international trends in wealth management international trends in wealth management market ......

TRANSCRIPT

Alain Picquet Partner

Copenhagen, 28 February 2013

International Trends in Wealth Management Market

1 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

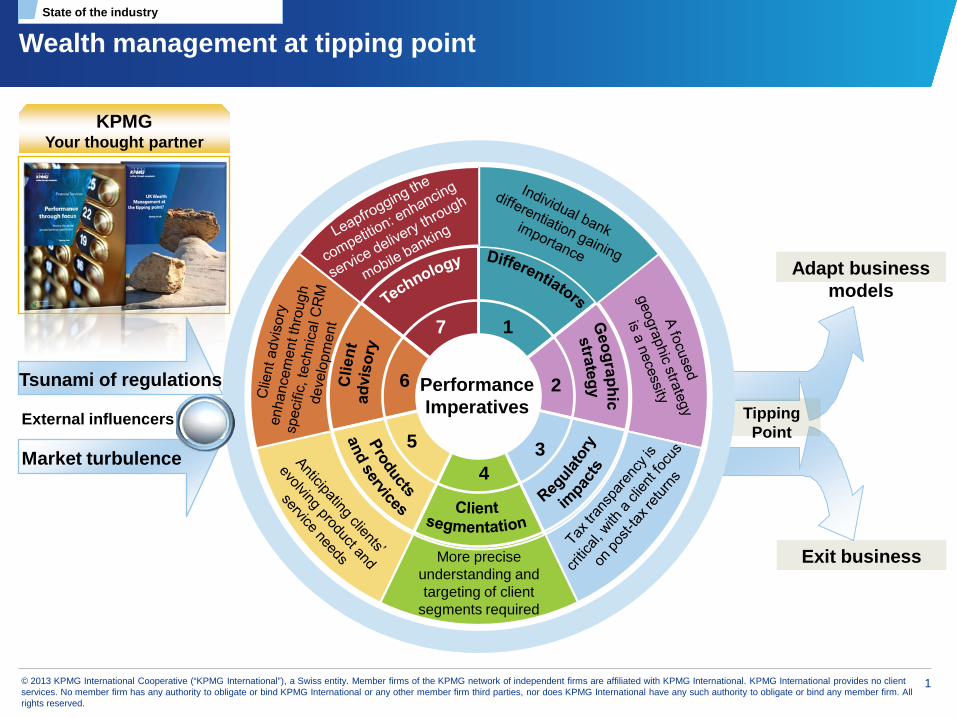

Wealth management at tipping point

Adapt business models

Exit business

Performance Imperatives Tipping

Point

Tsunami of regulations

Market turbulence

7 1

2

3 4

5

6

More precise understanding and targeting of client

segments required

Performance Imperatives

External influencers

KPMG Your thought partner

State of the industry

2 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

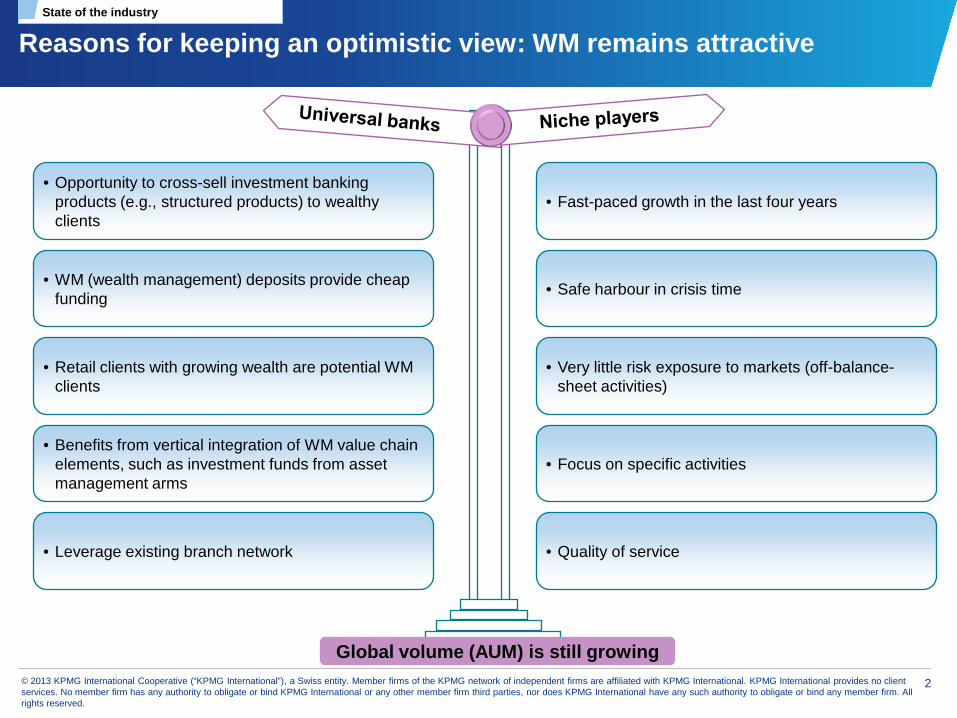

Reasons for keeping an optimistic view: WM remains attractive

• Opportunity to cross-sell investment banking products (e.g., structured products) to wealthy clients

• Benefits from vertical integration of WM value chain elements, such as investment funds from asset management arms

• Retail clients with growing wealth are potential WM clients

• WM (wealth management) deposits provide cheap funding

• Leverage existing branch network

• Fast-paced growth in the last four years

• Focus on specific activities

• Very little risk exposure to markets (off-balance-sheet activities)

• Safe harbour in crisis time

• Quality of service

Global volume (AUM) is still growing

State of the industry

3 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

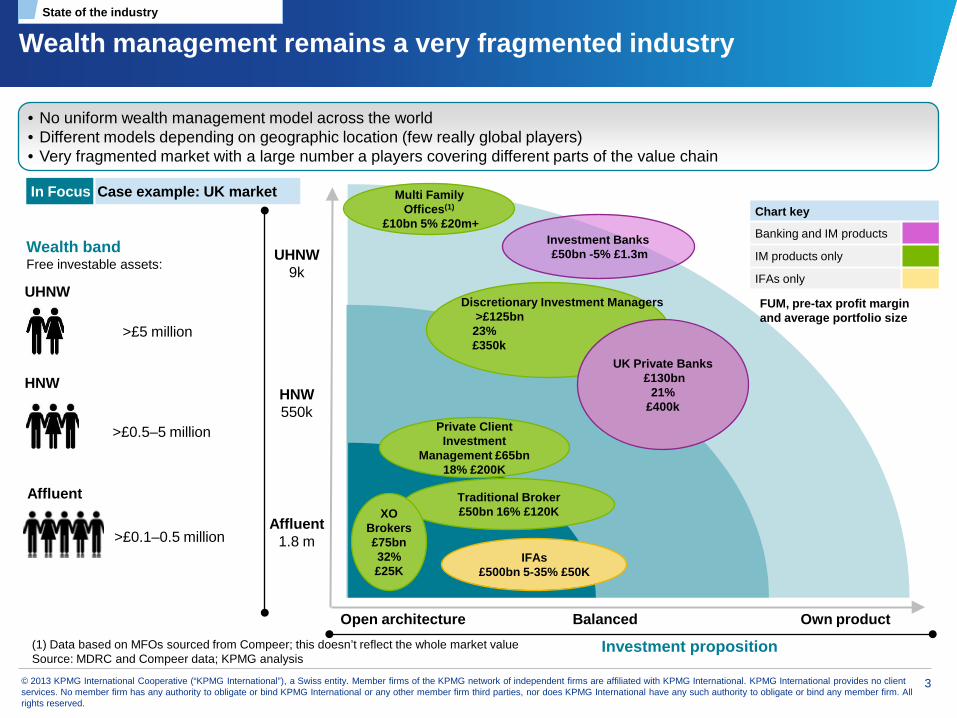

Wealth management remains a very fragmented industry

• No uniform wealth management model across the world • Different models depending on geographic location (few really global players) • Very fragmented market with a large number a players covering different parts of the value chain

Chart key

Banking and IM products

IM products only

IFAs only

Wealth band Free investable assets:

UHNW

>£5 million

>£0.5–5 million

>£0.1–0.5 million

Affluent

HNW

Balanced Open architecture Own product

Private Client Investment

Management £65bn 18% £200K

Traditional Broker £50bn 16% £120K

IFAs

£500bn 5-35% £50K

UK Private Banks £130bn

21% £400k

Investment Banks £50bn -5% £1.3m

XO Brokers

£75bn 32% £25K

Multi Family Offices(1)

£10bn 5% £20m+

UHNW 9k

HNW 550k

Affluent 1.8 m

Investment proposition

Discretionary Investment Managers >£125bn 23% £350k

FUM, pre-tax profit margin and average portfolio size

Case example: UK market In Focus

(1) Data based on MFOs sourced from Compeer; this doesn’t reflect the whole market value Source: MDRC and Compeer data; KPMG analysis

State of the industry

4 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

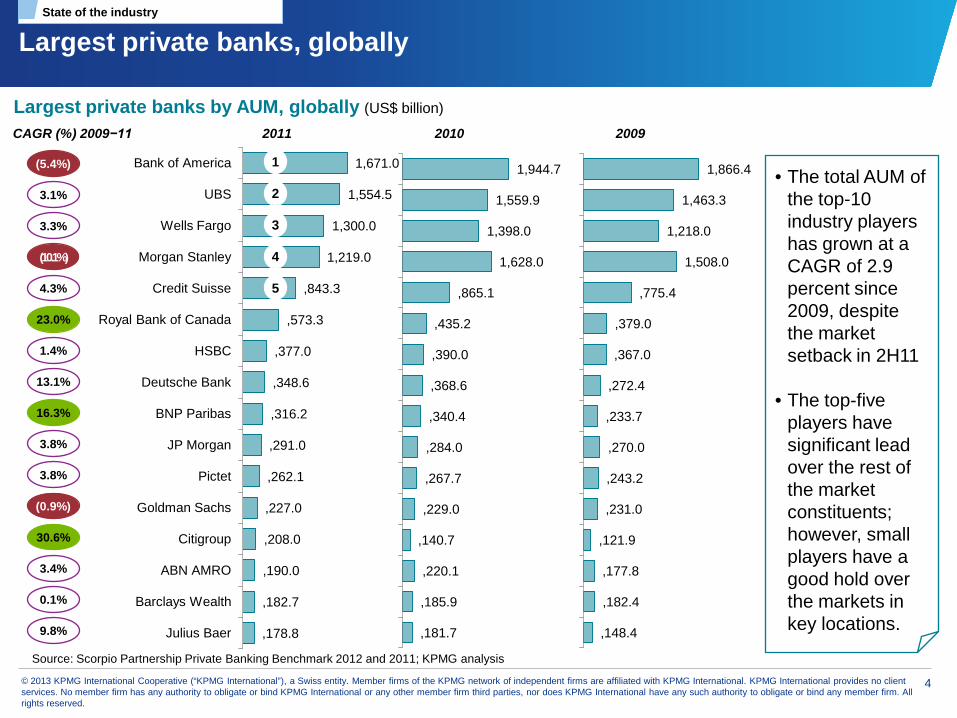

Largest private banks, globally

1,671.0

1,554.5

1,300.0

1,219.0

,843.3

,573.3

,377.0

,348.6

,316.2

,291.0

,262.1

,227.0

,208.0

,190.0

,182.7

,178.8

Bank of America

UBS

Wells Fargo

Morgan Stanley

Credit Suisse

Royal Bank of Canada

HSBC

Deutsche Bank

BNP Paribas

JP Morgan

Pictet

Goldman Sachs

Citigroup

ABN AMRO

Barclays Wealth

Julius Baer

(5.4%)

3.3%

(10.1%)

4.3%

23.0%

1.4%

13.1%

16.3%

3.8%

(0.9%)

30.6%

3.4%

0.1%

9.8%

3.8%

Largest private banks by AUM, globally (US$ billion) 2011 2010 2009 CAGR (%) 2009−11

1,944.7

1,559.9

1,398.0

1,628.0

,865.1

,435.2

,390.0

,368.6

,340.4

,284.0

,267.7

,229.0

,140.7

,220.1

,185.9

,181.7

1,866.4

1,463.3

1,218.0

1,508.0

,775.4

,379.0

,367.0

,272.4

,233.7

,270.0

,243.2

,231.0

,121.9

,177.8

,182.4

,148.4

3.1%

1

2

3

4

5

• The total AUM of the top-10 industry players has grown at a CAGR of 2.9 percent since 2009, despite the market setback in 2H11

• The top-five

players have significant lead over the rest of the market constituents; however, small players have a good hold over the markets in key locations.

Source: Scorpio Partnership Private Banking Benchmark 2012 and 2011; KPMG analysis

State of the industry

5 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Growth fuelled by emerging markets

1

Underlying trends impacting wealth management industry

Regulations to remain on the agenda

2

Changing business models for changing clients

3

IT and operations 7

Cost pressures/squeezed profitability

4

Consolidation of the industry

5

Geographical strategy/ cross-border banking

6

2013 and way forward

Pre crisis

Post crisis

Trends and key developments

Trends and imperatives

6 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

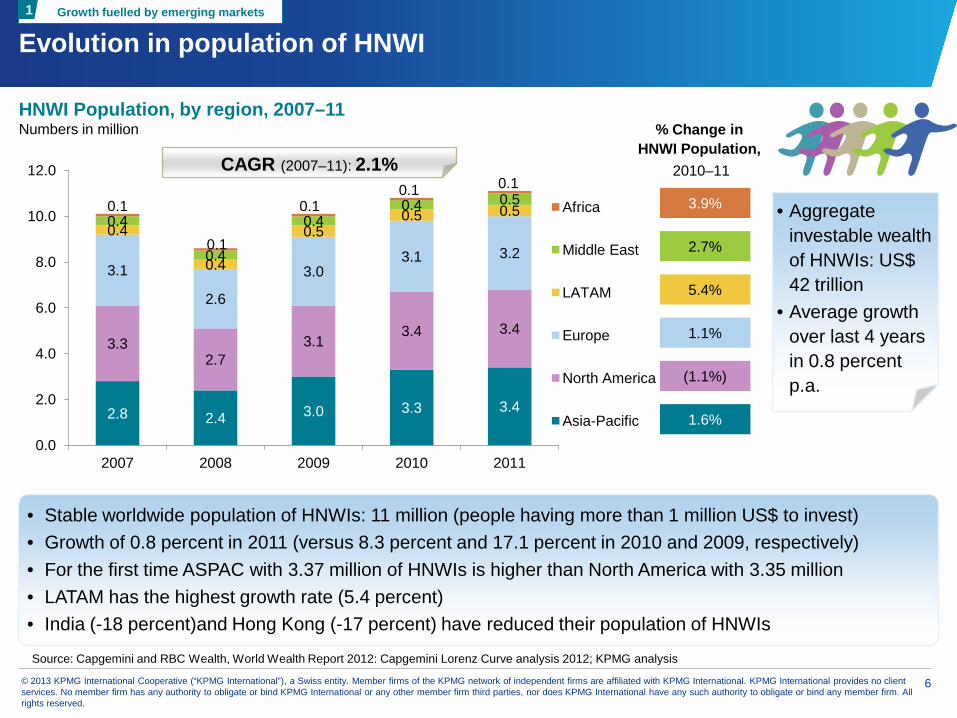

Evolution in population of HNWI Growth fuelled by emerging markets 1

2.8 2.4 3.0 3.3 3.4

3.3 2.7

3.1 3.4 3.4

3.1

2.6

3.0 3.1 3.2

0.4

0.4

0.5 0.5 0.5

0.4

0.4

0.4 0.4 0.5 0.1

0.1

0.1 0.1 0.1

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2007 2008 2009 2010 2011

Africa

Middle East

LATAM

Europe

North America

Asia-Pacific 1.6%

(1.1%)

1.1%

5.4%

2.7%

3.9%

% Change in HNWI Population,

2010–11

HNWI Population, by region, 2007–11 Numbers in million

CAGR (2007–11): 2.1%

• Stable worldwide population of HNWIs: 11 million (people having more than 1 million US$ to invest) • Growth of 0.8 percent in 2011 (versus 8.3 percent and 17.1 percent in 2010 and 2009, respectively) • For the first time ASPAC with 3.37 million of HNWIs is higher than North America with 3.35 million • LATAM has the highest growth rate (5.4 percent) • India (-18 percent)and Hong Kong (-17 percent) have reduced their population of HNWIs

• Aggregate investable wealth of HNWIs: US$ 42 trillion

• Average growth over last 4 years in 0.8 percent p.a.

Source: Capgemini and RBC Wealth, World Wealth Report 2012: Capgemini Lorenz Curve analysis 2012; KPMG analysis

7 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

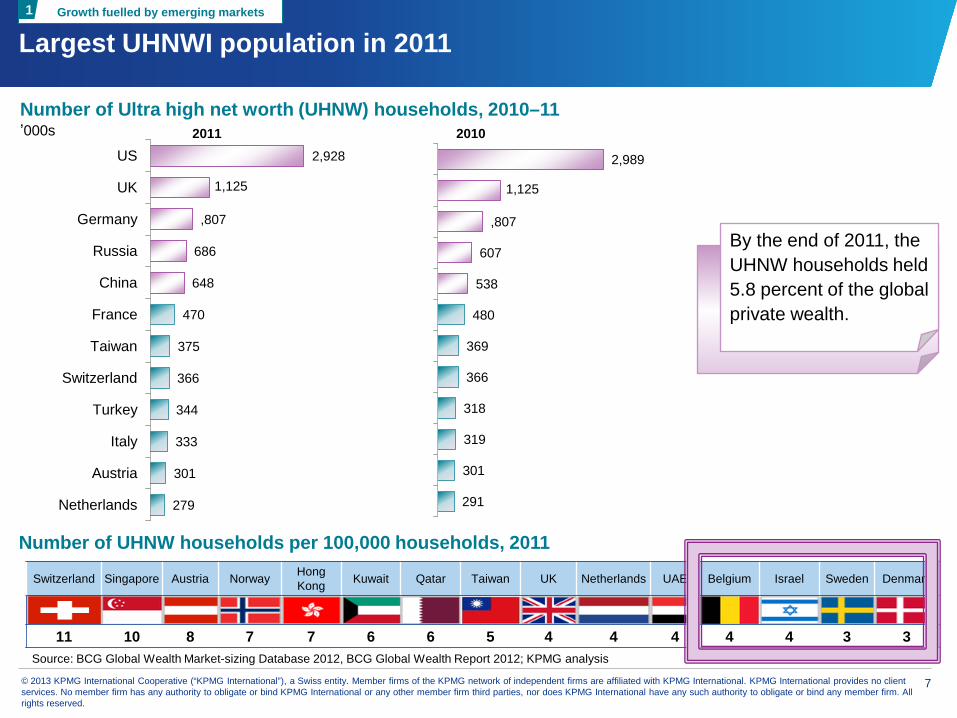

Largest UHNWI population in 2011

Number of Ultra high net worth (UHNW) households, 2010–11 ’000s

Number of UHNW households per 100,000 households, 2011

Switzerland Singapore Austria Norway Hong Kong Kuwait Qatar Taiwan UK Netherlands UAE Belgium Israel Sweden Denmark

11 10 8 7 7 6 6 5 4 4 4 4 4 3 3

2,928

1,125

,807

686

648

470

375

366

344

333

301

279

US

UK

Germany

Russia

China

France

Taiwan

Switzerland

Turkey

Italy

Austria

Netherlands

2,989

1,125

,807

607

538

480

369

366

318

319

301

291

2010 2011

Source: BCG Global Wealth Market-sizing Database 2012, BCG Global Wealth Report 2012; KPMG analysis

By the end of 2011, the UHNW households held 5.8 percent of the global private wealth.

Growth fuelled by emerging markets 1

8 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

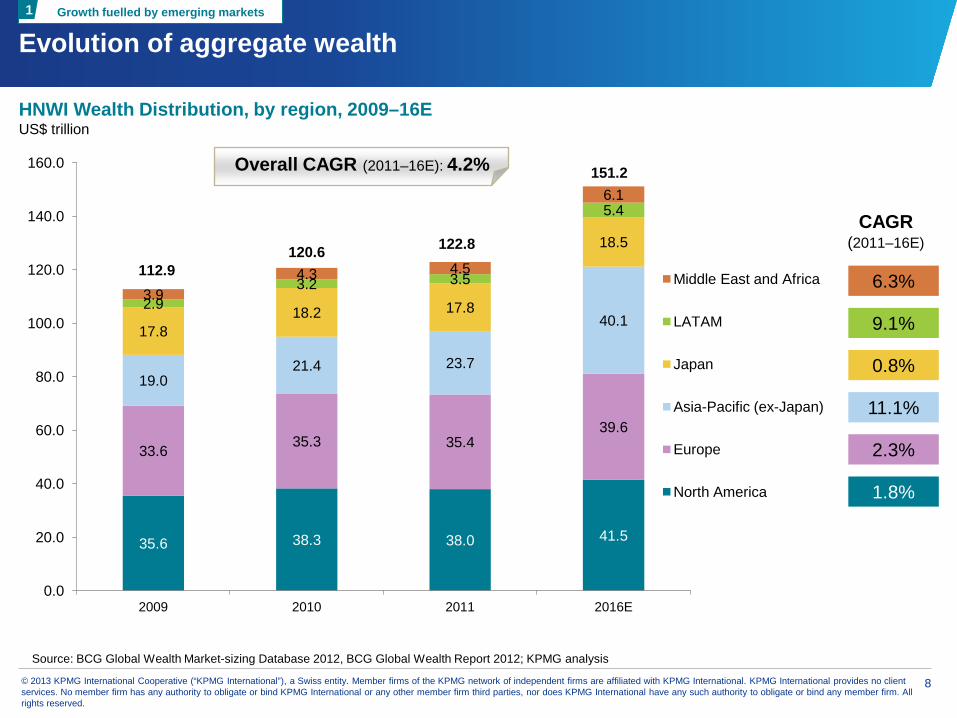

Evolution of aggregate wealth

35.6 38.3 38.0 41.5

33.6 35.3 35.4 39.6

19.0 21.4 23.7

40.1 17.8

18.2 17.8

18.5

2.9 3.2 3.5

5.4

3.9 4.3 4.5

6.1

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

2009 2010 2011 2016E

Middle East and Africa

LATAM

Japan

Asia-Pacific (ex-Japan)

Europe

North America

HNWI Wealth Distribution, by region, 2009–16E US$ trillion

1.8%

2.3%

11.1%

0.8%

9.1%

6.3%

CAGR (2011–16E)

Source: BCG Global Wealth Market-sizing Database 2012, BCG Global Wealth Report 2012; KPMG analysis

112.9 120.6 122.8

151.2 Overall CAGR (2011–16E): 4.2%

Growth fuelled by emerging markets 1

9 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

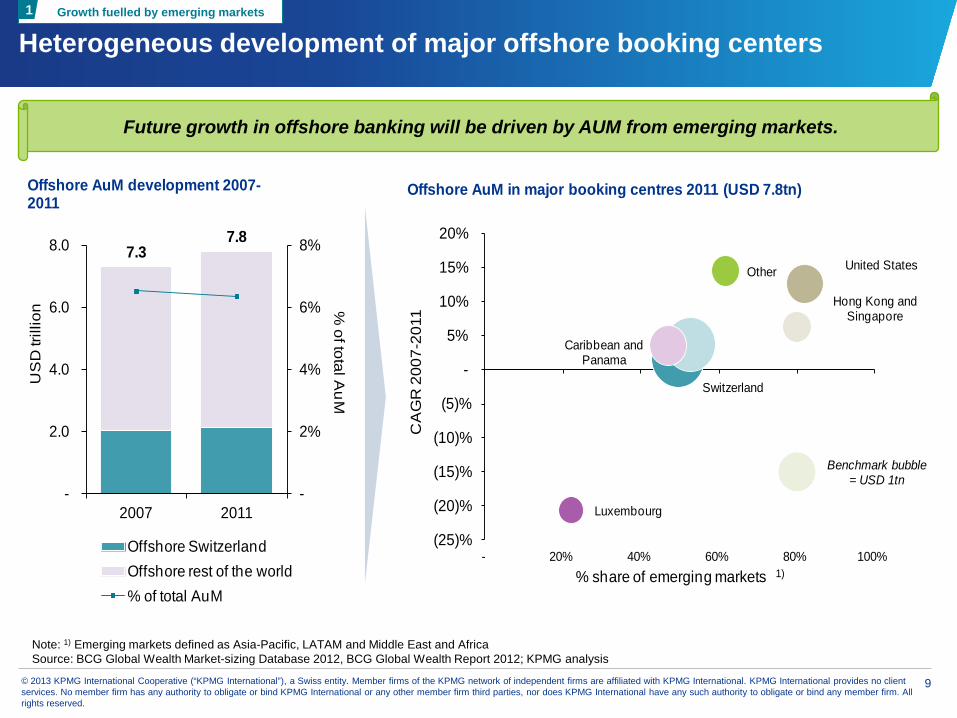

Heterogeneous development of major offshore booking centers Growth fuelled by emerging markets 1

7.37.8

-

2%

4%

6%

8%

-

2.0

4.0

6.0

8.0

2007 2011

% of total A

uM

US

D tr

illio

n

Offshore AuM development 2007-2011

Offshore SwitzerlandOffshore rest of the world% of total AuM

Switzerland

Caribbean and Panama

Luxembourg

Hong Kong and Singapore

United StatesOther

Benchmark bubble = USD 1tn

(25)%

(20)%

(15)%

(10)%

(5)%

-

5%

10%

15%

20%

- 20% 40% 60% 80% 100%

CA

GR

200

7-20

11

% share of emerging markets 1)

Offshore AuM in major booking centres 2011 (USD 7.8tn)

Future growth in offshore banking will be driven by AUM from emerging markets.

Note: 1) Emerging markets defined as Asia-Pacific, LATAM and Middle East and Africa Source: BCG Global Wealth Market-sizing Database 2012, BCG Global Wealth Report 2012; KPMG analysis

10 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

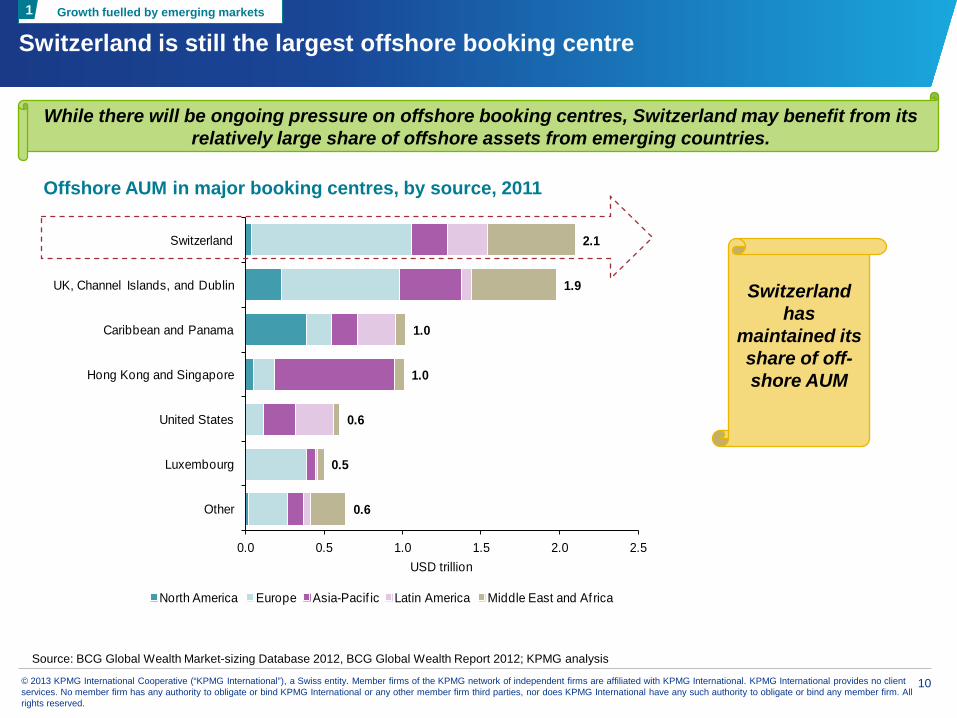

While there will be ongoing pressure on offshore booking centres, Switzerland may benefit from its relatively large share of offshore assets from emerging countries.

Switzerland is still the largest offshore booking centre

0.6

0.5

0.6

1.0

1.0

1.9

2.1

0.0 0.5 1.0 1.5 2.0 2.5

Other

Luxembourg

United States

Hong Kong and Singapore

Caribbean and Panama

UK, Channel Islands, and Dublin

Switzerland

USD trillion

North America Europe Asia-Pacif ic Latin America Middle East and Africa

Offshore AUM in major booking centres, by source, 2011

Switzerland has

maintained its share of off-shore AUM

Growth fuelled by emerging markets 1

Source: BCG Global Wealth Market-sizing Database 2012, BCG Global Wealth Report 2012; KPMG analysis

11 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

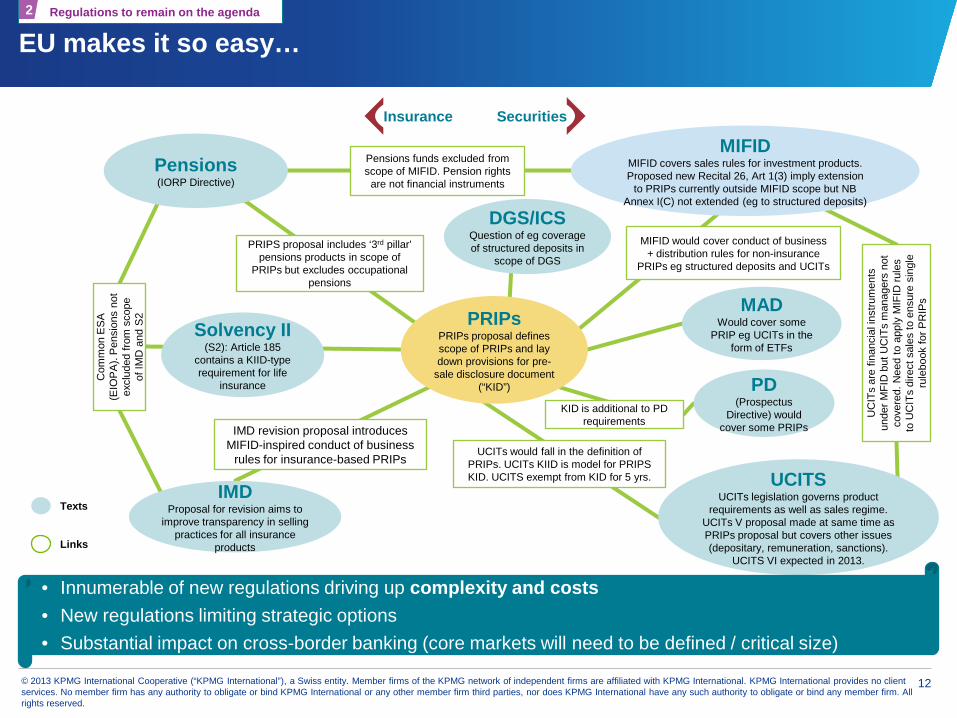

EU makes it so easy… Regulations to remain on the agenda 2

12 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

EU makes it so easy… Regulations to remain on the agenda 2

Insurance Securities

Pensions (IORP Directive)

IMD Proposal for revision aims to

improve transparency in selling practices for all insurance

products

PD (Prospectus

Directive) would cover some PRIPs

MAD Would cover some

PRIP eg UCITs in the form of ETFs

Com

mon

ES

A

(EIO

PA

). P

ensi

ons

not

excl

uded

from

sco

pe

of IM

D a

nd S

2

UC

ITs

are

finan

cial

inst

rum

ents

un

der M

FID

but

UC

ITs

man

ager

s no

t co

vere

d. N

eed

to a

pply

MIF

ID ru

les

to U

CIT

s di

rect

sal

es to

ens

ure

sing

le

rule

book

for P

RIP

s

IMD revision proposal introduces MIFID-inspired conduct of business

rules for insurance-based PRIPs

Solvency II (S2): Article 185

contains a KIID-type requirement for life

insurance

DGS/ICS Question of eg coverage of structured deposits in

scope of DGS

MIFID MIFID covers sales rules for investment products. Proposed new Recital 26, Art 1(3) imply extension

to PRIPs currently outside MIFID scope but NB Annex I(C) not extended (eg to structured deposits)

PRIPs PRIPs proposal defines scope of PRIPs and lay down provisions for pre-

sale disclosure document (“KID”)

UCITS UCITs legislation governs product

requirements as well as sales regime. UCITs V proposal made at same time as PRIPs proposal but covers other issues (depositary, remuneration, sanctions).

UCITS VI expected in 2013.

UCITs would fall in the definition of PRIPs. UCITs KIID is model for PRIPS KID. UCITS exempt from KID for 5 yrs.

MIFID would cover conduct of business + distribution rules for non-insurance

PRIPs eg structured deposits and UCITs

PRIPS proposal includes ‘3rd pillar’ pensions products in scope of

PRIPs but excludes occupational pensions

KID is additional to PD requirements

Texts

Links

Pensions funds excluded from scope of MIFID. Pension rights

are not financial instruments

• Innumerable of new regulations driving up complexity and costs • New regulations limiting strategic options • Substantial impact on cross-border banking (core markets will need to be defined / critical size)

13 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

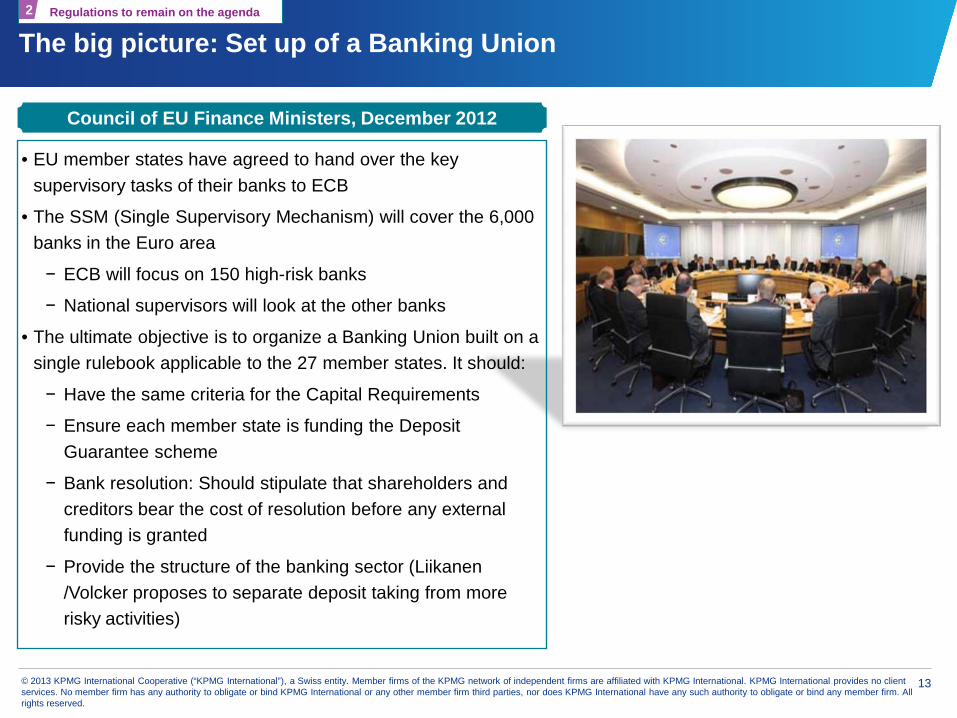

The big picture: Set up of a Banking Union

• EU member states have agreed to hand over the key supervisory tasks of their banks to ECB

• The SSM (Single Supervisory Mechanism) will cover the 6,000 banks in the Euro area

− ECB will focus on 150 high-risk banks

− National supervisors will look at the other banks

• The ultimate objective is to organize a Banking Union built on a single rulebook applicable to the 27 member states. It should:

− Have the same criteria for the Capital Requirements

− Ensure each member state is funding the Deposit Guarantee scheme

− Bank resolution: Should stipulate that shareholders and creditors bear the cost of resolution before any external funding is granted

− Provide the structure of the banking sector (Liikanen /Volcker proposes to separate deposit taking from more risky activities)

Regulations to remain on the agenda 2

Council of EU Finance Ministers, December 2012

14 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

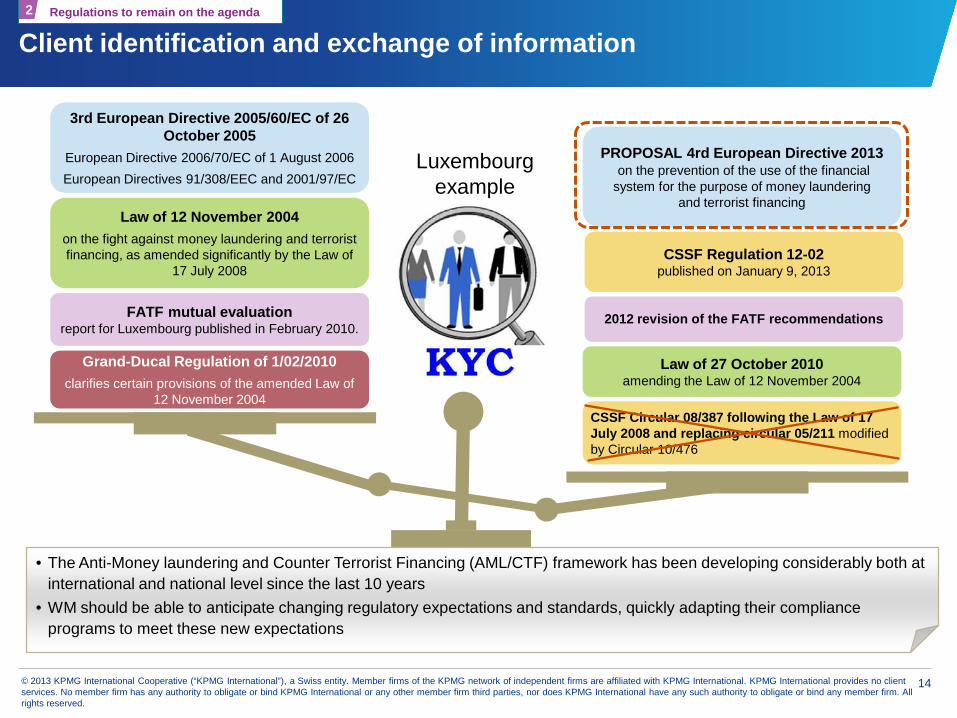

Client identification and exchange of information

Grand-Ducal Regulation of 1/02/2010 clarifies certain provisions of the amended Law of

12 November 2004

FATF mutual evaluation report for Luxembourg published in February 2010.

Law of 12 November 2004 on the fight against money laundering and terrorist financing, as amended significantly by the Law of

17 July 2008

3rd European Directive 2005/60/EC of 26 October 2005

European Directive 2006/70/EC of 1 August 2006 European Directives 91/308/EEC and 2001/97/EC

CSSF Circular 08/387 following the Law of 17 July 2008 and replacing circular 05/211 modified by Circular 10/476

Law of 27 October 2010 amending the Law of 12 November 2004

2012 revision of the FATF recommendations

PROPOSAL 4rd European Directive 2013 on the prevention of the use of the financial system for the purpose of money laundering

and terrorist financing

CSSF Regulation 12-02 published on January 9, 2013

• The Anti-Money laundering and Counter Terrorist Financing (AML/CTF) framework has been developing considerably both at international and national level since the last 10 years

• WM should be able to anticipate changing regulatory expectations and standards, quickly adapting their compliance programs to meet these new expectations

Regulations to remain on the agenda 2

Luxembourg example

15 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Client identification and exchange of information

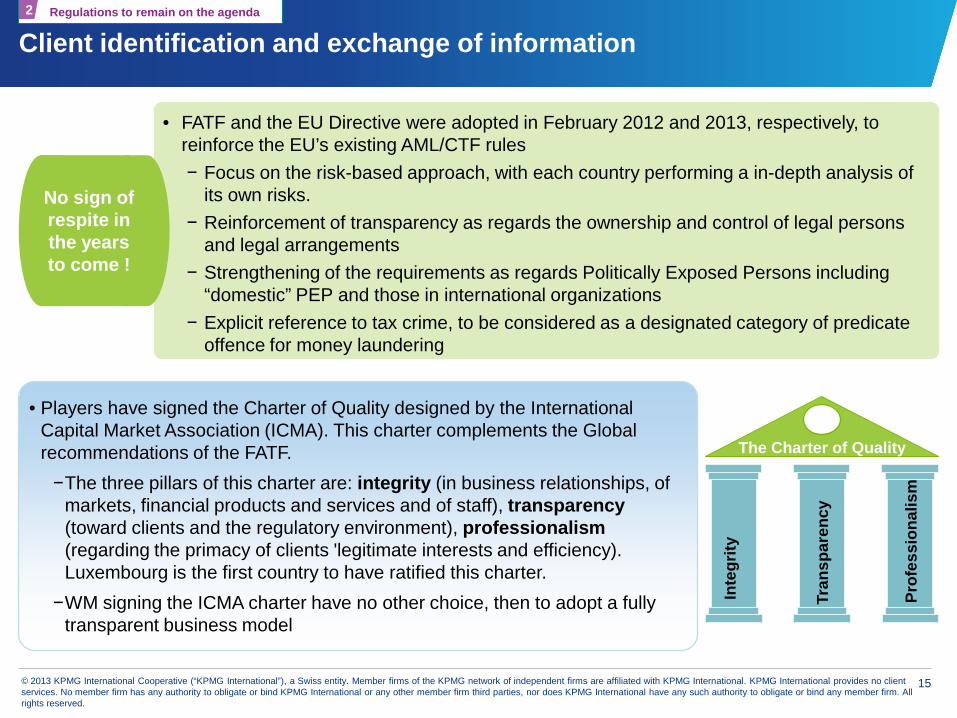

• Players have signed the Charter of Quality designed by the International Capital Market Association (ICMA). This charter complements the Global recommendations of the FATF.

−The three pillars of this charter are: integrity (in business relationships, of markets, financial products and services and of staff), transparency (toward clients and the regulatory environment), professionalism (regarding the primacy of clients 'legitimate interests and efficiency). Luxembourg is the first country to have ratified this charter.

−WM signing the ICMA charter have no other choice, then to adopt a fully transparent business model

The Charter of Quality

Inte

grity

Tran

spar

ency

Prof

essi

onal

ism

Regulations to remain on the agenda 2

• FATF and the EU Directive were adopted in February 2012 and 2013, respectively, to reinforce the EU’s existing AML/CTF rules − Focus on the risk-based approach, with each country performing a in-depth analysis of

its own risks. − Reinforcement of transparency as regards the ownership and control of legal persons

and legal arrangements − Strengthening of the requirements as regards Politically Exposed Persons including

“domestic” PEP and those in international organizations − Explicit reference to tax crime, to be considered as a designated category of predicate

offence for money laundering

No sign of respite in the years to come !

16 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Impact on the industry

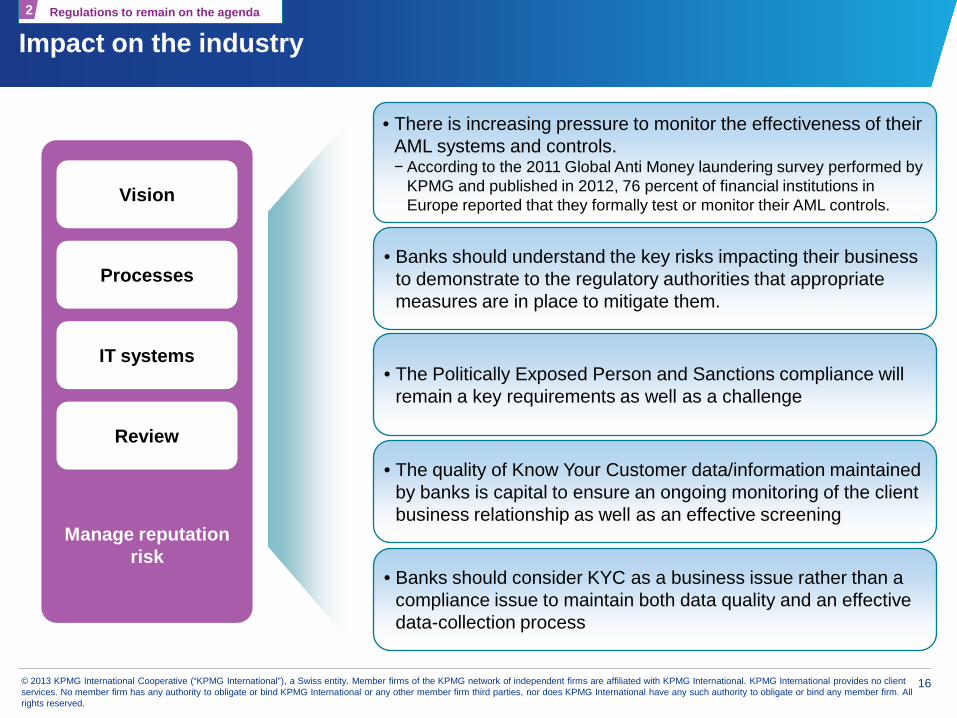

• There is increasing pressure to monitor the effectiveness of their AML systems and controls. − According to the 2011 Global Anti Money laundering survey performed by

KPMG and published in 2012, 76 percent of financial institutions in Europe reported that they formally test or monitor their AML controls.

• The quality of Know Your Customer data/information maintained by banks is capital to ensure an ongoing monitoring of the client business relationship as well as an effective screening

• The Politically Exposed Person and Sanctions compliance will remain a key requirements as well as a challenge

• Banks should understand the key risks impacting their business to demonstrate to the regulatory authorities that appropriate measures are in place to mitigate them.

• Banks should consider KYC as a business issue rather than a compliance issue to maintain both data quality and an effective data-collection process

Vision

Processes

IT systems

Review

Manage reputation risk

Regulations to remain on the agenda 2

17 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

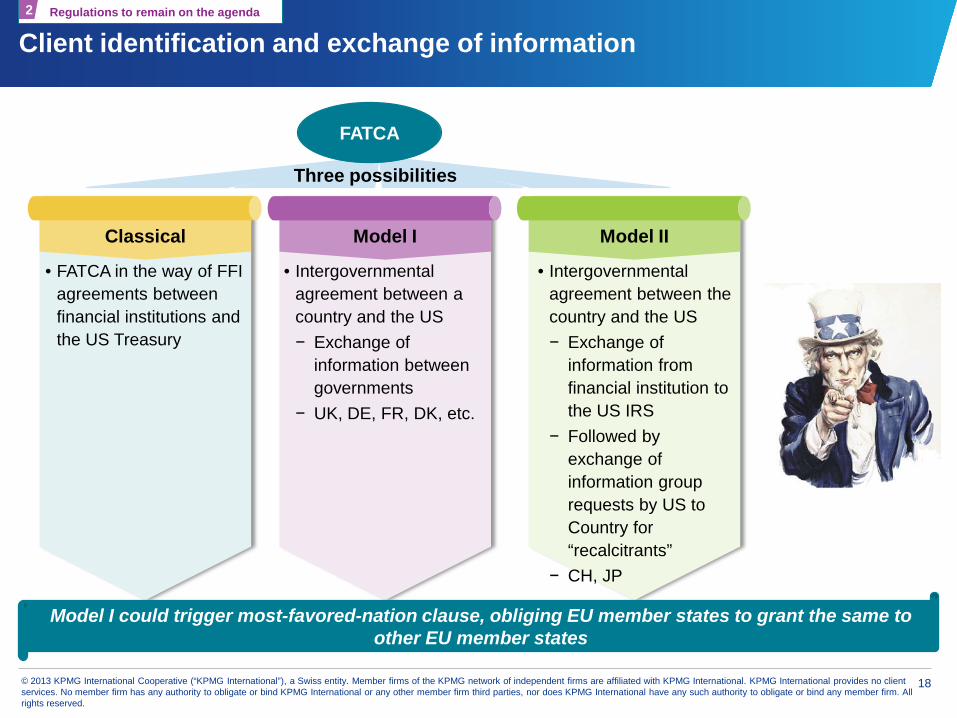

Client identification and exchange of information Regulations to remain on the agenda 2

• Landscape has changed dramatically since 2009 − Classical banking secrecy countries have concluded

agreements permitting exchange of information on demand

− Update of EU Savings Directive

• The US: “muscling their way through” − UBS and Bank Wegelin affairs in CH

− FATCA

• Swiss “Rubik” agreements − UK + Austria → signed

− Germany → failed

− Future → uncertain

Banking secrecy vs. automatic exchange of information

18 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Client identification and exchange of information Regulations to remain on the agenda 2

Classical

• FATCA in the way of FFI agreements between financial institutions and the US Treasury

Model I Model II

• Intergovernmental agreement between a country and the US − Exchange of

information between governments

− UK, DE, FR, DK, etc.

• Intergovernmental agreement between the country and the US − Exchange of

information from financial institution to the US IRS

− Followed by exchange of information group requests by US to Country for “recalcitrants”

− CH, JP

Three possibilities

Model I could trigger most-favored-nation clause, obliging EU member states to grant the same to other EU member states

FATCA

19 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

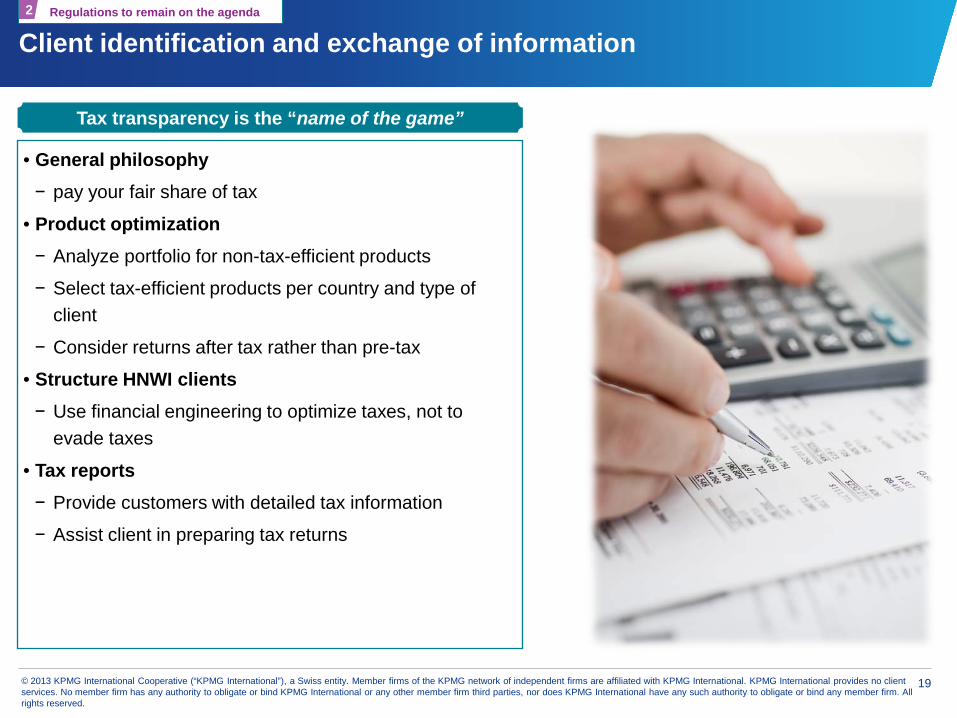

Client identification and exchange of information Regulations to remain on the agenda 2

• General philosophy − pay your fair share of tax

• Product optimization − Analyze portfolio for non-tax-efficient products

− Select tax-efficient products per country and type of client

− Consider returns after tax rather than pre-tax

• Structure HNWI clients − Use financial engineering to optimize taxes, not to

evade taxes

• Tax reports − Provide customers with detailed tax information

− Assist client in preparing tax returns

Tax transparency is the “name of the game”

20 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

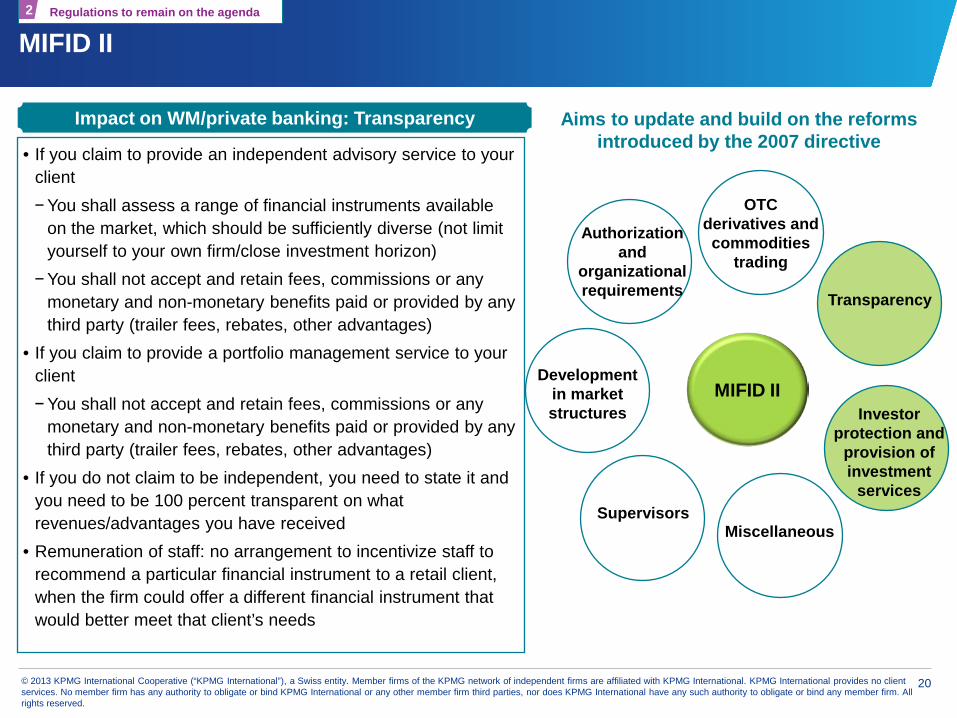

MIFID II Regulations to remain on the agenda 2

• If you claim to provide an independent advisory service to your client − You shall assess a range of financial instruments available

on the market, which should be sufficiently diverse (not limit yourself to your own firm/close investment horizon)

− You shall not accept and retain fees, commissions or any monetary and non-monetary benefits paid or provided by any third party (trailer fees, rebates, other advantages)

• If you claim to provide a portfolio management service to your client − You shall not accept and retain fees, commissions or any

monetary and non-monetary benefits paid or provided by any third party (trailer fees, rebates, other advantages)

• If you do not claim to be independent, you need to state it and you need to be 100 percent transparent on what revenues/advantages you have received

• Remuneration of staff: no arrangement to incentivize staff to recommend a particular financial instrument to a retail client, when the firm could offer a different financial instrument that would better meet that client’s needs

Impact on WM/private banking: Transparency

MIFID II

OTC derivatives and commodities

trading

Investor protection and

provision of investment

services

Transparency

Miscellaneous Supervisors

Authorization and

organizational requirements

Development in market structures

Aims to update and build on the reforms introduced by the 2007 directive

21 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

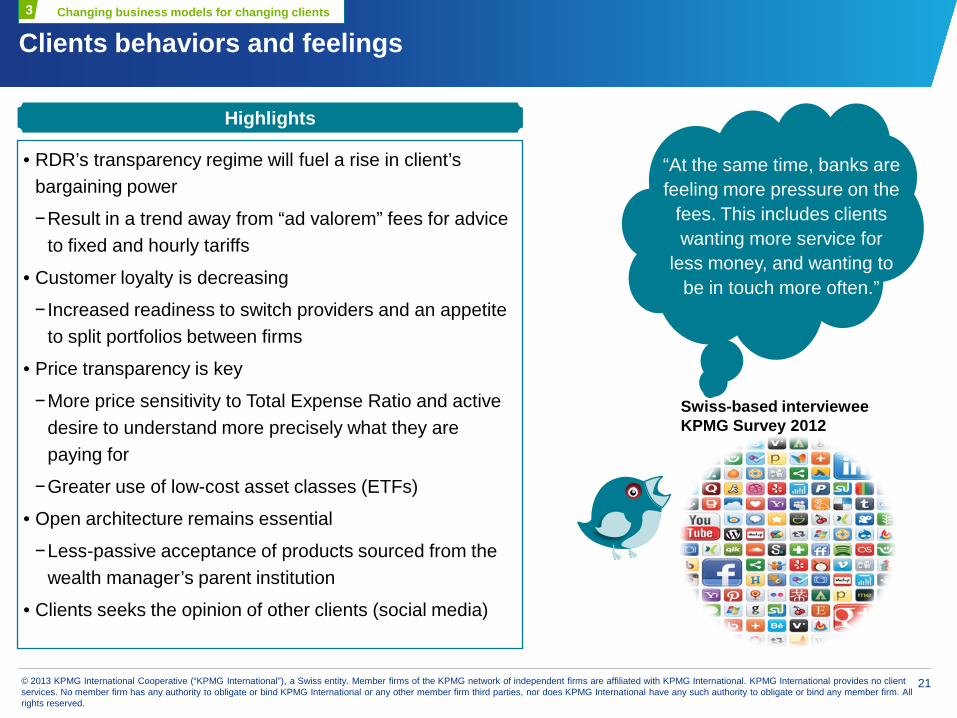

Clients behaviors and feelings Changing business models for changing clients 3

“At the same time, banks are feeling more pressure on the

fees. This includes clients wanting more service for

less money, and wanting to be in touch more often.”

Swiss-based interviewee KPMG Survey 2012

• RDR’s transparency regime will fuel a rise in client’s bargaining power

−Result in a trend away from “ad valorem” fees for advice to fixed and hourly tariffs

• Customer loyalty is decreasing

− Increased readiness to switch providers and an appetite to split portfolios between firms

• Price transparency is key

−More price sensitivity to Total Expense Ratio and active desire to understand more precisely what they are paying for

−Greater use of low-cost asset classes (ETFs)

• Open architecture remains essential

−Less-passive acceptance of products sourced from the wealth manager’s parent institution

• Clients seeks the opinion of other clients (social media)

Highlights

22 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

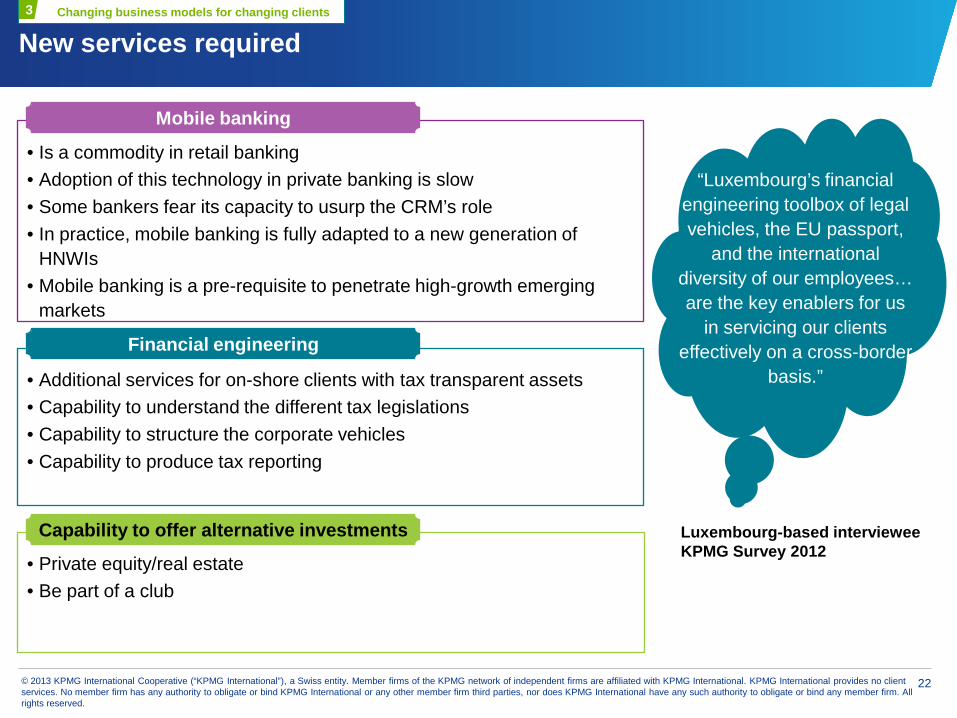

New services required

“Luxembourg’s financial engineering toolbox of legal vehicles, the EU passport,

and the international diversity of our employees… are the key enablers for us

in servicing our clients effectively on a cross-border

basis.”

Luxembourg-based interviewee KPMG Survey 2012

• Is a commodity in retail banking • Adoption of this technology in private banking is slow • Some bankers fear its capacity to usurp the CRM’s role • In practice, mobile banking is fully adapted to a new generation of

HNWIs • Mobile banking is a pre-requisite to penetrate high-growth emerging

markets

Mobile banking

• Additional services for on-shore clients with tax transparent assets • Capability to understand the different tax legislations • Capability to structure the corporate vehicles • Capability to produce tax reporting

Financial engineering

• Private equity/real estate • Be part of a club

Capability to offer alternative investments

Changing business models for changing clients 3

23 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

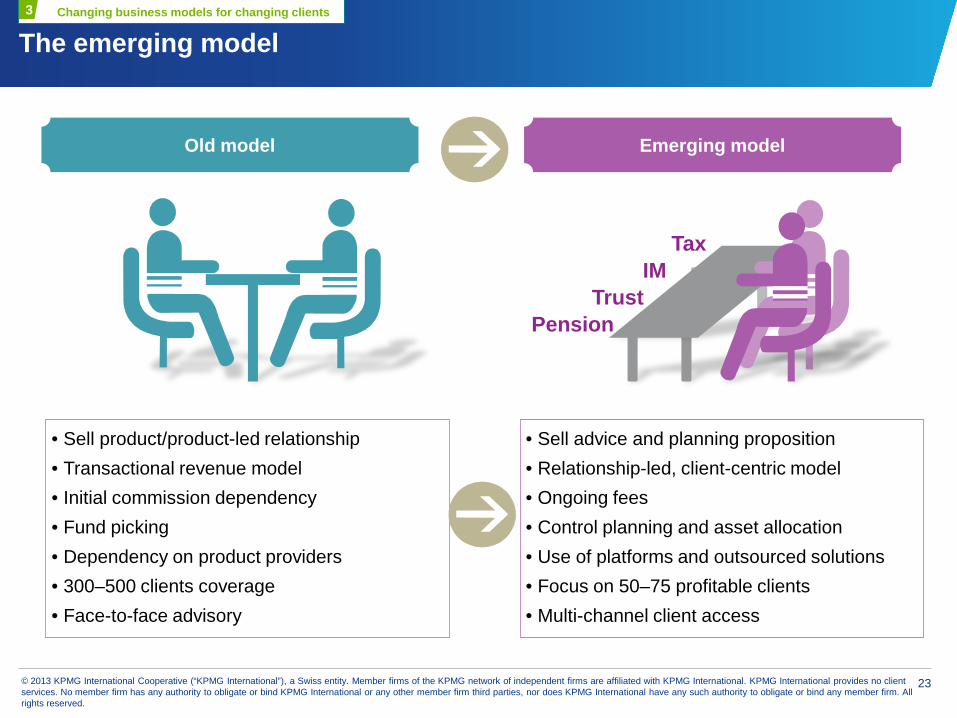

Tax IM

Trust Pension

• Sell advice and planning proposition • Relationship-led, client-centric model • Ongoing fees • Control planning and asset allocation • Use of platforms and outsourced solutions • Focus on 50–75 profitable clients • Multi-channel client access

• Sell product/product-led relationship • Transactional revenue model • Initial commission dependency • Fund picking • Dependency on product providers • 300–500 clients coverage • Face-to-face advisory

The emerging model

Old model Emerging model

Changing business models for changing clients 3

24 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

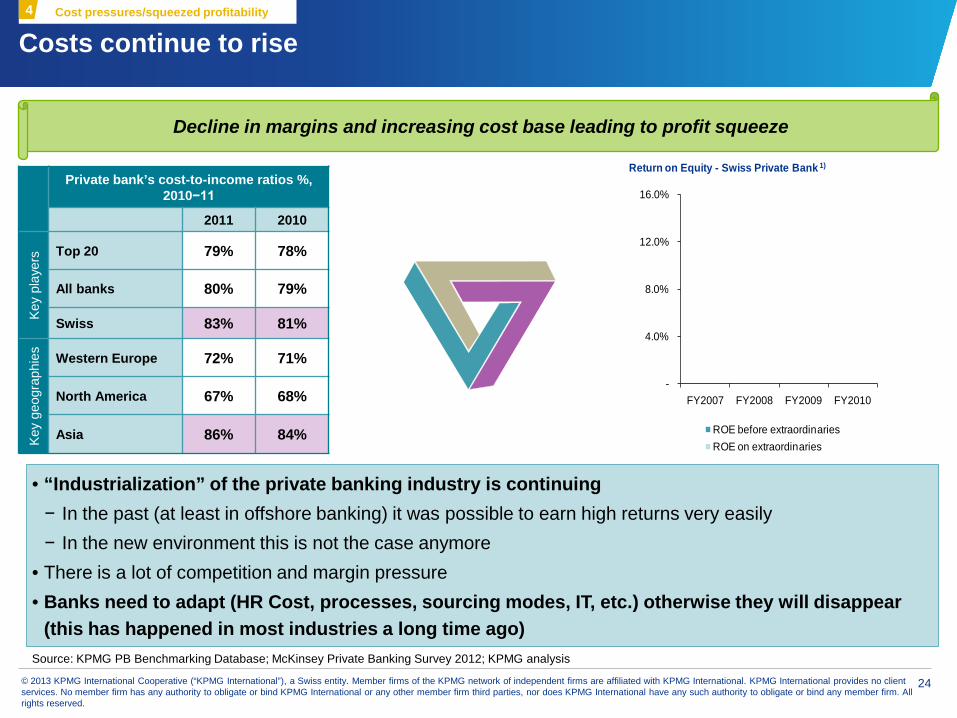

Costs continue to rise

-

4.0%

8.0%

12.0%

16.0%

FY2007 FY2008 FY2009 FY2010

Return on Equity - Swiss Private Bank 1)

ROE before extraordinariesROE on extraordinaries

Private bank’s cost-to-income ratios %, 2010−11

2011 2010

Key

play

ers Top 20 79% 78%

All banks 80% 79%

Swiss 83% 81%

Key

geog

raph

ies

Western Europe 72% 71%

North America 67% 68%

Asia 86% 84%

Decline in margins and increasing cost base leading to profit squeeze

Cost pressures/squeezed profitability 4

Source: KPMG PB Benchmarking Database; McKinsey Private Banking Survey 2012; KPMG analysis

• “Industrialization” of the private banking industry is continuing − In the past (at least in offshore banking) it was possible to earn high returns very easily − In the new environment this is not the case anymore

• There is a lot of competition and margin pressure • Banks need to adapt (HR Cost, processes, sourcing modes, IT, etc.) otherwise they will disappear

(this has happened in most industries a long time ago)

25 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

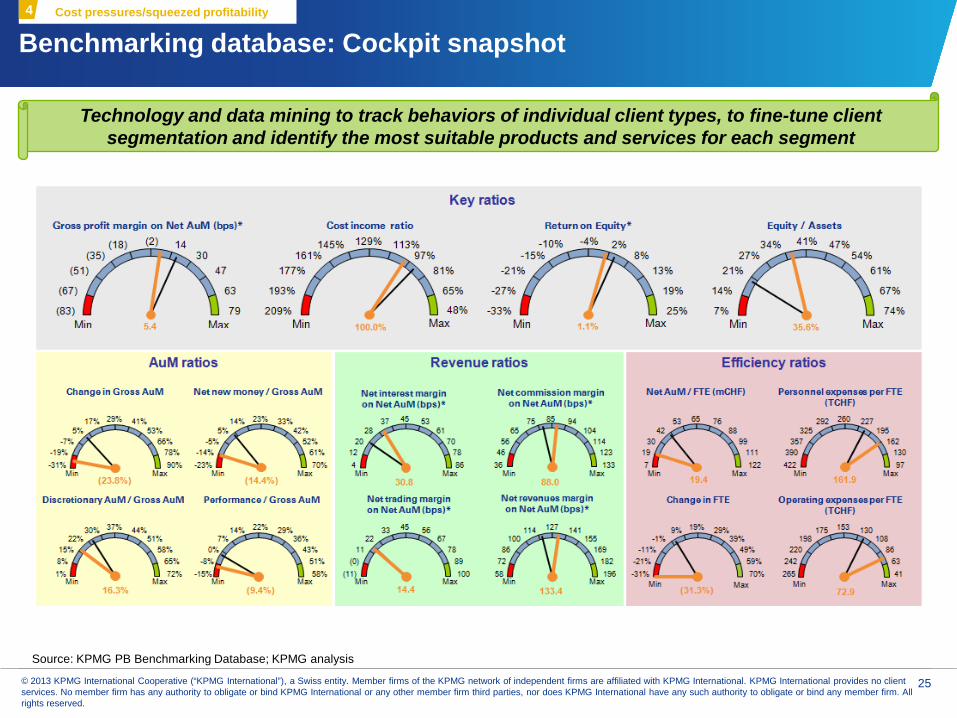

Benchmarking database: Cockpit snapshot Cost pressures/squeezed profitability 4

Technology and data mining to track behaviors of individual client types, to fine-tune client segmentation and identify the most suitable products and services for each segment

Source: KPMG PB Benchmarking Database; KPMG analysis

26 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

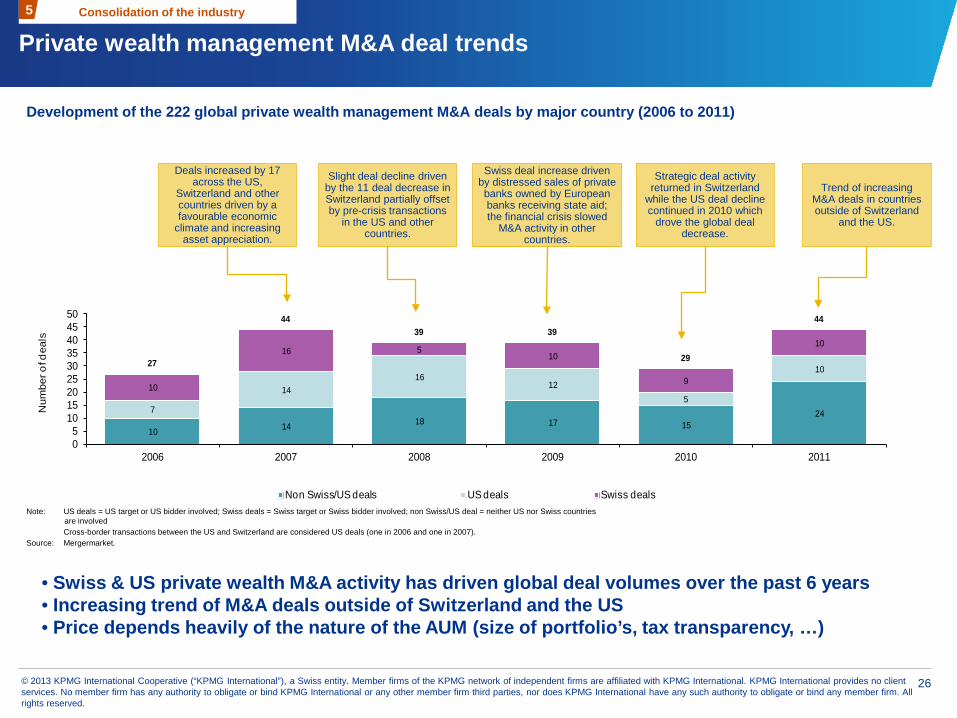

Private wealth management M&A deal trends

Development of the 222 global private wealth management M&A deals by major country (2006 to 2011)

Note: US deals = US target or US bidder involved; Swiss deals = Swiss target or Swiss bidder involved; non Swiss/US deal = neither US nor Swiss countries are involved

Cross-border transactions between the US and Switzerland are considered US deals (one in 2006 and one in 2007). Source: Mergermarket.

Deals increased by 17 across the US,

Switzerland and other countries driven by a favourable economic

climate and increasing asset appreciation.

Slight deal decline driven by the 11 deal decrease in Switzerland partially offset by pre-crisis transactions

in the US and other countries.

Swiss deal increase driven by distressed sales of private banks owned by European banks receiving state aid; the financial crisis slowed

M&A activity in other countries.

Strategic deal activity returned in Switzerland

while the US deal decline continued in 2010 which

drove the global deal decrease.

Trend of increasing M&A deals in countries outside of Switzerland

and the US.

10 14 18 17 15247

1416

125

10

10

16 510

9

10

27

4439 39

29

44

05

101520253035404550

2006 2007 2008 2009 2010 2011

Num

ber o

f dea

ls

Non Swiss/US deals US deals Swiss deals

• Swiss & US private wealth M&A activity has driven global deal volumes over the past 6 years • Increasing trend of M&A deals outside of Switzerland and the US • Price depends heavily of the nature of the AUM (size of portfolio’s, tax transparency, …)

Consolidation of the industry 5

27 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

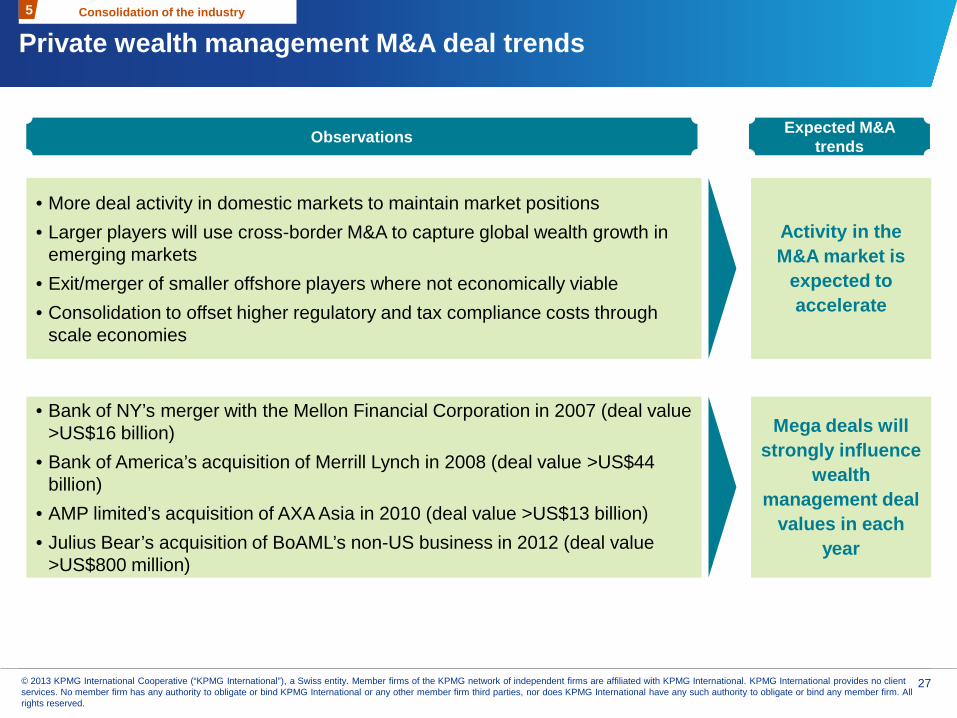

• More deal activity in domestic markets to maintain market positions • Larger players will use cross-border M&A to capture global wealth growth in

emerging markets • Exit/merger of smaller offshore players where not economically viable • Consolidation to offset higher regulatory and tax compliance costs through

scale economies

• Bank of NY’s merger with the Mellon Financial Corporation in 2007 (deal value >US$16 billion)

• Bank of America’s acquisition of Merrill Lynch in 2008 (deal value >US$44 billion)

• AMP limited’s acquisition of AXA Asia in 2010 (deal value >US$13 billion) • Julius Bear’s acquisition of BoAML’s non-US business in 2012 (deal value

>US$800 million)

Activity in the M&A market is

expected to accelerate

Mega deals will strongly influence

wealth management deal

values in each year

Private wealth management M&A deal trends Consolidation of the industry 5

Observations Expected M&A trends

28 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

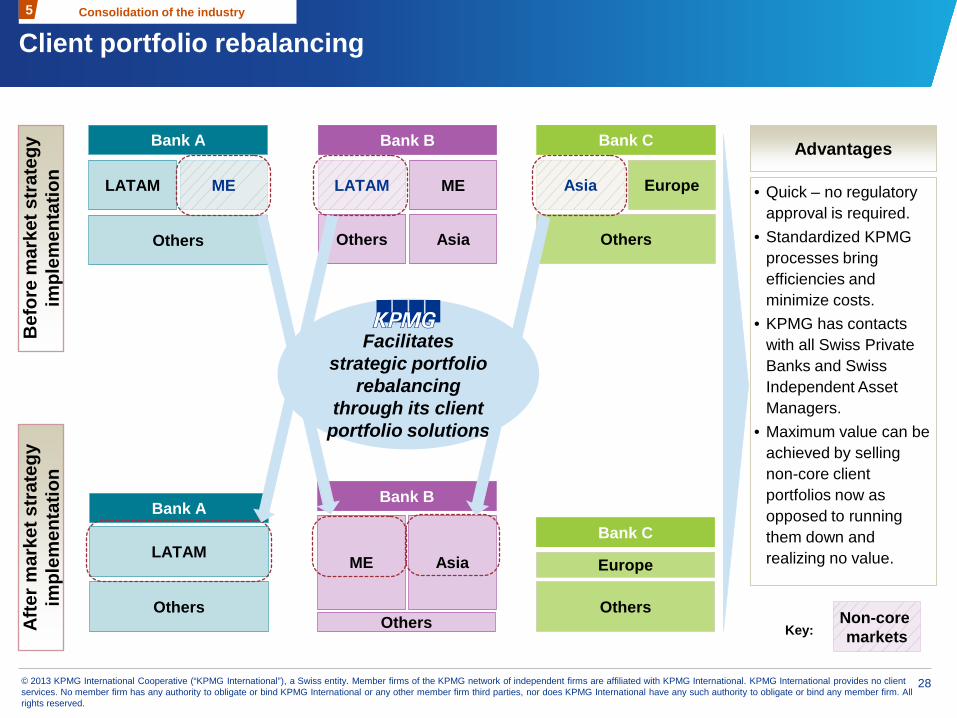

Asia ME

Bef

ore

mar

ket s

trat

egy

impl

emen

tatio

n Af

ter m

arke

t str

ateg

y im

plem

enta

tion

LATAM

Bank B

ME

Others

• Quick – no regulatory approval is required.

• Standardized KPMG processes bring efficiencies and minimize costs.

• KPMG has contacts with all Swiss Private Banks and Swiss Independent Asset Managers.

• Maximum value can be achieved by selling non-core client portfolios now as opposed to running them down and realizing no value.

Advantages

LATAM

Bank A

Others

Others

Bank B

LATAM

Bank A

Others

ME

KPMG Facilitates

strategic portfolio rebalancing

through its client portfolio solutions

Asia

Bank C

Europe

Others

Europe

Bank C

Others

Asia

Key: Non-core markets

Consolidation of the industry 5

Client portfolio rebalancing

29 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Be focused Geographical strategy/cross-border banking 6

• Banks must articulate a clear vision over which geographic markets they plan to focus on

• Bank may envisage to exit selected market where they have no critical size

• The classical cross-border banking model remains the main way to serve foreign market but is increasingly limited by regulations

• This reinforces the idea to have local presence in certain markets or co-operate with local partners

• Critical mass is becoming more important

Strategic direction

• Banks (especially smaller banks) should be specific about which client niche and countries they wish to reach and are in a position to serve on a long-term basis

• Understanding client segment performance is vital (especially in a period of margin erosion)

• Technology can assist banks in tracking behaviors of individual client types

• Data-mining should allow to identify the best products and services for each segment

Targeted approach is key to success

30 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

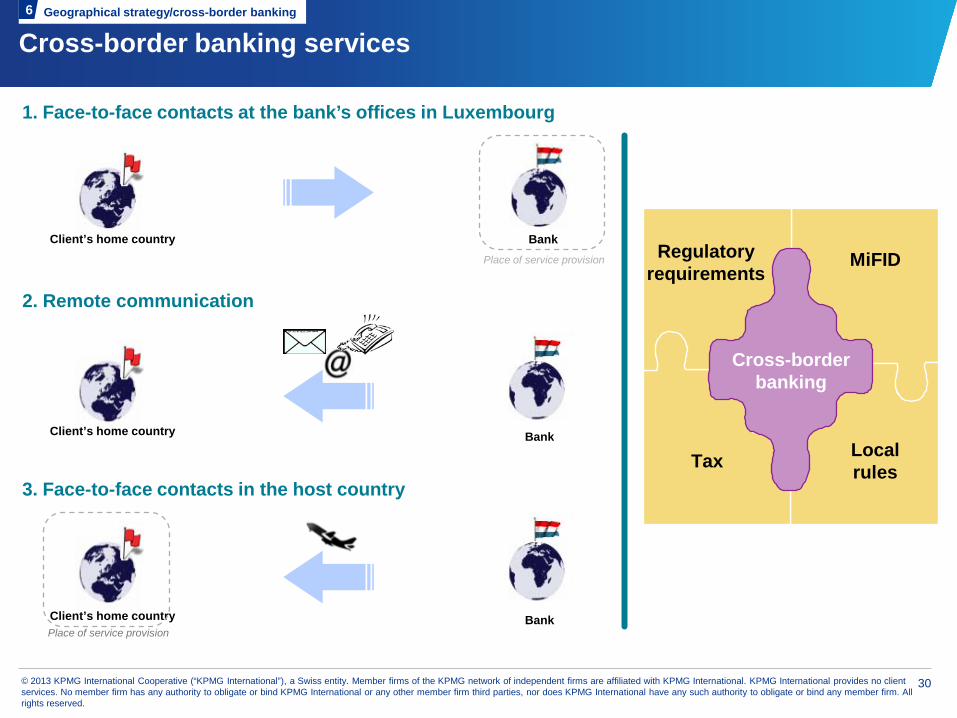

Cross-border banking services

Bank

Bank

Bank

MiFID Regulatory requirements

Cross-border banking

Local rules Tax

1. Face-to-face contacts at the bank’s offices in Luxembourg

Client’s home country

2. Remote communication 3. Face-to-face contacts in the host country

Client’s home country

Client’s home country

Place of service provision

Place of service provision

Geographical strategy/cross-border banking 6

31 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Cross-border banking manual

Permitted

Conditions apply

Not permitted

Comments

France

Activities

Face to face meeting in

Luxembourg (1)

Place of Service

General principles

Regulation

Legend

Crossborder supply (2)

Face to face meeting in

France(3)

ProspectionClient prospecting

/ /Prospects may be contacted by phone, email, fax and mail provided prior consent has been given. Specific conditions on information apply. Automated phone calls are forbidden.

External cooperation

/ /

/ // // /

Conditions apply for Cross border communication with prospects (see "Cold Calling" above).

"Carte de démarchage" required for clients visits

"Carte de démarchage" required for visit in France.

Cross border communication by mail is conditioned, fax and email are not applicable.

Methods used must not lead to expenses for the consumer.

Proactive prospect contact/Proactive promotion (including advertisement/information) of account openings or bank products or bank services

Carte de démarchage

Article L341-1 of the code monétaire et financier

Article L121.20-14 Code de la consommation

Art L.121-1 to L.121-7, L.122-11 Code de la consommation

Cold-calling

Reverse prospect contact (at the prospect's initiative) without solicitation of account openings or bank products or bank services

Reverse prospect contact (at the prospect's initiative) with solicitation of account openings or bank products or bank services Prospect contact for social events (birthday, Christmas cards, etc.)

Agreements with Finders (introducers of prospects resident in France) aiming at the referral of residents in France to the bank in LuxembourgWith External Asset Managers (ExAM) or investment advisers who are:

Ordonnance no 2005-648 of June 6th, 2005, relative to the distant

commercialization of financial services. Article L121.20-14 Code de la

consommation

Law n. 2006-1770 of 30 Dec 2006

L.341-6 and L.341-7 of the code monétaire et financier

Negotiation of financial conditions (e.g. fees, expenses, interest rate)

in France (dealing with residents in France)

outside France (dealing with residents in France)

Proactive prospect contact/Prospect managing: socializing, including advertisement/general information about the bank, without promotion of account openings or bank products or bank services

Ordonnance no 2005-648 of June 6th, 2005, relative to the distant

commercialization of financial services.

Finders require a clear mandate from the bank . Conditions apply

Account opening: providing the prospect with contractual documentation/bank forms and procuring prospect signature

Art L.121-1 to L.121-7, L.122-11 Code de la consommation

Article L341-1 of the code monétaire et financier

Prospect contact

Activities, products and issues to be solved

Places of service

Responses and short comments

Links to the relevant regulations

http://www.kpmgprivatebanking.com Access point

Geographical strategy/cross-border banking 6

32 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

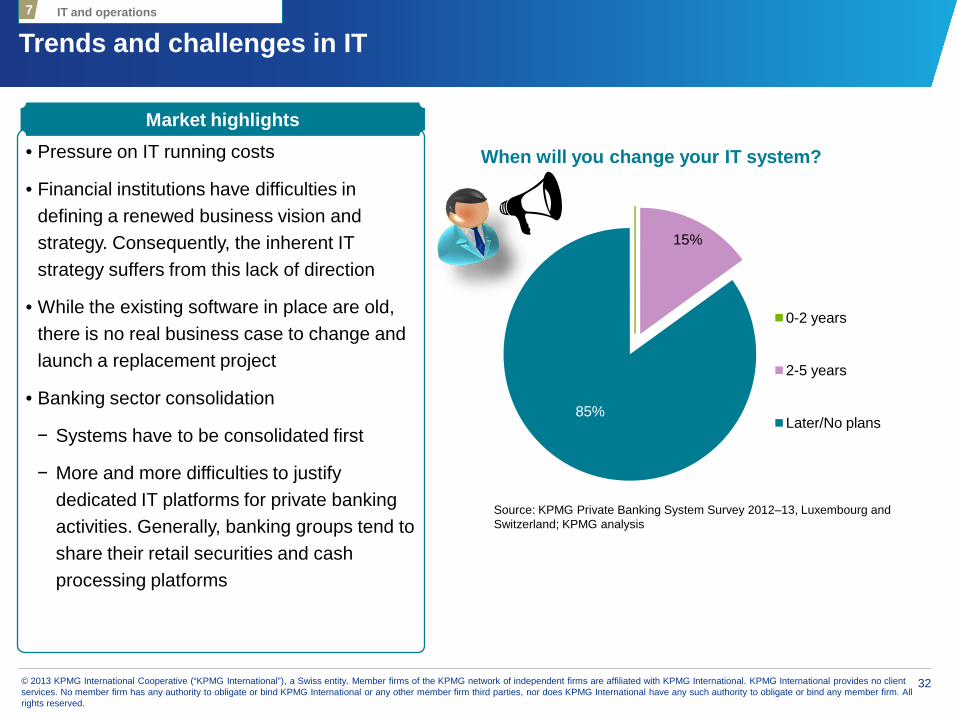

Trends and challenges in IT

• Pressure on IT running costs

• Financial institutions have difficulties in defining a renewed business vision and strategy. Consequently, the inherent IT strategy suffers from this lack of direction

• While the existing software in place are old, there is no real business case to change and launch a replacement project

• Banking sector consolidation

− Systems have to be consolidated first

− More and more difficulties to justify dedicated IT platforms for private banking activities. Generally, banking groups tend to share their retail securities and cash processing platforms

Market highlights

15%

85%

0-2 years

2-5 years

Later/No plans

When will you change your IT system?

Source: KPMG Private Banking System Survey 2012–13, Luxembourg and Switzerland; KPMG analysis

IT and operations 7

33 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

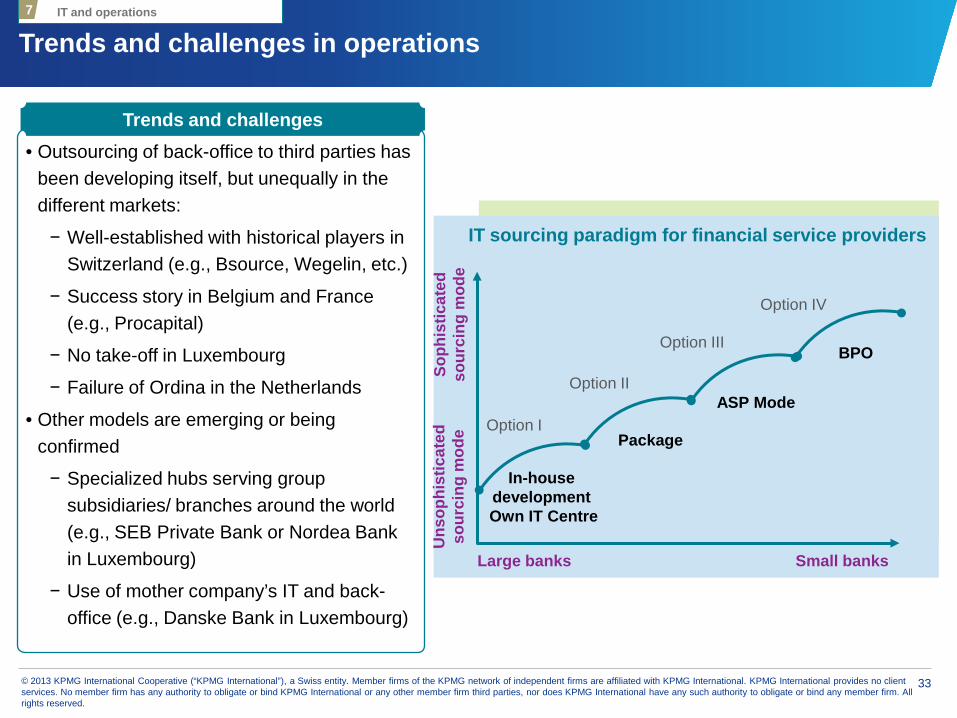

Trends and challenges in operations

• Outsourcing of back-office to third parties has been developing itself, but unequally in the different markets:

− Well-established with historical players in Switzerland (e.g., Bsource, Wegelin, etc.)

− Success story in Belgium and France (e.g., Procapital)

− No take-off in Luxembourg

− Failure of Ordina in the Netherlands

• Other models are emerging or being confirmed

− Specialized hubs serving group subsidiaries/ branches around the world (e.g., SEB Private Bank or Nordea Bank in Luxembourg)

− Use of mother company’s IT and back-office (e.g., Danske Bank in Luxembourg)

Trends and challenges

In-house development

Own IT Centre

Package

ASP Mode

BPO

Large banks Small banks

Option I

Option II

Option III

Option IV

Soph

istic

ated

so

urci

ng m

ode

Uns

ophi

stic

ated

so

urci

ng m

ode

IT sourcing paradigm for financial service providers

IT and operations 7

34 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

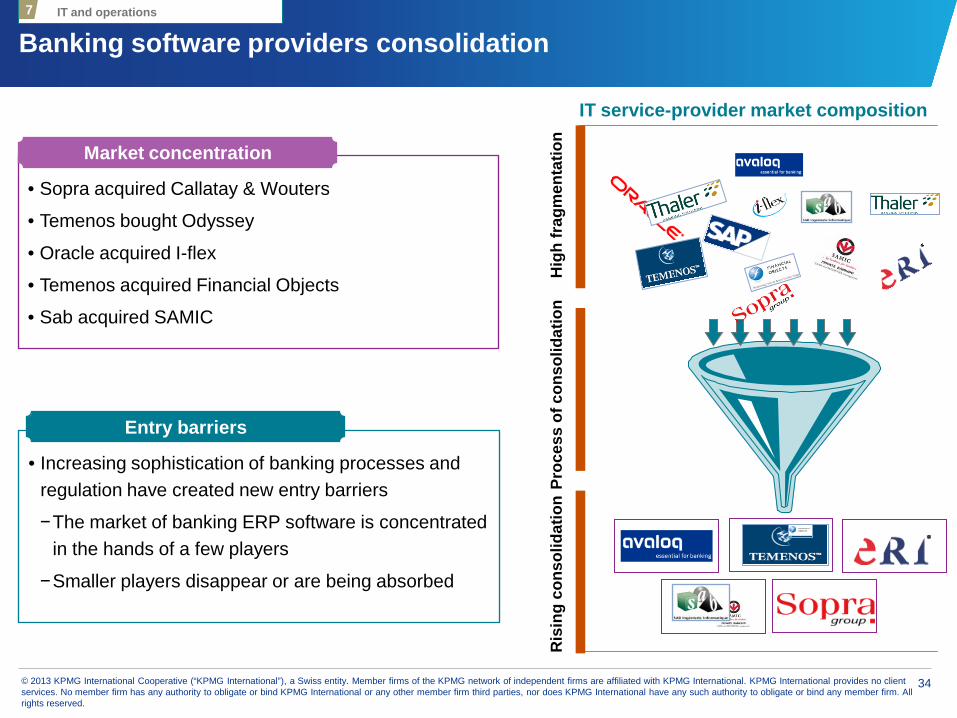

Banking software providers consolidation

IT service-provider market composition

Hig

h fr

agm

enta

tion

Ris

ing

cons

olid

atio

n Pr

oces

s of

con

solid

atio

n

• Sopra acquired Callatay & Wouters

• Temenos bought Odyssey

• Oracle acquired I-flex

• Temenos acquired Financial Objects

• Sab acquired SAMIC

Market concentration

• Increasing sophistication of banking processes and regulation have created new entry barriers

−The market of banking ERP software is concentrated in the hands of a few players

−Smaller players disappear or are being absorbed

Entry barriers

IT and operations 7

35 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Growth fuelled by emerging markets

1

Underlying trends impacting wealth management industry

Regulations to remain on the agenda

2

Changing business models for changing clients

3

IT and operations 7

Cost pressures/squeezed profitability

4

Consolidation of the industry

5

Geographical strategy/ cross-border banking

6

2013 and way forward Afterthoughts

and concluding remarks

Concluding remarks

36 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

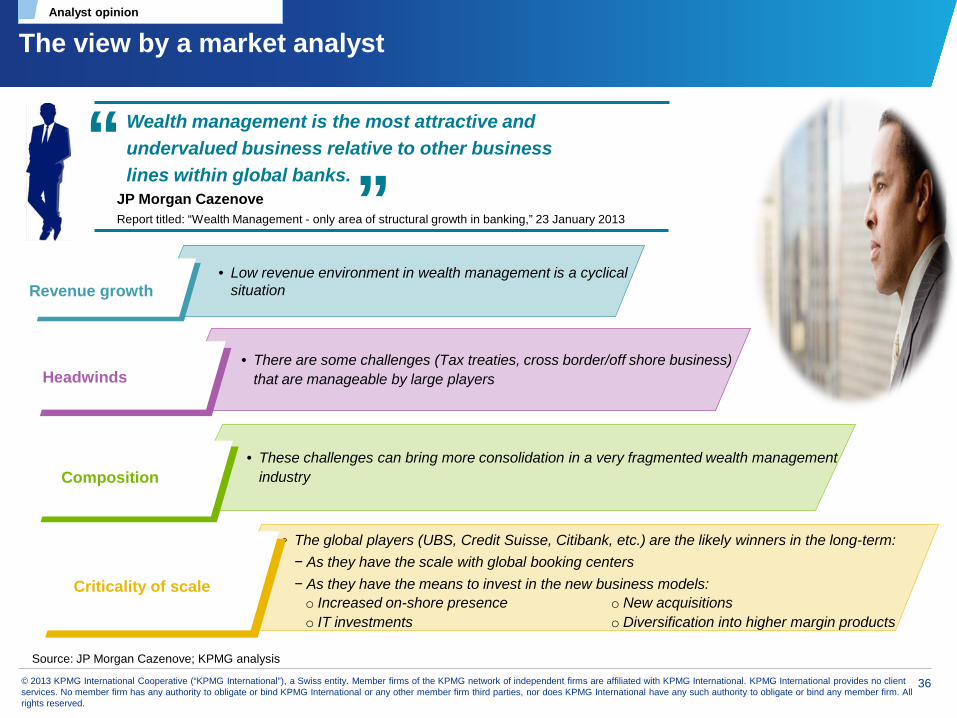

The view by a market analyst

Wealth management is the most attractive and undervalued business relative to other business lines within global banks.

“ ” JP Morgan Cazenove

Report titled: “Wealth Management - only area of structural growth in banking,” 23 January 2013

• Low revenue environment in wealth management is a cyclical situation

• There are some challenges (Tax treaties, cross border/off shore business) that are manageable by large players

• These challenges can bring more consolidation in a very fragmented wealth management industry

• The global players (UBS, Credit Suisse, Citibank, etc.) are the likely winners in the long-term: − As they have the scale with global booking centers − As they have the means to invest in the new business models: o Increased on-shore presence o IT investments

o New acquisitions o Diversification into higher margin products

Revenue growth

Headwinds

Composition

Criticality of scale

Analyst opinion

Source: JP Morgan Cazenove; KPMG analysis

37 © 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Audience questions and thoughts

Q A &

© 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

Thank you Alain Picquet

Partner Head of Advisory Head of Markets KPMG Luxembourg [email protected]