indian fertiliser sector - hdfc securities

TRANSCRIPT

INSTITUTIONAL RESEARCH

HDFC sec Investor Forum

Technology and New Age Businesses Key takeaways

29 Dec 2018

Amit Chandra [email protected] +91-22-6171-7345

Apurva Prasad [email protected] +91-22-6171-7327

CORPORATES MCap (Rs bn)

TECH & NEW AGE BUSINESSES

Infosys 2,858

L&T Infotech 298

L&T Tech 174

Hexaware 98

Zensar 52

MCX 37

Majesco 14

TECH EXPERTS

IBM NA

Capgemini NA

NASSCOM NA

UiPath NA

Infor NA

Large US Bank NA

Large European Bank NA

Akshay Ramnani [email protected] +91-22-6171-7334

2

Technology and New Age Businesses

We hosted ‘IT and New Age Business’ Investor Forum in Mumbai with 14 corporates/experts participating in the event. The participating corporates/experts were across the IT spectrum of (1) Large cap IT services (Infosys), (2) IT midcaps & smallcaps (L&T Infotech, L&T Tech, Hexaware, Zensar, Majesco), (3) Global Tech product & services majors (IBM, Capgemini), (4) Software products (Infor, UiPath), (5) Enterprise Tech Buyers (Large US/European Banks) and (6) Industry association (NASSCOM). We believe that Indian IT’s growth compass is intact and the insights from the forum validates key trends in (1) Rapid pivot to digital and hybrid cloud adoption, (2) Buoyant demand environment, (3) Captive/automation challenges and (4) Capability and sales augmentation to align with changing business and addressable market.

Infosys highlighted (1) Improved business momentum attributed to improving win-rate in large deals, (2) Expectation of moderation in the elevated attrition based on multiple interventions (compensation and variable payouts) and (3) Strong traction in Digital.

L&T Infotech highlighted (1) Rapid sales transformation (Agile staff vs. RFP specialists), (2) Strong positioning in digital (Analytics, Cloud infra and cybersecurity focus), (3) Micro-vertical strategy and reduction in client concentration risks (large deal wins across verticals – BFSI, Pharma). L&T Tech highlighted (1) Synergies from recent acquisitions (Esencia, Graphene), (2) Revival of high-margin verticals (Industrial Products, Process Industry), (3) Broad-based growth across verticals supported by strong deal wins.

Hexaware highlighted (1) Skilling initiatives, (2) Inorganic plans to augment growth, and (3) Near-term project fulfillment risk (strong

demand and tight labour market). Zensar highlighted (1) Strong deal wins driving core business, and (2) Increase in onsite component, lateral hiring and sub-contracting for large deals posing near-term margin hurdles. Majesco highlighted (1) Focus on sales engine following leadership change, and (2) Continuity of large addressable opportunity (via IBM channel).

IBM expert highlighted the scope of Hybrid cloud model, growth tapering in digital as it gains scale (expected to moderate to 17-20% growth) and the threat of automation. Capgemini experts elaborated the shift to larger vendors as digital scales, enterprise cloud adoption trends (public and private), increase in fresher intake and risk of lower profitability in digital ahead (such as large banks).

Uipath elaborated the RPA (robotic process automation) opportunity and use-cases, Strengthening SI partner ecosystem and platform comparison. Infor highlighted the trends between cloud and on-prem ERP, opportunity from integration of complex architecture and the impact from automation tools. NASSCOM representative highlighted the Skilling initiatives, Increase in workforce localisation and ER&D trends (captive intensity).

Tech expert from large US Bank spoke about shift away from staff augmentation, strengthening tech capabilities (vs. service providers) at captives and continuity in gradual shrinkage of legacy systems. Tech expert from large European bank elaborated shift from offshore to captive supported by increased use of automation and focus on IPs, cloud strategy and rapid adoption of newer technologies (Fintech competition).

Top Picks: TCS, LTI, LTTS, Zensar, Majesco

Technology sector Growth compass intact

3

Technology and New Age Businesses

Infosys was represented by Sandeep Mahindroo (Finance Controller and Head Investor Relations) and Subhra Das (Investor Relations). Following are the key takeaways:

Infosys (INFY) witnessing ‘much better’ business momentum as compared to last year. Large deal wins have accelerated to ~USD 1.5bn quarterly rate (normalised). More stability at the top management level is also leading to better deal wins. The company continues to focus on >USD 50mn deal buckets.

For INFY, Digital is higher margin business and the headcount delivery-mix in digital is similar to the company average. Recent surge in deal wins is a result of better win-rate as compared to increase in overall pipeline.

There is greater focus on the supply side as demand environment is strong. Attrition is elevated at 20% and is not sustainable. The company expects it to lower to 14-15% range. Interventions to attrition include (1) Timely compensation increase, and (2) Better variable payout in 1HFY19.

Transition period of recent large deals is expected to keep costs elevated in the near term, INFY will operate within guided EBIT margin band of 22-24%. There is limited probability for passage of H-1B legislation with mid-term elections behind.

INFY’s exposure to UK is lower vs. peers and does not expect risk from Brexit. Some clients of INFY are talking about early signs of trade war impact, although there are no concrete evidence of cuts in spend seen.

We are positive on INFY based on (1) Strong and broad-based deal win trajectory, (2) Robust Core verticals (BFSI/Retail) trend and acceleration in Manufacturing and Hi-tech verticals, (3) Digital-led growth, and (4) Stability in large accounts. Expect rev/EPS CAGR of 9/12% over FY18-21E and maintain BUY with TP of Rs 830.

Infosys (CMP Rs 657, Mcap Rs 2,858bn, BUY, TP Rs 830)

Surge in deals

Source : Company, HDFC sec Inst Research

YE March (Rs bn) FY17 FY18 FY19E FY20E FY21E

Net Revenue 684.85 705.22 830.48 930.67 1,024.59

EBITDA 186.05 190.10 221.22 253.85 282.95

APAT 143.53 147.34 165.18 182.74 205.24

Diluted EPS (Rs) 33.0 33.9 38.0 42.0 47.2

P/E (x) 19.9 19.4 17.3 15.6 13.9

EV / EBITDA (x) 13.3 13.4 11.4 9.8 8.6

RoE (%) 22.0 24.5 24.6 25.9 26.3

4

Technology and New Age Businesses

L&T Infotech was represented by Nitin Mohta, Head Investor Relations & Treasury Investment. Following are the key takeaways: Leadership & Strategy L&T Infotech (LTI) has laid out two key changes over the past two

years which include: 1) Sales & Marketing Transformation and 2) People and Capability Transformation. LTI’s salesforce has increased from 135 people to over 200 people currently and there is shift to ‘Agile’ sales staff as compared to RFP specialists earlier.

‘Minecraft’ and ‘ADEA’ programs were introduced (in late-2016) to mine large existing accounts (non T-20) and have delivered strong success. The program includes a dedicated sales manager, a dedicated delivery manager and a dedicated domain consultant for Top 21-to-50 accounts in addition to the T-20 accounts.

LTI has identified analytics, cyber security, cloud based infrastructure management as investment areas and it’s investing to augment its capabilities in those areas. The company aims to be a talent magnet in the industry. LTI has launched social media at workplace which makes collaboration very easy and replaces email communications.

Digital For LTI, Digital delivery-mix is not onsite heavy unlike peers. Lower

exposure to UI/UX and decade long relation with clients allows the company better onsite-offshore mix in digital.

Large Account Concentration Citi is the largest client (~15% of rev). LTI is making conscious

efforts like mining their lower bucket accounts to bring down concentration of Citi & other top accounts. Large deals across verticals like BFSI and Pharma will also help in reducing the client concentration.

Vertical strategy For each vertical that it operates in, LTI has at least one anchor

referenceable logo with USD 25-30mn in annual revenue. LTI is not focusing on Telecom and Public services industries. LTI does not intend to go big in Retail, whereas CPG & Pharma, BFS and Media & Hi-tech are growth verticals.

In each of the vertical that LTI operates in, they have a micro vertical focus. In BFS they are focused on capital market and wholesale banking and less on retail banking sub-vertical. In the Insurance vertical, LTI is focused on Property & Casualty as compared to Life & Annuity segment.

We are positive on LTI based on (1) Increasing penetration in Digital, (2) Ramp-up of large deals expected to accelerate BFSI CPG & Pharma, (3) Favourable delivery-mix, (4) Stable top accounts’ outlook, and (5) Marquee client base and robust management bandwidth. Maintain BUY with TP of Rs 2,255.

L&T Infotech (CMP Rs 1,731, Mcap Rs 298bn, BUY, TP Rs 2,255)

Strong ‘micro’ strategy

YE March (Rs bn) FY17 FY18 FY19E FY20E FY21E

Net Revenue 65.01 73.06 94.17 107.96 122.48

EBITDA 12.30 11.87 18.69 21.10 23.92

APAT 9.71 11.61 15.08 16.25 18.26

Diluted EPS (Rs) 56.1 67.1 87.2 93.9 105.5

P/E (x) 30.9 25.8 19.9 18.4 16.4

EV / EBITDA (x) 22.9 23.6 14.9 12.9 11.7

RoE (%) 36.9 33.2 35.5 32.1 30.6

Source : Company, HDFC sec Inst Research

5

Technology and New Age Businesses

L&T Tech (CMP Rs 1,701, MCap Rs 174bn, BUY, TP Rs 2,055)

Improving business mix L&T Technology Services (LTTS) was represented by Pinku Pappan, Head Investor Relations. Following are the key takeaways:

Transportation vertical (32% of rev) is expected to grow at >15% YoY, (2) Industrial products (21% of rev) expected to grow 10-11% YoY, (3) Telecom, Hi-tech (27% of rev) expected to grow at >15%, Process industry (14% of rev) is expected to grow at >15% and Medical devices (6% of rev) at >20%. LTTS plans to grow medical devices to ~10% of its revenue.

LTTS’ client base (51 of top 100 R&D spenders) includes 7 of the top-10 in Transportation vertical, 8 of the top-10 in Hi-tech vertical, 3 of the top-5 in Medical vertical, 7 of the top-10 in Industrial and Process vertical. LTTS’ top-30 customers have an R&D spend of USD 75bn (USD 375mn is LTTS’ revenue from its T-30) and LTTS’ average customer tenure has been >6 years.

Inorganic opportunities expected in areas of medical devices, automotive verticals and in valuation band of 1-2x EV/Rev. LTTS plans acquisitions to contribute USD 100mn to FY21 revenue.

Esencia and Graphene (1.7% of rev) are high-value business with better bill-rates and supporting growth in Hi-tech vertical.

Improvement in business-mix towards higher margin Industrial products, Process industry and Medical devices verticals are tailwinds for margin.

Positive on LTTS based on (1) Broad-based growth across verticals (led by Process Industry/ Transportation) and recovery in Industrial Product, (2) Continuity in large deal wins and strong pipeline, (3) Improving business-mix leading to better margin profile, (4) Large account mining opportunity in T-30 accounts and limited competition in multiple verticals, (5) Solution/ platform strategy driving cross vertical opportunities (Hi-tech-Automotive). Expect rev/EPS at 20/28% CAGR over FY18-21E and maintain BUY with TP of Rs 2,055.

YE March (Rs bn) FY17 FY18 FY19E FY20E FY21E

Net Revenue 32.48 37.47 51.32 61.67 73.12

EBITDA 5.85 5.76 9.34 11.44 13.75

APAT 4.25 4.74 7.06 8.17 10.11

Diluted EPS (Rs) 41.8 46.4 68.9 79.7 98.6

P/E (x) 40.7 36.6 24.7 21.3 17.2

EV / EBITDA (x) 29.3 29.6 18.2 14.5 11.7

RoE (%) 33.3 27.7 32.9 30.6 29.6

Source : Company, HDFC sec Inst Research

6

Technology and New Age Businesses

Hexaware (CMP Rs 330, Mcap Rs 98bn, BUY, TP Rs 475)

IMS/BPM growth leadership Hexaware was represented by R Srikrishna (CEO & Executive Director). Following are the key takeaways:

Tech labour market conditions are tight with full employment and a strong demand environment. Onshore hiring is a medium term plan to mitigate H-1B risk, however in the near-term cost escalation and project fulfillment is a risk. H-1B scenario is tighter than ever before and more executive barriers currently.

Structural challenge of the industry remains despite the macros and long term downward curve for the industry for legacy business.

In terms of contract renewals, similar trends are seen as compared to industry: industry trend of 30% of contracts getting renewed, 25% getting renewed with automation, 28% contracts change in service providers and 17% moving to captive.

Security, Automation, Cloud, Transformation business are 4 reasons for spend. Data center revenue streams shifting to AWS, Azure.

Hexaware leadership is also undergoing re-skilling in newer tech. The company is building strong internal tech – hired CTO in Jan 2018.

The company expects sustainable ~13% organic growth over medium-term. Spend plans of USD 250-300mn on acquisitions over 3 years (1x to 2x EV/rev valuation range) in areas of CX, Cloud and Design, inorganic revenue of ~USD 150mn over 3 years.

Positive on Hexaware based on (1) Continuity in IMS/BPM growth leadership, (2) Strong deal pipeline and larger deal size, (3) Strong traction in existing accounts ahead supported by ramp-up of large deal wins, (4) Geo expansion (Europe) and recovery in Enterprise Solutions (Microsoft partnership). Expect rev/EPS CAGR at 13/16% over CY17-20E and maintain BUY with TP of Rs 475.

YE December (Rs bn) CY16 CY17 CY18E CY19E CY20E

Net Revenue 35.35 39.42 46.71 55.64 62.96

EBITDA 5.78 6.55 7.45 8.84 10.04

APAT 4.20 4.99 6.22 6.90 7.85

Diluted EPS (Rs) 13.9 16.9 20.9 23.2 26.4

P/E (x) 23.7 19.6 15.8 14.2 12.5

EV / EBITDA (x) 16.1 13.9 11.9 9.7 8.2

RoE (%) 26.7 26.9 28.6 27.3 26.8

Source : Company, HDFC sec Inst Research

7

Technology and New Age Businesses

Zensar was represented by Navneet Khandelwal (CFO) and Ajay Bhandari (EVP). Following are the key takeaways:

Zensar has transformed itself over the last two years into a 100% Digital focussed company. The company has revamped its US sales engine, has become selective in chasing deals, adopted POC led sales pitch which has led to increase in deal win ratio.

TCV wins over the last 18 months has been USD 800mn (USD 600mn in FY18 and USD 200mn in 1HFY19). This includes two large USD 100mn deals and one USD 79mn large deal win.

Deal wins in the Cloud and Infrastructure (CIS) business have been significant. TCV bookings is up 70% YoY, deal pipeline is up 125% YoY and deal win ratio has improved to 50%. Total reported TCV is ~186mn (~24% of Total TCV). Total addressable market for CIS is USD 184bn till FY22.

The company is also investing in building Digital capabilities, ~70% of the investment is going into innovation and strengthening the Return on Digital (RoD) platform. Zensar has 34 cloud applications, 650+ releases and 50+ business process solutions. Zensar has filed 28 patents in the last two years (zero two years back).

Digital revenue has grown at a CAGR of 25% over FY16-18 (organic 12%). Digital is 44.2% of revenue and has grown at an eight quarter CQGR of 8.3%.

Core revenue (ex-MVS and RoW) has grown at a CQGR of 4.4%, while Non-core has fallen at 1.9% CQGR over the last four quarters. Within core revenue, Digital CQGR is +8.8% and traditional revenue CQGR is +1.1%. EBITDA margin in the core business is 15% vs 13% for the company average.

Penetration if Digital in Top-strategic accounts is higher, which is

reflected from the growth in USD 5mn+ accounts (grew from 14 to 20 in the last one year).

The company is actively exploring to sell the MVS business (USD 30mn, ~5% of rev), which is loss making. This will boost margins and is expected to be completed in the next two quarters.

The slowdown in Cynosure (acquired in March-18) slowed down in the 2QFY19 quarter due to completion of some large projects. This is expected to ramp-up from 4QFY19 onwards.

There is near-term margin pressure due to higher lateral hiring, higher on-site component in new deals and increase in sub-contract expenses (17% of 2QFY17 revenue, +484 bps YoY).

We have a positive view on Zensar based on (1) Focus on Digital POC led sales, (2) Robust deal wins, and (3) Growth visibility in the core business. We build 12/18/16% Revenue/EBITDA/PAT CAGR over FY19-21E. The stock trades at a P/E of 14.5/12.3x FY19/20E earnings.

Zensar (CMP Rs 230, Mcap Rs 52bn, BUY, TP Rs 335)

Digitally transformed

YE March (Rs bn) FY17 FY18 FY19E FY20E FY21E

Net Revenue 30.73 31.16 39.37 45.31 50.78

EBITDA 3.85 3.73 5.45 6.70 7.61

APAT 2.34 2.41 3.63 4.28 4.90

Diluted EPS (Rs) 10.3 10.6 16.0 18.8 21.6

P/E (x) 22.3 21.6 14.4 12.2 10.6

EV / EBITDA (x) 12.4 12.7 8.7 6.7 5.6

RoE (%) 16.7 15.1 19.6 19.8 19.5

Source : Company, HDFC sec Inst Research

8

Technology and New Age Businesses

MCX was represented by Sanjay Wadhwa (CFO). Following are the key takeaways:

MCX volume has recovered strongly in 3QFY19 led by crude and bullion. Total ADTV is up 8.6% QoQ and 32.3% YoY, Bullion is up 7.7% QoQ while energy is up 42.5% QoQ.

Fall in crude prices will have an impact on volume growth, energy volume in Dec-18 is up only 4.4% MoM vs 17.5% MoM jump in Nov-18.

Regulatory tailwinds have helped in increasing the hedging activity in bullions. Gold open interest which used to be ~8tons has now crossed 15tons. This will result in higher trading volume in bullions.

There is no impact on traded volumes after the launch of commodities trading by BSE and NSE. In-fact, ADTV in 3QFY19 is the highest in the last 18 quarters, despite increased competition.

Based on the latest interactions with the members, MCX is not considering any cut in transactions charges. However if situation demands can consider a 10% cut in pricing. Currently MCX charges Rs 26/mn for futures which is ~37% higher than what NSE charges for futures trade.

Partnership with retail banks subsidiaries is a positive and can boost trading volumes by additional 10%. Axis Securities has already started commodity derivative trading for its retail clients. Other brokerages like ICICI Securities and SBI Caps will start commodity services soon.

MCX is also evaluating spot exchanges for Gold and Natural Gas as an additional line of business. The company is also investing in its

own trading platform and will not be dependent on 63moons for spot exchange technology.

LES for options stopped in Oct-18, which resulted in a fall in options ADTV (down 53% QoQ in 3QFY19). The company will start charging for options only when volume reaches ~10% of futures trading volume (currently it’s ~2.1%).

SEBI approval for institutional participation in commodity derivative trading is expected soon. MFs and PMS will be allowed to participate in commodity trading which can boost trading volume, but this will take at least a year to reflect in volumes.

We see value in MCX based on (1) Embedded non-linearity, (2) ADTV growth despite rising competition, (3) Cost discipline and (4) Net cash of Rs 14bn (~38% of Mcap). We estimate revenue/PAT CAGR of 16/19% over FY18-21E. The stock trades at a P/E of 27/24.5x FY19/20E EPS.

MCX (CMP Rs 733, Mcap Rs 37bn, BUY, TP Rs 1,025)

Gradual improvement in volumes

Source : Company, HDFC sec Inst Research

YE March (Rs mn) FY17 FY18 FY19E FY20E FY21E

Net Revenue 2,594 2,598 3,106 3,559 4,087

EBITDA 796 719 1,034 1,295 1,658

APAT 1,266 1,084 1,379 1,520 1,812

Diluted EPS (Rs) 24.9 21.3 27.1 29.9 35.6

P/E (x) 29.4 34.4 27.0 24.5 20.6

EV / EBITDA (x) 26.7 28.5 19.7 15.2 11.4

RoE (%) 9.5 7.9 10.0 10.8 12.5

9

Technology and New Age Businesses

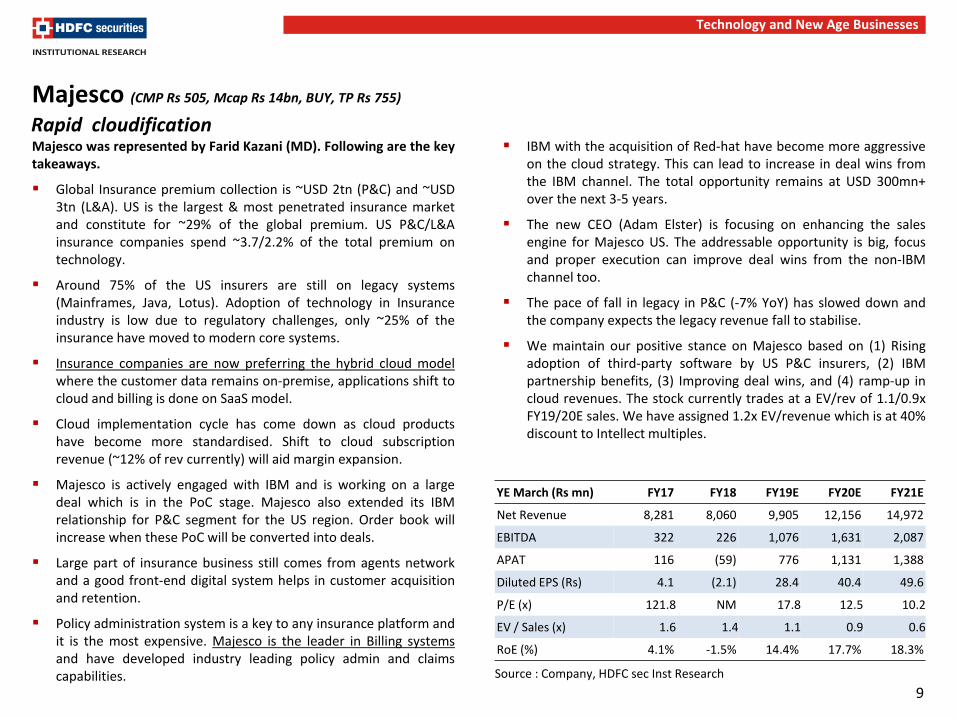

Majesco was represented by Farid Kazani (MD). Following are the key takeaways.

Global Insurance premium collection is ~USD 2tn (P&C) and ~USD 3tn (L&A). US is the largest & most penetrated insurance market and constitute for ~29% of the global premium. US P&C/L&A insurance companies spend ~3.7/2.2% of the total premium on technology.

Around 75% of the US insurers are still on legacy systems (Mainframes, Java, Lotus). Adoption of technology in Insurance industry is low due to regulatory challenges, only ~25% of the insurance have moved to modern core systems.

Insurance companies are now preferring the hybrid cloud model where the customer data remains on-premise, applications shift to cloud and billing is done on SaaS model.

Cloud implementation cycle has come down as cloud products have become more standardised. Shift to cloud subscription revenue (~12% of rev currently) will aid margin expansion.

Majesco is actively engaged with IBM and is working on a large deal which is in the PoC stage. Majesco also extended its IBM relationship for P&C segment for the US region. Order book will increase when these PoC will be converted into deals.

Large part of insurance business still comes from agents network and a good front-end digital system helps in customer acquisition and retention.

Policy administration system is a key to any insurance platform and it is the most expensive. Majesco is the leader in Billing systems and have developed industry leading policy admin and claims capabilities.

IBM with the acquisition of Red-hat have become more aggressive on the cloud strategy. This can lead to increase in deal wins from the IBM channel. The total opportunity remains at USD 300mn+ over the next 3-5 years.

The new CEO (Adam Elster) is focusing on enhancing the sales engine for Majesco US. The addressable opportunity is big, focus and proper execution can improve deal wins from the non-IBM channel too.

The pace of fall in legacy in P&C (-7% YoY) has slowed down and the company expects the legacy revenue fall to stabilise.

We maintain our positive stance on Majesco based on (1) Rising adoption of third-party software by US P&C insurers, (2) IBM partnership benefits, (3) Improving deal wins, and (4) ramp-up in cloud revenues. The stock currently trades at a EV/rev of 1.1/0.9x FY19/20E sales. We have assigned 1.2x EV/revenue which is at 40% discount to Intellect multiples.

Majesco (CMP Rs 505, Mcap Rs 14bn, BUY, TP Rs 755)

Rapid cloudification

YE March (Rs mn) FY17 FY18 FY19E FY20E FY21E

Net Revenue 8,281 8,060 9,905 12,156 14,972

EBITDA 322 226 1,076 1,631 2,087

APAT 116 (59) 776 1,131 1,388

Diluted EPS (Rs) 4.1 (2.1) 28.4 40.4 49.6

P/E (x) 121.8 NM 17.8 12.5 10.2

EV / Sales (x) 1.6 1.4 1.1 0.9 0.6

RoE (%) 4.1% -1.5% 14.4% 17.7% 18.3%

Source : Company, HDFC sec Inst Research

10

Technology and New Age Businesses

IBM was represented by financial services leader. Following are the key takeaways:

IBM is a leading global IT company (USD 80bn rev, USD 101bn MCap) headquartered in New York (part of DJIA-30), with operations in 170+ countries.

Indian IT & Automation

Cost arbitrage was a good pricing-lever for Indian IT companies earlier. However, automation is now gaining traction, Infrastructure management services being a prime example. T&M business is under severe threat with Automation driving greater efficiencies and cost saving supported by shorter development cycles of ‘bots’.

Digital Transformation

Enterprise clients are undertaking digital transformation only when they see disproportionate benefits such as protecting their business, introduction of a new business model or to mitigate cost pressure. IT services providers are no longer just interacting with CIOs, but also with other business heads (CXOs) in order to drive that change. IT service providers are required to change their methods of engagement with clients.

Business-mix of McKinsey, BCG, Deloitte etc. has changed and they now derive a larger chunk from analytics & IT consulting. Agile development of systems requires shift in work culture and people need to collaborate preferably at a single location. IBM is revamping millions of sq. ft of their offices to become ‘agile enabled’.

Initial windfall revenues in digital (first 15-20% of rev) is seen as enterprise clients are trying to experiment with some digital initiatives and also due to some reclassification of activities having AI/ML component, as digital.

Going from 20% digital to >50% digital requires cultural change, realignment & re-skilling of people. Re-skilling of people is a tough challenge and growth in digital can moderate to 17 to 20%.

Cloud Migration

Traditionally, financial services have not been too keen to go on cloud. IBM is pitching for a hybrid solution in which the core systems will be on-premise and peripherals can be on cloud. Core to non-core data assets ratio is currently at ~80:20. There is also good traction in private cloud as banks don’t want their sensitive data to go off-premise.

IBM (IT Products & Services)

Future is hybrid

11

Technology and New Age Businesses

Capgemini was represented by a Banking & Capital markets leader and an APAC Capital markets leader. Following are the key takeaways:

Capgemini is a leading global IT services company (EUR 13bn/USD 15.5bn rev, 12% EBIT, EUR 14bn M-cap) with headcount of 210,000 (57% in global delivery). Key verticals are BFSI (27%), Mfg, Auto & Life-science (22%), CPG & Retail (18%), Public sector (14%) and E&U and Chemicals (11%). Geographies composition at NorthAm (33% incl. former iGate), France (21%) and Rest of Europe (39%).

Growth Geographies

APAC is the fastest growing market, within APAC Japan, Australia, China & India are outperforming.

Insurance is driving growth in Japan, Australia & China. Banking is driving growth in India.

Growth in European Banks is driven by compliance requirements.

Digital Transformation

Similar trends are seen in banks across US, Europe and Australia with large budgets on simplification of the IT architecture. US banks are using the capabilities of core and are building Digital assets in the peripheral systems around the core. Over a period of time these core systems have become very complex & altering them is an expensive and time consuming proposition. There is huge amount of movement to cloud with Core assets to private cloud and non-core to public cloud.

Digital has better profitability as billing rates are higher due to differential skill sets required to execute. Over a period of time with availability of digital skill sets, bill rates are not expected to improve significantly and profitability may reduce. Digital development and testing happens offshore, an onsite-offshore effort-mix ratio of ~30:70 is fair to assume as compared to ~10:90 for legacy projects.

Digital initiatives are driven by a lot of niche companies, which don’t have scale. Enterprise clients are not comfortable working with smaller niche companies for longer duration digital initiatives.

There is large spend in AI & Analytics in risk & compliance within capital market segment. TCS and Wipro are strong Indian players in BFSI digital space.

Legacy IT, In-sourcing and Automation

Pricing structure is changing for legacy IT projects, billing hours have a decreasing trend with automation & efficiencies bringing down the required hours.

While deal value is high, the profitability of the deals is reducing. Tier-1 bank are hard negotiators, profitability is better in Tier-2 & Tier-3 banks.

Banks are increasing in-sourcing in areas which are legacy and stable and not in dynamic areas in which technology change is fast. Banks are also implementing RPA to make operations leaner and to remove manual interventions.

Capgemini (IT Services)

Shift to larger vendors

12

Technology and New Age Businesses

Core Banking Solutions

US banking systems are fragmented. CBS is solely used for transaction banking system, other areas like Corporate, Trade, On-boarding etc. have separate systems.

Temenos is aggressively capturing CBS market, they have a dominant position in Europe and they are also working in South America, Mexico, Brazil & Australia.

No significant traction in CBS business for Oracle Financial services in APAC impacted by weak partner ecosystem. In Europe, Oracle Financial services is doing well but market leader in that segment-geography is Temenos.

TCS’ BaNCS & Infosys’ Finacle are also competing with Oracle in CBS space. China CBS market is dominated by TCS BaNCS & Indian CBS market is dominated by Finacle.

Employees & Sub-contracting

Capgemini’s fresher salaries are higher than that of Indian IT companies and in the trailing year, there is an increase in fresher salaries. Capgemini is hiring a lot of freshers and deploying them on accounts (unbilled), Indian companies also following a similar model. For traditional work, lower bench strength is maintained and excess demand is fulfilled through sub-contracting.

Capgemini (IT Services)

Contd…

13

Technology and New Age Businesses

NASSCOM was represented by Deputy Director (Research). Following are the key takeaways:

Industry Overview

NASSCOM is a not-for-profit industry association. It is the apex body for USD 167 bn IT BPM industry in India. 2200+ members at NASSCOM constitute ~90% of the industry’s revenue.

As an industry, IT services, BPM and ER&D have become very crucial to the Indian economy accounting for 7.9% share of GDP & 45% share in total services export. Industry is expected to grow at 7-9% in FY19. IT services exports contributed USD 69bn.

Fastest growing verticals are BFSI, Retail (Omni channel & hyper-personalization), Manufacturing (smart factories, products & services), and Healthcare (Patient facing technology like robotics).

Offshoring in ER&D space either through GCCs (Global capability centers in ER&D) or through vendors is increasing which was not the case earlier. There is greater competition from captives for ER&D vendors with preference to safeguard their IPs.

Concerns over outcome of Brexit hover around UK geography but IT companies have not highlighted any concerns, yet.

Digital Transformation

NASSCOM expects digital technologies to grow by ~25% CAGR. They expect digital technologies to contribute ~38% to total revenue by 2025 (currently at 20-24%).

Hiring Trends

Hiring trends for Indian IT companies are strong for the past two quarters with revival in fresher hiring. Local hiring in USA is strong along with opening of local deliver centers. Indian IT has hired ~170,000 locals in the past 2-3 years in USA across California, Minnesota, Washington, North Carolina, Illinois, etc.

Skilling is an important focus area for NASSCOM, it includes re-skilling existing workforce & skilling the future workforce supported by partnering with academia.

NASSCOM (IT Industry Association)

‘All is well’

14

Technology and New Age Businesses

UiPath was represented by a senior sales director. Following are the key takeaways:

Overview

UiPath is a global software company headquartered in New York and among leading Robotic Process Automation (RPA) provider.

UiPath has 2,000+ customers across 16-17 countries. Large global customers include GE, Unilever, HP Inc, NASA (referral customer), US Fed Govt. In India, UiPath has 100+ clients in production stage. Services opportunity is 2-3x in India and is higher globally.

UiPath has raised ~USD 440mn capital till date. Investors include CapitalG, Accel Partners, Earlybird, Sequoia etc. Annual recurring revenue for TTM is ~USD 150mn (Competitors: Automation Anywhere and Blue Prism are at USD 150/100mn rev) and the company is valued at ~USD 3bn.

Blueprism does not have a strong India strategy however it’s very strong in Europe geography. Automation Anywhere is the biggest competitor for UiPath. In India, IBM and TCS are moving from Blueprism to UiPath.

The employee base has expanded from 470 in Feb-18 to ~1,600 Nov-18. They have 200+ people in India working in product development, product support, sales, pre-sales, back office functions etc.

TCS and Infosys are largely consuming bots for their BPO business. RPA is only a part of Wipro Holmes and UiPath’s RPA has wider acceptance as compared to Infosys’ RPA tools.

Verticals, Geographies & Offerings

Financial services & Manufacturing are key verticals. Apart from

key verticals they also operate in E-commerce, Telecom, Media, Pharma, Energy etc. There is also traction in US Government sector.

America & Europe lead the revenue share followed by Asia. In Asia, Japan is a fairly large market.

Licensing is on subscription basis, UiPath charges per bot and UiPath’s ability to integrate with all AI/ML engines stands out. Front office automation is also a key differentiator for the company.

In banking vertical, activities which are generally automated are business processes. In the non-banking vertical, automated activities are largely finance & accounts processes.

Partners & Ecosystem

UiPath partners with EY, KPMG, Deloitte, PwC, among SIs they partner with TCS, Cognizant, Capgemini, KPIT, Mastek, etc.

UiPath has created training academy and they have built a community edition of their tools. They have developed fairly large community of RPA developers. They provide multiple certifications and have created a developer marketplace.

Use Cases

Sumitomo Mitsui Banking Corporation (SMBC) saved 0.4mn hours annually across 200 operations. They have deployed 1,000+ bots and have deployed a large number of bots in risk & compliance process as well as multiple bots deployed in front office.

For a Media company, UiPath has automated advertisement slot booking process. Requests for slots comes from standard agencies in email, per slot rates are fixed. The bot picks up the information from email, puts it in spreadsheet and does the slotting.

UiPath (IT Products)

‘BOT’ify

15

Technology and New Age Businesses

Infor was represented by consulting leader. Following are the key takeaways:

Overview

Infor is an unlisted IT product company (USD 3bn rev) based out of US and headquartered in New York.

Infor provides cloud based ERP software for multiple Industries and they partner with AWS for cloud infrastructure. The company has a large support center in Hyderabad with ~3,000 people and has presence in 170 countries.

Revenue segments

~80% of the top line comes from manufacturing sector including Aerospace, Defense, Automotive etc. ~35% YoY growth on cloud, on-premise offerings are shrinking. Geographical split is USA ~45%; APAC ~16-20%.

Moving from an on-premise model to a cloud-model is moving from licensing-based to subscription-based revenue model, which hurts in the short term, unless it’s backfilled by sufficient number of customers to set off the dip in license revenue.

Offerings

SMAC (social, mobile, analytics and cloud) is central to the offerings. IoT is a big opportunity and Infor believes that they are well positioned for it as they are cloud-based, which is suitable for data heavy IoT.

Infor has multiple ERPs across industries. They have put in ~250 skills on their applications using AI. They provide zero cost integration between two or more of Infor’s products. Implementations are majorly outsourced, Infor partners with SIs like TCS, HCL Tech for implementation.

The company has a cloud based analytics tool ‘Birst’, which is designed to handle multiple sources of data in huge amount and then presenting it. Their platform ‘GT Nexus’ (2018 Gartner Magic Quadrant Leader for Multi-enterprise Supply Chain Business Networks) has Nike as customer.

Industry Overview

Recently Infor has seen a lot of demand for digital transformation which is more consulting-based. Every enterprise is sitting on multiple applications and they are trying to make a unified sense of the architecture. Automation technology is seeing a lot of traction and is growing rapidly.

Infor (IT Products)

On-prem to cloud transition

16

Technology and New Age Businesses

The bank was represented by Digital & cloud transformation leader. Following are the key takeaways:

Captive centers in India are comparable to that in the US in terms of technology and quality of resource. A lot of work related to front-end development, core processes and R&D work is being shifted to captives.

Banks are gradually becoming Tech driven enterprises. Huge pressure is there from Fin-tech and barriers to entry are reducing due to low cost and availability of Technology.

Investments are moving from turnkey projects to custom projects to build intelligent systems.

Most of the current vendors are not going to vanish but the requirements are going to change drastically (much beyond staff augmentation).

There is heavy focus on automation & disruptive technologies like AI, ML. Human to machine ratio is going to reduce over time.

Legacy IT spending will follow a gradual decline path. At the system level legacy fall can be 3-5% YoY. There is not going to be a steep fall in legacy spending at least for the next five years. However, post that legacy spend would dry up a lot faster than current level.

A longer duration outsourcing would require a larger and reliable IT vendor as a risk management process.

Large US Bank (Enterprise Buyer)

Captive accelerator 1

17

Technology and New Age Businesses

The bank was represented by senior technology leader. Following are the key takeaways:

In-sourcing activity in BFSI has increased in the last 2 years, primarily due to (1) Lack of high quality resources at the vendor end, (2) Risk of outsourcing core applications and IPs which have become critical in a hyper competitive environment, (3) Rupee depreciation has made the economics better, (4) Low cost availability of technologies like cloud and automation and, (5) Change in CIO at the bank-end can led to change in stance.

Applications which are closer to core business activity are transferred to captives while repetitive processes and large development projects which require upfront investment are still being outsourced.

Most of the critical work is moving to captives in Eastern Europe, Ireland and India. Also a lot of hiring is done from IT vendors at ~20-25% higher cost. This has resulted in higher attrition for Tier-1 IT vendors.

Indian IT companies were mostly known for handling legacy systems and datacenters but now have become capable of doing large Digital transformational projects.

In financial services industry regulation plays an important role, it

does not allow shift of customer data to public cloud. The non-sensitive information can go on public cloud but with riders. Banks are actively looking for a Hybrid cloud solution where all the data sits on-premise and the application shifts to cloud. This is where the spend is going to be in the next five years.

Increased competition from Fintech has forced large banks to adopt newer technologies. Indian IT players have been a key partner in setting-up and maintaining legacy systems but are now capable of delivering new-age Digital technologies. Companies who have handled the legacy systems for long are better equipped to handle the Digital transformation journey for a large enterprise.

Recent trends include increased use of Automation, especially in area of testing which have large teams deployed. Automation is not just for cost saving but also offers better efficiencies.

The recent visa issues are not being addressed by offshoring, however by increasing use of automation.

Quality of work-force is better onsite vs offshore, as onsite involves rigorous selection process led by clients.

Lot of companies from Eastern Europe (Luxoft), Accenture, IBM, Deloitte etc. are generally deployed for high end projects & shorter assignments onsite.

Large European Bank (Enterprise Buyer)

Captive accelerator 2

18

Technology and New Age Businesses

Disclosure: We, Apurva Prasad, MBA, Amit Chandra, MBA & Akshay Ramnani, CA, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. Research Analyst or his/her relative or HDFC Securities Ltd. does not have any financial interest in the subject company. Also Research Analyst or his relative or HDFC Securities Ltd. or its Associate may have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the Research Report. Further Research Analyst or his relative or HDFC Securities Ltd. or its associate does not have any material conflict of interest. Any holding in stock – Yes Disclaimer: This report has been prepared by HDFC Securities Ltd and is meant for sole use by the recipient and not for circulation. The information and opinions contained herein have been compiled or arrived at, based upon information obtained in good faith from sources believed to be reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. This document is for information purposes only. Descriptions of any company or companies or their securities mentioned herein are not intended to be complete and this document is not, and should not be construed as an offer or solicitation of an offer, to buy or sell any securities or other financial instruments. This report is not directed to, or intended for display, downloading, printing, reproducing or for distribution to or use by, any person or entity who is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction, availability or use would be contrary to law or regulation or what would subject HDFC Securities Ltd or its affiliates to any registration or licensing requirement within such jurisdiction. If this report is inadvertently send or has reached any individual in such country, especially, USA, the same may be ignored and brought to the attention of the sender. This document may not be reproduced, distributed or published for any purposes without prior written approval of HDFC Securities Ltd . Foreign currencies denominated securities, wherever mentioned, are subject to exchange rate fluctuations, which could have an adverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively assume currency risk. It should not be considered to be taken as an offer to sell or a solicitation to buy any security. HDFC Securities Ltd may from time to time solicit from, or perform broking, or other services for, any company mentioned in this mail and/or its attachments. HDFC Securities and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of the company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to any recommendation and other related information and opinions. HDFC Securities Ltd, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates, diminution in the NAVs, reduction in the dividend or income, etc. HDFC Securities Ltd and other group companies, its directors, associates, employees may have various positions in any of the stocks, securities and financial instruments dealt in the report, or may make sell or purchase or other deals in these securities from time to time or may deal in other securities of the companies / organizations described in this report. HDFC Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months. HDFC Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction in the normal course of business. HDFC Securities or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither HDFC Securities nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. HDFC Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the subject company or third party in connection with the Research Report. HDFC Securities Ltd. is a SEBI Registered Research Analyst having registration no. INH000002475.

19

Technology and New Age Businesses

HDFC securities Institutional Equities Unit No. 1602, 16th Floor, Tower A, Peninsula Business Park, Senapati Bapat Marg, Lower Parel, Mumbai - 400 013 Board : +91-22-6171 7330 www.hdfcsec.com