interim results 2006/07 - investisfiles.investis.com/deb_intermis2006and2007/interims 2006-7... ·...

TRANSCRIPT

0

Interim Results 2006/07

1

Chris Woodhouse

Finance Director

2

Results Highlights

Gross Transaction Value + 5.8%

Like for Like Sales - 4.5%

Gross Margin % -

40 bps

Profit before Tax £105.5m

Net Debt £1,046m

Proposed Interim Dividend 2.5p per share

Underlying Earnings Per Share 9.5p

(b)

Note:

(a) Includes £1.9m of capitalised bank fees written off.

(b) Net Debt excludes debt capitalisation fees

(a)

3

Trading Results H1 2007

£m H1 07 H1 06 % Change

Gross Transaction Value

EBITDA

1,287.8

186.4

1,216.8

198.2

+ 5.8

- 6.0

Operating Profit 139.6 153.1 - 8.8

Interest (34.1) (74.6)

Profit before Tax 105.5 78.5 + 34.4

Taxation (31.4) (23.4)

Profit after tax 74.1 55.1 + 34.5

Underlying Earnings per Share 9.5p 11.1p

4

£m H1 07 H1 06 % Change

Reported Operating Profit 139.6 153.1 - 8.8

• IAS 17 Flat Lining of Lease Rentals 7.3 7.7

• Share Option Costs 1.5 8.8

Underlying Operating Profit 148.4 169.6 - 12.5

Pro forma Interest (32.2) (34.0)

Pro forma Profit Before Tax 116.2 135.6 - 14.3

Pro forma Taxation (34.6) (40.5)

Adjusted Profit Before Tax 81.6 95.1 - 14.2

Adjusted Earnings per Share 9.5p 11.1p

Underlying Profit

(b) (b)

Note:

(a) Excludes capitalised bank fees written off; £1.9m (2006: £2.0m).

(b) Calculated on the basis of 859 million shares in issue for the full period.

(a)

5

1,28

8

1,21

7

1,11

3

1,04

3

800

1,400

H1 04 H1 05 H1 06 H1 07

Tota

l Sal

es (£

m)

Sales Growth H1 History

LFL 0.9% 4.2% 0.6% -4.5%

6

Sales Growth H1 2007

LFL RochesStores

New DeptStores

New DesireStores

International

% G

row

th

(4.5%)

7.0%

2.4%

0.7%

0.2%

+ 5.8%

7

Own Bought69.2%

Own Bought69.9%

Own Bought70.7%

Concessions28.9%

Concessions28.0%

Concessions27.5%

International 1.9%

International 2.1%

International 1.8%

40% 50% 60% 70% 80% 90% 100%

Gross Margin Movement H1 07H1 2007

Gross Margin Benefit bps

Roches impact - 30

Other - 10

Total - 40

Roches impact driven by sales mix and initial low margins as legacy stock was cleared through.

H1 06

H1 07

H1 07 (Exc Roches)

Sal

es M

ix

8

H1 07 (Roches) H1 07 (Debenhams Eire)

Roches Integration

First Half Impact of the Ex-Roches stores mitigated in Second Half by:

Increasing Own Bought Mix

No legacy stock

Renegotiation of Concession rates.

Chain fully stocked

Concessions42.2%

Roche Legacy Stock18.3% Own Bought

39.5%

Own Bought80.1%

Concessions19.9%

Other0.0%

9

Roches First Half Operating Performance

£ m H1 07

Gross Transaction Value 84.6

Gross Margin 32.4

Gross Margin Rate 38.3%

Costs (32.1)

EBITDA 0.3

Depreciation (1.2)

Operating Profit (0.9)

10

Store Costs

£ m H1 07 H1 07

(Exc Roches)

H1 06

Payroll 126.3 111.5 108.0

% to Sales 9.8% 9.3% 8.9%

Store Rent UK GAAP 60.0 53.1 50.1

IFRS Adjustment 7.8 7.8 7.8

Total Store Rent 67.8 60.9 57.9

% to Sales (UK GAAP)

Energy

% to Sales

4.7%

12.8

1.0%

4.4%

12.0

1.0%

4.1%

8.1

0.7%

19 new stores versus H1 06 of which 14 were Department stores and 5 Desire by Debenhams stores.

11

Warehouse and Distribution

Daventry DC closed Nov 05; Bedford DC closed July 06.

£ m H1 07 H1 07

(Exc Roches)

H1 06

Labour 8.2 7.9 10.5

Property 6.4 6.3 7.9

Transport 8.7 7.7 8.3

Total Distribution 23.3 21.9 26.7

% to Sales 1.8% 1.8% 2.2%

12

Store Numbers and FootageSq Ft. (k) Dept Stores Desires Total

2006 Close 9,474 122 4 126

Dept Stores Openings • Roches Acquisition 594.5 9

• Llandudno 46.5 1

Desire Store Openings • Birmingham Fort 12.8 1

• Kirkcaldy 14.4 1

• Merthyr 13.2 1

H1 07 Close 10,155 132 7 139

Dept Stores Openings • Wigan * 20 -

• Warrington 75 1

Desire Store Openings • Altrincham 15 1

• Walton on Thames 12.5 1

2007 Forecast 10,278 133 9 142

* Resite (represents incremental space)

13

Capital Expenditure Mix: 1H 2007

New Stores27%

Roches37%

Systems9%

Store Maintenance

11%

Other14%

Modernisations2%

Total Spend: £44.5m

14

42.925.6

36.1 41.1

10.6

10.210.3

16.9

31.1 68.5 42.1

72.0

19.0

0

20

40

60

80

100

120

140

160

Cap

ital S

pend

(£ m

)

Roches StoresNew StoresModernisationsOther

Capital Expenditure

2004 2005 2006 2007Capex £/ Sq. Ft.

New Stores 121 108 107 106

88.5

104.3

149

84.6

Est.

15

Balance Sheet Highlights

H1 07 H1 06 Movement

Fixed Assets 1,586 1,559 27

Stock 231 226 5

Other Working Capital (342) (348) 6

Net Debt (1,032) (1,743) 711

Liabilities and Charges (322) (320) (2)

Shareholders’

Funds 121 (626) 747

Fixed Charge Cover 2.5

Net Debt / EBITDA 3.4 x

Pension Surplus 26.1

(a)

Notes:

(a) MAA to February.

(b) Net Debt including debt capitalisation fees of £14.1m

£m

(b)(a)

16

Operating Cash flow

£m H1 07 H1 06

Reported Operating Profit 139.6 153.1

Depreciation 43.6 42.4

Amortisation 3.2 2.3

Profit on Disposal - 0.4

EBITDA 186.4 198.2

Working Capital –

Trading (7.4) 5.7

– Pension (5.6) (0.5)

Capital Expenditure (44.5) (51.5)

Operating Cash flow before Exceptionals, Financing & Taxation 128.9 151.9

Net Debt 1,046 1,777

Note:

(a) Net Debt excludes debt capitalisation fees

(a)

17

Rob Templeman

Chief Executive Officer

18

Agenda

First Half Sales Review

Strategy Update- Space

-

Multi Channel

-

Driving the Store Portfolio

Outlook

19

•

Relative good performance from non-clothing divisions

•

Menswear

•

Womenswear

•

Stock cover tight in last quarter due to Roches acquisition

•

Marketing –

competitors spend increasing

•

Un-modernised store performance

First Half Sales Review –

Key Points

20

SPACEGROWTH

OTHER ROUTES

TO MARKET

Strategy Update –

Multiple Growth Drivers

DepartmentStores

DesireStores

Roches

Internet

International

DRIVING THE

CORE

STORE

PORTFOLIO

Marketing

Stor

e S

ervi

ce

Refurbishment

Product

Improving Customer Service

Competitor advertising spend increasing

Autumnand

SpringRanges

Competitiveenvironment

Strategy to improve core

store performance

ProductImprovement

Marketing &

Promotion

AcceleratedStore

Refurbishment

StoreService &Enablers

Department Store Performance

22

Store Refurbishment Programme

•

Refurbishment drives higher sales

•

Higher returns on capital employed

•

Improves linear conversion and visual merchandising

•

Focus on outfit building/ ATV

•

Designer merchandise displayed in a premium manner

•

Improving the customer experience

•

Clear brand delineation

Refurbishment Programme

Refurbished stores continue to out-perform core estate

Refurbishment Trial Store Analysis

6.5%

5.0% 5.0%

-

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

2004Average

2005Average

2006Average

Post

- Pr

e U

plift

ver

sus

Cor

e St

ores

Marketing

Stor

e S

ervi

ce

Refurbishment

Product

23

Accelerating the Refurbishment Programme with Elements of the Desire Shop Fit

•

Introducing the Desire fixtures and branding

•

Creating a more premium feel particularly around Designer ranges

•

Focused on own-bought brands

•

Significant investment in window upgrade and mannequins

•

New graphics and point of sale

•

62 stores identified for refurbishment

•

Programme accelerating

Store Refurbishment Programme

Marketing

Stor

e S

ervi

ce

Refurbishment

Product

24Department

StoresDesireStores

Roches

New type shop fit

25Department

StoresDesireStores

Roches

New type shop fit

26Department

StoresDesireStores

Roches

New type shop fit

27

New type shop fit

Marketing

Stor

e S

ervi

ce

Refurbishment

Product

28

New type shop fit

Marketing

Stor

e S

ervi

ce

Refurbishment

Product

29

Products

•

Menswear

•

Entry price points sharpened. C. 8% of range first half, c. 13%

of range 2nd

half

•

Resourced and renegotiated commodity lines

•

New Head of Buying appointed and team strengthened

•

Range improving but still work to complete

•

New brand launched –

Mantaray

•

Womenswear

•

Division strengthened and more focused by splitting into Casual and Formal

•

Outerwear mix changing into more smarter casual/formal

•

Faster lead times from Turkey

•

Gorgeous brand launched

•

Margins/markdown improving

First Half Sales Review –

Actions Taken

Marketing

Stor

e S

ervi

ce

Refurbishment

Product

30

Driving the Store Portfolio –

New Product Developments

48 stores

Launch of two new own-brands – Mantaray & Gorgeous

GorgeousMantaray

•

Roll-out phase to more stores

•

Improving own-bought mix

All stores

Marketing

Stor

e S

ervi

ce

Refurbishment

Product

31

Designers at Debenhams – aspirational products at affordable prices

•

Medium term target c. £450 million

•

On target

•

Betty Jackson –

introduced into Home

•

Julian Macdonald –

Menswear and Home

•

Jeff Banks –

Home

•

New Designer Brands Launching

Melissa Odabash

–

Swimwear/Accessories

Belle & Bunty

–

Childrenswear

•

Limited Edition –

raising the awareness and testing new price boundaries.

Driving the Store Portfolio –

Product Innovation & Development

Marketing

Stor

e S

ervi

ce

Refurbishment

Product

32

Sourcing Hub Development

Driving the Store Portfolio –

Supply Chain

Far East

58%

Europe

22%

Turkey 8%India 6%

Other 6%

Far East

54%

Europe

15%

Turkey

14%

India 10%

Other 7%

Far East

51%

Europe 9%

Turkey

22%

India 13%

Other 5%

NOW YR 1 Medium Term

Marketing

Stor

e S

ervi

ce

Refurbishment

Product

33

£5.7m investment in RF technology – live in all stores October 2007

•

Radio frequency backed price change management

•

Millions of items of stock with price changes

•

Reduction in man hours dedicated to price changes

•

Trials completed @ 6 stores

•

Reduction in man hours dedicated to price changes

•

Pricing Accuracy

•

Clearer Pricing

•

Consumer Friendly

•

Faster sell through at first markdown

•

Faster stock turn

•

Roll out to all stores completed by the end of October

Driving the Store Portfolio –

Improving the Service Model

Marketing

Stor

e S

ervi

ce

Refurbishment

Product

34

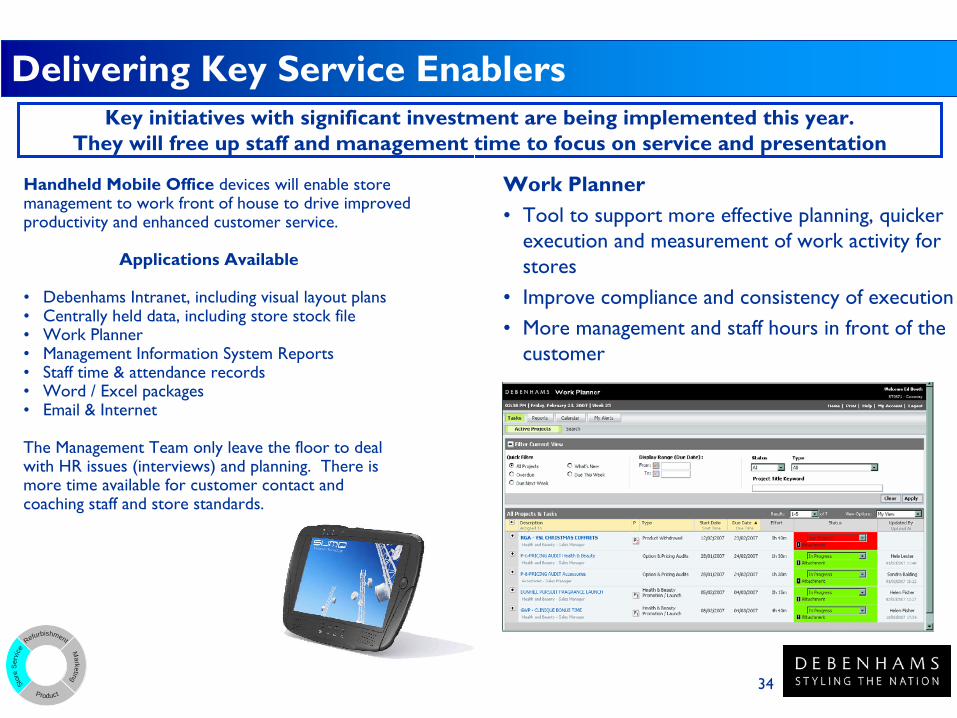

Key initiatives with significant investment are being implemented this year.

They will free up staff and management time to focus on service and presentation

Handheld Mobile Office

devices will enable store management to work front of house to drive improved productivity and enhanced customer service.

Applications Available

•

Debenhams Intranet, including visual layout plans•

Centrally held data, including store stock file•

Work Planner•

Management Information System Reports•

Staff time & attendance records•

Word / Excel packages•

Email & Internet

The Management Team only leave the floor to dealwith HR issues (interviews) and planning. There ismore time available for customer contact and coaching staff and store standards.

Work Planner

•

Tool to support more effective planning, quicker execution and measurement of work activity for stores

•

Improve compliance and consistency of execution

•

More management and staff hours in front of the customer

Delivering Key Service Enablers

Marketing

Stor

e S

ervi

ce

Refurbishment

Product

35

•

Substantial investment into new mannequins and window upgrade to showcase our products

•

Increase premium advertising and broadening our consumer reach•

Fashion Magazines

•

Home Magazines

•

Broadsheets and supplements

•

Home Catalogue

•

More emphasis on Style and Design

•

Store card relaunch

and upgrade on benefits•

Gold Card Upgrades

•

Higher Spend

•

Extra Benefits

•

Credit Card

•

Nectar Redemption•

Electronic Redemption

Driving the Store Portfolio -

Marketing

Marketing

Stor

e S

ervi

ce

Refurbishment

Product

36

New Space Growth –

New Department Stores

•

Potential for up to 240 stores

•

Flex size across deciles

•

Potential for new stores in big cities/towns such as:

•

Liverpool

•

Bath

•

Peterborough

•

Solihull

•

Poole

•

Stevenage

•

Strong contracted pipeline of new stores

•

New Development opportunities

•

High ROIC achieved on new stores

Debenhams is not represented in many key towns across the UK

DepartmentStores

DesireStores

Roches

37

Physically immature business with a strong pipeline of new stores

Presence in Top 500 UK Catchment Areas 29 Contracted New Store Pipeline

Source: Company Information Note(1) Re-sites(2) Excludes Roches acquisition(3) EBITDA on net capital invested

2006

/07

Bury St Edmunds Harlow

2008

/09

Newport

2009

/10

Crewe

Derby*

2007

/08

Carmarthen Ashford BlackpoolGlasgowPollokExeter* WrexhamBangor

(Wales)* Liverpool Dunfermline

Newbridge** DoncasterAyr**

2005

/06

WorkingtonHemel**

Wolverhampton

2010

/11

Newport

2009

/10

CreweNewport

2009

/10

Crewe

Derby*

2007

/08

Carmarthen Ashford BlackpoolGlasgowPollokExeter* WrexhamBangor

(Wales)* Liverpool DunfermlineDerby(1)

2007

/08

Carmarthen Ashford BlackpoolGlasgowPollokExeter(1) LlanelliBangor

(Wales)(1) Liverpool

Newbridge DoncasterAyr

2005

/06

WorkingtonHemel

12

10

6

8

132 Department Stores

3

Dunfermline

Bradford

Livingstone Bury

Wakefield Litchfield

BarnsleyLancaster

Llandudno Wigan(1)Warrington

40

32

19

9 84

16

7

8

7

10

5

1

1

5

5

19

17

14

13

6

1 0

4

12 00

10

20

30

40

50

1 2 3 4 5 6 7 8 9 10 NI / EIREDeciles of top 500 catchment areas

Stor

es

Potential SitesContracted or under NegotiationExisting Debenhams Stores

9 Roches Stores (Dublin, Cork, Waterford, Tallaght, Blanchardstown,

Galway, Limerick, Tralee, Blackrock )

NewcastleUpon Tyne Wood Green

Wrexham

New Space Growth –

New Department Stores

WhiteCity

Bath

Pre tax ROCE (2)

(3)

•

2004/05

36%•

2005/06

49%

DepartmentStores

DesireStores

Roches

38

Llandudno Photos

DepartmentStores

DesireStores

Roches

39

Llandudno Photos

DepartmentStores

DesireStores

Roche

40

Llandudno Photos

DepartmentStores

DesireStores

Roches

41

A unique concept with capacity for c.100 stores in high street and retail park locations

Clear Positioning flexed by market Desire Roll Out

Desire vs Department Stores

•

Target 15-20k sq ft

•

Town centre locations will be priority

•

Childrenswear will be part of core mix

•

Douwe

Egberts

Café

only if tertiary space is available

•

Range of accessories will be expanded

•

Refining the product offer

2004/05 Truro

2005/06 South Shields Orpington Falkirk

2006/07 The Fort, BirminghamMerthyr TydfilKirkcaldy AltrinchamWalton on Thames

•

Higher sales densities

•

Higher gross margin

•

Own-bought mix c. 93%

•

EBITDA margin in line with department stores.

New Space Growth –

New Desire Stores

2007/08 BallymenaFarehamWitneyWelwyn Garden CityNewton AbbeyGreat Yarmouth

DepartmentStores

DesireStores

Roches

0

2

4

6

8

10

12

04/05 05/06 06/07 07/08 08/09 09/10

Trading Year

Num

ber o

f Des

ire S

tore

sOpen Signed In Negotiation Planned

42

Desire

DepartmentStores

DesireStores

Roches

43

Desire

DepartmentStores

DesireStores

Roches

44

Desire

DepartmentStores

DesireStores

Roches

45

Desire

DepartmentStores

DesireStores

Roches

46

Desire

DepartmentStores

DesireStores

Roches

47

The R.O.I. is a growth opportunity –

Roches acquisition gives us scale

•

Acquired 9 stores as an asset purchase, 595 sq. ft. of new retail space.

•

Paid €29 million for assets

•

Integration process on schedule

•

All Stores now trading as Debenhams•

7 out of 9 stores completed first phase of refit to Debenhams•

All stores completed by year end•

Systems operational

•

Further work to complete on concessions

•

Earnings enhancing next year

Space Growth –

Roches Acquisition

DepartmentStores

DesireStores

Roches

48

Roches

DepartmentStores

DesireStores

Roches

Before After

Cork

Waterford

49

•

35 stores in 16 countries with a further 17 contracted locations

•

New stores opened in Russia, Germany and Romania

•

Strong opening programme and cash generation from International franchise stores at low risk

•

Significant opportunity to roll out Desire Stores internationally

•

Review order taking process and supply chain as scale grows

•

New countries –

Abu Dhabi, India, Jordan, Singapore, Malta

Strategy

4 7 9 14 1829

4047

57

0

10

20

30

40

50

60

70

80

00/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/7 2007/8 2008/9

Number of Contracted stores

70

International stores represent a considerable opportunity and there is a large opening programme for the forthcoming years

International Store Growth:

New Channel Growth –

International Franchises

Internet

International

50

5.9%

19.3%

13.4%

6.2%

26.8%29.4%

14.3%

(8.1%)

(2.6%)

-10.0%

0.0%

10.0%

20.0%

30.0%

Pre Period Post Period Uplift

% v

ersu

s La

st Y

ear

Orders Average Order Value Demand

Web Upgrade

•

Reliable site with the stability to manage our higher demand levels

•

Improved site navigation and cross selling

•

Improved availability of ranges to a wider audience

•

Developed Cosmetics micro sites

•

Uplift in order numbers and ATV. EBITDA up 12.9%

Demand Growth Uplift

Our new website has significant growth potential

Internet

International

51

Total sales six weeks to 15/4/07 + 2.9%

Like for like sales six weeks to 15/4/07

-

6.9%

Actions taken to improve sales performance•

Store refurbishment programme accelerating

•

New initiatives around customer service

•

New own-bought brands launching aimed at younger market

•

Product teams strengthened

New Space Growth

Internet

Outlook