increased automobile fuel efficiency and synthetic fuels: alternatives for reducing oil imports

TRANSCRIPT

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 1/292

Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing

Oil Imports

September 1982

NTIS order #PB83-126094

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 2/292

Library of Congress Catalog Card Nu mb er 82-600603

For sale by the Sup erintend ent of Docum ents,

U.S. Government Printing Office, Washington, D.C. 20402

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 3/292

Foreword

This report presents the findings of an assessment requested by the Senate Com-mittee on C om me rc e, Sc ience, and Transportation. The stud y assesses and c om pa resincreased automobile fuel efficiency and synthetic fuels production with respect to theirpo tential to reduc e c onventional oil c onsump tion, and their c osts and imp ac ts. Con-servation and fuel switching as a means of reducing stationary oil uses are also con-sidered , but in co nsiderably less de ta il, in order to ena b le estima tes of p lausible futureoil imports.

We a re g rate ful for the a ssistanc e o f the p rojec t a dvisory pa nels and the m any o ther

people who provided advice, information, and reviews. It should be understood, how-ever, that OTA assumes full responsibility for this report, which does not necessarilyrepresent the views of individual members of the advisory panels.

Director

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 4/292

Automobile Fuel Efficiency Advisory Panel

Maudine R. Cooper*National Urban League, Inc.

John FerronNational Automobile Dealers Association

Michael J. Rabins, Chairman Wayne State University

Donald FriedmanMinicar, Inc.

Herbert FuhrmanNational Institute for

Automobile Service Excellence

James M. GillThe Ethyl Corp.

R. Eugene Goodson**Hoover Universal, Inc.

Charles M. Heinen***Chrysler Corp.

Synthetic Fuels Advisory

Harvey O. BanksCamp Dresser McKee, Inc.

Ellen BermanConsumer Energy Council of America

Leslie BurgessFluor Corp.

Frank CollinsOil, Chemica l and Atom ic Workers

International Union

Thomas F. EdgarUniversity of Texas

Louis FrickE. 1. du Pent d e Ne mo urs & C o., Inc .

Bernard GillespieMobil Research and Development Co.

John B. HeywoodMassachusetts Institute of Technology

John HoldenFord Motor Co.

Maryann N. KellerPaine, Webber, Mitchell, & Hutchins

Paul LarsenGMC Truck and Coa ch Division

Robert D. NellConsumers Union

Kenneth OrskiGerma n Ma rshall Fund of the United States

Howard Young*United Auto Workers

PanelHans Landsberg, Chairman

Resources for the Future

Robert HowellRefinery ConsultantChairman, Synfuels SubcommitteeSierra Club

Sheldon LambertShell Oil Co.

John L. McCormickEnvironmental Policy Center

Edward MerrowRand Corp.

Richard K. PefleySanta Clara University

AlIan G. PulsipherTennessee Valley Authority

Robert ReillyFord Motor Co.

Fred WilsonTexac o, Inc.

NOTE: The Advisory Panels provide d ad vice and comment throug hout the assessment, but the memb ersdo not nec essarily a pprove , d isapp rove, o r end orse the rep ort for w hich OTA assume s full responsibility.

q Resigned from panel.q q Formerly with Institute for Interdisciplinary Engineering Stud&, Purdue University.

* q q Retired from ChryslercOrp.

ICurrently with LTV Corp.

iv

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 5/292

OTA Increased Automobile FuelSynthetic Fuels Project Staff

Efficiency and

Lionel S. Johns, Assista nt Direc to r, OTA

Energy, Mate ria ls, and Inte rnat iona l Sec urity Division

Richard E. Rowberg, Energy Program Manager

Synthetic Fuels and Project Coordination Increased Automobile Fuel Efficiency

Thomas E. Bull, Project Director John A. Alic , Autom ob ile Tec hnology

Paula J. Sto ne, Assistant Project Director Marjory S. Blumenthal, Cost Analysis and

Steven E. Plotkin, Environmental Analysis Econom ic and Soc ial Imp ac ts

and Execu tive Summ ary Larry L. Jenney, Automob ile Tec hnology

Richard W. Thoreson, Eco nomic Impac ts Richard Willow, Electric Vehicles

Contributors

David Strom Franklin TugwellDavid Sheridan, Editor

Administrative Staff

Lillian Quigg Edna Saunders Marian Grochowski Virginia Chick

Contractors

E. J. Bentz & Associates, Inc., Springfield, Va.Wright Water Engineers, Inc., Denver, Colo.Michael Chartock, Michael Devine, and Martin Cines,

University of Oklahoma, Norman, Okla.

Ge neral Resea rch Corp., San ta Barbara , Ca lif.

OTA Publishing Staff

John C. Holmes, Publishing Officer

John Berg ling Kathie S. Boss Debra M. Datc her Joe Henson

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 6/292

Acknowledgments

OTA thanks the following p eople who took time to p rovide information or review p art or a ll of the study.

John AcordMontana Department of Natural Resources

and Conservation

David AlberswerthWestern Organization of Resource Councils

Louis E, AllenWyoming State Engineer’s Office

Mo rris AltshulerU.S. Environmental Protection Agency

Marty AndersonTransportation Systems CenterDepartment of Transpo rtation

Ray BaldwinPlanning Department, Garfield County, Colo.

Craig BellWestern States Water Council

Martin J. Bernard, IllCenter for Transporta tion Resea rchArgonne National Laboratory

Don BischoffCalifornia Energy Commission

William BoehlyNat iona l Highw ay Traffic Safety Administrat ion

Charles BrooksU.S. Department of Energy

A. L. BrownEXXON Co a l Resourc es, USA, Inc .

George ByronTransportation Systems CenterDepartment of Transpo rtation

James ChildressNationa l Counc il on Synthe tic Fuels Produc tion

George ChristopulosWyoming State Engineer

David ColeOffice for the Study of Automotive Transpo rtationUniversity of Michigan

George Davis

U.S. Nationa l Committee for Internat ionalHydrology Program

Clarence DitlowCenter for Auto Safety

C. Gilmore DuttonAppropriations and Revenue CommitteeKentucky Legislative Research Commission

Vernon FahyNorth Dakota Sta te Engineer

Jack FitzgeraldU.S. Environmental Protection Agency

Ga ry FritzMontana Department of Natural Resources

and Conservation

Jack GilmoreDenver Research InstituteUniversity of Denver

Harris GoldWater Purification Associates

David Gushee

Congressional Research ServiceJack HannonE. 1. du Pent de Nemo urs & Co ., Inc .

Richard HildebrandU.S. Department of Energy

Frank von HippelCenter for Energy a nd Environmenta l Stud iesPrinc eton University

Edward HoffmanConsultant

Harriet Holtzman

Environmental Policy Institute

Darrell HowardTennessee Valley Authority

Richard HowardSouth Dakota Department of Water

and Natural Resources

Charles HudsonArgonne National Laboratory

James JohnDepartment of Mechanical EngineeringOhio State University

Arvid Joupi

Joseph KanianthraNational Highway Traffic Safety Administration

vi

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 7/292

Sarah La BelleArgonne National Laboratory

Jonathan LashNatural Resources Defense Council

Minh-Triet LethiOffice of Scienc e a nd Tec hnology Policy

Kevin MarkeyFriends of the Earth

David MarksDepartment of Civil EngineeringMassachusetts Institute of Technology

J. P. MatulaEXXON Research & Engineering Co.

Dennis McElwainAFL-CIO

C. E. McGeheeBattlement Mesa, Inc.

Gary McKenzieNationa l Sc ience Found at ion

Ron McMahanAbt/West

Gene MeyerShell Oil Co .

Carl NashNat iona l Highway Traffic Safety Adm inistrat ion

Christopher PalmerNationa l Audob on Soc iety

Laszlo PastorDRAVO Corp.

E. Pipe r

Energy Development Consultants, Inc.James PosewitzMontana Department of Fish, Wildlife,

and Parks

Frank RichardsonNat iona l Highw ay Traffic Safety Adm inistrat ion

Richard D. RidleyOccidental International Corp.

H. RobichaudANG Coal Gasification

Phil Scha rreTennessee Valley Authority

William SchriverU.S. Departme nt o f Lab or

Roger ShunU.S. Department of Energy

Tom SladekColorado School of Mines Research Institute

Catherine SlesingerGeneral Accounting Office

John H. SmithsonU.S. Department of Energy

Earl StakerUtah Dep uty Sta te Enginee r

Dick StrombotneNat iona l Highwa y Traffic Safety Adm inistrat ion

George Tauxe

Sc ience a nd Public Policy ProgramUniversity of Oklahoma

David TundermannU.S. Environmental Protection Agency

Wallac e TynerDepartment of Agricultural EconomicsPurdue University

Richard A. WaldeGulf Research and Development Co.

David WalkerColorado Water Conservation Board

George WangBechtel Group, Inc.

R. M. WhamOak Ridge National Laboratory

Mary Pat WilsonWESTPO

Edward P. YarmowichU.S. Department of Energy

vii

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 8/292

Contents

Chapter Page

I. Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

2.introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

3. Policy . . . . . . . . . . . . . .. .. .. .. ... . . $........ . . . . . . . . . . . . . . . . . . . . . . 35

4. issues and Findings. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

5. Increased Automobile Fuel Efficiency . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 105

6. Synthetic Fuels . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 157

T. Stationary Uses of Petroleum . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 183

8. Regional and National Economic Impacts . . . . . . . . . . . . . . . . . . . . . . . . . . . 195

9. Social Effects and Impacts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 219

10. Environment, Health, and Safety Effects and Impacts . . . . . . . . . . . . . . . . . . 237

11. Water Availability for Synthetic Fuels Development . . . . . . . . . . . . . . . . . . . 279

Index . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 291

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 9/292

Chapter 1

Executive Summary

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 10/292

Contents

Page

Introduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Conclusions and Comparisons . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3Import Reductions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5Technological and Economic Risks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6Additional Bases for Comparison-Environmental Social and

Economic Effects . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

policy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8Stimulating Oil Import Reductions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8Dealing With Other Effects . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Overview of the lmport Reduction Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10Increased Automobile Fuel Efficiency . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10Synthetic Fuels . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Reducing Stationary Uses of Oil. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22Electric Vehicles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

TABLES

Table No.

I. Projec ted Average Fuel Economy, 1985-2000 . . . . . . . . . . . . . . . . .2. Domestic Investment for Increased Fuel Efficiency . . . . . . . . . . . . . . . . . . . . .3. Consumer Costs for increased Automobile Fuel Efficiency, Without

Discounting Future Fuel Savings, Moderate Shift to Smaller Cars . . . . . . . . .4. Price of Synthetic Fuels Required To Sustain Production Costs . . . . . . . . . . .5. Two Comparisons of the Environmental impacts of Coal-Based Synfuels

Produc tion a nd Coa l-Fired Elec tric Generation . . . . . . . . . . .6. Summary of Annual Energy Requirements To Displace 2.55

Stationary Fuel Oil Use . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

FIGURES

Figure No.

l. Potential Oil Savings Possible by the Year 2000 . . . . . . . . . .

. . . . . . . . . . . . .MMB/D of. . . . . . . . . . . . .

. . . . . . . . . . . . .2. Estimated Investment Costs for the Oil Import Reduction Options . . . . . . . .

Page

11

13

1417

20

23

Page

4

6

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 11/292

Chapter 1

Executive Summary

INTRODUCTION

In 1981, U.S. oil imports averaged 5.4 millionbarrels per day (MMB/D)–approximately 34 per-c ent o f its oil c onsump tion and 15 pe rc ent o f itstotal energy use. This is potentially a serious riskto the ec onomy and sec urity of the United States.

Furthermore, recovery from the current recessionwill inc rea se d emand for oil and , although c ur-rently sta b le, do me stic oil prod uc tion is likely toresume a stea dy d ec line in the nea r future.

Several options exist for reducing oil imports.However, even with moderate increases in auto-mobile fuel efficiency, moderate success at de-veloping a synthetic fuels industry and the ex-pected reduction in stationary use of fuel oil, U.S.

oil imp orts c ould still be ove r 4 MMB/ D b y 2000,if the U.S. ec ono my is hea lthy and has not under-

go ne unforeseen struc tural c hang es tha t m ightreduce oil demand well below projected levels.

Only with vigorous promotion of all three op-tions and technological success can the Nationhope to eliminate oil imports before 2010.

Congress faces several decisions on how to re-duc e the U.S. dep ende nce on imported p etro-leum. Two op tions, inc reased autom ob ile effi-c ienc y and synthet ic fue ls, are p artic ularly likelyto be subjects of congressional debates. First,Cong ress ma y wa nt to c onside r new inc entivesto increase auto fuel efficiency beyond that man-

dated by the 1985 CAFE (Corporate Average Fuel

Efficiency) standards. Second, Congress will haveto d ec ide whether to co ntinue into the sec ondphase of the program to accelerate synfuels devel-

op me nt und er the Synthet ic Fue l Corp . (SFC). Thepurpose of this report is to assist Congress in mak-

ing these decisions and comparing these optionsby exploring in detail the major public and private

costs and benefits of increased automobile fuelefficiency and synthetic fuels production. A third

op tion for reduc ing imp orts-inc rea sed efficien-cy and fuel switching in stationary (nontranspor-ta tion) o il uses—is exam ined b riefly to a llow anassessment of potential future levels of oil im-ports. Finally, elec tric -po we red a utom ob iles areexamined.

CONCLUSIONS AND COMPARISONSImport Reductions

In the judg me nt of the Office o f Tec hnologyAssessment, increased automobile fuel efficiency,

synthetic fuels production, and reduced station-ary (nontransportation) use of oil can significantlydecrease U.S. dependence on oil imports dur-ing the next two to three decades. indeed, reduc-

ing oil imports as quickly as possible requires that

all three options be pursued. Electric cars areunlikely to play a significant role, however.

Although a precise forecast of the future contri-butions of the import reduction options is not fea-sible now, it is possible to draw some general

conclusions about their likely importance and toestimate what their contributions could be under

spe c ific c irc umsta nc es (see fig. 1).

First, increases in auto fuel efficiency will con-tinue, driven by market demand and foreign

competition. OTA b elieve s tha t, with strong andconsistent demand for high fuel efficiency, there

is a good chance that actual average new-car fueleffic iencies wo uld be greate r than O TA’ s low sc e-nario in which average new-car fuel economy*was projected to be:

30 miles per gallon (mpg) . . . . . . . in 198538 mpg . . . . . . . . . . . . . . . . . . . . ., in 199043 mpg . . . . . . . . . . . . . . . . . . . . ., in 199551 mpg . . . . . . . . . . . . . . . . . . . . . . in 2000

with a moderate shift in demand to smaller cars.Although this scenario is based on modest techni-

cal expectations, it is dependent on favorablemarket conditions. Domestic automakers are un-likely to commit the capital necessary to continue

*EPA values, based on 55 percent city, 45 percent highway. On-the-road fuel economy is expected to average about 10 percent less.

3

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 12/292

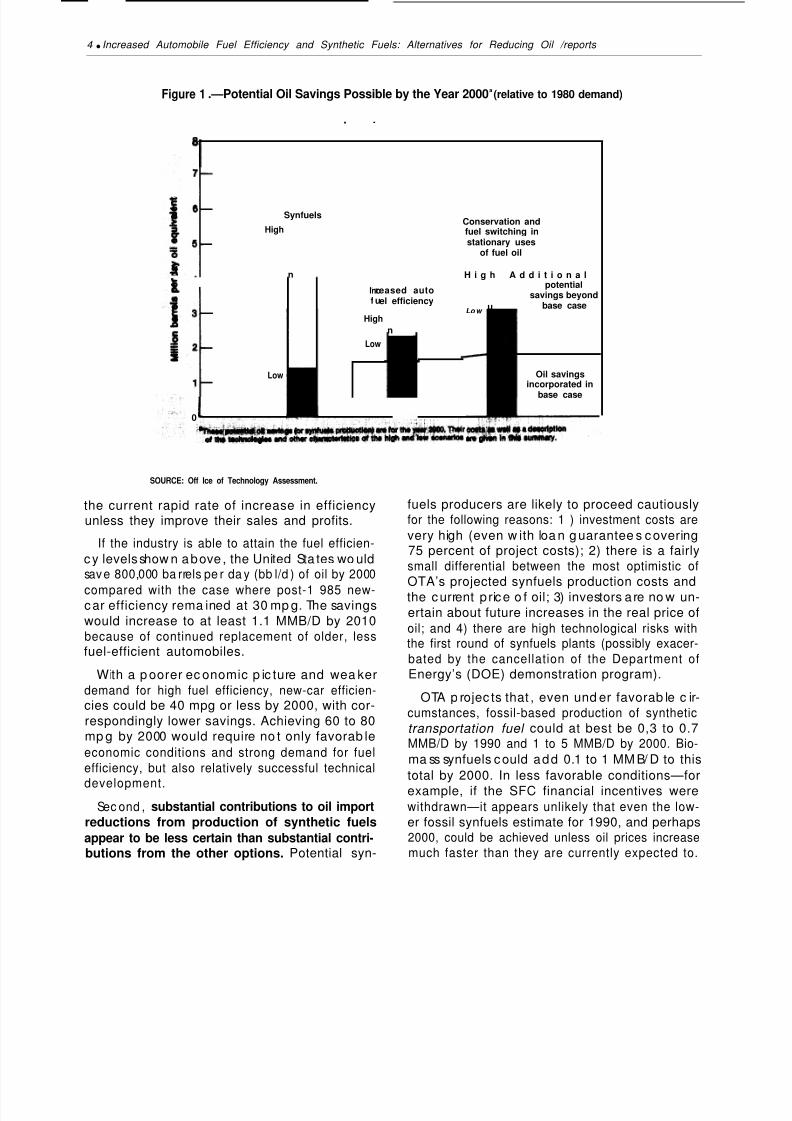

4 q Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil /reports

Figure 1 .—Potential Oil Savings Possible by the Year 2000a(relative to 1980 demand)

. .

Synfuels

High

n

Conservation andfuel switching instationary uses

of fuel oil

H i g h A d d i t i o n a l

Incf u

High

Low

‘- reased auto

u

potential

el efficiencysavings beyond

base case

n

Low Oil savingsincorporated in

base case

0

Lo w

SOURCE: Off Ice of Technology Assessment.

the current rapid rate of increase in efficiencyunless they improve their sales and profits.

If the industry is able to attain the fuel efficien-

c y levels show n a bove , the United Sta tes wo uldsave 800,000 ba rrels pe r da y (bb l/d ) of oil by 2000

compared with the case where post-1 985 new-c ar efficiency rema ined at 30 mp g. The savingswould increase to at least 1.1 MMB/D by 2010because of continued replacement of older, lessfuel-efficient automobiles.

With a p oorer ec onomic p ic ture and wea kerdemand for high fuel efficiency, new-car efficien-cies could be 40 mpg or less by 2000, with cor-respondingly lower savings. Achieving 60 to 80mp g by 2000 would require no t only favorab leeconomic conditions and strong demand for fuelefficiency, but also relatively successful technical

development.Sec ond , substantial contributions to oil import

reductions from production of synthetic fuelsappear to be less certain than substantial contri-butions from the other options. Potential syn-

fuels producers are likely to proceed cautiouslyfor the following reasons: 1 ) investment costs are

very high (even w ith loa n g uarantee s c overing75 percent of project costs); 2) there is a fairlysmall differential between the most optimistic ofOTA’s projected synfuels production costs andthe c urrent p ric e o f oil; 3) investors a re no w un-ertain about future increases in the real price ofoil; and 4) there are high technological risks withthe first round of synfuels plants (possibly exacer-bated by the cancellation of the Department ofEnergy’s (DOE) demonstration program).

OTA p rojec ts that , even und er favorab le c ir-cumstances, fossil-based production of synthetic

transportation fuel could at best be 0,3 to 0.7MMB/D by 1990 and 1 to 5 MMB/D by 2000. Bio-

ma ss synfuels c ould add 0.1 to 1 MM B/ D to thistotal by 2000. In less favorable conditions—forexample, if the SFC financial incentives werewithdrawn—it appears unlikely that even the low-er fossil synfuels estimate for 1990, and perhaps2000, could be achieved unless oil prices increasemuch faster than they are currently expected to.

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 13/292

Ch. 1—Executive Summary q 5

Ac hieving m uc h mo re tha n 1 MMB/ D of syn-fuels production by 2000 would require fortuitous

tec hnic al succ ess and either: 1 ) unamb iguousec onom ic profitability or 2) c ontinued financialincentives req uiring authoriza tions considerab lylarger than those currently assigned to SFC.Achieving production levels near the upper limits

for 2000 are likely to be de layed, p erhaps by a smuch as a decade, unless there is virtually a “warmobilization’ ’-type effort.

Third, there are likely to be large reductionsin the stationary use of fuel oil (currently 4.4MMB/D) in the next few decades. With just cost-effective conservation measures, stationary fueloil use could be reduced significantly. Additionalconservation measures by users of electricity andnatural gas could make enough of these fuelsavailable to replace the remaining stationary fueloil use by 2000. Total elimination of stationaryfuel oil use by 2000 is unlikely, however, becausesite-specific factors and differing investor paybackrequirements will mean that a significant fractionof the numerous investments needed for elimina-

tion will not be made.

Fourth, even a 20-percent electrification of theauto fleet—a market penetration that must beconsidered improbable within the next severaldecades—is unlikely to save more than about0.2 MMB/D. Electric cars are most likely to re-place small, low-powered–and thus fuel-efficient —conventional automobiles, minimizing poten-

tial oil savings.Plausible projections of domestic oil production

—expec ted by O TA to drop from 10.2 MMB/ Din 1980 to 7 MM B/D or lower by 2000—suggestthat oil imports could still be as high as 4 to 5MM B/D or more by 2000 unless imports are re-duc ed by a sta gna nt U.S. eco nomy o r by a re-sumption of rapidly rising oil prices. * Achievinglow levels of imports-to perhaps less than 2MM B/D within 20 to 25 years–is likely to requirea de gree o f suc c ess in the three ma jor op tionsthat is greater than can be expected as a result

of current policies.

*Rapidly rising oil prices are unlikely to occur simultaneously with

a stagnant U.S. economy unless the economies (and oil import re-quirements) of Europe and others are thriving at the same time.

costs

Except for stationary fuel oil reductions, eco-nomic analysis of the options for reducing oil im-ports involves a comparison of tentative cost esti-ma tes for mostly unproven technologies that will

not be deployed for 5 to 10 years or more. Even

if costs we re p erfec tly estimated for toda y’s mar-ket (and the estimates are far from perfect), dif-ferent rates of inflation in the different economic

sectors affecting the options could dramaticallyshift the comparative costs by the time technol-ogies are actually deployed. Figure 2 presentsOTA’s estimates for the investment costs for alloptions except electric cars. The costs are ex-pressed in dollars per barrel per day, which is theamount of investment needed to reduce petro-leum use a t a rate of 1 bb l/d . * In OTA’s judgment,

the estimated investment costs (in dollars perbarrel per day) during the 1990’s of automobileefficiency increases, synthetic fuels production,and reduction of stationary uses of oil are essen-tially the same, within reasonable error bounds.If Congress wishes to channel national invest-ments preferentially into one of these options,differentials in estimated investment costs can-not provide a compelling basis for choice.

On the other hand, investments during the1980’s to reduce stationary oil use (from the cur-

rent 4.4 to 3 MM B/D or less by 1990) and in-crease automobile fuel efficiency (to a 35 to 45mpg new-car fleet average by 1990) are likely to

cost less than the 1990-2000 investments in anyof the options.

Electric vehicles are likely to be very expensiveto the c onsume r—c osting p erhap s $3,000 mo reper vehicle than similar, conventional auto-mobiles or $300,000 to $400,000/bbl/d of oilsaved , (The la tter is not stric tly co mp arab le to in-

vestment costs for the other options. ) If batteriesmust be rep lace d a t mo de rate intervals, whic his necessary today, the total costs of electric carswould escalate.

*This measure was chosen in order to avoid problems that arisewhen comparing investments in projects with different lifetimes and

for which future oil savings may be discounted at different rates.

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 14/292

6 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

Figure 2.—Estimated Investment Costs for the Oil Import Reduction Options

Increased automobilefuel efficiency

I 45-80 mpgby 2000a

40-65 mpg , ,by 1995a-

Synfuels Reduction in stationaryuses of fuel oil

in the 1990’s

35-50 mpgby 1990a

Estimated 1985 cost ofconventional oil and gas

exploration anddevelopment in the United States

SOURCE: Office of Technology Assessment.

Technological and Economic Risks

The g eneral pe rce ption of the tec hnologica land ec onom ic risks of the imp ort red uc tion op-tions is: 1 ) that the reduction of stationary oil usehas comparatively predictable costs and few tech-nological risks; 2) that synthetic fuels have severeeconomic and technological risks; and 3) that in-creased auto fuel efficiency has moderate eco-nomic and tec hno log ica l risks. OTA’ s ana lysis in-

dic ates that these p ercep tions are c orrec t onlyto a limited extent.

Ž Although the costs and technology of fuelswitching are well known and involve little risk,the success of retrofitting a given building toincrease its energy efficiency often cannot be

q

q

q

accurately predicted because of site-specific

considerations that cannot be adequatelyquantified.

The d ifferenc es in risks betwe en synfue ls devel-opment and increased automobile fuel efficien-

cy are less a matter of overall magnitude thanof timing.Synfuel produc tion involves c onsiderab le tec h-nica l and ec ono mic risks for the first round ofcommercial-scale facilities, but once full-scaleprocess units have been demonstrated the risk

for future plants should drop substantially.Some increases in automobile fuel efficiencycan be implemented with negligible technolog-

ical and small economic risks, but increasesto very high efficiencies do involve significant

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 15/292

Ch. l—Executive Summary Ž 7

technical and economic risks. Also, as thenumber and rate of changes in automobiles in-

creases, there is increased risk that consumerswill not accept the automobiles and that insuffi-

cient development and testing will lead to pooron-the-road performance and/or product re-

calls.

Additional Bases for Comparison—Environmental, Social, and

Economic Effects

Increased auto fuel efficiency may reduce ve-hicle safety as cars are made smaller and lighter.But in all but extreme cases of vehicle size reduc-

tion, improvements in vehicle design and in-c reased passeng er use of sa fety restraints havethe p otential to o ffset a ny effec ts of reduc ed sizeand weight on the vehicle’s protection of its oc-

cupants in a crash.Continued pressure for increased fuel efficien-

cy will dictate new plant investments which willreinforce the ongoing restructuring of the U.S.auto industry. This restructuring involves a shiftin manufacturing away from the traditional pro-duc tion c ente rs to the Sun Belt and oversea s, andstronger industry ties with foreign manufacturers.The c om position a nd size of the ma nufac turingwork force may evolve towards a greater propor-

tion of skilled workers but fewer workers overall.Increased sophistication and capital investment

may be required for vehicle maintenance. A re-duction in the number of suppliers to the autoindustry may also result.

Large-scale synthetic fuels production wouldgenerate significant amounts of toxic sub-stances, posing risks of health damage to work-ers and possible risks to the public through con-tamination of ground waters or by smallamounts of toxics left in the fuels. There shouldnot be any technological barrier to adequatecontrol of these substances, but OTA concludesthat there are substantial reasons to be con-cerned about the adequacy both of proposedenvironmental protection systems and of the ex-isting regulatory structure.

Other important effects of synfuels produc-tion stem from the very large scale of both theindividual projects and, potentially, the industryas a whole. These m ay o verwhe lm the soc ial and

ec onom ic resources of nea rby po pulation ce n-ters, especially in sparsely populated areas of theWest. At national production levels of a few mil-lion barrels per day, impacts from coal and shale

mining and population pressures on wildernessareas and other fragile ecosystems can be sub-stantial even in comparison with major industriessuch as coal-fired power generation. On the other

hand , co nventional air pollution p rob lems fromsuch plants are likely to be considerably less than

those associated with similar amounts* of coal-fired power generation.

Finally, although water requirements for syn-fuels are a small fraction of total national con-sumption, growth of a synfuels industry could

either create or intensify competition for water,depending on both regional and local factors.Suc h com petition is of spe c ial conc ern in the a ridWest. Unfortunately, a reliable determination ofboth the cumulative impacts on other water usersand, in some instances, the actual availability ofwa ter for synfuels de velopm ent is prec lude d byphysical and institutional uncertainties, changingpublic attitudes towards water use priorities, andthe analytical shortcomings of existing studies.

However, in areas where there are relativelyfew obstacles to transferring water rights (e.g., as

is currently the case in Colorado), developersshould be ab le to obta in the wa ter they needbecause their consumption per barrel of oil pro-duced is small enough to enable them to pay arelatively high price without significantly affect-ing the final cost of their products.

Electric vehicles, if they are ever produced inlarge quantities, could have an important posi-tive environmental effect-the reduction ofautomobile exhaust emissions and resulting im-provements in urban air quality.

*On a “per unit of coal used” basis.

9a-2 e 1 ~ - a 2 - 2 : I: II J 3

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 16/292

8 • Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

POLICY

OTA’s analysis points to two conclusions thatmay warrant congressional consideration ofchange s in c urrent Fed eral energy p olic y.

First, c urrent policies affec ting investments in

energy conservation and domestic energy pro-duc tion a re not likely to result in leve ls of o il im-ports below 4 MMB/D in 2000, if the U.S. econ-omy is healthy and has not undergone unfore-seen structural changes that might reduce oil de-mand well below projected levels. During thenext 20 yea rs, OTA expec ts tha t, under thesepolicies, oil import reductions due to syntheticfuels prod uc tion and d ec rea sed sta tionary andautomobile oil use will be partially offset by adecrease in domestic production of conventionaloil. Reducing net oil imports to 1 or 2 MMB/Dor less by 2000 is likely to require more vigorous

pursuit of all options for reducing domestic con-sumption of conventional oil products. On theothe r hand , eliminat ion o f current c onservationand synthetic fuels production policies couldcause imports to range from 5 to 6 MMB/D by2000 under these same economic conditions.

Sec ond , current p olicies ma y not p rovide soc i-

ety with ad eq uate p rotec tion from some of theadverse side e ffec ts of synthetic fuels de velop -ment and increased automobile fuel efficiency.

Of particular concern are possible reductions inautomobile crash safety (as the number ofsmaller, more fuel-efficient cars increases), inade-

qua te c ontrol of toxic substanc es from synfuelsdevelopment, and adverse socioeconomic effectsfrom both options.

Because of the large technical, economic, andmarket uncertainties inherent in the analyses ofoil displacement options, Congress may wish toemphasize flexible incentives with provisions forperiodic review and adjustment. A stable com-mitment to oil import displac eme nt will be nec es-sary, however, to maximize the effect of suchpolicies.

Stimulating Oil Import ReductionsThe leve l of oil imp orts at the turn of the c en-

tury will be d ete rmined by m arket forces, mod i-fied by Government policy towards oil supply

and de ma nd. The imp osition of Fed eral polic yon the wo rkings of the private m arket ge nerallyis justified on the basis of the ma rket ’ s failure tovalue public costs and benefits. A particularly im-po rtant p ublic co st of U.S. dep end enc e o n im-

ported oil, for example, is the national securityproblem imposed by political instability in theMiddle East and the resulting potential for oil cut-offs. Although the precise magnitude of thesec osts is de ba tab le, most p eop le would a gree thatthey are significant ($5 to $50/bbl depending onvarious circumstances) and that the private mar-ket generally does not take them into account.

Efforts to displace imports also have both publicand private costs. In addition to the potential side

effects just mentioned, Government interferencein the oil marketplace can cause significant misal-

Iocations of resources. Congress will have to bal-ance costs and benefits, which cannot be re-duced to common measures and which changewith time, in a c omp lex trad eoff.

One policy option to displace imports is an en-ergy tax, either on oil imports or on oil in gen-eral. Both taxes have the advantage of encourag-ing alternatives to conventional oil consump-tion without predetermining which adjustmentswo uld b e ma de . They co uld b e used to p rovideconsistent price signals to the market—to assurethe auto industry, for example, that demand for

fuel-efficient cars would continue and to assuresynfuels de velop ers tha t they w ould rec eive a tleast a constant real price for their products. im-posing a tax only on transportation fuels wouldsend the sam e signal to b oth the auto industryand to producers of synthetic transportation fuels,

but this preferential treatment would be at theexpense of other conservation or synfuelsproduction investors.

All of these petroleum taxes also have a numberof o ther effec ts which must be c onsidered . Forexample, a tax only on oil imports leads to an

income transfer from domestic oil consumers todomestic oil producers; and all oil taxes can leadto reduced international competitiveness of do-mestic industries heavily dependent on oil, such

as the p etroc hemica l industry.

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 17/292

Ch. I—Executive Summary q 9

po lic ies c an a lso b e d irec ted spe c ifica lly at the

auto mo bile o r synfue ls industries. The m ost effec -tive of these options will be those that directlyaddress the factors that shape, direct, and limitthe contributions that the automobile and syn-fuels industries can make to import displacement.

The c ritical fac tors that d etermine the pa c e ofincreased automobile fuel efficiency are con-sumer demand for fuel efficiency and the finan-cial health of the domestic auto industry. If theindustry is uncertain about demand, it will be re-luctant to make the expensive investments. And

with continued poor sales, the industry will beless ab le to afford them.

Aside from ene rgy ta xes, Cong ress c an ma in-tain and stimulate consumer demand for fuel ef-ficiency by a variety of measures that would raise

the rela tive c osts to c onsume rs of o wning ineffi-

cient cars. For example, registration fees (onetime o r annua l) and purcha se ta xes or subsidiesare incentives that can be directly linked to fuel

efficiency. However, fuel-efficiency incentivestha t d o no t d isc rimina te w ith respec t to c a r sizewould tend to increase sales of small cars at theexpense of larger cars. Such discrimination mighthurt domestic manufacturers, which have been

most vulnerable to foreign competition in thesma ll-ca r market.

Cong ress c an also c hoose p olic ies aimed atauto production such as continuing to requiremanufacturers to improve fuel efficiency bymeans of stricter CAFE or similar standards thatwould ensure increased fuel efficiency even if de-

mand for this automobile attribute is low. Thisregulatory route might reduce some risks to auto-makers by requiring all to make similar invest-ments. On the other hand, car sales may sufferif the costs of the fuel savings—either in highersticker prices or reductions in some desirable ve-hicle attributes–are higher than consumers arewilling to pay. Fuel-economy requirements arelikely to be perceived by the industry as exceed-ingly risky unless the requirements are accom-

pa nied by m ea sures to stimulate d ema nd o r toease the resulting financial burden on the auto-makers.

To help ensure that the fuel-efficient cars areactually bought and that the automakers can ac-

quire the capital needed for increasing fuel effi-

ciency, Congress may also wish to directly pro-mote sales of fuel-efficient cars. A low-interest-rate loan program (with interest rates tied to fuel

efficiency) is one potentially effective mechanism.Congress may also wish to consider awarding di-rect grants or loan guarantees for qualifying in-

vestments in auto manufacturing facilities.

The fac tors that d etermine the pa ce of synfuels

development are the high degree of technical un-

ce rtainty and the c ontinuing uncertainty ab outfuture oil prices. Both areas of uncertainty con-tribute to doubts about profits.

Current Federal policy maintains the valuableincentives associated with SFC, but reemphasizesDOE’s research, development, and demonstra-

tion prog rams. The loan g uarantee me c hanismoffe red b y SFC signific antly imp rove s the p rob a-

bility of financial success for a developer andprobably will be necessary to ensure even a fewhundred thousand barrels per day of synfuels pro-

duction by the early 1990’s. Several major risksto synfuels investors remain, however. Cost over-runs couId nuIlify any potential profits becausedevelopers must base their product prices on themarket prices of competing fuels rather than on

synfuels production costs. It is also probable that

several first generation commercial-scale unitswill function p oorly, and rap id expa nsion o f theindustry ma y thereb y be d elayed .

Sinc e the SFC p rog ram ap pe ars to b e a ttrac t-ing the c ap ital needed to b uild and dem onstratea series of first generation commercial-scale pro-duction units, cancellation of DOE’s programsma y not turn out to b e p artic ularly harmful to syn-fuels development if the first plants performwell. However, cancellation of the demonstra-tion p rogram probab ly will mean that fewe r tech-nologies reach the stage where SFC support ispossible. Reemphasis of development programsmay also delay findings that would be useful infixing the technical problems that are likely toa rise in the first c om me rcia l-sc a le units. To he dge

against the possibility of poor operation delay-ing expansion, Congress may wish to support de-

velopment programs intended to demonstrate thetechnical feasibility of a variety of processes andto g ain ba sic knowledge of a nd e xperience with

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 18/292

10 q Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

these processes. Although these demonstrationprog ram s supp ort sec ond and third g ene rationprocesses, they w ill also p rovide eng ineering in-formation that may be useful for correcting tech-nical faults and reliability problems that may arisein first generation plants.

Dealing With Other EffectsAn important e ffect of increa sing autom ob ile

fuel efficiency is the potential for decreased auto-motive safety due to size and weight reduction.There ma y also b e m ajor emp loyment-relatedside effects associated with the restructuring ofthe auto industry and the accompanying acceler-

ated rates of capital investment by the industry.There a re familiar policy instruments that c an d ea lwith both of these effects. For the safety effects,Congress can choose among safety standards fornew cars, educational programs, and support of

sa fety R&D. Emp loyment effec ts ma y be e asedby minimizing plant relocations (through taxbreaks or direct assistance to the industry), or by

am eliorating the effects of em ployment reduc -tions through aid to c omm unities and affec tedworkers and other individuals.

potential environmental and worker-relatedproblems associated with synfuels developmentare substantial, and there is c ause fo r co nc ernab out the ad eq uac y of future reg ulation of thesynfuels industry. The Government can help to

assure that the private sector takes account ofthese prob lems. Spe c ific area s wo rthy of cong res-

sional attention include: the environmental re-sea rc h a nd reg ulatory prog ram s of t he Environ-mental Protection Agency (EPA), DOE, the Officeof Surfac e Mining, a nd the O cc upa tional Safetyand Health Administration, in light of recent

budget cuts and changes in program direction;the dismantling of DOE’s demonstration programfor synfuels technologies; and the progress of SFCin demanding appropriate consideration of siting,monitoring, pollution controls and occupationalsafety as a condition for financial assistance. Con-

gressional options range from holding oversighthearings to increasing the resources of the envi-ronmental regulatory agencies and shifting theirprog ram em pha ses by leg islation.

To mitiga te the soc ioeconomic e ffec ts on com-

munities from synfuels development, Congressmay wish to consider several forms of growthmanagement assistance, including loan guaran-

tees, grants, and technical assistance. Any newFederal initiatives in this area will be complicated,

however, by continuing arguments about relative

responsibilities of Federal, State, and local govern-ments and private industry. And new initiativesneed to be sensitive to the substantial differencesfrom location to location in the severity of im-pacts and the resources already available for miti-

gation.

OVERVIEW OF

Increased Automobile Fuel

Automo bile fuel effic ienc y ca n

THE IMPORT REDUCTION OPTIONS

Efficiency Projections of Fuel Economy

be increased Future oil savings from increased automobile

throug h a variety o f me asures, inc luding: fuel efficiency depend, first, on the magnitudeand character of future auto sales. In the past few

q

q

q

q

q

q

q

reductions in vehicle weight;improvements in conventional engines,transmissions, and lubricants;be tter c ontrol of engine ope rating pa ram -eters;

new engine and transmission designs;reduced aerodynamic drag;improvements in accessories; anddec reases in rolling resistanc e.

years, consumer preferences for such fuel-econ-omy-related characteristics as vehicle size andperformance have fluctuated while new car saleshave d rop pe d signific ant ly. Both the long-termsales average and consumer preference for fuel

efficiency will be critical determinants of the rateof p enetration o f fuel effic ienc y tec hnolog y.

Second, in response to changing consumerpreferences and foreign competition, the rate of

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 19/292

Ch. I—Executive Summary 11

change of vehicle technology has accelerated andold rules about how long it takes to put a newtec hnology into p lac e* a re no longer valid. Thepresent rapid rate of replacement of capital equip-ment puts a great strain on the do mestic a uto in-dustry. During the next several years, competitive

forces will push toward continued rapid techno-logical change, but the financial weakness of the

domestic auto industry will pull toward slowertec hnologica l cha nge . The strength of future for-eign c omp etition a nd co nsumer percep tions ofthe future price and availability of gasoline anddiesel fuel, among other factors, will influencethe balance of these opposing forces, and, conse-

quently, whether rapid increases in fuel efficiencyof domestically produced cars continue.

Third, t he efficienc y increa ses are not fully p re-dicta ble. There ca n be d iscrepanc ies be tween test

resuIts and the results obtained in actual use.Tec hnic al c omp rom ises that affec t ultima te p er-formance have to be made to allow better inte-gration with existing equipment, easier andcheaper production and assembly, and resistance

to extreme operating conditions and incorrectma intenance proced ures. Developm ent p rob-lems are not always solved satisfactorily; suchproblems could occur more frequently if techno-logical change accelerates.

OTA deve lope d p rojec tions (tab le 1) of plausi-ble ranges of average new-car fuel economy

based on varying expectations of the relative de-mand for different-sized cars and the effectivenessand rate of development and introduction of new

fuel-economy improvements. As reflected inthese projections, both technology and vehiclesize are critical factors for future fuel savings. Mar-ketplac e unc ertainty is reflecte d even a s ea rly asthe 1985 projections—manufacturers’ plans andthe technology are already established, but the

*For example, previous assumptions were: 5 years to move frominitial production decision to introduction of a technology in amodel line; 5 to 10 years to diffuse the technology throughout the

new car fleet; and 10 to 15 years of production to pay for the invest-ment. The estimate of 5 years to move from initial production deci-sion to introduction may now be a bit too low, while increasedrate of change of vehicle technology would necessarily reduce theother two estimates.

Table 1 .- Projected Average New-Car FuelEconomy,a1985.2000 (mpg)

1985 1990 1995 2000

No further shift towards smallercars beyond 1985 . . . . . . . . . . 30-34 36-45 39-5443-62

Moderate further shift tosmaller cars . . . . . . . . . . . . . . . 30-34 38-48 43-5951-70

Rapid shift to small cars . . . . . . 33-37 43-53 49-6558-78aBased on EPA city/highway (55/45 percent) cycle. Each of the mileage ranges(e g., 3034) reflects relative expectations of the performance and rate of develop-ment and deployment of new technologies. The lower value represents OTA’S

“low estimate” scenario, the upper value represents a “high estimate” scenario.

SOURCE: Office of Technology Assessment

Note on Table 1: Can We Do Better?

The projections in table 1 do not represent the t ec lmo /og i ca / limitof what could be achieved in this century. The most efficient auto-mobiles in each size class are likely to achieve considerably betterfuel economy than the average; for example, technologies are avail-able that probably can allow a new-car fleet average of 60 mpg by themid-1990’s with the same mix of vehicle sizes as today’s and adequatevehicle performance (compared with the table’s 1995 “same size mix”projection of 39 to 54 mpg). This ignores co nsume r preferenc es for veh ic /e features that cor) f / i c t with fue l economy maximization, how- ever. By the same argument, the 1981 new-car fleet average COUM have been 33 mpg if consumers had consistently chosen the most efficient

vehicle in each of the nine EPA size classes and producers had beenable to meet the demand. Instead, the actual 1981 model average toJanuary 1981 was 25 mpg.

Interestingly enough, if consumers had chosen only the most fuel-

efficient gasoline-powered automobiles in each size class, over 90percent of the vehicles would have been U, S.-manufactured cars orcaptive imports. The market problems of U.S. manufacturers in 1981cannot be traced primarily to an inability of U.S. manufacturers to pro-duce fuel-efficient cars, but depend on factors such as differencesin perceived value between American and imported automobiles.

The difference between average fuel efficiency, which is a func-tion of consumer preference, and potential fuel efficiency, whichassumes that every car in the fleet embodies the most fuel-efficientchoice of technologies available, is critical to understanding whyOTA’S projections may differ from other projections that apply a sin-gle choice of technologies to the entire fleet. The latter assumptionis realistic only if future consumers value fuel economy, relative toother automobile attributes, much higher than they do today.

projec tions still range from 30 to 37 mpg* (c om-pared to the 1981 level of 25 mpg).

How m uch fuel can b e saved by improved fueleconomy? Assuming 30 mpg as a base and using

the projections in table 1, continued develop-ments in automobile fuel efficiency could save0.6 to 1.3 MMB/D of oil by 2000. The lowervalue represents pessimistic expectations aboutthe advance of automobile technology and theshift towards smaller cars; the higher value repre-sents optimistic technological expectations and

continued substantial shifts to small cars. Contin-

* Based on a weighted average of 55 percent EPA city test cycleand 45 percent EPA highway cycle, the formula used to measurecompliance with currently mandated CAFE requirements.

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 20/292

12 q Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

ued diffusion of these technologies into theoverall fleet could save 0.8 to 1.7 MMB/D by2010 with no further technological advances be-

yond 2000. *

costs

OTA’ s c ost a na lysis of auto fuel-efficienc y im-provements concentrates on investment costs in

total d olla rs as we ll as dolla rs per ba rrel pe r da yof oil saved. Estimates of the costs for associatedtechnology and product development are in-cluded in the investment costs,** because they

are part of the normal outlays needed to put anynew vehicle in production and represent a sizablefraction of the fixed costs (i.e., costs independent

of production levels).

It is not possible to ma ke highly ac c urate esti-mates of the investment costs (per barrel per day

of o il save d), d ue to the unc ertainty assoc iatedwith predic ting ac tual effic ienc y inc rea ses thatwill be achieved. In addition, the cost of develop-ing technologies to the point where they can be

reliably mass-produced has been highly variable

and is difficult to predict.

Accurate cost estimation also is complicated bythe difficuIty of separating the cost of increasingfuel efficiency from the other costs of doing busi-ness. Increases in fuel efficiency are inextricablyintertwined with other changes in the car. For ex-

ample, the engine redesign for fuel efficiency may

incorporate other changes, to improve otherauto mob ile attribute s, at little ad ditional co st. De-sign changes that increase efficiency may improve

or d eg rad e o ther a ttribu tes suc h a s em issions orperformance.

If it is the industry’s judgme nt that c onsume rsdo value fuel efficiency, the normal cycle of cap-

ital turnover and vehicle improvement would re-

sult in an increase in fuel efficiency automatical-ly. Unfortunately, the “ normal” rate o f fuel effi-ciency increase is not really predictable because

*Assuming 1.26 trillion vehicle miles (automobile only) traveledannually in 2000, 1.31 trillion in 2010, and an on-the-road fuel ef-ficiency 10 percent less than EPA rated fuel efficiency.

**In this context, development means all of the engineering activ-ities needed to prove a design concept and determine how it canbest be integrated into the vehicle system and mass-produced.

it depends on marketplace preferences and cor-porate strategies.

Because of the difficulty of separating out themarginal fuel efficiency investments from the“normal” investments, OTA’s investment costestima tes (in dollars per ba rrel pe r day) in tab le

2 are the total investments (including develop-me nt c osts) allocated to increasing fuel efficien-cy, divided by the total fuel savings rate expected.

(See footnote c of ta ble 2 for the d eta ils of thec ost a l loc at ion.) These investme nt rates ma y besome wha t lower than the m arginal rates wo uldbe be c ause, in designing their “ normal” invest-ment programs, manufacturers probably will se-lect those investments with the highest potential

payoff in efficiency increase per dollars spent.

In any c ase, the rang e o f investment rates forincreased fuel efficiency for each time period

overlap the rates for investments in synfuels plants(see Synthetic Fuel section below), although the1985-90 fuel-efficiency rates would be lower than

the synfuels rates if widespread expectations foroverruns in early synfuels investments are provedcorrect,

The total domestic capital investment associ-ated with increased fuel efficiency would beabout $25 billion to $70 billion between 1985 and2000, or less than $2 billion to $5 billion annu-ally during the period. This level of investmentcan be compared with recent and projected capi-

tal investment by the industry* remembering thatpa rt of the fuel-effic iency investment c ould b e in-

cluded in “normal” capital expenditures if con-sumer d ema nd for fuel efficiency is high enoug h.For the period 1968-77, annual capital investmentby General Motors (GM), Ford, and Chrysler aver-aged $6.68 billion in constant 1980 dollars. In-vestments by these companies rose to $10.4 bil-

lion in 1979 and $10.8 billion in 1980, and areprojec ted by som e a na lysts to rise to $12 billionper year during 1980-84. The ability of thedomestic industry to maintain their expectedschedule of capital expenditures is dependent on

*The two sets of figures are not fully analogous. A portion of thedomestic industry’s costs are for overseas investments, while a por-

tion of the 1985-2000 fuel efficiency costs will be borne by outsidesuppliers rather than the major manufacturers.

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 21/292

Ch. I—Executive Summary q 1 3

Table 2.—Domestica Investment for Increased Fuel Efficiency

Total investmentCar sales New-car fuel Efficiency investment (billion 1980$

Time (mill ion/yr) efficiency (mpg)b (thousand 1980 $/bbl/day) during time period)

1985-1990 . . . . . . . . . . . . . . . . . . . . . . . . . 8.6 38-48 20-60 8-291990-1995 . . . . . . . . . . . . . . . . . . . . . . . . . 8.8 43-59 60-140 9-201995-2000 . . . . . . . . . . . . . . . . . . . . . . . . . 9.1 51-70 50-150 7-18

aASSUrneS 75 percent of all cars sold are manufactured domestically.

bFleet average m~les per gallon at end of time per iod, wi th mode ra t e shift in demand to W?’ Idler cars,CRepresents costs allocated t. fuel efficiency, including associated development costs of 40 percent of capital spending. lnVW3tm(3nt WaS allocated in the fOliOWing

way: 50 percent of the total engine investment is assumed to be for fuel efficiency; 75 percent of the total investment for conventional transmissions is for fuel effi-

ciency; and all of the investment for advanced materials substitution, automatic engine on/off, and energy storage devices is for fuel efficiency.dlncludes all capital costs associated with fuel efficiency, including fraction allocated tO other attributes, but excluding development costs,

SOURCE: Office of Technology Assessment.

a resump tion o f the ir former leve ls of sa les andp rofitab ility. There are a lrea dy signs tha t U.S. aut omanufacturers are beginning to cut back onplanned investments in the face of continuedpoo r sales and dec lining c ash reserves.

If consumer demand for fuel efficiency is con-

sistent ly strong, dom estic ma nufa c turers are likelyto respond by at least incorporating into their“ normal” * rate of c ap ital turnover as ma ny fuel-efficiency features as possible. if capital turnoveris limited to its historica l “ norma l” rates, then thefuel efficiencies shown in table 1 could still beachieved, but it would take longer to implementthe c hang es than is indic ate d b y the sc hed ulesshown in that table. In particular, implementa-tion of the low sc ena rio c ould require 25 percent

longer (relative to 1985) than the schedule intable 1; and the high scenarios could require 45percent longer. Whether the high or the low sce-

nario is eventually achieved, however, also de-pends on the success of technical developments.

If demand for fuel efficiency were high enough,however, the manufacturers would increase theirredesign/replacement rates. By adding $5 billionto $10 billion in capital expenditures during1985-2000, or $0.3 billion to $0.7 b illion per year(5 to 10 percent above “ norma l” ), ca pital turn-over can be speeded up to allow the low scenar-

ios to be achieved on the schedule in table 1.Similarly, if technology developments are suc-cessful, the high scenario could be achieved as

shown in table 1 with capital expenditures of $9

*Assuming “normal” capital turnover is: engines improved after6 years, on average, redesigned after 12 years; transmissions sameas engines; body redesigned every 7.5 years; no advanced-materials

substitution.

billion to $23 billion a bo ve “ normal” during theperiod 1985-2000, or $0.6 billion to $1.5 billionper year (10 to 20 percent a bo ve “ norma l” ).

If future demand for fuel efficiency is not high

enough to support these rates of change, in-creases in fuel efficiency will be further delayedunless required by new CAFE sta nd ards. On theother hand, CAFE standards without analogouslyhigh consumer demand for efficiency would re-quire the manufacturers to either defer expendi-tures for other improvements that might help carsales or to incur additional capital costs.

The c onsume r co sts of inc rea sed fuel efficien-cy, measured in dollars per gallon of gasolinesaved, are speculative because the variable costs

—mostly material and labor costs—are even more

difficult than investment costs to determine accu-

rate ly. OTA’ s ana lysis is based on a lterna tive as-sumptions about the degree of change in material

and labor costs. A direct calculation of these costswould have been expensive and the results diffi-

cult to defend because the source data is proprie-tary and highly dependent on judgments aboutthe success of adapting technologies to mass pro-duc tion. Table 3 show s the range of c osts a ttrib-uted to fuel efficiency assuming that consumersvalue future gasoline savings as highly as today’s

savings (i.e., without discounting future savings*)and that manufacturers pass through the fullcosts. Conceivably, foreign competition couldforce the manufacturers to absorb part of these

costs.

*The cost perceived by consumers would be about 2.5 times ashigh as those shown if the consumer discounts future fuel savingsat 25 percent per year, i.e., each future year’s savings during thelife of the car is valued at 25 percent less than the previous year’ssavings.

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 22/292

14 . Increased Autobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

Table 3.—Consumer Costs for Increased Automobile Fuel Efficiency, WithoutDiscounting Future Fuel Savings, Moderate Shift to Smaller Cars

Average new-car fuel Consumer costa ($/gal saved)

efficiency at end of No variable cost High variableTime period time period (mpg) increase costb increase

1985-1990 . . . . . . . . . . . . . . . . . . . . 38-48 0.15-0.40 0.40-1.101990-1995 . . . . . . . . . . . . . . . . . . . . 43-59 0.35-0.85 1.10-2.60

1995-2000 . . . . . . . . . . . . . . . . . . . . 51-70 0.30-0.95 0.90-2.80aA~~Urn~~ a ~aPltal recovew factor per year of 0,15 times the capital investment allocated to fuel efficiencybAssumes variable cost increas~ IS twice the capital charges associated with the capital investments allocated tO fuel efficiency.

SOURCE: Office of Technology Assessment.

The consumer costs of fuel efficiency rangefrom values that are easily competitive with to-day’s gasoline prices to values that are consider-ably higher, dep ending on the efficiency ga insactually achieved, the success of developing pro-duction techniques that can hold down variablecost increases, and the value consumers placeon future fuel savings. Investments for increased

efficiency for the 1990-2000 model years will lookparticularly risky if the current soft petroleummarket continues for a few more years, or if automanufacturers have difficuIty holding down theirlabor and materials costs.

Another important measure of the cost to con-

sumers of increased fuel efficiency is the increasein the pric e of ne w c ars req uired to rec over theindustry’s increased production costs. If themarket demand for fuel efficiency is strongenough to ensure that as much as possible of thecapital investment for fuel efficiency increases is

incorporated into the normal capital turnover,and if the variable costs of production can be held

c onstant, then the c ost* of ac hieving OTA’ s fuel-efficiency scenarios can be as low as $60 to $130per car during the 1985-2000 time period. Underthese conditions, an average of 35 to 45 mpgcould be achieved by 1990 without increasingnew-car costs.

If ac tual ma rket dem and for fuel effic ienc y isnot this high, automakers would be unlikely toincorporate a very high level of fuel efficiency in-

vestments into their normal capital turnover. Also,

the va riable c osts of p rod uct ion are likely to risesomew hat. The “ uppe r bound” for ad ded c osts —assuming large increases in variable costs and

*Assumes a capital recovery factor of 0.15.

no market-driven investme nt for fuel efficienc yincreases beyond 1985—is $800 to $2,300 per carduring the 1985-2000 period, and $250 to $500pe r ca r to ac hieve 35 to 45 mp g b y 1990. There-fore, the cost per car of increased fuel efficiencybeyond 1985 ranges from “clearly competitive”to “probably unacceptable. ”

Economic Impacts

The domestic automobile industry is in themidst of a massive investment program aimed atimproving the competitiveness of American auto-

mo biles. These expe nd itures are a ssoc iated with

important structural changes in the industry; andaccelerating the rate of capital turnover (for in-c rea sed fuel effic iency o r other rea sons) ma y ac -

celerate some of these trends.

Manufacturers are closing older, inefficientplants and building new ones that incorporate

extensive use of robots and other labor-savingtec hnology to inc rea se p rod uct ivity. For a num-be r of reasons, inc luding lowe r lab or and otherc osts, many of the new fac ilities ma y be built inthe Nation’s Sun Belt or overseas rather than inthe current North-Central auto manufacturingcenters, although recent labor concessions mayc hange this pic ture. Bec ause o f a shift in U.S. de -mand to smaller cars, which can be marketedmore universally, the incentive to produce in the

United States is diminishing. Finally, because rap-id c apita l turnove r is raising p roduc tion c osts a ta time when consumer demand for automobiles

has been sluggish, manufacturer profits havediminished and it ha s be c om e ha rde r for the firmsto secure capital at affordable costs.

American companies are forging more exten-sive ties with foreign manufacturers to design,

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 23/292

Ch. l—Executive Summary q 1 5

produce, and market fuel-efficient cars, and aremoving towards producing more nearly standard-ized automobiles that can compete in internation-

al markets. Current trends seem to be toward few-

er separate automotive manufacturing and supplyfirms worldwide; only GM and Ford appear tobe reasonably certain of remaining predominant-

ly American-owned.

Certain regions such as the industrial Midwest —and the Nation as a whole—will lose jobs ifthese structural changes continue. Job losses also

would occur, however, if the process is inter-rupted, because the restructuring represents theindustry’s response to the conditions that causedits present market problems, and it clearly isaimed at regaining sales.

Social Impacts

As auto manufacturing and supply activities be-co me m ore efficient and autom ated , there willbe important changes in the workplace environ-ment. Robots and other automated equipmentwill increasingly be used for the more routine and

dangerous jobs, and skilled workers such as engi-

neers and maintenance technicians should be-come a greater percentage of the smaller totalwo rk force . Shifting ma nufa c turing ove rsea s willred uc e U.S. emp loyme nt in p rima ry m anufa c tur-ing as well as in supplier companies. Althoughemployment losses may be larger in the supplierindustries, the effects in these industries will be

distributed over a larger geographical area. Em-ployment in related activities such as repair and

service will cha nge to a cc omm od ate the newauto characteristics—e.g., repairs of plastic bodycomponents require adhesives, not welding—andthe increasing sophistication and capital invest-ment required for vehicle maintenance will placenew de ma nds on shop s and de alers.

Fuel efficiency increases also affect automobile

ow ners by c hang ing the p hysic al a ttributes of the

vehicle and the ec onom ics of ow ning c ars. Forexample, a continued reduction in car size could

lead to increasing use of rentals for longer tripsor for occasional requirements for increased car-go-carrying capacity. Increases in the initial cost

of b uying a ca r are likely to lead to a co ntinua-tion of current trends of keeping cars longer,

resulting in a slower growth or reduction in new-car sales.

Environment, Health, and Safety

Increasing automobile fuel efficiency appearslikely to have a relatively benign effect on the nat-

ural environment and public health, becausemost of the efficiency measures have few adverse

effects on auto emissions, emissions associatedwith vehicle manufacturing, etc. An important ex-

ception may be any shift to widespread use ofdiesel engines, which could cause problems withvehicle particulate and nitrogen oxide (NO X)emissions. Also, the increased production of light-

weight materials—particularly aluminum—maycause additional impacts, such as increasedenergy consumption in processing and increasedde ma nd for ba uxite. On the o ther hand , signifi-c ant do wnsizing o f auto mo biles c ould a llow ei-

ther lower vehicle emissions or lower controlcosts to maintain current emission levels.

In contrast to their expected small effect on pol-

lution levels, fuel conservation measures thatstress reducing vehicle size may have a signifi-c an t a dverse e ffec t on vehic le sa fety. This is be-

cause of the important role in crash survivalplayed by “crush space”* and other size- andweight-related factors. Even a relatively small de-

c line in vehicle safe ty c ould c ause hund red s oreven thousands of additional deaths and seriousinjuries per year.

There is no w idely ac c ep ted estimate of thema gnitude of t his effec t. The Na tional Highw ayTraffic Safety Administration has projected a10,000 per year increase in traffic deaths fromvehicle size reductions by 1990, but this is basedon a limited data set and a number of simplifyingassumptions. And a net increase in traffic deathsis not inevitable, since increased usage of passen-ger restraints and improvements in vehicle design

could more than offset the effect of moderate sizereductions.

*With a smaller “crush space” (thus, more rapid deceJerat;on

of occupants in a crash), factors such as seatbelt and shoulder re-straint usage, better driver training and traffic control, and othersafety measures, become more important determinants of trafficsafety.

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 24/292

16 q Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

Synthetic Fuels

Production of a variety of fossil fuel-based syn-thetic fuels is planned or under development.

q Oil shale can be heated to release a liquidhydrocarbon material contained in the shale.After further upg rad ing a synthetic crude oilsimilar to high-quality natural crude oil can beproduc ed . This c an be refined into ga soline,diesel and jet fuels, fuel oils, and other prod -ucts.

q Coal can be partially burned in the presenceof steam to produce a so-called “synthesis” gasof carbon monoxide and hydrogen, fromwhich gasoline, methanol, diesel and jet fuel,and other liquid fuel products (“indirect lique-faction” ) or synthetic natural gas (SNG) c a nbe produced.

q

Coal also can be reacted directly with hydro-gen (which is itself generated from a reaction

of steam and coal) to produce a syntheticcrude oil (“ d irec t liquefa c tion” ). This oil c anbe c onverted to gasoline, jet fuel and otherproducts in specially equipped refineries.

Projection of Synfuels Development

The p rinc ipa l technica l deterrent to rap id d e-ploym ent of a synfuels industry is the lac k of p rov-en commercial-scale synfuels processes in theUnited States. Shale oil, indirect coal liquefaction,and SNG processes currently are sufficiently de-veloped that the demonstration of commercial-scale process units or modules is being pursued,but these first units are likely to require consider-

able modification before they can operate satis-factorily. Once these commercial-scale moduleshave been adequately demonstrated, full-sizec omme rc ial fac ilities c an b e c onstruc ted (fromseveral modules). in contrast, direct coal liquefac-

tion requires further development before com-me rc ialization a nd proba bly will not c ontributesignificantly to the synfuels industry before themid to late 1990’s. A ma jor tec hnic al ob stac le,the ha nd ling of high levels of solids in the p roc -ess streams, is not now und erstoo d we ll eno ughto allow developers to move directly to commer-cial- from small-scale units now in operation.

Normal planning, permitting, and constructionma y ta ke 7 to 8 yea rs for a la rge synfuels p lant,with the last 5 years or so devoted to construc-tion. Consequently, a first round of commercial-scale plants conceivably could be operating bythe late 1980’s, although these w ould b e quitevulnerable to delays and cost overruns. Beginning

a sec ond round of c onstruc tion be fore the firstset of plants has been fully demonstrated wouldrisk additional costly revisions and delays.

In addition to scheduling constraints caused by

technological readiness, shortages of experiencedmanpower (primarily chemical engineers andprojec t ma nage rs) c ould co nstrain the pa ce ofsynfuels development. On the other hand, prob-lems stemming from shortages of skilled crafts-men, construction materials, or specializedequipment probably can be averted because ofthe long Ieadtime before they are needed in large

numbers. However, some metals needed for cer-ta in stee l alloys a re ob ta ined almo st e xclusivelyfrom foreign sources.

Many variables affect the rate of development,and predictions are extremely speculative. It isOTA’ s judg me nt tha t under favorable circum-stances, fossil fuel-based production of synthetictransportation fuels could be 0.3 to 0.7 MMB/Dby 1990, growing to 1 to 5 MMB/D by 2000,de pe nding o n the succ ess of t he first round ofsynfuels plants and the fraction of those plantsthat produce transportation fuels as opposed to

fuel gases or fuel oils. Achievement of 0.3 MMB/Dby 1990 assume s tha t a sizab le c om me rcializa -tion program, such as that being pursued by the

Synthetic Fuels Corp., is c arried out, but tha ttechnical problems limit total production; 0.7MMB/D would require an increased number ofplant commitments within the next year or so,a virtually complete emphasis on liquid transpor-tation fuels, and a high level of tec hnic al succ esswith the first plants.

It must be stressed that even the “low” 0.3MMB/D production level maybe considered asoptimistic in light of c urrent e xpe c tat ions of a tleast short-term stability in oil prices, as well asremaining technical and environmental uncer-tainties. In addition, the dismantling of DOE’sdemonstration program may increase the per-ceived and actual technological risks of synfuels

8/14/2019 Increased Automobile Fuel Efficiency and Synthetic Fuels: Alternatives for Reducing Oil Imports

http://slidepdf.com/reader/full/increased-automobile-fuel-efficiency-and-synthetic-fuels-alternatives-for 25/292

Ch. l—Executive Summary q 1 7

development. Thus, the goals of the NationalSynfuels Production Program, created by Con-gress in 1980—0.5 MMB/D by 1987 and 2MMB/D by 1992—appear unattainable withouta crash program that would involve extraordi-nary technical and economic risks and exten-

sive Government intervention.

costs

The costs of synfuels are uncertain. First, thefac tors that limit rapid de ployment of the industrya lso a ffec t its c osts. Tec hnica l unce rtainties c om -