investor presentation - maybank.com€¦ · national commercial bank, saudi 33.1 4 dubai islamic...

TRANSCRIPT

0 www.maybank.com

Investor Presentation

Financial Results 2Q FY2014 and 1H FY2014 ended 30 June 2014

28 August 2014

Humanising Financial Services

1

Table of Contents

Financial Results: 2Q FY2014 and 1H FY2014 ended 30 June 2014

Appendix: Business Sector Review

11

2

27

1. Community Financial Services

2. Global Banking

3. Maybank Singapore

4. Bank Internasional Indonesia

5. Other segments

6. Affiliates

31

36

41

44

48

52

Executive Summary

Financial Performance

Prospects & Outlook

7. Quarterly Financial Summary 55

2 2

Overview (1/2) Maybank delivers higher YoY 1H FY2014 profit led by higher net fund based income, improved cost management and

lower impairment losses

Group loan growth improved to 7.5% for 1H, as loan performance

picked up in 2Q led by international markets

Malaysia 1H loan growth improved in 2Q largely contributed by CFS

growth at 9.8%. If adjusted for offshore foreign currency loans and

unrated bonds, Malaysia 1H annualised loan growth stands at 5.4%

Singapore 1H loan growth of 14.6%, exceeded target of 13.0%

Indonesia loan growth at 9.0% for 1H FY2014, with much stronger

performance in 2Q FY2014

Higher YoY 1H profit

growth, and higher PPOP

QoQ

Stronger loan growth across

all home markets

Net fund based income growth of 8.1% YoY, led by international (12.0%)

and CFS (3.5%)

Lower YoY overhead expenses of 2.7%

Lower impairment losses of 46.4% YoY

But offset by lower fee-based income of 18.0% YoY

2Q FY2014 PPOP higher by 5.6% from earlier quarter, but net profit

softer by 1.6% QoQ due to higher impairments

3 3

Overview (2/2) Group achieves good loan growth traction in 2Q, and funding strategy strengthens deposit growth

Group asset quality

improves

Group GIL improved to 1.50% from 1.86% a year ago, and 1.52% last

quarter

Rise in GIL for BII due to selected corporate accounts in confined sectors

1H Group net charge off rate at 20bps, and loan loss coverage at 107.7%

NIM within expected range

Group NIM at 2.36% as at June 2014 (Dec 2013: 2.43%)

NIM improves in Singapore, while Indonesia and Malaysia continue to

experience some compression

Capital position remains

healthy

Group total capital at 15.96% and CET1 at 11.44% as at 30 June 2014

(assuming an 85% DRP reinvestment rate)

Interim dividend of 24 sen consisting of 4 sen cash portion and 20 sen

electable portion for the Dividend Reinvestment Plan

Strategic deposit taking in

all key markets

2Q annualised deposit growth at 11.0% (1Q: 0%) spearheaded by

International at 11.4% with robust growth in Singapore at 18.1%

Improved focus on retail deposit taking across key markets

Selective growth on non-retail deposits to manage funding cost

4 4

FY2014 Group Targets Above peer growth in key markets and well above industry YoY in Singapore and Indonesia

Annualised YoY

Key Performance

Indicators

FY2014

Targets

1Q

FY2014*

2Q

FY2014*

1H

FY2014*

Industry

Average^

Industry

Average

Peer

Average** Maybank

Headline KPI

Return on Equity* 15.0% 13.8% 13.4% 13.5% - - - -

Other targets

Group Loans Growth 13.0% 5.3% 9.5% 7.5% - - 11.2% 13.1%

• Malaysia 12.0% (0.7)% 5.8% 2.5% 7.7% 9.2% 7.9% 8.2%

• Singapore# 13.0% 5.1% 23.7% 14.6% 8.2% 12.3% 16.6% 18.6%

• Indonesia# 17.0%- 20.0% (1.3)% 19.4% 9.0% 10.3% 13.7% 14.3% 25.5%

Group Deposits Growth 13.0% 0.0% 11.0% 5.5% - - 7.7% 9.1%

* Annualised

^ Numbers are annualised based on June 2014 position for Malaysia, Singapore and Indonesia

# in local currency terms

** Peer comparisons are computed for selected banks based on their June 2014 results. For peer banks which have yet to release their results, computation is based on their

previous quarter results

5 5

Review of 5-Year Strategic Objectives (1/5) Leading funding franchise and stable financing position in domestic market

Strategic Objective 1: Undisputed No. 1 Retail Financial Services provider in Malaysia by 2015

* Refers to Housing & Shophouse Loans

# The above market share for Cards refers to Receivables. In terms of Cardbase, Billings and Merchant Sales, Maybank is ranked No. 1

^ MBB ranking as at Dec’13

The above industry figure includes commercial banks and Non-Financial Institutions and 2Q’14 market share as at May’14

Q4’11 Q4’12 Q2’13 Q3’13 Q4’13 Q1’14 Q2’14

Q2’14

vs

Q1’14

MBB

Rank^

Deposits

Total Deposits 17.4% 17.1% 17.7% 17.7% 18.5% 18.2% 18.2% 1

Total Core Retail Deposits 18.1% 18.3% 18.3% 18.7% 19.0% 19.0% 19.2% 2

Retail CASA 23.3% 23.6% 23.1% 23.9% 24.8% 24.7% 24.5% 1

Retail Savings 28.1% 28.2% 28.0% 27.5% 29.8% 29.9% 29.7% 1

Retail Fixed Deposits (FD) 15.1% 15.2% 15.4% 15.6% 15.7% 15.7% 16.1% 2

Loans

Total Consumer/Household 16.4% 17.0% 17.1% 17.1% 17.2% 17.2% 17.2% 2

Auto (Purchase of transport vehicles) 19.2% 20.2% 20.5% 21.0% 21.5% 21.9% 22.4% 2

Total Mortgage* 13.2% 13.4% 13.3% 13.2% 13.1% 13.0% 13.0% 2

Credit Cards # 15.3% 15.2% 15.3% 15.3% 15.1% 15.1% 15.2% 2

Unit Trust 63.9% 60.2% 57.6% 56.8% 55.8% 54.5% 53.8% 1

Q4’11 Q4’12 Q2’13 Q3’13 Q4’13 Q1’14

Q1’14

vs

Q4’13

MBB

Rank^

Internet Banking – 3 months Active Users 35.68% 34.1% 34.0% 34.31% 33.94% 34.88% 1

Mobile Banking – 1 month Active Users 87.0% 80.5% 76.7% 75.43% 75.35% 75.04% 1

Branch Network 19.0% 19.0% 20.0% 23.0% 20.0% 20.0% 1

6 6

Review of 5-Year Strategic Objectives (2/5) Global Banking continues to roll-out regional business model across the region

Strategic Objective 2: Leading ASEAN wholesale bank eventually expanding

to Middle East, China & India

NOTABLE DEALS COMPLETED FROM JAN – JUN 2014

Regional League Table – Equities

Regional League Table – Regional Bonds

Source: Bloomberg

Countries : Malaysia, Indonesia, Singapore , Hong Kong,

Philippines, Thailand & Vietnam

Jun 2014 Dec 2013 Dec 2012

Ranking Advisor Ranking Advisor Ranking Advisor

1 Goldman

Sachs 1 UBS 1 UBS

2 HSBC Bank 2 Credit

Suisse 2 JP Morgan

3 Bank of

America 3

JP

Morgan 3

Morgan

Stanley

4 DBS Group 4 CIMB 4 Goldman

Sachs

7 Maybank 10 Maybank 11 Maybank

Jun 2014 Dec 2013 Dec 2012

Ranking Advisor Ranking Advisor Ranking Advisor

1 HSBC Bank 1 HSBC Bank 1 HSBC Bank

2 SCB 2 SCB 2 SCB

3 Citi 3 CIMB 3 CIMB

4 CIMB 4 DBS Group 4 DBS Group

6 Maybank 11 Maybank 5 Maybank

7 7

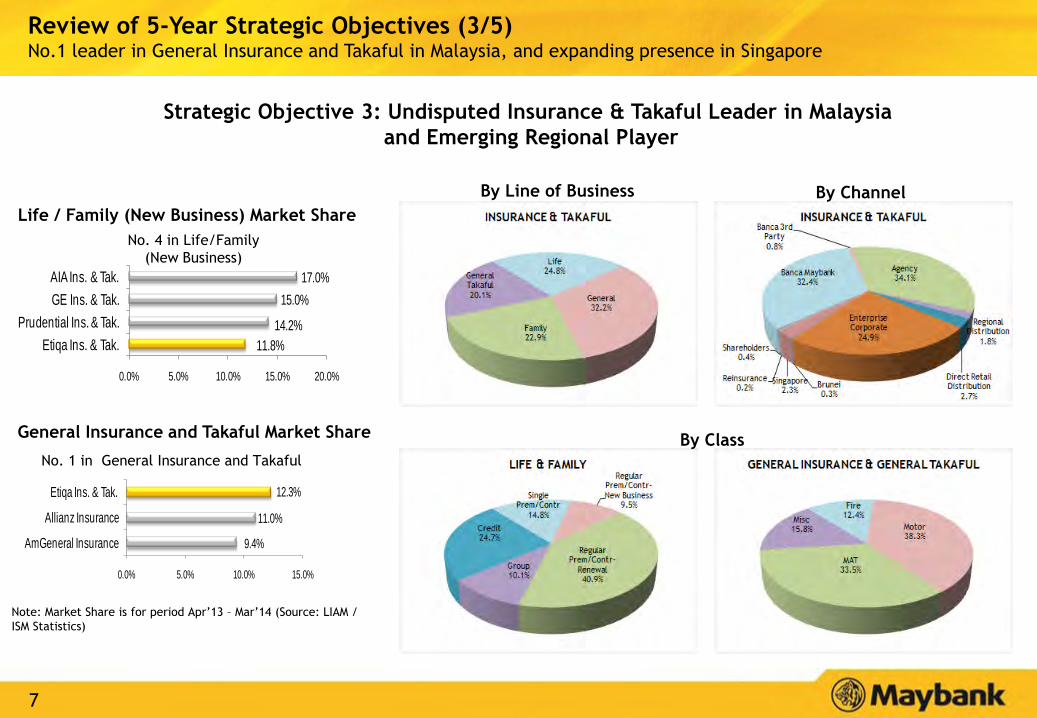

Review of 5-Year Strategic Objectives (3/5) No.1 leader in General Insurance and Takaful in Malaysia, and expanding presence in Singapore

Strategic Objective 3: Undisputed Insurance & Takaful Leader in Malaysia

and Emerging Regional Player

Life / Family (New Business) Market Share

General Insurance and Takaful Market Share

No. 4 in Life/Family

(New Business)

No. 1 in General Insurance and Takaful

Note: Market Share is for period Apr’13 – Mar’14 (Source: LIAM /

ISM Statistics)

11.8%

14.2%

15.0%

17.0%

0.0% 5.0% 10.0% 15.0% 20.0%

Etiqa Ins. & Tak.

Prudential Ins. & Tak.

GE Ins. & Tak.

AIA Ins. & Tak.

9.4%

11.0%

12.3%

0.0% 5.0% 10.0% 15.0%

AmGeneral Insurance

Allianz Insurance

Etiqa Ins. & Tak.

By Line of Business By Channel

By Class

8 8

Review of 5-Year Strategic Objectives (4/5) International PBT contribution at 30.2% for 1H FY14

Strategic Objective 4: Truly regional organisation with approx. 40% of pre-tax profit

derived from international operations by 2015

60.8% 23.5%

7.9% 7.8%

RM375.3b

69.8%

12.1%

3.4%

14.7%

Malaysia Singapore Indonesia Others

RM4.45b

Overseas:

39.2%

1H FY13

Net Income Profit Before Tax

1H FY14

Overseas:

35.5%

Overseas:

34.4%

Overseas:

31.5%

Overseas:

30.2%

Gross loans*

Overseas:

36.6%

* Including Islamic loans sold to Cagamas and excludes unwinding of interest & EIR adjustment

64.5% 15.7%

12.5%

7.3%

RM8.91b

65.6%

14.7%

13.8%

5.9%

RM9.03b

68.5%

14.7%

6.9%

9.9%

RM4.22b

63.4%

21.8%

8.4% 6.4%

RM331.9b

9 9

Review of 5-Year Strategic Objectives (5/5) Largest Malaysian Islamic bank gains market share in key segments

Strategic Objective 5: Global leader in Islamic Finance

26.2% 26.8%28.1%

28.9%30.6% 30.7% 31.1%

23.2% 22.5% 22.1% 22.5%23.8% 24.1%

25.1%

15.0%

20.0%

25.0%

30.0%

35.0%

Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14

Financing Deposit

Domestic Market Share

Jun-14 Jun-13

Automobile financing 37.5% 31.9%

Home Financing 24.3% 22.1%

Term financing 27.8% 25.8%

Maybank Islamic Market Share (Malaysia)

Maybank Islamic Contribution to Maybank Domestic

Financing as at June 2014

Year Contribution

Dec 2012 31.0%

Dec 2013 38.9%

June 2014 41.9%

Maybank Islamic, 41.9%

Maybank Conventional

Domestic, 58.1%

Bank

2013*

Total Assets 2013

(US$ b) Rank

Al Rajhi Bank, Saudi 74.6 1

KFH, Kuwait 57.2 2

Maybank Islamic, Malaysia 38.8 3

National Commercial Bank, Saudi 33.1 4

Dubai Islamic Bank, UAE 30.8 5

Global Position: 3rd Largest Islamic Bank by asset size

Note:

1. Conversion rate as at 31 Dec’13: USD1 = RM3.2757, IDR12,171, SAR3.7506, KWD 0.28236, AED3.6728

2. Source: Respective Bank’s Financial Statement Dec-13, Websites, Bloomberg & Mass Media, 2013

3.*Exclude Iran

10

Table of Contents

Financial Results: 2Q FY2014 and 1H FY2014 ended 30 June 2014

Appendix: Business Sector Review

11

2

27

1. Community Financial Services

2. Global Banking

3. Maybank Singapore

4. Bank Internasional Indonesia

5. Other segments

6. Affiliates

31

36

41

44

48

52

Executive Summary

Financial Performance

Prospects & Outlook

7. Quarterly Financial Summary 55

11 11

P&L Summary: 1H FY2014 Net Profit increased 3.4% YoY, on higher fund-based income, lower overhead expenses and lower impairment losses

RM million 1H FY14 1H FY13 YoY 2Q FY14 1Q FY14 QoQ 2Q FY13 YoY

Net interest income 4,800.2 4,808.9 (0.2)% 2,407.4 2,392.8 0.6% 2,381.5 1.1%

Net Fund based income (Islamic Banking) 1,458.7 981.9 48.5% 727.2 731.5 (0.6)% 506.7 43.5%

Net Fund Based income 6,258.9 5,790.8 8.1% 3,134.6 3,124.3 0.3% 2,888.2 8.5%

Non-interest income 2,597.0 3,069.6 (15.4)% 1,364.9 1,232.1 10.8% 1,705.4 (20.0)%

Fee based income (Islamic Banking) 159.0 303.5 (47.6)% 82.0 76.9 6.7% 159.4 (48.5)%

Net income from insurance business (100.4) (133.2) (24.6)% (102.2) 1.8 <0% (55.1) 85.7%

Net Fee Based income 2,655.6 3,239.9 (18.0)% 1,344.7 1,310.8 2.6% 1,809.7 (25.7)%

Net income 8,914.5 9,030.7 (1.3)% 4,479.3 4,435.1 1.0% 4,697.9 (4.7)%

Overhead expenses (4,254.8) (4,372.2) (2.7)% (2,086.4) (2,168.4) (3.8)% (2,214.3) (5.8)%

Pre-provisioning operating profit (PPOP)¹ 4,659.7 4,658.5 0.0% 2,392.9 2,266.7 5.6% 2,483.6 (3.7)%

Impairment losses (278.8) (520.0) (46.4)% (183.4) (95.4) 92.2% (436.4) (58.0)%

Operating profit 4,380.9 4,138.5 5.9% 2,209.5 2,171.3 1.8% 2,047.2 7.9%

Share of profits in associates 73.7 77.1 (4.4)% 37.3 36.5 2.2% 41.6 (10.5)%

Profit before taxation and zakat 4,454.6 4,215.6 5.7% 2,246.8 2,207.8 1.8% 2,088.8 7.6%

Profit attributable to equity holders (Net Profit)² 3,177.1 3,073.9 3.4% 1,575.5 1,601.6 (1.6)% 1,567.7 0.5%

EPS - Basic (sen) 35.6 36.1 (1.6)% 17.5 18.1 (3.4)% 18.2 (4.2)%

¹Pre-provisioning operating profit (PPOP)is equivalent to operating profit before impairment losses

²Net profit is equivalent to Profit attributable to equity holders of the Bank

12

4,658

1,748

906 791 258

1,207

419

4,660

1,920

909 702

113

1,398

402

Total Community FinancialServices

Corporate Banking Global Markets Investment Banking InternationalBanking

Insurance, Takaful &Asset Management

1H FY2013 1H FY2014

9.9% 0.3% -11.3%

9,031

3,532

1,107 911 784

2,597

770

8,915

3,646

1,136 788 591

2,797

739

Total Community FinancialServices

Corporate Banking Global Markets Investment Banking InternationalBanking

Insurance, Takaful &Asset Management

1H FY2013 1H FY2014

3.2% -13.5%

Global Banking (GB)

- 1.3%

-24.6% 7.7%

-10.2%

-4.0% 2.7%

Business Segment Performance: 1H FY2014 (1/2) Net income and PPOP for 1H FY2014 was softer, due to higher fee income gains in last year’s corresponding period

(RM

mill

ion

) (R

M m

illio

n)

Global Banking (GB) 0.0%

-56.2% 15.8% -4.1%

-11.8%

Note: Net income & pre-provisioning operating profit for group includes expenditures of Head Office & Others of RM669.5 million for 1H 2013 and RM783.1 million for 1H 2014

Net Income

Pre-provisioning Operating profit

13

Global Banking (GB) 5,791

2,706

780 348 94

1,809

456

6,259

2,800

777 360

79

2,026

478

Total CommunityFinancial Services

Corporate Banking Global Markets Investment Banking InternationalBanking

Insurance, Takaful& Asset

Management

1H FY2013 1H FY2014

3.5% -15.8% -0.4% 3.4% 12.0%

8.1%

-0.5%

4.9%

3,240

827 327 563 689 788

314

2,656

845 359 428 512 772

261

Total Community FinancialServices

Corporate Banking Global Markets Investment Banking InternationalBanking

Insurance, Takaful &Asset Management

1H FY2013 1H FY2014

-18.0 %

-25.8% -16.8% -24.0% 9.9% 2.3%

Global Banking (GB) -17.8%

-2.0%

Business Segment Performance: 1H FY2014 (2/2) Net fund based income was up 8.1% led by International Banking and Community Financial Services

(RM

mill

ion

) (R

M m

illio

n)

Fee-based Income -18.0%

Net Fund Based Income +8.1%

Note: Net fund based income includes expenditures of Head Office & Others of RM401.9 million for 1H FY13 and RM261.9 million for 1H FY14.

Fee-based income includes expenditures of Head Office & Others of RM267.6 million for 1H FY13 and RM521.2 million for 1H FY14

14

1,232

785

279

-97

228

37 2

77

1,365

902

212

86 92 73

(102)

82

Non-interestincome

Commission,service charges

and fees

Investment &Trading Income

Unrealised gain/(losses) onsecurities &derivatives

Foreign ExchangeProfit

Other Income Net Income fromInsurance Business

Fee Income fromIslamic Operations

1Q FY14 2Q FY14

-24.0% 189.0%

Fee based Income: 2Q FY2014 – QoQ (1/2) Core fee income increased by 10.8% QoQ due to higher commission, service charges and fees

14.9% -59.6% 98.6% -5822.3% 6.8%

10.8%

RM

million

15

3,070

1,754

875

(8) 309 140

(133)

304

2,597

1,687

491

(11) 320

110 (100)

159

Non-interestincome

Commission,service charges

and fees

Investment &Trading Income

Unrealised gain/(losses) onsecurities &derivatives

Foreign ExchangeProfit

Other Income Net Income fromInsurance Business

Fee Income fromIslamic Operations

1H FY2013 1H FY2014

-44.0% -27.2%

-15.4%

-3.8% -21.4% 24.6% -47.6% 3.8%

Fee based Income: 1H FY2014 – YoY (2/2) Core fee income decreased by 15.4% YoY primarily due to slower capital market activity in the first half of the year

RM

million

16

Group Loans Growth: 30 June 2014 Group loans growth picked up in 2Q, supported by robust international loans growth

30 Jun 14 31 Dec 13 YTD

Annualised 30 Jun 13 YoY

Group Gross Loans * 375.3 361.8 7.5% 331.9 13.1%

Malaysia (RM billion)** 226.4 223.6 2.5% 209.2 8.2%

Community Financial Services 159.4 151.9 9.8% 143.1 11.4%

Global Banking 67.0 71.7 (13.1)% 66.1 1.3%

International

(RM billion) 144.7 134.7 14.9% 119.4 21.2%

Singapore (SGD billion) 33.2 31.0 14.6% 28.0 18.6%

Consumer 11.1 10.6 9.6% 10.0 11.6%

Commercial 22.1 20.4 17.1% 18.1 22.5%

Indonesia (Rupiah trillion) 108.4 103.7 9.0% 86.4 25.5%

Consumer 37.6 35.3 12.8% 30.6 22.7%

Non-consumer 70.9 68.4 7.1% 55.8 27.1%

Other markets (RM billion) 29.8 26.3 27.0% 21.8 37.0%

Investment Banking

(RM billion) 4.2 3.5 37.6% 3.3 28.9%

*Including Islamic loans sold to Cagamas and excludes unwinding of interest

**Takes into account others portion - Jun 14: 0.0 vs Jun 13: (0.0)

17

RM billion 30 Jun 14 31 Dec 13 YTD

Annualised 30 Jun 13 YoY

Community Financial Services (Reported) 159.4 151.9 9.8% 143.1 11.4%

Community Financial Services (Re-based*) 159.4 151.4 10.5% 143.1 11.4%

Consumer (Reported) 128.4 121.9 10.6% 114.6 12.0%

Consumer (Re-based*) 128.4 122.2 10.2% 114.6 12.0%

Total Mortgage 56.8 53.8 11.2% 50.9 11.5%

Auto Finance 37.0 35.0 11.8% 32.9 12.7%

Credit Cards 5.5 5.6 (2.8)% 5.4 2.7%

Unit Trust 27.3 26.3 7.4% 24.2 12.9%

Other Retail Loans (Reported) 1.8 1.3 74.6% 1.3 38.0%

Other Retail Loans (Re-based*) 1.8 1.6 31.1% 1.3 38.0%

Business Banking + SME (Reported) 31.0 29.9 6.9% 28.5 8.7%

Business Banking + SME (Re-based*) 31.0 29.2 11.9% 28.5 8.7%

SME (Reported) 6.4 6.0 10.4% 5.4 17.8%

SME (Re-based*) 6.4 5.3 42.1% 5.4 17.8%

Business Banking (Reported) 24.6 23.9 6.0% 23.1 6.6%

Business Banking (Re-based*) 24.6 24.0 5.2% 23.1 6.6%

Global Banking (Corporate)

- Reported 67.0 71.7 (13.1)% 66.1 1.3%

- Re-based* 67.0 72.1 (14.3)% 66.1 1.3%

- Re-based** 74.1 75.4 (3.6)% 69.9 6.0%

Total Domestic^ 226.4 223.6 2.5% 209.2 8.2%

Malaysia Loans Growth: 30 June 2014 Consumer loan growth was above system, while Global Banking saw slower loan growth due to offshore financing

and repayments

*Re-based loan growth figures are based on adjusted 31 Dec 2013 position in line with migration of client accounts which are implemented on 1 January 2014

**Rebased loan growth figures include CB loans centred in Labuan and unrated bonds which is captured by Global Markets

^Including Islamic loans sold to Cagamas and excludes unwinding of interest and takes into accounts others portion – Jun 14: 0.0 vs Jun 13: (0.0)

18

30 Jun 14 31 Dec 13 YTD

Annualised 30 Jun 13 YoY

Group Gross Deposits 406.5 395.6 5.5% 372.5 9.1%

Malaysia

(RM billion) 265.1 259.1 4.6% 241.7 9.7%

Savings Deposits 38.7 37.6 6.2% 37.3 3.9%

Current Accounts 67.1 65.8 4.0% 56.5 18.8%

Fixed Deposits 137.4 138.3 (1.3)% 125.7 9.3%

Others 21.8 17.4 50.2% 22.2 (1.8)%

International 143.3 138.6 6.9% 132.1 8.5%

Singapore

(SGD billion) 35.0 34.0 5.9% 33.9 3.1%

Savings Deposits 4.3 4.1 6.0% 3.8 13.6%

Current Accounts 4.8 4.7 5.2% 3.4 38.8%

Fixed Deposits 25.2 24.7 4.2% 26.3 (4.1)%

Others 0.7 0.5 101.7% 0.4 76.3%

Indonesia

(Rupiah trillion) 106.2 107.5 (2.4)% 91.3 16.3%

Savings Deposits 24.3 24.7 (3.4)% 20.3 19.7%

Current Accounts 16.4 17.7 (14.6)% 15.1 8.7%

Fixed Deposits 65.5 65.1 1.3% 55.9 17.2%

Group Deposit Growth: 30 June 2014 Deposit growth improved in 2Q FY2014, with current accounts and savings deposits expanding in Malaysia and Singapore

19

LDR and CASA Ratio: 30 June 2014 CASA ratio was stable in key markets while Group LDR improved

Singapore BII Group

Group Malaysia

85.9% 86.6% 87.8% 87.9% 86.8%

38.8% 40.7% 39.9% 40.0% 39.9%

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14

93.7% 95.5% 95.7% 98.3% 101.1%

38.7% 39.7% 39.4% 37.8% 38.3%

85.0% 86.4% 87.0% 88.9% 90.8%

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14

LDR (Bank Level)

87.5% 88.2% 89.9% 91.0% 90.6%

34.2% 36.1% 36.1% 35.8% 35.7%

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14

LDR CASA

82.2% 84.6% 90.9% 93.5% 94.7%

21.2% 23.6% 25.9% 25.8% 25.8%

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14

20 20

Key Operating Ratios Operating ratios improved overall in 2Q but ROE and fee income ratio were still behind guidance

(%) 1H FY14 1H FY13 Variance

YoY 2Q FY14 1Q FY14

Variance

QoQ 2Q FY13

Return on Equity 13.5 14.4 (0.9)% 13.4 13.8 (0.4)% 14.7

Net Interest Margin 2.36 2.45 (9 bps) 2.35 2.37 (2bps) 2.44

Fee to Income Ratio 29.8 35.9 (6.1)% 30.0 29.6 0.4% 38.5

Loans-to-Deposit Ratio 90.6 87.5 3.1 % 90.6 91.0 (0.4)% 87.5

Cost to Income Ratio# 47.4 48.0 (0.6)% 46.3 48.6 (2.3)% 46.7

Asset Quality

Gross Impaired Loans Ratio 1.50 1.86 (36 bps) 1.50 1.52 (2 bps) 1.86

Net Impaired Loans Ratio 0.97 1.09 (12 bps) 0.97 0.99 (2 bps) 1.09

Loans Loss Coverage 107.7 103.5 4.2% 107.7 107.2 0.5% 103.5

Net Charge off rate (bps) 20 32 (12 bps) 17 23 (6 bps) 53

Capital Adequacy (Group)^

CET1 Capital Ratio 11.44 10.07 1.37 11.44 10.76 0.68 10.07

Total Capital Ratio 15.96 14.51 1.45 15.96 15.11 0.85 14.51

# Total cost excludes amortisation of intangibles for BII and Kim Eng.

^ The capital ratios are adjusted based on the assumption of 85% reinvestment rate under the DRP

21

Overheads: 1H FY2014 Group CIR improved to 47.4% from 48.0% a year ago

(RM million) 1H FY2014 1H FY2013

YoY

2Q FY2014

1Q FY2014

QoQ

Personnel costs 2,380.1 2,501.0 (4.8)% 1,142.8 1,237.3 (7.6)%

IT Expenses 260.3 296.9 (12.3)% 154.4 105.9 45.8%

Marketing Expenses 327.9 317.9 3.1% 192.6 135.3 42.3%

Admin &general expenses,

fees & brokerage,

establishment costs, and

depreciation & amortisation

1,286.5 1,256.5 2.4% 596.6 689.9 (13.5)%

Total 4,254.8 4,372.3 (2.7)% 2,086.4 2,168.4 (3.8)%

Group overheads composition

% 1H FY2014 1H FY2013 YoY 2Q FY2014 1Q FY2014 QoQ

Total Cost to Income 47.4% 48.0% (0.6)% 46.3% 48.6% 2.3%

Group JAW Position (1.4)% (2.8)%

22

86.0

427.6

270.5

-54.5

210.1

154.4

513.6

364.5

1QFY13

2QFY13

3QFY13

4QFY13

1QFY14

2QFY14

1H2013

1H2014

Allowances for losses on loans

Asset Quality: 30 June 2014 GIL and NIL improved both YoY and QoQ

Group Impaired Loans Ratio Allowance for losses on loans

1.86

1.57

1.28 1.22 1.09 1.18 1.09 1.06

0.95 0.99 0.97

2.84

2.44

2.00 1.90

1.78 1.89

1.86 1.83

1.48 1.52 1.50

Dec2011

Mar2012

Jun2012

Sep2012

Dec2012

Mar2013

Jun2013

Sep2013

Dec2013

Mar2014

Jun2014

Gross Impaired Loans Ratio (%)

Net Impaired Loans Ratio (%)

99.0%

103.5%

106.3%

107.5% 107.2% 107.7%

Loan loss coverage

(RM

mill

ion

)

23

Asset Quality by Market Stable asset quality for Malaysia and Singapore, while Indonesia continued to see elevated asset quality indicators

Malaysia Singapore BII Group

2.21 2.19 2.15

1.69 1.77

1.71

1.48 1.35

1.29

1.06 1.12

1.05

Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14

0.43 0.45

0.42

0.29 0.29

0.26 0.28

0.30

0.26

0.22 0.21 0.20

Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14

Gross Impaired Loans Ratio (%)

Net Impaired Loans Ratio (%)

1.96 1.82

2.15

2.81 2.98

3.53

1.43 1.76 1.70

2.46 2.53

2.95

Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14

24

Group Capital Adequacy: 30 Jun 2014 Total capital ratio at 15.96% (assuming 85% dividend reinvestment rate) and CET1 at 11.44%

11.64% 11.44% 11.38% 11.02%

13.19% 12.99% 12.93% 12.83%

16.16% 15.96% 15.90% 15.43%

Jun 14 Jun 14 Jun 14 Dec 13

Total Capital Ratio Tier 1 Capital Ratio CET 1 Capital Ratio

After proposed

dividend, assuming

85% reinvestment

rate

Group

Bank

Before

proposed

dividend

After proposed

dividend, assuming

85% reinvestment

rate

After proposed

dividend, based on

BNM’s Implementation

Guideline*

16.50% 16.22% 16.13%

15.61%

Jun 14 Jun 14 Jun 14 Dec 13

CET 1, Tier 1 and Total Capital Ratio

Note:

• CET1, Tier 1 and Total Capital Ratio are computed in accordance with Capital Adequacy Framework (Capital Components) issued by BNM in November 2012.

• Based on 85% reinvestment rate under the DRP, fully loaded, the CET1 Ratio would be at 10.67% (Group) and 9.57% (Bank) respectively.

* Capital ratios computed based on BNM’s implementation Guidelines on Capital Adequacy Framework (Capital Components) issued on 8th May 2013.

25

Dividend Dividend payout ratio will remain high in 2014 above policy rate of 40% - 60%

60.0% 61.0%

76.5% 74.9% 79.9% 74.7% 71.9%

68.9%

26

11

28 32 22.5 24

18

8

44

32

36

33

31

FY08** FY09 FY10 FY11 FP11 FY12 FY13 FY14

Final

Interim

The Board has recommended a single-tier interim dividend of 24 sen consisting of 4 sen cash portion and

20 sen electable portion for the Dividend Reinvestment Plan.

Dividend Payout Ratio

* Reinvestment rate for the Dividend Reinvestment Plan

** Adjusted for 1:4 Bonus Issue in February 2008 and 9:20 Rights Issue at RM2.74 in March 2009

# The Net Dividend is 28.5 sen of which 15 sen is single-tier dividend.

Gross Dividend (sen) and Payout Ratio (%)

85.9%*

85.7%*

88.2%* 85.9%*

88.5%* 91.1%*

86.1%*

88.6%*

#

N.A.*

26

Table of Contents

Financial Results: 2Q FY2014 and 1H FY2014 ended 30 June 2014

Appendix: Business Sector Review

11

2

27

1. Community Financial Services

2. Global Banking

3. Maybank Singapore

4. Bank Internasional Indonesia

5. Other segments

6. Affiliates

31

36

41

44

48

52

Executive Summary

Financial Performance

Prospects & Outlook

7. Quarterly Financial Summary 55

27

Malaysia

Market Outlook Key developments for 2H FY2014

Singapore

Indonesia

Outlook Key Developments

• Growth expected to taper in

2H 2014 and 2015 as

Government remains

committed to contain its

deficit spending

• GDP(f) 6.0% (2013: 4.7%)

• System loan(f) 9-10%

• System deposit(f) 7-8%

• GDP(f) 3.3% (2013: 3.9%)

• System loan(f) 10%

• System deposit(f) 3%

• Continued upward trend of

foreign fund flows dependent

on Jokowi’s ability to deliver

structural reforms

• GDP(f) 5.20% (2013: 5.78%)

• System loan(f) 16-17%

• System deposit(f) 11%

• From a 12-month high in July 2014, consumer spending is expected to

taper off in the event of further fuel subsidy removal, as seen last

year after the fuel hike in June 2013

• Low-to-mid low end segment may not be as hard hit as minimum

wage is set to increase

• Weaker 2H expected on the back of competition for deposits and in

selected segments such as trade loans

• Asset quality to remain steady in 2H

• SGD deposits gathering continue to soften but ability to raise USD

deposits improving

• BNM raised OPR by 25bps to 3.25% in July 2014 with another 25bps

hike expected

• Economic growth expected to taper in 2H 2014 and 2015 due to

tighter macroeconomic policies on domestic spending amid

Government’s commitment to reduce its deficit spending

• ETP-related investments and oil and gas investments expected to

gather pace

28

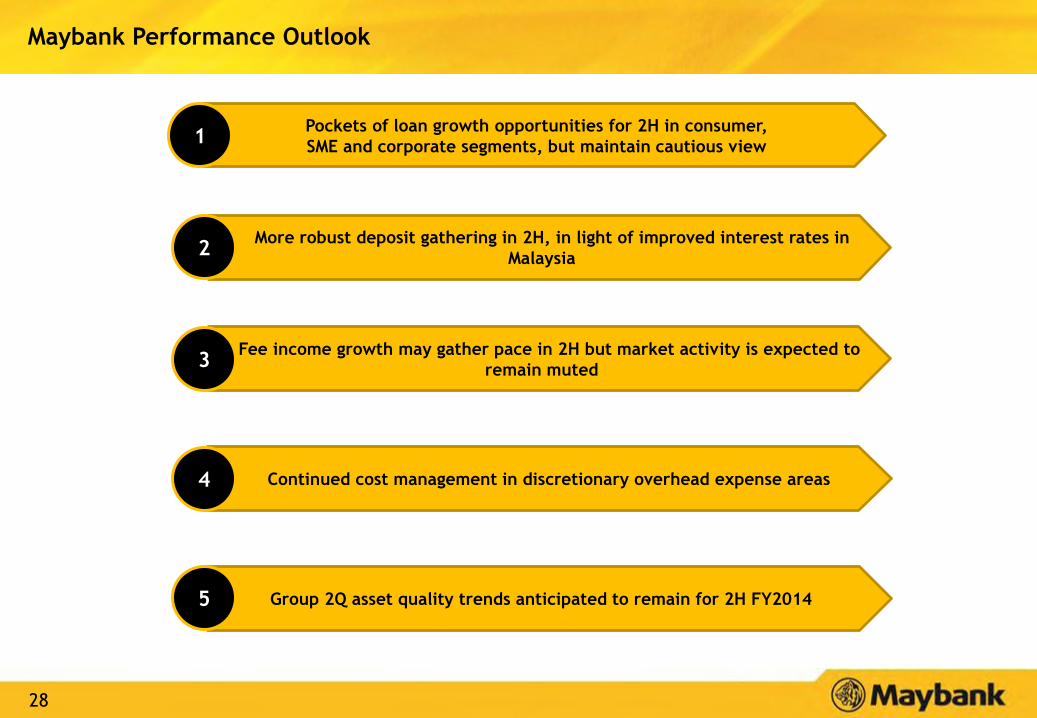

Pockets of loan growth opportunities for 2H in consumer,

SME and corporate segments, but maintain cautious view

More robust deposit gathering in 2H, in light of improved interest rates in

Malaysia

Fee income growth may gather pace in 2H but market activity is expected to

remain muted

Continued cost management in discretionary overhead expense areas

Group 2Q asset quality trends anticipated to remain for 2H FY2014

1

2

3

4

5

Maybank Performance Outlook

29

Key Performance Targets 2014

• Estimated at ~14.0% ROE

Group Loans Growth

Malaysia Loans Growth

Singapore Loans

Growth

Indonesia Loans

Growth

Group Deposits

Growth

• Loans growth expected to be in line with target driven by

International

• Range of 9%-10%, in line with system

• Expected to be in line with target

• Range of 16%-17%, in line with system

• Range of 10%-12%

30

Table of Contents

Financial Results: 2Q FY2014 and 1H FY2014 ended 30 June 2014

Appendix: Business Sector Review

11

2

27

1. Community Financial Services

2. Global Banking

3. Maybank Singapore

4. Bank Internasional Indonesia

5. Other segments

6. Affiliates

31

36

41

44

48

52

Executive Summary

Financial Performance

Prospects & Outlook

7. Quarterly Financial Summary 55

31

Community Financial Services (1/4) Growth in HNW and Affluent customer segments sustained with continued refinement of segment-led business model

and tactical campaigns

* Customer classification: HNW (IA > RM250K, TFA > RM1M); Affluent (IA between > RM 50K to < RM250K, TFA between > RM250K to < RM1m)

* TFA: Total Financial Assets (Deposits, Investments & Financing), IA: Investable Assets (Deposits & Investments)

124.4

128.7

133.5

137.3

141.6

6.26 6.30

6.37

6.48

6.54

6.10

6.20

6.30

6.40

6.50

6.60

115.0

120.0

125.0

130.0

135.0

140.0

145.0

2Q 2013 3Q 2013 4Q 2013 1Q 2014 2Q 2014

TFA RM billion Product per customer

96.7

98.7

101.0

103.2 104.7

2.90

2.95 2.99

3.04 3.08

2.80

2.90

3.00

3.10

3.20

92.0

94.0

96.0

98.0

100.0

102.0

104.0

106.0

2Q 2013 3Q 2013 4Q 2013 1Q 2014 2Q 2014

TFA RM billion Product per customer

Strategic product bundling for the Mass segment customers

under Maybank One has helped increase the Bank’s share-of-

wallet for Mass customers and defend the bank’s market

share for Mass segment.

Emphasis will remain on product bundling of Maybank One to

expand market share in the Mass segment.

Continued refinement of segment-led business model and

implementation of tactical campaigns to create customer

stickiness has sustained growth in the HNW and Affluent

segment.

Currently, the following brands serve the needs of our HNW

and Affluent customers with segment specific privileges:

• Private Wealth for Ultra HNW segment

• Premier Wealth for HNW segment

• Aspire for Affluent segment

HNW & Affluent Customer TFA grew 12.1% (Ann.)

with higher product cross sell ratio

Mass Customer TFA grew 7.3% (Ann.) with focus on

increasing customer’s share of wallet

32

Community Financial Services (2/4) Loans expanded by 10.5% (annualised) despite intense market competition

114.6 117.8

121.9 124.9

128.4

17.1 17.1

17.2 17.2 17.2

17

17.1

17.2

17.3

90

100

110

120

130

2Q 2013 3Q 2013 4Q 2013 1Q 2014 2Q 2014

Loan Balance RM billion Market Share %

122.2*

143.1 146.8

151.9 154.5

159.4

2Q 2013 3Q 2013 4Q 2013 1Q 2014 2Q 2014

CFS Loan Balance RM billion

28.5 29.0

29.9 29.6

31.0

2Q 2013 3Q 2013 4Q 2013 1Q 2014 2Q 2014

Loan Balance RM billion

Consumer loans annualised growth was mainly driven by mortgage

growth of 11.2%, auto growth of 11.8% and retail lending growth of

8.7%.

Retail SME saw a growth of 42.1% (ann.) was primarily driven by

higher term loan facilities utilisation by customers given the

positive business sentiment and competitive pricing.

Business Banking grew 5.2% (ann.) driven by higher utilisation of

term loan facilities but offset by lower utilisation of trade

facilities owing to intense price competition in the market.

Overall loans growth for CFS grew 10.5% (Ann.) to

RM159.4 billion

Consumer loans grew 10.2% (Ann.) to RM128.4 billion

Retail SME and Business Banking loans improved by

11.9% (Ann.) to RM31.0 billion

151.4*

29.2*

*Re-based loan growth figures are based on adjusted 31 Dec 2013 position in line with migration of

client accounts which are implemented on 1 January 2014.. Annualised growth is computed based

on rebased position.

33

Community Financial Services (3/4) Amidst stiff rate competition to attract depositors, CFS deposit grew by 9.6% (annualised)

102.7 105.4

107.5 111.0 112.4

18.3 18.7

19.0 19.0 19.1

16.0

17.0

18.0

19.0

20.0

21.0

22.0

80.0

90.0

100.0

110.0

120.0

2Q 2013 3Q 2013 4Q 2013 1Q 2014 2Q 2014

Deposit Balance RM billion Market Share %

107.2*

161.3

168.2

172.9 169.6

174.2

2Q 2013 3Q 2013 4Q 2013 1Q 2014 2Q 2014

Deposit Balance RM billion

CFS Deposits grew 9.6% (Ann.) mainly driven by

consumer deposit growth

Consumer deposit grew 9.7% (ann.) on the back of fixed deposit

(12.1%) and CASA (6.1%) growth due to strategic use of CRM

analytics and implementation of tactical segment focused

campaigns.

Retail SME grew 11.2% (ann.) while Business Banking was up 4.5%

(ann.) due to higher fixed and demand deposits as a result of

competitive pricing and tactical account management initiatives to

improve customer relationships to attract deposits.

Consumer Deposit saw strong growth of 9.7% (Ann.)

CFS

Deposi

t

Consu

mer

Deposi

t

Reta

il S

ME +

BB

Deposi

t

Retail SME and Business Banking deposits improved 9.4%

(Ann.)

58.6 62.9

65.5

58.5 61.8

2Q 2013 3Q 2013 4Q 2013 1Q 2014 2Q 2014

Deposit Balance RM billion

166.2*

59.1*

*Re-based loan growth figures are based on adjusted 31 Dec 2013 position in line with migration of

client accounts which are implemented on 1 January 2014.. Annualised growth is computed based

on rebased position.

34

Community Financial Services (4/4) Stronger credit asset quality with continued decline in GIL

3,257.9 3,281.9

2,837.5 2,872.4 2,812.7

2.3 2.2

1.9 1.9

1.8

1.5

2.0

2.5

2Q 2013 3Q 2013 4Q 2013 1Q 2014 2Q 2014

1,500.0

2,000.0

2,500.0

3,000.0

GIL RM million GIL %

CFS GIL improved to 1.8% with YoY reduction from 2.3% Consumer GIL rate declined YoY to 0.5% from 0.6%, the

lowest in the industry

Retail SME and Business Banking GIL declined YoY to

7.0% from 9.0% due to better credit asset quality

CFS GIL has shown QoQ improvement, ending at 1.8% for

2Q 2014

GIL % 2Q'13 3Q'13 4Q'13 1Q'14 2Q'14

CFS 2.3 2.2 1.9 1.9 1.8

Consumer 0.6 0.6 0.5 0.5 0.5

Mortgage 0.9 0.8 0.7 0.8 0.7

Auto 0.5 0.5 0.4 0.5 0.5

Credit Cards 1.0 0.9 0.9 1.0 0.8

Unit Trust Loan 0.1 0.1 0.04 0.04 0.1

Retail SME/ BB 9.0 9.0 7.4 7.5 7.0

SME 4.3 4.3 3.5 3.5 3.0

BB 10.1 10.1 8.4 8.4 8.0

715.1 685.3 620.3

667.0 670.1

0.6 0.6

0.5 0.5 0.5

0.4

0.5

0.6

0.7

2Q 2013 3Q 2013 4Q 2013 1Q 2014 2Q 2014

400.0

500.0

600.0

700.0

800.0

GIL RM million GIL %

2,542.8 2,596.6 2,217.2 2,205.4 2,142.5

9.0 9.0

7.4 7.5 7.0

5.0

7.0

9.0

11.0

2Q 2013 3Q 2013 4Q 2013 1Q 2014 2Q 2014

1,000.0

1,500.0

2,000.0

2,500.0

GIL RM million GIL %

35

Table of Contents

Financial Results: 2Q FY2014 and 1H FY2014 ended 30 June 2014

Appendix: Business Sector Review

11

2

27

1. Community Financial Services

2. Global Banking

3. Maybank Singapore

4. Bank Internasional Indonesia

5. Other segments

6. Affiliates

31

36

41

44

48

52

Executive Summary

Financial Performance

Prospects & Outlook

7. Quarterly Financial Summary 55

36

Global Banking (1/4) Corporate banking loans lower by 13.1% (annualised) as at end June 2014

2.6

31.0

32.5

2.7

34.1

34.9

2.6

28.8

35.5

Jun'14

Dec'13

Jun'13

Trade Finance and Others

Overdraft

Trade Finance market share ¹

Corporate Banking GILR at 1.59%

Total GB loans lower by 13.1% (ann.) to RM67.0 billion but

grew 1.3% YoY

-7.2% YoY

+1.7% YoY

RM billion

1Market share of total trade products (On Balance Sheet items, Contingent Liabilities and

Others)

+9.4% YoY

2.05% 2.01%

1.36%

1.62% 1.59%

Jun'13 Sep'13 Dec'13 Mar'14 Jun'14

Term Loan

26.0% 25.6%

27.1%

25.5%

24.8%

Jun'13 Sep'13 Dec'13 Mar'14 Jun'14

37

Global Banking (2/4) Global Markets’ business regionally saw PBT growth of 5.8% YoY for 1H FY2014

45.3%

32.1%

20.6%

0.3%

0.9%

0.8%

A

RM17.8

billion

Commercial

Papers

1,016

1,076

1H FY13 1H FY14

47.6 46.4 47.7 50.8 50.9

37.7 39.4 39.5 40.9 41.4

8.6 9.7 9.2 10.6 8.7

Jun 13 Sep 13 Dec'13 Mar'14 Jun'14

Others

PDS/CorpBonds

Govt.Securities

95.5

57.2% 19.7%

19.0%

1.0%

3.0%

0.2%

<A

27.3%

23.1% 24.1%

16.9%

8.6%

730 646

501 608

1H FY13 1H FY14

Net interest income

Non-interest income

1,254 1.8%

Group Securities Portfolio grew 7.6% YoY

+7.6% YoY

93.9 102.3 101.0

96.4

PBT and Revenue grew by 5.8% and 1.8% YoY respectively

5.8%

1,231

PBT Revenue

RM

million

Note: PBT & Revenue includes regional performance

Group Securities Portfolio: 40.0% Foreign Securities as at

Jun 2014

RM 101.0

billion

YTD Jun 14

52.7% of GM PDS (Maybank Conventional Domestic) rated

“AA” or above as at Jun 2014

RM14.7

billion RM

billion

YTD Jun 14 YTD Jun 13

Government

Securities

-Domestic

Government

Securities

-Foreign

PDS/Corp

Bonds

-Domestic

PDS –

Foreign

Others (NIDs,

BA, etc)

26.3%

24.5% 22.9%

17.3%

9.1%

PDS/Corp

Bonds

-Domestic

RM93.8

billion

Government

Securities

-Domestic

Government

Securities

-Foreign

PDS –

Foreign

Others (NIDs,

BA, etc)

YTD Jun 13

SA (Govt.

Guaranteed)

AAA

AA

SA (Govt.

Guaranteed) AAA

AA

A Commercial

Papers

Note: Group PDS (Maybank Domestic) for YTD Jun 2013 and YTD Jun 2014 are RM18.0 billion

and RM20.6 billion respectively

<A

38 38

Malaysia, RM233.2 (39%)

Singapore, RM136.4 (23%)

Thailand, RM132.3 (22%)

Indonesia, RM9.0 (2%)

Philippines, RM26.8 (5%)

Hong Kong, RM27.5 (5%) Others,

RM26.0 (4%)

Global Banking (3/4) Maybank Kim Eng’s 1H FY2014 total income registered at RM591.2mil

YTD June 2014 Equity Brokerage League Table by Country

* Ranking is not disclosed in respective exchanges

Note: Maybank Kim Eng represents the combined business of Maybank IB and business segments under Maybank Kim Eng Holdings

1H FY2014 Total Income (RM’Mil)

RM591.2mil

Country Rank Market Share Trading Value

(RM’Mil)

Thailand 1 9.9% 76,797

Malaysia 3 9.4% 49,907

Indonesia 5 4.4% 17,372

Philippines 5 7.1% 10,376

Singapore N/A* 5.9% 42,341

Hong Kong Tier2 0.2% 13,742

1H FY2014 Fee-based Income for Malaysia

783.7

591.2

1H FY2013 1H FY2014

- 24.6% YoY

RM

Million

Total Income for Maybank Kim Eng declined 24.6% YoY

Arrangers' Fees 33%

Brokerage 47%

Other Fee Income

4%

Agency/ Guarantee Fees

2%

Advisory Fees 3%

Placement Fees 8%

Primary Subscriber's

Fees 1% Underwriting

Fees 2%

39 39

Global Banking (4/4) Maybank Kim Eng achieved the Top 3 position in ASEAN Investment Banking & Advisory League Table

ASEAN IB&A League Tables – As at June 2014

2,617

2,649

2,684

2,763

4,597

5,298

5,879

6,879

8,360

12,174

8.9%

9.0%

9.1%

9.4%

15.6%

18.0%

20.0%

41.4%

28.4%

41.4%

AmInvestment Bank Bhd

Deutsche Bank

CIMB Group

BoA Merrill Lynch

Maybank

DBS

UOB

Morgan Stanley

Lazard

Credit Suisse

Market Share - M&A Volume (USD'Mil)

3,986

4,111

4,580

4,938

5,139

5,171

5,278

5,510

6,738

9,889

3.6%

3.7%

4.1%

4.4%

4.6%

4.6%

4.7%

4.9%

6.0%

8.8%

Deutsche Bank

JPMorgan

Siam Commercial Bank

DBS

Maybank

Citi

BoA Merrill Lynch

CIMB Group

Standard Chartered Bank

HSBC

Market Share - DCM + Loans Volume (USD'Mil)

7,925

8,033

8,360

8,706

9,215

9,318

10,082

10,233

10,629

13,814

5.21%

5.29%

5.50%

5.73%

6.06%

6.13%

6.63%

6.73%

6.99%

12.7%

Morgan Stanley

Standard Chartered Bank

Lazard

BoA Merrill Lynch

CIMB Group

UOB

HSBC

Maybank

DBS

Credit Suisse

Market Share - IB&A Volume (USD'Mil)

311

358

392

497

618

665

776

873

909

1,021

3.0%

3.5%

3.8%

4.8%

6.0%

6.5%

7.6%

10.0%

8.9%

41.4%

AmInvestment Bank Bhd

RHB Capital Bhd

DBS

Maybank

Goldman Sachs

BoA Merrill Lynch

UBS

Credit Suisse

Citi

CIMB Group

Market Share - ECM Volume (USD'Mil)

Source: Dealogic

40

Table of Contents

Financial Results: 2Q FY2014 and 1H FY2014 ended 30 June 2014

Appendix: Business Sector Review

11

2

27

1. Community Financial Services

2. Global Banking

3. Maybank Singapore

4. Bank Internasional Indonesia

5. Other segments

6. Affiliates

31

36

41

44

48

52

Executive Summary

Financial Performance

Prospects & Outlook

7. Quarterly Financial Summary 55

41

Maybank Singapore (1/2) Loans increased by 14.6% (annualised) as at June, spurred by stronger lending growth of 17.1% to businesses

7.8 7.8 8.7

3.9 4.4 8.7

3.1 4.0

4.2 3.2 4.3 0.6

5.3 6.1 6.5

2.9 2.6 2.3

1.7 1.9 2.3

Jun-13 Dec 13 Jun-14

Other (Consumer)

Car Loan

Housing Loan

Others (Corporate)

Non-Bank financialInstGeneral Commerce

Building & Const

Loans portfolio expanded by 14.6% (annualised) to

reach S$33.2 billion as of June 2014.

Business loans grew 17.1% (annualised) to S$22.1

billion as of Jun 2014. Growth was mainly driven

by trade finance loans, coupled with higher

lending to non-bank financial institutions.

Consumer loans grew 9.6% annualised to reach

S$11.1 billion as of Jun 2014. Housing and other

personal loans continued to register strong growth.

However, car loans continued to decline due to the

limited COE (certificate of entitlement) supply and

tight regulatory financing limits.

0.45 0.44 0.46 0.43

0.30 0.31 0.28

0.31 0.29 0.32 0.28 0.24 0.23 0.22

Dec 12 Mar 13 Jun 13 Sep-13 Dec-13 Mar-14 Jun-14

GIL Ratio NIL Ratio

Asset Quality improved YoY in June 2014

10.6%

13.6% 11.1% 13.6% 13.8% 13.3%

18.6%

10.4% 15.3%

15.1%

16.4% 19.5%

17.3%

16.5%

Dec 12 Mar 13 Jun 13 Sep 13 Dec 13 Mar 14 Jun 14

Maybank Singapore Growth Industry Growth

Maybank Singapore loans growth of 18.6% YoY

Diversified Loan Portfolio

14.6% annualised

28.0 31.0 33.2

Consumer

33%

Corporate

67%

SG

D b

illion

42

Maybank Singapore (2/2) PBT rose 5.6% YoY to S$209 million, led by gains in fee based income of 20.4% and fund based income of 17.5%

(SGD mil) 1H FY2014 1H FY2013 YoY

Net Fund Based income 244.62 208.12 +17.5%

Net Fee Based income 150.77 125.27 +20.4%

Net income 395.39 333.39 +18.6%

Overhead expenses 166.88 144.56 +15.4%

Operating profit 228.51 188.83 +21.0%

Profit before taxation 209.09 198.08 +5.6%

• PBT grew 5.6% YoY or S$11 million to S$209.09 million in the first half of FY 2014, buoyed by robust growth

across fee- and fund- based income.

• Fee-based income increased 20.4% YoY, led by growth in treasury, wealth management and trade finance

income.

• Fund-based income rose 17.5% YoY on the back of improvements in both loan margin and loan base.

• Overhead expenses increased by 15.4% YoY due to greater human capital investments.

43

Table of Contents

Financial Results: 2Q FY2014 and 1H FY2014 ended 30 June 2014

Appendix: Business Sector Review

11

2

27

1. Community Financial Services

2. Global Banking

3. Maybank Singapore

4. Bank Internasional Indonesia

5. Other segments

6. Affiliates

31

36

41

44

48

52

Executive Summary

Financial Performance

Prospects & Outlook

7. Quarterly Financial Summary 55

44

Bank Internasional Indonesia (1/3) 1H FY2014 net profit Impacted by NIM compression and increased provisioning

Note: Published results based on Bank Indonesia classification

(IDR bil) 1H FY2014 1H FY2013 YoY 2Q FY2014 1Q FY2014 QoQ

Net Fund Based income 2,953 2,810 5% 1,506 1,447 4%

Net Fee Based income 1,076 992 8% 572 504 13%

Net income 4,029 3,803 6% 2,078 1,952 6%

Overhead expenses (2,723) (2,651) 3% (1,355) (1,367) (1)%

Personnel (1,095) (1,227) (11)% (592) (503) 18%

General & Administrative (1,628) (1,424) 14% (764) (864) (12)%

Operating profit 1,307 1,152 13% 722 585 24%

Provisions Expenses (703) (324) 117% (368) (335) 10%

Non Operating Income/ Expenses (93) 139 (167)% (123) 30 (515)%

Profit Before Tax before Minority Interest 511 966 (47)% 232 279 (17)%

Net Profit 336 681 (51)% 147 189 (22)%

EPS - Basic (IDR) 5.5 12.1 (55)% 2.4 3.1 (22)%

45

5.73% 5.34% 5.20%

4.75%

Dec-12 Jun-13 Dec-13 Jun-14

14.7 15.1 17.7 16.4

18.8 20.3 24.7 24.3

52.5 55.7 64.9 65.2

86.0 91.1

107.3 105.9

Dec-12 Jun-13 Dec-13 Jun-14

Current Account Saving Account Time Deposit

25.5 23.9 31.0 29.4

27.1 30.2 35.3 38.3

28.3 31.1

35.8 38.3 80.9 85.2 102.1

106.0

Dec-12 Jun-13 Dec-13 Jun-14

Global Banking Business Banking Retail Banking

Net Interest Margin (Consolidated)

Asset Quality (Consolidated)

Loans composition (Consolidated)

Deposits Growth (Consolidated)

IDR trillion 16.2% YoY

Bank Internasional Indonesia (2/3) Loans expanded by 7.7% (annualised) as at end June 2014

24.5% YoY IDR trillion

2.19% 1.85%

2.85%

3.61%

1.26% 1.13%

2.24%

2.77%

Dec-12 Jun-13 Dec-13 Jun-14

Impaired Loan Gross Impaired Loan Net

7.7% (Ann.)

-2.5% (Ann.)

46

753 769

33 35

1H FY2013 1H FY2014

Total Revenue Profit Before Tax

2.66%2.85% 2.85%

3.05% 3.08%

1.38%1.57% 1.46% 1.30% 1.47%

Jun'13 Sep'13 Dec'13 Mar'14 Jun'14

NPL Gross (%) NPL Net (%)

168

66

234 201

77

278

New Used Total

1H FY2013 1H FY2014

Revenue and PBT (IDR billion)

(Stand Alone)

Consumer Financing (IDR billion)

(Stand Alone)

Unit Financing (’000 unit)

(Consolidated)

Asset Quality

(Consolidated)

+5.7% +15.6%

+20%

+36%

+18.7%

Bank Internasional Indonesia (3/3) Higher profits in WOMF due to improving operational efficiency despite tighter regulations

3,052

4,149

Jun'13 Jun'14

47

Table of Contents

Financial Results: 2Q FY2014 and 1H FY2014 ended 30 June 2014

Appendix: Business Sector Review

11

2

27

1. Community Financial Services

2. Global Banking

3. Maybank Singapore

4. Bank Internasional Indonesia

5. Other segments

6. Affiliates

31

36

41

44

48

52

Executive Summary

Financial Performance

Prospects & Outlook

7. Quarterly Financial Summary 55

48

Islamic Banking Total income grew YoY by 25.8% driven by higher fund based income

Group Islamic Banking Income

* Group Islamic Banking includes Maybank Islamic and the Group’s other Islamic

operations

** Other operating income comprise of fee income and other income

RM million 1H FY2014 1H FY2013 YoY

Growth

Fund based income 1,458.7 981.9 48.5%

Other operating income** 159.0 303.5 -47.6%

Total Income 1,617.7 1,285.4 25.8%

Maybank Islamic: Improving key ratios

Jun-14 Jun-13

Financing to Deposit Ratio (Adjusted) 90.4% 94.1%

Islamic Financing to Total Domestic

Loans 41.9% 34.4%

Gross Impaired Financing Ratio 0.67% 0.80%

Net Impaired Financing Ratio 0.46% 0.57%

Maybank Islamic: Total Gross Financing grew by 18.2%

(annualised) to RM94.8 bil

22.50

17.68

21.45

4.29

9.77 11.20

25.25

20.76

22.97

4.22

9.92 11.42

+24%

+35%

+14%

+3%

+4%

AITAB Mortgage Term Financing Others (CFS) Term Financing Others (GB)

Dec-13 Jun-14

q-3%

RM

billion

GB: +3% CFS: +22%

49

Insurance and Takaful Market leadership retained for General Insurance and Takaful

Total Assets (RM billion)

Gross Premium

-21.8% YoY

Profit Before Tax (RM million)

• PBT includes estimated transfer of RM39.57 million from Family Fund in June 2014

+2.1% YoY

+13.8% (Ann.)

* Market ranking in the bracket.

** Market Share & ranking data is for period Jan – Dec, except for 2013 (which is based

on rolling 12 months ending Mar’14). (Source: LIAM / ISM Statistics)

Insurance & Takaful – Market Share

50

Maybank Philippines Despite higher net interest income, PBT declined on lower non interest income and higher overheads

1,639.7

1,882.3

311.1 295.9

1H FY2013 1H FY2014

Revenue

PBT

37,257.5 41,141.6

50,587.3

43,293.2

As at 31 Dec 13 As at 30 June 14

PESO

Mil Gross

Loans

CustomerDeposits

Revenue and PBT

• PBT decreased by 4.9% YoY for the 1H FY2014 mainly due

to lower non interest income (NOII) and higher overheads.

• NOII was impacted by lower trading gains. Overheads rose

largely due to the additional 23 new branches from the

existing 56 as at Jun 2013.

• Gross loans grew 20.9% (annualised) driven by an increase

in term loans.

• Customer deposits was down by 28.8% (annualised) mainly

caused by a decline in fixed deposits and savings accounts.

• Gross impaired loans ratio was higher by 73 bps to 3.51%

from 2.78% in 4Q FY2013 previously, due to an increase in

impaired loan balance by PESO 409.1 million. Gross Loans and Deposits

Key Highlights

*Annualised growth

Key Ratios

1H

FY2014 4Q FY13

Return on assets 0.81% 1.09%

Return on equity 1.17% 5.41%

Cost-to-income ratio 80.04% 73.47%

Loans-to-deposit ratio 95.03% 73.65%

Gross Impaired Loans Ratio 3.51% 2.78%

Net Interest Margin 5.64% 5.12%

No. of branches 79 77

+14.8% YoY

-4.9% YoY

+20.9%*

-28.8%*

PESO

Mil

51

Table of Contents

Financial Results: 2Q FY2014 and 1H FY2014 ended 30 June 2014

Appendix: Business Sector Review

11

2

27

1. Community Financial Services

2. Global Banking

3. Maybank Singapore

4. Bank Internasional Indonesia

5. Other segments

6. Affiliates

31

36

41

44

48

52

Executive Summary

Financial Performance

Prospects & Outlook

7. Quarterly Financial Summary 55

52

An Binh Bank Revenue rose 6.0% backed by higher interest income from loans

739.8 784.4

214.4 170.3

1H FY2013 1H FY2014

Revenue

PBT

37,558.4 36,774.4

40,794.3 39,948.5

As at 31 Dec 13 As at 30 June 14

GrossLoans

CustomerDeposits

Revenue and PBT

Gross Loans and Deposits

• Although operating profit grew by VND50.5 billion YoY, PBT for

1H FY2014 declined by 20.5% due to higher loan loss

provisioning.

• Net interest income grew by VND102.1 billion backed by the

strong loan growth in FY2013.

• Overheads declined by 1.2% in line with cost saving

initiatives.

• Gross loans was down 4.2% (annualised) due to lower lending

to corporate, FI and retail banking.

• Despite intense market competition for term deposits, the

decline in customer deposits was slower at 4.2% (annualised).

• Gross NPL ratio rose to 5.58% from 3.91% in 4Q FY2013 mainly

due to lower loan base.

Key Ratios 1H FY2014 4Q FY2013

Return on assets 0.60% 0.30%

Return on equity 5.90% 3.20%

Cost-to-income ratio 64.56% 66.36%

Loans-to-deposit ratio 92.05% 92.07%

Gross NPL Ratio 5.58% 3.91%

Net Interest Margin 2.73% 2.98%

Key Highlights

+6.0% YoY

-20.5% YoY

-4.2%*

-4.2%*

VN

D B

il

VN

D B

il

*Annualised growth

53

24.9 27.1

18.2 18.1

1H FY2013 1H FY2014

Revenue

PBT

MCB Bank Revenue growth of 9.1% YoY owing to higher net interest income

268.5 303.3

620.4 672.8

As at 31 Dec 13 As at 30 June 14

GrossLoans

CustomerDeposits

• Revenue grew by 9.1% or PKR2.2 billion YoY on the

back of higher net interest income due to a policy

rate hike, resulting in NIMs improvement of 37bps.

• However, PBT marginally declined by 0.6% YoY

attributed to higher overheads and lower share of

associates’ profit in 1H FY2014.

• Gross loans rose 25.9% (annualised) led by private

sector business.

• Customer deposits expanded 16.9% (annualised)

contributed by higher CASA.

• Gross NPL ratio improved by 138 bps from 4Q FY2013

due to the drop in NPL amount, coupled with the

increase in loan base.

Revenue and PBT

Gross Loans and Deposits

+25.9%*

+16.9%*

-0.6% YoY

+9.1% YoY

Key Ratios 1H FY2014 4Q FY2013

Return on assets 2.79% 2.76%

Return on equity 22.99% 22.81%

Cost-to-income ratio 37.92% 40.40%

Loans-to-deposit

ratio 45.08% 43.27%

Gross NPL Ratio 7.29% 8.67%

Net Interest Margin 5.82% 5.45%

Key Highlights

PKR B

il

PKR B

il

*Annualised growth

54

Table of Contents

Financial Results: 2Q FY2014 and 1H FY2014 ended 30 June 2014

Appendix: Business Sector Review

11

2

27

1. Community Financial Services

2. Global Banking

3. Maybank Singapore

4. Bank Internasional Indonesia

5. Other segments

6. Affiliates

31

36

41

44

48

52

Executive Summary

Financial Performance

Prospects & Outlook

7. Quarterly Financial Summary 55

55

Group Gross Loans by quarter

31 Dec 13 31 Mar 14 Q1

Annualised 30 Jun 14

Q2

Annualised % Portfolio

Group Gross Loans * 361.8 366.6 5.3% 375.3 9.5%

Malaysia (RM billion)** 223.6 223.2 (0.7)% 226.4 5.8% 60%

Community Financial Services 151.9 154.5 6.9% 159.4 12.5% 70%

Global Banking 71.7 68.6 (17.1)% 67.0 (9.5)% 30%

International

(RM billion) 134.7 139.9 15.3% 144.7 13.9% 39%

Singapore (SGD billion) 31.0 31.4 5.1% 33.2 23.7%

Consumer 10.6 10.7 3.8% 11.1 15.3% 33%

Commercial 20.4 20.7 5.8% 22.1 28.1% 67%

Indonesia (Rupiah trillion) 103.7 103.4 (1.3)% 108.4 19.4%

Consumer 35.3 36.2 10.0% 37.6 15.1% 35%

Non-consumer 68.4 67.2 (7.1)% 70.9 21.7% 65%

Other markets (RM billion) 26.3 28.7 37.0% 29.8 15.6% 21%

Investment Banking

(RM billion) 3.5 3.6 7.6% 4.2 66.4% 1%

*Including Islamic loans sold to Cagamas and excludes unwinding of interest

**Takes into account others portion - Jun 14: 0.0 vs Jun 13: (0.0)

56

Malaysia Gross Loans by quarter

RM billion 31 Dec 13 31 Mar 14 Q1

Annualised 30 Jun 14

Q2

Annualised % Portfolio

Community Financial Services

(Reported) 151.9 154.5 6.9% 159.4 12.5% 70%

Community Financial Services

(Re-based*) 151.4 154.5 8.2% 159.4 12.5%

Consumer (Reported) 121.9 124.9 9.6% 128.4 11.3% 81%

Consumer (Re-based*) 122.2 124.9 8.8% 128.4 11.3%

Total Mortgage 53.8 55.0 9.2% 56.8 12.8% 44%

Auto Finance 35.0 35.9 11.0% 37.0 12.3% 29%

Credit Cards 5.6 5.4 (14.5)% 5.5 9.4% 4%

Unit Trust 26.3 26.9 8.4% 27.3 6.2% 21%

Other Retail Loans (Reported) 1.3 1.7 114.0% 1.8 27.4% 1%

Other Retail Loans (Re-based*) 1.6 1.7 32.8% 1.8 27.4%

Business Banking + SME (Reported) 29.9 29.6 (3.8)% 31.0 17.7% 19%

Business Banking + SME (Re-based*) 29.2 29.6 5.7% 31.0 17.7%

SME (Reported) 6.0 5.7 (22.2)% 6.4 45.4% 21%

SME (Re-based*) 5.3 5.7 34.9% 6.4 45.4%

Business Banking (Reported) 23.9 23.9 0.8% 24.6 11.1% 79%

Business Banking (Re-based*) 24.0 23.9 (0.7)% 24.6 11.1%

Global Banking (Corporate)

- Reported 71.7 68.6 (17.1)% 67.0 (9.5)% 30%

- Re-based* 72.1 68.6 (19.5)% 67.0 (9.5)%

- Re-based** 75.4 74.6 (4.3)% 74.1 (2.9)%

Total Domestic^ 223.6 223.2 (0.7)% 226.4 5.8% 70%

*Re-based loan growth figures are based on adjusted 31 Dec 2013 position in line with migration of client accounts which are implemented on 1 January 2014

**Rebased loan growth figures include CB loans centred in Labuan and unrated bonds which is captured by Global Markets

^Including Islamic loans sold to Cagamas and excludes unwinding of interest and takes into accounts others portion – Jun 14: 0.0 vs Jun 13: (0.0)

57

Group Deposits by quarter

31 Dec 13 31 Mar 14 1Q

Annualised 30 Jun 14

2Q

Annualised % Portfolio

Group Gross Deposits 395.6 395.7 0.0% 406.5 11.0%

Malaysia

(RM billion) 259.1 258.2 (1.5)% 265.1 10.7% 65%

Savings Deposits 37.6 39.1 16.1% 38.7 (3.5)% 15%

Current Accounts 65.8 64.0 (10.9)% 67.1 19.4% 25%

Fixed Deposits 138.3 136.6 (4.9)% 137.4 2.3% 52%

Others 17.4 18.5 23.4% 21.8 72.8% 8%

International 138.6 139.4 2.3% 143.3 11.4% 35%

Singapore

(SGD billion) 34.0 33.5 (6.0)% 35.0 18.1%

Savings Deposits 4.1 4.3 15.6% 4.3 (3.4)% 12%

Current Accounts 4.7 4.3 (27.4)% 4.8 40.7% 14%

Fixed Deposits 24.7 24.2 (8.5)% 25.2 17.3% 72%

Others 0.5 0.6 148.3% 0.7 40.3% 2%

Indonesia

(Rupiah trillion) 107.5 104.3 (12.0)% 106.2 7.4%

Savings Deposits 24.7 24.0 (10.6)% 24.3 4.0% 23%

Current Accounts 17.7 15.4 (51.2)% 16.4 25.4% 15%

Fixed Deposits 65.1 64.8 (1.8)% 65.5 4.4% 62%

58

Mohamed Rafique Merican

Group Chief Financial Officer

Contact: (6)03-2074 7878

Email: [email protected]

MALAYAN BANKING BERHAD

14th Floor, Menara Maybank

100, Jalan Tun Perak

50050 Kuala Lumpur, Malaysia

Tel : (6)03-2070 8833

www.maybank.com

Narita Naziree

Head, Group Performance Reporting & Investor Relations

Contact: (6)03-2074 8017

Email: [email protected]

Disclaimer. This presentation has been prepared by Malayan Banking Berhad (the “Company”) for information purposes only and does not purport to contain all the

information that may be required to evaluate the Company or its financial position. No representation or warranty, express or implied, is given by or on behalf of the

Company as to the accuracy or completeness of the information or opinions contained in this presentation.

The presentation does not constitute or form part of an offer, solicitation or invitation of any offer, to buy or subscribe for any securities, nor should it or any part of

it form the basis of, or be relied in any connection with, any contract, investment decision or commitment whatsoever.

The Company does not accept any liability whatsoever for any loss howsoever arising from any use of this presentation or their contents or otherwise arising in

connection therewith.

Investor Relations Contact

Humanising Financial Services