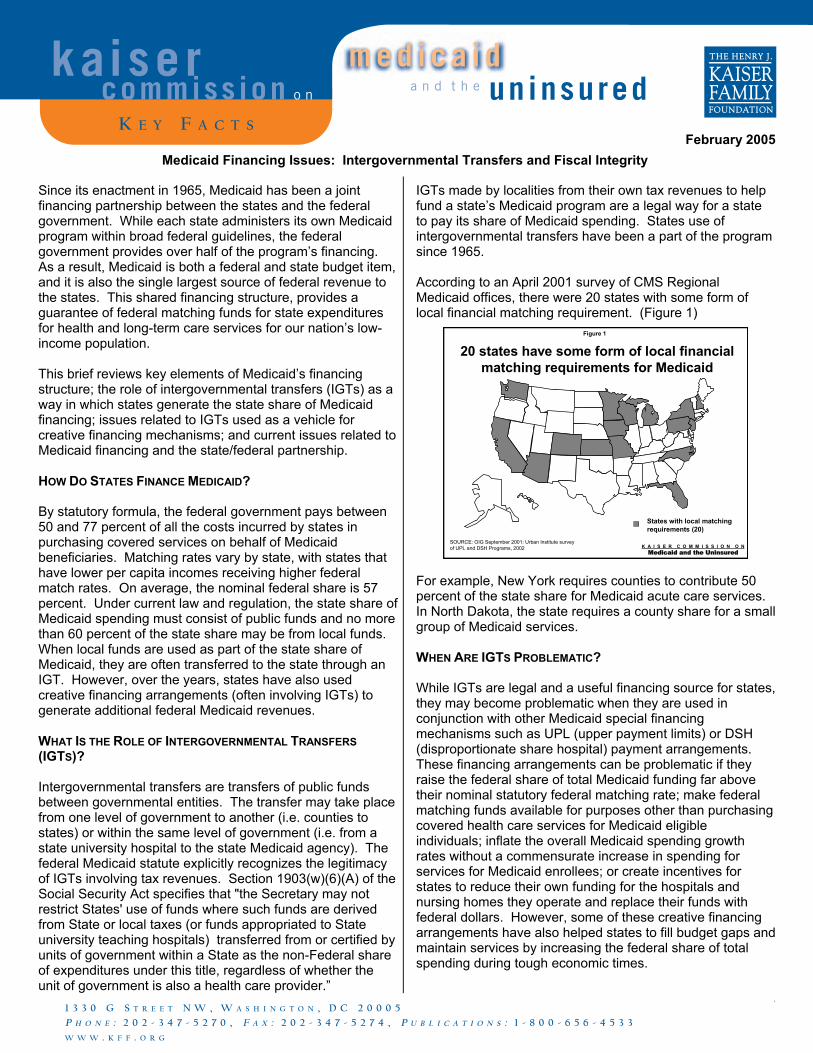

According to an April 2001 survey of CMS Regional Medicaid offices, there were 20 states with some form of local financial matching requirement. (Figure 1)

Figure 1

K A I S E R C O M M I S S I O N O NMedicaid and the Uninsured

20 states have some form of local financial matching requirements for Medicaid

SOURCE: OIG September 2001: Urban Institute survey of UPL and DSH Programs, 2002

States with local matching requirements (20)

This brief reviews key elements of Medicaid’s financing structure; the role of intergovernmental transfers (IGTs) as a way in which states generate the state share of Medicaid financing; issues related to IGTs used as a vehicle for creative financing mechanisms; and current issues related to Medicaid financing and the state/federal partnership. HOW DO STATES FINANCE MEDICAID? By statutory formula, the federal government pays between 50 and 77 percent of all the costs incurred by states in purchasing covered services on behalf of Medicaid beneficiaries. Matching rates vary by state, with states that have lower per capita incomes receiving higher federal match rates. On average, the nominal federal share is 57 percent. Under current law and regulation, the state share of Medicaid spending must consist of public funds and no more than 60 percent of the state share may be from local funds. When local funds are used as part of the state share of Medicaid, they are often transferred to the state through an IGT. However, over the years, states have also used creative financing arrangements (often involving IGTs) to generate additional federal Medicaid revenues.

For example, New York requires counties to contribute 50 percent of the state share for Medicaid acute care services. In North Dakota, the state requires a county share for a small group of Medicaid services. WHEN ARE IGTS PROBLEMATIC? While IGTs are legal and a useful financing source for states, they may become problematic when they are used in conjunction with other Medicaid special financing mechanisms such as UPL (upper payment limits) or DSH (disproportionate share hospital) payment arrangements. These financing arrangements can be problematic if they raise the federal share of total Medicaid funding far above their nominal statutory federal matching rate; make federal matching funds available for purposes other than purchasing covered health care services for Medicaid eligible individuals; inflate the overall Medicaid spending growth rates without a commensurate increase in spending for services for Medicaid enrollees; or create incentives for states to reduce their own funding for the hospitals and nursing homes they operate and replace their funds with federal dollars. However, some of these creative financing arrangements have also helped states to fill budget gaps and maintain services by increasing the federal share of total spending during tough economic times.

WHAT IS THE ROLE OF INTERGOVERNMENTAL TRANSFERS (IGTS)? Intergovernmental transfers are transfers of public funds between governmental entities. The transfer may take place from one level of government to another (i.e. counties to states) or within the same level of government (i.e. from a state university hospital to the state Medicaid agency). The federal Medicaid statute explicitly recognizes the legitimacy of IGTs involving tax revenues. Section 1903(w)(6)(A) of the Social Security Act specifies that "the Secretary may not restrict States' use of funds where such funds are derived from State or local taxes (or funds appropriated to State university teaching hospitals) transferred from or certified by units of government within a State as the non-Federal share of expenditures under this title, regardless of whether the unit of government is also a health care provider.”

a n d t h e uninsuredkaiser

commiss ion o n

K E Y F A C T S

1 3 3 0 G S T R E E T N W , W A S H I N G T O N , D C 2 0 0 0 5

P H O N E : 2 0 2 - 3 4 7 - 5 2 7 0 , F A X : 2 0 2 - 3 4 7 - 5 2 7 4 , P U B L I C A T I O N S : 1 - 8 0 0 - 6 5 6 - 4 5 3 3

W W W . K F F . O R G

med i ca i d

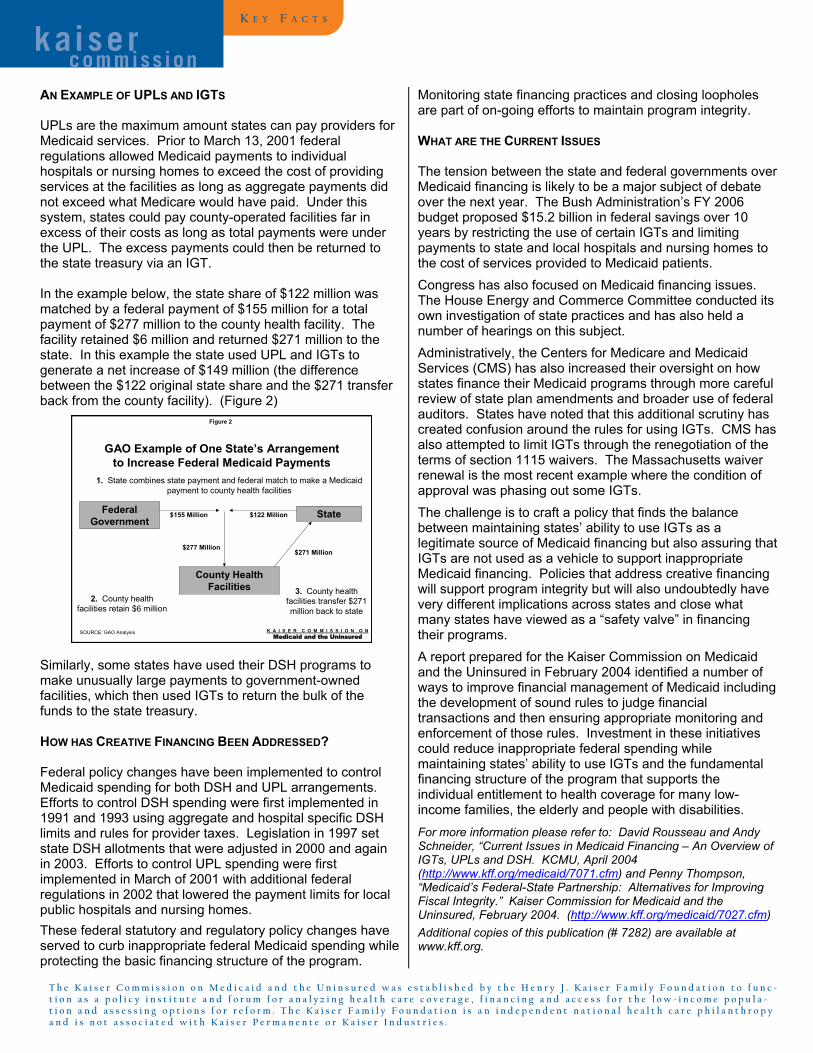

AN EXAMPLE OF UPLS AND IGTS UPLs are the maximum amount states can pay providers for Medicaid services. Prior to March 13, 2001 federal regulations allowed Medicaid payments to individual hospitals or nursing homes to exceed the cost of providing services at the facilities as long as aggregate payments did not exceed what Medicare would have paid. Under this system, states could pay county-operated facilities far in excess of their costs as long as total payments were under the UPL. The excess payments could then be returned to the state treasury via an IGT. In the example below, the state share of $122 million was matched by a federal payment of $155 million for a total payment of $277 million to the county health facility. The facility retained $6 million and returned $271 million to the state. In this example the state used UPL and IGTs to generate a net increase of $149 million (the difference between the $122 original state share and the $271 transfer back from the county facility). (Figure 2)

Similarly, some states have used their DSH programs to make unusually large payments to government-owned facilities, which then used IGTs to return the bulk of the funds to the state treasury. HOW HAS CREATIVE FINANCING BEEN ADDRESSED? Federal policy changes have been implemented to control Medicaid spending for both DSH and UPL arrangements. Efforts to control DSH spending were first implemented in 1991 and 1993 using aggregate and hospital specific DSH limits and rules for provider taxes. Legislation in 1997 set state DSH allotments that were adjusted in 2000 and again in 2003. Efforts to control UPL spending were first implemented in March of 2001 with additional federal regulations in 2002 that lowered the payment limits for local public hospitals and nursing homes. These federal statutory and regulatory policy changes have served to curb inappropriate federal Medicaid spending while protecting the basic financing structure of the program.

Monitoring state financing practices and closing loopholes are part of on-going efforts to maintain program integrity. WHAT ARE THE CURRENT ISSUES The tension between the state and federal governments over Medicaid financing is likely to be a major subject of debate over the next year. The Bush Administration’s FY 2006 budget proposed $15.2 billion in federal savings over 10 years by restricting the use of certain IGTs and limiting payments to state and local hospitals and nursing homes to the cost of services provided to Medicaid patients. Congress has also focused on Medicaid financing issues. The House Energy and Commerce Committee conducted its own investigation of state practices and has also held a number of hearings on this subject. Administratively, the Centers for Medicare and Medicaid Services (CMS) has also increased their oversight on how states finance their Medicaid programs through more careful review of state plan amendments and broader use of federal auditors. States have noted that this additional scrutiny has created confusion around the rules for using IGTs. CMS has also attempted to limit IGTs through the renegotiation of the terms of section 1115 waivers. The Massachusetts waiver renewal is the most recent example where the condition of approval was phasing out some IGTs.

Figure 2

K A I S E R C O M M I S S I O N O NMedicaid and the Uninsured

GAO Example of One State’s Arrangement to Increase Federal Medicaid Payments

Federal Government

State

County Health Facilities

1. State combines state payment and federal match to make a Medicaid payment to county health facilities

$155 Million $122 Million

$277 Million

3. County health facilities transfer $271 million back to state

2. County health facilities retain $6 million

$271 Million

SOURCE: GAO Analysis

The challenge is to craft a policy that finds the balance between maintaining states’ ability to use IGTs as a legitimate source of Medicaid financing but also assuring that IGTs are not used as a vehicle to support inappropriate Medicaid financing. Policies that address creative financing will support program integrity but will also undoubtedly have very different implications across states and close what many states have viewed as a “safety valve” in financing their programs. A report prepared for the Kaiser Commission on Medicaid and the Uninsured in February 2004 identified a number of ways to improve financial management of Medicaid including the development of sound rules to judge financial transactions and then ensuring appropriate monitoring and enforcement of those rules. Investment in these initiatives could reduce inappropriate federal spending while maintaining states’ ability to use IGTs and the fundamental financing structure of the program that supports the individual entitlement to health coverage for many low-income families, the elderly and people with disabilities. For more information please refer to: David Rousseau and Andy Schneider, “Current Issues in Medicaid Financing – An Overview of IGTs, UPLs and DSH. KCMU, April 2004 (http://www.kff.org/medicaid/7071.cfm) and Penny Thompson, “Medicaid’s Federal-State Partnership: Alternatives for Improving Fiscal Integrity.” Kaiser Commission for Medicaid and the Uninsured, February 2004. (http://www.kff.org/medicaid/7027.cfm) Additional copies of this publication (# 7282) are available at www.kff.org.

K E Y F A C T S

kaiser commiss ion

T h e K a i s e r C o m m i s s i o n o n M e d i c a i d a n d t h e U n i n s u r e d w a s e s t a b l i s h e d b y t h e H e n r y J . K a i s e r F a m i l y F o u n d a t i o n t o f u n c -t i o n a s a p o l i c y i n s t i t u t e a n d f o r u m f o r a n a l y z i n g h e a l t h c a r e c o v e r a g e , f i n a n c i n g a n d a c c e s s f o r t h e l o w - i n c o m e p o p u l a -t i o n a n d a s s e s s i n g o p t i o n s f o r r e f o r m . T h e K a i s e r F a m i l y F o u n d a t i o n i s a n i n d e p e n d e n t n a t i o n a l h e a l t h c a r e p h i l a n t h r o p ya n d i s n o t a s s o c i a t e d w i t h K a i s e r P e r m a n e n t e o r K a i s e r I n d u s t r i e s .