in the supreme court of queenslandbrisbane o.s. no. …

TRANSCRIPT

IN THE SUPREME COURT OF QUEENSLAND O.S. No. 929/97

Brisbane

[P.D. Mortgage Services Pty Ltd v Marquart]

BETWEEN:

P.D. MORTGAGE SERVICES PTY LTD

A.C.N. 065 740 847

Applicant

AND:

ROBERT ANTHONY MARQUART Respondent

REASONS FOR JUDGMENT - FRYBERG J.

Judgment delivered 29th August 1997

The respondent is the registered proprietor of an estate in fee simple in land at 55 Railway Parade, Norman Park, more particularly described as the land contained in Lot 1 on R.P. 40735 in the County of Stanley, Parish of Bulimba, title reference 13012217. The applicant (“PDMS”) is the registered first mortgagee of that land. There is a second mortgage of the land registered in favour of a former solicitor of the respondent. On Christmas Eve 1996, a caveat was lodged on behalf of the respondent forbidding the registration of any instrument affecting the land. Sections 3 and 4 of the caveat were as follows:

“3. Interest being claimed

Interest as Registered Proprietor

4. Grounds of claim

(a) Mortgage No. 700520265 to P D Mortgage Services Pty Ltd is void on the basis that the Mortgagee and/or its agents engaged in conduct which was fraudulent, misleading and/or deceptive, and/or unconscionable.

(b) P D Mortgage Services Pty Ltd lacks the power of sale under Mortgage No. 700520265.

(c) P D Mortgage Services Pty Ltd has failed to take reasonable care to ensure that the subject property was sold at the market value.”

In form, these sections are defective. Section 3 ought to specify the estate claimed by the caveator, viz an estate in fee simple; although this can probably be inferred from the terms actually used. Section 4 should specify the basis of that claim, which in this case is the fact that the caveator is the registered proprietor. Nothing turns on these deficiencies.

On 31st January this year, PDMS applied for the removal of the caveat. That application was heard before me by way of trial in the civil list. PDMS contends that in early 1995 it lent $145,000.00 to Mr Marquart; that this money (or at least $110,000.00 of it) fell due for repayment on 17th February 1996; that Mr Marquart failed to repay it and thereafter failed to pay interest on it; that it gave notice of exercise of power of sale in March 1996 and duly entered into possession of the land in May 1996; and that it now requires removal of the caveat in order to complete a contract for the sale of the land. Mr Marquart, who appeared before me unrepresented, opposed the order. It is not easy to articulate the grounds of his opposition as they emerged in the course of the hearing. However, as best I could understand it, he alleges that PDMS was at all material times an agent for a company called Private Mortgage Lending Limited (“PML”) in everything it did, or was affected by knowledge of PML's conduct; and that as against him, PML was guilty of fraud, misleading or deceptive conduct, unconscionable conduct or breach of contract. He further alleges that he has the capacity to sell the land almost immediately for a higher price than is payable under the sale by PDMS and intends to do so. Finally, he contends that the amount claimed by PDMS is incorrect.

The Land Title Act 1994 prescribes who may lodge a caveat1. The registered owner of a lot is a person by whom a caveat may be lodged. A caveat lodged by the registered owner does not lapse under s. 126 of the Act. However, the court has a discretion to order its removal2. The exercise of this discretion should be approached on the basis that the caveator is in a position equivalent to that of an applicant for an interlocutory injunction to restrain sale3, save perhaps that an undertaking as to damages may not always be necessary. Precisely how this is to be applied in a case where the standing of the caveatee as such is challenged by the caveator need not be examined in this case. Mr Marquart did not suggest that PDMS had no interest in the land, although he has commenced an action to have that interest set aside. Nor, as will appear, need I concern myself with questions of onus of proof. Prima facie, PDMS is entitled to exercise its power of sale. The questions for me are whether there is, in Mr Marquart's action, a serious question to be tried; and what course is favoured by the balance of convenience.

Serious question to be tried

PML was incorporated on 2nd August 1993. Its original directors were a Mr Huntress and a Mr and Mrs Dachroeden. Its principal place of business was originally at Surfers Paradise. Its principal activity was described in the records of the Australian Securities Commission as “lending agents”. A man named Thomas John O'Toole was associated with it in some way though not initially as either a director or shareholder. O'Toole either was or had been a bankrupt.

1 Section 122.

2 Section 127.

3 Re Barman's Caveat [1994] 1 Qd R 123.

In or before August 1993, O'Toole met by chance Mr James Wilson, a solicitor and partner in the firm Purvis Duncan. O'Toole and Mr Wilson had been to school together, although Mr Wilson had not seen O'Toole for 25 years. On behalf of PML, O'Toole asked Mr Wilson to provide advice regarding PML's capacity to borrow money from the public without issuing a prospectus. Mr Wilson advised that the only way that could be done was by the issue of promissory notes under an exemption relating to prescribed interests under the Corporations Law. On 24th August 1993, O'Toole on behalf of PML wrote to Mr Wilson and sought his advice whether a proposed advertisement was “legally correct”. The advertisement invited the reader to “Think big dollars lending your money to PML”. Mr Wilson advised that the proposed advertisement did not breach the Corporations Law, but, as he said in evidence, also advised that “there were a lot of protocols and compliances to be observed”. As Mr Wilson remembered it, the proposal to borrow on promissory notes was never actually implemented, although it is clear that he performed work as a solicitor in relation to the proposal with a director of PML and in discussions with the Reserve Bank, the Australian Securities Commission, printers and Price Waterhouse during February 1994.

In April 1994, O'Toole replaced Mr Dachroeden as the company secretary of PML and on 1st July 1994, O'Toole and Georgina Mary O'Toole replaced Mr and Mrs Dachroeden as directors. At about this time, a fresh proposal was made by PML to Purvis Duncan. This proposal sought to take advantage of the fact that under the Corporations Law it was not necessary in certain circumstances for a prospectus to be issued in respect of loans made though a solicitor's trust account. This proposal involved the idea that PML would find both lenders and borrowers, the latter through an associated company, Private Mortgage Finance Limited (“PMF”) of which the O‘Tooles were also directors and O'Toole the principal executive officer.

Purvis Duncan agreed to participate in this scheme and to allow their trust account to be utilised. From 15th

March until 20th June 1994, PML's registered office was at their premises. Who played what role in relation to the establishment of the scheme and its subsequent operation at Purvis Duncan is not clear. Both Mr Wilson and another partner Mr McLeod, (who described Mr Wilson as his “predecessor”) sought in evidence to distance themselves from it. Mr Wilson said that at about the time PML decided that it was not going to proceed with the promissory note proposal, he was making arrangements to leave Purvis Duncan. He said he was not involved in setting up the arrangement involving PDMS; and that when PML put its proposal forward, he did little more than tell them they were at liberty to refer people who wished to invest in the private mortgage market to the firm. He said his background was as a commercial lawyer, not as a securities lawyer, and that for this reason, he avoided any more contact than he needed to have with the proposal. He said it was handed over to Mr McLeod and a Mr Lee to take further.

Mr McLeod, on the other hand, thought that Mr Wilson was the one who set up PDMS and denied that he was involved at all. In an affidavit filed before the trial, he swore, “Neither [PMF] or [PML] have any connection whatever with PDMS or Purvis Duncan.” However, in cross-examination, he admitted he could not say whether PDMS was incorporated as a result of Purvis Duncan acting for PML. He said Mr Wilson had given some advice and had “originally” had a position as one of the directors of PDMS. As he understood it, PML and its associate were either in the process of canvassing or were about to canvas people to lend money and other people to borrow money. They sought advice from Purvis Duncan about the propriety of doing that by way of advertisements, and after making their own enquiries, Purvis Duncan recommended incorporation of PDMS for PML, to facilitate the lending. He said PML paid the costs of acquiring the shelf company, which appears inconsistent with his earlier evidence that O'Toole did not instruct Purvis Duncan to establish PDMS. He agreed the directors of PDMS were partners of Purvis Duncan from time to time, and it existed solely to deal with transactions initiated by

PML. He said Purvis Duncan charged fees for doing the conveyancing which the arrangement produced.

Mr McLeod emphasised that PDMS had no funds of its own. It was, he said, simply a vehicle to facilitate the consolidation of funds from various lenders and the administration of mortgages securing the loan of the consolidated funds. He said that the way the arrangement worked, both in general and in this particular case, was that lenders would be referred to Purvis Duncan by PML. They would place their money in the Purvis Duncan trust account. Thereby they would become clients of Purvis Duncan. At the same time, they would sign a standard form “Letter of Appointment, Authority, Direction and Release“4.

When a lender was found, his or her money would be placed with PDMS as trustee. It would then lend the money on first mortgage security to borrowers referred by PML. According to Mr McLeod, neither Purvis Duncan nor PDMS acted on behalf of PML.

A central question for me is whether the model thus presented by Mr McLeod in fact represents the nature of the various transactions accurately. To begin with, it should be noted that Mr McLeod was not entirely consistent in his description of the model. At a later point in his evidence, he said:

“Purvis Duncan did not advertise for funds in its own right. It was not approached by borrowers in its own right. Private Mortgage Lending was the broker who undertook those two roles of locating the investors and locating the borrowers. Now, directions as to both those entities, both the lenders and the borrowers, were then provided to us by way of instruction on behalf of the lenders and we followed those directions.

Let me get this clear. Are you saying that there was this firm Private Mortgage Lending which either itself or with

4 I shall refer to the terms of this letter a little later.

its associate company solicited people to lend funds, solicited for people to borrow funds, went along to your firm to carry out the mechanics of the transaction through PD? - - That's correct, Your Honour.”

There are a number of matters which Mr Marquart brought out in evidence which suggest that the transactions and relationships did not accord with the model described by Mr McLeod. It is necessary to scrutinise what happened in some detail to see why this is so.

From the second half of 1994 until early 1996, PML advertised in national newspapers with an advertisement some 12cm high and 7.5cm wide. The text of the advertisement was, “PRIVATE MORTGAGE LENDING LIMITED will pay you 15% PA. 12-month term. Interest paid monthly. First Mortgage Security.” There followed telephone numbers and addresses for offices in Brisbane, Sydney and Melbourne. In or about February 1995, Miss Leanne Pearce “provided” $110,000.00 to PML. The money came from her superannuation fund known as Gaterise Unit Trust, and was directed to PML on the advice of the person who had originally set up the superannuation fund. Miss Pearce, who gave evidence before me, asserted that the money was given to PML and she was “almost positive” that the cheque was made out to PML. She thought that PML was a company set up to lend funds to developers. Somehow, her funds got into Purvis Duncan's trust account. I was not favoured with evidence of how this happened.

In December 1994, Mr Derek Chapman had deposited $10,000.00 with Purvis Duncan. That money was placed in the firm's trust account, to be lent out on first mortgage security by PDMS. In February 1995, Eric Stuart Gaul and Georgia Gaul advanced at least $26,000.00 to someone. This money also, by some mechanism which I cannot describe in detail, found its way to the trust account of Purvis Duncan. The circumstances of these deposits were not in evidence. I shall refer to the trustees of the Gaterise Unit Trust, the Gauls and Mr Chapman as “the lenders”, a description used by the applicant's witnesses.

At or about the time the lenders paid their money, each executed the document headed “Letter of Appointment, Authority, Direction and Release”. This was addressed to Purvis Duncan. The operative parts were as follows:

“FUNDS FOR INVESTMENT TO BE LOANED ON FIRST MORTGAGE SECURITY

I/we acknowledge that you are acting on behalf of me/us and that PRIVATE MORTGAGE LENDING LIMITED A.C.N. 061 116 185 (“PML”) are authorised by me/us to provide to you all necessary directions and authorities for the advance of moneys lodged in your trust account by me/us on my/our behalf.

I/we AUTHORISE AND DIRECT you to pay all moneys held in your trust account on my/our behalf from time to time upon the written direction of PML, for investment upon the security of a First Registered Mortgage/s over real property (whether vacant land, land with improvements, residential, commercial/industrial or howsoever described) (“the security property”).

You are authorised to prepare a First Registered Mortgage together with the collateral securities (if any) as directed by PML (“the securities”).

Your searches and/or enquiries in relation to the security property are to be limited to those instructed by me/us to PML.

I/we acknowledge that I/we intend relying on the commercial judgement and advice of PML in relation to the adequacy of the security property and the Borrower's ability to meet its obligations under the securities. We are not relying upon your firm for any prudential advices in connection with the proposed loan. I/we acknowledge that an independent valuation of the security property will be furnished to me/us by PML.

Your instructions in this transaction are limited by the terms of this letter and I/we release Purvis Duncan from any liability accordingly. You are authorised to sign the securities on my/our behalf to enable them to be registered. You are authorised to insert details of the Borrower in the form titled “Lenders Direction the Borrower”, once the identity of the Borrower is known.

I/we acknowledge that further moneys may be provided by other lenders and these moneys may be secured jointly as part of a Contributory Mortgage.

The receipt by you of this letter of appointment, authority, direction and release shall be a good and sufficient discharge for your firm to act on my/our behalf in this transaction.”

The arrangement reflected by this document strikes me as quite an extraordinary arrangement as between solicitor and client, if that was really what the relationship was. The solicitors' attempt to protect themselves by this letter in my view arguably reflects the reality that they were taking instructions from PML and from no one else. As Mr Wilson himself conceded, the arrangement reflected in the document was simply not satisfactory if the true relationship of solicitor and client existed between the solicitors and the lenders:

“I don't think that's at all satisfactory, really, to be quite frank with you. that's not the way I would prefer to have done it or preferred to have had it done.

In your view what's the unsatisfactory aspect of that sort of arrangement? - - Well, I personally would have thought that the Law Society requirements would have been that the instructions and the directions had to come direct from the client but you know, that's not for me to say. That's just my opinion.”

The respondent was a developer. He was, I think, a builder by trade. In February 1995, he wanted funds to develop a block of four townhouses on the land the subject of the caveat. At that time, the land had been cleared and Council approval had been given for the construction of the townhouses. He had negotiations with O'Toole. On 9th February 1995, he received a letter from PMF, signed by O'Toole. I shall quote part of it only:

“JOINT VENTURE ADVANCE TO YOU AGAINST PROPERTY SITUATED AT 55 RAILWAY PARADE, NORMAN PARK IN THE STATE OF QUEENSLAND.

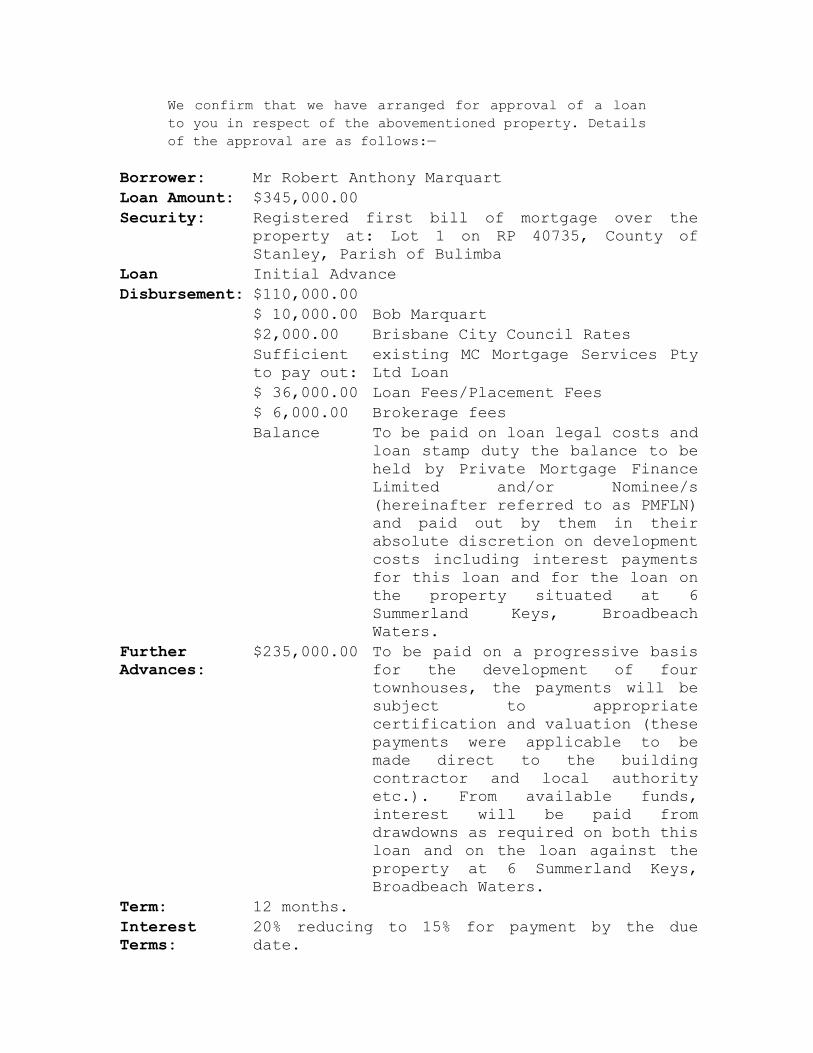

We confirm that we have arranged for approval of a loan to you in respect of the abovementioned property. Details of the approval are as follows:—

Borrower: Mr Robert Anthony MarquartLoan Amount: $345,000.00Security: Registered first bill of mortgage over the

property at: Lot 1 on RP 40735, County of Stanley, Parish of Bulimba

Loan Initial AdvanceDisbursement: $110,000.00

$ 10,000.00 Bob Marquart$2,000.00 Brisbane City Council RatesSufficient to pay out:

existing MC Mortgage Services Pty Ltd Loan

$ 36,000.00 Loan Fees/Placement Fees$ 6,000.00 Brokerage feesBalance To be paid on loan legal costs and

loan stamp duty the balance to be held by Private Mortgage Finance Limited and/or Nominee/s (hereinafter referred to as PMFLN) and paid out by them in their absolute discretion on development costs including interest payments for this loan and for the loan on the property situated at 6 Summerland Keys, Broadbeach Waters.

Further Advances:

$235,000.00 To be paid on a progressive basis for the development of four townhouses, the payments will be subject to appropriate certification and valuation (these payments were applicable to be made direct to the building contractor and local authority etc.). From available funds, interest will be paid from drawdowns as required on both this loan and on the loan against the property at 6 Summerland Keys, Broadbeach Waters.

Term: 12 months.Interest Terms:

20% reducing to 15% for payment by the due date.

Type of Loan: Interest only, payable monthly.The Loan to At no time will the loan exceed the loan to

value ratioValue Ratio: of 69%”

The letter concluded:

“[T]he Mortgagee reserves the right to withdraw its offer of finance should the valuation and/or searches or inquiries prove unsatisfactory. This offer shall remain open for acceptance until 5pm Thursday 9 February, 1995, after which time it shall be deemed to have lapsed.”

The letter is signed by the respondent against the word “Accepted” and the signature is dated 9th February 1995. The respondent deposed that he was required by O'Toole to accept or reject the offer on the day on which he received it, and had no time to take advice.

An important part of the respondent's case is the proposition that upon his acceptance of this offer, the lender became obliged to provide loan funds of $345,000.00 and/or that the lender misled him to believe this would occur. It is common ground that at most, no more than $145,000.00 was provided. The respondent contends that his inability to repay the funds was caused by the lender's breach of the loan agreement. Because of that breach, he argues, he was unable to complete the townhouses and sell them. He has not explained why he could not borrow the balance elsewhere, but I infer that the mortgage to PDMS made this impractical. PDMS did not really challenge the link between PMF and PML. However, Mr McLeod asserted that PDMS knew nothing of the letter of 9th February 1995 and that it never agreed to advance more than $145,000.00, which it did advance. He said it had no legal relationship with PMF or PML and could not be responsible for either of them.

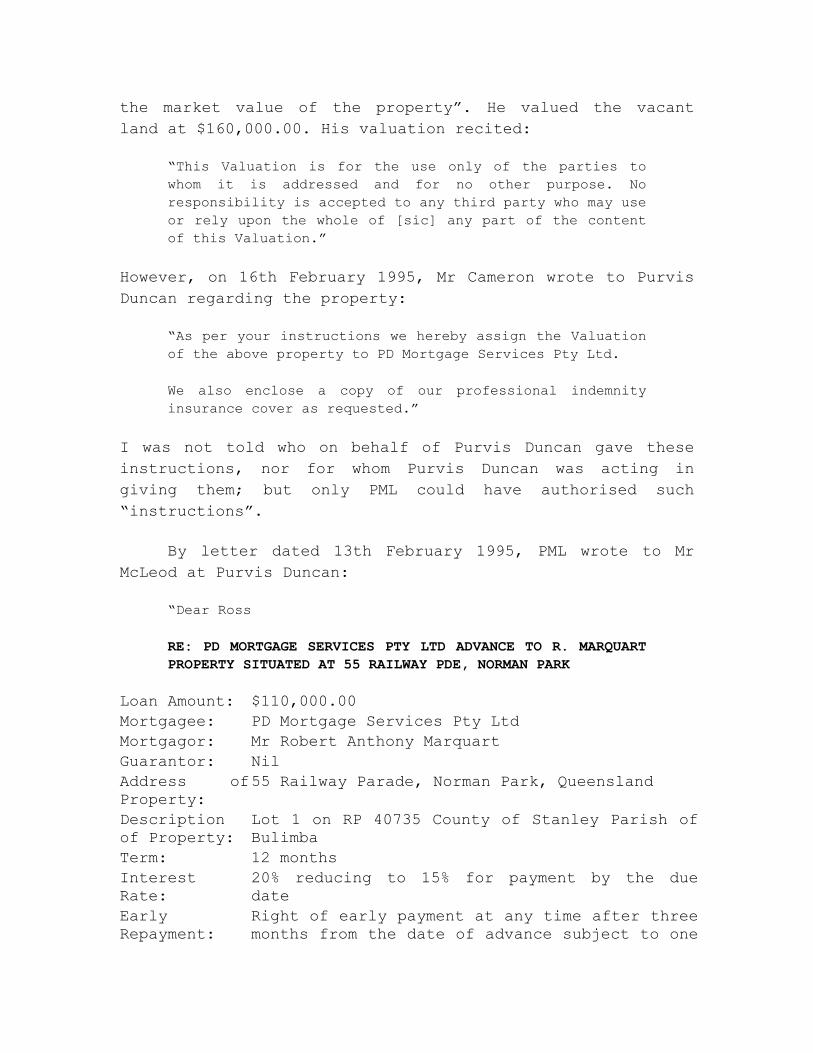

On 1st February 1995, Mr David Cameron, a registered valuer, carried out a valuation of the land the subject of the caveat. He did so “under instructions from Private Mortgage Lending Limited for the purpose of ascertaining

the market value of the property”. He valued the vacant land at $160,000.00. His valuation recited:

“This Valuation is for the use only of the parties to whom it is addressed and for no other purpose. No responsibility is accepted to any third party who may use or rely upon the whole of [sic] any part of the content of this Valuation.”

However, on 16th February 1995, Mr Cameron wrote to Purvis Duncan regarding the property:

“As per your instructions we hereby assign the Valuation of the above property to PD Mortgage Services Pty Ltd.

We also enclose a copy of our professional indemnity insurance cover as requested.”

I was not told who on behalf of Purvis Duncan gave these instructions, nor for whom Purvis Duncan was acting in giving them; but only PML could have authorised such “instructions”.

By letter dated 13th February 1995, PML wrote to Mr McLeod at Purvis Duncan:

“Dear Ross

RE: PD MORTGAGE SERVICES PTY LTD ADVANCE TO R. MARQUART PROPERTY SITUATED AT 55 RAILWAY PDE, NORMAN PARK

Loan Amount: $110,000.00Mortgagee: PD Mortgage Services Pty LtdMortgagor: Mr Robert Anthony MarquartGuarantor: NilAddress of Property:

55 Railway Parade, Norman Park, Queensland

Description of Property:

Lot 1 on RP 40735 County of Stanley Parish of Bulimba

Term: 12 monthsInterest Rate:

20% reducing to 15% for payment by the due date

Early Repayment:

Right of early payment at any time after three months from the date of advance subject to one

months notice and payment of one months interest at the lower rate of payment or payment of two months interest at the lower rate where no such notice is given. However, any payment from the sales of residential unit sites or any development on the secured property will only require one months written notice without any additional payment required.

There will need to be provision for variations to this mortgage document, which will eventually extend this mortgage to $345,000.00 this loan being $110,000.00 and a further loan of $235,000.00 to be drawn down against development work.”

Not surprisingly, Mr McLeod seems to have taken this letter as instructions to prepare documentation. On 15th February 1995 he wrote to the respondent enclosing the bill of mortgage in duplicate, requisitions on title, an estimate of Purvis Duncan's costs and outlays, a letter of acceptance and a statutory declaration regarding the identity of the property. He listed the documents which were required in return and also what would be required on settlement. Although at first he denied doing so, he later admitted that he delivered the letter to PML. The respondent executed the documentation the following day. His signature was witnessed by O'Toole.

The mortgage which was subsequently registered provides for a loan of $110,000.00. There appears to be no special provision of the type referred to in the letter from PML, although there is an “all debts” clause. The letter of acceptance was addressed to Purvis Duncan and PDMS. It authorised Purvis Duncan to deduct their costs and outlays from the loan advance. It contained a direction for the payment of rates and land tax of a little over $2,600.00. It contained a direction to pay out the existing mortgagee of the land an amount just under $40,000.00. It contained a further direction to pay $10,000.00 to the respondent and the balance, over $56,000.00, to PML.

On 17th February 1995, the mortgage document was executed by Mr McLeod on behalf of PDMS. At the same time, Purvis Duncan debited the account of the Gaterise Unit Trust in its trust account ledger the sum of $100,000.00, and credited that amount to the account of PDMS. Five days later it transferred a further $10,000.00 from the Gaterise account to the PDMS account. Each credit to the PDMS account was described as “Advance monies” from the Gaterise Trust. All but $4,023.00 of the total of $110,000.00 was disbursed in accordance with the respondent's direction by 16th March 1995.

On 13th April 1995, PML wrote to Purvis Duncan again. The form of letter was similar to that of 13th February. This time the loan amount was $35,000.00 and the body of the letter provided:

“Ross, could you please prepare a variation to the existing $110,000.00 mortgage to allow for an increase of $35,000.00 which will take the loan to $145,000.00, terms and conditions to be the same as existing documentation.

Please find enclosed the original Cameron Brothers Valuers confirmation of Progress Draw Number 1 for the unit development at the abovementioned site. It is for an amount of $52,660.00.

DISBURSEMENT OF FUNDS

The $35,000.00 advance will be disbursed as follows:—

$10,000.00 Payable to the Builder - J. Tang Construction$100 Payable to the Cameron Brothers Valuers$TBA Purvis Duncan Solicitors Legal Costs and Outlays$ Balance To be held in Purvis Duncan's Trust Account to be

disbursed on Private Mortgage Lending Limited's instructions.”

In the light of this letter and that of 13th February 1995 I found Mr McLeod's denial that PDMS had any means of knowing that the project might not have been able to proceed if funds were withheld, disingenuous.

On 18th April the respondent executed another letter of acceptance addressed to Purvis Duncan. In that letter, he directed the solicitors to pay the amount of the increased loan under 4 headings. J. Tang Construction and Cameron Brothers were to be paid the amounts referred to above. Purvis Duncan were to receive $1,350.00 for costs and outlays. The balance, $23,550.00, was to be held in the Purvis Duncan trust account “to be disbursed in accordance with the written directions of the mortgagor”. The respondent subsequently authorised payments of approximately another $10,000.00, but there is no evidence of any authority for disbursement of the remainder.

Next day, 19th April 1995, Purvis Duncan transferred the Gauls' $26,000.00 and $9,000.00 of Mr Chapman's $10,000.00 from their respective accounts in the Purvis Duncan trust account ledger to that of PDMS. Again, the amount transferred was described in the ledger as “Advance monies”. They paid the builder and the valuer as directed; and applied a further $1,293.00 for their own costs and outlays. In July 1995, $6,000.00 was paid to The Queensland Building Services Authority and in August some small amounts were paid for valuation fees and for solicitors' costs and outlays. Most of the remainder, over $16,300.00, was paid to PML between July and November 1995, together with the balance of $4,023.00 from the first loan, purportedly as “interest”. Counsel for PDMS conceded in written submissions that three of the “interest” payments were paid out of the trust account without the respondent's authority.

There is some evidence that up until early 1996, PML was generally collecting interest on behalf of those whom it had induced to advance money; but there is no evidence that the lenders in this case authorised PML to handle the interest on their behalf, nor that they authorised Purvis Duncan to make interest payments out of capital which, according to the solicitors, was held by PDMS on their behalf. It does not appear that the solicitors ever informed them that interest payments were being met from

their capital. It is worth noting, however, that Mr McLeod explicitly denied that Purvis Duncan was involved in the interest collection process prior to February 1996. On the face of the trust account ledger, that is not true.

The evidence does not disclose when building work came to a halt, nor the value of the work completed at that time. I infer it ceased some time in the first half of 1995. Mr McLeod asserted that no further advances were made because the lending ratio was exceeded, but in the absence of a valuation, the ratio could not have been known. Whether funds were available is not apparent from the evidence.

PML's dealings with Mr McLeod were not limited to his capacity as a partner of Purvis Duncan and director of PDMS. In cross-examination, the respondent put to Mr McLeod a series of letters addressed to Mr McLeod's wife, Mrs J.S. McLeod, one of which was addressed “care of Purvis Duncan Solicitors Attention Ross McLeod”. These letters purported to remit amounts of almost $5,600.00 from PML to Mrs McLeod. At first, Mr McLeod asserted that the letters constituted a series of invoices upon which only one payment was made to his wife. That payment, he said, related to an introduction by her of investors named Barnes and Nafras Pty Ltd to PML. Cross-examined by Mr Marquart, he explained that payment this way:

“My wife initially rang PML at some stage and wishing - or she was considering making an investment with PML herself and she was offered an opportunity, as were a lot of other representatives, to be paid a commission for introducing various investors to Private Mortgage Lending Limited and there was one payment made which was made at some stage. It certainly does not involve your loan. It was other funds from another entity all together.”

Later Mr McLeod described the money as “a spotter's fee”. He asserted that the money was paid to his wife “in her own capacity as an introducer of funds”. He saw no relationship between these payments and his assertion that the only benefit Purvis Duncan got from the transaction was its fees

for preparing documentation. Closer examination of the documents disclosed that, while the lenders may have been associated with each other, there were seven different transactions involving over half a million dollars. Mrs McLeod was sent three separate payments in June and October 1995 and January 1996. There was no explanation of why $2,290.00 of the payments was paid in cash rather than by cheque. Mrs McLeod gave no evidence.

The activities of PML, perhaps not surprisingly, attracted the attention of the Australian Securities Commission. The Commission formed the view that PML was prima facie engaged in illegal fundraising. On 19th January 1996, the Commission informed PML that in its opinion, PML was offering prescribed interests in contravention of the Corporations Law. PML was given an opportunity to obtain legal advice. It neither made application to register a prospectus nor made any submission to show that it was not required to do so. On 2nd February 1996 the Commission formally required an undertaking by PML to cease all advertising and offering of prescribed interests and (in effect) to cease dealing in interest payments. It threatened proceedings for an injunction and/or the appointment of receivers if the undertakings sought were not provided. Apparently PML complied with the requirements of the Commission. It wrote to the respondent on 5th February advising that future interest payments should be made direct to Purvis Duncan and on the same day requested Purvis Duncan to attend to “all interest arrangements” in accordance with the ASC requirements.

There were a number of reasons for the ASC's actions. They included the fact that the audit report for the period ending 30th June 1994 on PML was qualified in these terms:

“We have been unable to determine between 30 June 1994 and the date of this report, whether the company has been trading profitably. Subsequent to the end of the financial year, the accounting and other records of the company have not been kept in a suitable form such that

it is possible to establish the current financial position.”

The Commission noted that O'Toole had twice between discharged from bankruptcy prior to becoming a director of PML. It also noted a number of related party transactions, particularly joint venture agreements between PML and borrowers, which had not been disclosed to lenders.

Whether because of the requirement to cease advertising or for some other reason, PML appointed an administrator in June 1996, and less than a month later its creditors resolved that it be wound up.

This evidence satisfies me that Mr Marquart has an arguable case that PDMS was at all material times the agent of PML or was otherwise affected by PML's conduct; and that PML was guilty of breach of contract and misleading or deceptive conduct. Whether it is possible to make out a case of fraud on the part of PML, I cannot say. I am also unable to form any rational estimate of the amount of damages which the respondent might recover from PML. It is also arguable that the lenders lent their money to PML or PDMS and are creditors rather than beneficiaries. I note that the applicant relied only on the existence of an express or implied trust, not a constructive trust.

There are two other arguments to which I should refer. The first was raised by Mr McLeod in correspondence but was not relied upon in argument before me. It was asserted that the respondent was in breach of the terms of the mortgage because he entered into a joint venture agreement for the development of the land with PMF. The evidence does not satisfy me that there was any genuine joint venture; but in any event, this argument succumbs to the existence of the arguable case described above. Second, it was submitted that under the terms of the offer from PMF, the respondent was not entitled to receive funds if the “loan to value ratio” exceeded 69%. It was submitted that this would have prevented the respondent receiving further funds, as the ratio was, it was submitted, exceeded after the second

advance. It suffices to say that the evidence before me does not demonstrate a factual basis for the second submission. Precisely what the value would have been at the time the funds were due to be provided is not disclosed. In any event, it might be necessary to examine whether, given the large “up front” payments to PML, the situation was brought about by the conduct of PML. It might have been mathematically impossible to avoid infringing the ratio, in which case it would be necessary to construe the term in the light of the upfront payments which the contract provided for. I do not think the ratio clause argument provides a sufficient reason to doubt the arguability of the respondent's case.

I have set out the evidence which has led me to these conclusions at some length, probably at greater length than is ordinarily warranted in a case of this sort, because of the fact that the respondent has been unrepresented. The difficulties which confront a judge in such a situation are well known. Inevitably, during the hearing, I was obliged to some degree to descend into the arena and to ask more questions than ordinarily I would ask. A number of those questions have produced answers which are reflected in the foregoing account. I am very conscious of the risk of becoming intellectually committed to a view by that process of asking questions. I have endeavoured to avoid becoming thus committed, but have thought it best to set out the evidence at some length, so that others may judge whether my endeavours have been successful.

Because of the nature of the proceedings it is also undesirable that I say too much on issues of credibility. It is, however, necessary that I say something. I did not find the evidence of either Mr Wilson or Mr McLeod satisfactory. There may have been some excuse for Mr Wilson's vagueness - it is three years since he worked at Purvis Duncan. I saw no excuse for Mr McLeod's often argumentative and less than frank approach. Since all that the respondent must do is establish the existence of an arguable question to be tried, I will say no more.

Balance of convenience

When one turns to the question of the balance of convenience, the most unusual feature of this case becomes relevant. That feature is the fact that both parties wish to sell the subject land. The dispute seems to be about who should sell it. There is also a dispute about what should happen to the proceeds of sale. The respondent submits that if he is not to have them, they should be paid into court. The applicant submits that it is entitled to sell the land and retain the proceeds.

Consistently with its assertion that it holds the mortgage as bare trustee for the lenders, the applicant proposes to distribute the net proceeds of sale among the lenders. It not only asserts an entitlement to do this; it submits that the lenders' need for the money is a factor in favour of the course which it proposes, taking the interests of third parties into account in relation to the balance of convenience. On this submission, the fact that PDMS has no funds of its own is irrelevant.

The respondent contends that he will be able to enter into a contract for a higher price, albeit only slightly higher, than will be obtained under the applicant's contract. However, there is no affidavit by the proposed buyer to support this submission.

Removal of the caveat would not, by itself, enable the respondent to sell the land. He would not be able to give a clear title to it without paying out PDMS and the second mortgagee or obtaining an order requiring PDMS pending trial to accept a sum in court as substitute security for its mortgage. There are no proceedings on foot directed toward that end, and a course which would require the institution of further proceedings is not one which would be favoured on the balance of convenience.

In my judgment, the proper course to take in this case is to order the removal of the caveat upon conditions. This will enable the mortgagee's contract to be completed. Since

the price under the contract is less than PDMS's claim, no part of the net proceeds of sale will be immediately available for the second mortgagee. I do not think PDMS should be permitted to dissipate the funds. In a sense, the land is presently available as security for the claim of each party against the other. That position should be preserved. In my judgment, the proceeds of sale after expenses should be paid into court, to abide the outcome of the respondent's action currently on foot against the applicant. This will also protect the position of the second mortgagee.

This will mean that the respondent's action must proceed to trial. I cannot emphasise how important it is that the respondent should obtain legal representation for that purpose. His case will necessarily involve complex factual investigations and pleading and proving complex propositions of law. It is a task quite beyond a lay person and perhaps even an inexperienced lawyer. Only if he has experienced legal representation can his case be properly dealt with, and only then is there any prospect of a sensible resolution of it. If he cannot be provided with proper legal representation, there is every likelihood that eventually it will have to be struck out, for it is not the function of the court to formulate the respondent's case for him. If it proceeds to trial, it may confidently be expected to take much longer than it would take if the respondent were represented and to waste the resources of the court, as well as those of PDMS and any others who may be joined. The trial judge will be confronted with the difficulties involved in remaining dispassionate which such a situation always produces, but in a particularly acute form. In these circumstances I think I should impose conditions to ensure that the payment into court is not a waste of time, by requiring the applicant to seek Legal Aid or other assistance from lawyers. I can hardly imagine a case where the need for legal aid is greater than here; but of course, the decision whether to grant it is for others.

I will hear the parties on what orders should be made to give effect my decision and what consequential directions if any should be made in the respondent's action.

Powered by TCPDF (www.tcpdf.org)