interest rate and purchasing power parity

DESCRIPTION

FinanceTRANSCRIPT

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-1

Interest Rate Parity Defined

IRP is an arbitrage condition. If IRP did not hold, then it would be possible for

an astute trader to make unlimited amounts of money exploiting the arbitrage opportunity.

Since we don’t typically observe persistent arbitrage conditions, we can safely assume that IRP holds.

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-2

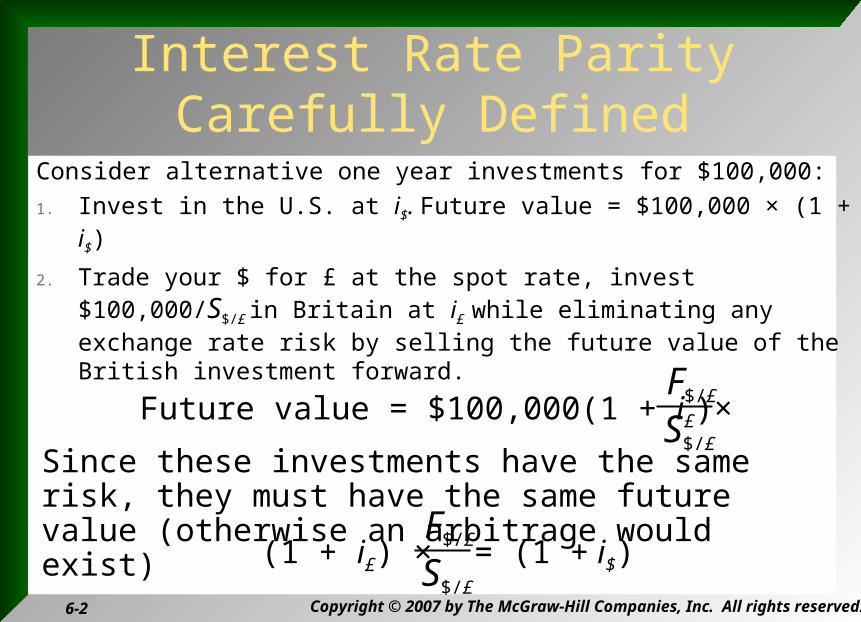

Interest Rate Parity Carefully Defined

Consider alternative one year investments for $100,000:

1. Invest in the U.S. at i$. Future value = $100,000 × (1 + i$)

2. Trade your $ for £ at the spot rate, invest $100,000/S$/£ in Britain at i£ while eliminating any exchange rate risk by selling the future value of the British investment forward.

S$/£

F$/£Future value = $100,000(1 + i£)×

S$/£

F$/£(1 + i£) × = (1 + i$)

Since these investments have the same risk, they must have the same future value (otherwise an arbitrage would exist)

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-3

IRP

Invest those pounds at i£

$1,000

S$/£

$1,000

Future Value =

Step 3: repatriate future value to the

U.S.A.

Since both of these investments have the same risk, they must have the same future value—otherwise an arbitrage would exist

Alternative 1: invest $1,000 at i$ $1,000×(1 + i$)

Alternative 2:Send your $ on a round trip to Britain

Step 2:

$1,000

S$/£

(1+ i£) × F$/£

$1,000

S$/£

(1+ i£)

=

IRP

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-4

Interest Rate Parity Defined

The scale of the project is unimportant

(1 + i$) F$/£

S$/£

× (1+ i£)=

$1,000×(1 + i$) $1,000

S$/£

(1+ i£) × F$/£=

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-5

Interest Rate Parity Defined

Formally,

IRP is sometimes approximated as

i$ – i¥ ≈S

F – S

1 + i$

1 + i¥ S$/¥

F$/¥=

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-6

Forward Premium

It’s just the interest rate differential implied by forward premium or discount.

For example, suppose the € is appreciating from S($/€) = 1.25 to F180($/€) = 1.30

The forward premium is given by:

F180($/€) – S($/€) S($/€) ×

360180

f180,€v$ = =$1.30 – $1.25

$1.25 × 2 = 0.08

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-7

Interest Rate Parity Carefully Defined

Depending upon how you quote the exchange rate ($ per ¥ or ¥ per $) we have:

1 + i$

1 + i¥

S¥/$

F¥/$ =1 + i$

1 + i¥ S$/¥

F$/¥=or

…so be a bit careful about that

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-8

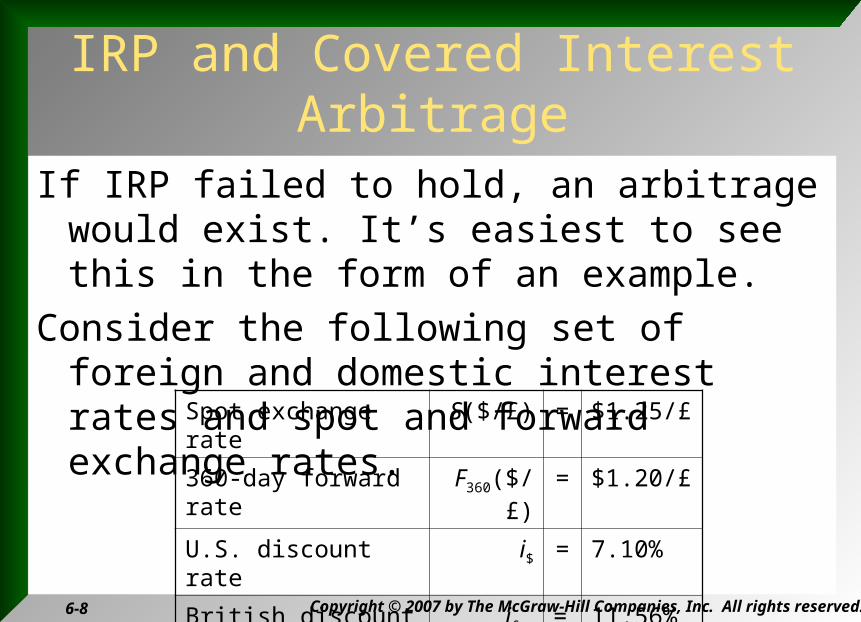

IRP and Covered Interest Arbitrage

If IRP failed to hold, an arbitrage would exist. It’s easiest to see this in the form of an example.

Consider the following set of foreign and domestic interest rates and spot and forward exchange rates.

Spot exchange rate S($/£) = $1.25/£

360-day forward rate F360($/£) = $1.20/£

U.S. discount rate i$ = 7.10%

British discount rate i£ = 11.56%

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-9

IRP and Covered Interest Arbitrage

A trader with $1,000 could invest in the U.S. at 7.1%, in one year his investment will be worth

$1,071 = $1,000 (1+ i$) = $1,000 (1,071)

Alternatively, this trader could

1. Exchange $1,000 for £800 at the prevailing spot rate,

2. Invest £800 for one year at i£ = 11.56%; earn £892.48.

3. Translate £892.48 back into dollars at the forward rate F360($/£) = $1.20/£, the £892.48 will be exactly $1,071.

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-10

Arbitrage I

Invest £800 at i£ = 11.56%

$1,000

£800

£800 = $1,000×$1.25

£1

In one year £800 will be worth

£892.48 = £800 (1+ i£)

$1,071 = £892.48 ×£1

F£(360)

Step 3: repatriate to the U.S.A. at

F360($/£) = $1.20/£ Alternative 1:

invest $1,000 at 7.1%FV = $1,071

Alternative 2:buy pounds

Step 2:

£892.48

$1,071

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-11

Interest Rate Parity & Exchange Rate Determination

According to IRP only one 360-day forward rate, F360($/£), can exist. It must be the case that

F360($/£) = $1.20/£

Why?

If F360($/£) $1.20/£, an astute trader could make money with one of the following strategies:

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-12

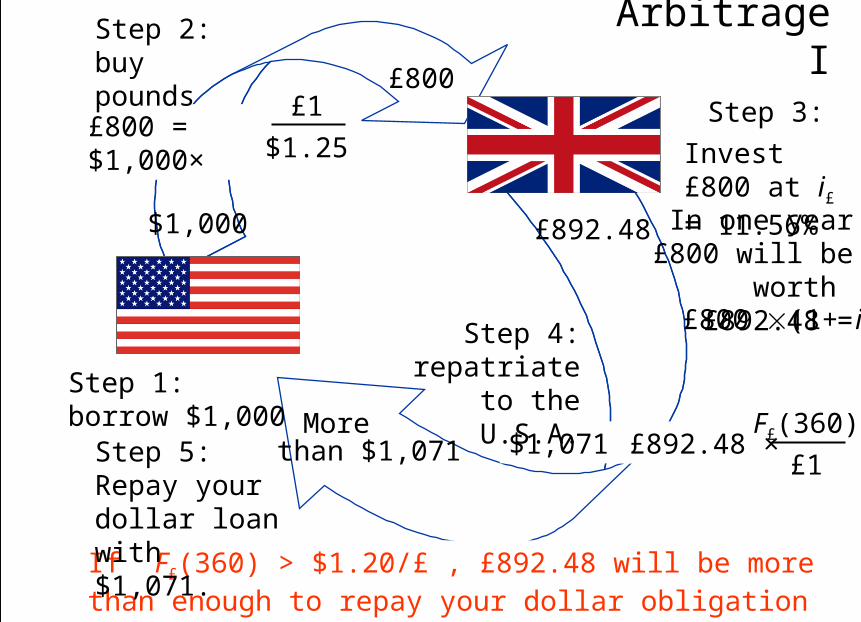

Arbitrage Strategy I

If F360($/£) > $1.20/£

i. Borrow $1,000 at t = 0 at i$ = 7.1%.

ii. Exchange $1,000 for £800 at the prevailing spot rate, (note that £800 = $1,000÷$1.25/£) invest £800 at 11.56% (i£) for one year to achieve £892.48

iii. Translate £892.48 back into dollars, if

F360($/£) > $1.20/£, then £892.48 will be more than enough to repay your debt of $1,071.

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-13

Arbitrage I

Invest £800 at i£ = 11.56%

$1,000

£800

£800 = $1,000×$1.25

£1

In one year £800 will be worth

£892.48 = £800 (1+ i£)

$1,071 < £892.48 ×£1

F£(360)

Step 4: repatriate to the U.S.A.

If F£(360) > $1.20/£ , £892.48 will be more than enough to repay your dollar obligation of $1,071. The excess is your profit.

Step 1: borrow $1,000

Step 2:buy pounds

Step 3:

Step 5: Repay your dollar loan with $1,071.

£892.48

More than $1,071

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-14

Arbitrage Strategy II

If F360($/£) < $1.20/£

i. Borrow £800 at t = 0 at i£= 11.56% .

ii. Exchange £800 for $1,000 at the prevailing spot rate, invest $1,000 at 7.1% for one year to achieve $1,071.

iii. Translate $1,071 back into pounds, if

F360($/£) < $1.20/£, then $1,071 will be more than enough to repay your debt of £892.48.

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-15

Arbitrage II

$1,000

£800

$1,000 = £800×£1

$1.25

In one year $1,000 will be worth $1,071 > £892.48 ×

£1

F£(360)

Step 4: repatriate to

the U.K.

If F£(360) < $1.20/£ , $1,071 will be more than enough to repay your dollar obligation of £892.48. Keep the rest as profit.

Step 1: borrow £800

Step 2:buy dollars

Invest $1,000 at i$

Step 3:Step 5: Repay

your pound loan with £892.48 .

$1,071

More than £892.48

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-16

IRP and Hedging Currency Risk

You are a U.S. importer of British woolens and have just ordered next year’s inventory. Payment of £100M is due in one year.

IRP implies that there are two ways that you fix the cash outflow to a certain U.S. dollar amount:

a) Put yourself in a position that delivers £100M in one year—a long forward contract on the pound. You will pay (£100M)(1.2/£) = $120M in one year.

b) Form a forward market hedge as shown below.

Spot exchange rate S($/£) = $1.25/£

360-day forward rate F360($/£) = $1.20/£

U.S. discount rate i$ = 7.10%

British discount rate i£ = 11.56%

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-17

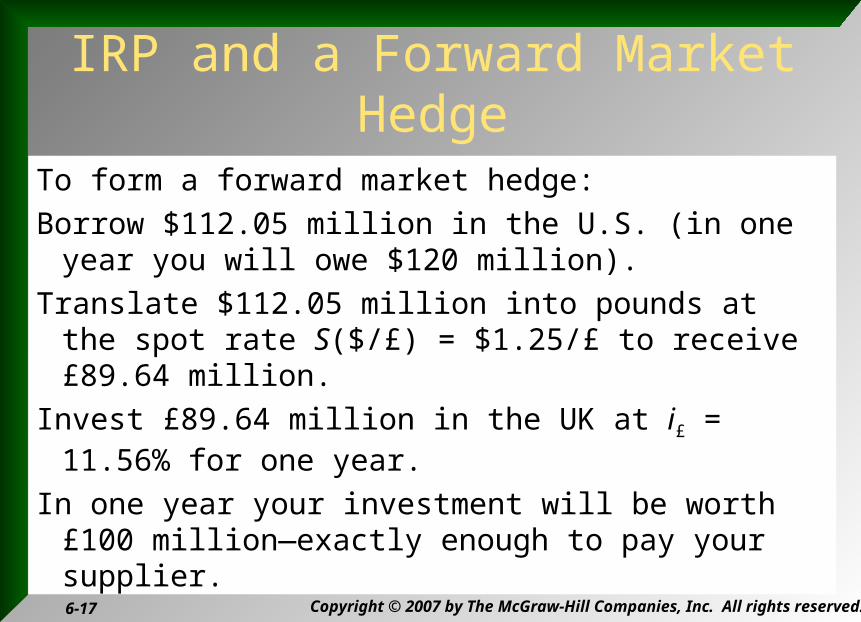

IRP and a Forward Market Hedge

To form a forward market hedge:

Borrow $112.05 million in the U.S. (in one year you will owe $120 million).

Translate $112.05 million into pounds at the spot rate S($/£) = $1.25/£ to receive £89.64 million.

Invest £89.64 million in the UK at i£ = 11.56% for one year.

In one year your investment will be worth £100 million—exactly enough to pay your supplier.

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-18

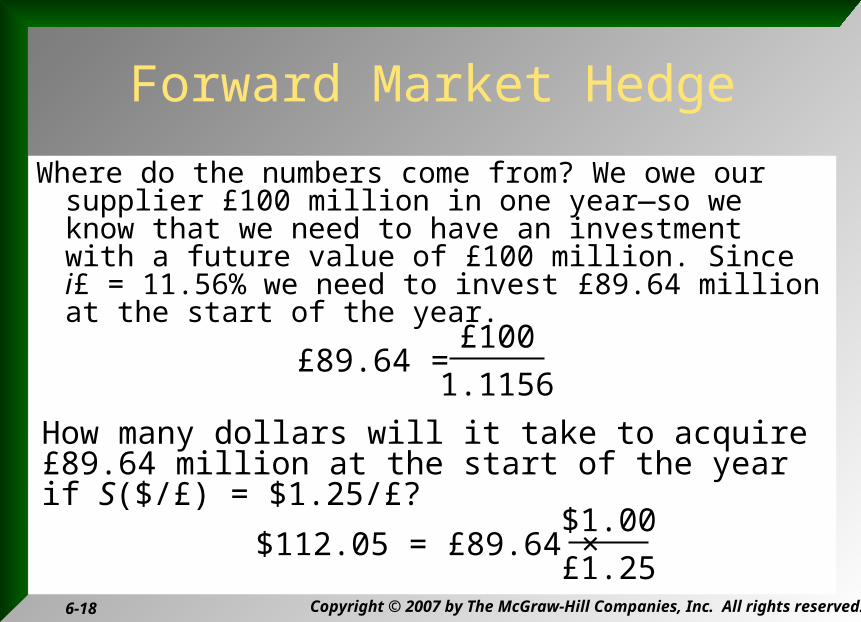

Forward Market Hedge

Where do the numbers come from? We owe our supplier £100 million in one year—so we know that we need to have an investment with a future value of £100 million. Since i£ = 11.56% we need to invest £89.64 million at the start of the year.

How many dollars will it take to acquire £89.64 million at the start of the year if S($/£) = $1.25/£?

£89.64 = £100

1.1156

$112.05 = £89.64 × $1.00

£1.25

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-19

Reasons for Deviations from IRP

Transactions Costs The interest rate available to an arbitrageur for

borrowing, ib,may exceed the rate he can lend at, il. There may be bid-ask spreads to overcome, Fb/Sa < F/S Thus

(Fb/Sa)(1 + i¥l) (1 + i¥

b) 0 Capital Controls

Governments sometimes restrict import and export of money through taxes or outright bans.

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-20

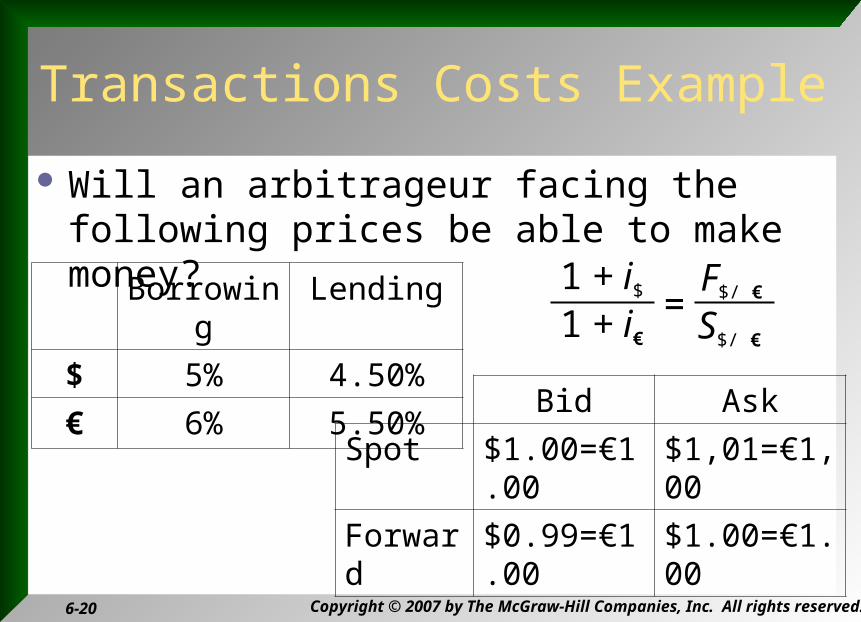

Transactions Costs Example

Will an arbitrageur facing the following prices be able to make money?

Borrowing Lending

$ 5% 4.50%

€ 6% 5.50% Bid Ask

Spot $1.00=€1.00 $1,01=€1,00

Forward $0.99=€1.00 $1.00=€1.00

1 + i$

1 + i€ S$/ €

F$/ €=

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-21

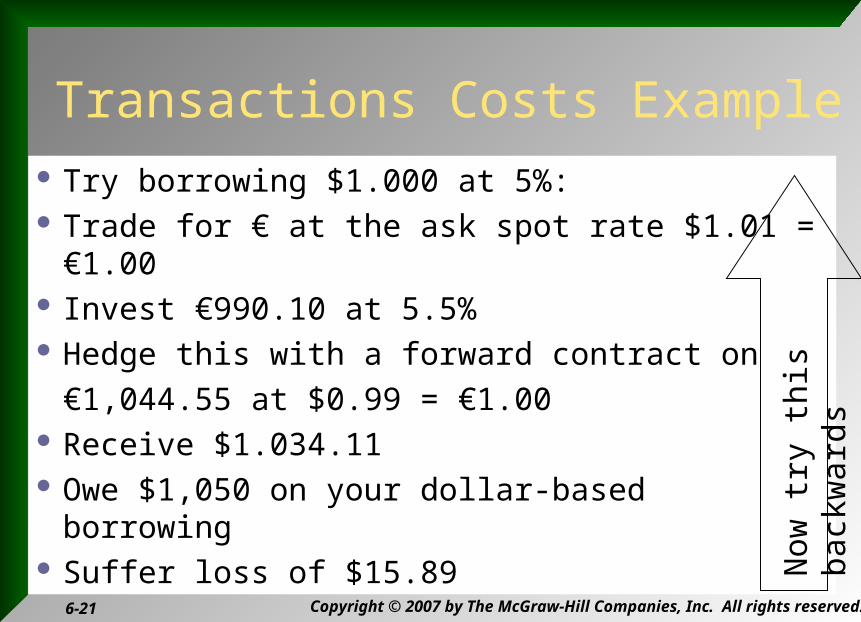

Try borrowing $1.000 at 5%: Trade for € at the ask spot rate $1.01 = €1.00 Invest €990.10 at 5.5% Hedge this with a forward contract on

€1,044.55 at $0.99 = €1.00 Receive $1.034.11 Owe $1,050 on your dollar-based borrowing Suffer loss of $15.89

Transactions Costs Example

Now

try

this

bac

kwar

ds

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-22

'Uncovered Interest Rate Parity

Parity condition stating that the difference in interest rates between two countries is equal to the expected change in exchange rates between the countries’ currencies. If this parity does not exist, there is an opportunity to make a profit."i1" represents the interest rate of country 1"i2" represents the interest rate of country 2"E(e)" represents the expected rate of change in the exchange rate

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-23

E.g. assume that the interest rate in America is 10% and the interest rate in Canada is 15%. According to the uncovered interest rate parity, the Canadian dollar is expected to depreciate against the American dollar by approximately 5%. Put another way, to convince an investor to invest in Canada when its currency depreciates, the Canadian dollar interest rate would have to be about 5% higher than the American dollar interest rate.

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-24

Purchasing Power Parity

PPP suggests that the purchasing power of a consumer will be similar when purchasing goods in a foreign country or in the home country. If inflation in a foreign country differs from inflation in the home country, the exchange rate will adjust to maintain equal purchasing power.

Currencies in countries with high inflation will be weak according to PPP, causing the purchasing power of goods in the home country versus these countries to be similar.

Inflation differentials are offset by exchange rate changes.

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-25

Absolute Purchasing Power Parity

This concept posits that the exchange rate between two countries will be identical to the ratio of the price levels for those two countries. This concept is derived from a basic idea known as the law of one price, which states that the real price of a good must be the same across all countries

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-26

Big Mac index

The Economist, which compares the prices of a Big Mac burger in McDonald's restaurants in different countries. The Big Mac Index is presumably useful because although it is based on a single consumer product that may not be typical, it is a relatively standardized product that includes input costs from a wide range of sectors in the local economy, such as agricultural commodities (beef, bread, lettuce, cheese), labor (blue and white collar), advertising, rent and real estate costs, transportation, etc.

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-27

Purchasing Power Parity and Exchange Rate Determination

The exchange rate between two currencies should equal the ratio of the countries’ price levels:

S($/£) = P£

P$

S($/£) = P£

P$

£150$300

= = $2/£

For example, if an ounce of gold costs $300 in the U.S. and £150 in the U.K., then the price of one pound in terms of dollars should be:

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-28

Relative purchasing power parity

Relative purchasing power parity relates the change in two countries' expected inflation rates to the change in their exchange rates. Inflation reduces the real purchasing power of a nation's currency. If a country has an annual inflation rate of 10%, that country's currency will be able to purchase 10% less real goods at the end of one year

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-29

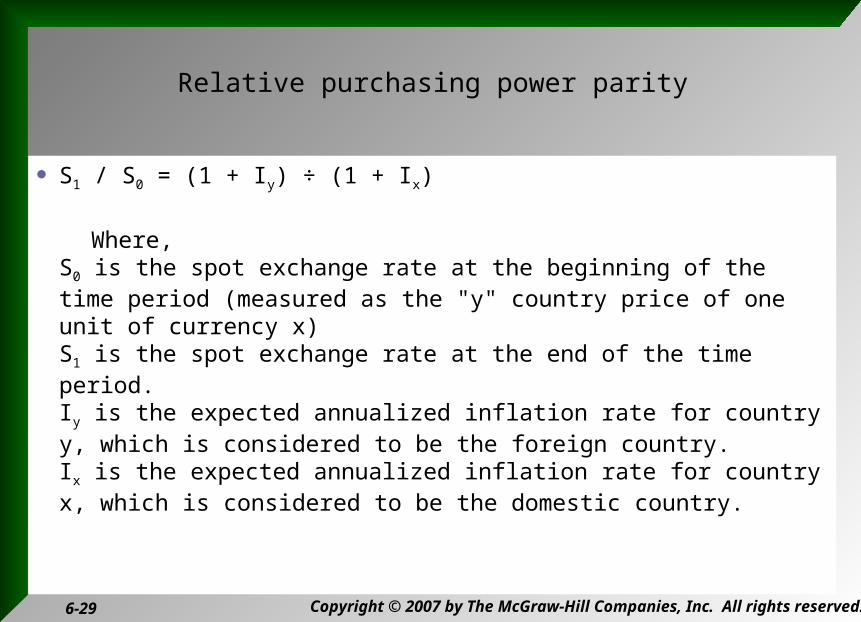

Relative purchasing power parity

S1 / S0 = (1 + Iy) ÷ (1 + Ix)

Where,S0 is the spot exchange rate at the beginning of the time period (measured as the "y" country price of one unit of currency x)S1 is the spot exchange rate at the end of the time period.Iy is the expected annualized inflation rate for country y, which is considered to be the foreign country.Ix is the expected annualized inflation rate for country x, which is considered to be the domestic country.

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-30

Purchasing Power Parity and Exchange Rate Determination

Suppose the spot exchange rate is $1.25 = €1.00 If the inflation rate in the U.S. is expected to be

3% in the next year and 5% in the euro zone, Then the expected exchange rate in one year

should be $1.25×(1.03) = €1.00×(1.05)

F($/€) = $1.25×(1.03)€1.00×(1.05)

$1.23€1.00

=

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-31

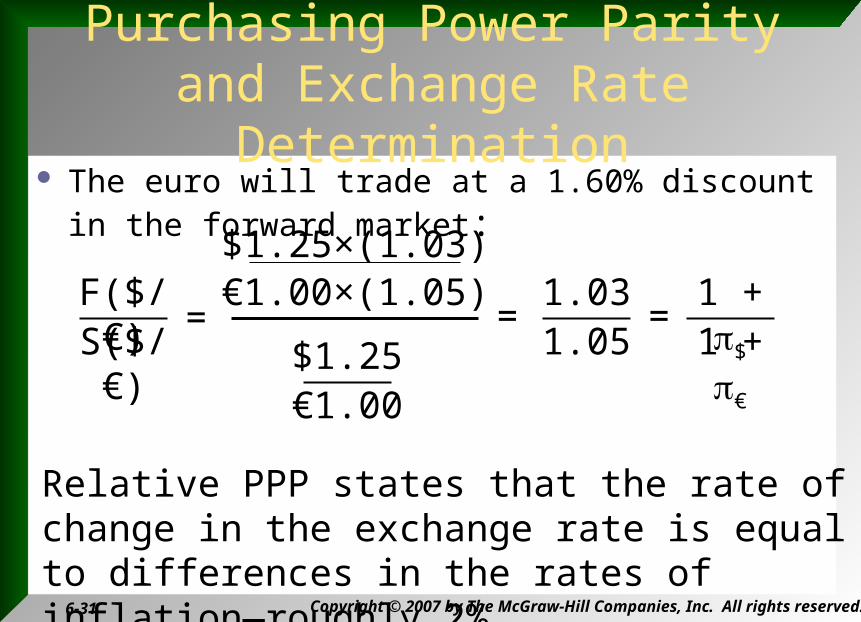

Purchasing Power Parity and Exchange Rate Determination

The euro will trade at a 1.60% discount in the forward market:

$1.25€1.00

= F($/€)S($/€)

$1.25×(1.03)€1.00×(1.05) 1.03

1.051 + $

1 + €

= =

Relative PPP states that the rate of change in the exchange rate is equal to differences in the rates of inflation—roughly 2%

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-32

Brainstorming

Japan has typically had lower inflation than the United States. How would one expect this to affect the Japanese yen’s value? Why does this expected relationship not always occur?

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-33

Solution

Japan’s low inflation should place upward pressure on the yen’s value. Yet, other factors can sometimes offset this pressure. For example, Japan heavily invests in U.S. securities, which places downward pressure on the yen’s value.

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-34

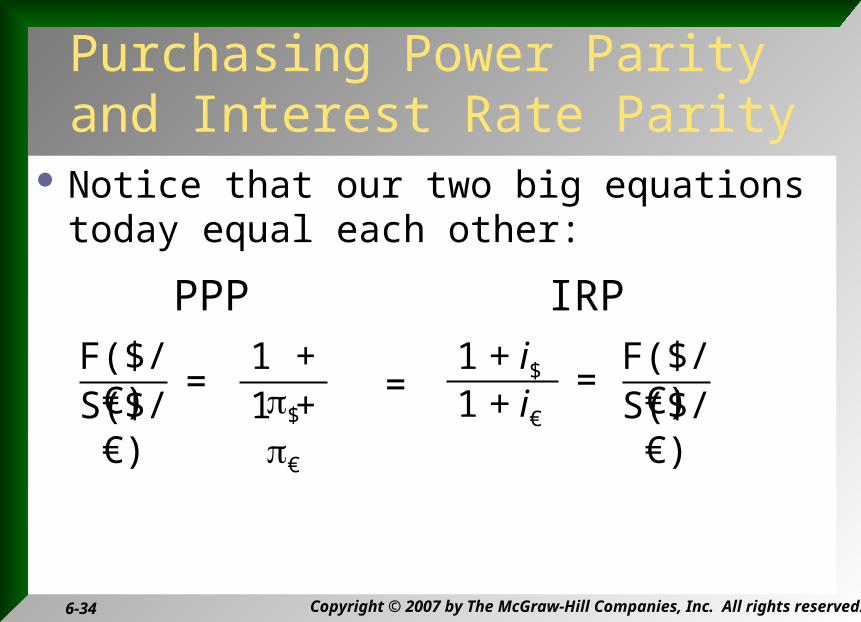

Purchasing Power Parity and Interest Rate Parity

Notice that our two big equations today equal each other:

= = F($/€)S($/€)

1 + $

1 + €

PPP

1 + i€

1 + i$ =F($/€)S($/€)

IRP

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-35

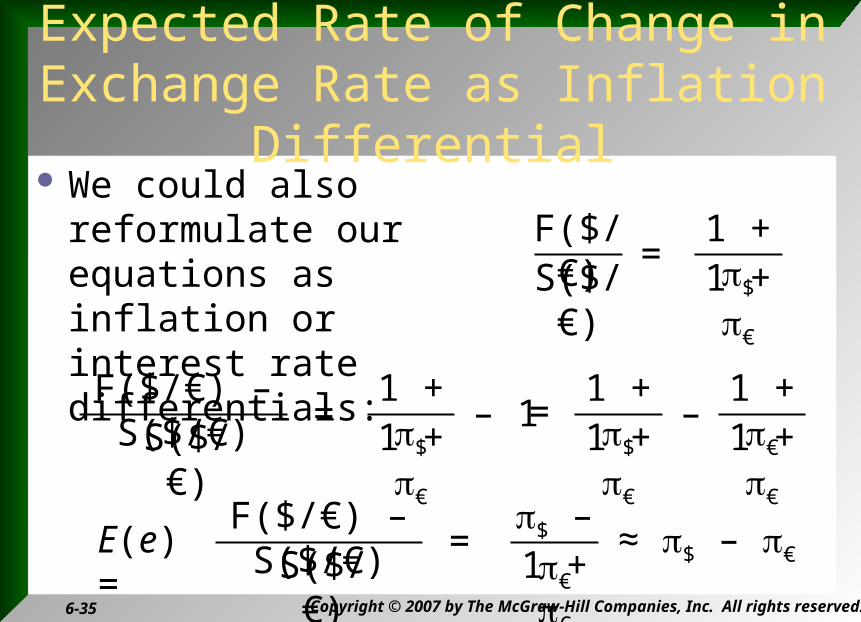

Expected Rate of Change in Exchange Rate as Inflation Differential

We could also reformulate our equations as inflation or interest rate differentials:

= F($/€) – S($/€)

S($/€)1 + $

1 + €

– 1 = 1 + $

1 + €

–

1 + €

1 + €

= F($/€)S($/€)

1 + $

1 + €

= F($/€) – S($/€)

S($/€)$ – €

1 + €

E(e) = ≈ $ – €

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-36

Expected Rate of Change in Exchange Rate as Interest Rate Differential

= F($/€) – S($/€)

S($/€)i$ – i€

1 + i€E(e) = ≈ i$ – i€

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-37

Quick and Dirty Short Cut

Given the difficulty in measuring expected inflation, managers often use

≈ i$ – i€$ – €

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-38

Brainstorming

Assume that the nominal interest rate in Mexico is 48 percent and the interest rate in the United States is 8 percent for one‑year securities that are free from default risk. Describe the expected nominal return to U.S. investors who invest in Mexico.

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-39

Solution

According to PPP, the Mexican peso should depreciate by the amount of the differential between U.S. and Mexican inflation rates. Using a 40 percent differential, the Mexican peso should depreciate by about 40 percent. Given a 48 percent nominal interest rate in Mexico and expected depreci ation of the peso of 40 percent, U.S. investors will earn about 8 percent.

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved. 6-40

Evidence on PPP

PPP probably doesn’t hold precisely in the real world for a variety of reasons. Haircuts cost 10 times as much in the developed world as in the

developing world. Film, on the other hand, is a highly standardized commodity that is

actively traded across borders. Shipping costs, as well as tariffs and quotas can lead to deviations from

PPP. There may not be substitutes for traded goods. Therefore, even when a

country’s inflation increases, the foreign demand for its products will not necessarily decrease (in the manner sug gested by PPP) if substitutes are not available.

PPP-determined exchange rates still provide a valuable benchmark.