institutional presentation 2 q13 v3

DESCRIPTION

TRANSCRIPT

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

| Apresentação do Roadshow

1

As of June, 2013 August, 2013

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

Statements regarding the Company’s future business perspectives and projections of operational and

financial results are merely estimates and projections, and as such they are subject to different risks and

uncertainties, including, but not limited to, market conditions, domestic and foreign performance in general

and in the Company’s line of business.

These risks and uncertainties cannot be controlled or sufficiently predicted by the Company management

and may significantly affect its perspectives, estimates, and projections. Statements on future

perspectives, estimates, and projections do not represent and should not be construed as a guarantee of

performance. The operational information contained herein, as well as information not directly derived from

the financial statements, have not been subject to a special review by the Company’s independent

auditors and may involve premises and estimates adopted by the management.

2

Disclaimer

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

| Company overview

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232 .1 Platform of brands of reference

Arezzo&Co is the leading Company in the footwear and accessories sector through its platform of Top of Mind brands

1

4

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232 .2 Company overview

Arezzo&Co is the reference in the Brazilian retail sector and has a unique positioning combining growth with high cash generation

1

5

Notes:

1. LTM as of June, 2013.

2. Refers to the Brazilian women footwear market (source: Euromonitor, IBGE and Company estimates) . Estimated for 2011.

Leading company

in the footwear

and accessories

sector with

presence in all

Brazilian states

Controlling

shareholders are

the reference in

the sector

Development of

collections with

efficient supply

chain

Asset light: high

operational

efficiency

Strong cash

generation and

high growth

9.8 million pairs of shoes (1)

591 thousand handbags (1)

2,842 points of sale

12% market share (2)

More than 40 years of

experience in the sector

Wide recognition

~11,500 models created

per year

Lead time of 40 days

7 to 9 launches per year

90% outsourced production

ROIC of 32.7% in 2Q13

2,014 employees

Net revenues CAGR:

33.2% (2007- 2Q13¹)

Net Profit CAGR: 39.6%

(2007- 2Q13¹)

Increased operating

leverage

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

Founded in 1972

Focused on brand and

product

Consolidation of industrial

business model located in

Minas Gerais

1.5 mm pairs per year

and 2,000 employees

Focus on retail

R&D and production

outsourcing on Vale dos Sinos

- RS

Franchises expansion

Specific brands for each

segment

Expansion of distribution

channels

Efficient supply chain

First store

Fast Fashion

concept

Launch of the

first design with

national success

+

Schutz launch

Launch of

new brands

Merger

Commercial operations

centralized in São Paulo

Strategic Partnership

(November 2007)

Industry Reference Foundation and structuring Industrial Era Corporate Era Retail Era

2012 and 2013 70‟s 80‟s 90‟s 00‟s

Opening of the first

shoe factory

Opening of the flagship

store at Oscar Freire

.3 Successful track record of

entrepreneurship

The right changes at the right time accelerated the Company's development 1

Consolidate

leadership

position

Initial Public Offering

(February 2011)

6

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

Post-offering

.4 Shareholder structure 1

Notes:

1. Arezzo&Co capital stock is composed of 88,637,034 common shares, all nominative, book-entry shares with no par value.

2. Including Stock Option Plan – Arezzo&Co’s executives

Shareholder structure as of September, 2013. 7

52.4% 47.6%

Birman family Others

1 Management ²

0.9%

Float

46.7%

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

8

.5 Culture & Management

1 01 That which is not transparent should not be done.

02 Always be true, so that at some point you are not false in your job. Always be authentic.

03 Clearly negotiate your goals and responsibilities, and consider compliance as a requirement for

continuity.

04 Do not uncover problems only. Blaming others will never be the solution. Take risks, propose

solutions. If you disagree with something, act!

05 Formalize everything, even in an informal way.

06 Always be flexible. Always be willing and ready for changes.

07 Goals met are, at least, the basis for the next goal.

08 Unite we stand! Divergences are constructive, conflicts are destructive.

09 A humble stance: the key to our success.

10 Enjoy. Like. Get involved. And always be happy!

Principles of success at Arezzo&Co:

2154

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232 .6 Strong platform of brands

Strong platform of brands, aimed at specific target markets, enables the Company to capture growth from different income segments

1

9

Notes:

1. Points of sales (2Q13); O = Owned Stores; F = Franchised Stores; MB = Multi-brand Stores; EX = Exports

2. % of each brand gross revenues (FY 2012)

3. 2Q13 (LTM) gross revenues, internal market only: does not include other revenues (not generated by the 4 brands)

4. % total (2Q13 LTM) gross revenues

Trendy

New

Easy to wear

Eclectic

Fashion

Up to date

Bold

Provocative

16 - 60 years old 18 - 40 years old

R$ 305.00/pair

R$ 705.9 million R$ 422.9 million

Pop

Flat shoes

Affordable

Colorful

12 - 60 years old

R$ 99.00/pair

R$ 36.9 million

Design

Exclusivity

Identity

Seduction

R$ 960.00/pair

R$ 4.7 million

20 - 45 years old

60.3% 36.1% 3.2% 0.4%

Brands

profile

Female

target

market

Sales

Volume 3

% Gross

Revenues 4

Retail price

point

Foundation 1972 1995 2008 2009

MB

7

O

2

O

17

F

332

MB

994

R$ 189.00/pair

O

28

F

29

MB

1,509

Dis

trib

uti

on

ch

an

nel

1

POS 1

%

gross

rev.2

72% 15% 12% 7% 49% 36%

EX

14

1%

EX

132

8%

EX

45

49% 9% 42%

MB

858

O

9

EX

5

46% 53% 1%

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232 .7 Multiple distribution channels

1

10

Flexible platform through three distribution channels with differentiated strategies, maximizing the Company's profitability

Gross Revenues per Channel

56 owned stores

being 7 Flagship

stores

Reach about 1,161

cities and 2,425

multi-brands

361 franchises in

more than 160 cities

Broad distribution in

every Brazilian state

Gross Revenue Breakdown – (R$ mm)¹

Franchises Multi-brands Owned stores Exports ² Total

Notes:

1. 2Q13 (LTM) gross revenues

2. Also includes other revenues in the domestic market

46% 25% 23% 6% 100%

554

304

283

63 2

1,204

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

| Business model

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

Management

BRANDS OF REFERENCE

Customer focus: we are at the forefront of Brazilian women fashion and design

Multi-channel Sourcing & Logistics Communication &

Marketing

SEASONED

MANAGEMENT

TEAM WITH

PERFORMANCE

BASED INCENTIVES

NATIONWIDE

DISTRIBUTION

STRATEGY

EFFICIENT

SUPPLY CHAIN

SOLID MARKETING

AND

COMMUNICATION

PROGRAM

ABILITY TO

INNOVATE

R&D

1 2 3 4 5

12

Unique business model in Brazil

2

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232 .1 Ability to Innovate

We produce 7 to 9 collections per year 2 I. Research

Creation: 11,500 SKUs / year

II. Development III. Sourcing IV. Delivery

Arezzo&Co fulfills the various aspirations of women, delivering on average 5 new models per day, allowing for consistent desire-driven purchases

Available for selection:

63% of SKUs created / year

13

Stores: 52% of SKUs created /

year

Creation

Launch

Orders

Production

Delivery

Normal sale

Discount sale

Winter I Winter II Winter III Summer I Summer II Summer III Summer IV

Activities JAN FEV MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

CRM – VIP sales

In-store events – PA

Stylists Fashion Advisors

.2 Broad media plan

2

14

The brand has an integrated and expressive communication strategy, from the creation

of campaigns to the point of sales

Strong presence in printed media

85 inserts in printed media in 170 pages in 2012 (32 million readers) Over 300 exhibition in fashion editorials in 1S13

Digital communication

Presence in electronic media and television

Demi Moore

Seasonal showroom in Los Angeles near

the Red Carpet Season

Celebrity Endorsement Marketing Events

830k accesses to site/month

(120k monthly access to Schutz‟s Blog)

Average navigation time: 8 minutes

Gisele Bündchen Blake Lively

+750 exhibition on TV e 150 exhibition in cinema in 2012 + 80 million impact

* Source: Indexsocial/ Agência Espalhe, 2013

Over 3 mm followers/ fans: Facebook,

Instagram and Twitter (all 4 Brands)

Arezzo is leader in interactions*

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232 .2 Communication & marketing program

reflected in every aspect of the stores

Stores constantly modified to incorporate the concept of each new collection, creating desire-driven purchases

2

15

All visual communication at stores is monitored and updated simultaneously throughout Brazil for each new collection

Flagship stores Store layout & visual merchandising

POS materials (catalogs, packaging, among others)

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

Distinguished storefront

.2 Atmosphere of stores: differentiated

concepts for each brand 2

16

Verão – Flagship Oscar Freire

Inverno – Flagship Oscar Freire

Visual merchandising:

Updates at low cost investment

Brings relevant information from

each collection to stores’ level

3 main updates per year

Chameleon project: constant

modification to incorporate the new

collection’s concept

Vídeo Wall

Closet Essentials

Niches and lighting

Jackets and accessories

Campaigns and marketing actions

Preeminence for products

Differentiated products

Exposure of a large variety of

products

Selling area inventory: lower

necessity of area for storage

Atmosphere of a jewelry store

Private shop experience

Focus on exclusivity, design and

highly selected materials

Wall display

Combos

Each theme is disposed in different niches

Accessories Sophisticated lighting Storage

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

Reception: 100,000 units/ day

Storage: 100,000 units/ day

Picking: 150,000 units/ day

Distribution: 200,000 units/ day

.3 Flexible production process…

2

17

Production speed, flexibility and scalability to ensure Arezzo&Co‟s expected growth based on asset light model

Arezzo’s scale and structure gives flexibility to source a large number

of SKU’s from various factories on a short time frame at competitive

prices

Owned factory with capacity to produce 1.1 million pairs annually

and strong relationship with Vale dos Sinos production cluster as

the main outsourcing region

Sourcing Model Gains of scale

Joint purchases Certification and auditing of suppliers

In-house certification and auditing ensure quality and punctuality

(ISO 9001 certification in 2008)

Coordination of material purchase jointly with shoe, handbag and

accessories’ suppliers

New Distribution Center Sourcing model – 90% of production outsourced

Consolidation and improvement of distribution in

national scale

1 2

3 4

10,2%

89,8%

AREZZO&CO OWNED FACTORY

OTHERS

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232 .4 Large capillarity and scale of store

chain 2

18

Brand Average

size (m2)

Net Revenue/ m2

(R$ 000s)

Total

Stores 1,2

67 324 399

111 214 638

1,650 10 214

1,030 6 368

234 13 206

Mono-brand store chain with high capillarity, reaching more than 160 cities and well-positioned among the retail companies Size and average sales per mono-brand stores - 2012

5

332 franchises +

17 owned stores(i) +

994 multi-brand clients

(i) 4 discount outlet

29 franchises +

28 owned stores(ii) +

1,509 multi-brand clients

(ii)1 discount outlet

Points of sale (2Q13)

TOTAL

9 owned stores

858 multi-brand clients

2 owned store +

7 multi-brand clients

361 franchises6 +

56 owned stores6 +

2,425 multi-brand clients

=2,842 points of sales

Source: IBGE, Companies’ Reports; number of stores according to latest data provided by the Companies Notes: 1. Considers only mono-brand stores of Arezzo and Schutz; 2. For Hering, considers only Hering Store chain stores; 3. 2008 data; 4. Net Revenue (assuming that sales taxes and deduction = 30% of gross revenues); 5. Considers Arezzo + Schutz, except for outlets, handbags’ stores and Schutz franchise; 6. Including export market

GDP³: 18%

A&C¹: 17%

GDP³: 55%

A&C¹: 57%

GDP³: 15%

A&C¹: 15%

GDP³: 7%

A&C¹: 7%

GDP³: 5%

A&C¹: 4%

57 sq m

85 sq m

80 sq m

Points of sale – average size: new stores are

increasing network average size

2010 2011 new stores 2012 new stores 2013 new stores

80 sq m

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232 .4 ...through owned stores…

Capturing value from the chain while developing retail know how and brands‟ visibility

2 Flagship Stores

19

Arezzo – Iguatemi / SP

Schutz – Oscar Freire/ SP

Anacapri – Eldorado/ SP

Greater brand awareness coupled with operational efficiencies

Clustering higher productivity stores in main areas (mainly SP and RJ) improving

operational efficiency and profitability:

Direct costumers interaction develops retail competences which are also reflected at

franchised stores

Flagship stores ensure greater visibility and reinforce brand image

R$ 3,289M

R$ 5,119M

Ow

ned

Fra

nchis

e

Annual Average

Sales per Store

2012

Total sales area and # of owned stores (sq. m)

# owned Stores

Arezzo – Oscar Freire/ SP

Schutz – Morumbi/ SP

88% 91% 81% 77%

80% 78% 80%

12% 9%

19%

23%

20%

22% 20%

2007 2008 2009 2010 2011 2012 2Q13

Flagship

Standard store

1,044

1,369 2,067

2,967

4,686

5,897 5,842

6 10

21 29

45

57 56

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

Structure applied to retail in order to achieve better sales and margin results as well as integrating and connecting all monobrand stores‟ back office

2

20

.4 … based on a retail oriented

structure...

Strong focus on Franchise & Owned Store performance

• All sales team (4000+) get connected through national internet broadcast for 3 Sales Conferences per year, creating an aligned sales pitch and great sense of motivation before each season

• Large service program to assist franchisees on sales and profitability goals

• Recurring training programs in products, fashion trends, sales techniques, store management, IT, among others

• Strong visual merchandising, trade marketing and ambiance investments and training

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

Intense retail training

Ongoing support: average of 6 stores/ consultant and average of

22 visits per store/ year

Strong relationship with and ongoing support to franchisee

IT integration with our franchises amount 100%

As mono-brand stores, franchises reinforce the branding in each

city they are located

2

4 or more

franchises

1 franchise

2 franchises

3 franchises

49%

10%

27%

15%

.4 …with efficient management of the

franchise network...

Model allows rapid expansion with little invested capital by Arezzo&Co and high profitability to franchisees Successful Partnership: “Win – Win” Franchise Concentration per Operator

100% of on-time payments

96% satisfaction of franchises1

Excellency in Franchising Award in the last 8 years (ABF)

Best Franchise in Brazil (2005 and 2012) and in the sector for 7 years since 2004

(# of Franchisees by # of Franchises)

Notes: 1H13 data

1. 96% of the current franchisees indicated they would be interested in opening a

franchise if they did not already have one

2. Annual sales of R$ 3,3 million + average initial investment of R$ 900 thousand +

working capital of R$ 600 thousand

21

5-year contract and average payback of 40 months2

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232 .4 ...and of the multi-brand stores

2

Multi-brand stores

22

Multi-brand stores‟ Gross Revenue¹ LTM Improved distribution and brand visibility Greater brand capillarity

Presence in over 1,161 cities

Rapid expansion at low investment and risk

Main Focus: share of wallet

Owner’s loyalty

Schutz Club – Relationship program that gives

advantages to the 50 Top Multi-brand stores, such as

better products display, training and awards to the best

sales teams.

Important sales channel for smaller cities

Sales team optimization: internal team and commissioned sales

representatives

Multi-brand stores widen the distribution capillarity and the brands‟ visibility, resulting in a strong retail footprint

Notes:

1. Domestic market only LTM

255.9

303.6

2,224

2,425

2000

2050

2100

2150

2200

2250

2300

2350

2400

2450

2500

210.000

220.000

230.000

240.000

250.000

260.000

270.000

280.000

290.000

300.000

2Q12 LTM 2Q13 LTM

Gross Revenue (R$ mn) # Stores

Multi-brand stores

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

Years

at Arezzo

Years of

experience

.5 Seasoned and professional

management team 2

Years

at Arezzo

Years of

experience Name

Title

Highly qualified management team

Stock option plan for key executives

Performance based compensation package for all employees

Independent business units leveraged on a single shared service structure: Industrial, Logistics, Financial and HR

Alexandre Birman

CEO

Claudia Narciso

Arezzo

David Python

Schutz

Yumi Chibusa

Anacapri

Milena Penteado

Alexandre Birman

Thiago Borges

CFO and Investor Relations Officer 18

14

2

18

24

10

5 10

5 15

5 13

Schutz

David Python

Supply Chain/

Sourcing

Cisso Klaus

CFO

Thiago Borges

CTO

Kurt Richter

HR

Raquel Carneiro

Marco Coelho

Internal Auditing

Arezzo

Claudia Narciso

Alexandre Birman

Anacapri

Yumi Chibusa

Alexandre

Birman

Milena Penteado

23

Name

Title

Kurt Ritchter

Director – CTO

Cisso Klaus

Director – Supply Chain/ Sourcing

Marco Coelho

Director – Internal Auditing

Raquel Carneiro

Director – HR

11

9

30

3

32

47

41

13

Maicon Americo

Director – Commercial 1 20

Commercial

Maicon Americo

Independent business units

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232 .6 Corporate governance

2

24

Welerson Cavalieri

Risk, Audit and Finance Committee

Juliana Rozenbaum (Coordinator)

José Bolonha (Coordinator)

Committees

Strategy Committee People Committee

Members:

Guilherme A. Ferreira and Thiago Borges (CFO)

Members:

Fabio Hering, Carolina Faria and Arthur N.

Grynbaum¹

Members:

Claudia Soares and Raquel Carneiro (HR

Director)

The new Board is comprised of 10 members, of which 4 are independent, and has a very large engagement on the strategic planning of Arezzo&Co

Name Experience Name Experience

Title Title

Board of Directors

Anderson Birman Chairman of the Board

Founder and Chairman of the Board, with over 40 years of

experience in the industry

Carolina Faria Member

Marketing consultant at True Brand & Business – Soul

Brand Services from 2010 to 2012. Previously, worked as

an executive at Ambev.

Fabio Hering Independent member

CEO and board member of Cia. Hering, where he has

been working for over 28 years.

Rodrigo C. Galindo Independent member

CEO of Kroton Educacional S/A, one of the biggest

education companies in the world, with over 500 thousand

students in colleges.

Welerson Cavalieri

Member

Partner at INDG/FALCONI Consultores de Resultados,

where he works for more than 19 years. Previously, was

an executive in big mining companies.

Juliana Rozenbaum Member

Over 13 years of experience as sell side equity research

analyst, focused mainly in retail and consumer companies.

Claudia Soares Independent Member

Former CFO and IR Officer at Via Varejo S.A. and

Executive Vice-President of Market Strategy at Companhia

Brasileira de Distribuição – GPA.

José Murilo Carvalho Member

President of the Attorney’s Association of Minas Gerais,

Board Member of the Brazilian Bar Association

Guilherme A. Ferreira Independent Member

CEO of Bahema Participações, board member of Pão de

Açúcar, Banco Signatura Lazard, Eternit, Tavex and Rio

Bravo Investimentos

José Bolonha Vice Chairman of the Board

Founder and CEO of “Ethos Desenvolvimento Humano e

Organizacional“; Board member of the Inter-American

Economic and Social Council (UN, WHO

1- CEO of Grupo Boticário (largest franchise company in Brazil)

and Vice-President at Abihpec (Brazilian Association Personal

Hygiene, Perfumes & cosmetics Industries)

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

| Market Overview and

| Sourcing and Industry Characteristics

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232 .1 Social upward mobility driving internal

consumption 3

26

Income growth and job creation lead to rapid social upward mobility and increasing internal consumption

2003 70 (36%) 54 (27%) 96 (55%)

+14 mi (2003-14E)

+49 mi (2003-14E)

2014E 2011

27 (14%) 22 (11%) 13 (8%)

66 (38%)

100 (52%)

115 (59%)

(Consumption growth as a result of the upward mobility in social classes; indexed 100 = class D/E)

Source: IBGE, FGV, LCA, Bain & Co., BCG, Roland Berger, IPC Maps

Classes A/B: monthly income above R$6,977 | Class C: monthly income between R$1,618 and R$6,977 | Class D: monthly income between R$1,013 and R$1,618 | Class E: monthly income below R$1,013

Class

D/E Class

C Class

B Class

A

Out-of Home Food

Furniture

Apparel and

Footwear

Prescription/OTC drugs

Hygiene and

Personal Care

Footwear and

apparel have the

largest growth

potential

Class C

Class A/B

Class D/E

Brazil experiences an accelerated process of social upward migration... (Millions of people)

1.0x

1.0x

1.0x

1.0x

4.2x

3.2x

3.4x

3.4x

7.0x

5.6x

5.3x

5.6x

9.4x

7.9x

7.3x

7.6x

Classes A/B: monthly income above R$4,808 | Class C: monthly income between R$1,115 and R$4,408 | Class D: monthly income between R$768 and R$1,115 | Class E: monthly income below R$768

...Resulting in a significant rise of consumer goods consumption, including Footwear and Apparel

1,0x 3,7x 6,6x 9,2x

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

30%

40%

15%

15%

Footwear Consumption 2013

10%

40% 42%

8%

Income Class

27

.2 Brazilian footwear market overview

3 Arezzo&Co has a significant stake of the women footwear market and has consistently increased its market share

Sports

Men

Kids

Women

Footwear

Class A Class D/E

Class C Class B

Arezzo&Co‟s market share1

Source: IBOPE Inteligência (Pyxis), Satra, World Bank, ABICALÇADOS, IEMI, MTE, MDIC, / SECEX, IBGE

Note: 1. Based on Euromonitor research and IBOPE Inteligência (Pyxis). Estimated Arezzo&Co market share considering women footwear market

Total footwear market (R$ bn)

Women footwear

Total footwear

2013E

CAGR (03-13E): + 9.2%

15.9

40.3

4%

7% 8%

9% 10%

11%

2007 2008 2009 2010 2011 2012

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232 .3 Brazilian handbags market overview

3 Arezzo&Co also has a relevant position within the fast growing handbag market in Brazil

Source: IBOPE Inteligência (Pyxis), Satra, World Bank, ABICALÇADOS, IEMI, MTE, MDIC, / SECEX, IBGE

Arezzo&Co current sell out breakdown 2Q13 LTM (R$ mn) Breakdown based on owned stores

Consolidated (including handbags and shoes) market

share: 9,3%

Opportunity to consolidate handbag leading position

86%

11%

Footwear

Handbags303.6

Note: 3% accessories

Total handbags market (R$ bn)

Women handbags

Total handbags

2013E

CAGR (03-13E): + 10.7%

4.0

5.1

Total addressable market (R$ bn)

80%

20%

Footwear

Handbags

19.9

28

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

Pairs

(millions)

Production World share

China 12,597 62.4%

Índia 2,060 10.2%

Brazil 894 4.4%

Vietnam 760 3,8%

Indonesia 658 3.3%

Pakistan 292 1.4%

Brazil is the third biggest footwear producer, with production mostly destined to supply

the domestic market. Competitive costs, flexibility on minimum production and short

lead time are the pillars to serve the fast fashion market

.4 Footwear Industry - Global Overview

and competitive advantages

Pairs (millions) Consumption World share

China 2,700 15.2%

USA 2,335 13.4%

India 2,034 11.7%

Brazil 780 4,5%

Japan 693 4.0%

Indonesia 627 3.6%

BRAZIL

Lead time: 40 days

Minimum/model: 800 pairs

Minimum/construction: 4,000 pairs

Production cap. (pairs) 894 million

Cost (w/o tax): USD 21/pair

Cost (w/tax): USD 27/pair

CHINA (different clusters)

Lead time: 120 to 150 days

Minimum/model: 5,000 pairs

Minimum/construction: 20,000 pairs

Production cap. (pairs): 12,000 million

Cost (FOB): USD 16-18/pair

Cost (DDP): USD 42-45/pair

INDIA

Lead time: 160 days

Minimum/model: 5,000 pairs

Minimum/construction: 20,000 pairs

Production cap. (pairs): 2,060

million

Cost (FOB): USD 15/pair

Cost (DDP): USD 23/pair

ITALY

Lead time: 70 days

Minimum/model: 800 pairs

Minimum/construction: 4,000 pairs

Production cap. (pairs): 202 million

Cost (FOB): USD 35/pair

Cost (DDP): USD 49/pair

VIETNAM

Lead time: 120 to 150 days

Minimum/model: 2,000 pairs

Minimum/construction: 8,000 pairs

Production cap. (pairs): 760million

Cost (FOB): USD 18/pair

Cost (DDP): USD 26/pair

3

Source: Abicalçados, Footwear News, Company estimates 29

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

Brazil is recognized by the quality and high specialization within different and complex

categories of shoes. The industry has been qualitatively developed in order to add

value to products and thus increase its competitive advantages over Asian suppliers

.5 Footwear Industry - Global footwear

offering

Global Footwear Offering: the higher and more centralized the country is

in the pyramid, the more focused it is in fashion, creation, design, luxury market ,

marketing and distribution management, with smaller production scale

Equipment assembly

Manufacturing operation

Manufacturer with own design and mostly local brand

Manufacturer with own design and global brand

Global Brands

Receive product and process specifications, as well as components and raw material

Assembly activities only

Usually don’t produce; Creation + own brand management Design and product specification Mostly internationally outsourced Supply chain management Totally decide over marketing and commercialization

Valu

e a

dd

ed

+

-

France

Italy Spain

Taiwan Brazil

Mexico

China India

Thailand Vietnam Other global

suppliers

Indonesia

B

A

C

D

E

Industry segmentation vs. value creation:

3

Source: BNDES, Company estimates 30

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232 .6 Arezzo&Co sourcing: Brazilian

competitive advantages

Vale dos Sinos region offer strong competitive advantages, a combination of production capacity, production flexibility, skilled labor and strong structure to support incentives for innovation and strengthening of industry‟s competitiveness

Source: Abicalçados, 2012 / ASSINTECAL / FAO / AICSUL.

Brazil is the world’s third largest

footwear producer

The world’s largest cattle: 13% of

the market

RS: 1 third (R$ 1 billion) of

Brazilian revenue in leather industry

Vale dos Sinos: one of the world’s

largest footwear manufacturing hubs

1,700 companies and entities: components,

footwear, machinery, tanneries, trade entities,

research and teaching institutions

Abundant skilled and specialized labor

Production flexibility:

volume X variety X speed

Production (million pairs)

Jobs (thousands)

819

338

Production (million pairs)

Jobs (thousands)

270

138

Production (million pairs)

Jobs (thousands)

216

110

BRAZIL

SOUTHERN REGION

VALE DOS SINOS

Vale dos Sinos: 26% of Brazilian footwear production

3

31

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

Trends and style

Design Technical

Design Engineering Samples Showroom

Logistics and distribution Store

Raw material price negotiations Scheduling + Manufacturer negotiation

1 2 3 4 5 6 7

.8 Arezzo&Co Sourcing Process and

supply chain management

Sourcing process and supply chain management focused on ensuring flexibility, speed

and cost control in the creation of new products Arezzo&Co sourcing process:

Coordinated management of production chain associated with Investments in product engineering: specific know

how

Arezzo&Co Raw materials

Finished products

Cost control

Engineering folder

Cost management efficiency

Quality standard guarantee

Efficient lead time

Flexibility

Chemicals and textile

Components

3

32

SKU

MODEL

CONSTRUCTION

10%

35%

70%

Reuse from collection to collection:

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

| Value Drivers Update

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

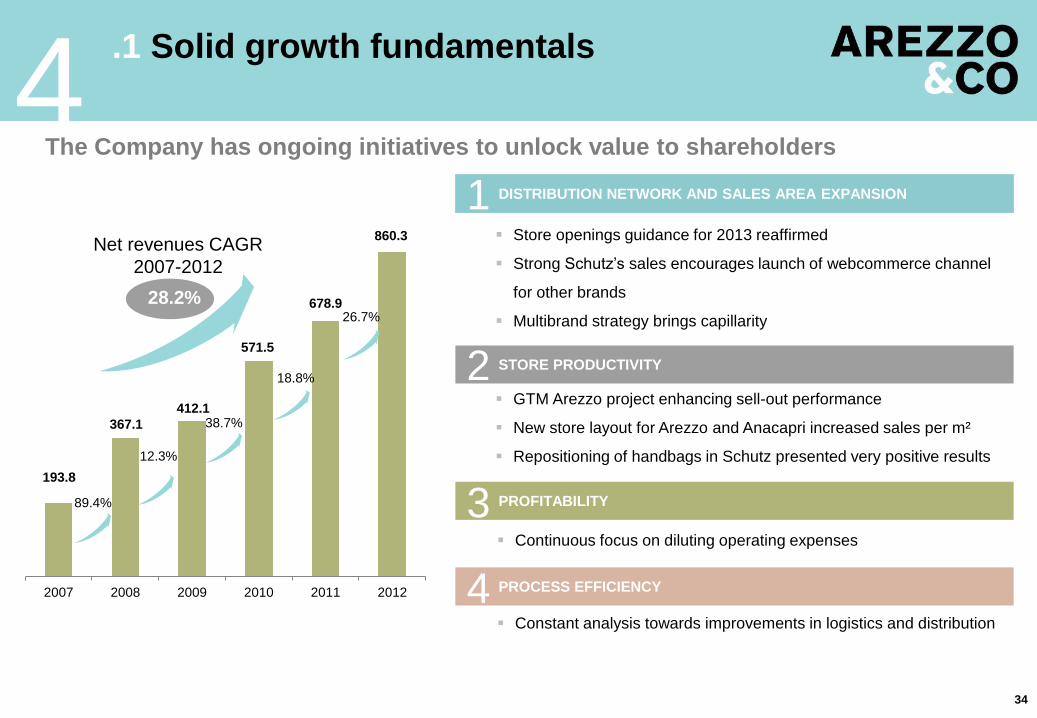

B:232 .1 Solid growth fundamentals

4

34

The Company has ongoing initiatives to unlock value to shareholders

193.8

367.1

412.1

571.5

678.9

860.3

2007 2008 2009 2010 2011 2012

89.4%

12.3%

38.7%

18.8%

26.7%

Net revenues CAGR

2007-2012

28.2%

Store openings guidance for 2013 reaffirmed

Strong Schutz’s sales encourages launch of webcommerce channel

for other brands

Multibrand strategy brings capillarity

DISTRIBUTION NETWORK AND SALES AREA EXPANSION

GTM Arezzo project enhancing sell-out performance

New store layout for Arezzo and Anacapri increased sales per m²

Repositioning of handbags in Schutz presented very positive results

STORE PRODUCTIVITY 2

Continuous focus on diluting operating expenses

PROFITABILITY 3

Constant analysis towards improvements in logistics and distribution

PROCESS EFFICIENCY 4

1

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232 .1 2013 Expansion Plan

Since IPO, for 2 consecutive years, store opening guidance was achieved; 2013 expansion is committed to 53 new stores with 14% growth in sales area

4

1) Includes international store operation

33

58

53 In addition to the store openings,

the company is committed to

expand existing stores by a total

of 1,000 sqm in 2013 and 2014

90% of the contracts already

signed

17 stores opened in 1H13

274 296 342

389

29

45

57

63

303

341

399

452

2010 2011 2012 2013

# Owned Stores

# Franchises

35

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

36

.1 Web commerce

4 With a strong growth in the last twelve months, web commerce represents 5% of

Schutz brands revenues

Best store in terms of sales in the whole chain

80 thousand pairs sold in the last 12 months

Vast and rich product mix assortment

5%+ of Schutz brand revenues in the 1H13

Roll-out to other brands expected in 2014

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

37

.2 GTM Arezzo

4 Under GTM Arezzo the Company expects to increase the product accuracy with new collection calendar a shorter lead time

Life cycle More fashion content; largest collections

presented to the franchisees

Collection

Continuables

Classic

Showroom

Fashion complement

Fast fashion

Continuables

Classic

Supply model

Fashion complement using information

from the sell out

Capturing quick trends, not only from

Arezzo’s stores, but also from market

research

Products automatically replaced in the

stores with some season colors

Open size run replacement

Products also automatically replaced in

the stores; only two colors. Full mark-up

sell-through

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

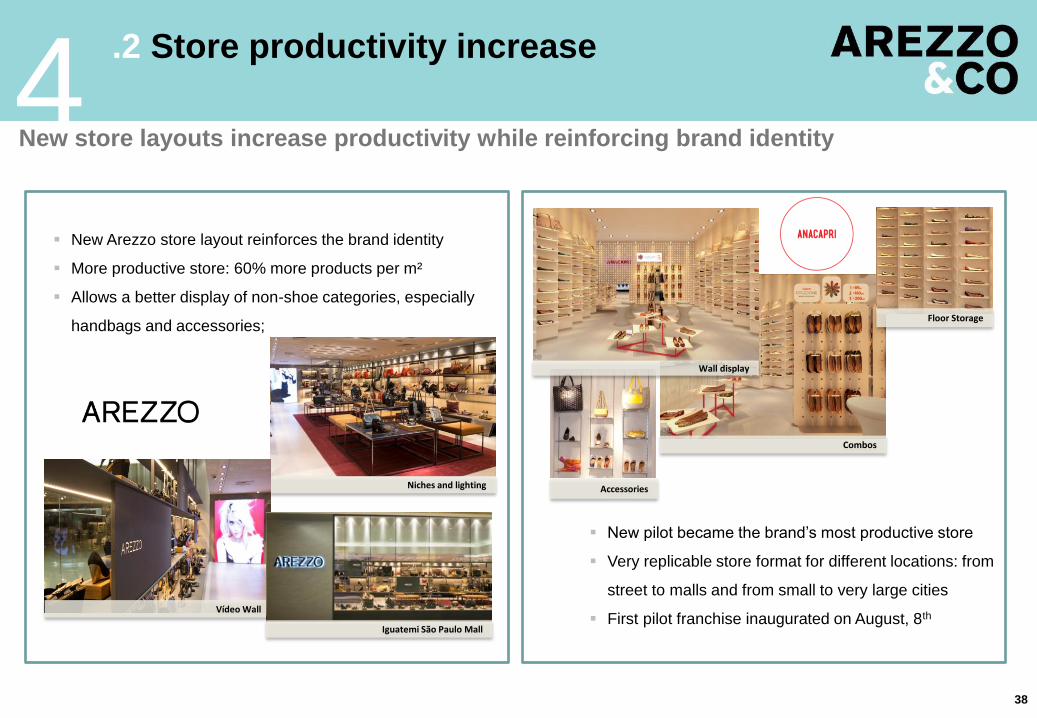

B:232 .2 Store productivity increase

4

38

Niches and lighting

Vídeo Wall

Iguatemi São Paulo Mall

Wall display

Combos

Accessories

Floor Storage

New Arezzo store layout reinforces the brand identity

More productive store: 60% more products per m²

Allows a better display of non-shoe categories, especially

handbags and accessories;

New pilot became the brand’s most productive store

Very replicable store format for different locations: from

street to malls and from small to very large cities

First pilot franchise inaugurated on August, 8th

New store layouts increase productivity while reinforcing brand identity

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

39

.2 Schutz handbags

4 New positioning of handbags in Schutz brand resulted in strong growth

Focus on product development fostering supply chain

Target strategy designed for each channel

Subdivision of categories by potential use

Reduction in the number of models

Different product mix by channel

Recent repositioning of Schutz handbags delivering positive results

5%

9%

2Q12 2Q13

Handbags as % of

Schutz revenues

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232 Key takeaways

40

Undisputable category leader 1

Significant growth potential 2

Reference brands 3

Scalable platform with operating leverage 5

Efficient and market oriented supply chain 4

High return on invested capital 6

4

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

| 2Q13 Financial Highlights 05

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232 .1 Operational and financial highlights

5

42

111.8 134.5 209.3 251.4 74.0

87.6

129.8 147.6

60.2

69.8

104.7

131.3

3.0

1.9

6.5

5.2

2Q12 2Q13 1H12 1H13

20.3%

16.0%

450.3

18.0%

535.4

18.3% 20.1%

25.4%

18.9%

13.7% 249.0

293.9

The Company’s main sales channels presented growth in 2Q13. In special, Franchises increased

20.3%, leveraged by 52 stores openings and expansion of 10 stores in the last twelve months.

Gross Revenue by channel – Domestic Market (R$ million)

Franchise Multi-brand Owned Stores Others¹

SSS Sell-out (owned stores + franchise )

SSS Sell-in (franchises)

1) Other: decreasing of 35.0% in 2Q13 and 20,3% in 1H13

1.2%

5.5%

3.7%

6.7%

n/a

10.4%

n/a

14.5%

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

255 276 309 361

25 31

50

56 16.3

18.4

23.1

28.0

2Q10 2Q11 2Q12 2Q13

+58359

417

280307 +52

+27

21.1%

13.3%

25.6%

Franchises Owned Stores Total sq m

5

43

.2 Operational and financial highlights

Key highlights

Strong Gross Revenue growth, especially in the Schutz brand that increased by 35.0% in 2Q13 compared to 2Q12

2Q13 ended with 417 store chain and Sales area expansion of 21.1% year-over-year

2Q13 Net Revenue increased by 19.1% year-over-year

Number of Stores (R$ mn) and Total Area (sq m - „000) CAGR 07-13 (2Q13 LTM): 33.2%

Net Revenues (R$ mn)

Area CAGR 07- 13 (1Q13LTM): 17.0%

199.5 237.6 193.8

367.1 412.1

571.5 678.9

860,3

2Q12 2Q13 2007 2008 2009 2010 2011 2012

19.1%

89.4%

12.3%

38.7%

26.7% 18.8%

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

8.0

57.316.9%20.6%

34.6 40.5

49.3

69.1

17.4%17.0%

15.9% 15.8%

2Q12 2Q13 1H12 1H13

EBITDA EBITDA margin

5

44

.3 Operational and financial highlights

Gross Profit (R$ million)

89.9

106.1

157.1

195.5

45.1% 44.6%

43.5% 44.6%

2Q12 2Q13 1H12 1H13

Gross profit Gross margin

17.9%

24.4%

EBITDA (R$ million)

15.6%

1 2.8%

25.8 29.1 36.6

48.4

12.9% 12.2%

11.6% 11.0%

2Q12 2Q13 1H12 1H13

Net income Net Margin

5.3 41.9

Net Income (R$ million)

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

45

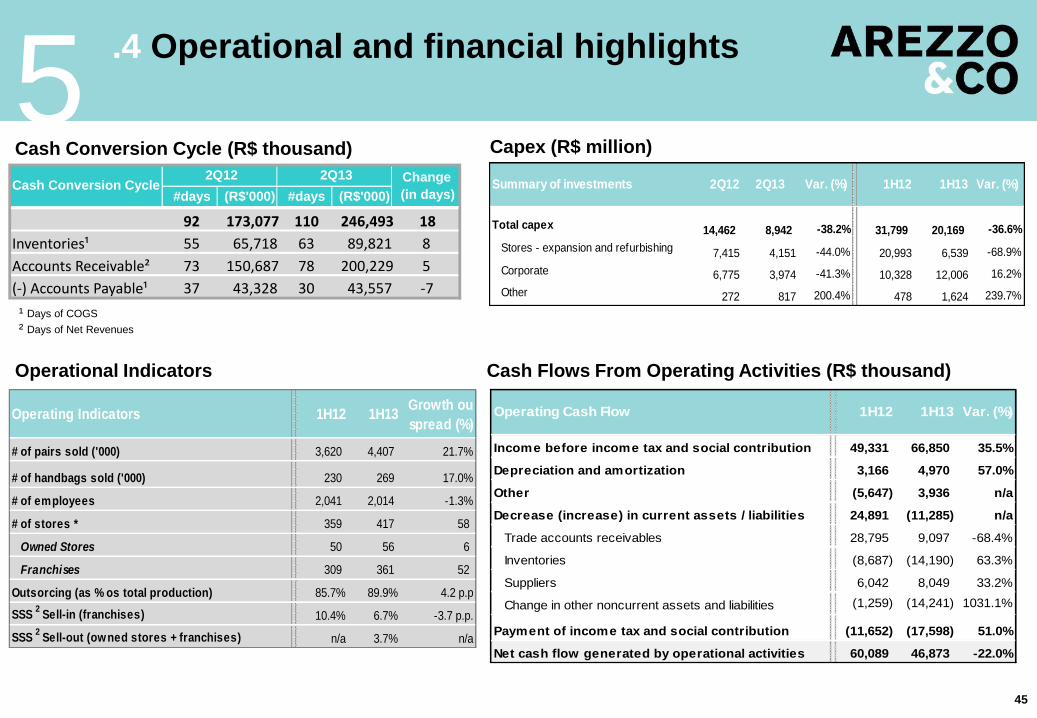

5 .4 Operational and financial highlights

Cash Conversion Cycle (R$ thousand)

Cash Flows From Operating Activities (R$ thousand)

Capex (R$ million)

¹ Days of COGS

² Days of Net Revenues

Operational Indicators

,

,

,

,

Total capex 14,462 8,942 -38.2% 31,799 20,169 -36.6%

Stores - expansion and refurbishing 7,415 4,151 -44.0% 20,993 6,539 -68.9%

Corporate 6,775 3,974 -41.3% 10,328 12,006 16.2%

Other 272 817 200.4% 478 1,624 239.7%

Summary of investments Var. (%)1H132Q12 1H122Q13 Var. (%)

1H12 1H13 Growth ou

spread (%)

# of pairs sold ('000) 3,620 4,407 21.7%

# of handbags sold ('000) 230 269 17.0% 0.2%

# of employees 2,041 2,014 -1.3%

# of stores * 359 417 58

Owned Stores 50 56 6

Franchises 309 361 52

Outsorcing (as % os total production) 85.7% 89.9% 4.2 p.p

SSS 2 Sell-in (franchises) 10.4% 6.7% -3.7 p.p.

SSS 2 Sell-out (owned stores + franchises) n/a 3.7% n/a

Operating Indicators

Income before income tax and social contribution 49,331 66,850 35.5%

Depreciation and amortization 3,166 4,970 57.0%

Other (5,647) 3,936 n/a

Decrease (increase) in current assets / liabilities 24,891 (11,285) n/a

Trade accounts receivables 28,795 9,097 -68.4%

Inventories (8,687) (14,190) 63.3%

Suppliers 6,042 8,049 33.2%

(1,259) (14,241) 1031.1%

Payment of income tax and social contribution (11,652) (17,598) 51.0%

Net cash flow generated by operational activities 60,089 46,873 -22.0%

Change in other noncurrent assets and liabilities

1H13 Var. (%)Operating Cash Flow 1H12

#days (R$'000) #days (R$'000)

92 173,077 110 246,493 18

Inventories¹ 55 65,718 63 89,821 8

Accounts Receivable² 73 150,687 78 200,229 5

(-) Accounts Payable¹ 37 43,328 30 43,557 -7

Cash Conversion Cycle 2Q12 2Q13 Change

(in days)

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

46

5 .5 Operational and financial highlights

Indebtedness (R$ thousand)

Indebtedness totaled R$ 107.9 million in 2Q13 versus

R$ 87.9 million in 1Q12

Long-term debt relevance stood at 43.7% in 2Q13 versus

53.1% in 1Q12

Indebtedness policy remained conservative, with low

weighted-average cost of Company's total debt

2Q12 1Q13 2Q13

Cash 205,819 213,306 214,411

Total debt 51,117 87,880 107,862

Short term 25,548 41,226 60,763

% total debt 50.0% 46.9% 56.3%

Long-term 25,569 46,654 47,099

% total debt 50.0% 53.1% 43.7%

Net debt (154,702) (125,426) (106,549)

Cash position and

Indebtedness

EBITDA LTM 118.007 149.731 155.575

Net debt/EBITDA LTM -1,3x -0,8x -0,7x

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

47

Appendix

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

48

.4 Key financial indicators

A

1 - Includes non-recurring expense in 1Q12 in Other Operating Revenues and Expenses: Arezzo&Co terminated its contract with Star Export Assessoria e Exportação Ltda. (“Star”), which had been providing

technical support and advice services for procurement and inspection of independent factories and workshops contracted to make products. As part of the termination, a payment of R$ 8 million was made and

Star signed a five-year non-compete agreement. On the same date, a contract was signed with another company that has the same technical capability, providing the same type of services on special commercial

terms to reduce costs while maintaining the same quality of services.

2 - Working Capital: current assets minus cash, cash equivalents and marketable securities less current liabilities minus loans and financing and dividends payable.

3 - Invested capital: working capital plus fixed assets and other long-term assets less income tax and deferred social contribution.

4 - Net debt is equal to total interest-bearing debt position at the end of a period less cash and cash equivalents and short-term financial investments.

2Q12 2Q13Growth or

spread%1H12 1H13

Growth or

spread%

Net revenues 199,468 237,639 19.1% 360,829 438,678 21.6%

COGS (109,533) (131,581) 20.1% (203,721) (243,187) 19.4%

Gross profit 89,935 106,058 17.9% 157,108 195,491 24.4%

Gross margin 45.1% 44.6% -0.5 p.p. 43.5% 44.6% 1.1 p.p. -

SG&A (57,050) (67,965) 19.1% (110,972) (131,347) 18.4% - 10,915.00

% of Revenues 28.6% 28.6% 0.0 p.p 30.8% 29.9% -0.9 p.p

Selling expenses (40,895) (48,582) 18.8% (75,152) (92,445) 23.0% - 7,687.00

Ow ned stores (18,543) (22,020) 18.8% (34,042) (44,357) 30.3% - 3,477.00

Selling, logistics and supply (22,352) (26,562) 18.8% (41,110) (48,088) 17.0% - 4,210.00

General and administrative expenses (14,209) (17,891) 25.9% (25,808) (35,220) 36.5% - 3,682.00

Other operating revenues (expenses)1 (197) 893 n/a (6,846) 1,288 n/a 1,090.00

Depreciation and amortization (1,749) (2,385) 36.4% (3,166) (4,970) 57.0% - 636.00

Ebitda 34,634 40,478 16.9% 49,302 69,114 40.2%

Ebitda margin 17.4% 17.0% -0.4 p.p. 13.7% 15.8% 2.1 p.p.

Net income 25,763 29,057 12.8% 36,615 48,423 32.2%

Net margin 12.9% 12.2% -0.7 p.p. 10.1% 11.0% 0.9 p.p.

Working capital2 - as % of revenues 21.8% 26.1% 4.3 p.p 21.8% 26.1% 4.3 p.p

Invested capital3 - as % of revenues 29.4% 33.9% 4.5 p.p. 29.4% 33.9% 4.5 p.p.

Total debt 51,117 107,862 111.0% 51,117 107,862 111.0%

Net debt4 (154,702) (106,549) n/a (154,702) (106,549) n/a

Net debt/EBITDA LTM -1.3 X -0.7 X n/a -1.3 X -0.7 X n/a

Key financial indicators

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

49

.5 History – Franchises and Owned Stores

A

1. Includes areas in square meters of 9 international stores

2. Includes 5 outlet-type stores with a total area of 1,227 m2

3. Includes areas in square meters of stores expansion

2Q12 3Q12 4Q12 1Q13 2Q13

Sales area 1,3 - Total (m²) 23,112 24,531 26,543 26,659 27,996

Sales area - franchises (m²) 18,005 19,125 20,646 20,731 22,154

Sales area - Ow ned stores2 (m²) 5,107 5,406 5,897 5,928 5,842

Total number of domestic stores 351 368 390 391 408

# of franchises 301 316 334 335 353

Arezzo 295 300 311 312 324

Schutz 6 16 23 23 29

# of owned stores 50 52 56 56 55

Arezzo 19 19 19 19 17

Schutz 22 24 27 27 27

Alexandre Birman 1 2 2 2 2

Anacapri 8 7 8 8 9

Total number of international stores 8 9 9 9 9

# of franchises 8 8 8 8 8

# of owned stores 0 1 1 1 1

History - Franchises and Owned Stores1

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

50

.6 Balance Sheet - IFRS

A Assets 2Q12 1Q13 2Q13

Current assets 441,382 539,360 537,059

Cash and cash equivalents 4,799 8,427 7,515

Financial Investments 201,020 204,879 206,896

Trade accounts receivables 150,687 211,251 200,229

Inventory 65,718 87,481 89,821

Taxes recoverable 7,393 15,797 18,460

Other credits 11,765 11,525 14,138

Non-current assets 105,507 132,558 137,303

Long-term receivables 16,135 15,657 15,530

Financial Investments 98 178 21

Taxes recoverable 360 377 377

Deferred income and social contribution 8,705 8,007 6,898

Other credits 6,972 7,095 8,234

Property, plant and equipment 47,693 63,338 65,014

Intangible assets 41,679 53,563 56,759

Total Assets 546,889 671,918 674,362

Liabilities 2Q12 1Q13 2Q13

Current liabilities 107,458 146,211 148,087

Loans and financing 25,548 41,226 60,763

Suppliers 43,328 69,021 43,556

Dividends and interest on equity capital payable 9,701 0 9,346

Other liabilities 28,881 35,964 34,422

Non-current liabilities 29,984 52,102 54,386

Loans and financing 25,569 46,654 47,099

Related parties 975 969 978

Other liabilities 3,440 4,479 6,309

Equity 409,447 473,605 471,889

Capital 105,917 106,857 156,000

Capital reserve 172,830 173,838 125,190

Income reserves 105,407 173,544 153,162

Profit 25,293 19,366 37,537

Total liabilities and shareholders' equity 546,889 671,918 674,362

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

51

.7 Income Statement - IFRS

A Income statement - IFRS 2Q12 2Q13 Var.% 1H12 1H13 Var.%

Net operating revenue 199,468 237,639 19.1% 360,829 438,678 21.6%

Cost of goods sold (109,533) (131,581) 20.1% (203,721) (243,187) 19.4%

Gross profit 89,935 106,058 17.9% 157,108 195,491 24.4%

Operating income (expenses): (57,050) (67,965) 19.1% (110,972) (131,347) 18.4%

Selling (41,811) (49,709) 18.9% (76,818) (95,008) 23.7%

Administrative and general expenses (15,042) (19,149) 27.3% (27,308) (37,627) 37.8%

Other operating income net (197) 893 n/a (6,846) 1,288 n/a

Income before financial result 32,885 38,093 15.8% 46,136 64,144 39.0%

Financial income 810 666 -17.8% 3,195 2,706 -15.3%

Income before income taxes 33,695 38,759 15.0% 49,331 66,850 35.5%

Income tax and social contribution (7,932) (9,702) 22.3% (12,716) (18,427) 44.9%

Current (6,164) (8,593) 39.4% (11,409) (19,061) 67.1%

Deferred (1,768) (1,109) -37.3% (1,307) 634 -148.5%

Net income for period 25,763 29,057 12.8% 36,615 48,423 32.2%

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232

52

.8 Cash Flow Statement - IFRS

A Statement of cash flow 2Q12 2Q13 1H12 1H13

Operating activities

Income before income tax and social contribution 33,695 38,759 49,331 66,850 1

231 7,139 (2,481) 8,906

Depreciation and amortization 1,749 2,385 3,166 4,970

Income from financial investments (2,743) (2,896) (6,604) (6,165)

Interest and exchange rate 1,336 5,057 814 5,067

Other (111) 2,593 143 5,034

Decrease (increase) in assets

Customer receivables 22,801 11,471 28,795 9,097

Inventory (108) (2,716) (8,687) (14,190)

Recoverable taxes 2,331 (2,663) 2,796 (4,179)

Variation other current assets (1,378) (3,394) (65) (3,223)

Judicial deposits (123) (359) (641) 545

Decrease (increase) in liabilities

Suppliers (12,798) (25,464) 6,042 8,049

Labor liabilities 4,100 4,338 1,269 (181)

Fiscal and social liabilities 1,268 (2,467) (4,347) (8,771)

Variation in other liabilities (477) 1,732 (271) 1,568

Payment of income tax and social contribution (11,652) (13,935) (11,652) (17,598)

Net cash flow from operating activities 37,890 12,441 60,089 46,873

Net cash used in investing activities (52,221) (7,906) (68,207) (30,266)

Net cash used in financing activities - third parties 18,937 14,926 11,644 8,712

Net cash used in financing activities (6,020) (20,373) (14,255) (29,322)

Increase (decrease) in cash and cash equivalents (1,414) (912) (10,729) (4,003)

Increase (decrease) in cash and cash equivalents (1,414) (912) (10,729) (4,003)

Adjustments to reconcile net income with

cash from operational activities

R:152

G:216

B:218

R:80

G:179

B:207

R:216

G:181

B:163

R:177

G:181

B:121

R:119

G:119

B:119

R:217

G:217

B:217

R:160

G:160

B:160

R:208

G:240

B:232 IR Contacts

Thiago Borges

Leonardo Pontes dos Reis, CFA

Phone: +55 11 2132-4300

www.arezzoco.com.br

CFO and IR Officer

IR Manager