india telecom infrastructure: constratints and opportunities

TRANSCRIPT

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 1/21

I

C

DIA TONSTR

A

LECO

INTS

it Morya

INFRAND OP

STRUC

PORTU

URE: TNITIES HE

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 2/21

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 3/21

3

EXECUTIVE SUMMARY India is the third largest in terms of subscriber base and number one in terms of mobile

growth. It has overtaken China in terms of subscriber acquisition and is adding around 6-

7 mn lines every month. Adding to it, several compelling economic, demographic and

social factors are also likely to fuel subscriber growth in the country. The high average

real GDP growth of 8% in each of the last three years; a large young, working population

(65% below 35 years by 2011); a fast-growing and progressively richer middle class; and

a huge disparity in affordability of wireless services vs actual mobile penetration, are all

pointers to the potential demand in the pipeline.

But we still have a long way to go, as vast geography is still not covered. Right now,

cellular telecom service providers are present in more than 5,000 towns and cities andone lakh plus villages across the country. In terms of tele-density there is a wide gap-with

metros at around 40 and rural areas at 2.5. Indian market is also unique as it has the

lowest call tariff in the world, lowest ARPU, and highest minutes of usage.

While the economic and demographic environment in India are conducive to strong

subscriber growth in the coming years, there are three industry-related factors that could

present a challenge to operators either in terms of subscriber growth or profitability at the

cost of growth or both. These factors are: affordability of handsets, high upfront cost of

setting up of own telecom infrastructure in new geographies and shortage of 2G

spectrum.

However, like every cloud has a sliver lining; these constraints forced the telecom

industry to become operationally more efficient and profitable by evolving new business

models like infrastructure sharing and outsourcing of network. These challenges

channelized the energy of telecom service providers in identifying probable technological

solutions and utilizing the other vast established infrastructures (like power lines) to reach

the end customers.

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 4/21

4

1. INTRODUCTION Indian telecom market has seen an explosive growth in last five years and Indian market

with 180 million connections has emerged as one of the largest in the world and the

second largest telecom market of Asia. Indian telecom market offer huge headroom for

growth with teledensity at 18 % till now.

Figure 1: Region-wise Mobile Subscriber Base

Source: COAI, AUSPI, 2007

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 5/21

5

Source: COAI, Voice&Data, October 2006

India has the lowest mobile penetration among the top 50 developed and emerging

markets of the world and has a lower wireless spend to GDP ratio than other emerging

markets, confirming the huge latent growth potential.

Source: COAI, Voice&Data, October 2006

Indian telecom market present different set of opportunities and challenges to telecomoperators and low ARPU, High capital efficiency, low handset prices, vast geographic

market, and High prepaid user share are the typical characteristics of the market.

Revenue growth20

15

1110

9

0

5

10

15

20

2002 2003 2004 2005 2006

$ B i l l i o

CAGR

Subscriber growth164

98

76

5344

0

60

120

180

2002 2003 2004 2005 Aug-06

CAGR

Figure 3: Revenue Growth in Indian Telecom Market

Figure 2: Subscriber Growth in Indian Telecom Market

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 6/21

6

1. CURRENT STATE OF TELECOM INFRASTRUCTURE On the rural spread, India has a total of 638,499 villages out of which about 44,856

villages are uninhabited as per 2001 census. So, 594,000 inhabited villages account for

72.22% of the total population of India. Till date, we have covered only 60% of India's

geography, and a large part of rural geography is yet to be covered. Infrastructure support

for mobile services will act as a catalyst for rural growth. Even in the past, the

government has provided a lot of support to rural people by deploying MARR (multi

access rural radio), and VPT (village public telephones). Presently, around 559,000

villages have VPT, and for the remaining 35,000 villages, VPT are to be set up either on

satellite or on other technologies. The USO initiative of providing mobile services will

help in increasing mobile footprint in rural areas, as till date communication in majority

of the villages has been possible only through community phones i.e. VPT or wireline

phones.

Table 1: Wireless Coverage- Current Status

Area Total No of Towns/

Villages in India

Cellular Coverage

No of

Towns/Villages

Percentage

Urban India 5,151 4,900 95

Rural India 607,000 350,000 57

Source: COAI, Macquarie Research, August 2006

Presently, 80% of the towers are located in urban areas, and remaining 20% are in rural

India. We are seeing a shift, and it is expected that in couple of years it would be 60% in

urban, and 40% in rural areas, as 70% of the population resides there, and a lot of

coverage is yet to happen. Indian teledensity is at around 19%. Out of this, urban

teledensity is at around 49.53%, and rural teledensity is at around 1.84%. There is a wide

gap between urban and rural teledensity, and the digital divide needs to be bridged. The

latest initiative of DoT will help in covering around 22% of India's population, thereby

providing mobile connections to people residing in remote and far-flung areas.

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 7/21

7

Table 2: Wireless Network Infrastructure in India

Year ‐end

December

Base

Stations

Base Station

Controllers

Mobile Switching

Centres

2001 3,636 169 57

2002 6,322 227 76

2003

10,273 273 86

2004 18,643 456 120

2005 35,165 681 169

2006 *70,000 Source: COAI, Macquarie Research, August 2006

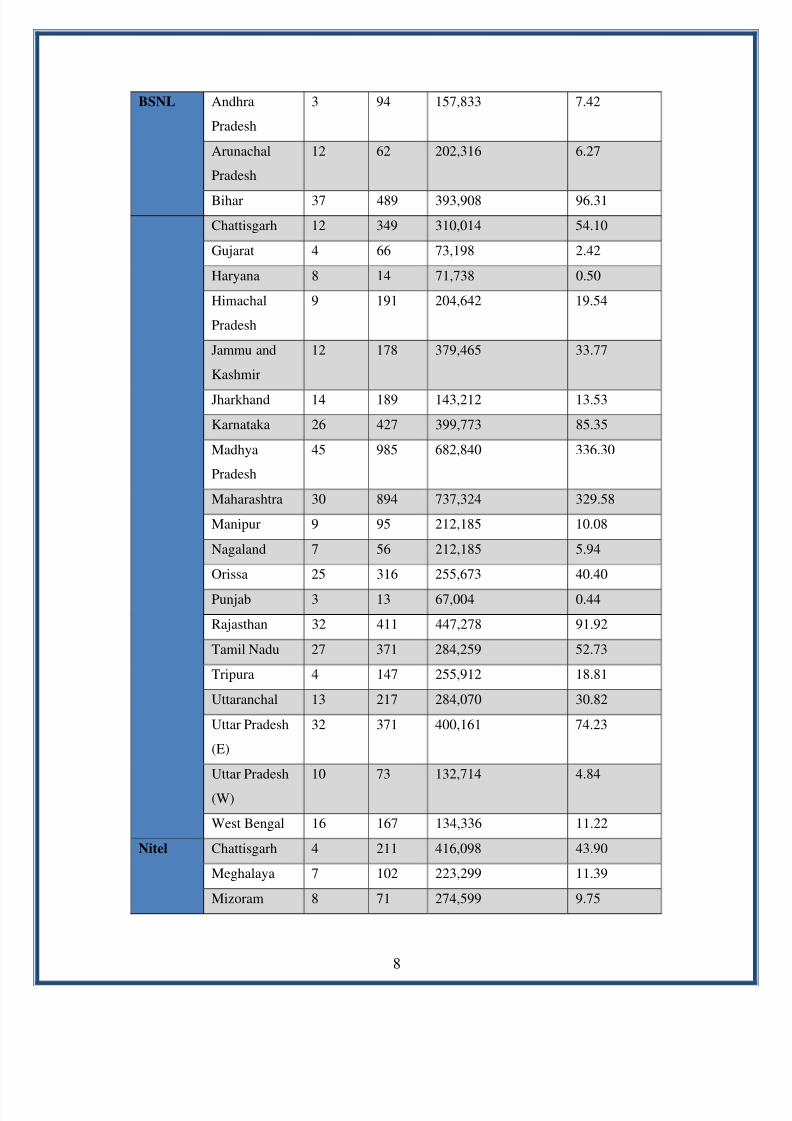

DoT is planning to set up 7,871 mobile towers across 212,034 villages, covering a 270

mn rural population under the USO initiative. In the latest bid, companies like BSNL,

GIL, Hutchison Essar, Nitel, Quipo, and Reliance Comm infrastructure will set up 7,871

mobile towers in around 500 districts across India and would initially provide voice

services. The tower companies will be provided remuneration on a quarterly basis for a

period of five years from USO fund.

Table 3: Expected Investment in Infrastructure under USO

Financial Bid Results for Part of USO

Company State Districts Towers USO

Amount/Tower/Year

(in Rs)

USO

Amount in 5

Years

(in Rs

Crore)

GTL

Infra

Andhra

Pradesh

14 287 592,196 84.98

Assam 20 90 265,066 11.93

Uttar Pradesh

(E)

13 134 141,333 9.47

Hutch

Essar

Andhra

Pradesh

5 200 388,081 38.81

Maharashtra 3 123 197,331 12.14

Sikkim 3 8 162,321 0.65

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 8/21

8

BSNL Andhra

Pradesh

3 94 157,833 7.42

Arunachal

Pradesh

12 62 202,316 6.27

Bihar 37 489 393,908 96.31

Chattisgarh 12 349 310,014 54.10

Gujarat 4 66 73,198 2.42

Haryana 8 14 71,738 0.50

Himachal

Pradesh

9 191 204,642 19.54

Jammu and

Kashmir

12 178 379,465 33.77

Jharkhand 14 189 143,212 13.53

Karnataka 26 427 399,773 85.35

Madhya

Pradesh

45 985 682,840 336.30

Maharashtra 30 894 737,324 329.58

Manipur 9 95 212,185 10.08

Nagaland 7 56 212,185 5.94

Orissa 25 316 255,673 40.40

Punjab 3 13 67,004 0.44

Rajasthan 32 411 447,278 91.92

Tamil Nadu 27 371 284,259 52.73

Tripura 4 147 255,912 18.81

Uttaranchal 13 217 284,070 30.82

Uttar Pradesh

(E)

32 371 400,161 74.23

Uttar Pradesh

(W)

10 73 132,714 4.84

West Bengal 16 167 134,336 11.22

Nitel Chattisgarh 4 211 416,098 43.90

Meghalaya 7 102 223,299 11.39

Mizoram 8 71 274,599 9.75

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 9/21

9

Reliance

Comm

Infra

Himachal

Pradesh

2 104 156,480 8.14

Jharkhand 4 116 159,000 9.22

Kerala 11 46 98,700 2.27

Orissa 5 116 159,000 9.22

Quipo Uttar Pradesh

(W)

11 88 100,000 4.40

Total 500 7,871 9,775,544 1582.78

Source: Voice&Data, September 2006

3. TRENDS IN TELECOM INFRASTRUCTURE SPACE 3.1Wireline

According to Research and Markets, the dynamics of wireline service are changing and

these fastest changes in the market dynamics also create new revenue opportunities for

service providers, including managed services, IP telephony, as well as QoS and SLA

offerings. To take advantage of these opportunities, service providers will need to either

acquire resources to provide a wide range of services in order to avoid reliance upon

shrinking individual service silos, or develop strategic relationships and partnerships.

According to infrastructure service providers, the main trends are follows:

Change in technology platform-xDSL

Tough competition from OEMs with bundling of product solutions and services

Price erosion

Consolidation of services-voice, data and video convergence

3.1.1 Demands from operators Cost efficient network up gradation solutions

Looking for lowering Capex and Opex

Higher revenues per subscriber

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 10/21

10

3.2 Wireless Consolidation is already taking place in the world in the wireless infrastructure space.

Because of consolidation, major wireless infrastructure players will look at their business

model (following the consolidation) and their manpower base and this will lead intorestructuring globally. This may not be an indication of a slowdown, but their strategy for

pruning costs and improving productivity will see realignment in business.

However, technology will drive the market growth. New innovations will continue as the

entire global telecommunication market is yet to be tapped and there is enough room for

growth, but some geography throws some tough hurdles. In this case, wireless telecom

service providers and infrastructure companies will have to work together to offer

customized solutions.

3.3 Demands from operators Telecom operators are looking at curtailing project implementation costs. This can be via

sharing passive infrastructure and selecting one prime vendor to undertake the end-to-end

implementation. Operators are looking for solutions that provide them with

lower Opex and also help them in generating higher ARPUs and taking leadership.

Spectrum allocation by the government is a main concern among operators as well asinfrastructure providers. Another concern for infrastructure providers are dropping prices.

4. CONSTRAINTS AND OPPORTUNITIES

4.1 Constraints

4.1.1 Inadequate Infrastructure The growth of telecom service providers is directly connected with the reach of their

network. In terms of market share, growth of service providers is dependent upon there

ability to tap rural subscribers. However, till date 43% of Indian villages lack telecom

network. It is very costly proposition for telecom service providers to install their own

infrastructure in rural areas. Also, due to low population density, high operational cost of

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 11/21

11

infrastructure and low per capita income (leads to low ARPU) of villagers, it seems to be

operationally expensive too for service providers to operate in rural areas.

4.1.2 High OpEx Another major issue which is acting as the bottleneck in the growth of telecom is the high

operational and maintenance cost of network. One of the major contributor in the

operational cost of telecom network is the high cost of infrastructure like electricity, land

and human resources.

4.1.3 Insufficient Spectrum Additionally, in order to achieve a sustainable growth, adequate spectrum is required.

The available bands for GSM spectrum are 900 Mhz and 1,800 Mhz. As of today, the 900

Mhz band has been fully utilized and the 1,800 Mhz band has miniscule availability.

Therefore, government initiative is required to sort out this problem to support the growth

of telecom in India.

Figure 4: Spectrum Map of India

Source: TRAI, Macquarie Research, August 2006

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 12/21

12

Source: Source: TRAI, Macquarie Research, August 2006

4.2 Constraints or Opportunities? Every constraint store bags of opportunities for service providers, telecom equipment

manufactures and newly entrant telecom infrastructure companies. The only requirement

to harness the potential of Indian telecom market lies in innovating at business as well as

at technical front. Some of the business opportunities and solutions are explained in the

following sub-sections.

4.2.1 Telecom Infrastructure Sharing Infrastructure sharing has been used by operators to get rid of their non-core activities, so

that they can focus on their core business. Not only does it help in reduction of capex as

well as opex, it also helps in reducing management bandwidth for non-core activities as

the operation is now taken up by IP-1 players. And the IP-1 company charges a monthly

fee from the operator, which includes infrastructure usage and operations and

maintenance charges on a monthly basis.

Till March 2007, there were around 100,000-120,000 towers in India of which around 15-

18% were shared. Over the next two years, all operators put together will add around

160,000-170,000 towers; even if 35% of these are shared, one is looking at 56,000-

59,500 sites. Site sharing is not only limited to mobile, IP-1 players can target users in

wireless broadband, broadcasting, DTH, FM radios and WiMax operators.

Table 4: GSM spectrum requirement in Metros and A Circles by March 2008

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 13/21

13

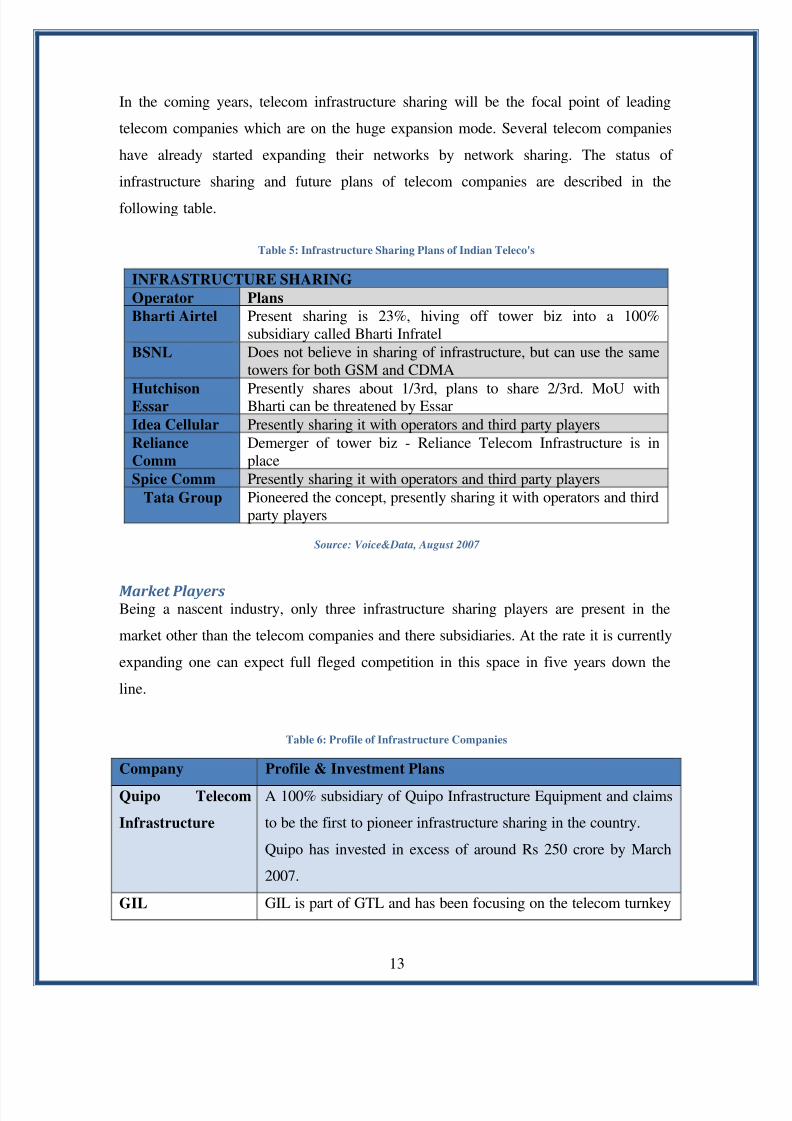

In the coming years, telecom infrastructure sharing will be the focal point of leading

telecom companies which are on the huge expansion mode. Several telecom companies

have already started expanding their networks by network sharing. The status of

infrastructure sharing and future plans of telecom companies are described in the

following table.

Table 5: Infrastructure Sharing Plans of Indian Teleco's

INFRASTRUCTURE SHARING

Operator Plans

Bharti Airtel Present sharing is 23%, hiving off tower biz into a 100%

subsidiary called Bharti Infratel

BSNL Does not believe in sharing of infrastructure, but can use the same

towers for both GSM and CDMA

HutchisonEssar

Presently shares about 1/3rd, plans to share 2/3rd. MoU withBharti can be threatened by Essar

Idea Cellular Presently sharing it with operators and third party players

Reliance

Comm

Demerger of tower biz - Reliance Telecom Infrastructure is in

place

Spice Comm Presently sharing it with operators and third party players

Tata Group Pioneered the concept, presently sharing it with operators and third

party players

Source: Voice&Data, August 2007

Market Players Being a nascent industry, only three infrastructure sharing players are present in the

market other than the telecom companies and there subsidiaries. At the rate it is currently

expanding one can expect full fleged competition in this space in five years down the

line.

Table 6: Profile of Infrastructure Companies

Company Profile & Investment Plans

Quipo Telecom

Infrastructure

A 100% subsidiary of Quipo Infrastructure Equipment and claims

to be the first to pioneer infrastructure sharing in the country.

Quipo has invested in excess of around Rs 250 crore by March

2007.

GIL GIL is part of GTL and has been focusing on the telecom turnkey

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 14/21

14

space for a long time. GIL has an experience of executing 16,000

sites connecting 16 mn subscribers

GIL has invested around Rs 1,000 crore and plans are on to invest

Rs 2,030 crore by March 2008.

Essar Telecom

infrastructure

It is a year old company and plans to leverage on telecom

activities of the Essar Group.

Essar has invested around Rs 150-200 crore and is planning for a

further investment of Rs 1,200 crore by March 2008

Source: Voice&Data, August 2007

The Innovation Mantra in infrastructure sharing In order to reduce Capex and Opex, tower subsidiaries and IP-1 players should focus on a

lot of innovation activities including site design, shelter design, power management, useof non-conventional energy, and others as in the coming days telecom players will have

to grapple with a lot of engineering, business and technology complexities as and when

they talk about coexistence of 2G, 3G, and WiMax under the same roof.

Figure 5: Infrastructure Sharing: Opportunities and Challenges

Opportunities Challenges

Huge numbers are throwing up new opportunities for IP-

1 and tower subsidiaries

Is the market big enough to accommodate more than a dozen

players?There is a vast rural opportunity which needs to be

tapped by the operator as we are presently covering only

60-65% geography

Tower subsidiaries and IP-1 players will have to focus on

significant reduction of Capex and Opex

Lowering of Capex and Opex will help operators to

focus more on marketing and customer services thereby

outsourcing towers to infrastructure players

Tower subsidiaries and IP-1 players have to share towers

with as many players as possible to keep rentals significantly

lower

A pan-India presence will provide a lot of cost

advantages vis-à-vis localized presence

Tower subsidiaries will face problems since mobile

operators will not be comfortable sharing their business plan,

and finally towers

Apart from organic growth, IP-1 players are also looking

at inorganic growth

IP-1 players should constantly focus on quality of service

and cost reduction

An open player policy in the mobile space will lead to

more players resulting in more sharing

DoT is yet to give a final go ahead on backhaul sharing

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 15/21

15

The players also should do a lot of balancing to provide error-free service in both urban

and rural areas. In urban areas, the focus would be more on providing interference-free

service irrespective of technologies. Whereas in rural areas, the focus would be more on

providing increased coverage. So the players will focus on design, power management,

and shelters, and this will decide who will top the table. For cost reduction, telecom

companies should focus on optimum design for multiple users and cost reduction on the

power front.

4.2.2 Operation and Maintenance Outsourcing O&M outsourcing is a business model, under which telecom carriers, enterprises or

institutions outsource the tasks of maintenance and management related to their telecom

networks, mainframe systems, and service platforms to professional outsourcing service

providers. The execution of O&M outsourcing is divided into three categories:

• Outsource to single service provider

Figure 6: Outsource to single service provider

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 16/21

16

• Outsource to Multiple Service Providers

Figure 7: Outsource to Multiple to Service Providers

• Outsource to Outsource to service provider offering secondary vendor

managementFigure 8: Outsource to Multiple Service Providers

Source: O&M Outsourcing, http://www.huwai.com

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 17/21

17

O&M outsourcing will help Indian teleco’s lower their cost and increase their core

competence.

4.2.3 BPL (Broadband over Power Lines) In the Indian scenario BPL can be used by the wire line service providers to increase

penetration of telecom network and reduce operational expenditure.

Defining BPL Broadband over Power Line (BPL) is a technology that allows Internet data to be

transmitted over utility power lines. In order to make use of BPL, subscribers are not

dependent on a phone, cable or a satellite connection. Instead, a subscriber installs a

modem that plugs into

an ordinary wall outlet

and pays a subscription

fee similar to those paid

for other types of

Internet service.

BPL works bymodulating high-

frequency radio waves

with the digital signals

from the Internet. These

radio waves are fed into

the utility grid at

specific points. They

travel along the wires

and pass through the

utility transformers to

subscribers' homes and businesses. Wires and sockets are used simultaneously for

electricity and data transmission, without causing disruption to either

Figure 9: Working of BPL

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 18/21

18

Global Experience in BPL Broadband over power lines has already made its presence in the United States and the

Europe. This has significantly reduced the overall wireless infrastructure cost for telecom

companies in these regions.

BPL in India & Add on features India offers huge opportunity in terms of broadband over power lines implementation.

Sooner or later, transferring voice and data through power lines will be a reality in India

as well.BPL technology can also be used for smart grid application control using data

transfer over an existing electric grid, and improving their control of energy reserves.

It can detect real-time theft detection, Detection of any malfunctions or service

distribution disorders, alert on misuse of any utility service, real-time power usage

detection. Security and surveillance issues can also be handled by this technology by

placing audio and video devices at strategic point and transferring the data through power

lines

Various Challenges in BPL implementation in India The biggest challenge for wide scale use of this technology is the opposition from users

of the same spectrum. They fear interference from BPL in their radio signal. In both

access and in-house high-speed BPL technologies, multiple carriers spread signals over a

broad range of frequencies that are used by other services.

This spectrum is also used for public safety and law enforcement, and government

aeronautical radio navigation and radio navigation satellite. Each of these authorized

services in the spectrum can get harmful interference. The close proximity of access BPL

equipment on utility poles may affect the operation of cable television service and high-

speed digital transmission service, such as DSL.

4.2.3 Green Solution for Wireless Infrastructure Development In the present Indian scenario we propose Green solution for the improvement in the

wireless infrastructure in India.

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 19/21

19

Defining Green Solution This 'green' solution provides a feasible and efficient alternative to using fuel generators

when a main grid connection is not available or it will take months or years to connect or

finally, where electricity tariffs are expected to rise sharply in the next few years.

Once installed, the cost of power is almost zero, and wind and solar powered cell sites

require minimal maintenance unlike a diesel driven generator which generally requires, at

a minimum, a monthly visit for refueling and they can also be heavily prone to theft. This

translates into added savings in operating expenditure (OPEX), a key factor to emerging

market network operators.

Global Experience on Green solution Motorola has implemented wind and solar solution at an operational MTC Namibia cell

site where the solution has become the electrical power source for the site to help telecom

infrastructure.

Telecom companies are

framing strategies to

produce portions of the

Reach GSM equipment

locally in order to

provide low-cost

solutions for rural and

urban cell site

deployments. As part of

this initiative, Motorola

announced a new commercial and production strategy that aims to reduce initial network

rollout costs by having elements of its Reach GSM portfolio manufactured locally.

Learning’s for India & how Indian companies can benefit The green solution can be implemented in Indian scenario. As part of its business strategy

Motorola has already started working on it and phased deployments of over 1,300 units

have been started in India to serve major cellular operators in the local market. The reach

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 20/21

20

strongbox, a DC outdoor enclosure for Motorola's Horizon II macro BTS, will be the first

product delivered under this strategy.

5. CONCLUSION

The growth of the telecom industry in the past few years has been unimaginable. Indian

telecom market has emerged among the fastest growing markets worldwide in last couple

of years and amidst rumors of a possible slowdown in the wireless infrastructure market

in the world (excluding India) in 2007-08, India has shown sustainable growth in net

additions of mobile subscribers in the past one year.

Present rapid growth has necessitated significant amount of investment in building up

wireless infrastructure in country but several bottlenecks like low spectrum, high cost of

infrastructure deployment etc. has made the task daunting and challenging for telecom

service providers. Newer and innovative means like broadband over power lines, green

solutions and infrastructure sharing can be used for cost effective telecom infrastructure

building in India.

REFERENCES 1. Subham Majumdar & Sunaina Dhanuka (August 2006), India Telecom Sector ,

Macquire Research Equities

2. Song Jiuang (January 2007), Operation and Maintenance Management Outsourcing,

Road to Telecom Service Outsourcing, Issue 1, Huwai Service

3. Babu Ranjan K, Mobile Jam, [available at:

http://voicendata.ciol.com/content/top_stories/407091001.asp], [viewed on:

November 26, 2007]

4. Overall Analysis: Basic Services Struggle as Mobile Shines, Voice & Data, Issue

July 2007, [available at: http://voicendata.ciol.com/content/vNd100/2007vol-

II/407070626.asp], [viewed on: November 26, 2007]

5. Network Management Services: In-house Vs Outsourcing, Voice & Data, Issue July

2007, [available at:

8/14/2019 India Telecom Infrastructure: Constratints and Opportunities

http://slidepdf.com/reader/full/india-telecom-infrastructure-constratints-and-opportunities 21/21

http://voicendata.ciol.com/content/goldbook/goldbook07/107031308.asp], [viewed

on: November 26, 2007]

6. Wireline Infrastructure: Awaiting Broadband Push, [available at:

http://voicendata.ciol.com/content/goldbook/goldbook07/107031308.asp], [viewed

on: November 26, 2007]

7. Power Management: Critical Focus, [available at:

http://voicendata.ciol.com/content/goldbook/goldbook07/107031236.asp], [viewed

on: November 26, 2007]

8. Outsourcing Trends: Eye on the Globe, [available at:

http://voicendata.ciol.com/content/goldbook/goldbook07/107031234.asp], [viewed

on: November 26, 2007]

9. Ibrahim Ahmed , MOST Appropriate, [available at:

http://voicendata.ciol.com/content/columns/editorial/107020701.asp], [viewed on:

November 26, 2007]