hedging against uncertainty in e-payments: what cfo's … webinar... · hedging against...

TRANSCRIPT

Hedging against uncertainty in e-Payments: What CFO's need to know for 2012

Presented in partnership with:

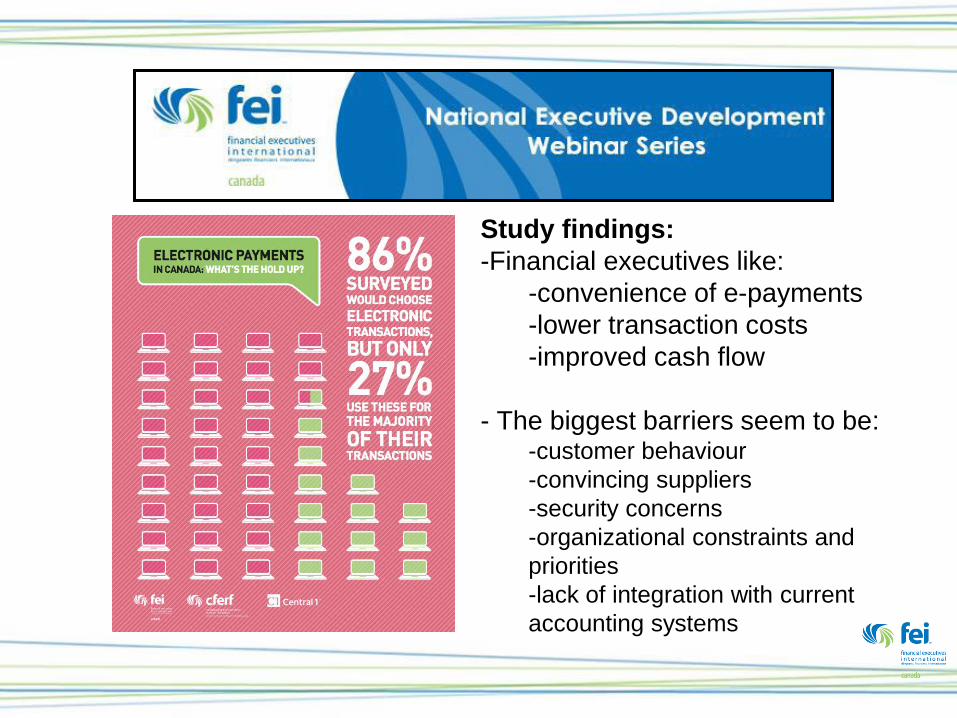

Study findings:

-Financial executives like:

-convenience of e-payments

-lower transaction costs

-improved cash flow

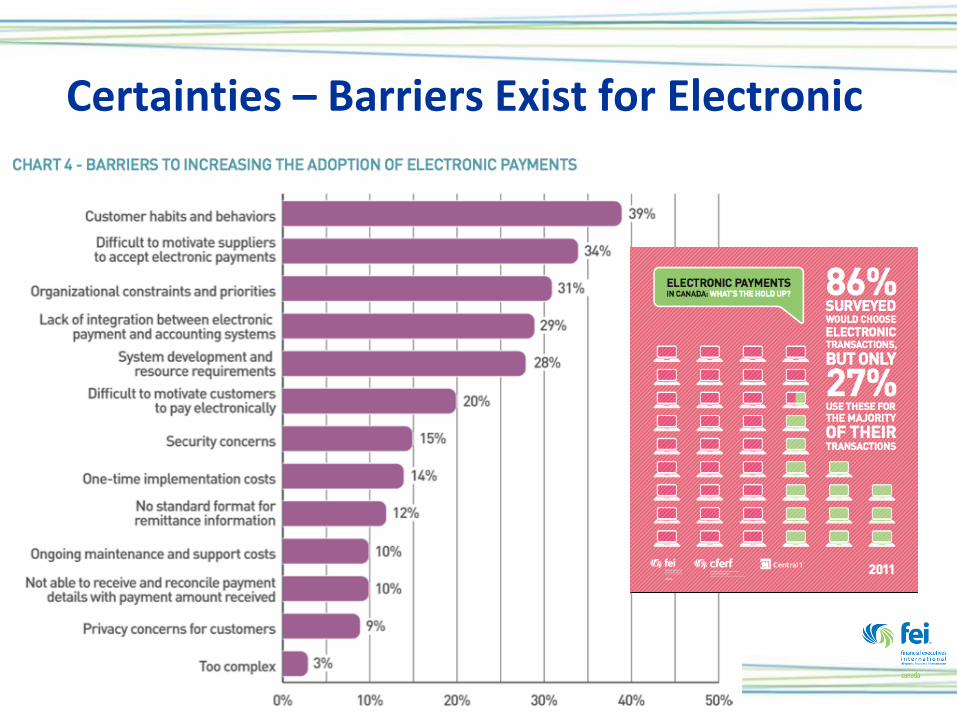

- The biggest barriers seem to be: -customer behaviour

-convincing suppliers

-security concerns

-organizational constraints and

priorities

-lack of integration with current

accounting systems

Presenters: • Oscar van der Meer, Chief Technology & Payments Officer, Central 1

• Doug Kreviazuk, VP Policy & Public Affairs, Canadian Payments Association

• Kirkland Morris, Vice-President, Enterprise Strategy, Interac Association/ Acxsys

Moderator: Michael Conway, CA, Chief Executive and National President, FEI Canada

Oscar van der Meer Chief Technology & Payments Officer

Payments Business

May/June 2010

Certainties - Cost

• The cost of moving traditional payments is expensive AND increasing

5

Source: Canadian Payments Association

Certainties – Barriers Exist for Electronic

Polling Question

Who should take the lead to work on reducing these barriers?

A. Government

B. Financial Institutions

C. Your company

Uncertainty – Innovation & Change

• System, policy, standards – Task Force for the Payments System Review - standards

– Voluntary code of conduct for the credit and debit card industry

– PCI Compliance

• Mobile – Near Field Communication (NFC) & Person-to-Person (P2P)

– Mobile acquiring

• Cheque Images – Cheque replacement document

– Remote deposit

Uncertainty – Investment

& Risk

Consider for your payments strategy

• Part A - Manage your cost surrounding cheque processing

• Part B – Invest strategically/selectively in electronic processing

Consider for your payments strategy Part A

• Manage costs around cheques

– Audit current payment operations • Cheque returns

• Cheque archiving and retrieval

• OCR & imaging

• Fraud management

Consider for your payments strategy Part B

• Invest strategically/selectively in electronic processing

– External Barriers • Increasing uptake/consumer behaviour

– Research with your customers

– Incentives or disincentives for clients and suppliers

» Offer faster payment processing for electronic

» Offer discounts

» Charge administration fees

– Usability/account validation

– Security perceptions

Consider for your payments strategy Part B

• Invest strategically/selectively in electronic processing

– Internal Barriers • Reconciliation/internal process

– Use email in the interim to advise supplier of invoice(s) being paid

– Experiment with electronic invoicing

– Establish internal validation systems to match payments

– Leverage account validation routines

Consider for your payments strategy Part B

• Invest strategically/selectively in electronic processing

– Take Action — Walk before you run • Test & learn — Pilot projects

• Practice what you preach — start by adopting electronic payments internally for payroll and expense reports

• Talk to your vendors of core systems

• Explore new payments options e.g. eTransfers

• Get involved in the discussion

Polling Question 2

Does your company have an active program in place to reduce the number of cheques you either receive or send?

A. Yes

B. No

C. Partially

16

Getting ready for 2012: Update of the work of the Task Force for the

Payments System Review and the CPA’s Payments Strategy

Doug Kreviazuk Vice-President, Policy & Public Affairs Canadian Payments Association

Payment System Review

Has focused its work on:

• Safety, soundness & efficiency

• Innovation

• Competitive landscape

• Needs of consumers & businesses

• Review of oversight mechanisms

17

Market Gaps

• Overarching & common regulation across all payments

• Limitations of CPA’s mandate

• Access & participation within the clearing system

• Straight-through processing (i.e. user to user)

• Enhanced remittance data

• Interoperability with other/global payments systems

18

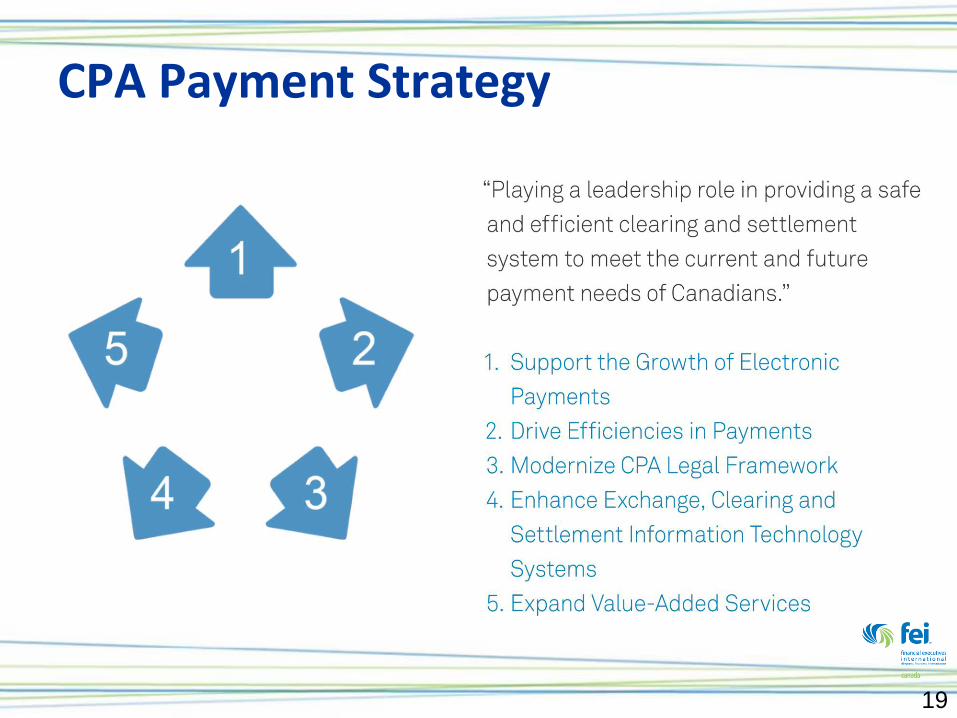

CPA Payment Strategy

19

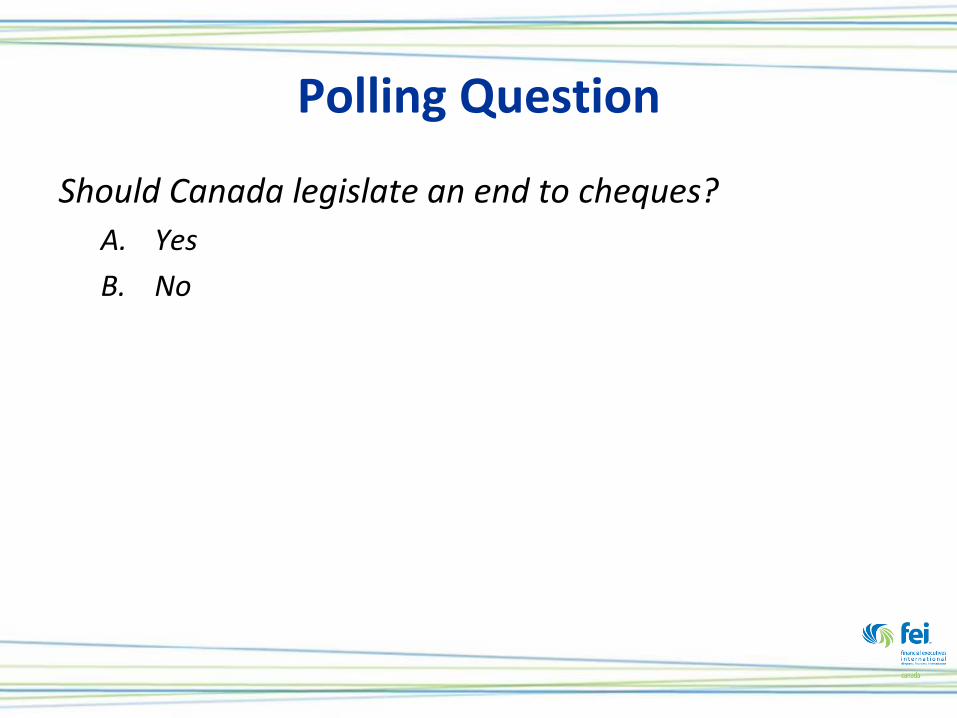

Polling Question

Should Canada legislate an end to cheques?

A. Yes

B. No

Pillar 1: Electronic Payments

21

• Improving electronic bill payments

• Facilitating contactless payments at the point-of-sale (POS)

• Focus on mobile payments

• Enhancing the framework for online payments

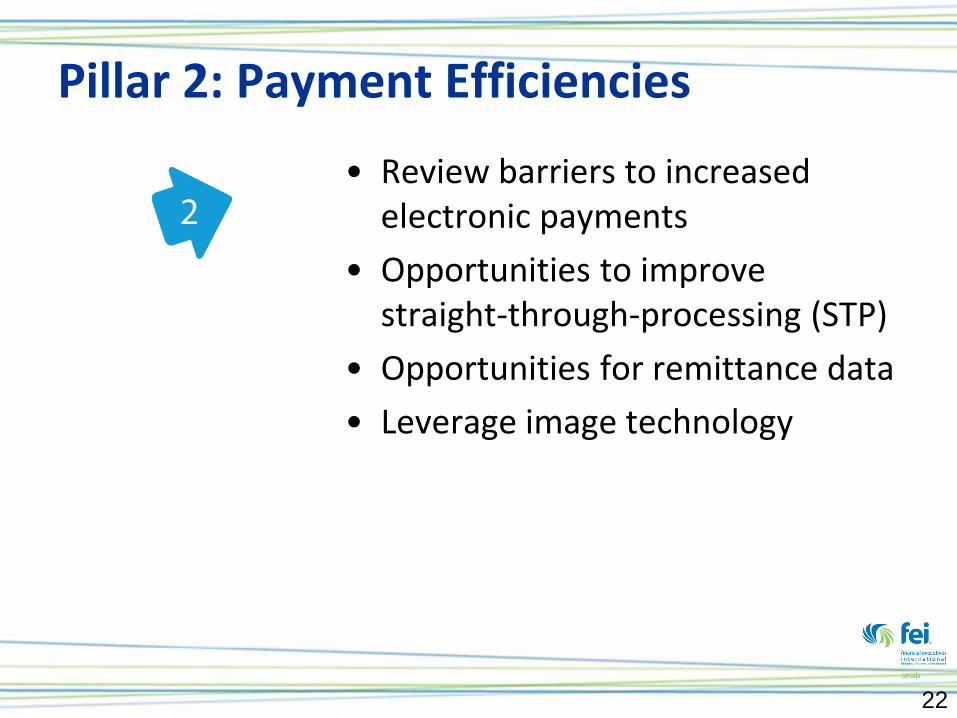

Pillar 2: Payment Efficiencies

22

• Review barriers to increased electronic payments

• Opportunities to improve straight-through-processing (STP)

• Opportunities for remittance data

• Leverage image technology

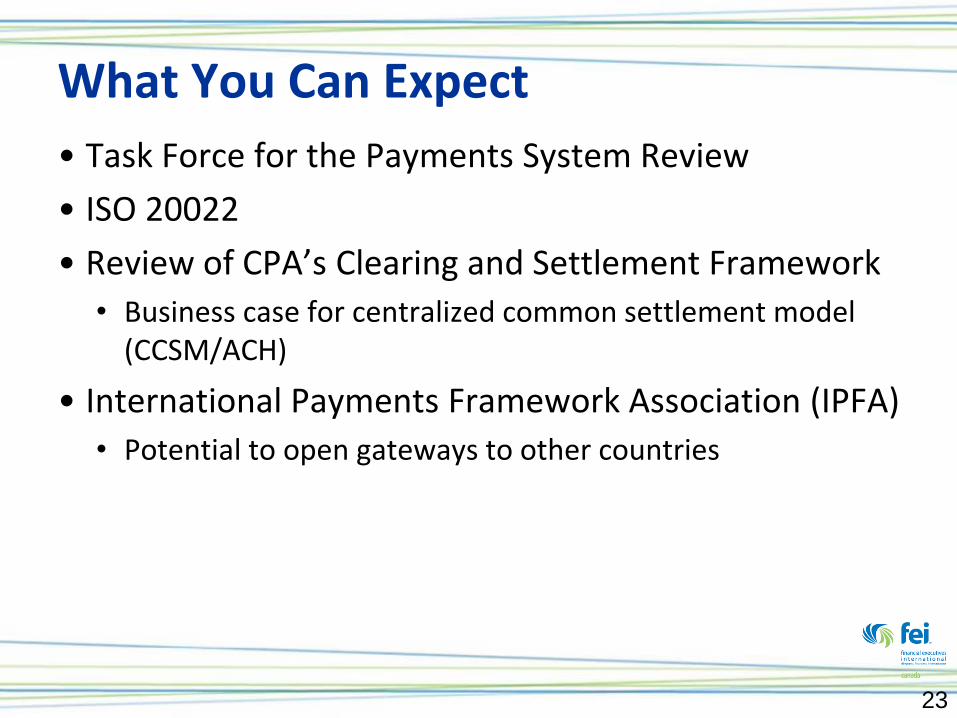

What You Can Expect

• Task Force for the Payments System Review

• ISO 20022

• Review of CPA’s Clearing and Settlement Framework

• Business case for centralized common settlement model (CCSM/ACH)

• International Payments Framework Association (IPFA)

• Potential to open gateways to other countries

23

24

Kirkland Morris Vice-President, Enterprise Strategy Interac Association / Acxsys Corporation

The Payments Landscape – An INTERAC Perspective

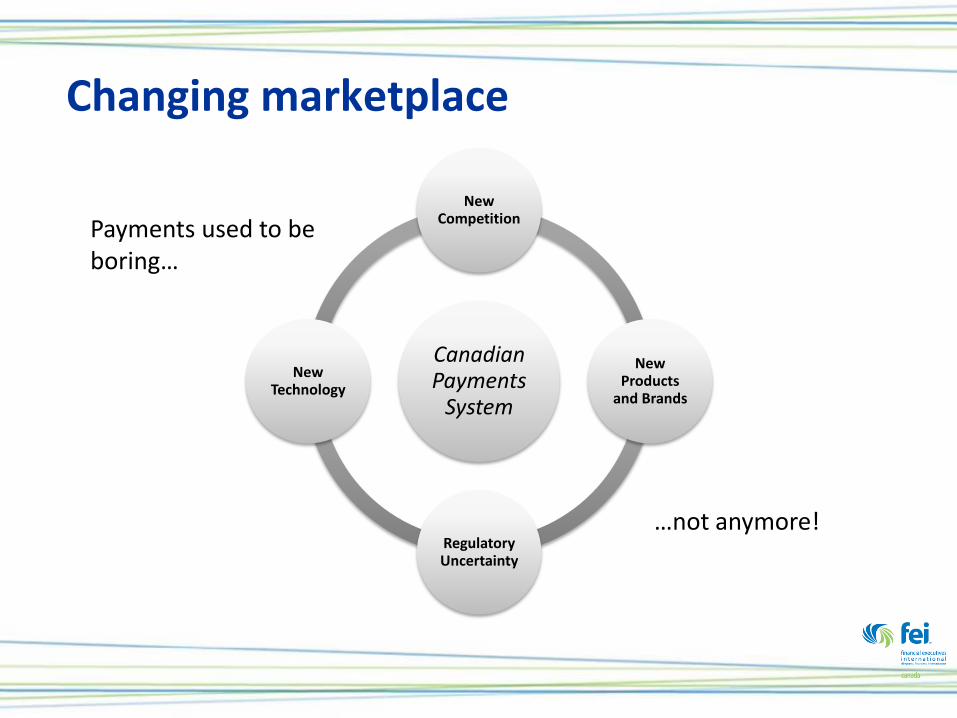

Changing marketplace

Canadian Payments

System

New Competition

New Products

and Brands

Regulatory Uncertainty

New Technology

Payments used to be boring…

…not anymore!

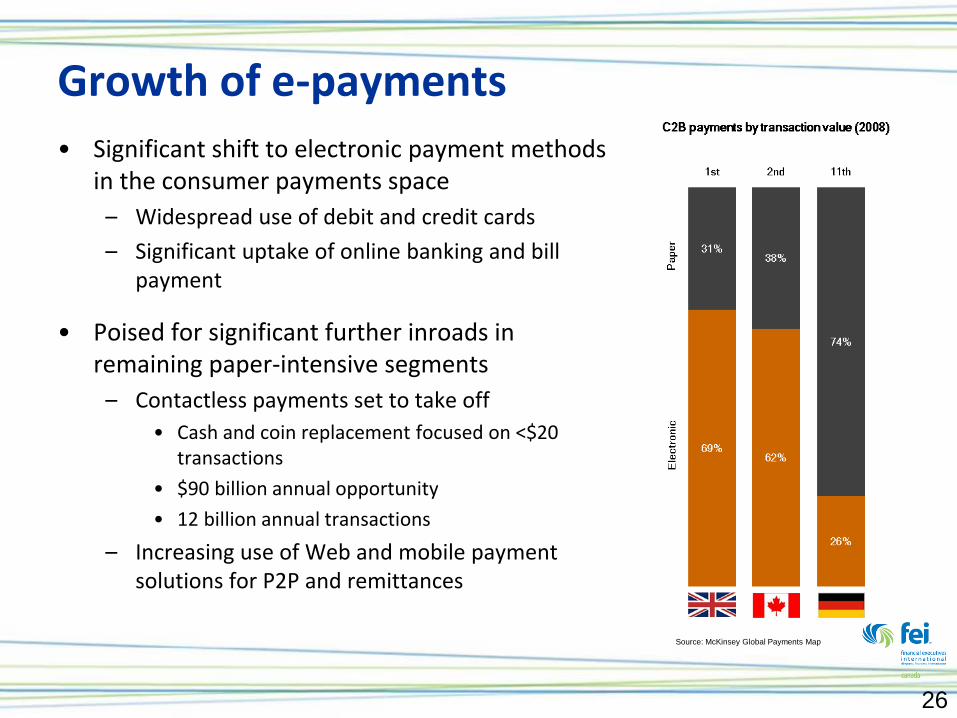

Growth of e-payments

• Significant shift to electronic payment methods in the consumer payments space

– Widespread use of debit and credit cards

– Significant uptake of online banking and bill payment

• Poised for significant further inroads in remaining paper-intensive segments

– Contactless payments set to take off

• Cash and coin replacement focused on <$20 transactions

• $90 billion annual opportunity

• 12 billion annual transactions

– Increasing use of Web and mobile payment solutions for P2P and remittances

26

Source: McKinsey Global Payments Map

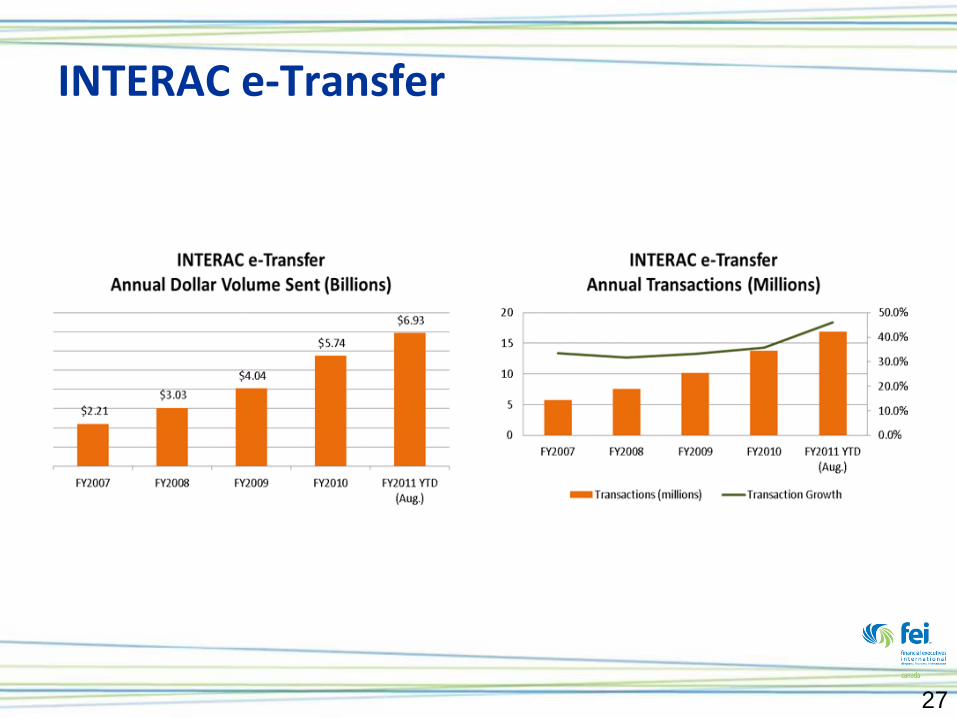

INTERAC e-Transfer

27

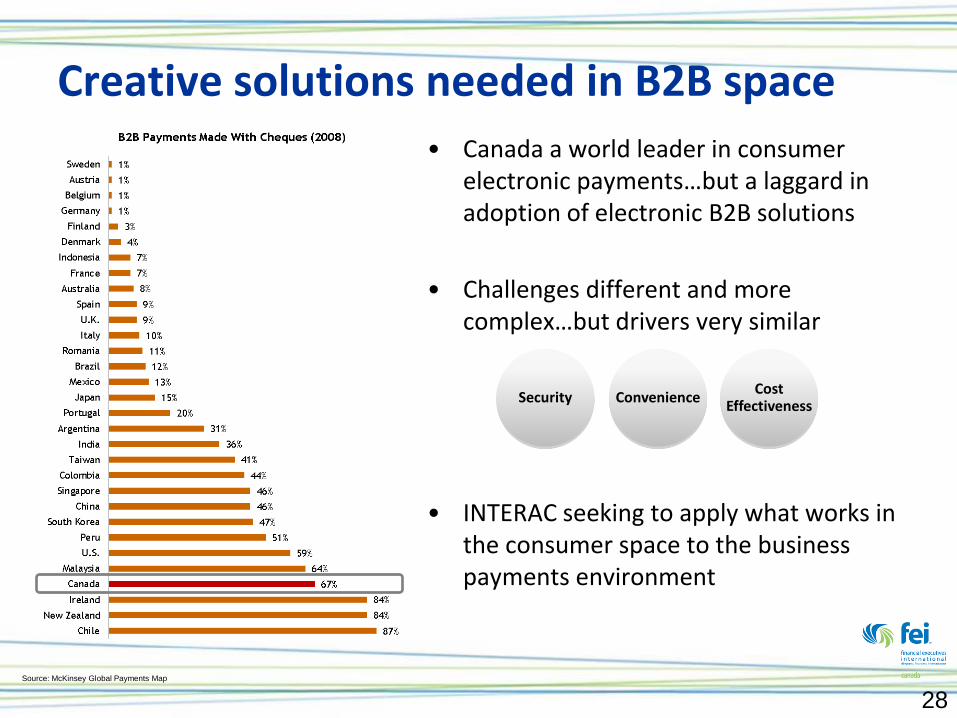

Creative solutions needed in B2B space

28 Source: McKinsey Global Payments Map

• Canada a world leader in consumer electronic payments…but a laggard in adoption of electronic B2B solutions

• Challenges different and more complex…but drivers very similar

• INTERAC seeking to apply what works in the consumer space to the business payments environment

Security Convenience Cost

Effectiveness

Looking ahead to 2012

• Significant uncertainty across the payments landscape

• Some things will become clearer in the year ahead – Task Force report due at year-end

– Consumer response to contactless payment will be evident

– Mobile payments trials in Canada and elsewhere will help shape use cases, business models, value propositions

• But, we are a long way from equilibrium – Government response to the Task Force and potential public policy decisions?

– Mobile payment adoption and who will win?

– Solving the security and fraud challenge with next generation authentication?

– Finding the right formula for B2B?

29

Questions ?

30