international consortium on governmental financial management (icgfm) 20 th annual international...

TRANSCRIPT

International Consortium on Governmental Financial Management (ICGFM)

20th Annual International Conference on New Developments in Governmental Financial Management

Changing Organizations and Approaches: Examining Federal, State and Municipal Government Initiatives

Governmental Coordination and Collaboration in Mexico

May 8, 2006 - Miami, Florida - USA

1. Initial thoughts

2. History of the mexican tax system

3. Organization of the National System of Fiscal Coordination (SNCF)

4. Acomplishments of the system

5. Recent breakthroughs

INDEX

Introduction:

Since:

• The taxing powers of subnational governments are different.

• An unequal distribution of income and taxpayers is a fact.

• A fiscal jungle (approximately 500 different taxes) creates

inconvenients for every taxpayer, efficient collection,

expenditure sufficiency and the income distribution between

states.

It was necessary:

• To centralize the tax administration of national taxes.

• The administrative collaboration to take advantage of the efficiency

of subnational governments in certain taxes.

• The use of distribution formulas to transfer resources from the

Federal government to the States (earmarked and non earmarked).

• The introduction of redistributive and compensatory elements that

reduce or eliminate the horizontal inequity and estimulate the fiscal

efficiency in state revenue.

• The establishment of fiscal rules of coordination and fiscal

corresponsability.

The Fiscal Coordination in Mexico:

• Is the backbone of the mexican federalism.

• Its agenda includes income (tax policy and administration), expenditure (transfers, budget and accountability) and debt (public debt and pensions)

• Is an armonic system, that is perfectible.

A Finance Secretary in a Subnational Government:

• Is elected by the Governor.

• They are responsible for the management of the state public treasury, with functions as:

Definition of the state fiscal policy: income, expenditure and public debt.

Financial management. Tax administration and intergubernamental

coordination with the Federal government and the Municipalities.

Administrative collaboration due to the agreements signed with the Federal government in areas such as tax collection or fiscal supervision.

• Has a tenure of 6 years; can be reelected.

Basis of the National System of Fiscal Coordination (SNCF):

• The Fiscal Coordination Law (LCF).

• The Administrative Collaboration in Federal Fiscal Issues (CCAMFF)

• The Permanent Commission of Fiscal Functionaries.

• The Technical and Work Groups.

• .The Monitoring Committees of the system

• The transfers distribution system.

Transfers in Mexico

Descentralization Agreements

Exceeding Oil Revenues(ARE-FIES)

Stabilization Fund for the Income of State Entities (FEIEF )

Earmarked

• Basic Education Fund (FAEB)

• Health Fund (FASA)

• Social Infrastructure Fund (FAIS)

• Fund for the strengthening of Municipalities and demarcations of the Federal District (FORTAMUN-DF)

• Multiple Contributions Fund (FAM)

• Technological and Adult Education Fund (FAETA)

• Public Security Fund (FASP)

Non Earmarked

Tax sharing agreement“Participaciones”Branch 28 of the Federal Budget (PEF)

• General Fund of “Participaciones” (FGP)

• Municipal Promotion Fund (FFM)

• Special taxes on products and services (IEPS): cigarrettes, alcholic beverages and beer.

• Others

• Economic Incentives: tax on the possession of vehicles (tenecia), tax on new automobiles (ISAN) and administrative collaboration

Contributions Fund for State govermentsBranch 33 PEF

Support program for the stregthening of the federal entities (PAFEF)

Branch 39 PEF

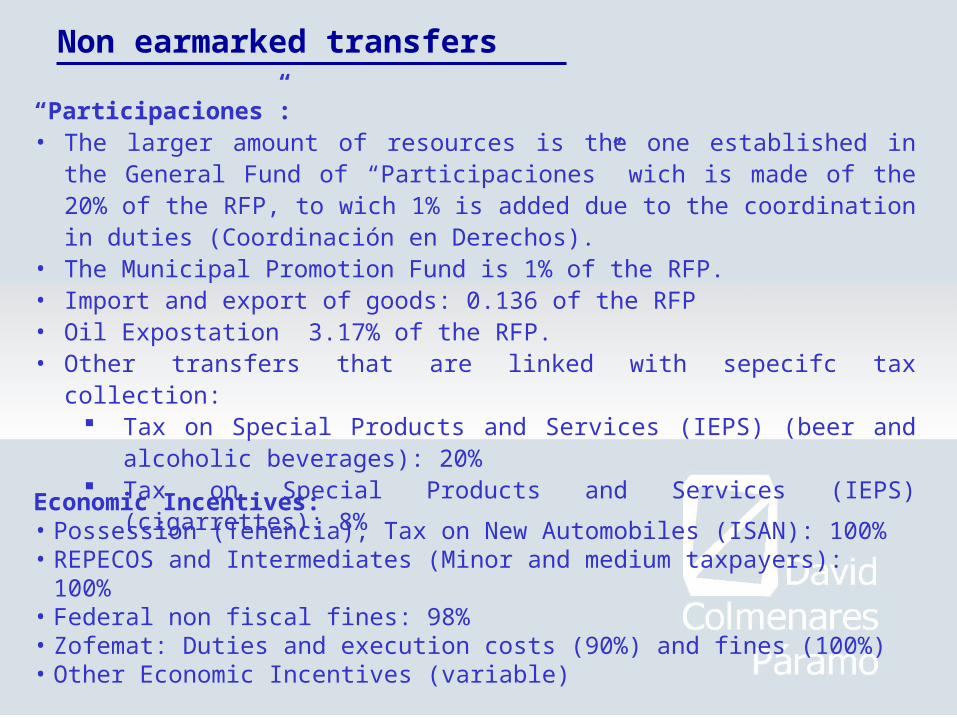

Non earmarked transfers

“Participaciones”:• The larger amount of resources is the one established in the General Fund of

“Participaciones” wich is made of the 20% of the RFP, to wich 1% is added due to the coordination in duties (Coordinación en Derechos).

• The Municipal Promotion Fund is 1% of the RFP.• Import and export of goods: 0.136 of the RFP• Oil Expostation 3.17% of the RFP.• Other transfers that are linked with sepecifc tax collection:

Tax on Special Products and Services (IEPS) (beer and alcoholic beverages): 20%

Tax on Special Products and Services (IEPS) (cigarrettes): 8%

Economic Incentives:• Possession (Tenencia), Tax on New Automobiles (ISAN): 100%• REPECOS and Intermediates (Minor and medium taxpayers): 100%• Federal non fiscal fines: 98%• Zofemat: Duties and execution costs (90%) and fines (100%)• Other Economic Incentives (variable)

Earmarked transfers:

• The grouping in a branch of the federal budget of the resources that are

destined to education, health, fight against poverty, public securyty, etc.

• The uilization of Descentralization agreements, imply the financial participation of

local governments (pari-passus): hidrological infrastructure, technological

education and agricultural development

• Additional resources destines to investment have been recently added:

- PAFEF, destined to financial saneamiento and investment in infrastructure. - Trust Fund for the Infrastructure in the Sates (FIES), resources that come

from the exceeding oil revenues (ARE).- Stabilization Fund for the Income of the Federal Entities, resources that

come from the extraordinary rights on the oil exportation.

• This resources are conditioned, distributed trough formulas that are concerted with the states and approved by Congress.

• Controlled to Congress and the Federation.

• Work with regulations decided between the states and the Federation.

¿What is the Fiscal Coordination in Mexico?:

• It is an agreement between the sub-national and the Federal governments that establishes the Fedral government is responsible for the administration of the most important taxes, such as the value added tax (IVA), the tax on personal and corportae income (ISR) and the special tax on products and services (IEPS).

• In exchange they receive “participaciones” a percentage of the sharable federal revenue (RFP).

• Through the agreement of administrative collaboration, the sates take part in the collection and fiscal supervision of federal taxes.

• This collaboration is done thrugh shared work programs, and the incentive the states have to participate is that they keep the 100 percent of what they collect.

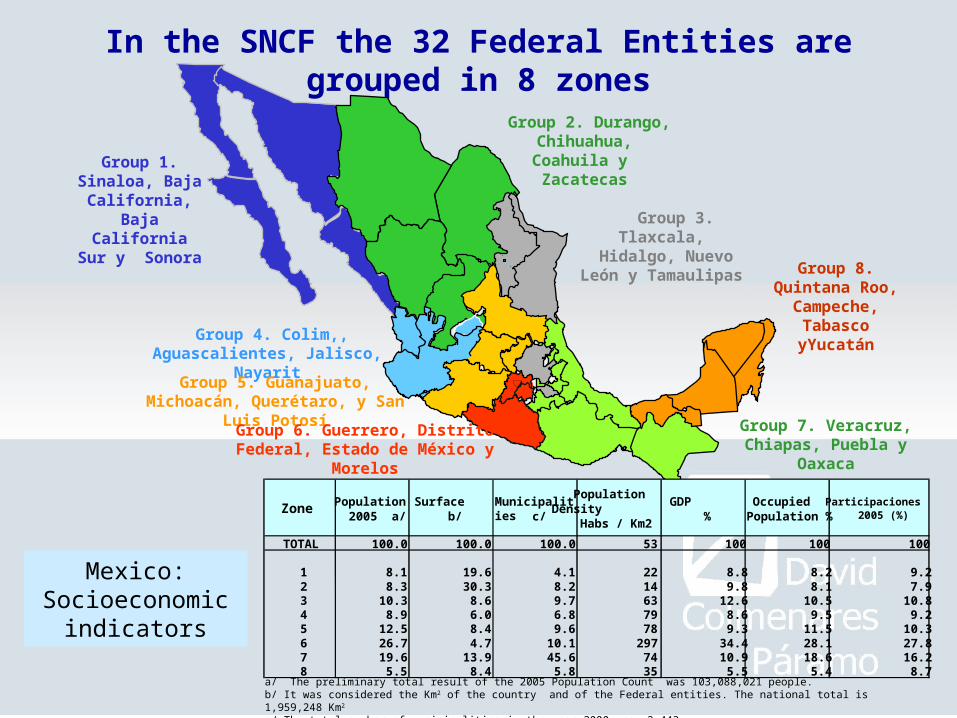

In the SNCF the 32 Federal Entities are grouped in 8 zones

Group 2. Durango, Chihuahua, Coahuila y

Zacatecas

Group 3. Tlaxcala, Hidalgo, Nuevo León y

Tamaulipas

Group 4. Colim,, Aguascalientes, Jalisco, Nayarit

Group 5. Guanajuato, Michoacán, Querétaro, y San Luis Potosí

Group 6. Guerrero, Distrito Federal, Estado de México y Morelos

Group 7. Veracruz, Chiapas, Puebla y Oaxaca

Group 8. Quintana Roo, Campeche,

Tabasco yYucatán

Group 1. Sinaloa, Baja California, Baja California Sur y Sonora

Zone Population 2005 a/

Surface b/

Municipalitiesc/

Population Density

Habs / Km2

GDP %

Occupied Population %

Participaciones 2005 (%)

TOTAL 100.0 100.0 100.0 53 100 100 100

1 8.1 19.6 4.1 22 8.8 8.2 9.22 8.3 30.3 8.2 14 9.8 8.1 7.93 10.3 8.6 9.7 63 12.6 10.5 10.84 8.9 6.0 6.8 79 8.6 9.5 9.25 12.5 8.4 9.6 78 9.3 11.5 10.36 26.7 4.7 10.1 297 34.4 28.1 27.87 19.6 13.9 45.6 74 10.9 18.6 16.28 5.5 8.4 5.8 35 5.5 5.4 8.7

Mexico: Socioeconomic

indicators

a/ The preliminary total result of the 2005 Population Count was 103,088,021 people.b/ It was considered the Km2 of the country and of the Federal entities. The national total is 1,959,248 Km2

c/ The total number of municipalities in the year 2000 was 2,443.

1. Initial thoughts

2. History of the mexican tax system

3. Organization of the National System of Fiscal Coordination (SNCF)

4. Acomplishments of the system

5. Recent breakthroughs

INDEX

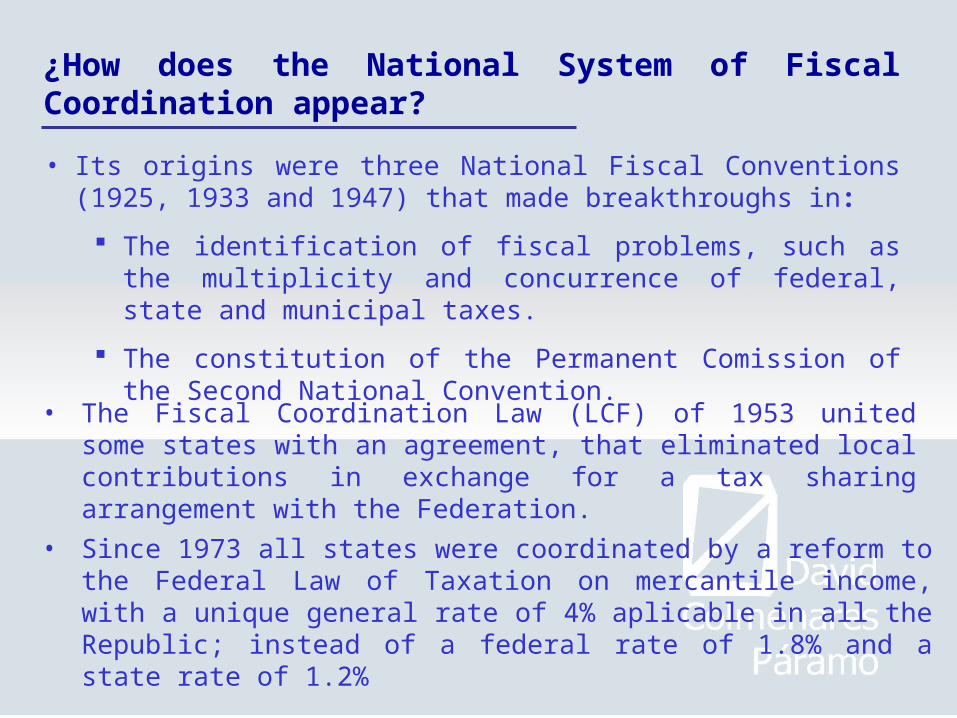

¿How does the National System of Fiscal Coordination appear?

• Its origins were three National Fiscal Conventions (1925, 1933 and 1947) that made breakthroughs in:

The identification of fiscal problems, such as the multiplicity and concurrence of federal, state and municipal taxes.

The constitution of the Permanent Comission of the Second National Convention.

• The Fiscal Coordination Law (LCF) of 1953 united some states with an agreement, that eliminated local contributions in exchange for a tax sharing arrangement with the Federation.

• Since 1973 all states were coordinated by a reform to the Federal Law of Taxation on mercantile income, with a unique general rate of 4% aplicable in all the Republic; instead of a federal rate of 1.8% and a state rate of 1.2%

• In 1978, the 1953 LCF is repealed and a new Law of Fiscal

Coordination is approved. This law begins its application in 1980; it

constitues the legal basis of the National System of Fiscal coordination

(SNCF).• In 1980 the value added tax (IVA) is introduced and the SNCF begins

to operate, instead of a tax sharing arrengement for each particular tax,

it creates a global sharing arrengement based on the sharable federal

revenue (RFP).• Before 1980, the particular tax sharing arrengements created

problems in the administration and efficient distribution of

resources.• To solve this, the concept of sharable tax revenue is created.

• In 2001 the federal window of coordination with the federal entities is

strengthened with the establishment of the Unit of Coordination with

Ferderal Entities (UCEF) and by giving it complete fiscal coordination

powers: Income, Expenditure and Debt

Antecedents of the actual National System of Fiscal Coordination

Sharable Tax Revenue (RFP)

Source: UCEF-SHCP

GROSS

RFP

• Compensations and

Devolutions

• Possession (Tenencia)

• New Automobiles

• 20% on Alcoholic Beverages

• 20% on Beer

• 8% on Cigarrettes

• 6% on Lotterys, Raffles and

Draws.

• Extraordinary on oil

extraction

• Additional on oil extraction

• Economic Incentives

Duties:• Ordinary on oil extraction.

• Extraordinary on oil extraction.

• Additional on oil extraction

• On Mining

• Income (ISR)

• Asstes (IA)

• Value Added (IVA)

• Special Products and Services (IEPS)

• Imports

• Exports

• New Automobiles (ISAN)

• Possession (Tenenecia)

• Actualizations and surcharges

• Others

MINUS

Non Tax Revenue

Tax

Revenue NET

RFP NOT INCLUDED

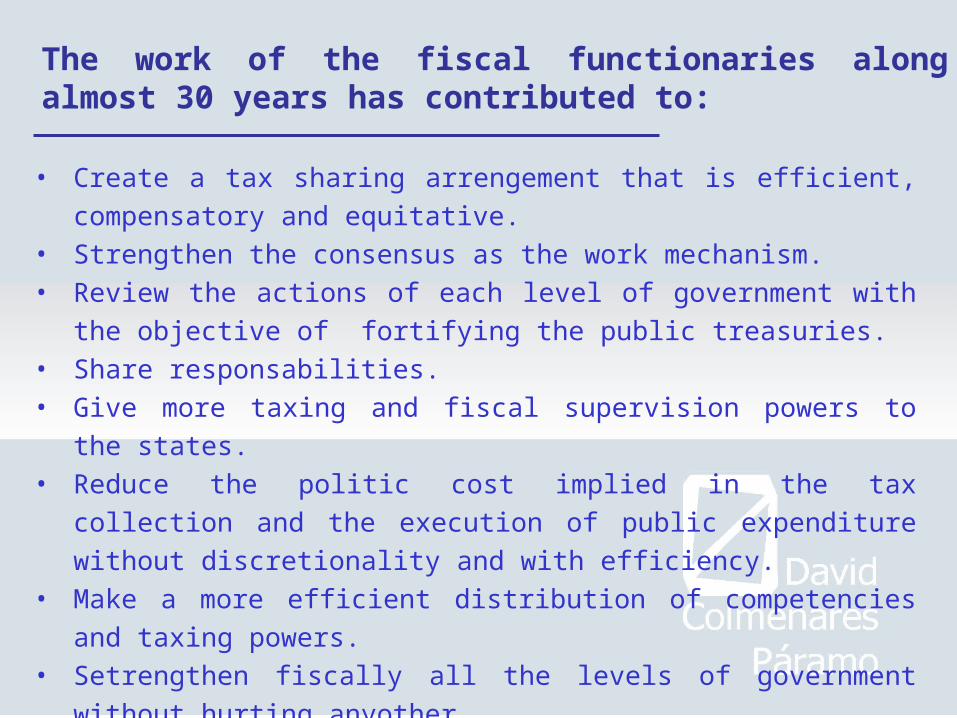

• Create a tax sharing arrengement that is efficient, compensatory and

equitative. • Strengthen the consensus as the work mechanism.• Review the actions of each level of government with the objective of

fortifying the public treasuries.• Share responsabilities.• Give more taxing and fiscal supervision powers to the states.• Reduce the politic cost implied in the tax collection and the execution of

public expenditure without discretionality and with efficiency. • Make a more efficient distribution of competencies and taxing powers.• Setrengthen fiscally all the levels of government without hurting

anyother. • More transparency and accountability at all levels of government.

The work of the fiscal functionaries along almost 30 years has contributed to:

1. Initial thoughts

2. History of the mexican tax system

3. Organization of the National System of Fiscal Coordination (SNCF)

4. Acomplishments of the system

5. Recent breakthroughs

INDEX

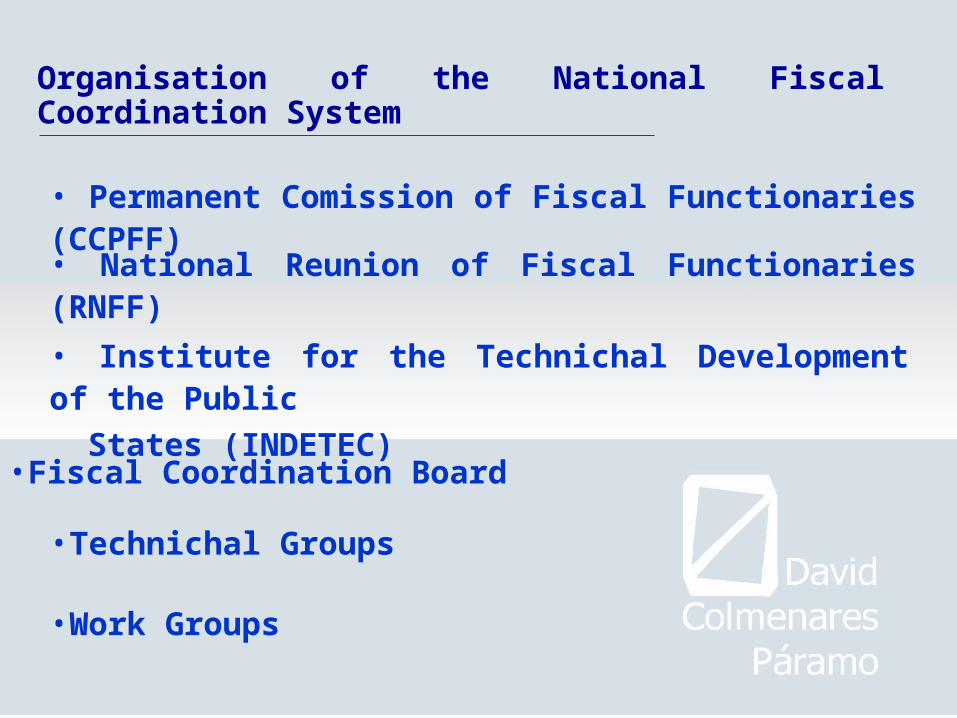

Organisation of the National Fiscal Coordination System

• Permanent Comission of Fiscal Functionaries (CCPFF)

• Institute for the Technichal Development of the Public

States (INDETEC)

• Fiscal Coordination Board

• Technichal Groups

• Work Groups

• National Reunion of Fiscal Functionaries (RNFF)

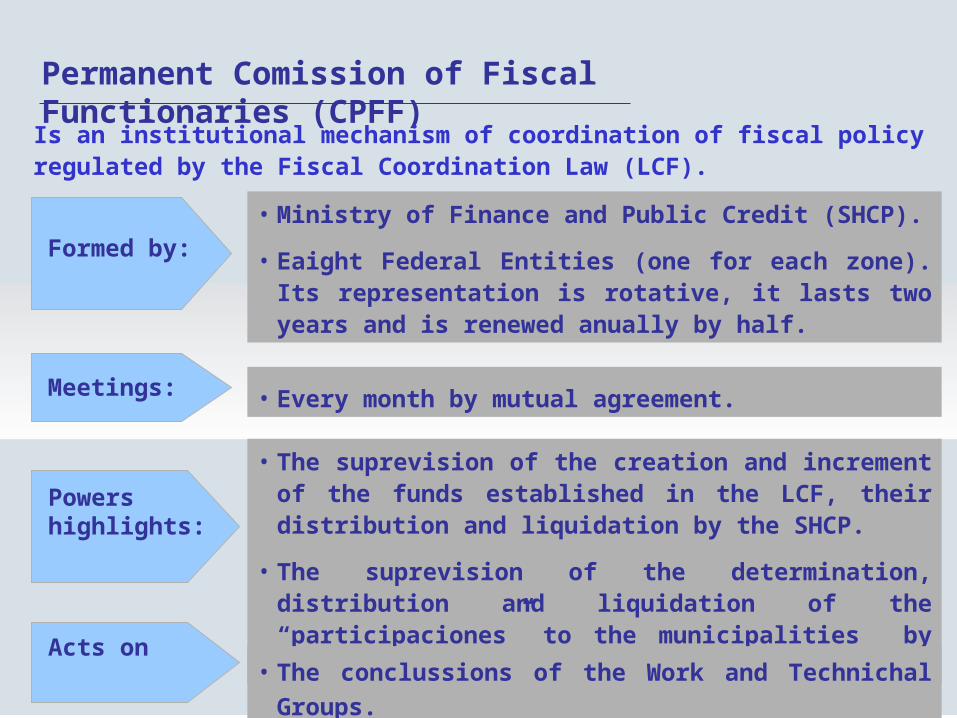

Permanent Comission of Fiscal Functionaries (CPFF)

Formed by:

Meetings:

Powers highlights:

• Ministry of Finance and Public Credit (SHCP).

• Eaight Federal Entities (one for each zone). Its representation is rotative, it lasts two years and is renewed anually by half.

• Every month by mutual agreement.

• The suprevision of the creation and increment of the funds established in the LCF, their distribution and liquidation by the SHCP.

• The suprevision of the determination, distribution and liquidation of the “participaciones” to the municipalities by the SHCP and the Federal Entities.

Is an institutional mechanism of coordination of fiscal policy regulated by the Fiscal Coordination Law (LCF).

• The conclussions of the Work and Technichal Groups.Acts on

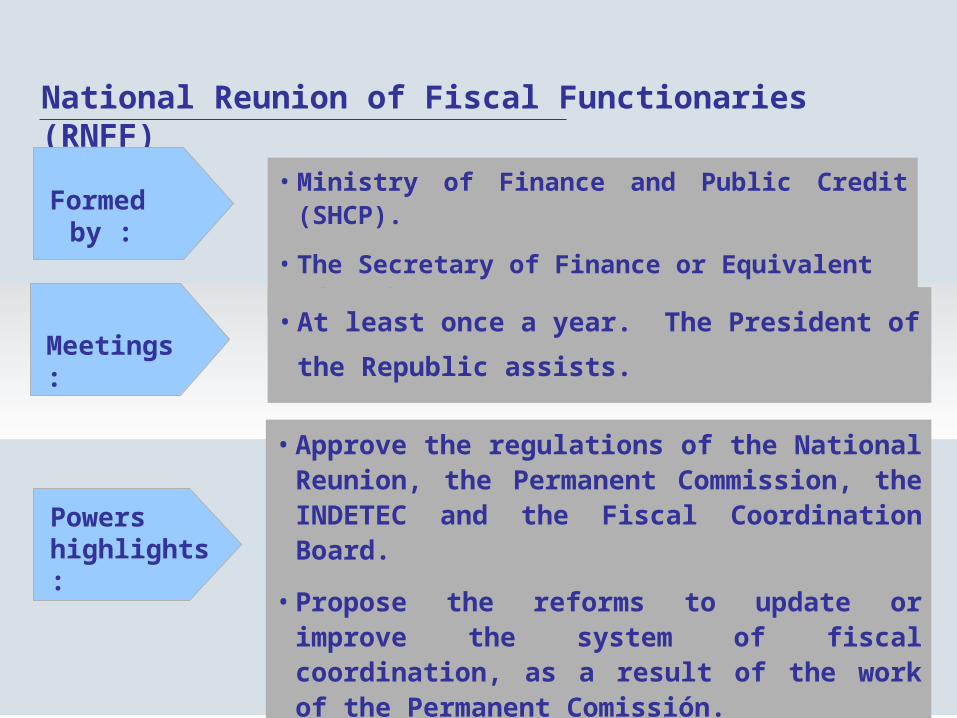

National Reunion of Fiscal Functionaries (RNFF)

• Ministry of Finance and Public Credit (SHCP).

• The Secretary of Finance or Equivalent of each Sate.

• At least once a year. The President of the

Republic assists.

• Approve the regulations of the National Reunion, the Permanent Commission, the INDETEC and the Fiscal Coordination Board.

• Propose the reforms to update or improve the system of fiscal coordination, as a result of the work of the Permanent Comissión.

Formed by :

Meetings:

Powers highlights:

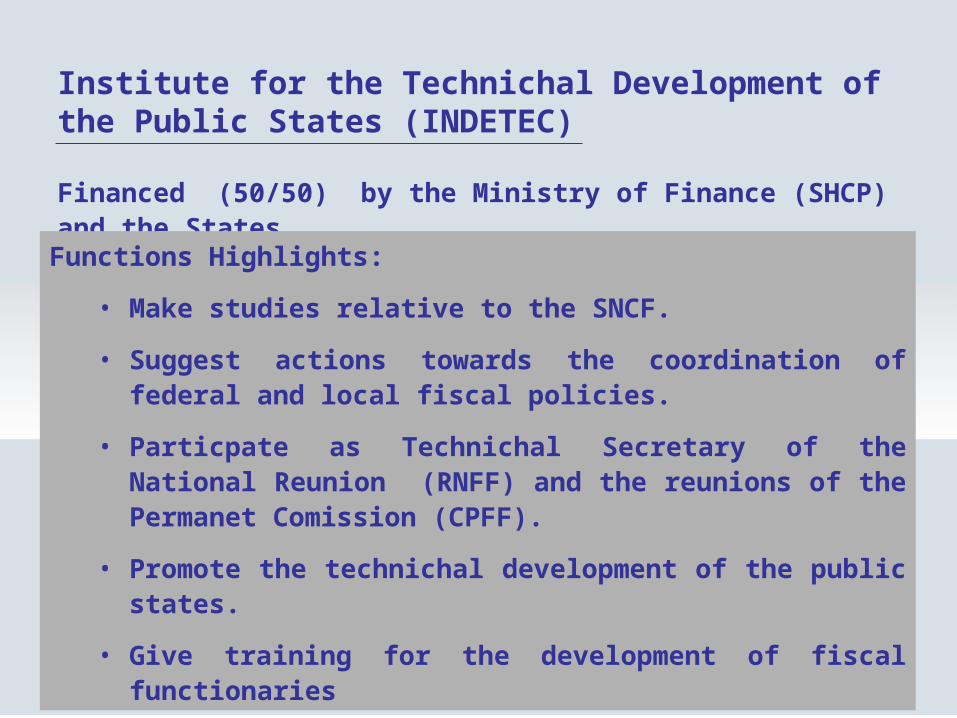

Institute for the Technichal Development of the Public States (INDETEC)

Financed (50/50) by the Ministry of Finance (SHCP) and the States

Functions Highlights:

• Make studies relative to the SNCF.

• Suggest actions towards the coordination of federal and local fiscal policies.

• Particpate as Technichal Secretary of the National Reunion (RNFF) and the reunions of the Permanet Comission (CPFF).

• Promote the technichal development of the public states.

• Give training for the development of fiscal functionaries

Fiscal Coordination Board

Is the body where the controversies of particulars over the application of the Fiscal Coordination Law by the States are solved.

The duties of the CPFF are developed through Groups:

Technichal: Coordinated by the SHCP

Work: Coordinated by the Sates

• Tax Collection

• Federal Fiscal Audit

• Budget and Federalized

Exopenditure

• Legal

• International Commerce

• Public Debt and Pension systems

• Strategic Group of the Tibutary

Administration Service (SAT)

• Supervisison Committee of the “particiapciones”

system

• Supervisison Committee on federal contributions

• Coordinated revenue, Local Revenue and Taxing

Powers

• Study of the “participaciones” system.

• Study of the operation of the porperty and water

Institutions

• Study of the Federal Reserve Zones (ZOFEMAT)

• Harmonization of budgeting and accountability

principles.

• Updated annually

The UCEF

SHCP

SSIIncome

SSEExpenditure

SSHDebt

UCEF

Fiscal Attorney

TESOFE Treasury

States

Municipalities

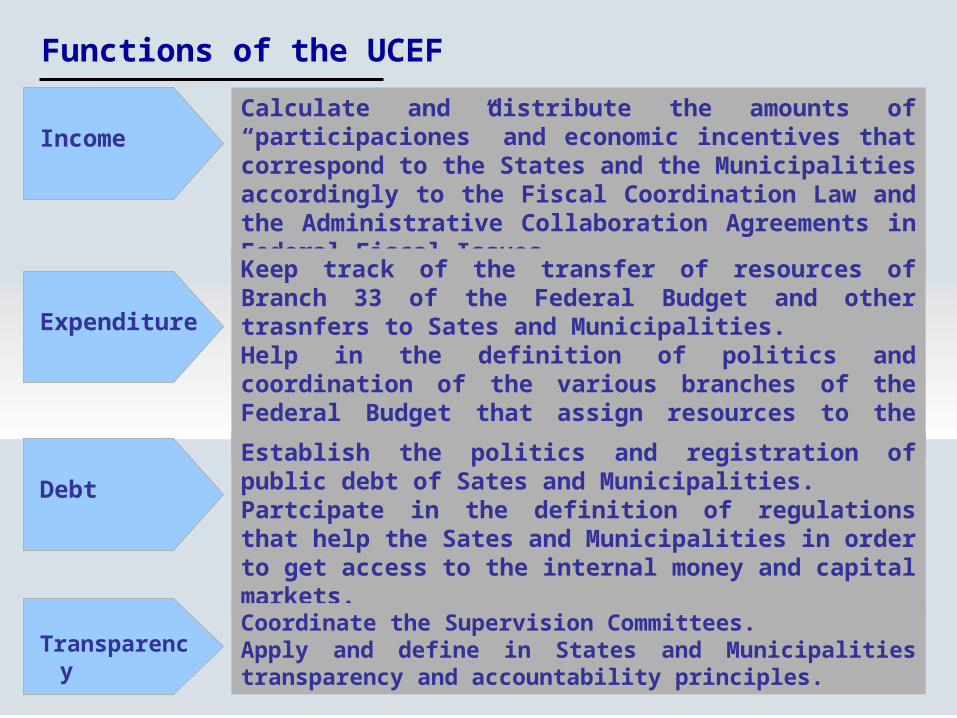

Calculate and distribute the amounts of “participaciones” and economic incentives that correspond to the States and the Municipalities accordingly to the Fiscal Coordination Law and the Administrative Collaboration Agreements in Federal Fiscal Issues.

Keep track of the transfer of resources of Branch 33 of the Federal Budget and other trasnfers to Sates and Municipalities.Help in the definition of politics and coordination of the various branches of the Federal Budget that assign resources to the States.

Establish the politics and registration of public debt of Sates and Municipalities.Partcipate in the definition of regulations that help the Sates and Municipalities in order to get access to the internal money and capital markets.

Functions of the UCEF

Income

Expenditure

Debt

TransparencyCoordinate the Supervision Committees.Apply and define in States and Municipalities transparency and accountability principles.

1. Initial thoughts

2. History of the mexican tax system

3. Organization of the National System of Fiscal Coordination (SNCF)

4. Acomplishments of the system

5. Recent breakthroughs

INDEX

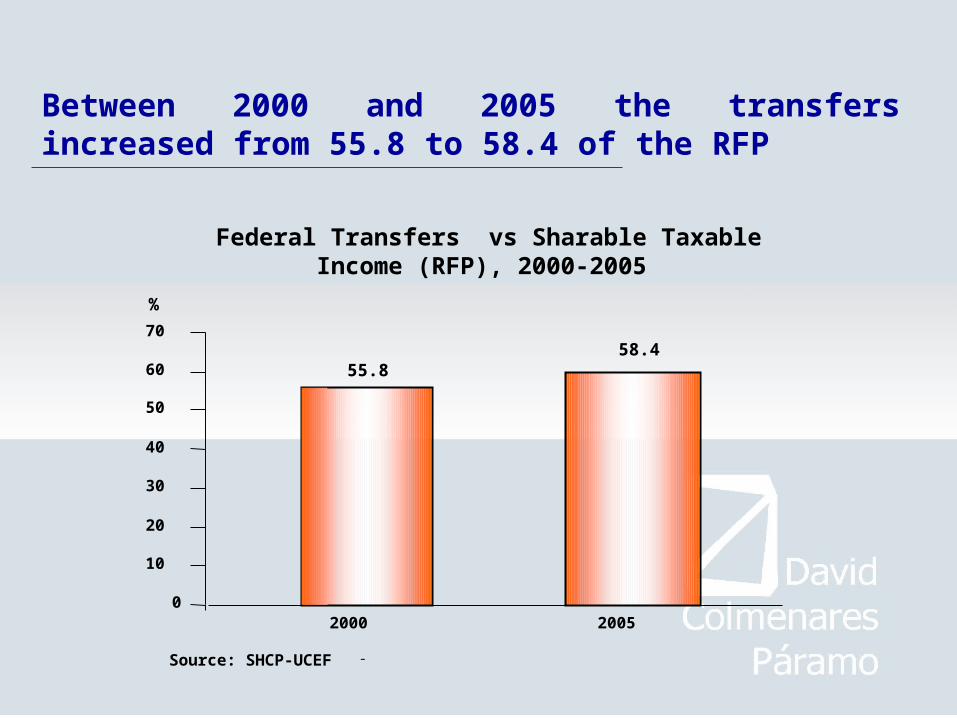

A. An increase in the amount of resources transfered to the States and Municipalities from 12.5% to 58.4% of the sharable federal revenue (RFP) between 1979 and 2005

Total Transfers to States and Municipalities 1979-2005(Thousands of millions of pesos of 1993)

The SNCF has had as principal accomplishments:

0

20

40

60

80

100

120

140

160

1979 1980 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Participaciones

Contributions

Descentralization Agreements

PAFEF

ARE-FIES

21.0 % of the RFP12.5 %

of the RFP

56.5 % of the RFP

58.4% of the RFP

29.0 % of the RFP

17.5 % of the RFP

President Vicente Fox

55.8 % of the RFP

Between 2000 and 2005 the transfers increased from 55.8 to 58.4 of the RFP

Source: SHCP-UCEF -

0

10

20

30

40

50

60

70

2000 2005

%

55.858.4

Federal Transfers vs Sharable Taxable Income (RFP), 2000-2005

6.4

4.9

4.3

3.63.4 3.3

3.53.3

3.6 3.7 3.7 3.6 3.63.8 3.8

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

0

1

2

3

4

5

6

7

National Media

State with the minor

per capit assignation

State with the mayor

per capita assignation

Number of times of the mayorassignation against the minor one.

“Participaciones” and economic incentives 1990-2004. Relation between the maximum and the minimun per capita assignation (1993 Pesos)

Source: SHCP-UCEF

B.There was an important advance in the search of equalization of the distribution of the “Participaciones” (since the 1990 reforms):

• The per capita wedge between the States that received more and the ones that received less was reduced from 6.4 to 3.8 times.

• In the FFM were included incentives to increase the local fiscal effort in the collection of property and water contributions.

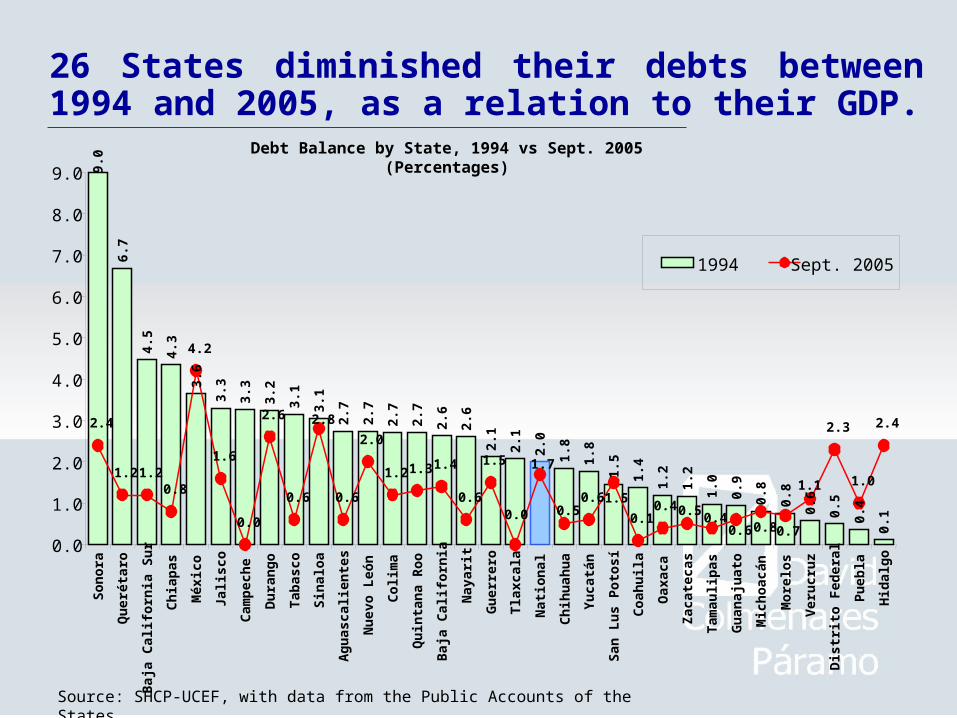

C. The increase in the federal transfers has contributed to the fact that the consolidated debt of States and Municipalities has not grown in real terms betwen 1994 and 2004.

Source: SHCP-UCEF, with data from the Public Accounts of the States.

Debt Balance by State, 1994 vs 2004(Millions of pesos of 1993)

164 285332

1994 2004

1,214

349

722581

110

541

5

301

790

128 98 0307

2,071

61

448344

13983

191

685

61124

609

0

500

1,000

1,500

2,000

2,500

3,000

So

no

ra

Jalis

co

Nu

evo

Le

ón

Qu

eré

taro

Ch

iap

as

Ba

ja C

alif

orn

ia

Ch

ihu

ah

ua

Sin

alo

a

Du

ran

go

Ta

ba

sco

Gu

err

ero

Co

ah

uila

Ca

mp

ech

e

Qu

inta

na

Ro

o

Gu

an

aju

ato

Ta

ma

ulip

as

Ag

ua

sca

lien

tes

Ve

racr

uz

Sa

n L

uis

Yu

catá

n

Ba

ja C

alif

orn

ia

Oa

xaca

Mic

ho

acá

n

Na

yarit

Co

lima

Pu

eb

la

Mo

relo

s

Tla

xca

la

Za

cate

cas

Hid

alg

o

2,59

7

2,90

9

2,16

9

1,18

5

946

923

851

510

807

479

476

476

461

416

375

340

336

322

319

282

281

240

231

206

177

144

133

126

114

21

1,396

238

708

1994 2004

Federal District 1,361 9,475

State of Mexico 4,473 6,716

National 26,686 29,274

26 States diminished their debts between 1994 and 2005, as a relation to their GDP.

Debt Balance by State, 1994 vs Sept. 2005(Percentages)9.

0

6.7

4.5

4.3

3.6

3.3

3.3

3.2

3.1

3.1

2.7

2.7

2.7

2.7

2.6

2.6

2.1

2.1

2.0

1.8

1.8

1.5

1.4

1.2

1.2

1.0

0.9

0.8

0.8

0.6

0.5

0.4

0.1

2.4

1.2 1.20.8

4.2

1.6

2.6

0.6 0.6

2.0

1.4

0.6

1.5

0.60.5

1.71.2 1.3

0.00.0 0.1

0.6 0.8 0.7

1.01.1

2.3 2.42.8

1.50.4 0.5 0.4

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

So

no

ra

Qu

erét

aro

Baj

a C

alif

orn

ia S

ur

Ch

iap

as

Méx

ico

Jalis

co

Cam

pec

he

Du

ran

go

Tab

asco

Sin

alo

a

Ag

uas

calie

nte

s

Nu

evo

Leó

n

Co

lima

Qu

inta

na

Ro

o

Baj

a C

alif

orn

ia

Nay

arit

Gu

erre

ro

Tla

xcal

a

Nat

ion

al

Ch

ihu

ahu

a

Yu

catá

n

San

Lu

s P

oto

sí

Co

ahu

ila

Oax

aca

Zac

atec

as

Tam

aulip

as

Gu

anaj

uat

o

Mic

ho

acán

Mo

relo

s

Ver

ucr

uz

Dis

trit

o F

eder

al

Pu

ebla

Hid

alg

o

1994 Sept. 2005

Source: SHCP-UCEF, with data from the Public Accounts of the States.

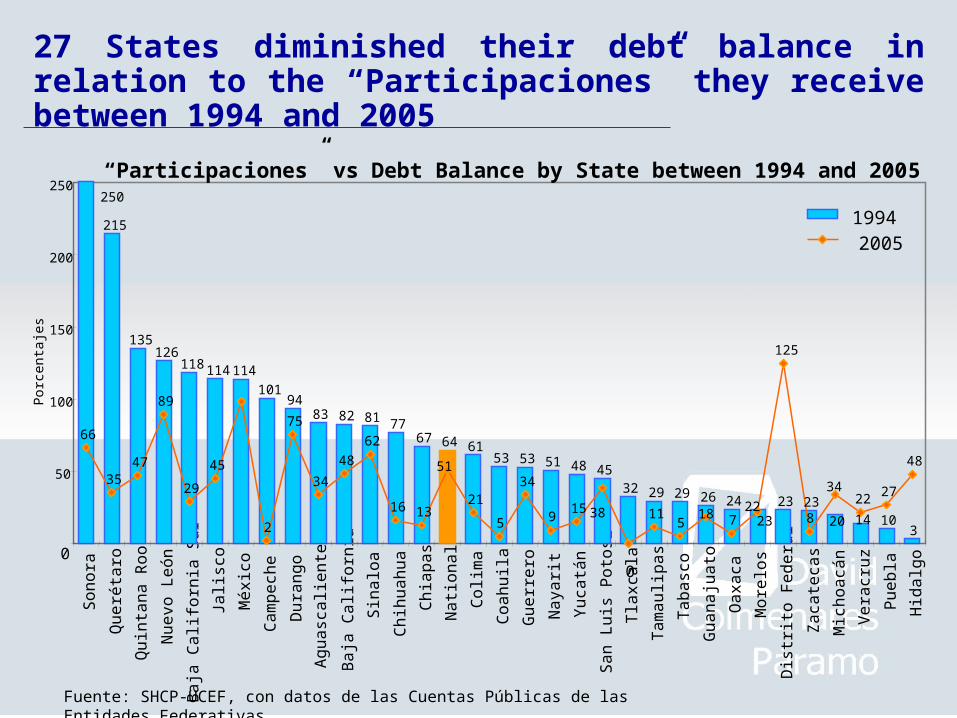

27 States diminished their debt balance in relation to the “Participaciones” they receive between 1994 and 2005

00

So

no

ra

Qu

eré

taro

Qu

inta

na

Ro

o

Nu

evo

Le

ón

Ba

ja C

alif

orn

ia S

ur

Jalis

co

Mé

xico

Ca

mp

ech

e

Du

ran

go

Ag

ua

sca

lien

tes

Ba

ja C

alif

orn

ia

Sin

alo

a

Ch

ihu

ah

ua

Ch

iap

as

Na

tion

al

Co

lima

Co

ah

uila

Gu

err

ero

Na

yarit

Yu

catá

n

Sa

n L

uis

Po

tosí

Tla

xca

la

Ta

ma

ulip

as

Ta

ba

sco

Gu

an

aju

ato

Oa

xaca

Mo

relo

s

Dis

trito

Fe

de

ral

Za

cate

cas

Mic

ho

acá

n

Ve

racr

uz

Pu

eb

la

Hid

alg

o

“Participaciones” vs Debt Balance by State between 1994 and 2005

215

135126

118 114 114

10194

83 82 81 7767 64 61

53 53 51 48 4532 29 29 26 24 23 23

103

250

1423 20

66

3547

89

29

45

2

75

34

48

62

16 1321

5

34

915 11

5 7

125

8

22 27

48

38

51

2218

3450

100

150

200

250

Por

cent

ajes

19942005

Fuente: SHCP-UCEF, con datos de las Cuentas Públicas de las Entidades Federativas

Of the proposals some have to be presented and voted in Congress and others have to do with administrtive collaboration and fiscal coordination between the Federation and the States.

D. National Convention of the Public States (CNH)

An important moment for the fiscal coordination was the National Convention of the Public States , in which the CPFF acted as Technichal Secretary. Some of the results were:

The reception of 452 Proposals

from the participants and

the society. The generation of 341 Proposals in 7 Tables of Analysis

The establishment of 7 General Objectives and 42 change strategies The generation of

323 agreements (taken by consensus) that were traduced in specific actions.

1. Initial thoughts

2. History of the mexican tax system

3. Organization of the National System of Fiscal Coordination (SNCF)

4. Acomplishments of the system

5. Recent breakthroughs

INDEX

In the CPFF and as a result of the CNH there have been advances that involve compromise by all levels of government:

• The “participaciones” to the States and Municpalities are guaranteed.

• It defines rules for the distribution of the Fund for Stabilization of Oil Revenue.

• REPECOS (Minor taxpayers)• International commerce, • Sports fishing, • Tax surcharge on some personal income:

wages and fees, selling and rent of real estate, profesional servics, (deductibles from the federal income tax).

New taxing powers for States in

New Fiscal Regime for

PEMEX

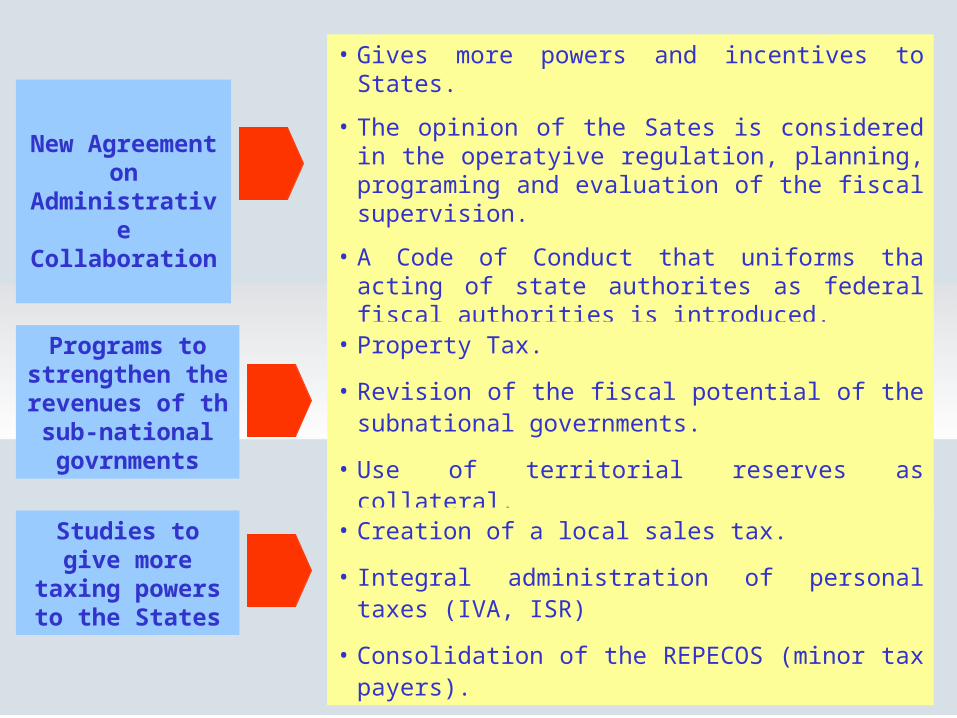

• Gives more powers and incentives to States.

• The opinion of the Sates is considered in the operatyive regulation, planning, programing and evaluation of the fiscal supervision.

• A Code of Conduct that uniforms tha acting of state authorites as federal fiscal authorities is introduced.

• Property Tax.

• Revision of the fiscal potential of the subnational governments.

• Use of territorial reserves as collateral.

Programs to strengthen the revenues of th sub-national govrnments

New Agreement on

Administrative Collaboration

• Creation of a local sales tax.

• Integral administration of personal taxes (IVA, ISR)

• Consolidation of the REPECOS (minor tax payers).

Studies to give more taxing

powers to the States

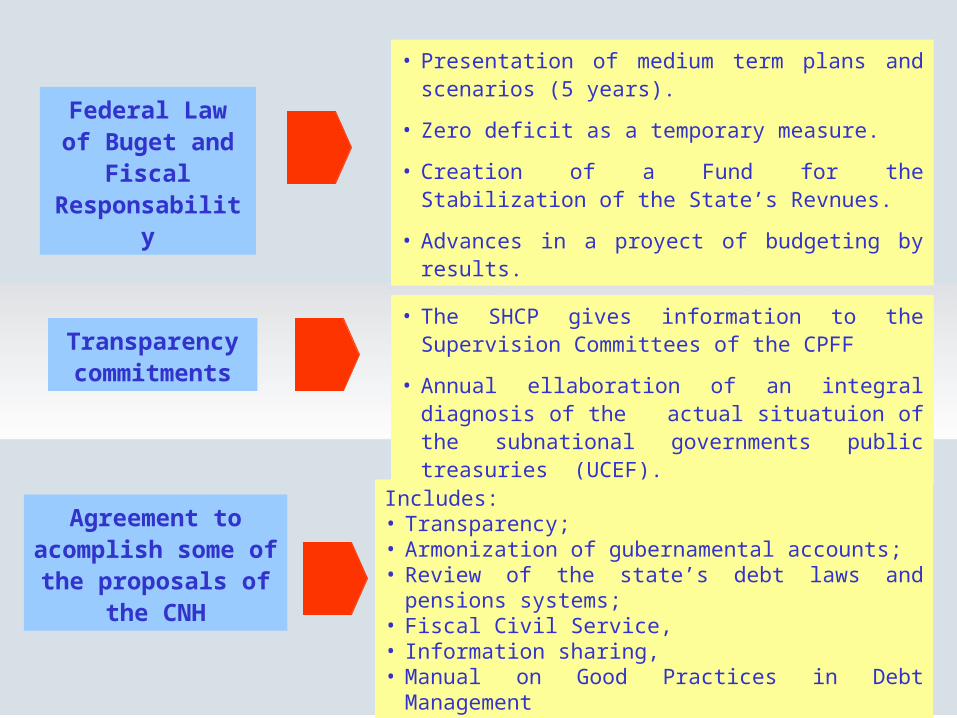

• Presentation of medium term plans and scenarios (5 years).

• Zero deficit as a temporary measure.

• Creation of a Fund for the Stabilization of the State’s Revnues.

• Advances in a proyect of budgeting by results.

• The SHCP gives information to the Supervision Committees of the CPFF

• Annual ellaboration of an integral diagnosis of the actual situatuion of the subnational governments public treasuries (UCEF).

Transparency commitments

Federal Law of Buget and Fiscal Responsability

Includes:• Transparency; • Armonization of gubernamental accounts; • Review of the state’s debt laws and pensions systems; • Fiscal Civil Service,• Information sharing,• Manual on Good Practices in Debt Management

Agreement to acomplish some of the proposals of the

CNH

ANNEX

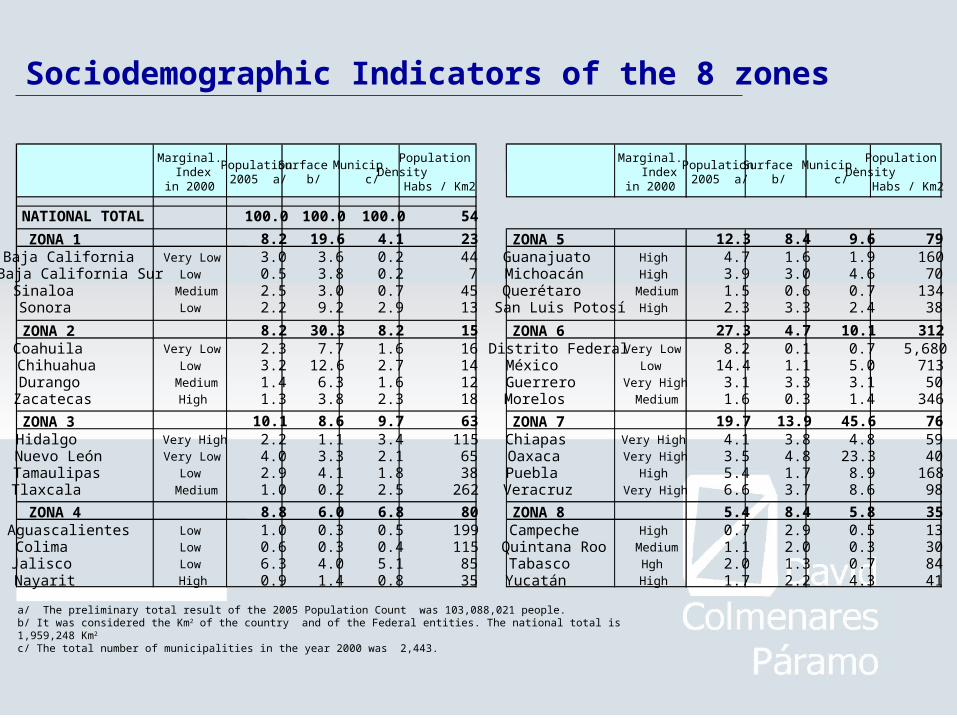

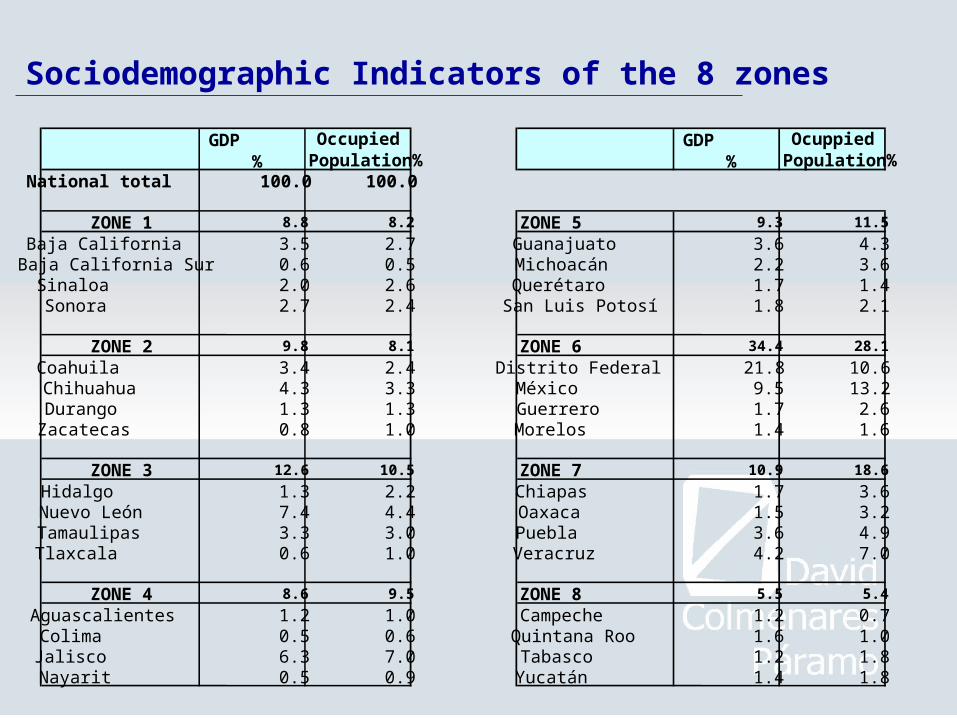

Sociodemographic Indicators of the 8 zones

Marginal. Index

in 2000

Population 2005 a/

Surface b/

Municip. c/

PopulationDensity

Habs / Km2

Marginal. Index

in 2000

Population 2005 a/

Surface b/

Municip. c/

Population Density

Habs / Km2

NATIONAL TOTAL 100.0 100.0 100.0 54

ZONA 1 8.2 19.6 4.1 23 ZONA 5 12.3 8.4 9.6 79Baja California Very Low 3.0 3.6 0.2 44 Guanajuato High 4.7 1.6 1.9 160Baja California Sur Low 0.5 3.8 0.2 7 Michoacán High 3.9 3.0 4.6 70Sinaloa Medium 2.5 3.0 0.7 45 Querétaro Medium 1.5 0.6 0.7 134Sonora Low 2.2 9.2 2.9 13 San Luis Potosí High 2.3 3.3 2.4 38

ZONA 2 8.2 30.3 8.2 15 ZONA 6 27.3 4.7 10.1 312Coahuila Very Low 2.3 7.7 1.6 16 Distrito Federal Very Low 8.2 0.1 0.7 5,680Chihuahua Low 3.2 12.6 2.7 14 México Low 14.4 1.1 5.0 713Durango Medium 1.4 6.3 1.6 12 Guerrero Very High 3.1 3.3 3.1 50Zacatecas High 1.3 3.8 2.3 18 Morelos Medium 1.6 0.3 1.4 346

ZONA 3 10.1 8.6 9.7 63 ZONA 7 19.7 13.9 45.6 76Hidalgo Very High 2.2 1.1 3.4 115 Chiapas Very High 4.1 3.8 4.8 59Nuevo León Very Low 4.0 3.3 2.1 65 Oaxaca Very High 3.5 4.8 23.3 40Tamaulipas Low 2.9 4.1 1.8 38 Puebla High 5.4 1.7 8.9 168Tlaxcala Medium 1.0 0.2 2.5 262 Veracruz Very High 6.6 3.7 8.6 98

ZONA 4 8.8 6.0 6.8 80 ZONA 8 5.4 8.4 5.8 35Aguascalientes Low 1.0 0.3 0.5 199 Campeche High 0.7 2.9 0.5 13Colima Low 0.6 0.3 0.4 115 Quintana Roo Medium 1.1 2.0 0.3 30Jalisco Low 6.3 4.0 5.1 85 Tabasco Hgh 2.0 1.3 0.7 84Nayarit High 0.9 1.4 0.8 35 Yucatán High 1.7 2.2 4.3 41

a/ The preliminary total result of the 2005 Population Count was 103,088,021 people.b/ It was considered the Km2 of the country and of the Federal entities. The national total is 1,959,248 Km2

c/ The total number of municipalities in the year 2000 was 2,443.

GDP %

OccupiedPopulation%

GDP %

OcuppiedPopulation%

National total 100.0 100.0

ZONE 1 8.8 8.2 ZONE 5 9.3 11.5

Baja California 3.5 2.7 Guanajuato 3.6 4.3Baja California Sur 0.6 0.5 Michoacán 2.2 3.6Sinaloa 2.0 2.6 Querétaro 1.7 1.4Sonora 2.7 2.4 San Luis Potosí 1.8 2.1

ZONE 2 9.8 8.1 ZONE 6 34.4 28.1

Coahuila 3.4 2.4 Distrito Federal 21.8 10.6Chihuahua 4.3 3.3 México 9.5 13.2Durango 1.3 1.3 Guerrero 1.7 2.6Zacatecas 0.8 1.0 Morelos 1.4 1.6

ZONE 3 12.6 10.5 ZONE 7 10.9 18.6

Hidalgo 1.3 2.2 Chiapas 1.7 3.6Nuevo León 7.4 4.4 Oaxaca 1.5 3.2Tamaulipas 3.3 3.0 Puebla 3.6 4.9Tlaxcala 0.6 1.0 Veracruz 4.2 7.0

ZONE 4 8.6 9.5 ZONE 8 5.5 5.4

Aguascalientes 1.2 1.0 Campeche 1.2 0.7Colima 0.5 0.6 Quintana Roo 1.6 1.0Jalisco 6.3 7.0 Tabasco 1.2 1.8Nayarit 0.5 0.9 Yucatán 1.4 1.8

Sociodemographic Indicators of the 8 zones