introduction to management accounting by asst prof. jonlen desa

TRANSCRIPT

INTRODUCTION TO MANAGEMENT ACCOUNTING

ASST PROF. JONLEN DESA

MANAGEMENT ACCOUNTING

Management accounting is the process of identification, measurement, preparation, analyze, interpretation and communication of financial information used by management to take various decisions for the enterprise.

Management accounting provides necessary financial information to the managers and it is an aid to help managers take proper and effective decisions.

It provides information to all stakeholders of a company.

Management accounting has a wide scope, which includes cost accounting, financial accounting, budgetary control, inventory control etc.

Management accounting is a system of accounting that assists management in taking decisions.

Thus management accounting is an important branch of accounts that provides necessary information to the decision makers to make decisions for the company on behalf of its owners.

DEFINITION

“ Management Accounting is concerned with accounting information that is useful to management.”- Robert Anthony

“ Management Accounting is concerned with supplying financial data useful to management at all levels in managing and administering an enterprise.”- W.B. Meferland

MANAGERIAL DECISIONS

Make or Buy Dropping or Adding Product Line Purchase or Lease Selling Agents or Sales Force Product Mix Price Mix Promotion Mix

SCOPE

Financial Accounting Cost Accounting Budgetary Control Management Information System Capital Budgeting Statistical Techniques Data interpretation Reporting/Communication

EVOLUTION

The main aim of financial accounting is to know about the profitability and financial position of the firm and also to communicate the same to its stakeholders.

Financial accounting conveys meaningful information to the outsiders, but it fails to communicate valuable information to the management, in the absence of which, decision making becomes difficult.

With the evolution of joint stock companies, there is separation of ownership and management.

Hence management accounting evolved to help managers take decisions for the benefit of the company, based on the information provided by financial and cost accounts.

OBJECTIVES / FUNCTIONS

Planning and Policy Formulation Helps in decision making Helpful in reporting Controlling Assists in motivating

LIMITATIONS

Expensive Delays in Decisions Dependency on data Inaccuracy of information Evolutionary stage

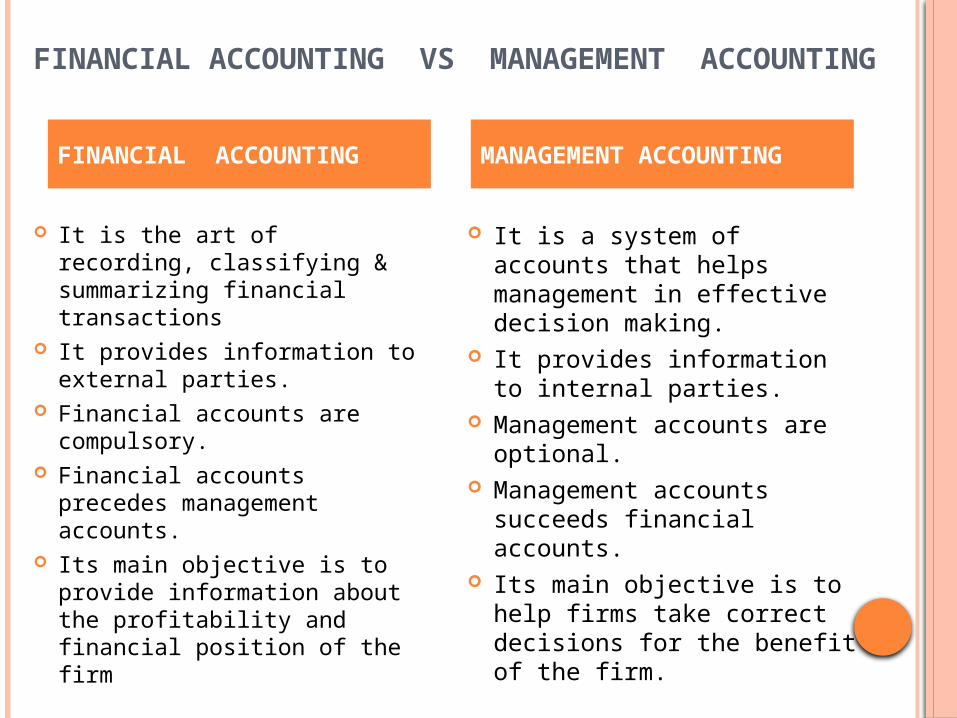

FINANCIAL ACCOUNTING VS MANAGEMENT ACCOUNTING

It is the art of recording, classifying & summarizing financial transactions

It provides information to external parties.

Financial accounts are compulsory.

Financial accounts precedes management accounts.

Its main objective is to provide information about the profitability and financial position of the firm

It is a system of accounts that helps management in effective decision making.

It provides information to internal parties.

Management accounts are optional.

Management accounts succeeds financial accounts.

Its main objective is to help firms take correct decisions for the benefit of the firm.

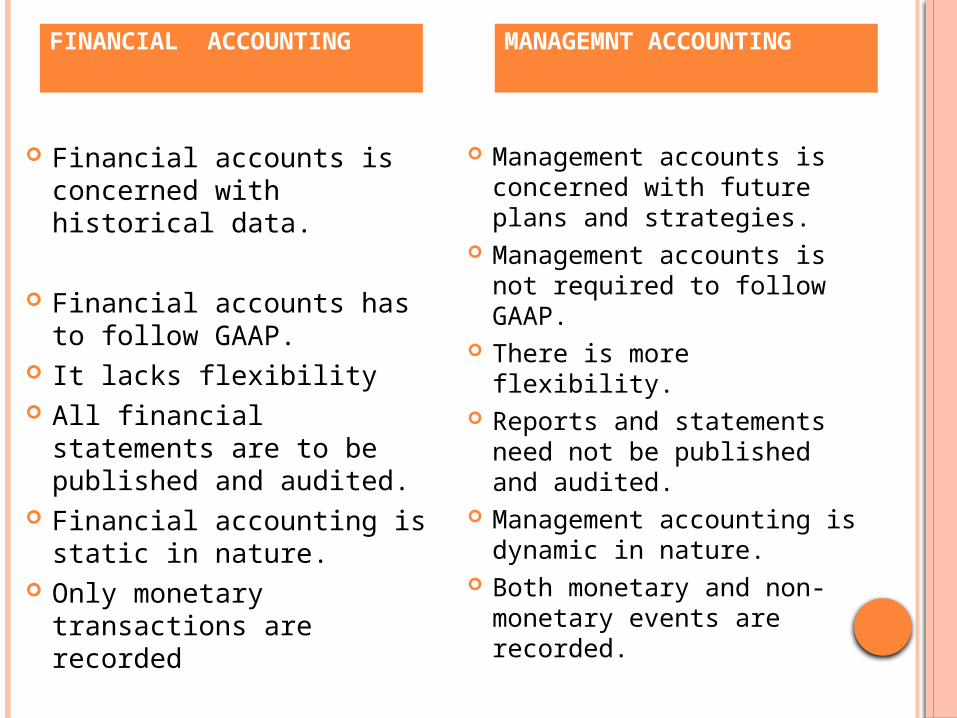

FINANCIAL ACCOUNTING MANAGEMENT ACCOUNTING

Financial accounts is concerned with historical data.

Financial accounts has to follow GAAP.

It lacks flexibility All financial statements are to

be published and audited. Financial accounting is static in

nature. Only monetary transactions are

recorded

Management accounts is concerned with future plans and strategies.

Management accounts is not required to follow GAAP.

There is more flexibility. Reports and statements need

not be published and audited. Management accounting is

dynamic in nature. Both monetary and non-

monetary events are recorded.

FINANCIAL ACCOUNTING MANAGEMNT ACCOUNTING

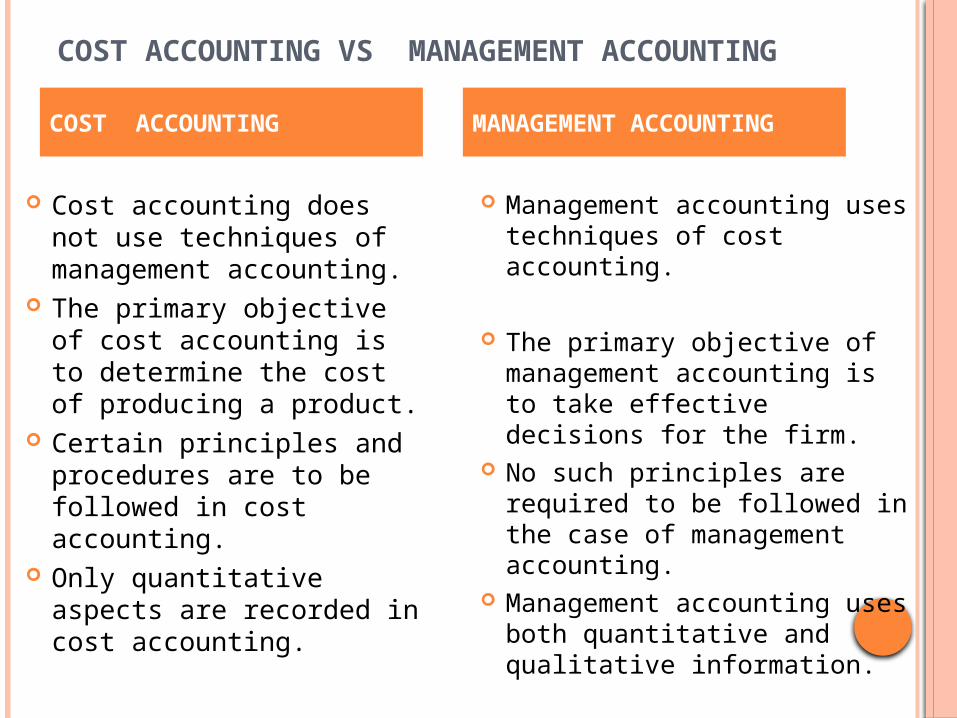

COST ACCOUNTING VS MANAGEMENT ACCOUNTING

Cost accounting does not use techniques of management accounting.

The primary objective of cost accounting is to determine the cost of producing a product.

Certain principles and procedures are to be followed in cost accounting.

Only quantitative aspects are recorded in cost accounting.

Management accounting uses techniques of cost accounting.

The primary objective of management accounting is to take effective decisions for the firm.

No such principles are required to be followed in the case of management accounting.

Management accounting uses both quantitative and qualitative information.

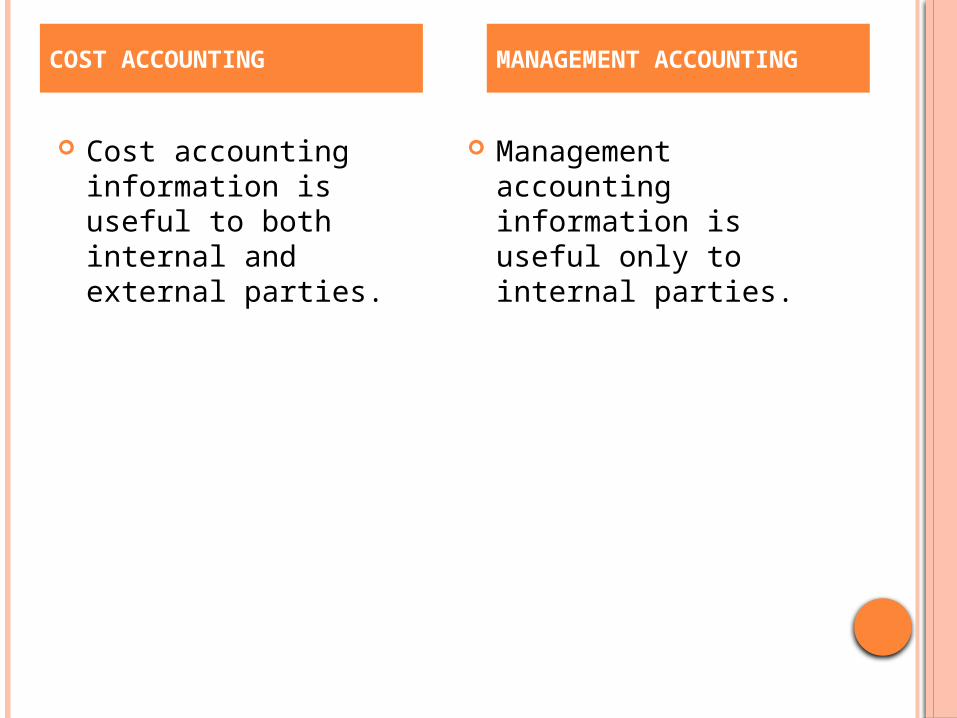

COST ACCOUNTING MANAGEMENT ACCOUNTING

Cost accounting information is useful to both internal and external parties.

Management accounting information is useful only to internal parties.

COST ACCOUNTING MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTANT

Management accountant is a person who is entrusted with management accounting.

He is also known as “Controller of accounts”. He plays a significant role in decision making in an

organization. He is responsible for installation, development &

efficient functioning of the management accounting system.

He plays an important role in gathering, compiling, reporting and interpreting accounting information.

He occupies a significant position in an organization.

ROLE OF MANAGEMENT ACCOUNTANT

The management accountant provides useful information for decision making.

He collects different data from various departments.

He helps measure actual performance with the budget.

He can help increase the efficiency of the business

He can help management chalk out future plan of action on the basis of past results.

He can also render valuable assistance in investment opportunities, expansion activities, working capital requirement, corporate planning etc.

RESPONSIBILITIES & DUTIES

The installation & interpretation of all accounting records of the company.

The preparation and interpretation of the financial statements of the company.

The compilation of production costs. The taking and costing of all physical inventories. Continuous audit of all accounts and records of the

company wherever located. The preparation and filing of tax returns. The maintenance of records of all contracts and

leases.

FUNCTIONS OF MANAGEMENT ACCOUNTANT

To establish, coordinate and administer an adequate plan for the control of operations.

To compare performance with standards and to report and interpret its results to all levels of management.

To administer tax policies and procedures. To supervise preparation of reports to Government

agencies. To assure protection of assets of the company

through internal control or insurance coverage. To provide regular information and updates to the

management on various issues, so as to help the management take timely and correct decisions.

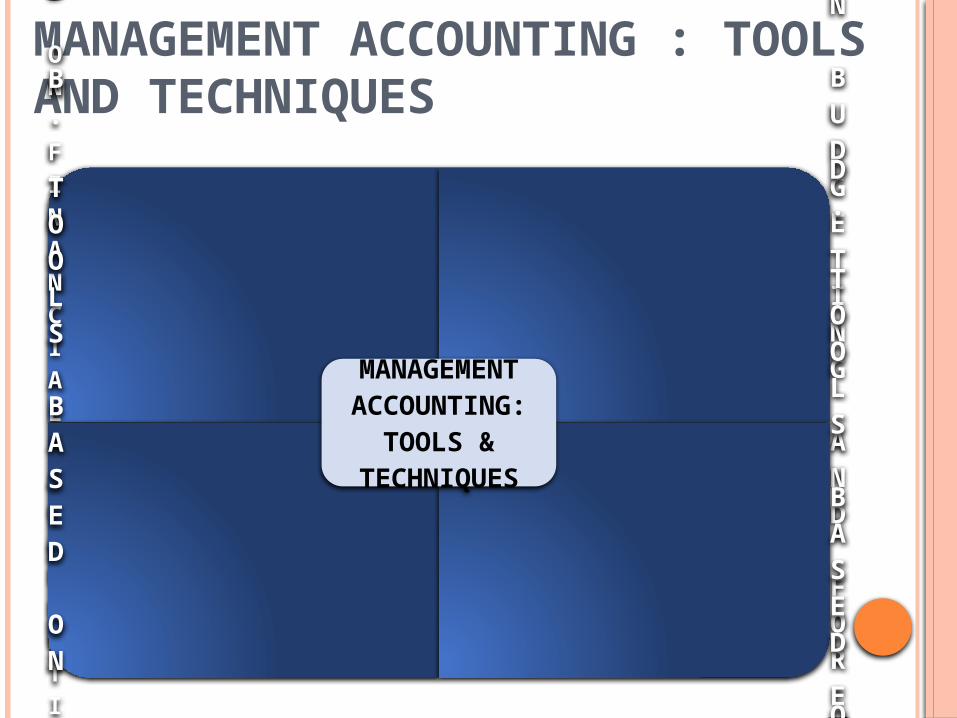

MANAGEMENT ACCOUNTING : TOOLS AND TECHNIQUES

A. TOOLS BASED ON FINANCIAL ACCOUNTING

C. TOOLS BASED ON BUDGETING AND FORECATING

B. TOOLS BASED ON COST ACCOUNTING

D. TOOLS BASED ON MATHEMATICS

MANAGEMENT ACCOUNTING:

TOOLS & TECHNIQUES

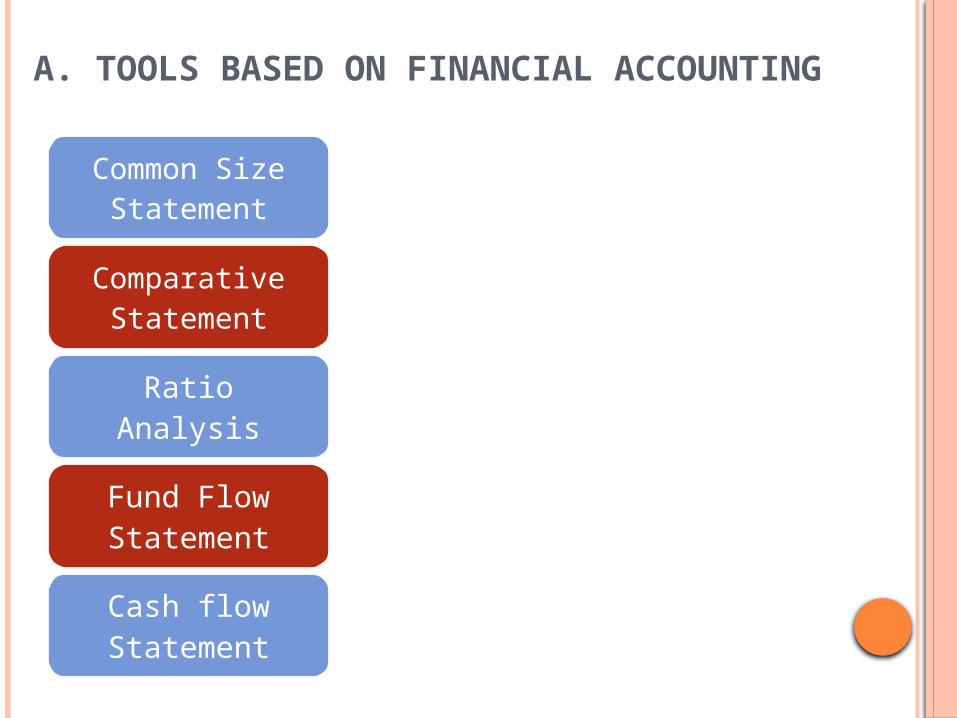

A. TOOLS BASED ON FINANCIAL ACCOUNTING

Common Size Statement

Comparative Statement

Ratio Analysis

Fund Flow Statement

Cash flow Statement

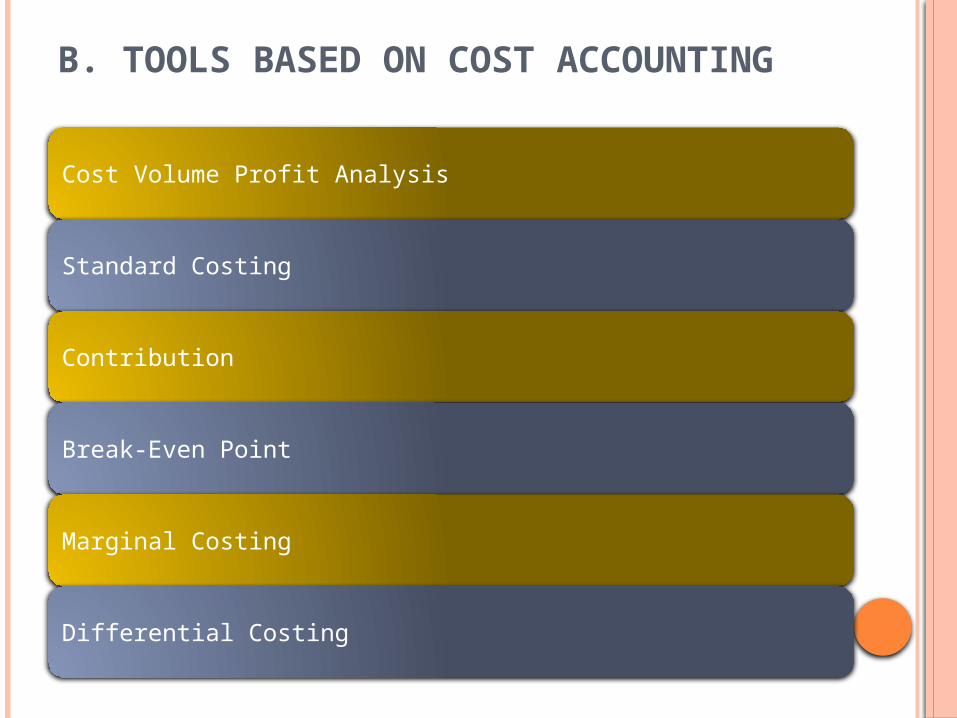

B. TOOLS BASED ON COST ACCOUNTING

Cost Volume Profit Analysis

Standard Costing

Contribution

Break-Even Point

Marginal Costing

Differential Costing

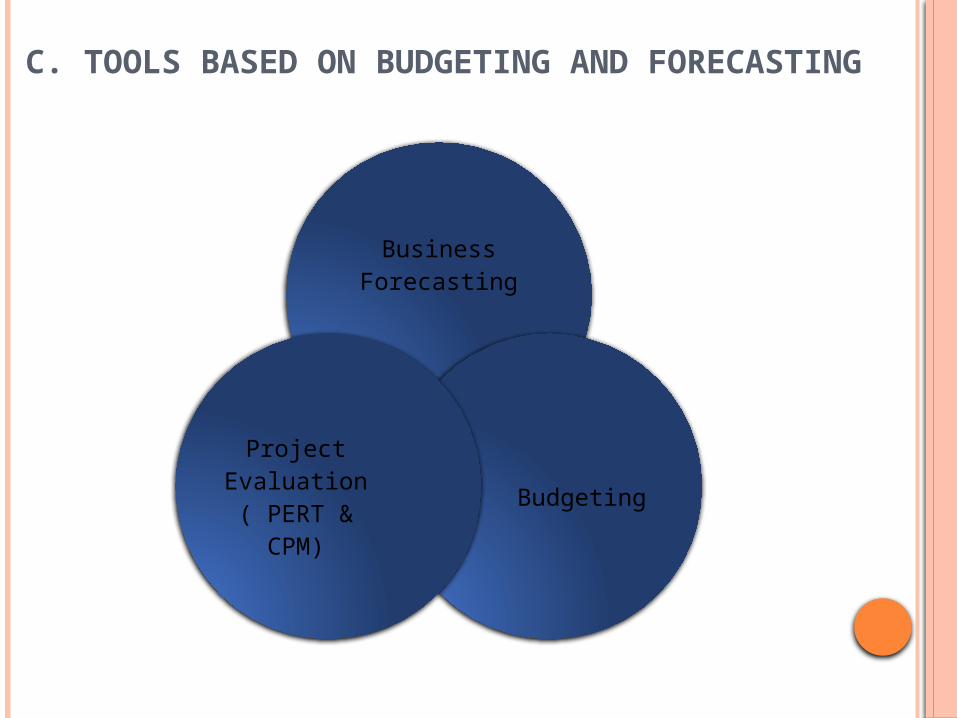

C. TOOLS BASED ON BUDGETING AND FORECASTING

Business Forecasting

Budgeting

Project Evaluation ( PERT &

CPM)

D. TOOLS BASED ON MATHEMATICS

Correlation Analysis

Regression Analysis

Time Series Analysis

Trend Analysis

Operations Research

Simulation Theory