mwf 3:15-4:30 gates b01 handout #7 international parity ... week posting... · international parity...

TRANSCRIPT

Course web page: http://Stanford2008.pageout.net

Handout #7

International Parity ConditionsInterest Rate Parity and the Fisher Parities

MWF 3:15-4:30 Gates B01

Slides to highlight: 4-15, 21-27, 39-43, 60-69, 81-84,95-105, 112, 114, 120.

Yee-Tien “Ted” Fu

5-2

Levich

Luenberger

Solnik

Eun

Wooldridge

Additional Reading Assignments for this Week

Chap 5

Chap

Chap 2

Chap 7

Scan Read

Pages

Pages

Pages

Pages

Chap 9 Pages

Foreign Exchange Parity Relations

International Parity Conditions

Multiple Regression Analysis with Qualitative Information: Binary (or Dummy) Variables

http://highered.mcgraw-hill.com/sites/dl/free/0072521279/91312/eun21279_ch09_dr.pdf

5-3

World Interest Rates Table

7.25%Mar 04 2008Aug 05 2008The Reserve Bank of Australia

2.75%Sep 13 2007Sep 18 2008Swiss National Bank

2%Apr 30 2008Aug 05 2008Federal Reserve

4.25%Jul 03 2008Aug 07 2008European Central Bank

0.5%Feb 21 2007Jul 15 2008Bank of Japan

5%Apr 10 2008Jul 10 2008Bank of England

3%Apr 22 2008Jul 15 2008Bank of Canada

Current Interest RateLast ChangeNext MeetingCentral Bank

Major Central Banks Overview

http://www.fxstreet.com/fundamental/interest-rates-table/

5-4

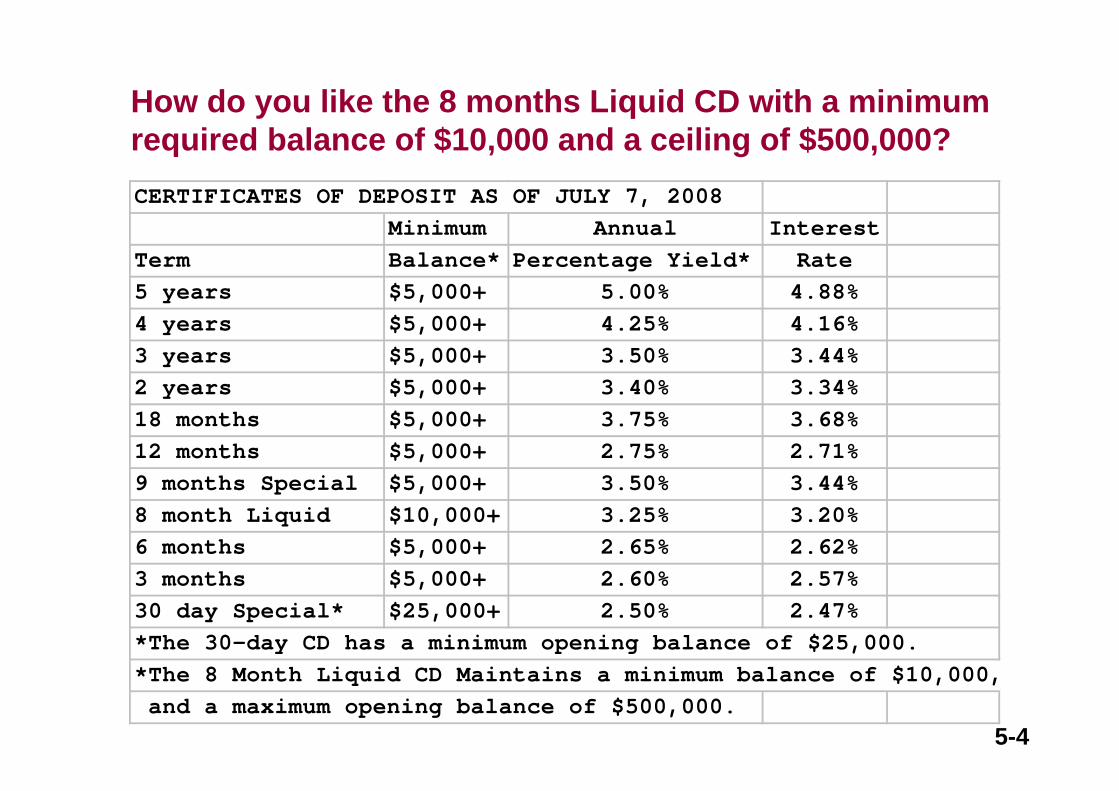

CERTIFICATES OF DEPOSIT AS OF JULY 7, 2008Minimum Annual Interest

Term Balance* Percentage Yield* Rate5 years $5,000+ 5.00% 4.88%4 years $5,000+ 4.25% 4.16%3 years $5,000+ 3.50% 3.44%2 years $5,000+ 3.40% 3.34%18 months $5,000+ 3.75% 3.68%12 months $5,000+ 2.75% 2.71%9 months Special $5,000+ 3.50% 3.44%8 month Liquid $10,000+ 3.25% 3.20%6 months $5,000+ 2.65% 2.62%3 months $5,000+ 2.60% 2.57%30 day Special* $25,000+ 2.50% 2.47%*The 30-day CD has a minimum opening balance of $25,000.*The 8 Month Liquid CD Maintains a minimum balance of $10,000, and a maximum opening balance of $500,000.

How do you like the 8 months Liquid CD with a minimum required balance of $10,000 and a ceiling of $500,000?

5-5

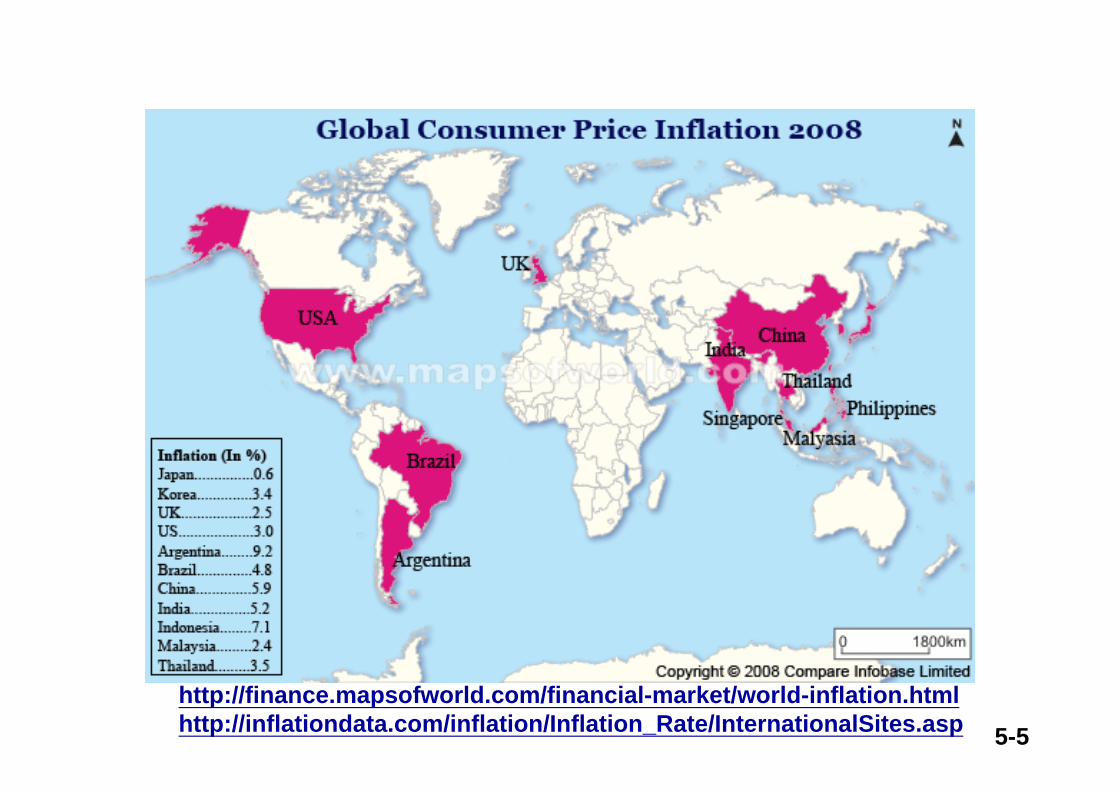

http://finance.mapsofworld.com/financial-market/world-inflation.htmlhttp://inflationdata.com/inflation/Inflation_Rate/InternationalSites.asp

5-6

Exchange Rates Table

http://www.x-rates.com/

5-7

July 2007

http://www.economist.com/markets/bigmac/

5-8

International Parity Relations Linear Approximationwhere Spot Rate S are in indirect quote (FC/DC or FC/$)

Solnik 2.1

Interest Rate Parity

Forward Rate Unbiased Property

Uncovered Interest Parityor Fisher International Effect

Purchasing Power Parity (relative version) PPP

IRPFIE

FRU

5-9

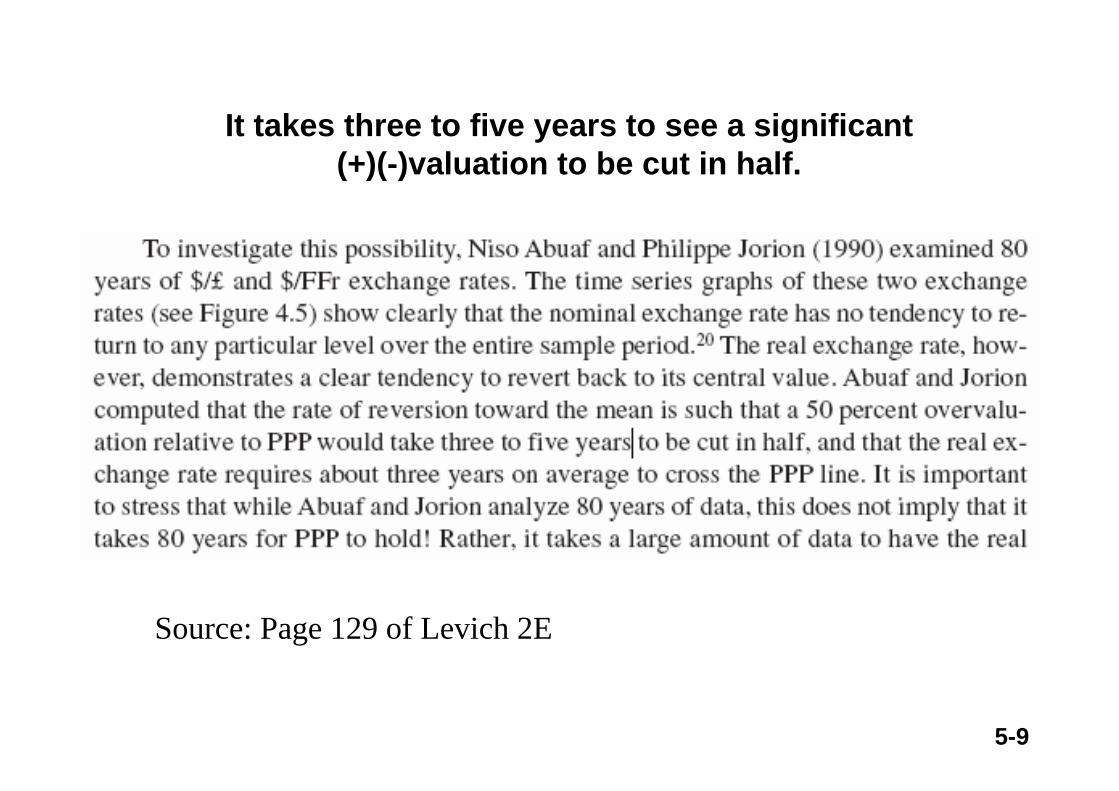

Source: Page 129 of Levich 2E

It takes three to five years to see a significant (+)(-)valuation to be cut in half.

Foreign Exchange MarketsInternational Parity Conditions

Interest Rate Parity and the Fisher Parities

MS&E 247S International InvestmentsYee-Tien (Ted) Fu

5-11

The long run is a misleading guide to current affairs. In the long run we are all dead. Economists set themselves too easy, too useless a task if in tempestuous seasons they can only tell us when the storm is long past, the ocean will be flat.

- John Maynard Keynes

Long-Run versus Short-Run

5-12

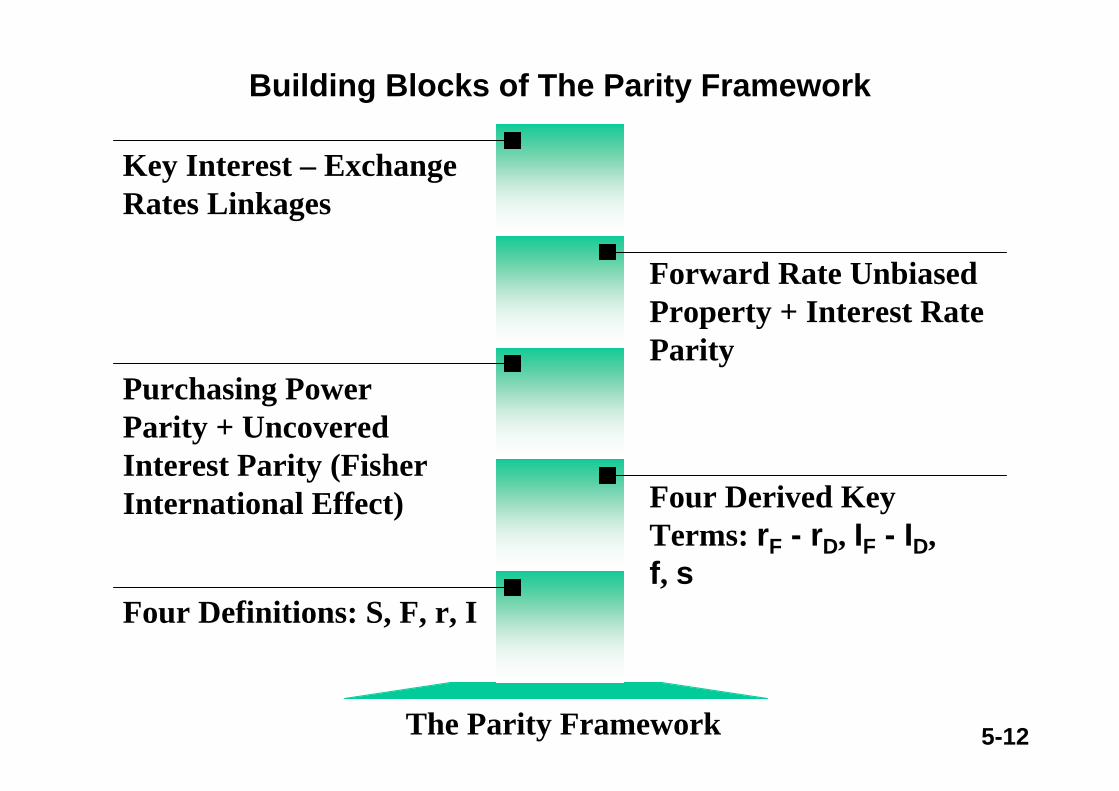

Building Blocks of The Parity Framework

The Parity Framework

Four Definitions: S, F, r, I

Four Derived Key Terms: rF - rD, IF - ID,f, s

Purchasing Power Parity + Uncovered Interest Parity (Fisher International Effect)

Forward Rate Unbiased Property + Interest Rate Parity

Key Interest – Exchange Rates Linkages

5-13

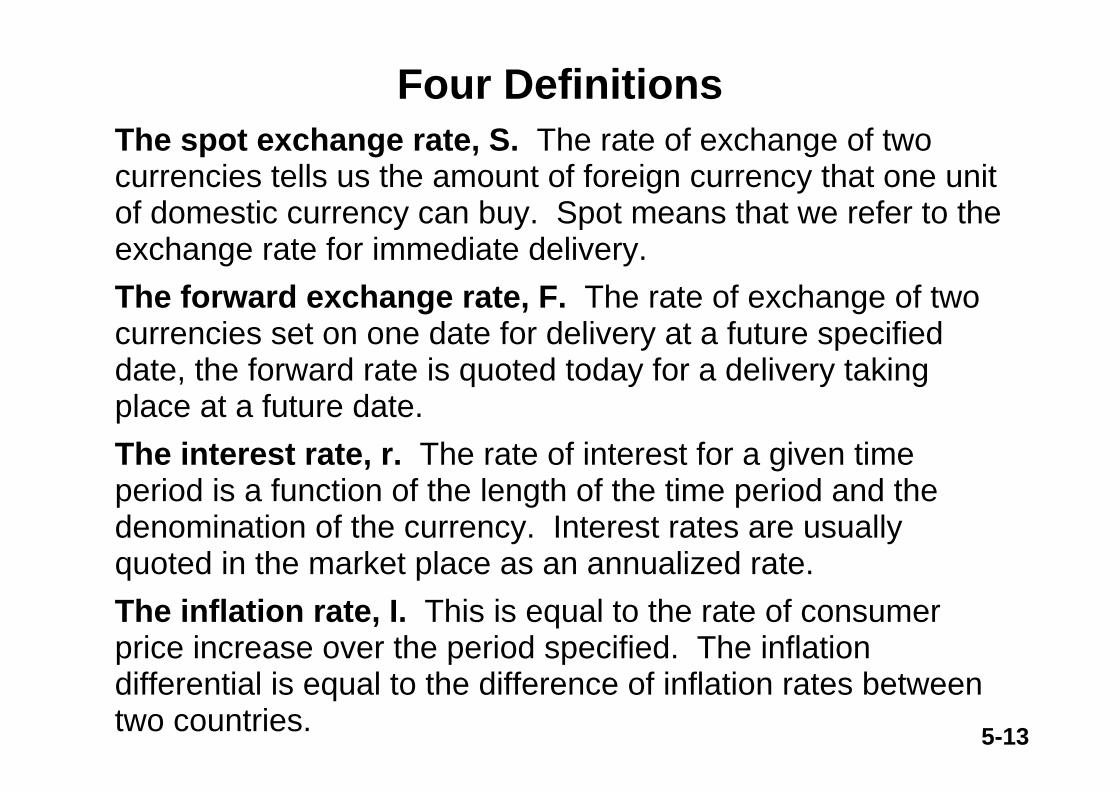

Four DefinitionsThe spot exchange rate, S. The rate of exchange of two currencies tells us the amount of foreign currency that one unitof domestic currency can buy. Spot means that we refer to the exchange rate for immediate delivery.The forward exchange rate, F. The rate of exchange of two currencies set on one date for delivery at a future specified date, the forward rate is quoted today for a delivery taking place at a future date.The interest rate, r. The rate of interest for a given time period is a function of the length of the time period and the denomination of the currency. Interest rates are usually quoted in the market place as an annualized rate.The inflation rate, I. This is equal to the rate of consumer price increase over the period specified. The inflation differential is equal to the difference of inflation rates between two countries.

5-14

The interest rate differential, rF - rD. The interest rate differential is equal to the difference in interest rates between two countries.

The inflation differential, IF - ID. The inflation differential is equal to the difference of inflation rates between two countries.

The forward discount or premium, f. This is often calculated as an annualized percentage deviation from the spot rate:

The exchange rate movement, s. This is equal to the spot exchange rate movement over the period specified. f = (F-S0)/S0 and s = (S1-S0)/S0

Four Derived Key Terms

annualized forward premium (discount)

forward rate - spot ratespot rate

= × × 100 %12no. months forward

5-15

F0,1

F0,2

F1,1

F1,2

t = 0 1 2 3 n……

S1S0 S2 S3

Forward exchange rate premium f = (F-S0)/S0

Exchange rate movement over the period specified

s = (S1-S0)/S0

Spot rate: S0 = S current time

Forward rate: F0,1 = F contract signing time, time to maturity

5-16

You operate a sesame oil plant, buying sesame seeds and produce sesame oil out of it. You have an MBA degree and you learned in your finance course that you should obtain price forecast from commodity futures market. You just found on the futures market that the futures price of sesame seeds and sesame oil are about the same next year. How should you modify your production plan for the next year? Should you contract out / swap your next year’s capacity to another oil plant? Should you mothball your business for one year? Should you upgrade to other value-adding and profitable operations? What other key information (e.g., futures price for ten years into the future) may also help you make a prudent and informed decision?

5-17

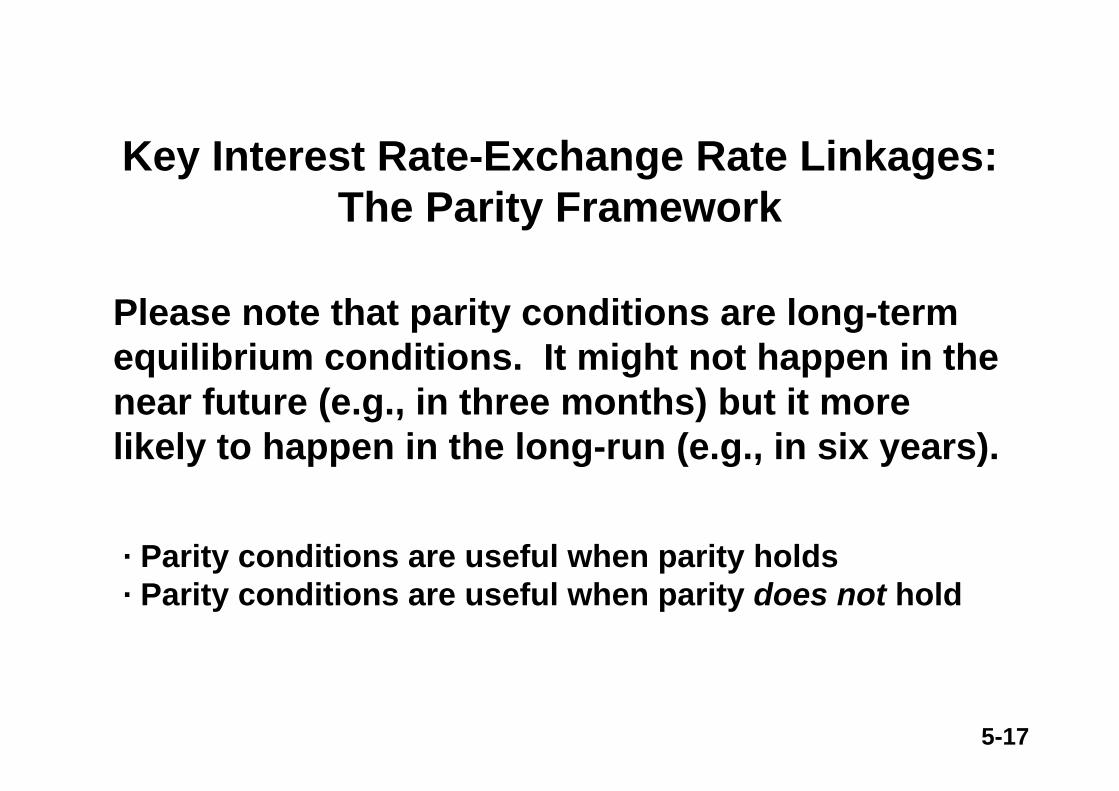

· Parity conditions are useful when parity holds· Parity conditions are useful when parity does not hold

Key Interest Rate-Exchange Rate Linkages: The Parity Framework

Please note that parity conditions are long-term equilibrium conditions. It might not happen in the near future (e.g., in three months) but it more likely to happen in the long-run (e.g., in six years).

5-18

Four International Parity ConditionsPurchasing Power Paritylinking spot exchange rates and inflationAbsolute PPP: The price of a market basket of U.S. goods equals the price of a market basket of foreign goods when multiplied by the exchange rate.Relative PPP: The percentage change in the exchange rate equals the percentage change in U.S. goods prices less the percentage change in foreign goods prices.

Uncovered Interest Paritylinking interest rates and inflationFisher Effect: For a single economy, the nominal interest rate equals the real interest rate plus the expected rate of inflation.International Fisher Effect: For two economies, the U.S. interest rate minus the foreign interest rate equals the expected difference of inflation rates between two countries.

5-19

Interest Rate Paritylinking forward exchange rates and expected spot exchange rate The forward exchange rate premium equals (approximately) the U.S. interest rate minus the foreign interest rate.

Forward Rate Unbiased Propertylinking forward exchange rates and expected spot exchange ratesForeign Exchange Expectations: Today’s forward premium (for delivery in n days) equals the expected percentage change in the spot rate (over the next n days).

Four International Parity Conditions

5-20

International Parity Relations Linear Approximationwhere Spot Rate S are in indirect quote (FC/DC or FC/$)

Solnik 2.1

Interest Rate Parity

Forward Rate Unbiased Property

Uncovered Interest Parityor Fisher International Effect

Purchasing Power Parity (relative version) PPP

IRPFIE

FRU

5-21

We will now look at the parity conditions that link the spot and forward exchange markets with the international money and bond markets.

We first develop the parity conditions in a theoretical setting, starting with the perfect capital market (PCM) assumptions. Then we analyze the impact of relaxing the PCM assumptions (e.g., no taxes, complete certainty).

Parity Conditions

5-22

We will begin with interest rate parity. The interest rate parity condition offers us an easy opportunity to relax the PCM assumptions and show the effect of introducing taxes into our financial calculations.

Secondly, we present the Fisher parities, named after Irving Fisher who derived these relationships in the late 19th century.

Thirdly, we introduce the forward rate unbiased condition as the final parity relationship.

Parity Conditions

5-23

While PPP involves arbitrage in goods, the other three parity conditions involve arbitrage opportunities in financial markets where transaction costs are usually lower.

However, financial markets are often subjected to controls or restrictions and taxes that limit the ability of market participants to complete an arbitrage transaction.

The Usefulness of theParity Conditions

5-24

When controls or taxes that are present create a deviation from a parity condition, the magnitude of the deviation reveals how profitable it will be for an agent to “overcome” that control or tax.

The Usefulness of theParity Conditions

5-25

As with PPP, financial market transactions often involve risk. Some of the risks, such as price risk, credit risk, country risk, etc., may apply to the parity financial conditions if the agent is unable to hedge them. [credit risk: the risk that a borrower will be unable to make timely payment of interest or principal]

If a parity condition is violated because of uncertainty, agents must compare their risk aversion to that in the market. Agents who are less (more) risk averse than the overall market will find that the violation of parity presents a profit (hedging) opportunity.

The Usefulness of theParity Conditions

5-26

In which country would you invest in the short-term and in the long-term?

Interest rates One year Inflation rates,%Belgian franc 611/16 - 69/16 1.4Deutschmark 55/16 - 53/16 2.2Sterling 75/8 - 71/2 2.7Swiss franc 4 - 37/8 1.9US dollar 611/16 - 69/16 3.2Italian lira 113/4 - 115/8 5.5Japanese yen 21/16 - 2 -0.2

Rx

Old Data, Old Data, Old Data

5-27

World Interest Rates Table

7.25%Mar 04 2008Aug 05 2008The Reserve Bank of Australia

2.75%Sep 13 2007Sep 18 2008Swiss National Bank

2%Apr 30 2008Aug 05 2008Federal Reserve

4.25%Jul 03 2008Aug 07 2008European Central Bank

0.5%Feb 21 2007Jul 15 2008Bank of Japan

5%Apr 10 2008Jul 10 2008Bank of England

3%Apr 22 2008Jul 15 2008Bank of Canada

Current Interest RateLast ChangeNext MeetingCentral Bank

Major Central Banks Overview

http://www.fxstreet.com/fundamental/interest-rates-table/

5-28

5-29

http://finance.mapsofworld.com/financial-market/world-inflation.htmlhttp://inflationdata.com/inflation/Inflation_Rate/InternationalSites.asp

5-30

Exchange Rates Table

5-31

July 2007

5-32

• If an investor can receive a higher interest rate by lending money in a foreign currency than by lending money in the domestic currency, it makes sense for the investor to lend in the foreign currency.

• This is done by exchanging the domestic currency for foreign currency, lending the foreign currency, and then converting the money plus interest back into the domestic currency at the maturity of the loan.

• However, as the exchange rate may vary over the tenor of the loan, the investor is exposed to the risk that the foreign currency may depreciate against the domestic currency by more than the difference between the two interest rates. In this case, the investor will make a loss by lending in foreign currency.

Rx

5-33

Korean Won: Depreciation versus Interest Rate Differential(in % per year)

Solnik 2.3

5-34

From 1991 to 1996, the won had a much higher interest rate than the dollar (an annual differential around 10%), but the exchange rate with the dollar remained stable. In 1997, the Asian crisis hit many currencies in the region and the won was devalued by some 50%.

Averaging over the 1991-97 period, we find that the interest rate differential roughly matches the currency depreciation. So any investor applying the strategy to invest in this high-interest-rate currency would have made a profit for several years and lost all of it in 1997.

Solnik 2.3

5-35

Interest Rate Parity

The forward exchange rate premium equals (approximately) the U.S. interest rate minus the foreign

interest rate.

( ) £iiSSF −=− $

Driven by arbitrage between the spot and forward exchange rates, and money market interest rates.

Interest Rate Parity: The Relationship between Interest Rates, Spot Rates, and Forward Rates

5-36

IRP draws on the principle that, in equilibrium, two investments that are exposed to the same risks must have the same return.

IRP is maintained by arbitrage.

The Relationship among Interest Rates, Spot Rates, and Forward Rates

Interest Rate Parity

5-37

Convert the $1 into (1/St) £ at the current spot rate St ($/£), and then invest it in a £ security with i£. At the same time, cover exposure to £by selling the entire proceeds at the current one-period forward rate, Ft, 1.

Suppose an investor invests $1 in a US$ security with interest rate i$ for one period.At the end of one period, wealth = $1 x (1 + i$ ).Alternative:

= $1 x x (1 + i£) x Ft, 1endingwealth

1.0St

Interest Rate Parityin a Perfect Capital Market

5-38

Equating the two:

$1 x x (1 + i£) x Ft, 1 = $1 x (1 + i$ )1.0St

Rearranging terms:Ft, 1

St

1 + i$1 + i£

=

Subtracting 1 from each side:

Ft, 1 - St

St

i$ - i£1 + i£

=

Interest Rate Parityin a Perfect Capital Market

(5.1)

5-39

Subject: The Intuition of Covered and Uncovered Interest Parity (1) In equation 5.1 on covered interest parity, if sterling interest rates are low, how can we get US$ based investors to hold sterling assets? The answer is that we offer them a more favorable forward rate (higher F in terms of $/GBP) to offset the low GBP interest rate. So the market is working by pricing F to offset a known low GBP interest rate.

Tips -- Intuition Check from Professor Levich

£

£$1,

1 iii

SSF

t

tt

+−

=−

(5.1)

5-40

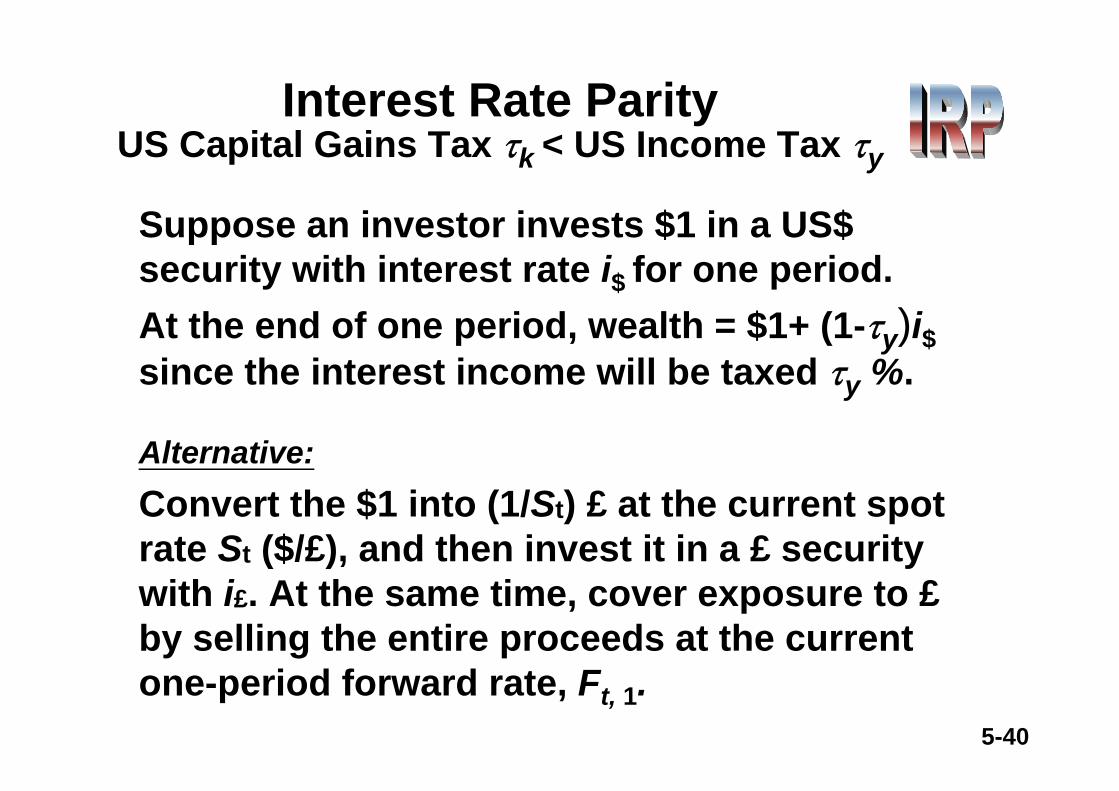

Convert the $1 into (1/St) £ at the current spot rate St ($/£), and then invest it in a £ security with i£. At the same time, cover exposure to £by selling the entire proceeds at the current one-period forward rate, Ft, 1.

Suppose an investor invests $1 in a US$ security with interest rate i$ for one period.At the end of one period, wealth = $1+ (1-τy)i$ since the interest income will be taxed τy %.

Alternative:

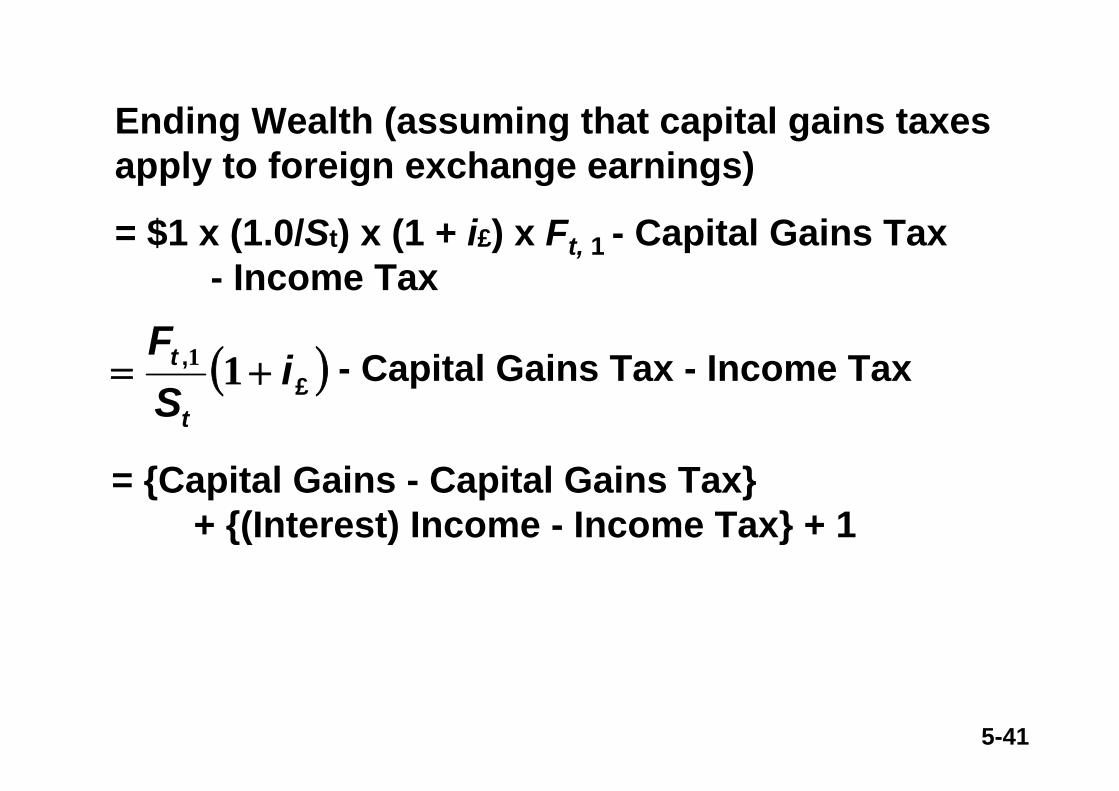

Interest Rate ParityUS Capital Gains Tax τk < US Income Tax τy

5-41

Ending Wealth (assuming that capital gains taxes apply to foreign exchange earnings)

= $1 x (1.0/St) x (1 + i£) x Ft, 1 - Capital Gains Tax - Income Tax

( )£, i

SF

t

t += 11 - Capital Gains Tax - Income Tax

= {Capital Gains - Capital Gains Tax}+ {(Interest) Income - Income Tax} + 1

5-42

( ) ( ) { }

( ) ( ) ( ){ } 1111

111

1

11

+−+⎭⎬⎫

⎩⎨⎧

+−

−=

+−+⎭⎬⎫

⎩⎨⎧

+−

−+−

=

££,

£££,

£,

iiS

SF

iiiS

SFi

SSF

yt

ttk

yt

ttk

t

tt

ττ

ττ

( )£, iS

SF

t

tt +−

11

is the hedged foreign exchange earnings.

Note that the term

We have used the income tax rate on £isince all interest, whatever the currency or country of source, is subject to that rate.

yτ

5-43

Equating the two:

Rearranging terms:

So:

Interest Rate ParityUS Capital Gains Tax τk < US Income Tax τy

( ) ( ) ( ){ } ( ) $££, $ iiiS

SFyy

t

ttk τττ −+=−++

⎭⎬⎫

⎩⎨⎧

+−

− 111111 1

( ) ( )ykt

tt

iii

SSF

ττ −+−

=−−

11

11

£

£$,

k

y

t

tt

iii

SSF

ττ

−

−×

+−

=−

11

11

£

£$,

5-44

While some investors may enjoy a lower tax rate on foreign exchange than on interest earnings, banks and other major players do not; such investors, for whom international investment is a normal business, pay the same tax on interest and foreign exchange earnings.

However, investors who do pay lower taxes on foreign exchange earnings than on interest income may find valuable tax arbitrage opportunities.

5-45

For example, suppose interest rates and exchange rates are such that interest parity holds precisely on a before-tax basis:

With i$ = 12%, i£ = 8%, US Capital Gains Tax Rate τk = 10%, US Income Tax Rate τy = 25%U.S. dollar investments yield {$1 + (1 - τy)i$ - 1}/1 = 9% after tax, while £ investments yield after tax:

=> The pound investment will be preferred on anafter-tax basis.

£

£$1,

1 iii

SSF

t

tt

+−

=−

( ) ( ) ( ){ }%.

££,

691

11111 1

=−−++

⎭⎬⎫

⎩⎨⎧

+−

− iiS

SFy

t

ttk ττ

5-46

More generally, if covered interest parity holds on a before-tax basis, investors with favorable capital gains treatment will prefer investments denominated in currencies trading at a forward premium.

It is a natural extension of our argument to show that in the same tax situation, borrowers will prefer to denominate borrowing in currencies at a forward discount.

5-47

Here are some prices in the international money markets:

Spot rate = $0.75/A$Forward rate (one year) = $0.77/A$Interest rate (A$) = 7% per yearInterest rate ($) = 9% per year

Assuming that no transaction costs or taxes exist, do covered arbitrage profits exist in the above situation? Describe the flows.

Beginning with 1 A$,Buy $ in the spot market

Buy $ in the forward marketfinal $ = S x (1 + r$)final $ = (1 + rA$ ) x F

5-48

0.75 X (1+0.09) < (1+0.07) X 0.77Therefore, investing in A$ is more profitable.Hence (1) borrow in US$, (2) purchase A$ on the spot market, (3) sell A$ forward and make a profit.

The annual dollar return on dollars invested in Australia is (1.07 x .77)/.75 – 1 = 9.85%. The return exceeds the 9% return on dollars invested in the United States by 0.85% per annum. Hence arbitrage profits can be earned by borrowing dollars or selling dollar assets, buying A$ in the spot market, investing the A$ at 7%, and simultaneously selling the A$ interest and principal forward for one year for dollars.

5-49

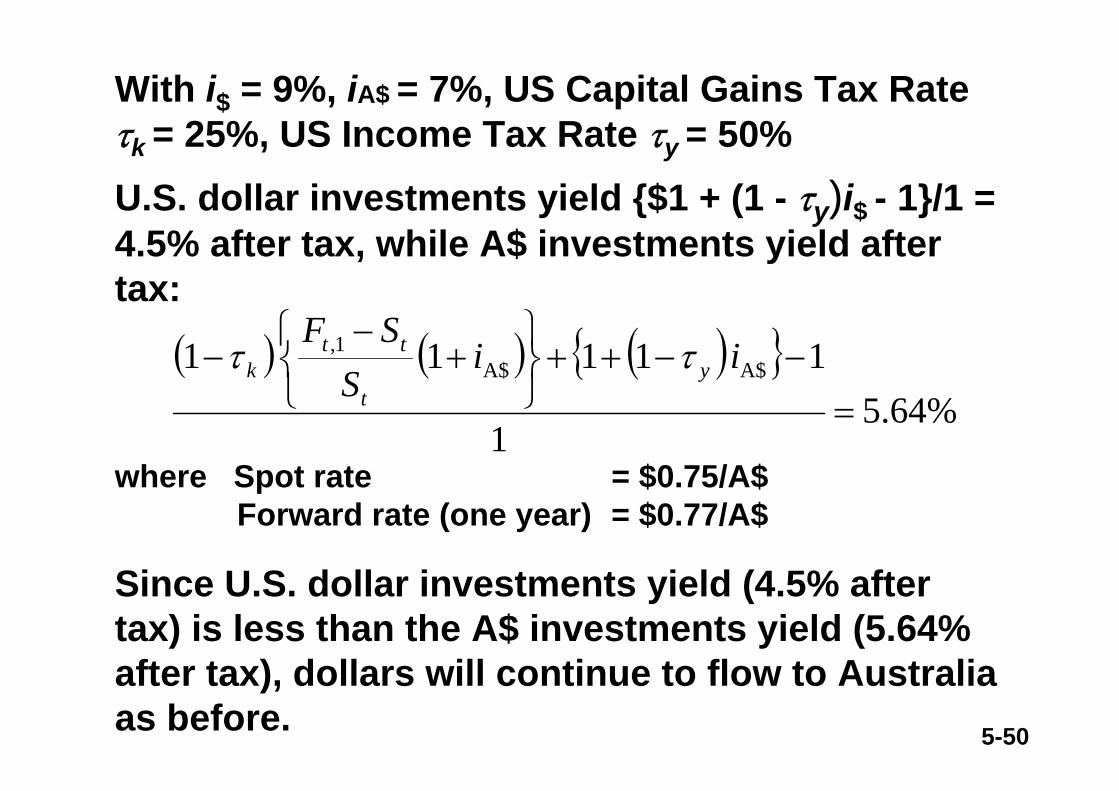

Suppose no transaction costs exist. Let the capital gains tax on currency profits equal 25%, and the ordinary income tax on interest income equal 50%. In this situation, do covered arbitrage profits exist? How large are they? Describe the transactions required to exploit these profits.

[Answer to Question 3c, 10 points] [Previous exam question]In this case, the after-tax interest differential in favor of the U.S. is (.90 x .50 - .07 x .50) / (1 + .07 x .50) = (.045 - .035) / 1.035 = 0.97%, while the after-tax forward premium on the A$ is (.77 - .75) x .75/.75 = 2%. Since the after-tax forward premium exceeds the after-tax interest differential, dollars will continue to flow to Australia as before.

5-50

U.S. dollar investments yield {$1 + (1 - τy)i$ - 1}/1 = 4.5% after tax, while A$ investments yield after tax:

( ) ( ) ( ){ }%64.5

1

1 111 1 A$A$1,

=−−++

⎭⎬⎫

⎩⎨⎧

+−

− iiS

SFy

t

ttk ττ

With i$ = 9%, iA$ = 7%, US Capital Gains Tax Rate τk = 25%, US Income Tax Rate τy = 50%

where Spot rate = $0.75/A$Forward rate (one year) = $0.77/A$

Since U.S. dollar investments yield (4.5% after tax) is less than the A$ investments yield (5.64% after tax), dollars will continue to flow to Australia as before.

5-51

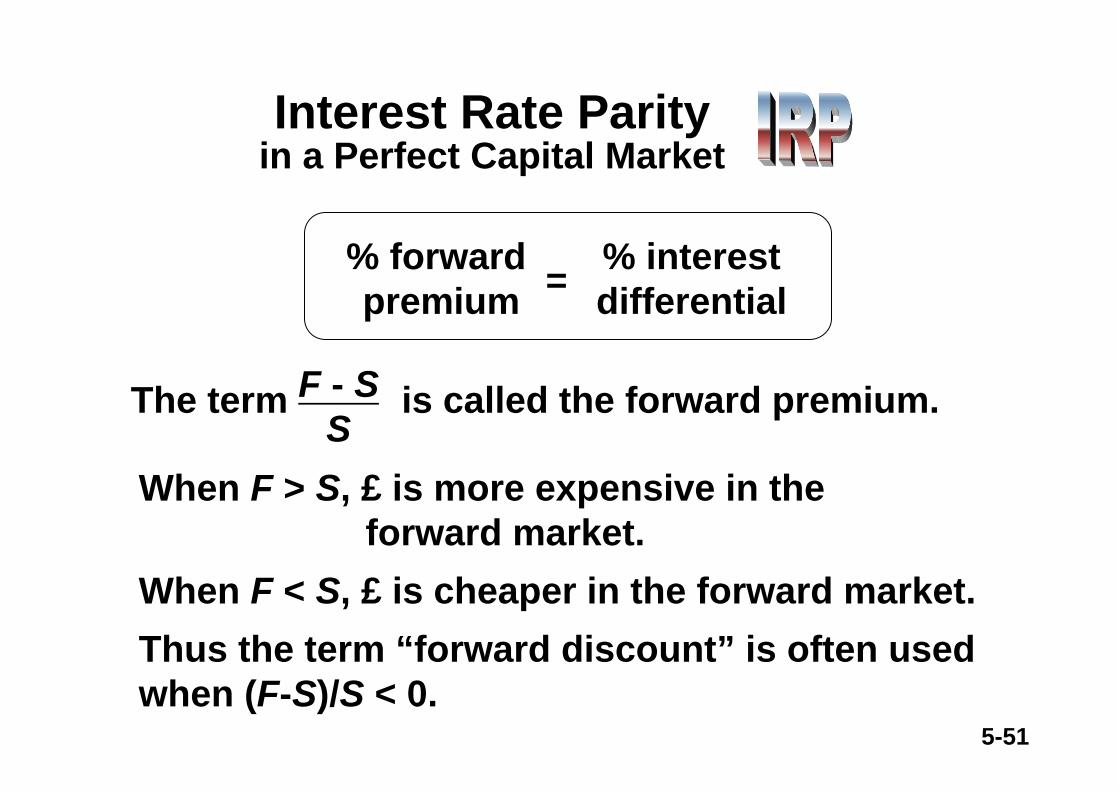

=% forward premium

% interest differential

The term is called the forward premium.F - SS

When F > S, £ is more expensive in the forward market.

When F < S, £ is cheaper in the forward market.Thus the term “forward discount” is often used when (F-S)/S < 0.

Interest Rate Parityin a Perfect Capital Market

5-52

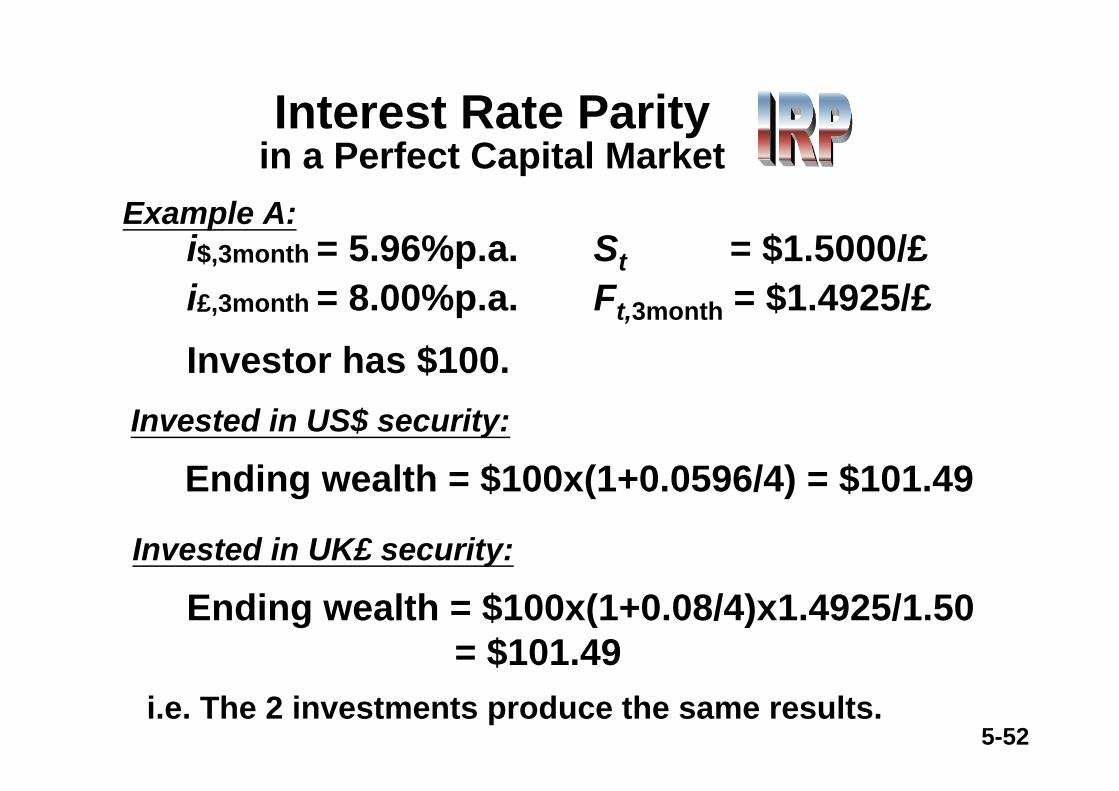

Example A:i$,3month = 5.96%p.a.i£,3month = 8.00%p.a.

St = $1.5000/£Ft,3month = $1.4925/£

Investor has $100.Invested in US$ security:

Ending wealth = $100x(1+0.0596/4) = $101.49

Invested in UK£ security:

Ending wealth = $100x(1+0.08/4)x1.4925/1.50= $101.49

i.e. The 2 investments produce the same results.

Interest Rate Parityin a Perfect Capital Market

5-53

Example A continued:

Forward discount on UK:

Interest differential between the US$ and the UK£:

(F-S)/S = (1.4925-1.5)/1.5 = -0.50%

(i$ - i£ )/(1 + i£ ) = (0.0596/4-0.08/4)/(1+0.08/4)= -0.005

With £ at a forward discount, UK interest rates are higher than US interest rates to preserve IRP.

Interest Rate Parityin a Perfect Capital Market

5-54

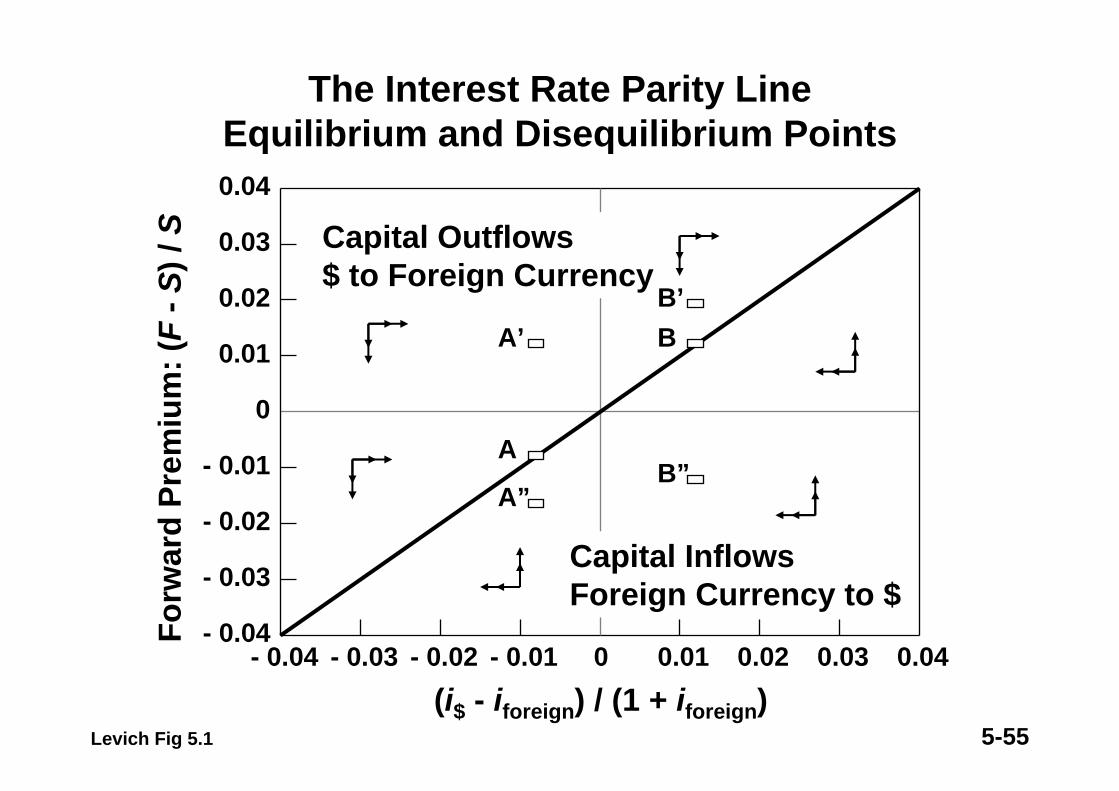

Suppose in example A, F’ = $1.52/£ > F = $1.4925/£.So, investors favor UK£ over US$ investments. This results in point A’ in Figure 5.1.

The location of A’ => the incentive for risk-free covered arbitrage flows out of US$ and into UK£.

For an investor who held US$ securities initially:1. Sell US$ security at 5.96% => i$ rises2. Buy £ spot at $1.50 => St rises3. Buy UK£ security at 8.00% => i£ falls4. Sell £ forward at $1.52 => Ft falls5. (i$ - i£ ) rises and (Ft-St) falls => move rightward and downward to parity line!

Example of Covered Interest Arbitrage to Exploit Deviations from Interest Rate Parity

5-55

The Interest Rate Parity LineEquilibrium and Disequilibrium Points

Levich Fig 5.1

0.04

0.03

0.02

0.01

0

- 0.01

- 0.02

- 0.03

- 0.040.040.030.020.010- 0.01- 0.02- 0.03- 0.04

Forw

ard

Prem

ium

: (F

-S) /

S

(i$ - iforeign) / (1 + iforeign)

Capital Outflows$ to Foreign Currency

Capital InflowsForeign Currency to $

A

A’

A”

BB’

B”

5-56

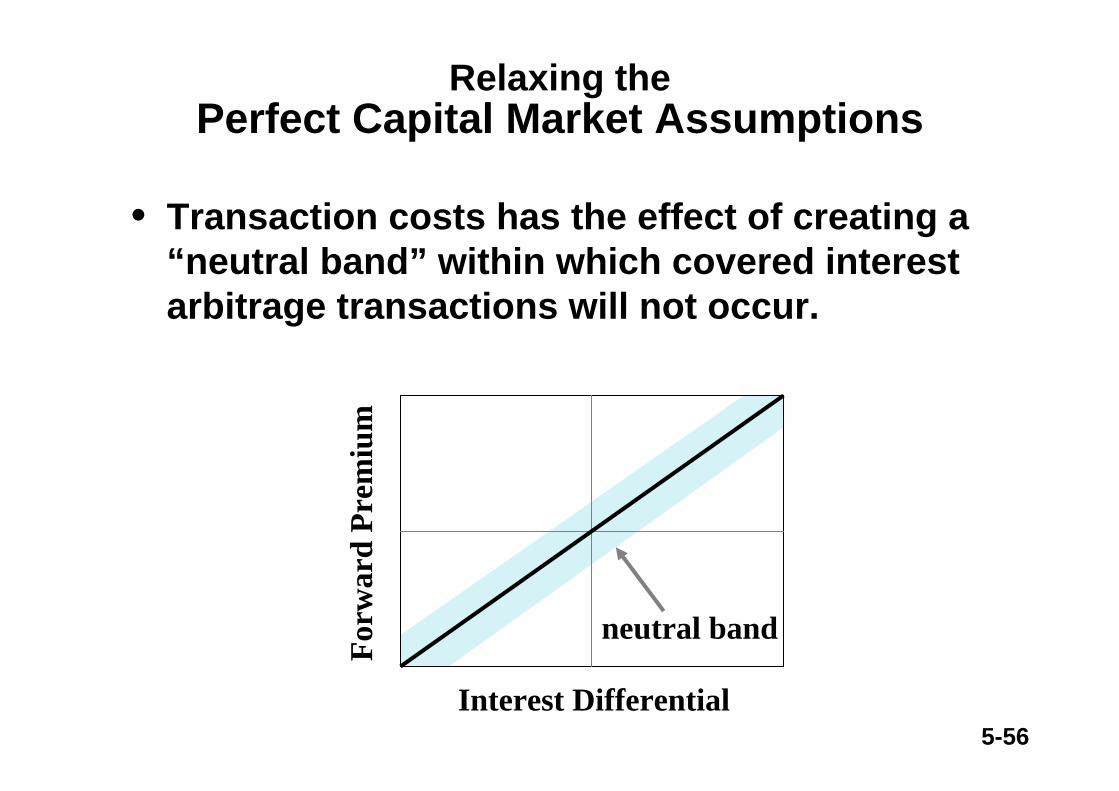

Relaxing thePerfect Capital Market Assumptions

• Transaction costs has the effect of creating a “neutral band” within which covered interest arbitrage transactions will not occur.

Forw

ard

Prem

ium

Interest Differential

neutral band

5-57

Relaxing thePerfect Capital Market Assumptions

• Differential capital gains and ordinary income tax rates can tilt the 45° slope of the IRP line. ¤ However, the actual impact depends on the

exact tax rates, the number of people who are subject to those rates, and transactions costs which may dominate the role of taxes.

• There are also uncertainty risks.¤ Placing orders takes time and market prices

may change.¤ The foreign investment may present country

risks.

5-58

The 4 transactions describe covered interest arbitrage. We also could call it “round-trip”arbitrage, during which a person can begin with $1, conduct 4 transactions, and wind up with more than $1.

Example of Covered Interest Arbitrage to Exploit Deviations from Interest Rate Parity

5-59

time dimensioncu

rren

cy d

imen

sion

Jan 1 Jul 1US$

£

B A

C D

spot forward

interest rate

interest rate

Example of Covered Interest Arbitrage to Exploit Deviations from Interest Rate Parity

5-60

The profit from making these transactions isapproximately the % deviation from IRP, defined as

Example of Covered Interest Arbitrage to Exploit Deviations from Interest Rate Parity

Notice in Figure 5.1 that the marginal impact of each of the 4 transactions has the effect of pushing the configuration of the rates back towards IRP.

Ft, 1 - St

St

i$ - i£1 + i£

d t = -

5-61

Empirical Evidence on Interest Rate Parity (Levich 2E, pp. 152-55)

(5.1)tt

t

tt

iii

SSF

εβα ++−

+=−

t?

t?$,1,

1

Testing whether α=0 and β=1 in the following simple linear regression would not be appropriate even though the IRP line is a 45o line passing through the origin -- given the role played by transaction costs, it is clear that observations could cluster inside the neutral band in any number of ways.

5-62

Empirical Evidence on Interest Rate ParityEmpirical Evidence on the Neutral Band

(Levich 2E, page 153)

• The Eurocurrency markets made it possible to examine two securities that differed only in terms of their currency of denomination.

• The general result is that IRP holds in the short-term Eurocurrency market after accounting for transaction costs.

• For longer-term securities, a study found significant deviations from parity that represent profit opportunities even after adjusting for transaction costs.

5-63

• More recently, Helen Popper (1993) analyzed long-term covered interest parity using five-year and seven-year securities and the interest differential implied by currency swaps of matching maturities.

• For her sample of major countries in the mid-1980s, Popper found that deviations from long-term covered interest parity are only slightly higher (about 10 bp or 0.1%) than deviations from short-term covered interest parity.

5-64

• In a related study, however, Donna Fletcher and Larry Taylor (1994) examined 5-, 7-, and 10-year securities for deviations from long-term covered interest parity.

• They reported that in every test market, there are significant deviations from parity that represent profit opportunities even after adjusting for transaction costs.

• Deviation from parity open a window of opportunity for firms and may partly explain the rapid growth in long-term currency swaps.

5-65

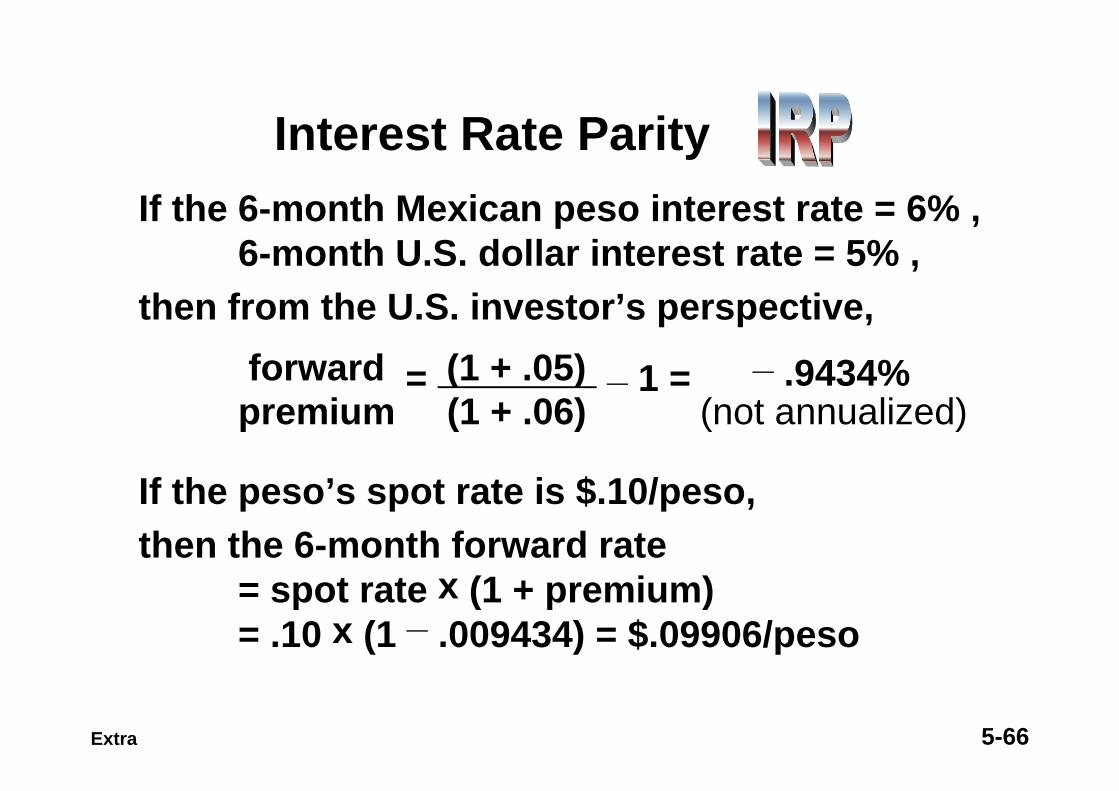

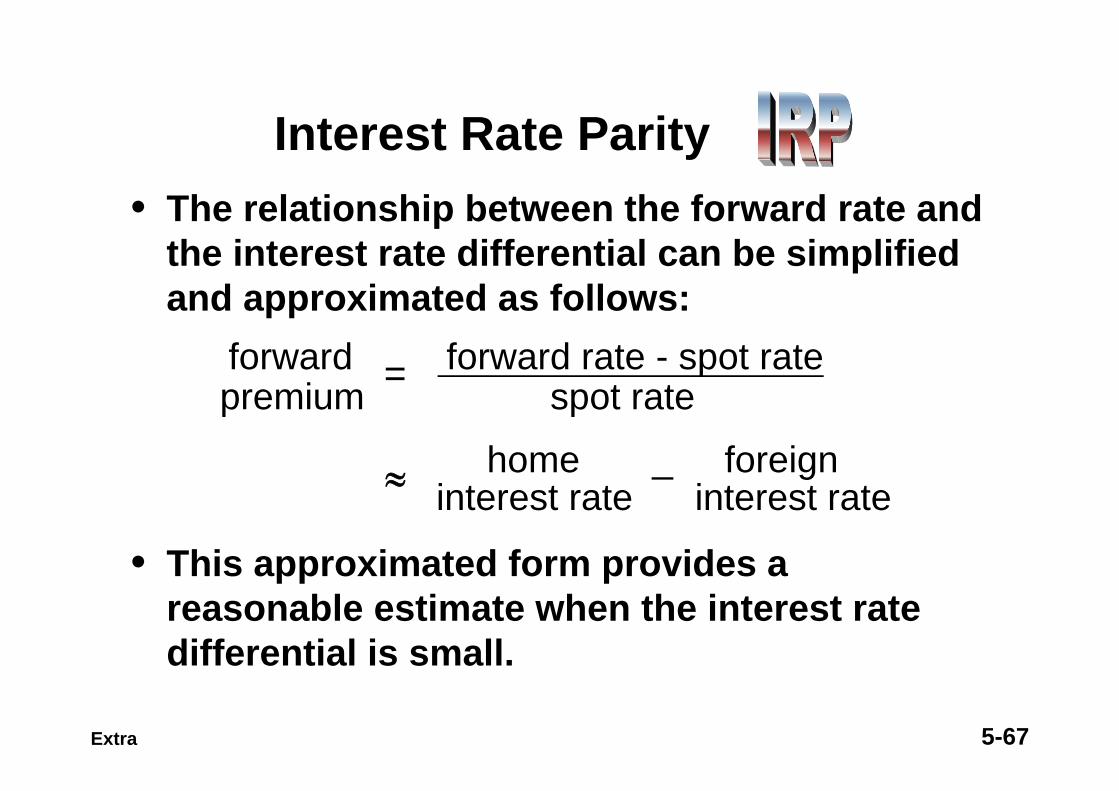

• When market forces cause interest rates and exchange rates to be such that covered interest arbitrage is no longer feasible, the equilibrium state achieved is referred to as interest rate parity (IRP).

• When IRP exists, the rate of return achieved from covered interest arbitrage should equal the rate available in the home country. By simplifying and rearranging terms:

forward = (1 + home interest rate) _ 1premium (1 + foreign interest rate)

Extra

Interest Rate Parity

5-66

If the 6-month Mexican peso interest rate = 6% ,6-month U.S. dollar interest rate = 5% ,

then from the U.S. investor’s perspective,forward = (1 + .05) _ 1 = _ .9434%premium (1 + .06) (not annualized)

If the peso’s spot rate is $.10/peso,then the 6-month forward rate

= spot rate x (1 + premium)= .10 x (1 _ .009434) = $.09906/peso

Extra

Interest Rate Parity

5-67

• The relationship between the forward rate and the interest rate differential can be simplified and approximated as follows:

forward = forward rate - spot rate premium spot rate

≈ home _ foreigninterest rate interest rate

• This approximated form provides a reasonable estimate when the interest rate differential is small.

Extra

Interest Rate Parity

5-68

Graphic Analysis of Interest Rate Parity

-4

Interest Rate Differential (%)home interest rate - foreign interest rate

ForwardPremium (%)

ForwardDiscount (%)

-2

2

4

1 3-1-3

IRP line

Extra

5-69

Graphic Analysis of Interest Rate ParityHome Interest Rate - Foreign Interest Rate (%)

ForwardPremium (%)

ForwardDiscount (%)

-2

-4

2

4

1 3-3-1

IRP lineZone of potential covered interest

arbitrage by foreign investors

Zone of potential covered interest

arbitrage by local investors

Zone where covered interest

arbitrage is not feasible

Extra

5-70

• IRP generally holds. Where it does not hold, covered interest arbitrage may still not be worthwhile due to transaction costs, currency restrictions, differential tax laws, political risk, etc.

• When IRP exists, it does not mean that both local and foreign investors will earn the same returns. What it means is that investors cannot use covered interest arbitrage to achieve higher returns than those achievable in their respective home countries.

Extra

Interest Rate Parity

5-71

Correlation Between Spot and Forward Rates

Because of interest rate parity, a forward rate will normally move in tandem with the spot rate. This correlation depends on interest rate movements.

t0 t2t1

Inte

rest

Rat

es iAiU.S.

time

t0 t2t1

Spot

and

Forw

ard

Rat

esSpotA

ForwardA.

timeExtra

5-72

The Fisher Parities

Fisher Effect (Fisher Closed)

For a single economy, the nominal interest rate equals the real interest rate plus the expected rate of inflation.

( )US$$~PEri Δ+=

Driven by desire to insulate the real interest against expected inflation,

and arbitrage between real and nominal assets.

5-73

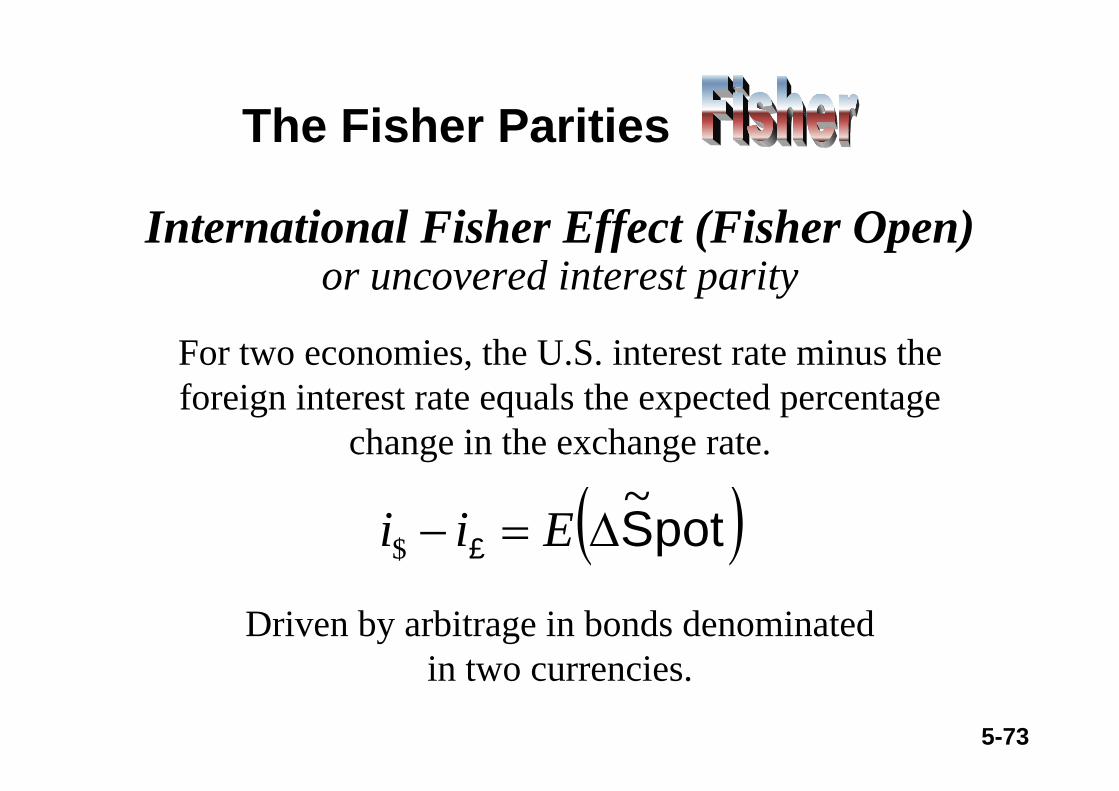

The Fisher Parities

International Fisher Effect (Fisher Open)or uncovered interest parity

For two economies, the U.S. interest rate minus the foreign interest rate equals the expected percentage

change in the exchange rate.

( )potS£~

$ Δ=− Eii

Driven by arbitrage in bonds denominatedin two currencies.

5-74

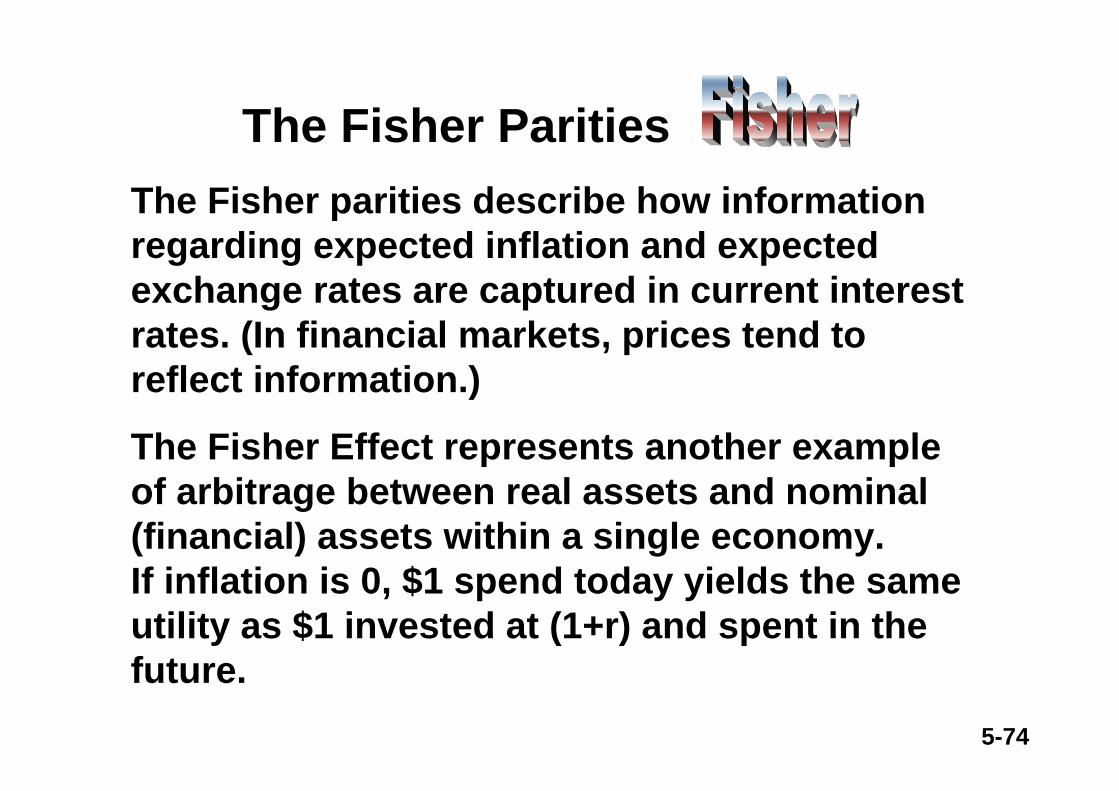

The Fisher parities describe how information regarding expected inflation and expected exchange rates are captured in current interest rates. (In financial markets, prices tend to reflect information.)

The Fisher Effect represents another example of arbitrage between real assets and nominal (financial) assets within a single economy. If inflation is 0, $1 spend today yields the same utility as $1 invested at (1+r) and spent in the future.

The Fisher Parities

5-75

Assume PCM, expected inflation E(p), investor hold $1 in cash.

=> can buy commodity with $1 and sell thecommodity for $1[1 + E(p)] at the end of oneperiod.

To be indifferent between this commodity purchase and an interest-bearing security, the latter needs an end-of-period value of

$1(1+r)[1+E(p)].

~

~

~

The Fisher Effect

5-76

Since the return on security is normally quoted in nominal terms to yield $1(1+i),

(1+i) = (1+r)[1+ E(p)]

or i = r + E(p) + r E(p)

Since in most developed countries, inflation and real interest rates are low, the Fisher Effect is approximately:

~

~ ~

i = r + E(p)~

The Fisher Effect

5-77

Fisher Closed Parity Example:If I grow a tree in an inflation era (invest in a real asset), I will benefit from two sources of revenue growth: the cubic inches increases of 2.9% of the volume of the tree, plus the price increase of 2.5% of the timber. Therefore, if a finance company hopes to attract my investment (in a nominal or financial asset), the company will have to pay me (1+2.9%) x (1+2.5%) – 1, or roughly 2.9%+2.5%, to make me indifferent of two investments (one in real asset (e.g., tree) and one in nominal asset (e.g., bonds or certificate of deposits)). Therefore, financial interest rate (nominal rate of return) = real interest rate (muscle growth rate) + expected inflation (fat growth rate).

5-78

To execute the arbitrage implied by the Fisher Effect, individuals will move out of financial assets into commodities when inflation is high. When inflation is receding, individuals will prefer financial assets to lock in higher returns. When the Fisher Effect holds, nominal / financial assets fully reflect expected inflation and preserve the real rate of return.

% nominal % real % expectedinterest rate interest rate inflation= +

The Fisher Effect

5-79

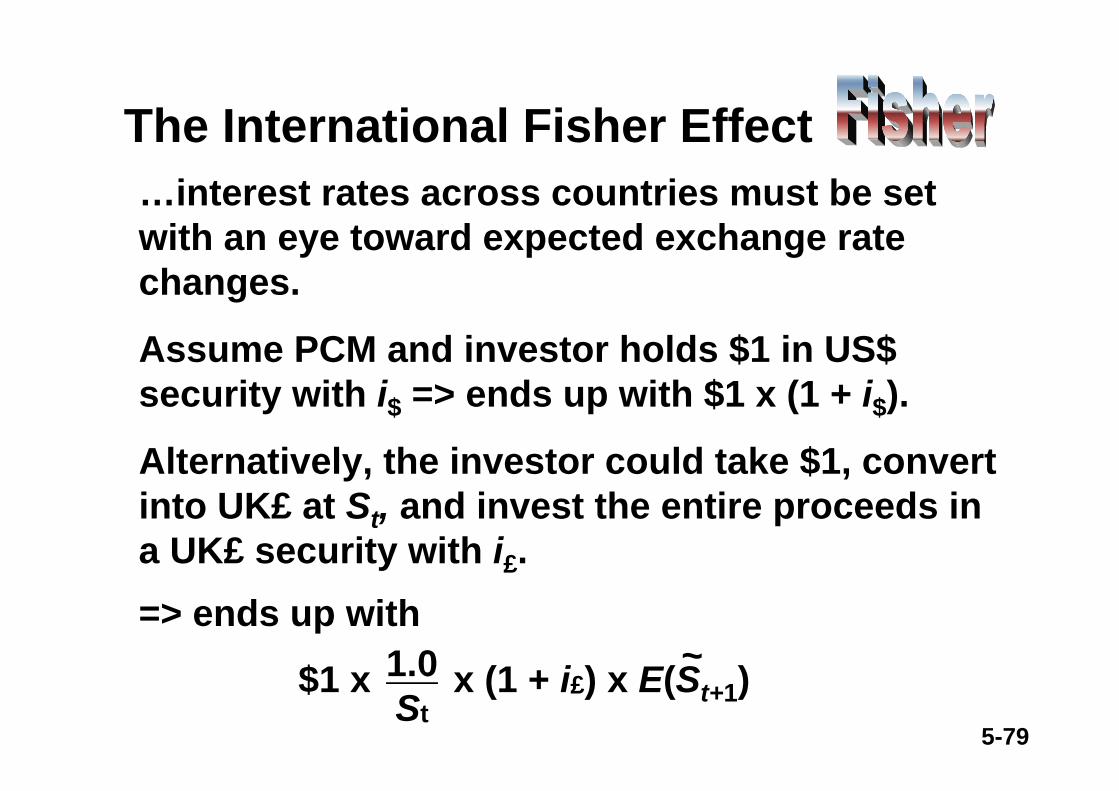

…interest rates across countries must be set with an eye toward expected exchange ratechanges.

Assume PCM and investor holds $1 in US$ security with i$ => ends up with $1 x (1 + i$).

Alternatively, the investor could take $1, convert into UK£ at St, and invest the entire proceeds in a UK£ security with i£. => ends up with

$1 x x (1 + i£) x E(St+1)1.0St

~

The International Fisher Effect

5-80

Under PCM assumptions, both investments share the same maturity, risk, and final currency denomination, and hence the same ending wealth:

$1 x x (1 + i£) x E(St+1) = $1 x (1 + i$ )1.0St

~

Rearranging terms:

E(St+1)St

1 + i$1 + i£

=~

The International Fisher Effect

5-81

Subtracting 1 from each side:

E(St+1) - St

St

i$ - i£1 + i£

=

Note that the RHS of (5.5) is approximatelyi$ - i£ when i£ is small.

~

% expected exchange % interestrate change differential=

(5.5)

The International Fisher Effect

5-82

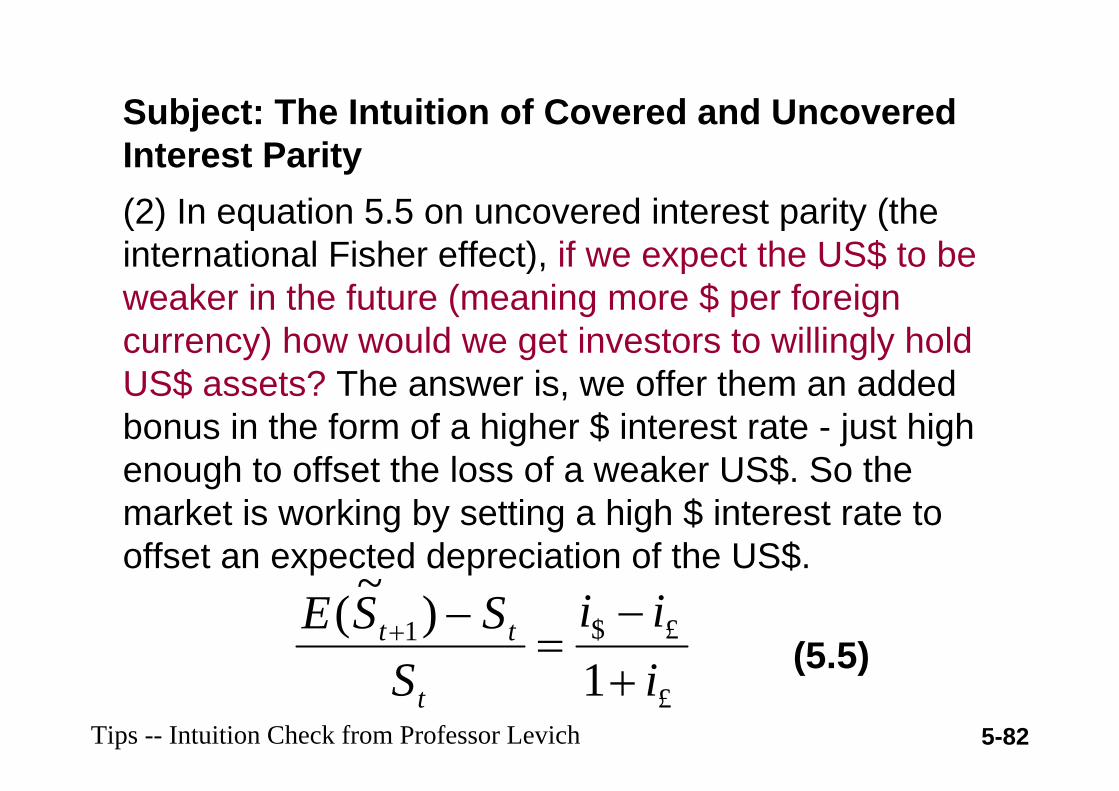

Subject: The Intuition of Covered and Uncovered Interest Parity (2) In equation 5.5 on uncovered interest parity (the international Fisher effect), if we expect the US$ to be weaker in the future (meaning more $ per foreign currency) how would we get investors to willingly hold US$ assets? The answer is, we offer them an added bonus in the form of a higher $ interest rate - just high enough to offset the loss of a weaker US$. So the market is working by setting a high $ interest rate to offset an expected depreciation of the US$.

Tips -- Intuition Check from Professor Levich£

£$1

1)~(

iii

SSSE

t

tt

+−

=−+

(5.5)

5-83

Relaxing thePerfect Capital Market Assumptions

• Transaction costs result in a neutral band around the parity line, while differential taxes can possibly tilt the parity line.

• Since the ending value of the foreign investment depends on an uncertain future spot rate, an exchange-risk premium may be required.

5-84

Empirical Evidence on the International Fisher Effect (Levich 2E, pp. 160-63)

1t?

t?$,1

1 ++ +

+−

=−

tt

t

tt

iii

SSS ε

Under the assumption of rational expectations, St+1 = E(St+1 ) + εt+1, we can rewrite the International Fisher Effect as:~

Testing whether α=0 and β=1 in the following simple linear regression would reveal whether the interest differential provides a good forecast of the future spot rate change.

1t?

t?$,1

1 ++ +

+−

+=−

tt

t

tt

iii

SSS εβα

5-85

Figure 5.5 presents a graph of the interest differential on Euro-$ and Euro-DM deposits at quarter t and the spot exchange rate change ($/DM) one quarter in the future. The graph shows that exchange rate changes from a volatile series that switches between sizable positive and negative values. In comparison, the interest differential is a relatively smooth and calm series that takes on positive values over most of the sample period. Figure5.5 suggests little relationship between the current interest differential and the future realized exchange rate change. In aformal regression test of equation (5.12), we find coefficients with standard errors in parentheses:α = 0.007 (0.008), β = -0.070 (0.827), R2 = 0.001, N = 108, D-W (Durbin-Watson statistic) = 1.75These results clearly reject the α = 0 and β = 1 hypothesis.

Note: Please refer to Chapter 12 Serial Correlation and Heteroskedasticity in Time Series Regressions of Wooldridge’s Introductory Econometrics for details about D-W.

5-86

Empirical Evidence onthe International Fisher Effect

• Empirical tests indicate that the International Fisher Effect condition performs poorly in individual periods.

• However, over extended periods of time, it appears that currencies with high interest rates tend to depreciate, and vice versa, as predicted.

5-87

• According to the Fisher effect, nominal risk-free interest rates contain a real rate of return and an anticipated inflation. If the same real return is required across countries, differentials in interest rates may be due to differentials in expected inflation.

• According to PPP, exchange rate movements are caused by inflation rate differentials. The international Fisher effect (IFE) theory suggests that currencies with higher interest rates will depreciate because the higher rates reflect higher expected inflation.

Extra

The International Fisher Effect

5-88

• According to the IFE, the expected effective return on a foreign investment should equal the effective return on a domestic investment:

(1 + if ) (1 + ef ) _ 1 = ihwhere ih = interest rate in the home country

if = interest rate in the foreign countryef = % change in the foreign currency’s value

• Solving for ef : ef = (1 + ih ) _ 1(1 + if )

• The simplified form, ef ≈ ih_ if , provides

reasonable estimates when the interest rate differential is small.Extra

The International Fisher Effect

5-89

JapanU.S.Canada

JapanU.S.Canada

JapanU.S.Canada

InvestorsResiding

in

Attemptto

Invest in ihReturn

in HomeCurrency

RealReturnEarnedif ef Ih

Japan

U.S.

Canada

555

888

131313

58

13

58

13

58

13

0- 3- 8

30

- 5

850

555

888

131313

333

666

111111

222

222

222

% % % % % %

Extra

The International Fisher Effect

Old data, Old data, Old dataOld Data, Old Data, Old Data

5-90

BritainNew Z.Brazil

BritainNew Z.Brazil

BritainNew Z.Brazil

InvestorsResiding

in

Attemptto

Invest in ihReturn

in HomeCurrency

RealReturnEarnedif ef Ih

BritainIh=2.5%

New ZealandIh=3.4%

BrazilIh=4.8%

555

888

131313

58

13

58

13

58

13

0- 3- 8

30

- 5

850

555

888

131313

333

666

111111

222

222

222

% % % % % %

Extra

The International Fisher Effect

5-91

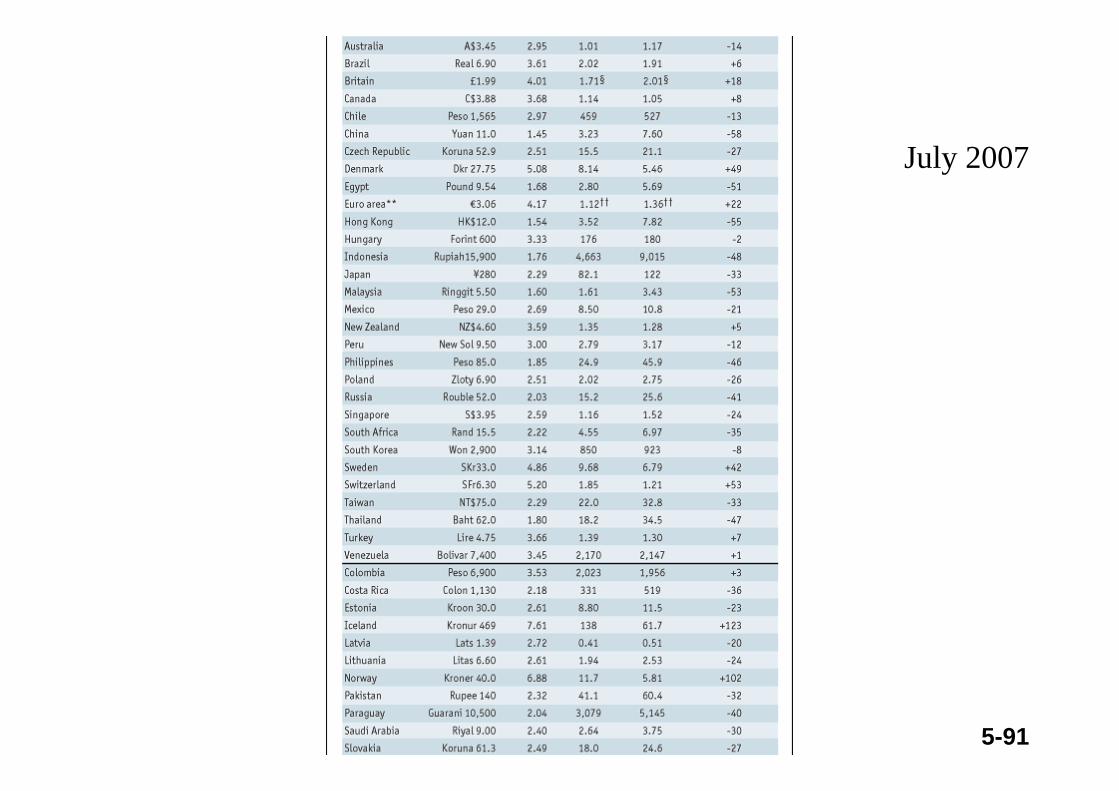

July 2007

5-92

Graphic Analysis of the International Fisher EffectInterest Rate Differential (%)

home interest rate - foreign interest rate

-2

-4

2

4

1 3-1-3

IFE line

Higher returns from investing in foreign deposits

Lower returns from investing in foreign deposits

%Δ in the foreign

currency’s spot rate

Extra

5-93

• While the IFE theory may hold during some time frames, there is evidence that it does not consistently hold.

• A statistical test can be developed by applying regression analysis to the historical exchange rates and nominal interest rate differentials:

ef = a0 + a1 { (1+ih)/(1+if) - 1 } + μThe appropriate t-tests are then applied to a0and a1, whose hypothesized values are 0 and 1 respectively.

Extra

The International Fisher Effect

5-94

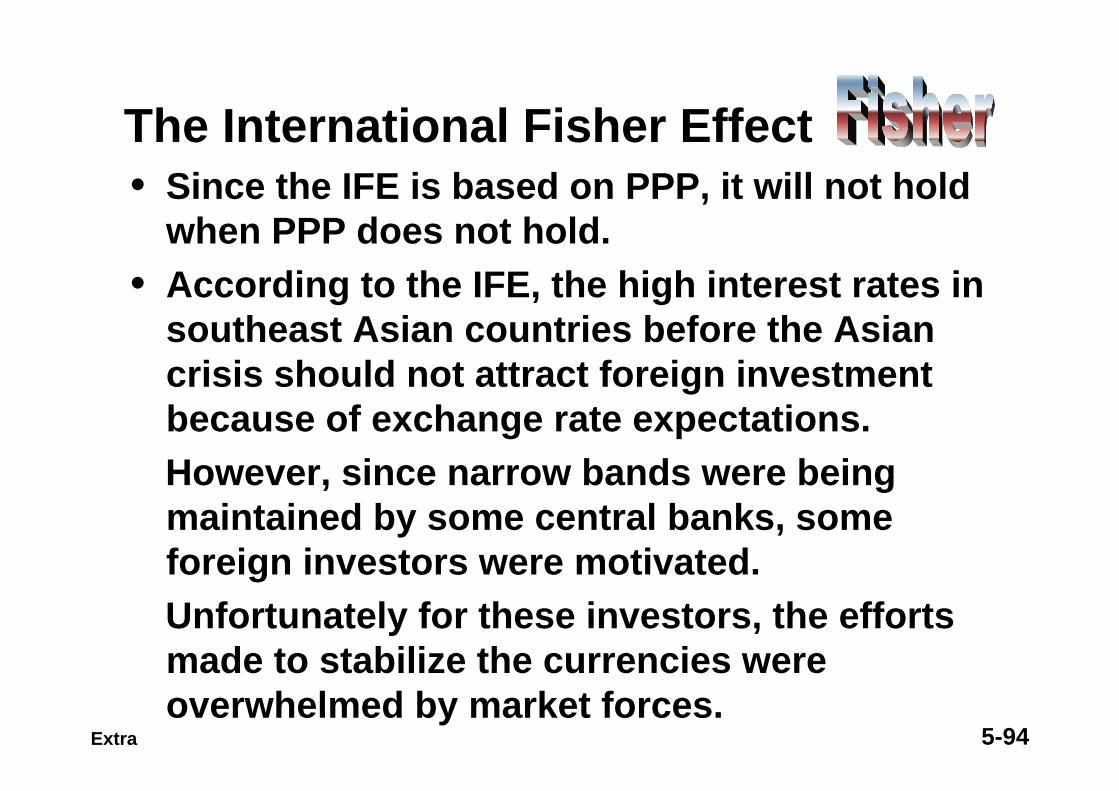

• Since the IFE is based on PPP, it will not hold when PPP does not hold.

• According to the IFE, the high interest rates in southeast Asian countries before the Asian crisis should not attract foreign investment because of exchange rate expectations.However, since narrow bands were being maintained by some central banks, some foreign investors were motivated.Unfortunately for these investors, the efforts made to stabilize the currencies were overwhelmed by market forces.

Extra

The International Fisher Effect

5-95

Comparison of IRP, PPP, and IFE Theories

Extra

Forward RateDiscount or Premium

Exchange RateExpectations

Inflation RateDifferential

Interest RateDifferential

Interest Rate Parity(IRP)

FisherEffect

InternationalFisher Effect (IFE)

PurchasingPower Parity (PPP)

5-96

The Forward Rate Unbiased Condition

Forward Rate UnbiasedToday’s forward premium (for delivery in n days)

equals the expected percentage change in the spot rate (over the next n days).

( ) ( )( ) ttntttt SSSESSF −=− +~

Driving force: Market players monitor the difference between today’s forward rate (for delivery in n days)

and their expectation of the future spot rate (n days from today).

5-97

Given the PCM assumptions,

the interest rate parity condition,

£

£$1,

1 iii

SSF

t

tt

+−

=−

and the International Fisher Effect,

£

£$1

1)~(

iii

SSSE

t

tt

+−

=−+

(5.1)

(5.5)

The Forward Rate Unbiased Condition

5-98

t

tt

t

tt

SSF

SSSE −

=−+ 1,1)

~(

% Expected exchangerate change =

% Forwardpremium

If the average deviation between today’s forward rate and the actual future spot exchange rate

is near zero, then the forward rate is an unbiased predictor of the spot rate.

(5.16)

The Forward Rate Unbiased Condition

1,tF

tS

5-99

The Forward Rate Unbiased Condition

• A forward rate bias may imply market inefficiency, or it may reflect a risk premium.

• Empirical data reveals that the forward rate and future spot rate track along a very similar path, though F tracks “below” the future Swhen the spot rate is rising, and vice versa.

• On the other hand, actual exchange rate changes form a volatile series, while the forward premium is relatively smooth and calm.

5-100

The forward rate unbiased condition is monitored by speculators, who in the PCM setting, trade in the forward contract only at prices equal to the expected future spot rate.

When we relax the PCM assumptions, it is clear that the forward rate unbiased condition depends on 2 further assumptions...

The Forward Rate Unbiased Condition

5-101

(1) Market Efficiency:Speculators are able to form unbiased expectations of future spot rates; and

11 )~( ++ = tt SSE

(2) Forward Rate Pricing: )~( 11, += tt SEFSpeculators choose to trade forward contracts at prices equal to their expectations.

Forward rates will be biased if either assumption fail.

The Forward Rate Unbiased Condition

5-102

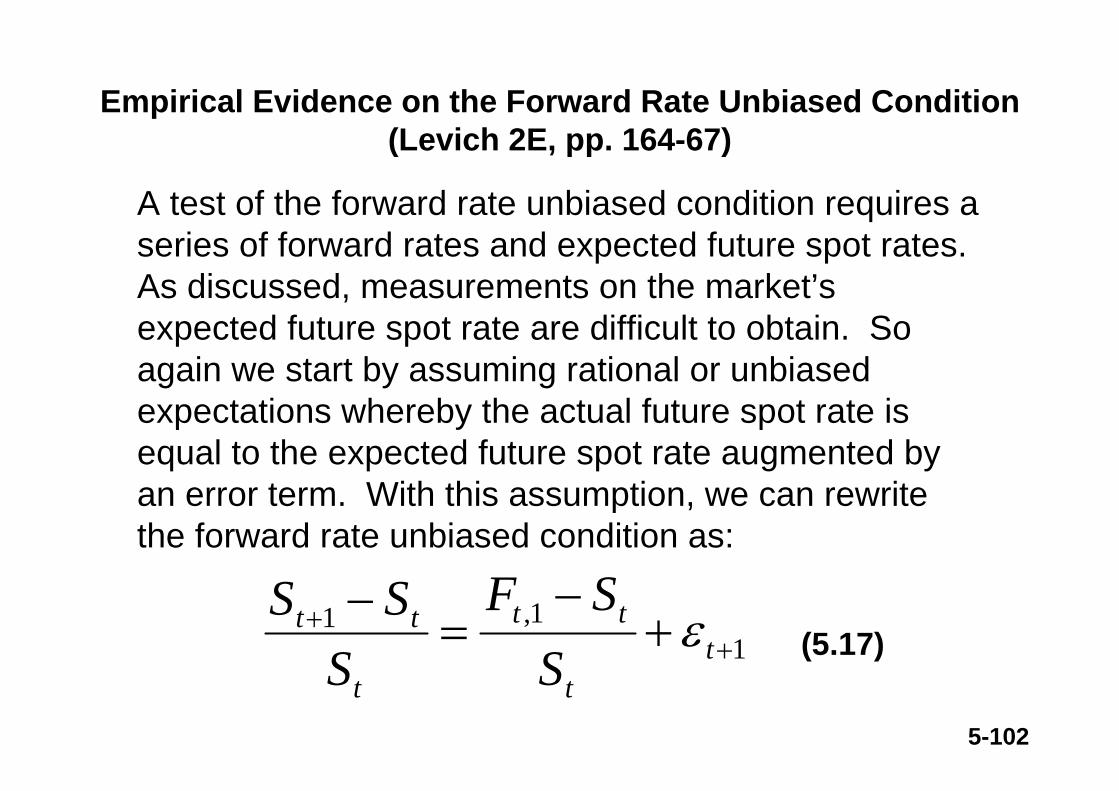

Empirical Evidence on the Forward Rate Unbiased Condition (Levich 2E, pp. 164-67)

11,1

++ +

−=

−t

t

tt

t

tt

SSF

SSS ε (5.17)

A test of the forward rate unbiased condition requires a series of forward rates and expected future spot rates. As discussed, measurements on the market’s expected future spot rate are difficult to obtain. So again we start by assuming rational or unbiased expectations whereby the actual future spot rate is equal to the expected future spot rate augmented by an error term. With this assumption, we can rewrite the forward rate unbiased condition as:

5-103

Empirical Evidence on the Forward Rate Unbiased Condition (Levich 2E, pp. 164-66)

Tests Using the Level of Spot and Forward Exchange Rates

11,1 ++ ++= ttt FS εβα (5.18)

Figure 5.7A One-Month Forward and Future Spot Rates, and Figure 5.7B Three-Month Forward and Future Spot Rates reveal that the forward rate and the future spot rate track along a very similar path. Therefore, we expect that a regression of the level of the future spot rate against the level of the present forward rate, such as:

would produce coefficients α and β near 0 and 1, respectively, and a high R2 for the regression.

5-104

Inspection of Figure 5.7 reveals another interesting pattern. It appears as if the forward rate tracks “below”the future spot rate when the spot rate is rising, and “above” the future spot rate when the spot rate is falling. As a result, the forward rate misses all of the “turning points” in the spot rate series.

Tests Using the Level of Spot and Forward Exchange Rates

5-105

Forecast BiasUsing the Forward Rate as a Forecast for the British Pound

$1.00

$1.20

$1.40

$1.60

$1.80

$2.00

$2.20

$2.40

$2.60

1975 1980 1985 1990 1995 2000

Forward Rate

RealizedSpot Rate

Madura

5-106

Graphic Evaluation of Forecast PerformanceUsing the Forward Rate as a Forecast for the British Pound

Rea

lized

Spo

t Rat

e

$1.00

$1.50

$2.00

$2.50

$1.00 $1.50 $2.00 $2.50

Forecast (Forward Rate)

PerfectForecast

Line

Madura

5-107

Empirical Evidence on the Forward Rate Unbiased Condition (Levich 2E, pp. 166-67)

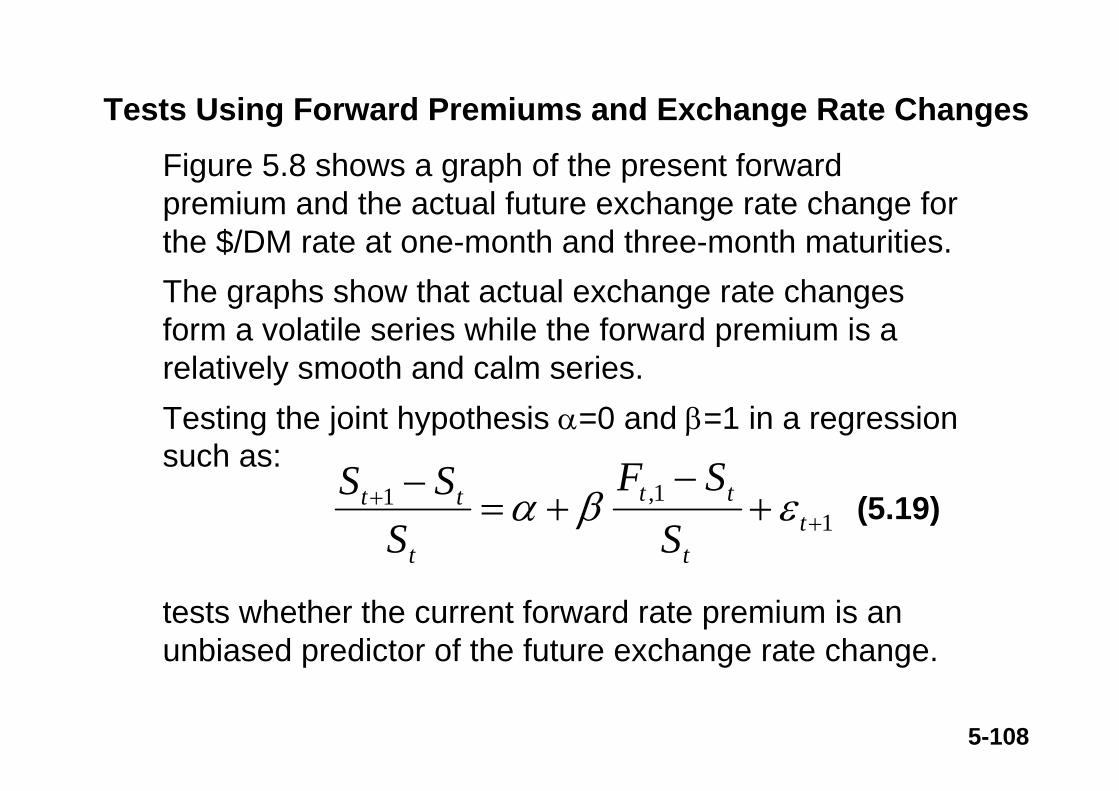

Tests Using Forward Premiums and Exchange Rate Changes

Our perception of the forward rate as a predictor changes when we examine percentage changes in exchange rates rather than the levels. In percentage rate form, the forward rate unbiased condition of equation (5.15) requires us to compare the present forward premium with the expected future exchange rate change.

t?

t?$,11 1 i

iiS

SSd t

t

ttt +

−−

−= +

+ (5.15)

5-108

11,1

++ +

−+=

−t

t

tt

t

tt

SSF

SSS εβα (5.19)

Figure 5.8 shows a graph of the present forward premium and the actual future exchange rate change for the $/DM rate at one-month and three-month maturities. The graphs show that actual exchange rate changes form a volatile series while the forward premium is a relatively smooth and calm series.Testing the joint hypothesis α=0 and β=1 in a regression such as:

tests whether the current forward rate premium is an unbiased predictor of the future exchange rate change.

Tests Using Forward Premiums and Exchange Rate Changes

5-109

In table 5.1, we see that the α=0 and β=1 hypothesis is rejected for the DM and every other currency in the sample; the data indicate that β is negative and significant for several currencies.

Thus, the analysis of exchange rate changes suggests that the forward premiums are poor predictor of the future exchange rate change, and often times a biased predictor.

As we will see in Chapters 7 and 8, this empirical finding may offer good news through the hope it offers forecasters to beat the forward rate at forecasting exchange rate changes.

Tests Using Forward Premiums and Exchange Rate Changes

5-110

When interest rate parity (IRP) holds, the covered cost of funds is identical across all currencies; there are neither bargains nor bad deals on a covered basis.

We have referred to the parity conditions as “benchmark” or “break-even” points.

When the International Fisher Effect holds, the expected cost of borrowed funds is identical across currencies and the expected return on invested funds is identical across currencies on an uncovered basis.

Policy Matters - Private Enterprises

5-111

When the forward rate unbiased condition holds, the expected cash flows associated with hedging or not hedging a currency exposure are identical.

If all of the parity conditions are valid at each and every moment in time, then all financial choices would be fairly priced compared with the alternatives.

Policy Matters - Private Enterprises

5-112

But empirical evidence shows that while many of the parity conditions may hold “in most cases” or “on average,” at times the parity conditions are violated.

As a result, managers may have an opportunity to make profit maximizing decisions by exploiting deviations from the parity conditions.

Policy Matters - Private Enterprises

5-113

A manager who holds US$ can obtain € in the future by following two alternative paths. By taking the low cost path, the manager is engaging in “one-way arbitrage”.

Example of one-way arbitrage in foreign exchange and security markets:

Application : Interest Rate Parity & One-Way Arbitrage

5-114

D

AB

One-Way ArbitrageA manager who holds US$ now wants € in the future.

time dimensioncu

rren

cy d

imen

sion

Jan 1 Jul 1US$

€

Buy €forward

at F

Path 1

Invest US$ at i$

Path 2

C

Buy €spot at S

Invest € at i€

By taking the lower cost path, the manager is engaging in one-way

arbitrage.

5-115

Suppose that an investor holds US$ cash and wishes to make a € payment in 6 months. The investor has 2 alternatives to choose between:

Path 1: Invest US$ for 6 months, buy € forward on Jan 1 for July 1 deliveryCost = )1( 6$,1,1 monthsJulyJan iF +

)1( 6,1 monthseuroJan iS +

Path 2: Buy € spot on Jan 1, invest € for 6monthsCost =

One-Way Arbitrage

5-116

In the absence of transaction costs, the two alternatives will be identical. But when transaction costs are present, an investor may favor one alternative over another, even though no round-trip arbitrage profits are possible.

One-way arbitrage then is simply picking the lowest-priced (highest-priced) alternative when buying (selling) for a transaction between 2 corners of the box in Figure 5.9.

One-Way Arbitrage

5-117

Spot A$: $0.6793-$0.68031-month Forward A$: $0.6800-$0.68101-month Euro A$: 4.00-4.125% p.a.1-month Euro $: 6.0625-6.1875% p.a.Note: Euro$ are US$ on deposit in non-US banks.

Borrowing $ for 30 days, buying A$ spot, investing A$ for 30 days, and selling A$ forward will result in a cost of

Example of One-Way Arbitrage Profits

0023.10.6800 )120.04000(10.6803 )120.061875(1

=×+×+

counter-clockwise:

5-118

In both cases, borrowing one unit of currency costs more than the unit of currency

=> no round-trip arbitrage profits

Borrowing A$, selling A$ spot, investing $, and buying A$ forward will result in a cost of

0009.10.6793 )120.060625(1

0.6810 )120.04125(1=

×+×+

clockwise:

Example of One-Way Arbitrage Profits

5-119

Assuming that your firm has a payment of A$ 1 million due in 30 days and you want to lock in the price today, how should you transact?

Path 1 (clockwise): Investing US$ for 30 days, buying A$ spot, investing A$ for 30 days, and selling A$ at the forward rate. The cost of path 1 is:

$$6780.0$$6776.012/060625.01

$$6810.0 AAA<=

+

Example of One-Way Arbitrage Profits

5-120

Path 2 (counter-clockwise): Selling US$ for A$ at the spot rate and then investing A$ for 30 days.

The cost of path 2 is:

$$6780.012/04000.01$$6803.0 AA

=+

Path 1 is preferred since the cost is lower.

Example of One-Way Arbitrage Profits

5-121

Policy Matters - Private Enterprises

• Managers may make profit maximizing decisions by exploiting deviations from the parity conditions, or they may want to avoid or hedge the risks of such deviations.

• Application 1: IRP & One-Way Arbitrage¤ One-way arbitrage is picking the better-priced

alternative for a transaction in the presence of transaction costs.

5-122

Policy Matters - Private Enterprises

• Application 2: Credit Risk & Forward Contracts¤ The costs of using an outright forward versus a

synthetic forward for hedging may differ for firms because credit risk is usually priced in bank loans but not in forward contracts.

• Application 3: IRP & the Country Risk Premium¤ The deviations of government securities from

IRP provides a measure of the political risk differences among countries.

5-123

Policy Matters - Private Enterprises• Appln 4: Are Deviations from IFE Predictable?

¤ Even if the deviations are zero on average, a nonrandom pattern can present a profit opportunity.

• Appln 5: Are Deviations from IFE Excessive?¤ Under a system of pegged exchange rates, any

interest rate differential represents a deviation.¤ A speculator may (1) invest in the high interest rate

currency when the peg is expected to hold, or (2) borrow the high interest rate currency when the peg is expected to change by more than the interest differential.

5-124

Strategy 1: Investing in the High-Interest-Rate CurrencyA current application of this principle was the surge of U.S. investment into Mexican government securities.

During 1992, peso-denominated, short-term securities had yields of 7-16 percentage points greater than US$ government securities. With the foreign exchange value of peso depreciating gradually, at about 5 percent per year, the realized International Fisher Effect deviations were substantial, enough to draw large sums to U.S. investment into Mexico. For example, in late 1992 the Fidelity Short-Term World Income Fund, a $631 million fund managed by Fidelity Investments of Boston, held almost 17 percent of its assets in peso-denominated securities.

This strategy failed in late 1994, when the peso suffered a maxi-devaluation and took back more than the excess interest paid on peso securities.

5-125

A slightly more complex application of the same principle involved currencies within the European Exchange Rate Mechanism (ERM). As we described in Chapter 2, currencies within the ERM were pegged to one another, but within bands of 2.25 percent for most currencies and 6.0 percent for the British pound and Italian lira. Suppose, as was the case in early 1991, that three-month Euro-£ interest rates were 14 percent while comparable Euro-DM interest rate was 9 percent. By borrowing Euro-DM and investing in Euro-£, the speculator would earn 5 percent per annum. As long as the DM/£ rate did not depreciate by more than 5 percent per annum, the strategy would add incremental profits to a short-term investment portfolio. The strategy worked reasonably well through the early 1990s, as the ERM held up and interest rate differentials persisted.

5-126

Strategy 2: Borrowing the High-Interest-Rate CurrencyIn September 1992, the European Exchange Rate Mechanism (ERM) came under stress and fears mounted that several currencies would have to devalue or exit the ERM.Anticipating this, speculators had an opportunity to invoke an alternative strategy -- borrowing the high-interest-rate currency while owning the low-interest-rate currency and betting against the preservation of the ERM. In early September 1992, three-month Euro-£ rates were only 0.50 percent higher than Euro-DM rates. Euro-lira rates, however, were some 6.00 percent higher than Euro-DM rates. Still, paying this interest differential for a few weekswas a modest cost relative to the exchange rate changes that occurred -- a 14 percent depreciation of the pound (from 2.78 DM/£ to 2.40 DM/£) and a 13 percent depreciation of the lira (762 lira/DM to 863 lira/DM).

5-127

Policy Matters - Private Enterprises

• Appln 6: IFE and Diversification Possibilities¤ Can passive investors gain by holding a

diversified portfolio of international currencies on an unhedged basis?

• Appln 7: IFE, Long-Term Bonds & ExchangeRate Predictions

¤ When IFE is extended to long-term bonds (n-period investments) :

( ) ( )( ) tn

nn

nt Sii

SE ×+

+=+

nSF,

$,

11~

5-128

Policy Matters - Public Policymakers

• The Fisher parities can provide information regarding how closely national financial markets are linked to one another, and what price, if any, a nation is paying for perceived political and economic risks.

• The interest rate differential may be a useful indicator of policy credibility for countries following pegged exchange rate policies.

5-129

Assignment for Chapter 5Exercises 1, 4, 5, 6.

5-130

Chapter 5, Exercise 1. Interest Rate ParityHint:Suppose the US and UK three-month interest rates are respectively 6% and 8% per annum and that the spot rate is $1.55/£.a. Calculate the forward premium (or discount)

on the £ expressed on a per annum basis.First: Find the 3-month forward premium as follows:3-month forward premium = )

41()

44( ££$ iii

+−

Second: Multiply the above number by 4 to obtain the per annum forward premium

5-131

Chapter 5, Exercise 4. Fisher International Effect

The following data were taken from the July 28, 1994 issue of the Currency and Bond Market Trends by Merrill Lynch:

JAPAN BRITAIN USSpot exchange rates: 98.75¥/$ $1.53/£ ----5-year bonds: 3.73% 7.94% 6.88%10-year bonds: 4.34 8.24 7.2420-year bonds: 4.70 8.26 7.40

Compute the break-even exchange rate for investors weighing the choice between $-bonds and Yen-bonds, and between $-bonds and Pound sterling bonds for each of the three maturities. Note: Assume that interest is paid twice yearly.

5-132

Chapter 5, Exercise 4. Fisher InternationalHint:A “break-even” exchange rate is the exchange rate that would make a risk-neutral investor indifferent between the US$ bond and the foreign currency denominated bond. In other words, it is the exchange rate that makes the Fisher International effect (i.e. uncovered interest rate parity) hold:

ntnt i

iSSE 2* )

2121()(

++

=+

where n = number of years to maturityof the bond

5-133

Chapter 5, Exercise 6. Fisher International Effect Hint:Suppose that the interest rates in question #5 reflect a 0.5% per annum currency risk premium for bond investors to willingly hold US$-denominated bonds.a. Compute the expected exchange rate on the

maturity date of the bond in this case.n

tnt iiSSE 2* )

2121()(

++

=+

In the above formula,0.085 0.5%) - (9% i ==

5-134

£

$1

11)~(

ii

SSE

t

t

++

=+ for one period

2

£

$2 )11

()~(ii

SSE

t

t

++

=+ for two periods

n

t

nt

ii

SSE )

11

()~(

£

$

++

=+ for n periods

See Page 158 Application 7 in Levich 1Eor Page 175 Application 7 in Levich 2E.

Chapter 5, Exercise 6. Fisher International Effect Hint:

5-135

CERTIFICATES OF DEPOSIT AS OF JULY 5, 2006Minimum Annual Interest

Term Balance* Percentage Yield* Rate5 years $5,000+ 4.65% 4.55%4 years $5,000+ 4.55% 4.45%3 years $5,000+ 4.50% 4.40%2 years $5,000+ 4.50% 4.40%18 months $5,000+ 4.35% 4.26%12 months $5,000+ 4.30% 4.21%7 months Special $5,000+ 5.25% 5.12%6 months $5,000+ 4.10% 4.02%3 months $5,000+ 4.00% 3.92%30 day Special* $25,000+ 4.00% 3.92%9 month liquid CD $10,000+ 5.00% 4.88%

*The 30-day CD has a minimum opening balance of $25,000.*The 9 Month Liquid CD Maintains a minimum balance of $10,000.

How do you like the 7 months special with a minimum required balance of only $5,000? Are you surprised?

5-136

CERTIFICATES OF DEPOSIT AS OF JULY 2, 2007Minimum Annual Interest

Term Balance* Percentage Yield* Rate5 years $5,000+ 4.50% 4.40%4 years $5,000+ 4.50% 4.40%3 years $5,000+ 4.50% 4.40%2 years $5,000+ 4.50% 4.40%18 months $5,000+ 4.35% 4.26%12 months $5,000+ 4.30% 4.21%6 months $5,000+ 5.00% 4.88%5 months Liquid $10,000+ 5.20% 5.07%3 months $5,000+ 4.00% 3.92%30 day Special* $25,000+ 4.00% 3.92%

*The 30-day CD has a minimum opening balance of $25,000.*The 5 Month Liquid CD Maintains a minimum balance of $10,000.

How do you like the 5 months Liquid CD with a minimum required balance of only $10,000? Are you surprised?

5-137

CERTIFICATES OF DEPOSIT AS OF JULY 7, 2008Minimum Annual Interest

Term Balance* Percentage Yield* Rate5 years $5,000+ 5.00% 4.88%4 years $5,000+ 4.25% 4.16%3 years $5,000+ 3.50% 3.44%2 years $5,000+ 3.40% 3.34%18 months $5,000+ 3.75% 3.68%12 months $5,000+ 2.75% 2.71%9 months Special $5,000+ 3.50% 3.44%8 month Liquid $10,000+ 3.25% 3.20%6 months $5,000+ 2.65% 2.62%3 months $5,000+ 2.60% 2.57%30 day Special* $25,000+ 2.50% 2.47%*The 30-day CD has a minimum opening balance of $25,000.*The 8 Month Liquid CD Maintains a minimum balance of $10,000, and a maximum opening balance of $500,000.

How do you like the 8 months Liquid CD with a minimum required balance of $10,000 and a ceiling of $500,000?