jun 2009 tatum survey

TRANSCRIPT

Survey of Business Conditions06.01.2009

2

Click Here to Add Slide Headline

2

Click Here to Add Slide Headline

Tatum Survey of Business Conditions SummaryAs of June 1, the Tatum Index of Business Conditions reached its highest level since

September 2007, just before the Recession began. This is the 7th consecutive month of increase in the Index, further confirming that business conditions, and the economy, are beginning to recover.

The percentage related to the 60 day outlook of conditions worsening is only 9% -- the first time it has been below 10% in more than a year.

The improvements are not dramatic, but they are consistent in overall positive trend.

Financial markets have stabilized, and demand is improving broadly. Our Survey detected the beginnings of the end of the Recession in the first quarter, and the

early indications continue to suggest that the Recovery will begin in earnest in the second half of this year.

The strength in the outlook for employment and “Cap-Ex” shows a gathering confidence that the worst is over and a recovery is under way. If the current and

recent trends continue, then we believe the recovery will ultimately be declared to have begun in the second or third quarters, and that the third quarter will likely

have a positive rate of real growth.

3

Click Here to Add Slide Headline

3

Click Here to Add Slide Headline

Tatum Index of Business ConditionsThe Tatum Index of Business Conditions is a simple average of the ratio of our

respondents who are reporting improvement versus those who are reporting a worsening in business conditions for the past 30 days and the next 60 days.

As of June 1st, the Tatum Index of Business Conditions increased for the seventh month in a row from 2.29 to 3.01. The three-month moving average is now above 2 for the first time in 9 months. It increased from 1.58 to 2.32.

The Index clearly shows businesses are seeing measurable improvements. Confidence about the near term future is the highest

it has been in over a year, and it is heading in the right direction.

4

Click Here to Add Slide Headline

4

Click Here to Add Slide Headline

Tatum Index of Business Conditions

5.5 4.8

9.8 9.5

8.5

12.3

5.4 5.2 6.0

5.1

2.2 2.1 1.7 2.0 1.4 1.2 1.5

2.1 2.7 2.6

1.7 2.0

0.9 0.4 0.4 0.5 0.6 0.8

1.7 2.3

3.0

0

4

8

12

16

12/06

01/07

02/07

03/07

04/07

05/07

06/07

07/07

08/07

09/07

10/07

11/07

12/07

01/08

02/08

03/08

04/08

05/08

06/08

07/08

08/08

09/08

10/08

11/08

12/08

01/09

02/09

03/09

04/09

05/09

06/09

Index 3 Mo. Avg.

5

Click Here to Add Slide Headline

5

Click Here to Add Slide Headline

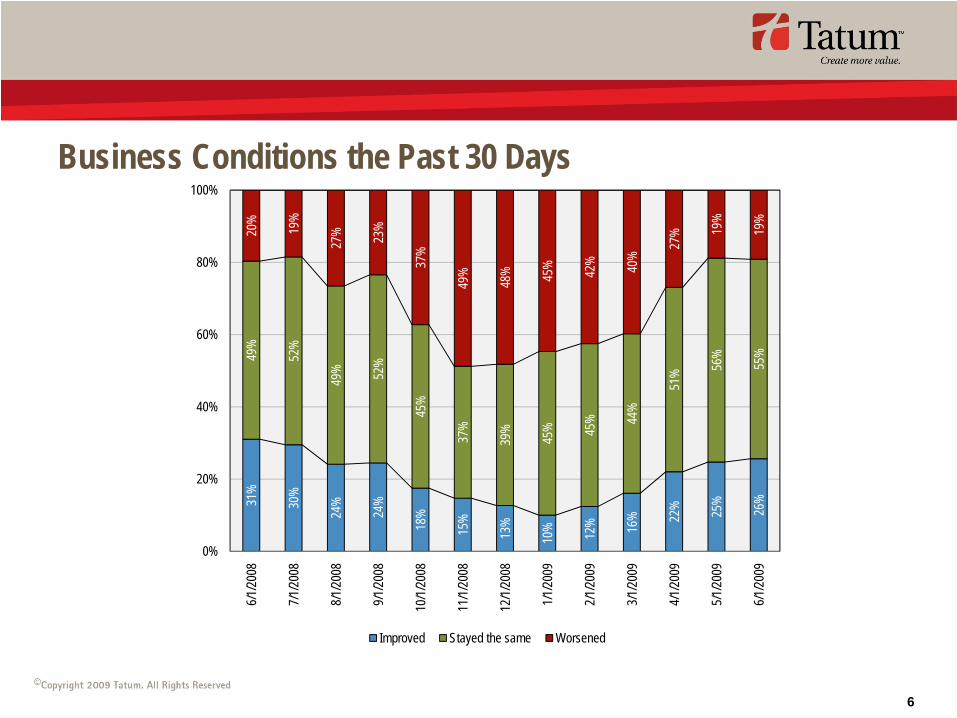

Business Conditions - TrendsIn the past 30 days, business conditions:

Improved for 26% of our respondents, an increase from 25%.Worsened for 19%, the same percentage reported last month. Stayed about the same for 55%, compared to 56% last month.

The improvement was about the same as last month. We anticipate the recovery will be slow, although our Survey participants are becoming

somewhat more positive with each passing month.

6

Click Here to Add Slide Headline

6

Click Here to Add Slide Headline

Business Conditions the Past 30 Days

31%

30%

24%

24%

18%

15%

13%

10% 12% 16

% 22% 25%

26%

49%

52%

49% 52

%

45%

37%

39%

45% 45

% 44%

51% 56

%

55%

20%

19%

27% 23%

37%

49%

48% 45

% 42% 40%

27% 19

%

19%

0%

20%

40%

60%

80%

100%

6/1/20

08

7/1/20

08

8/1/20

08

9/1/20

08

10/1/

2008

11/1/

2008

12/1/

2008

1/1/20

09

2/1/20

09

3/1/20

09

4/1/20

09

5/1/20

09

6/1/20

09

Improved Stayed the same Worsened

7

Click Here to Add Slide Headline

7

Click Here to Add Slide Headline

Business Conditions - Trends

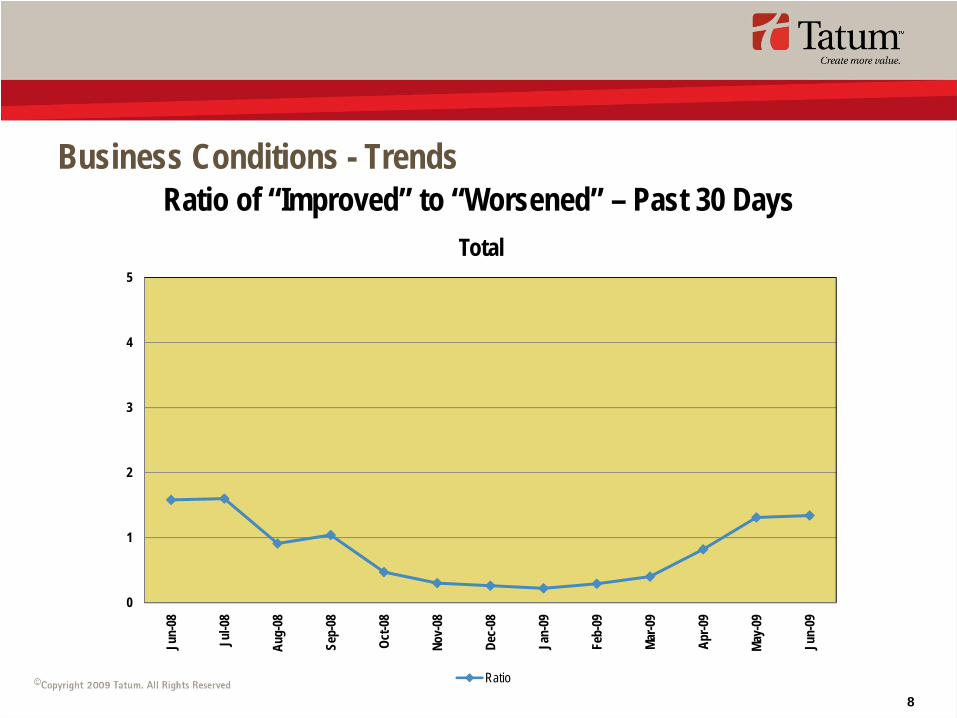

The ratio of “Improved-to-Worsened” in the last 30 days increased slightly from 1.31 to 1.34. This is the second month in a row the ratio has been above one (1).

A very slight improvement from the prior month.

8

Click Here to Add Slide Headline

8

Click Here to Add Slide Headline

Business Conditions - TrendsRatio of “Improved” to “Worsened” – Past 30 Days

0

1

2

3

4

5

Jun-

08

Jul-0

8

Aug-

08

Sep-

08

Oct-0

8

Nov-

08

Dec-

08

Jan-

09

Feb-

09

Mar-0

9

Apr-0

9

May-

09

Jun-

09

Total

Ratio

9

Click Here to Add Slide Headline

9

Click Here to Add Slide Headline

Business Conditions - TrendsIn the next 60 days, business conditions are expected:

To improve for 42% of our respondents, an increase from 39% reported last month. To get worse for 9%, a decrease from 11% reported last month. To remain about the same at 49% compared to the 50% reported last month.

The results of the 60-day outlook improved noticeably from last month. The “Will Worsen” percentage is now in single digits.

10

Click Here to Add Slide Headline

10

Click Here to Add Slide Headline

Business Conditions - TrendsNext 60 Days

46%

44%

42%

42%

32%

20%

21% 26

%

27% 29% 35

% 39% 42

%

41%

43%

41% 45%

42%

38% 40

%

43% 43% 47

%

50% 50

% 49%

12%

13%

17% 14%

26%

42% 39

% 31%

30% 24

% 14% 11% 9%

0%

20%

40%

60%

80%

100%6/1

/2008

7/1/20

08

8/1/20

08

9/1/20

08

10/1/

2008

11/1/

2008

12/1/

2008

1/1/20

09

2/1/20

09

3/1/20

09

4/1/20

09

5/1/20

09

6/1/20

09

Improve Stay the same Worsen

11

Click Here to Add Slide Headline

11

Click Here to Add Slide Headline

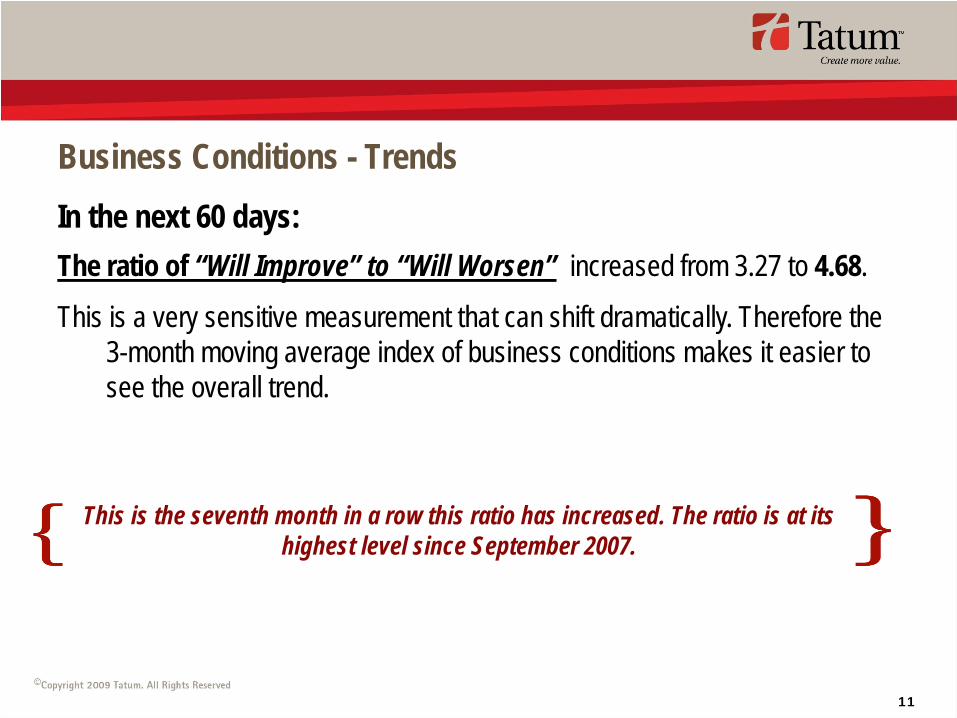

Business Conditions - TrendsIn the next 60 days:The ratio of “Will Improve” to “Will Worsen” increased from 3.27 to 4.68.

This is a very sensitive measurement that can shift dramatically. Therefore the 3-month moving average index of business conditions makes it easier to see the overall trend.

This is the seventh month in a row this ratio has increased. The ratio is at its highest level since September 2007.

12

Click Here to Add Slide Headline

12

Click Here to Add Slide Headline

Business Conditions - TrendsRatio of “Will Improve” to “Will Worsen” – Next 60 Days

0

2

4

6

8

10

12

Jun-

08

Jul-0

8

Aug-

08

Sep-

08

Oct-0

8

Nov-

08

Dec-

08

Jan-

09

Feb-

09

Mar-0

9

Apr-0

9

May-

09

Jun-

09

Total

Ratio

13

Click Here to Add Slide Headline

13

Click Here to Add Slide Headline

Business Conditions – Current ResultsOrder Backlogs

In the past 30 days:The percentage of respondents who reported an improvement in backlogs decreased from 26% to 24%. The percentage reporting lower backlogs remained at 23%.

In the next 60 days:The percentage of respondents who indicated expectations of higher backlogs increased from 38% to 43%. The “Will Worsen” percentage decreased from 11% to 8%. This is the first time in a year the “Will Worsen” percentage has been in single digits.

The outlook for order backlogs is at the highest level in the last 13 months. This is the fifth month in a row the percentages for the next

60 days have improved. Businesses are seeing more orders and rebuilding inventories accordingly.

14

Click Here to Add Slide Headline

14

Click Here to Add Slide Headline

Business Conditions – Current Results

Order Backlog Analysis

Past 30 Days

Next 60 Days

0%

20%

40%

60%

80%

100%

6/1/20

08

7/1/20

08

8/1/20

08

9/1/20

08

10/1/

2008

11/1/

2008

12/1/

2008

1/1/20

09

2/1/20

09

3/1/20

09

4/1/20

09

5/1/20

09

6/1/20

09

Improved Stayed the same Worsened

0%

20%

40%

60%

80%

100%

6/1/20

08

7/1/20

08

8/1/20

08

9/1/20

08

10/1/

2008

11/1/

2008

12/1/

2008

1/1/20

09

2/1/20

09

3/1/20

09

4/1/20

09

5/1/20

09

6/1/20

09

Will improve Will stay the same Will worsen

15

Click Here to Add Slide Headline

15

Click Here to Add Slide Headline

Business Conditions – Current ResultsCapital Expenditure Commitments

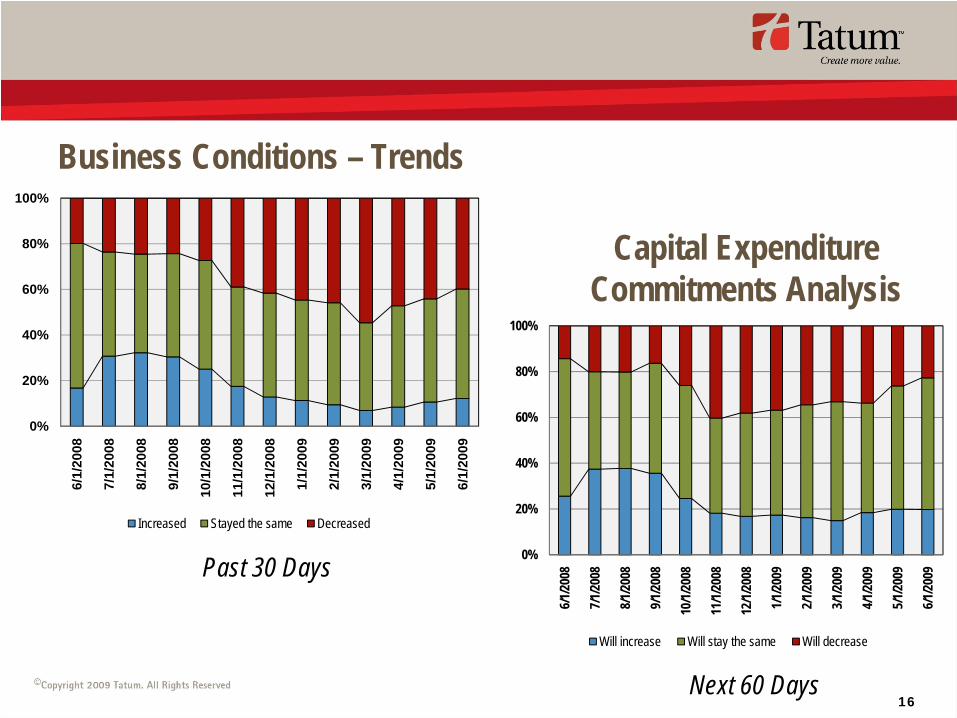

In the past 30 days:The percentage of respondents committing more on capital equipment increased from 11% to 12%. The percentage that committed less on capital decreased from 44% to 40%.

In the next 60 days:The percentage of respondents who said they plan to commit more for capital assets in the next 60 days remained at 20%. The percentage who expected to commit less decreased from 26% to 23%.

For the third month in a row, businesses are showing a willingness to spend money for capital goods. This is an

encouraging trend. When both capital expenditure commitments and employment results show improvement, this is the strongest indicator the Recession has passed the bottom as these tend to

be lagging indicators.

16

Click Here to Add Slide Headline

16

Click Here to Add Slide Headline

Business Conditions – Trends

Capital Expenditure Commitments Analysis

Past 30 Days

Next 60 Days

0%

20%

40%

60%

80%

100%

6/1/

2008

7/1/

2008

8/1/

2008

9/1/

2008

10/1

/200

8

11/1

/200

8

12/1

/200

8

1/1/

2009

2/1/

2009

3/1/

2009

4/1/

2009

5/1/

2009

6/1/

2009

Increased Stayed the same Decreased

0%

20%

40%

60%

80%

100%

6/1/20

08

7/1/20

08

8/1/20

08

9/1/20

08

10/1/

2008

11/1/

2008

12/1/

2008

1/1/20

09

2/1/20

09

3/1/20

09

4/1/20

09

5/1/20

09

6/1/20

09

Will increase Will stay the same Will decrease

17

Click Here to Add Slide Headline

17

Click Here to Add Slide Headline

Business Conditions – Current ResultsEmployment

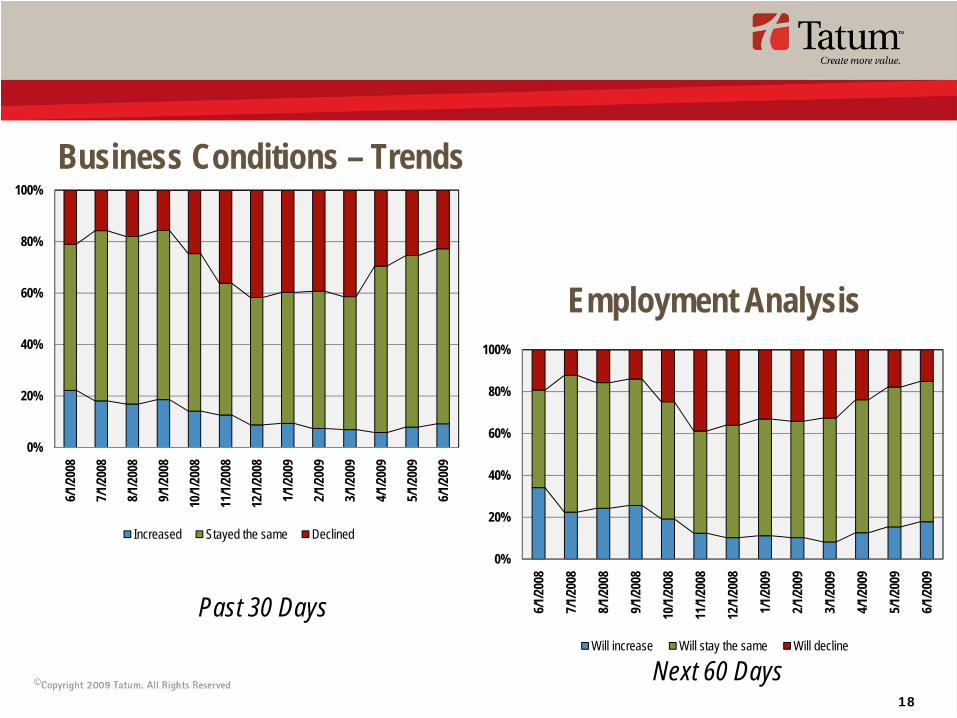

In the past 30 days:The percentage of respondents hiring more workers rose slightly from 8% to 9%. The percentage that indicated they did less hiring decreased from 25% to 23%.

In the next 60 days:The percentage indicating they plan to increase hiring rose from 15% to 18% last month. The percentage who expect to reduce hiring decreased from 18% to 15%.

As we commented last month, our respondents are experiencing an improvement in the employment picture. In June, this outlook strengthened. Because of the lag in reporting results, we expect the unemployment statistics may have already peaked, pending

the fallout from the auto industry restructurings.

18

Click Here to Add Slide Headline

18

Click Here to Add Slide Headline

Business Conditions – Trends

Employment Analysis

Past 30 Days

Next 60 Days

0%

20%

40%

60%

80%

100%

6/1/20

08

7/1/20

08

8/1/20

08

9/1/20

08

10/1/

2008

11/1/

2008

12/1/

2008

1/1/20

09

2/1/20

09

3/1/20

09

4/1/20

09

5/1/20

09

6/1/20

09

Increased Stayed the same Declined

0%

20%

40%

60%

80%

100%

6/1/20

08

7/1/20

08

8/1/20

08

9/1/20

08

10/1/

2008

11/1/

2008

12/1/

2008

1/1/20

09

2/1/20

09

3/1/20

09

4/1/20

09

5/1/20

09

6/1/20

09

Will increase Will stay the same Will decline

19

Click Here to Add Slide Headline

19

Click Here to Add Slide Headline

Business Conditions – Current ResultsCapital Availability and Pricing

The past 30 days:The percentage of respondents indicating an improvement increased from 22% to 25%. The percentage who indicated conditions worsened increased from 10% to 13%.

In the next 60 days:The percentage of the respondents who expect improvement in financing conditions in the next 60 days decreased from 38% to 36% The percentage saying conditions will get worse decreased from 11% to 9%.

Overall for both time periods there was no change from last month. We believe this reflects a stabilization in capital markets and confidence on the part of borrowers to whom the banks are capable and willing to lend money,

albeit with stricter terms and conditions, and at higher rates.

20

Click Here to Add Slide Headline

20

Click Here to Add Slide Headline

Business Conditions – Trends

Capital Availability /Pricing Analysis

Past 30 Days

Next 60 Days

0%

20%

40%

60%

80%

100%

6/1/20

08

7/1/20

08

8/1/20

08

9/1/20

08

10/1/

2008

11/1/

2008

12/1/

2008

1/1/20

09

2/1/20

09

3/1/20

09

4/1/20

09

5/1/20

09

6/1/20

09

Improved Stayed the same Worsened

0%

20%

40%

60%

80%

100%

6/1/20

08

7/1/20

08

8/1/20

08

9/1/20

08

10/1/

2008

11/1/

2008

12/1/

2008

1/1/20

09

2/1/20

09

3/1/20

09

4/1/20

09

5/1/20

09

6/1/20

09

Will improve Will stay the same Will worsen

21

Click Here to Add Slide Headline

21

Click Here to Add Slide Headline

Survey Participation Demographics – IndustryManufacturing/Processing 23%Service 22%Technology 14%Healthcare 11%Financial 7%Wholesale 4%Construction 3%Real Estate 3%Bio-Tech/Life Sciences 3%Transportation 3%Other 7%

22

Click Here to Add Slide Headline

22

Click Here to Add Slide Headline

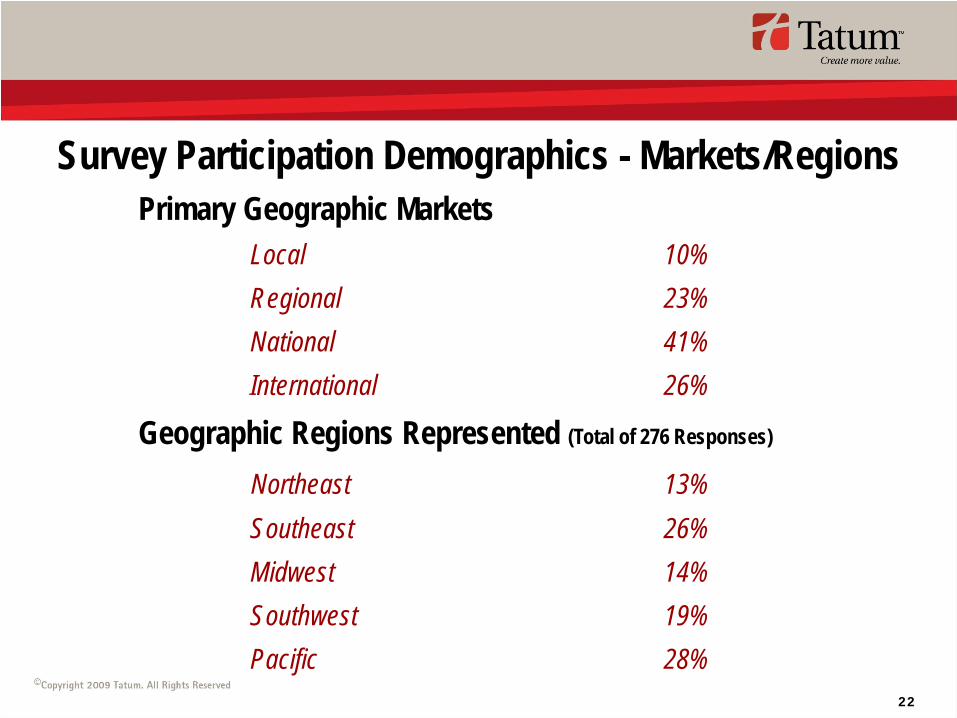

Survey Participation Demographics - Markets/RegionsPrimary Geographic Markets

Local 10%Regional 23%National 41%International 26%

Geographic Regions Represented (Total of 276 Responses)

Northeast 13%Southeast 26%Midwest 14%Southwest 19%Pacific 28%

23

Click Here to Add Slide Headline

23

Click Here to Add Slide Headline

Survey Participation Demographic Summary

The following are on relative scales from our respondents:

Regions: Industries*:Strongest – Southwest Strongest – Financial

Weakest – Pacific Weakest – Service* With statistically significant participation

Markets Served: Company Size:Strongest – National Strongest – Pre-Revenue/Large

Weakest – Regional/International Weakest – Small/Mid-Market

24

Click Here to Add Slide Headline

24

Click Here to Add Slide Headline

Survey of Business Conditions

Compiled and Analyzed bySam Norwood – Senior Partner

Glen Passin – Partner

Any use or reproduction of the contents of this report without the written consent of Tatum, LLC is strictly prohibited. The authors are not engaged in rendering legal,

investment or other professional services by publication of this report. Information contained in this report should not be used as a substitute for professional advice, legal,

investment or otherwise, on any particular issue.