investor & analyst day 2015 mtu aero engines ag london, 25

TRANSCRIPT

Investor & Analyst Day 2015

MTU Aero Engines AG

London, 25 November 2015

Investor & Analyst Day 2015 25 November 2015 2

Agenda – MTU Investor and Analyst Day 2015

Time Agenda Speaker

11:00 – 11:10 Welcome Michael Röger

11:10 – 11:20 Excellent Position in an Attractive Market Reiner Winkler

11:20 – 12:10

Geared Turbofan: Flying and Producing

Efficiently

Technology Roadmap: Key for Success

Dr. Rainer Martens

12:10 – 13:00

Geared up for Growth with a Broad Portfolio

Emerging Markets Slowdown:

A severe Threat?

MRO business: Uniquely Positioned for

Growth

Michael Schreyögg

Investor & Analyst Day 2015 25 November 2015 3

Agenda – MTU Investor and Analyst Day 2015

Time Agenda Speaker

13:00 – 14:00 Lunch Break

14:00 – 14:40 Flight hour Agreements: Beneficial for the

Operator and MRO Provider

Reiner Winkler

Michael Schreyögg

14:40 – 15:20 Financials & Outlook Reiner Winkler

15:20 End of Conference

Excellent Position in an

Attractive Market

Reiner Winkler, Chief Executive Officer

London, 25 November 2015

Investor & Analyst Day 2015 25 November 2015 5

Status Market Indicator 2014 A 2015 E 2016 E

Passenger Traffic +6.0% +6.7%

Airline Profits $16 bn $29 bn

Crude Oil (Brent) 100 $ 54 $

Airliner Deliveries 1,350 ~ 1,390

Airliner Orderbook 11,520 11,710

Airliner Engine Fleet 41,410 43,350

Market Overview

Source: IATA, Ascend, EIA

Investor & Analyst Day 2015 25 November 2015 6

Commercial OEM: Milestones Set for Future Growth

• Over 7,000 GTF engines on firm order or

optioned

• PW1100G-JM (A320neo) received its

FAA certification in Jan 2015

• GTF performance in flight test programs

according to plan

• Ramp up of new engine programs

successfully initiated

• Extension of MTU AE Polska in operation

• First development modules for GE9X in

production

• First flight of Gulfstream G500 (PW814) in

May 15 and MRJ (PW1200G) in Nov 15

Investor & Analyst Day 2015 25 November 2015 7

Military Business: Stable Business with Strong Export Potential

• In

• Kuwait signed a MoU for 28 Eurofighter

Typhoon aircraft

• First flight of CH-53K powered by GE38

took place in October

• MTU received the EASA certification for

maintaining TP400

• TP400 engine production fully ramped up

Investor & Analyst Day 2015 25 November 2015 8

MRO: Workload Secured for Decades

• MTU signed MRO network agreement for

the PW1100G-JM in Jun 2015

• Optimization of V2500 FhA agreements

on track

• MTU Maintenance Hannover started

maintenance work for airlines in Iran

• GEnx TCF MRO capability established

Investor & Analyst Day 2015 25 November 2015 9

MTU’s Agenda for 2016

• Assembly line for the PW1100G-JM engine in operation

• GTF module production ramped up according to plan

• Position of MTU in the changing MRO market environment optimized

• Continuous improvement of Flight hour Agreement performance

• MRO readiness at MTU Maintenance Hannover for PW1100G-JM achieved

• Technology roadmap to sustain and improve market position pursued

• Implementation of the new IFRS rule 15 underway

Geared Turbofan:

Flying and Producing Efficiently

Dr. Rainer Martens, Chief Operating Officer

London, 25 November, 2015

Investor & Analyst Day 2015 25 November 2015 11

GTF offers a superior fuel burn consumption at lower maintenance cost

Fan drive gear

3 stg LPC

8 stg HPC

3 stg LPC

10 stg HPC

2 stg HPT

3 stg LPT

2 stg HPT

7 stg LPT

• 25% less stages

• 45% less airfoils

• lower cycle

temperature

• higher propulsive

efficiency

• higher low spool

component

efficiency

• shorter, lighter

The GTF Concept at a Glance: GTF versus Direct Drive Turbo Fan

Source:

cfmaeroengines

Source:

P&W

LPC = Low Pressure Compressor

HPC = High Pressure Compressor

LPT = Low Pressure Turbine

HPT = High Pressure Turbine

stg = Stages

Investor & Analyst Day 2015 25 November 2015 12

The GTF Concept at a Glance: Enabling a Reduced Noise Footprint

Year 2000

Narrowbody aircraft

leaving Munich airport

Noise Simulation: Pratt & Whitney SEL Contour Source: Wyle Laboratories

Year 2015

GTF powered A320 NEO

Noise footprint reduced

by approx. 70%

GTF engines help protecting the environment

Investor & Analyst Day 2015 25 November 2015 13

2015 Development Milestones GTF Engines, PW800, GE9X and GE38

PW1500G /

CSeries

PW1100G-

JM /

A320neo

PW1200G /

MRJ

PW1400G /

MS-21

PW1900G /

PW1700G /

E-Jet 2nd

Gen.

PW800 /

G500,

G600

GE9X /

B777X

GE38 /

CH-53K

First Engine

to Test 2015

2016

2015

Design

Freeze

Tested in

Flying

Testbed N/A

2015

2016 2017 N/A

Engine

Certification 2016 2015 2016

2017 2018 2018*

First Flight 2016 2016

2017 2018

EIS /

Aircraft

Certification

2016 2015 2017 2017 2018

2020

2018

2019 2020 2019

* GE38: Certification of whole aircraft system after flight testing is completed

Investor & Analyst Day 2015 25 November 2015 14

2009 2015 2020

Turbines 800 1150 1850

Compressors 200 320 1580

Turbine

Center

Frame

30 380 350

Engine

Assembly30 110 290

Total 1060 1960 4070

MTU faces a steep increase in commercial engine business

Production Ramp Up

+10%

Yearly increase

+15%

Yearly increase

Investor & Analyst Day 2015 25 November 2015 15

Strategic Setup Production and Supply Chain

Risk Mitigation

The Supply Chain is based on 2 MTU Manufacturing Sites and a Worldwide Network of Suppliers

• Keeping and improving MTU’s high tech knowledge in Munich

• MTU Polska as prime source for ‘mid tech’ parts – supplier as second source

• Dual Source

• Development of advanced manufacturing technology at MTU Munich

High Tech

MTU AE Munich

• Sophisticated parts and

production processes

• Automation

• Development of new

production technologies

• Know How to support all MTU

sites and suppliers

Raw Material, Mid-Low Tech Mid - Low Tech

MTU AE Polska

• Adopting established parts and

production lines from Munich

• Improvement of ‘mid tech’ parts

and production processes

• Module assembly improved with

know how transferred from

automotive industry

Supplier

• Raw parts

• Finished parts as second source

• ‘Low tech’ parts from low cost

countries

Investor & Analyst Day 2015 25 November 2015 16

• Ramp Up Monitoring for

• Engineering & manufacturing

processes

• Infrastructure & production

concepts

• Suppliers

• Shop Floor Management

• Office Management

New approaches improve speed, quality and risk

mitigation

Measures Ensuring MTU’s Ramp Up Capability

Infrastructure

• Blisk-Building

• Logistic-Building

• Extension MTU-Polska

• NEO Assembly

Building 076

• MRO Readiness Hannover

Infrastructure is in place

New Production Concepts

Prime Supplier

Management

Topics are addressed and well under way to support production ramp up

• Blisk

• Blades and Vanes LPT

• Vanes HPC

• Rings

• Supply-Chain Titan-Aluminid

Procurement Teams are operative

• Blisk-production

• Rotor-production

• Case-production

• NEO engine assembly

• Electrochemical milling (PECM) Nickel-Blisk

• Hub-Strut-Case production GE9X MTU AE Polska

• Innovative blade-production MTU AE Polska

• Additive manufacturing

High Tech remains our differentiator

Operational

excellence

Investor & Analyst Day 2015 25 November 2015 17

Blisk Manufacturing

Production System Building 077

• Increase of machine hours per year from

3,500 to 6,000

• Increase of Blisk output per year from 500 to

3,600

• 50% reduction of indirect costs

• More efficient use of area

• Increase of shifts from 15 to 18

• Introduction of full automation with option of

man free production

Changes, Improvements

Investor & Analyst Day 2015 25 November 2015 18

New Logistics Building

• Increase of goods received per year from

80,000 to 115,000 within 5 years

• Improved efficiency leads to a 14% reduction

of process time

• Efficient flow oriented processes

• 30% reduction in lead time

• Weather protected storage of goods

Changes, Improvements New Logistics Building

Investor & Analyst Day 2015 25 November 2015 19

Rotor, Stator Production

Changes, Improvements

• Reduction of small quantity part numbers by

70%

• 12% reduction in hourly rate

• 30% reduction in labor time for turning

operations

• Increase of disc quantity per year from

2,300 to 3,000

• Decommissioning of 14 machines clears

700 sqm production area

Production System Rotor

Investor & Analyst Day 2015 25 November 2015 20

Extension Polska

Production MTU AE Polska

• 20,000 sqm shop floor

• 180k hours engineering capacity

• Low labour rates

• Execution of V2500 Upshare

• ‘Mid Tech’ competencies are kept within

MTU putting suppliers under pressure

• GE9X Hub Strut Case production at lowest

costs

• Flow oriented assembly lines

Changes, Improvements

Investor & Analyst Day 2015 25 November 2015 21

NEO Engine Assembly

Production System NEO Engine Assembly

• New civil engine assembly line with 220

engines per year

• Logistic system is based on pull/just-in-

sequence principle

• Flow oriented assembly line

• High tech transportation and assembly

system

• IT-Supported work flows

Changes, Improvements

Investor & Analyst Day 2015 25 November 2015 22

Summary GTF

• The GTF is a new revolutionary design with unmatched performance

• The market success of this very efficient and successful product requires MTU’s

supply chain to come to a new level of quantity and quality

• Successful production ramp up in the past and already implemented activities put

MTU’s supply chain in an excellent position to execute the future ramp up efficiently

Technology Roadmap:

Key for Success

Dr. Rainer Martens, Chief Operating Officer

London, 25 November, 2015

Investor & Analyst Day 2015 25 November 2015 24

Market Demands - Requirements for Future Engines

Bu

sin

ess

En

vir

on

men

t

Req

uir

em

en

ts

Next generation commercial & military engines

Performance improvement programs (PIP)

Environmental regulations

Flight hour Agreements

Reduction of emissions and noise

Aggressive production cost targets

Maintenance cost reduction measures

Engineering disciplines & manufacturing at excellence

Investor & Analyst Day 2015 25 November 2015 25

MTU‘s Technology Roadmap – Meeting the Requirements

Integrated

Compression-

System

Optimal High

Speed LPT

& TCF

Improve efficiency, weight, design

and pressure ratios

High Temp.

Light Weight

LPT Materials

Additive

Manufacturing Expand portfolio of parts and change

of design philosophy

Virtual Design

& Production

Improve production processes

with an analytical simulation of all

relevant parameters

Improve efficiency, weight design,

temperature and erosion/corrosion

capability

Pro

duct

Enab

ler

Higher cycle parameters, reduce

weight, enabling new designs and

their producabillity

Investor & Analyst Day 2015 25 November 2015 26

Execution of MTU‘s Technology Roadmap – Technology Network

Bauhaus Luftfahrt

University Hannover:

• Airfoil Dynamics

• MRO

ETH Zürich

University Stuttgart:

• Turbines

• Turbine Test Facility

RWTH & FhG Aachen:

• Compressor Aerodynamic

• Manufacturing Technologies

TU München:

• Component Design

DLR Köln:

• Computational Fluid Dynamics

• Compressor Testing

• Ceramic Matrix Composites

BW University Neubiberg:

• More Electric Engine

Investor & Analyst Day 2015 25 November 2015 27

Next Generation GTF - Characteristics

OPR 60+

integrated

compression

system

Ultra efficient

high speed

expansion system

Ultra high BPR 14 -20

with lowest

fan pressure ratio

MTU’s Technolgy Roadmap will lead to the next generation GTF – applicable for all

thrust ranges

Newest light weight

and

heat resistant materials

BPR = By Pass Ratio

OPR = Overall Pressure Ratio

Investor & Analyst Day 2015 25 November 2015 28

Timeline of Future Engine Concepts

∆SFC %

∆CO2 %

V2500

1st gen GTF

2nd gen GTF

Future propulsion concepts

2000 2010 2030 2040 2050 2020

BPR 5

OPR 36

BPR 12

BPR 14-20

OPR 60+

The geared jet engine concept offers a substantial improvement potential

- 15%

- 25%

- 45%

Source:

ENOVAL

Investor & Analyst Day 2015 25 November 2015 29

A few Words about Electric Flight: Basic Concepts

Hybrid – electric

• Combined system consisting of gas turbine and

fans driven by electric motors

• Gas turbine used to generate either electric power

or thrust

• Batteries required

Source: Airbus

Electric

• Thrust generated with fans driven by electric

motors. No gas turbines on board.

• Energy required for the electric motors is

provided by batteries or fuel cells

Weight is driving the use of electric components

Investor & Analyst Day 2015 25 November 2015 30

Battery Technology:

• For an application in short range regional jets todays batteries require a tenfold improvement in

energy density as well as in power density – both requirements are contradictory

• Extrapolating todays improvement in Battery Technology it will take more than 30 years to achieve

the required improvements

Power Distribution and Conversion:

• Using today’s conventional electrical power distribution and power conversion (electric – thrust)

technologies would lead to high weight not suitable in commercial aircraft

• Use of high temperature superconductivity will be required. Cooling down to a temperature of ~45°K

( -230°C) is necessary. A blackout of cooling will result in loss of thrust

Flight safety and Certification:

• All these new technologies have to prove reliability and have to be certified

A few Words about Electric Flight: Technical Challenges

Today Electric Flight can only be realized for small short-range (2-4 seats) aircraft.

For small regional jets electric flight might be imaginable in 30+ years.

Investor & Analyst Day 2015 25 November 2015 31

Summary Technology

• MTU‘s Technology Roadmap will lead to a next generation GTF – incorporating a wide

range of new technologies

• With the next generation GTF MTU is well positioned to cover the full range of thrust

for future aircraft and applications

• Turbo Engines will power aircrafts for a long time – the challenges for incorporating

electric flight are very high

Investor & Analyst Day 2015 25 November 2015 32

Thank you for your attention!

Questions & Answers

Geared up for Growth with a

Broad Portfolio

Michael Schreyögg, Chief Program Officer

London, 25 November 2015

Investor & Analyst Day 2015 25 November 2015 34

Business Jet & Regional Jet Market

PW300/PW500/PW800

• Installed base of more

than 7,000 engines

• 10 business jet

applications in operation

• Dassault Falcon 8X in

development

• PW800 exclusive engine

for future Gulfstream

large business jets

PW1200/PW1500

PW1700/PW1900

• 3,400 orders and options

• GTF family exclusively

powers future Regional

Jets from Embraer,

Mitsubishi and

Bombardier

• New market for MTU

OEM with a future market

share of 90% expected

CF34

• ~6,600 engines flying

• Exclusive powerplant for

current regional jets

• Fast MRO growth with

over 800 off-wing shop

visits

• 12% market share

Expected average annual growth rate of mid teens until 2025

Investor & Analyst Day 2015 25 November 2015 35

Narrowbody Market

PW1100G-JM

• Strong order book

• ~50% market share on

A320neo family in total;

higher market share of

~70% on A321neo

• 15% improved fuel

efficiency, additional 2%

by 2019

• Designed for lower

maintenance cost

V2500

• ~ 5,600 engines flying

• Strong growth of spare

parts sales until mid of

next decade

• #1 MRO provider -

capability in 2 locations

CFM56

• Largest installed fleet

• Strong MRO growth

• #1 independent provider:

over 10% market share

• ~ 900m$ new contract

wins in 2015

• 3 MTU MRO locations

with CFM56 capability

Excellent narrowbody market position leads to continuous OEM & MRO growth

Investor & Analyst Day 2015 25 November 2015 36

Widebody Market

GE9X

• Revenue potential 4 bn€

• 950 orders and options

• Entry into service

expected in 2020

• Exclusive engine for

Boeing 777X

• MTU will be partner of

GE-MRO network

GEnX

• Market share of 60% on

787, exclusive on 747-8

• In production since 2011

• ~770 engines in service

• Market expectation of

4,400 engines

• MTU is partner of the

GE-MRO network

• Exp. MRO revenue 3 bn€

GE90-110/-115B

• ~ 1,500 engines flying; strong MRO growth

• Independent MRO offer with growing market share

• 5 exclusive customers with contract volume of ~1 bn$

Strong partnership with GE Aviation in the widebody market

Investor & Analyst Day 2015 25 November 2015 37

Military Business

GE38

• Power for CH-53K for US

marine corps

• Latest Technology

Turboshaft engine

• First flight October 2015

• Engine could be used for

additional applications

• Strong transatlantic

partnership

TP400-D6

• Ramp up successfully

achieved

• More than 100 engines

produced

• 16 aircraft are operated

by 5 nations

• Aircraft well positioned

for export

EJ200

• Strong revenue

contribution, both

OEM&MRO

• 450 Eurofighter in service

• 1,180 engines delivered

• Production of until 2021

• Strong export potential

Successful new product introduction for the international military market

Emerging Markets Slowdown:

A Severe Threat?

Michael Schreyögg, Chief Program Officer

London, 25 November 2015

Investor & Analyst Day 2015 25 November 2015 39

Emerging Market Slowdown Represents a Risk for OE and

Aftermarket

● Emerging markets (EM) currently experience slower or negative GDP growth and

large currency depreciations against the US$

This is caused by the slowdown in China, sliding commodity prices and the looming

prospect of rising US interest rates

● Passenger traffic growth in EM has remained robust in September

IATA Sep: Lat. Am. +7.9%, Asia +6.8%, China +12.5%, India +13.2%, Russia +12.1%

● EM represent 32% of the commercial jet engine fleet and 36% of firm orders to be

delivered in the next 3 years

How much of MTU’s fleet and orders is exposed to a potential slowdown of EM?

Investor & Analyst Day 2015 25 November 2015 40

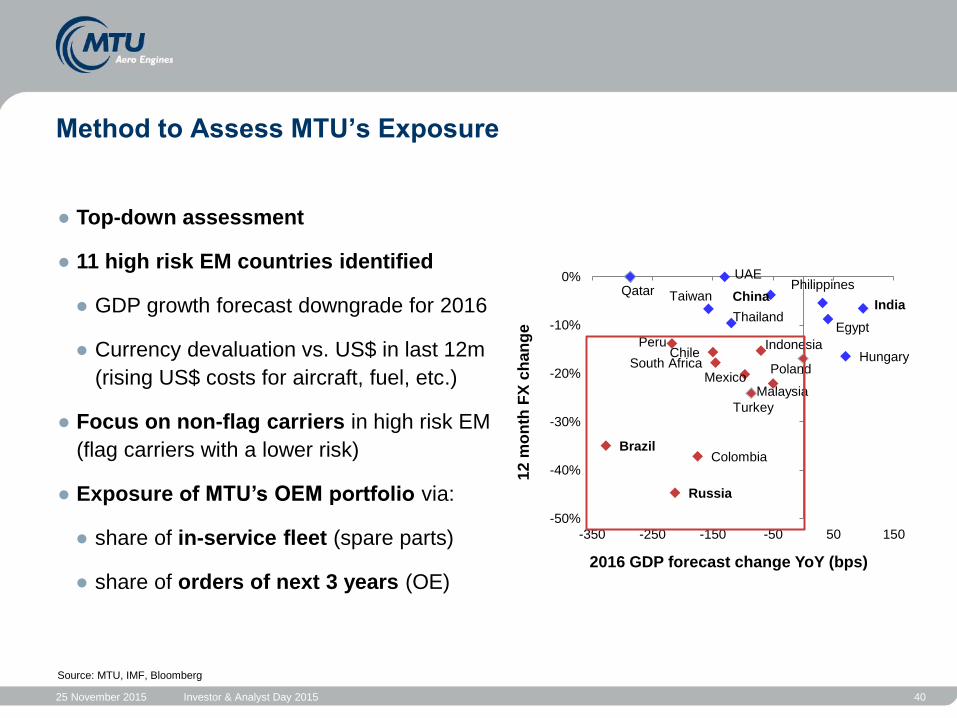

Method to Assess MTU’s Exposure

Source: MTU, IMF, Bloomberg

● Top-down assessment

● 11 high risk EM countries identified

● GDP growth forecast downgrade for 2016

● Currency devaluation vs. US$ in last 12m

(rising US$ costs for aircraft, fuel, etc.)

● Focus on non-flag carriers in high risk EM

(flag carriers with a lower risk)

● Exposure of MTU’s OEM portfolio via:

● share of in-service fleet (spare parts)

● share of orders of next 3 years (OE)

China India

Indonesia

Malaysia

Philippines Qatar Taiwan

Thailand

UAE

Russia

Colombia Brazil

Turkey

Mexico South Africa Poland

Hungary Chile Peru

Egypt

-50%

-40%

-30%

-20%

-10%

0%

-350 -250 -150 -50 50 1501

2 m

on

th F

X c

han

ge

2016 GDP forecast change YoY (bps)

Investor & Analyst Day 2015 25 November 2015 41

Exposure of MTU Deliveries is Limited and Below Industry Average

Source: Ascend, MTU

MTU OEM portfolio EM High risk EM Non-flag carriersin high-risk EM

0

1

2

3

4

# engines to be delivered until 2018

[000]

100%

(3,036 engines)

42%

13% 7%

Emerging

Markets

(EM) High risk

Flag carrier Non-flag carriers

Advanced

Developing

Industry average: 17% 10%

Investor & Analyst Day 2015 25 November 2015 42

Exposure of MTU Fleet is also Limited and Below Industry Average

Source: Ascend, MTU

MTU OEM portfolio EM High risk EM Non-flag carriersin high-risk EM

0

2

4

6

8

10

12

14

# engines in service

[000]

13,200 (100%)

30%

9% 4%

High risk Flag carriers Non-flag carriers

Developing

Advanced

Industry average: 12% 8%

Emerging

Markets

(EM)

Investor & Analyst Day 2015 25 November 2015 43

MTU‘s Exposure to Emerging Markets: Limited and Manageable

● 11 emerging countries have been identified as high risk (Brazil, Russia, Mexico,

Indonesia, Turkey, Poland, Colombia, South Africa, Malaysia, Chile, Peru)

● High risk EM have ordered 13% of MTU’s engines to be delivered in the next 3 years

and operate 9% of MTU’s fleet

● This reduces to 7% and 4% respectively when only secondary carriers in high risk EM

are considered

● Such shares are below industry average

● Should it occur, this risk is limited and manageable for MTU

MRO Business:

Uniquely Positioned for Growth Michael Schreyögg, Chief Programm Officer

London, 25 November 2015

Investor & Analyst Day 2015 25 November 2015 45

MTU’s Diversified Approach Ensures a Broad Market Coverage

CF34, CF6, CFM56, GE90G,

PW2000, V2500

LM IGTs, Vericor

V2500, CFM56

Parts repair

GEnx, GP7000, PWC, V2500,

PW1000G, GE9X

•Over 700 customers (airlines,

MROs, lessors…)

•#1 independent for engine

MRO

• Integrated solutions

•120 IGT/ Marine customers

•JV with China Southern

•JV with Lufthansa Technik

(ASSB)

•MTU is OEM network partner

•MRO share is secured at

program entry for entire life

Independent Airline

cooperation OEM

cooperation 1 2 3

Investor & Analyst Day 2015 25 November 2015 46

0

10

20

30

40

50

60

2015 2017 2019 2021 2023 2025

MTU’s MRO Portfolio is the Basis for Future Growth

MRO Sales ($bn)

CAGR

Market

Approach

Portfolio

6%

No access as

of today

-

8%

Independent

or

Airline

Cooperation

CF34, CFM56,

CF6, GE90G,

PW2000,

V2500

17% OEM

Cooperation PW1000G, GEnx,

GP7000, V2500…

CAGR 2015-25

Total Market ~8%

MTU-served ~10%

Source: MTU, escalated

MTU has the largest engine MRO portfolio of all providers:

The market MTU serves will grow over-proportionally at 10% p.a.

Investor & Analyst Day 2015 25 November 2015 47

Independent Business

• Market CAGR ~8% over

next 10 years

• Increasing demand for

integrated solutions

• Consolidation of pure

independents expected

• Direct customer contact

• Highly competitive market with

strong price and performance

focus

• Customized services

• Largest MRO portfolio,

#1 independent

• Tailored/ integrated solutions

over entire engine life

• Alternative material solutions

• High MTU internal synergies

MARKET TRENDS CHARACTERISTICS MTU POSITIONING

1

Investor & Analyst Day 2015 25 November 2015 48

Independent: Evolution of MTU‘s Business Model From an engine MRO to a provider of service solutions 1

beyond MRO

Vertical integration

Long-term

leasing/ financing

End-of-life

solutions for

operators and

asset owners

1980s 1990s 2000s 2010s 2020s

related services

•Classic engine MRO

•Parts repair

•LRU management

•Spare engine support

•Trend monitoring

•On-site services

Additional services up to Total Engine Care (TEC®)

•Alternatives to MRO

•Engine life extension and exit strategies

Integrated solutions

Engine MRO

Thrust solutions and asset management

•Leasing

Investor & Analyst Day 2015 25 November 2015 49

OEM Cooperation

• Increasing OEM market

coverage

• OEM-FHA share has grown

up to 40%

• Majority of new engines are

sold with OEM-FHA

• Airline concentration on

core business

• OEM is contract holder

• Long term deals with focus

on reducing life-cycle cost

• Competition within OEM

network

• OEM program share secures

MRO workload for decades

• Standardization of

workscopes leads to

economies of scale

• Use of MTU‘s expertise to

best manage fleets of OEMs

• Future capacity additions in

low cost environment

2

MARKET TRENDS CHARACTERISTICS MTU POSITIONING

Investor & Analyst Day 2015 25 November 2015 50

Airline Cooperation

• 60% of global order books

come from emerging markets

• Strong growth young airlines

with large future fleets

• Interest to build up MRO

expertise

• Partners provide baseload

volume and access to

licences

• Presence in growing markets

helps 3rd party business

• Highly competitive shops due

to low labor cost environment

• Local presence with high

MTU quality standards

• Activities in low-cost labor

countries

• Access to fast growing

Chinese/Asian market via JV

• MTU network benefits from

more repair volume and

offload

3

MARKET TRENDS CHARACTERISTICS MTU POSITIONING

Investor & Analyst Day 2015 25 November 2015 51

MTU Maintenance Zhuhai – A Success Story Joint Venture with China Southern Air Holding

3

• 50:50 joint venture since 2001

• Portfolio: V2500-A5, CFM56-3/5B/7

future potential: PW1100G, LEAP

• Capacity: 300 shop visits after extension

2012 (+50%)

• Employees: >700

• #1 provider in China

• Close to 1,800 shop visits

• US$ revenues doubled

within 5 years (2010-15)

• Over 800 m$ contract

wins in 2015

• 3rd largest airline worldwide

• 100 million passengers in 2014

• Over 600 aircraft in operations with

~1,000 engines in JV portfolio

• 24 A320neo orders with PW1100G

2.1

7.6

2015 2025

Revenues

(bn. $)

13.7%

CAGR

Shop visits

2015 2025

8.7%

CAGR 1,254

546

44%

15%

13%

28%

Shop visits (2014)

CSA

China Asia

Company Key Facts Fast Growing Chinese Market

Partner China Southern Competitiveness

Investor & Analyst Day 2015 25 November 2015 52

MTU’s Diversified Approach Ensures a Broad Market Coverage

•Remain #1 provider with

customer focus

•Provide integrated lifecycle

services

•Develop current cooperation

• Investigate future cooperation

potential

•Provide cost efficient

industrialized MRO

•Leverage OEM network

Independent Airline

cooperation OEM

cooperation 1 2 3

Investor & Analyst Day 2015 25 November 2015 53

Outlook

CAGR

~ 10%

w/o MTU Zhuhai

high single digit

% of USD revenue volume incl. MTU Zhuhai 100%, Airline Coop. only CSA; 3rd party customers MTU Zhuhai included in independent

Independent

Airline

Cooperation

OEM

Cooperation

2015 2025

Airline

Cooperation

OEM

Cooperation Independent

• All market channels contribute to strong MRO revenue increase –

with OEM cooperation growing fastest

• Independent segment remains the biggest contributor in 10 years time

Investor & Analyst Day 2015 25 November 2015 54

Thank you for your attention!

Questions & Answers

Flight hour Agreements – Beneficial for

the Operator and MRO Provider

Reiner Winkler, Chief Executive Officer

Michael Schreyögg, Chief Program Officer

London, 25 November 2015

Investor & Analyst Day 2015 25 November 2015 56

Evolution of Engine Maintenance Contract Options

time

Se

rvic

e s

co

pe

TRADITIONAL

Time &

Material

(T&M)

Fixed

price/Not

to exceed

FIXED RATE

INTEGRATED

SOLUTIONS

Flight hour

Agreements

(FhA)

Investor & Analyst Day 2015 25 November 2015 57

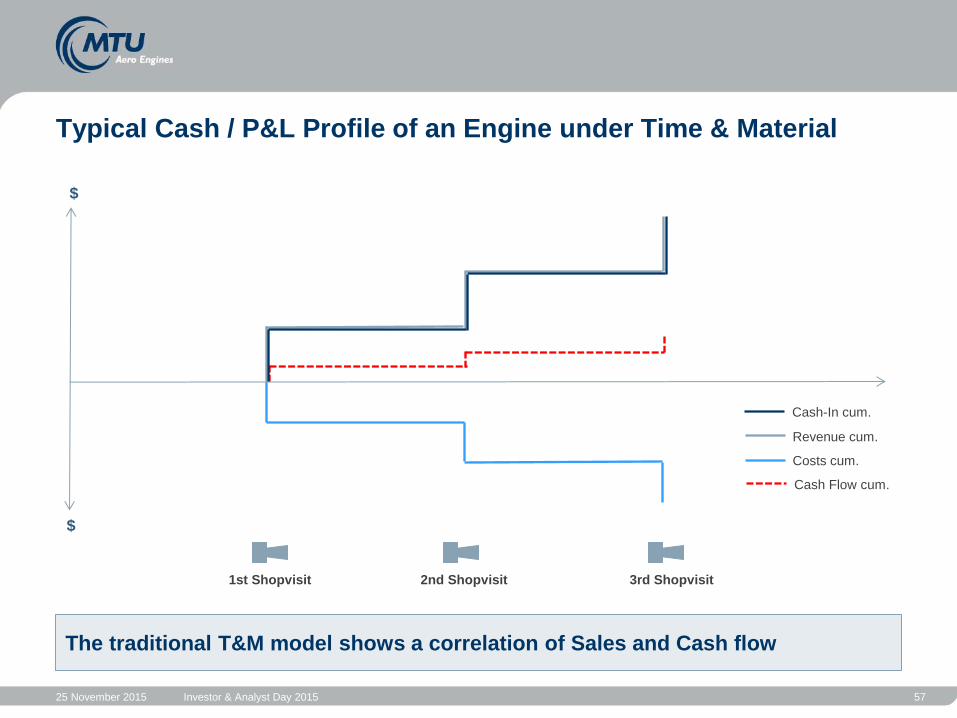

Typical Cash / P&L Profile of an Engine under Time & Material

$

$

The traditional T&M model shows a correlation of Sales and Cash flow

1st Shopvisit 2nd Shopvisit 3rd Shopvisit

Revenue cum.

Costs cum.

Cash Flow cum.

Cash-In cum.

Investor & Analyst Day 2015 25 November 2015 58

$

$

Revenue cum.

Costs cum.

Cash Flow cum.

FhAs lead to an improved Cash Flow profile, P&L recognition remains unchanged

Cash-In cum.

1st Shopvisit 2nd Shopvisit 3rd Shopvisit

Typical Cash / P&L Profile of an Engine under FhA

Investor & Analyst Day 2015 25 November 2015 59

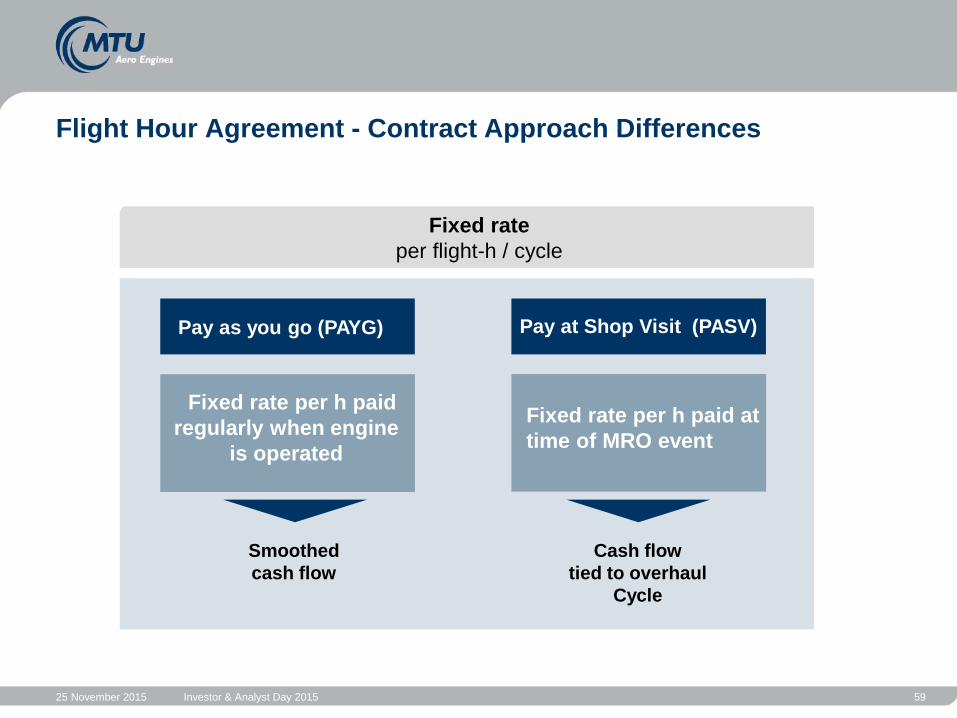

Flight Hour Agreement - Contract Approach Differences

Pay as you go (PAYG)

Fixed rate per h paid

regularly when engine

is operated

Fixed rate

per flight-h / cycle

Smoothed

cash flow

Cash flow

tied to overhaul

Cycle

Fixed rate per h paid at

time of MRO event

Pay at Shop Visit (PASV)

Investor & Analyst Day 2015 25 November 2015 60

Flight Hour Agreements – Benefits

Operator MRO provider

• MRO cost predictability and

transparency

• Predictable cash-flow

• Risk transfer to MRO provider

• Additional services and

insurance options

• Exclusive shop visit volume

• Predictable and steady cash-

flow and workload

• Possibility to include service

packages (e.g. unscheduled

event coverage, lease

engines, training…)

• Simple invoicing

• More flexible inventory

management

Advantages can only be generated with a long term agreement, optimizing the

whole fleet instead of single events

Investor & Analyst Day 2015 25 November 2015 61

• Workscoping

• Material management

• Repair development

• Coatings

What Can be Done in Order to Improve FhA Performance?

Increase on-wing time

Reduce Shop Visit costs

• On-wing support

• Engine trend monitoring

• Coatings

• Select standard

• Removal strategy

• Modifications

Investor & Analyst Day 2015 25 November 2015 62

Improving FhA Performance – On-Wing Support

• AGB oil leakage detected

• AGB removed on-site

• AGB repaired and installed

again

• Aircraft back in operation after

one weekend

• Shop visit avoided

Example 1: Accessory Gear Box

(AGB) oil leakage

• Fully equipped mobile container

to perform LPT module swaps

on-site

• LPT module changed

• Shop visit avoided

Example 2: Low Pressure Turbine

(LPT) swap

Investor & Analyst Day 2015 25 November 2015 63

Improving FhA Performance – Engine Trend Monitoring

HPT stage 2 blade

crack

Example 1: High Pressure Turbine

(HPT) stage 2 blade crack

• HPT Boroscope inspection (BSI)

stage 1&2

• BSI findings: 1 blade cracked

• Engine removed

• Secondary damage avoided

Example 2: Broken Bolt

Bolt broken

• Variable Stator Vane

Bolt broken

• Engine inspected

• On-site bolt replacement

• Shop visit avoided

Investor & Analyst Day 2015 25 November 2015 64

Improving FhA Performance – Erosion Coating (ERCoatnt)

ERCoatnt ERCoatnt ERCoatnt

uncoated uncoated uncoated

Profile nearly unchanged

Profile with material loss

and sharpened trailing edge

Investor & Analyst Day 2015 25 November 2015 65

Summary

• Demand for Flight hour Agreements is increasing

• FhAs do not lead to a change in the revenue profile but to

a change in the cash flow profile

• The airlines as well as the OEMs benefit from FhAs

• The MRO service cost are improved by an increase in

reliability and by lower cost per shop visit

Investor & Analyst Day 2015 25 November 2015 66

Typical Financial Profile of a 10 Years FhA Contract

Shopvisit

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

FHA Cash In (cum.)

FHA Cost (cum.)

FHA Revenue (cum.)

$ Accumulated

$ Cost per Shopvisit

TO

TA

L S

ale

s

TO

TA

L C

osts

Increase OWT

Reduce SV Cost

Investor & Analyst Day 2015 25 November 2015 67

Typical Financial Profile of a 10 Years FhA Contract

Shopvisit

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

FHA Cash In (cum.)

FHA Cost (cum.)

FHA Revenue (cum.)

$ Accumulated

$ Cost per Shopvisit

TO

TA

L C

osts

T

OTA

L S

ale

s

Benefit

Investor & Analyst Day 2015 25 November 2015 68

Cash Flow Streams of V2500 IAE FhA Agreements

Airline

Customers

OEM-MRO

subcontracting

for engines under FhA

Income from

Flight hour Agreement

Roughly 60% of the V2500 fleet is under FhA contract with IAE

IAE Partner,

e.g. MTU OEM

Spares Purchase IAE Partner

e.g. MTU MRO

Investor & Analyst Day 2015 25 November 2015 69

Summary

• IAE currently works together with airline customers on several cost reduction initiatives

for FhA agreements

• Impacting MTU´s financials via

• Less shop visits from IAE and therefore less sales for MRO division short term

• Lower spare parts sales short term, but…

• Higher EBIT margin on spare parts short term

with a higher total EBIT over life of each contract

• Improvement of Free Cash Flow already short term,

as IAE has to pay less for FhA shop visits

Investor & Analyst Day 2015 25 November 2015 70

Thank you for your attention!

Questions & Answers

Financials & Outlook

Reiner Winkler, Chief Executive Officer

London, 25 November 2015

Investor & Analyst Day 2015 25 November 2015 72

Financial Highlights 9M 2015

* w/o market-to-market valuations of US$, options and others

84

119

0

20

40

60

80

100

120

140

9M 2014 9M 2015

178

231

3,50

4,53

0,00

1,00

2,00

3,00

4,00

0

50

100

150

200

250

300

9M 2014 9M 2015

271

333

9,6%10,2%

0%

2%

4%

6%

8%

10%

0

100

200

300

400

9M 2014 9M 2015

2.812

3.257

0

500

1.000

1.500

2.000

2.500

3.000

3.500

9M 2014 9M 2015

Revenues (m€) EBIT adj. / EBIT adj. Margin (m€ / %)

Net Income adj. / EPS adj. (m€ / €)* Free Cash Flow (m€)

+16%

+23%

+30%

+42%

Investor & Analyst Day 2015 25 November 2015 73

Guidance 2015

in m€ FY 2014

Guidance 2015

Revenues 3,914 ~ 4,600

EBIT adj. 383

9.8%

~ 430

Net income adj. 253 ~ 295

• Guidance 2015 based on 1,10 US$/€

• Commercial US$ OE sales up high single digit

• Commercial US$ spare parts sales up low to mid single digit

• Military revenues down 10%

• Commercial MRO US$ sales up low to mid single digit

• R&D (P&L) down by 10 m€

• Tax rate in 2015: 30%

• FCF at high double digit million number

Investor & Analyst Day 2015 25 November 2015 74

New IFRS 15: Revenues from Contracts with Customers

• IASB and FASB intend to harmonize IFRS and US-GAAP regulation on revenue

recognition

• IFRS 15 was issued in May 2014 and will replace previous standards

• IFRS 15 regulates revenue recognition in more detail, by providing a 5-step-model and

respective application guidance:

1) Identify the contract

2) Identify performance obligations

3) Determine the transaction price

4) Allocate transaction price to performance obligations

5) Recognize revenue when performance obligation is satisfied

Background IFRS 15

Investor & Analyst Day 2015 25 November 2015 75

New IFRS 15: Revenues from Contracts with Customers

• IASB rules mandatory application of IFRS 15 from 2018 onwards; postponed by 1 year

• In Europe application of IFRS 15 requires EU endorsement which is now expected for

Q1/2016

• MTU has launched an internal project in 2015 with the support of auditor firms to

assess implication from IFRS 15

• All active customer contracts are examined w.r.t

• Classification of performance obligations (i.e. FHA contract related services)

• Classification/Presentation of sales and cost of sales elements (i.e. concessions)

Update November 2015

Investor & Analyst Day 2015 25 November 2015 76

Head- and Tailwinds 2016

Military: Stable

New engine Sales (Com. OE): Stable

Spare parts Sales (Com. Spares): Low to mid single digit

Commercial MRO: High single digit

Tailwind from US$ fx-rate due to improved Hedge book

Slight headwind from Com. OE mix and R&D (P&L)

Revenue Growth

Investor & Analyst Day 2015 25 November 2015 77

US$ Exchange Rate / Hedge Portfolio

2015 2016 2017 2018

Average hedge rate (US$/€):

(mUS$)

Hedge Book as of November 25, 2015 (% of net exposure)

984 (=93%)

1.25

749 (=68%)

1.25 1.15

500 (=40%)

130 (=10%)

1.22

Investor & Analyst Day 2015 25 November 2015 78

Long Term Outlook 2014 – 2025 - Update

Investment Phase

2014-2017

Consolidation Phase

2018-2025

Revenues

Military:

Com. OE:

Com. Spares:

Com. MRO:

Military:

Com. OE:

Com. Spares:

Com. MRO:

EBIT adjusted Growth in line with revenues Growth stronger than revenues

Net Income adj. Growth stronger than EBIT adj. Growth in line with EBIT adj.

CCR* Low double digit % High double digit %

Updated: Less Volume GP7000 OE 2016ff Higher growth rate PW1100G-JM

FX tailwind (Airbus production rate increase)

Investor & Analyst Day 2015 25 November 2015 79

Key Takeaways

• MTU well prepared with its technology roadmap for future engine projects

• Production and supply chain strategy for the ramp up is implemented

• MTU benefits from its broad product portfolio in all business segments

• Risk of slowdown in emerging markets is manageable

• Diversified MRO market access options and product portfolio ensures future growth

• FhAs lead to a win-win situation for both airlines and MRO providers

• Measurements to improve FhA performance are in place

• Internal project launched for the IFRS 15 implementation

• For 2016 MTU is committed to another year with

earnings growth

Investor & Analyst Day 2015 25 November 2015 80

Thank you for your attention!

Questions & Answers

Investor & Analyst Day 2015 25 November 2015 81

Cautionary Note Regarding Forward-Looking Statements

Certain of the statements contained herein may be statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. In addition to statements that are forward-looking by reason of context, the words “may,” “will,” “should,” “expect,” “plan,” “intend,” “anticipate,” “forecast,” “believe,” “estimate,” “predict,” “potential,” or “continue” and similar expressions identify forward-looking statements.

Actual results, performance or events may differ materially from those in such statements due to, without limitation, (i) competition from other companies in MTU’s industry and MTU’s ability to retain or increase its market share, (ii) MTU’s reliance on certain customers for its sales, (iii) risks related to MTU’s participation in consortia and risk and revenue sharing agreements for new aero engine programs, (iv) the impact of non-compete provisions included in certain of MTU’s contracts, (v) the impact of a decline in German or other European defense budgets or changes in funding priorities for military aircraft, (vi) risks associated with government funding, (vii) the impact of significant disruptions in MTU’s supply from key vendors, (viii) the continued success of MTU’s research and development initiatives, (ix) currency exchange rate fluctuations, (x) changes in tax legislation, (xi) the impact of any product liability claims, (xii) MTU’s ability to comply with regulations affecting its business and its ability to respond to changes in the regulatory environment, (xiii) the cyclicality of the airline industry and the current financial difficulties of commercial airlines, (xiv) our substantial leverage and (xv) general local and global economic conditions. Many of these factors may be more likely to occur, or more pronounced, as a result of terrorist activities and their consequences.

The company assumes no obligation to update any forward-looking statement.

Any securities referred to herein have not been and will not be registered under the U.S. Securities Act of 1933, as amended (the “Securities Act”), and may not be offered or sold without registration thereunder or pursuant to an available exemption therefrom. Any public offering of securities of MTU Aero Engines to be made in the United States would have to be made by means of a prospectus that would be obtainable from MTU Aero Engines and would contain detailed information about the issuer of the securities and its management, as well as financial statements.

Neither this document nor the information contained herein constitutes an offer to sell or the solicitation of an offer to buy any securities.

These materials do not constitute an offer of securities for sale in the United States; the securities may not be offered or sold in the United States absent registration or an exemption from registration.

No money, securities or other consideration is being solicited, and, if sent in response to the information contained herein, will not be accepted.