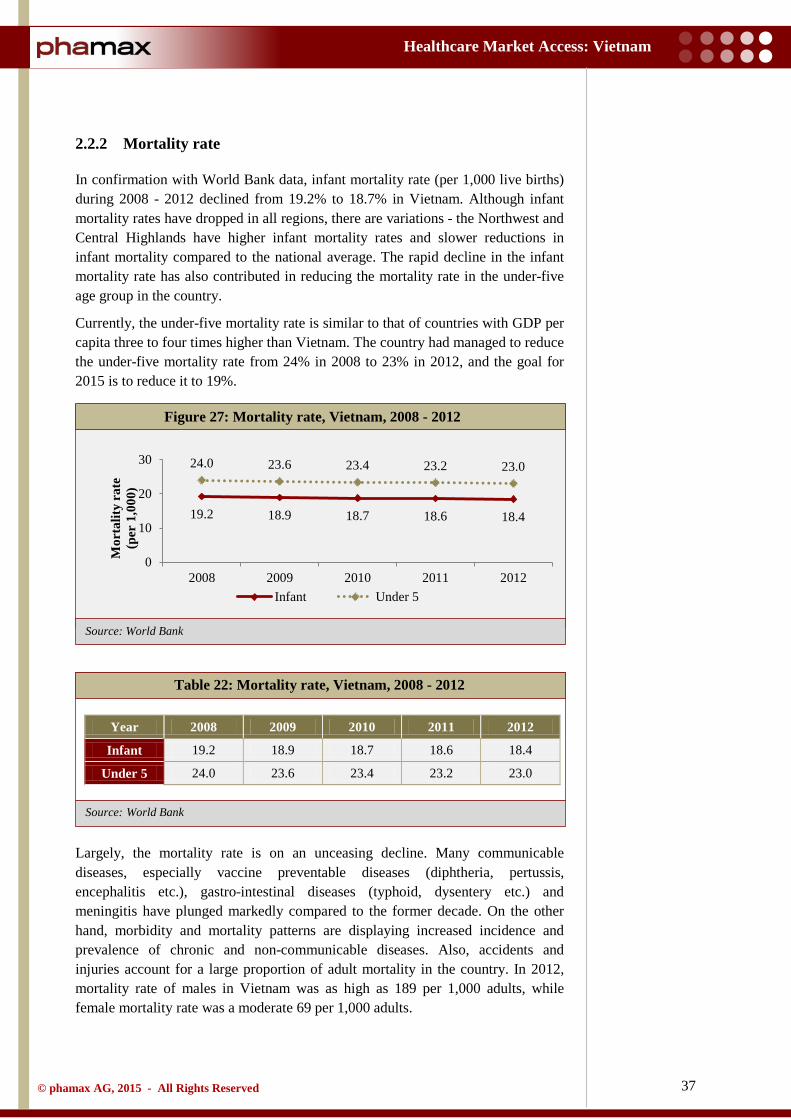

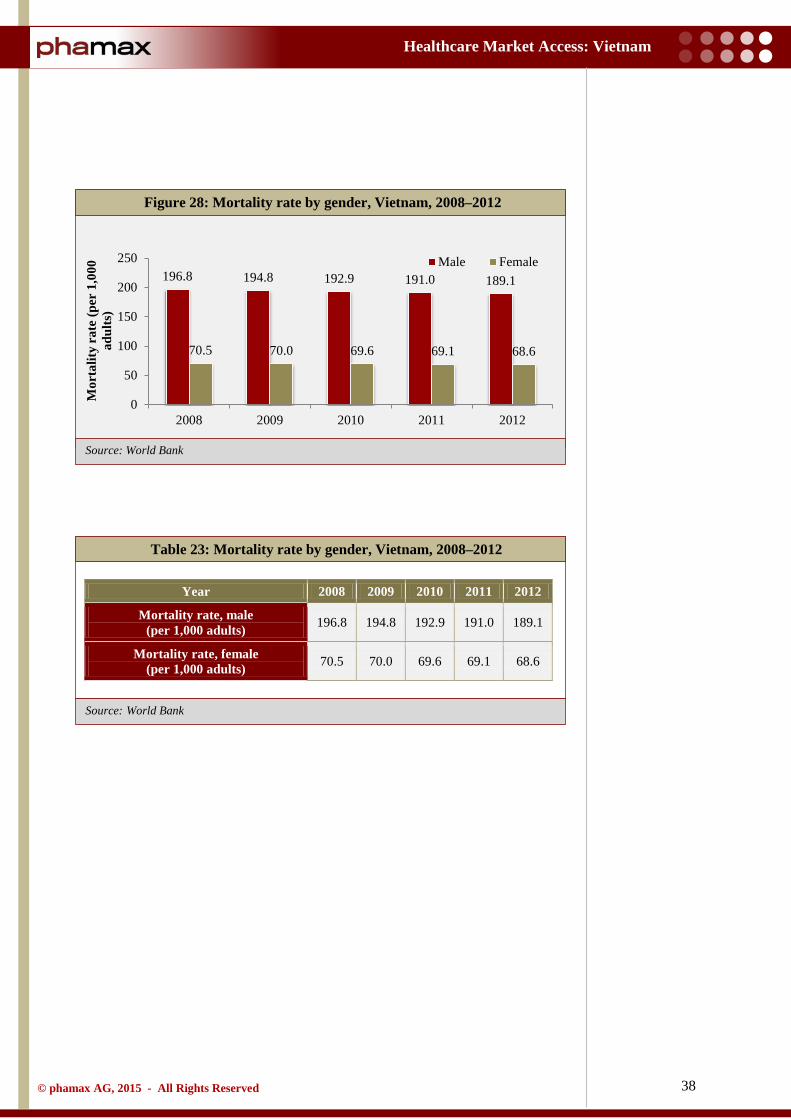

healthcare market access: vietnam - phamax · 1.3 demographics ... 2009 - 2012..... 22 table 15:...

TRANSCRIPT

2

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

1. COUNTRY LANDSCAPE ................................................................................................................................... 9

1.1 Economic environment ........................................................................................................... 9

1.2 Economic indicators ............................................................................................................. 10

1.2.1 Gross domestic product ................................................................................................ 10

1.2.2 Gross national income .................................................................................................. 12

1.2.3 Inflation ........................................................................................................................ 14

1.2.4 Foreign exchange reserves ............................................................................................ 16

1.2.5 Current account balance ............................................................................................... 17

1.2.6 Government net debt .................................................................................................... 17

1.2.7 Exchange rate ............................................................................................................... 18

1.2.8 Foreign direct investment ............................................................................................. 19

1.2.9 Trade balance ................................................................................................................ 22

1.3 Demographics ....................................................................................................................... 23

1.3.1 Population ..................................................................................................................... 23

1.3.2 Growth of middle class ................................................................................................. 25

1.3.3 Education and literacy .................................................................................................. 26

1.3.4 Access to internet.......................................................................................................... 27

1.3.5 Employment ................................................................................................................. 27

1.4 Political structure and environment ...................................................................................... 30

1.4.1 Current government ...................................................................................................... 31

1.5 Trade associations ................................................................................................................ 32

1.5.1 Vietnam Pharmaceutical Companies Association ........................................................ 32

1.6 Opportunity and challenges .................................................................................................. 33

2 HEALTHCARE INFRASTRUCTURE ............................................................................................................ 34

2.1 Healthcare system ................................................................................................................. 34

2.2 Health status ......................................................................................................................... 36

2.2.1 Life expectancy............................................................................................................. 36

2.2.2 Mortality rate ................................................................................................................ 37

2.3 Healthcare policy .................................................................................................................. 39

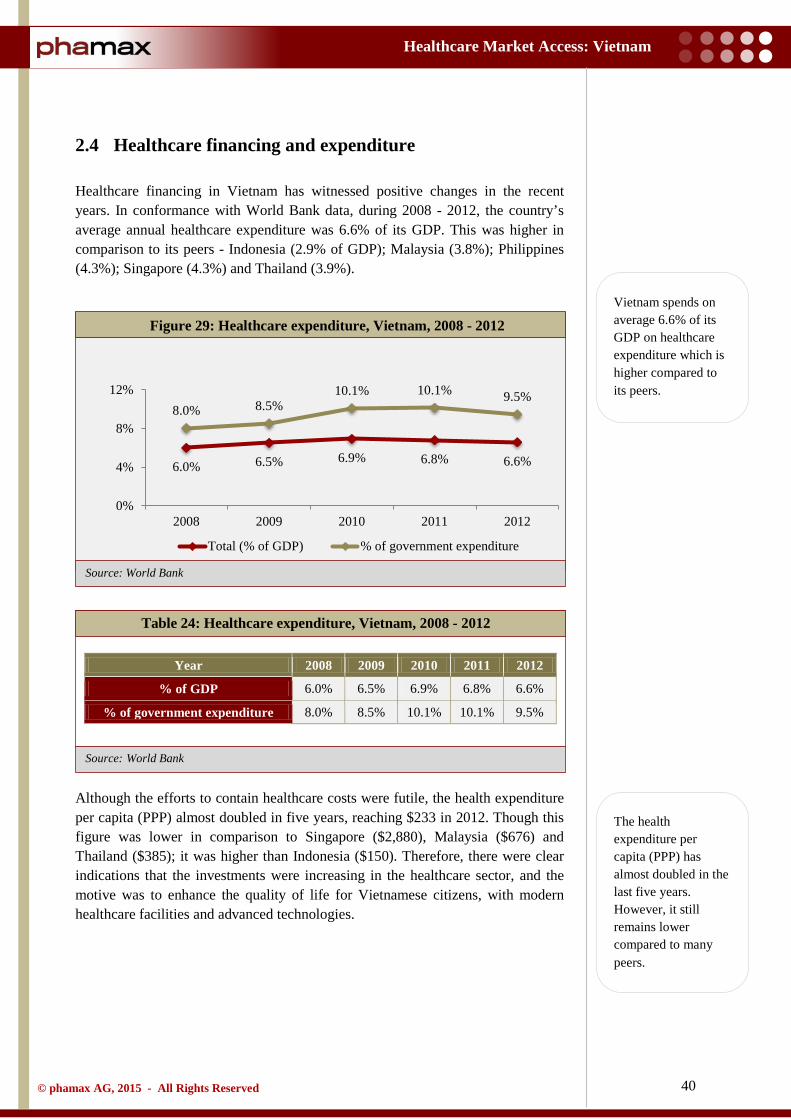

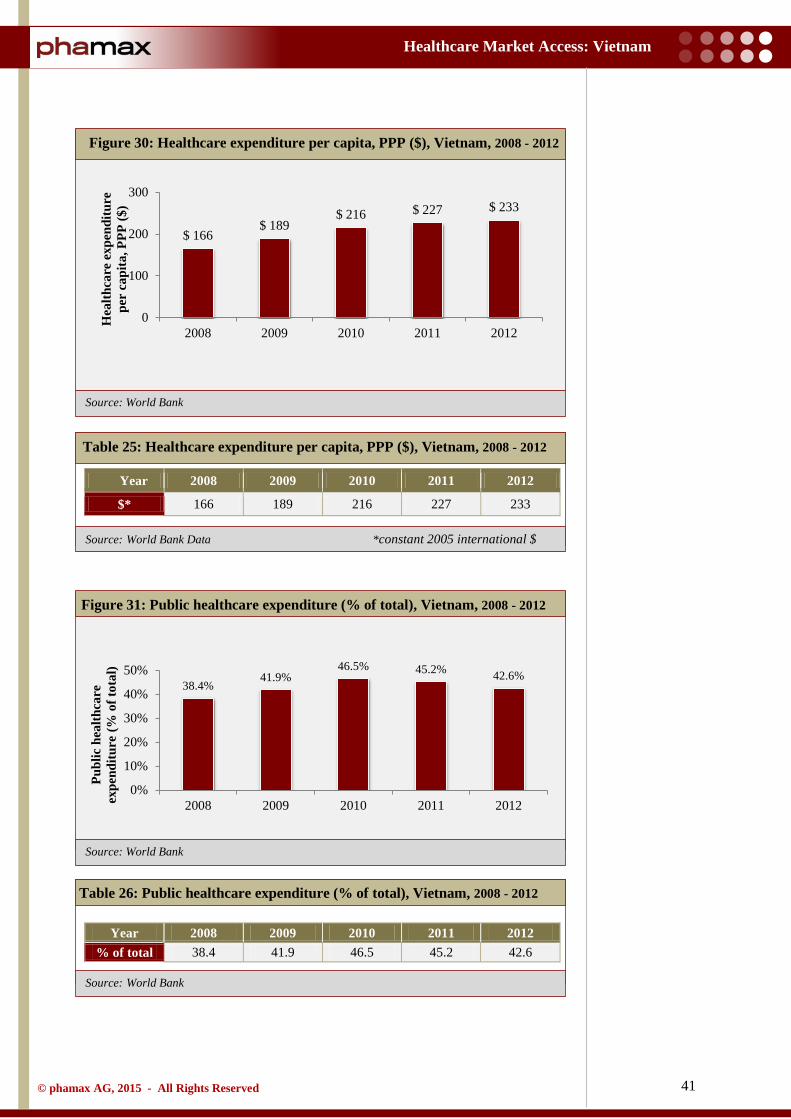

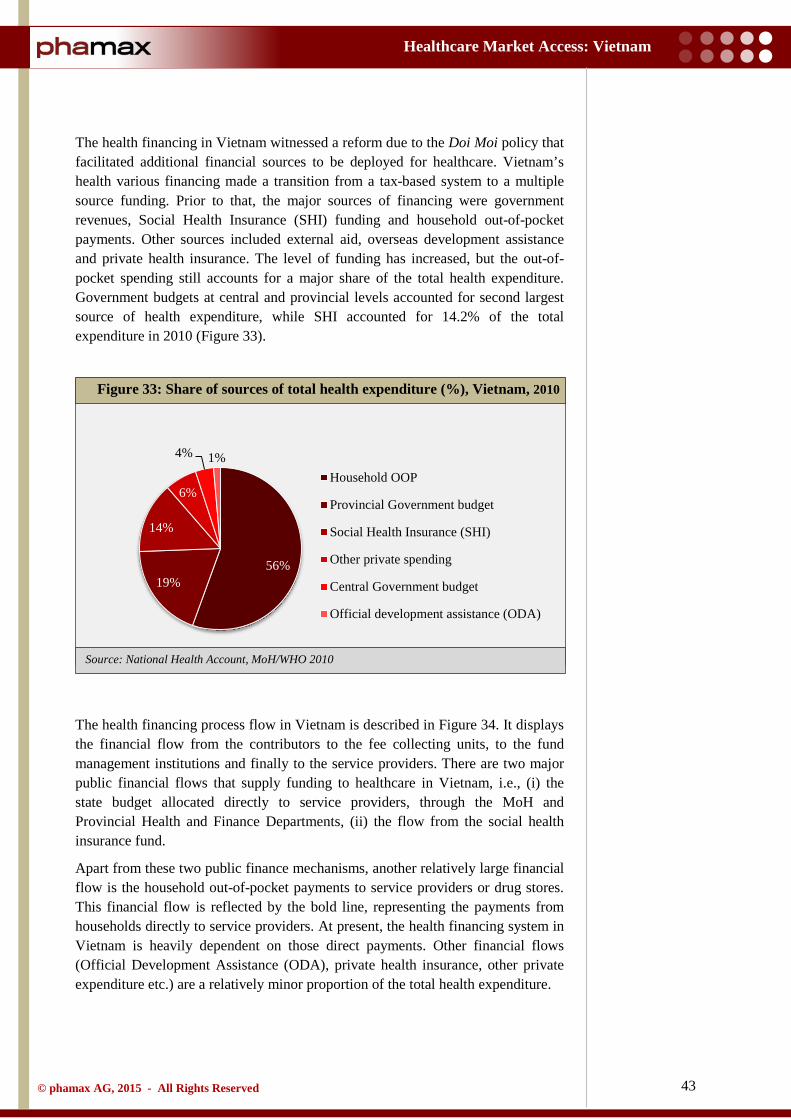

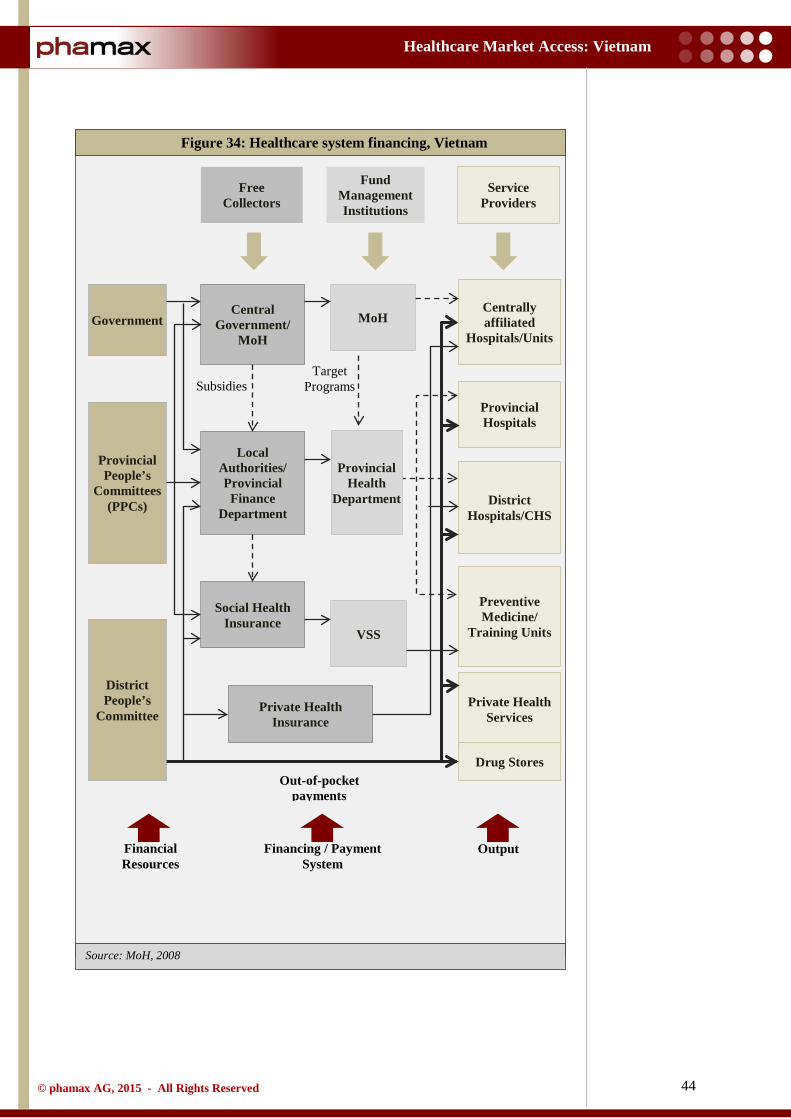

2.4 Healthcare financing and expenditure .................................................................................. 40

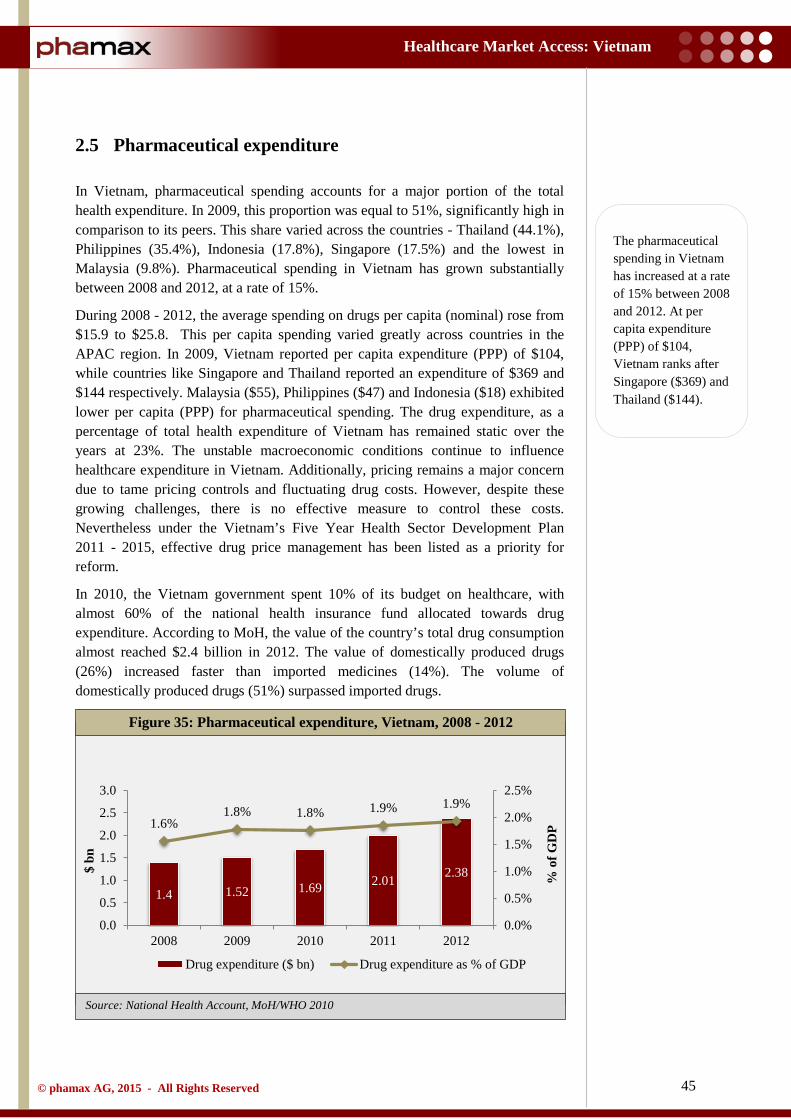

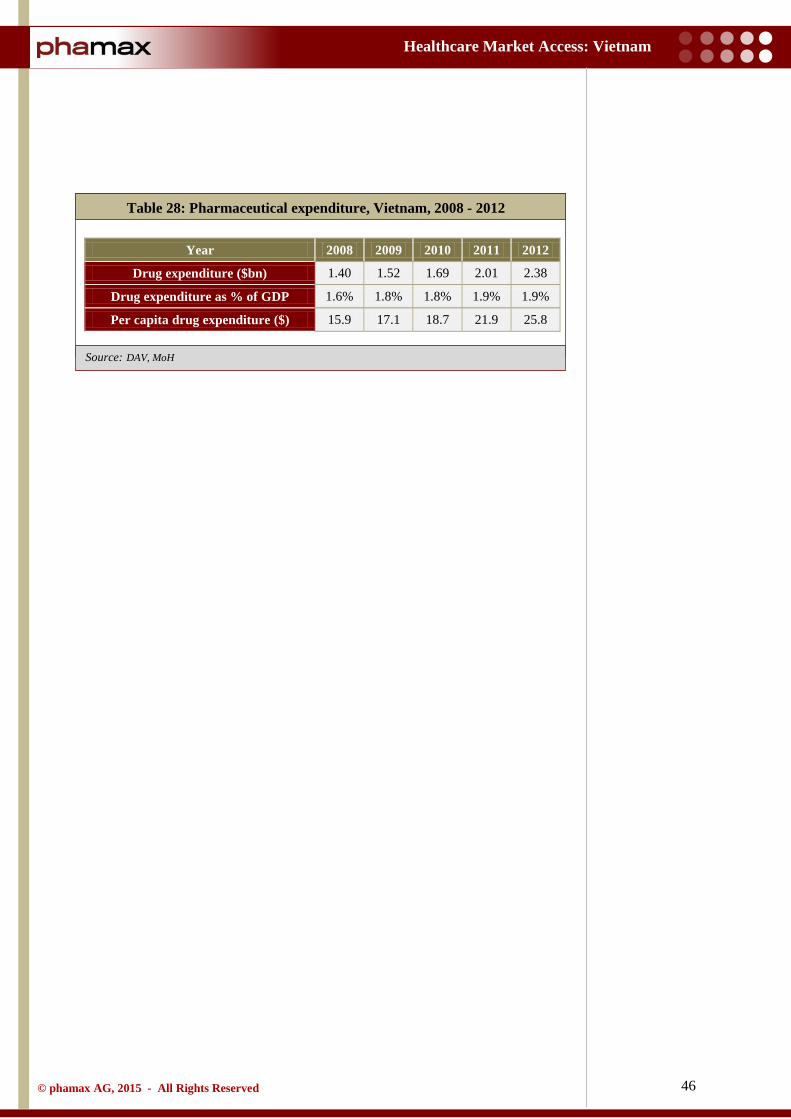

2.5 Pharmaceutical expenditure .................................................................................................. 45

TABLE OF CONTENTS

3

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

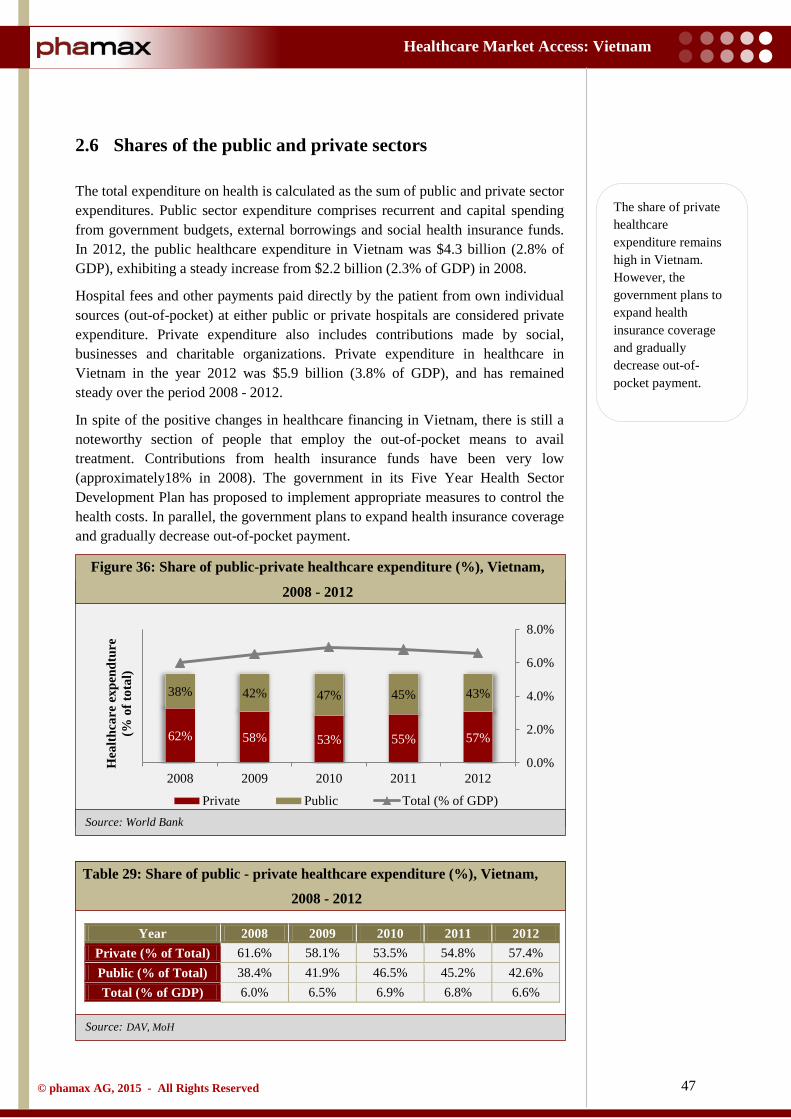

2.6 Shares of the public and private sectors ............................................................................... 47

2.7 Spending in pharmaceutical R&D ........................................................................................ 48

2.8 Health insurance ................................................................................................................... 49

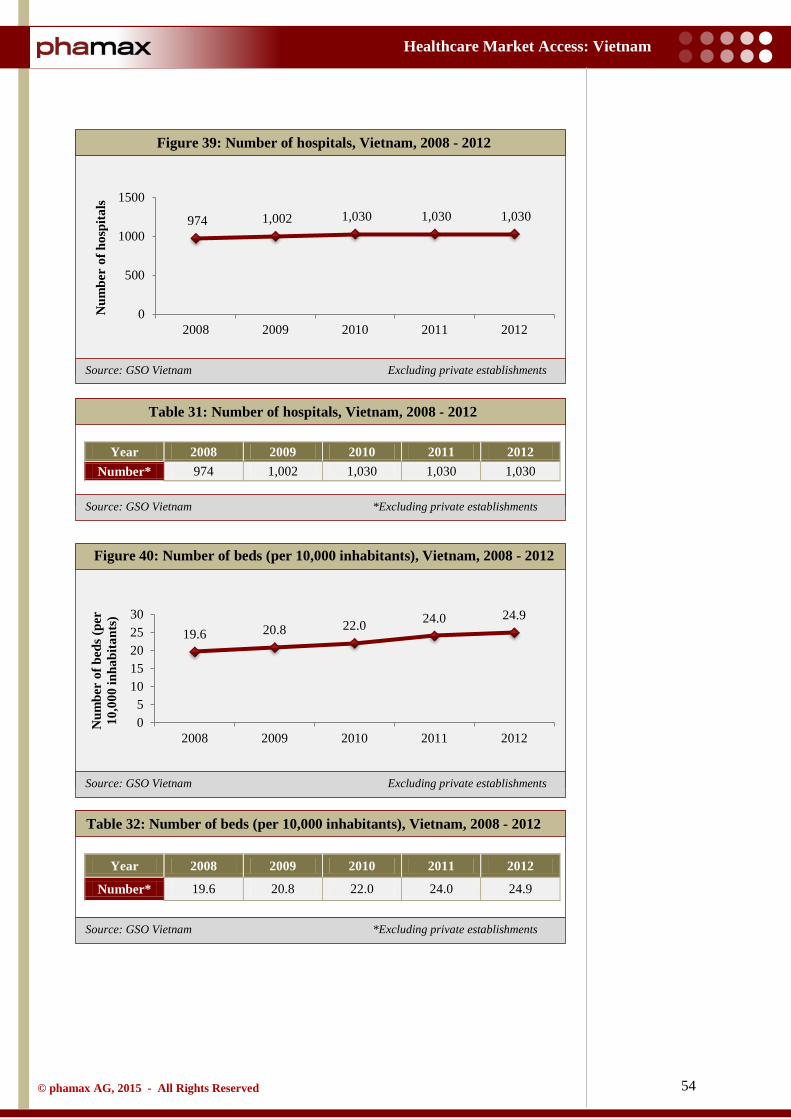

2.9 Hospital sector ...................................................................................................................... 52

2.9.1 Major hospital profiles .................................................................................................. 55

2.9.1.1 Bach Mai Hospital .................................................................................................... 55

2.9.1.2 Cho Ray Hospital...................................................................................................... 56

2.9.1.3 Hue Central Hospital (HCH) .................................................................................... 56

2.9.1.4 Hanoi French Hospital (L’Hôpital Français de Hanoi) ............................................ 56

2.9.1.5 Hospital C in Da Nang .............................................................................................. 56

2.9.1.6 Viet Duc Hospital (Vietnam - Germany Hospital) ................................................... 57

2.9.1.7 Trieu An Hospital (TAH) ......................................................................................... 57

2.9.1.8 Hong Ngoc Hospital ................................................................................................. 57

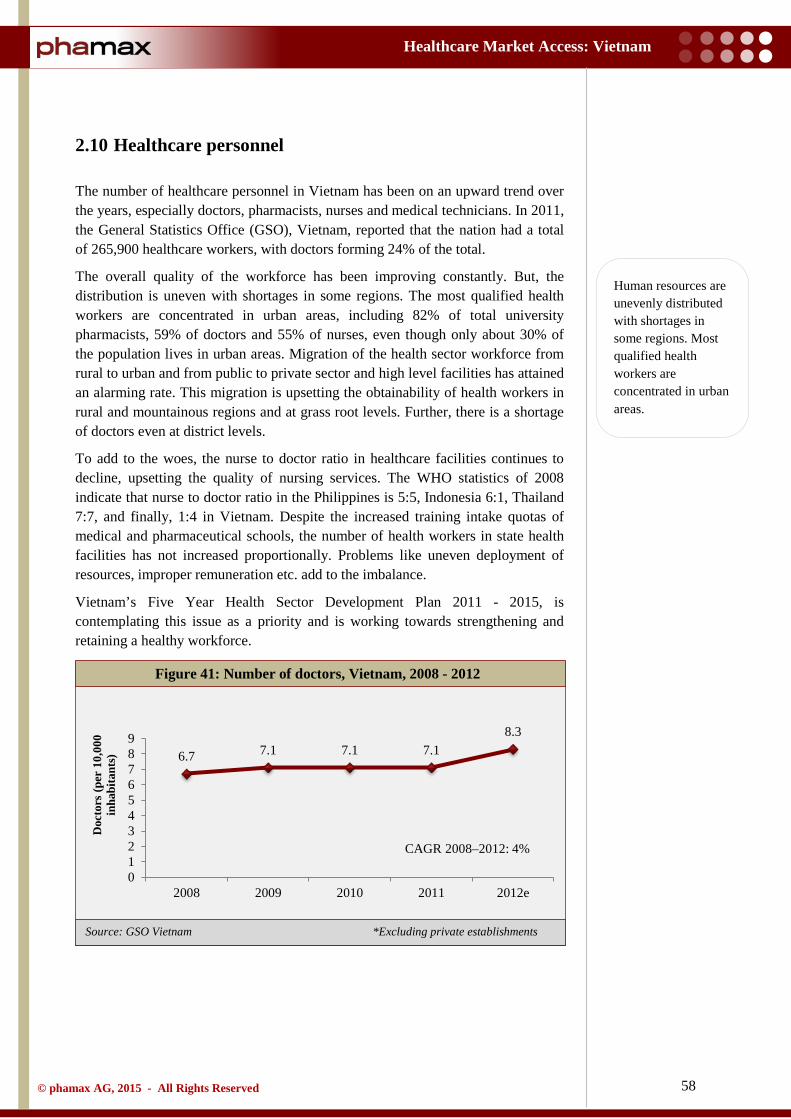

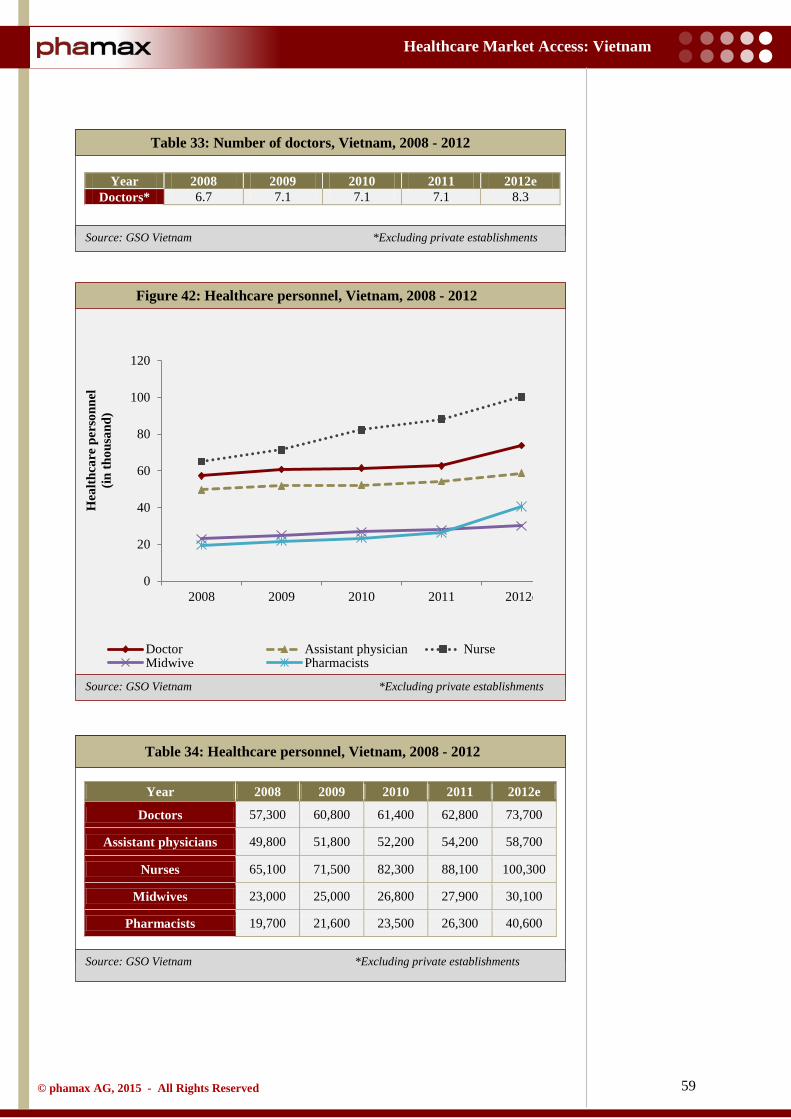

2.10 Healthcare personnel ............................................................................................................ 58

3 OVERVIEW OF PHARMACEUTICAL MARKET ...................................................................................... 60

3.1 Market overview ................................................................................................................... 60

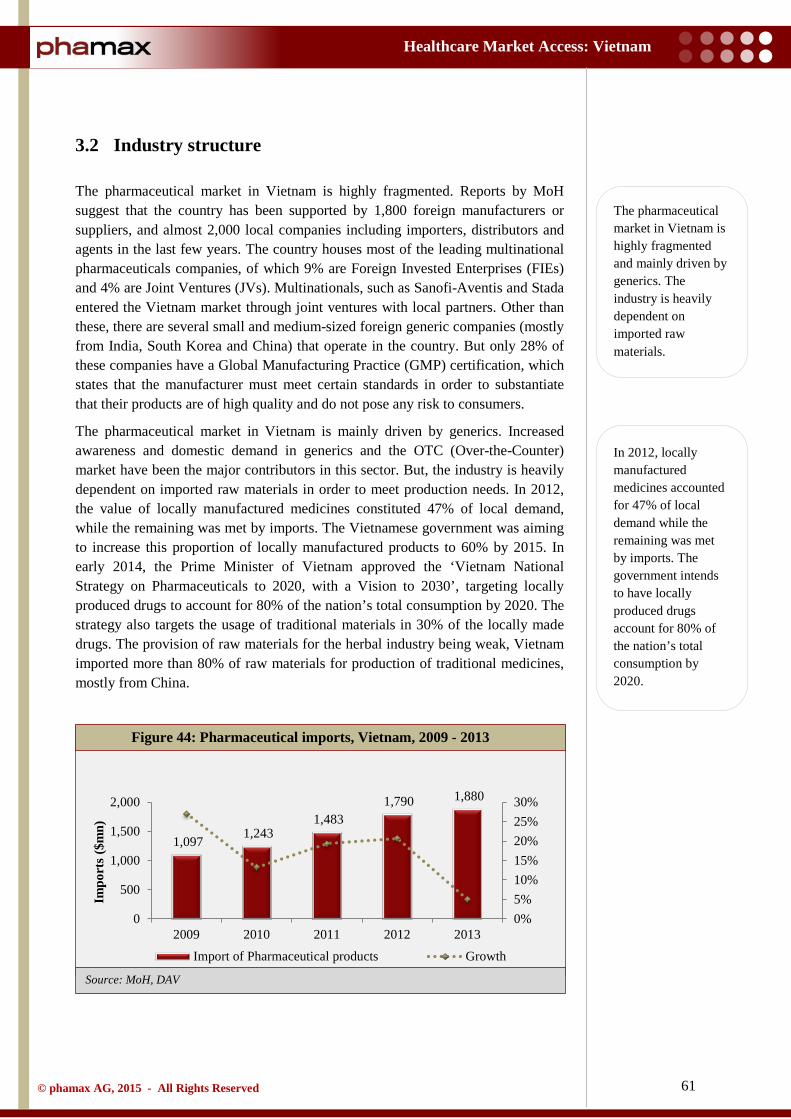

3.2 Industry structure .................................................................................................................. 61

3.3 Market segments ................................................................................................................... 64

3.4 Opportunities and challenges ................................................................................................ 65

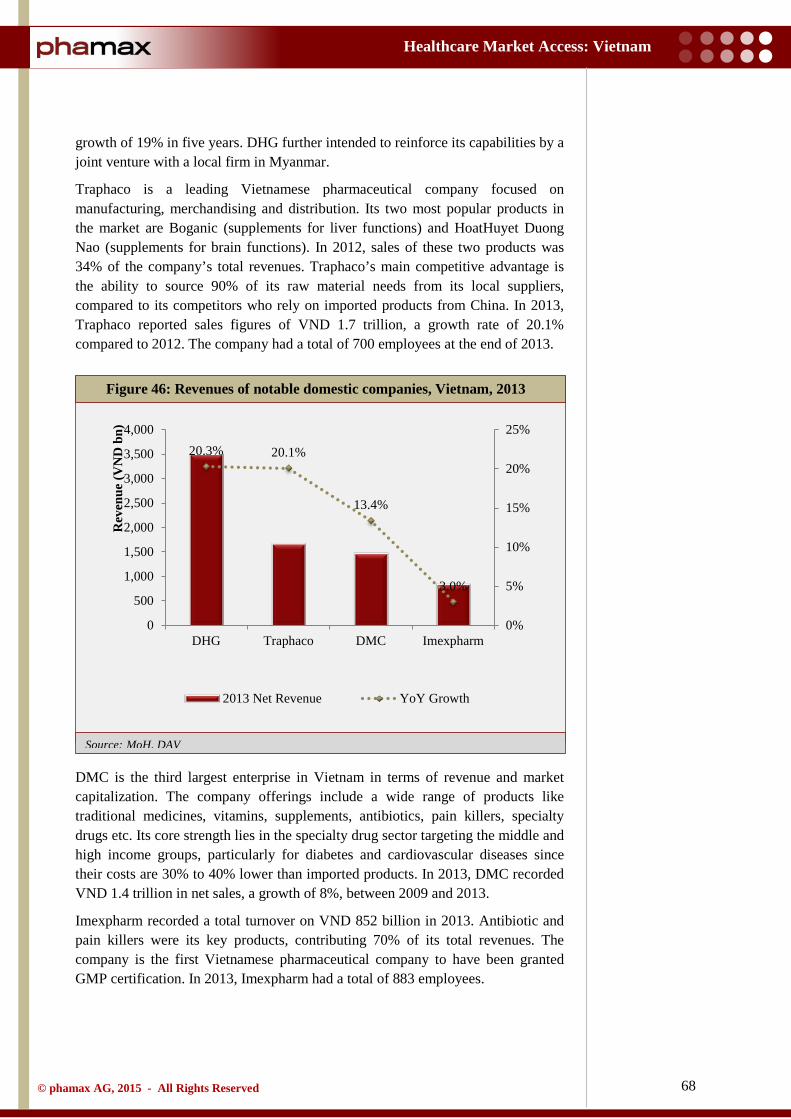

3.5 Major players ........................................................................................................................ 67

3.6 Key products ......................................................................................................................... 70

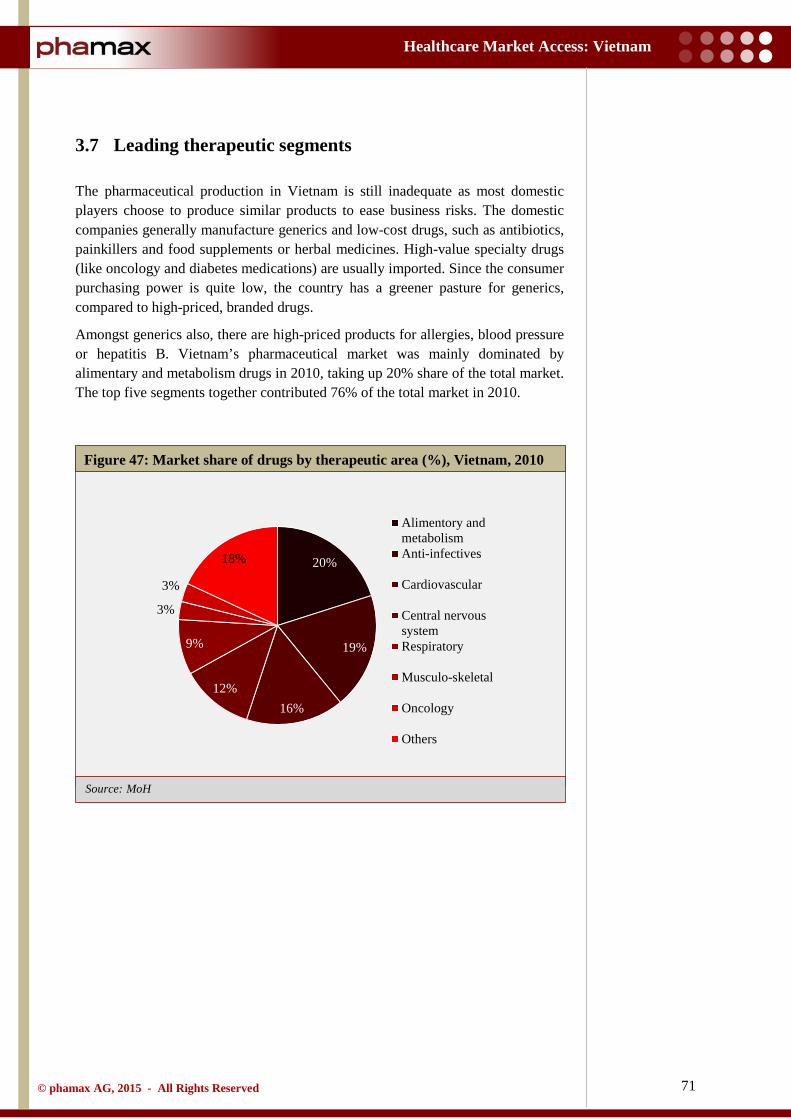

3.7 Leading therapeutic segments .............................................................................................. 71

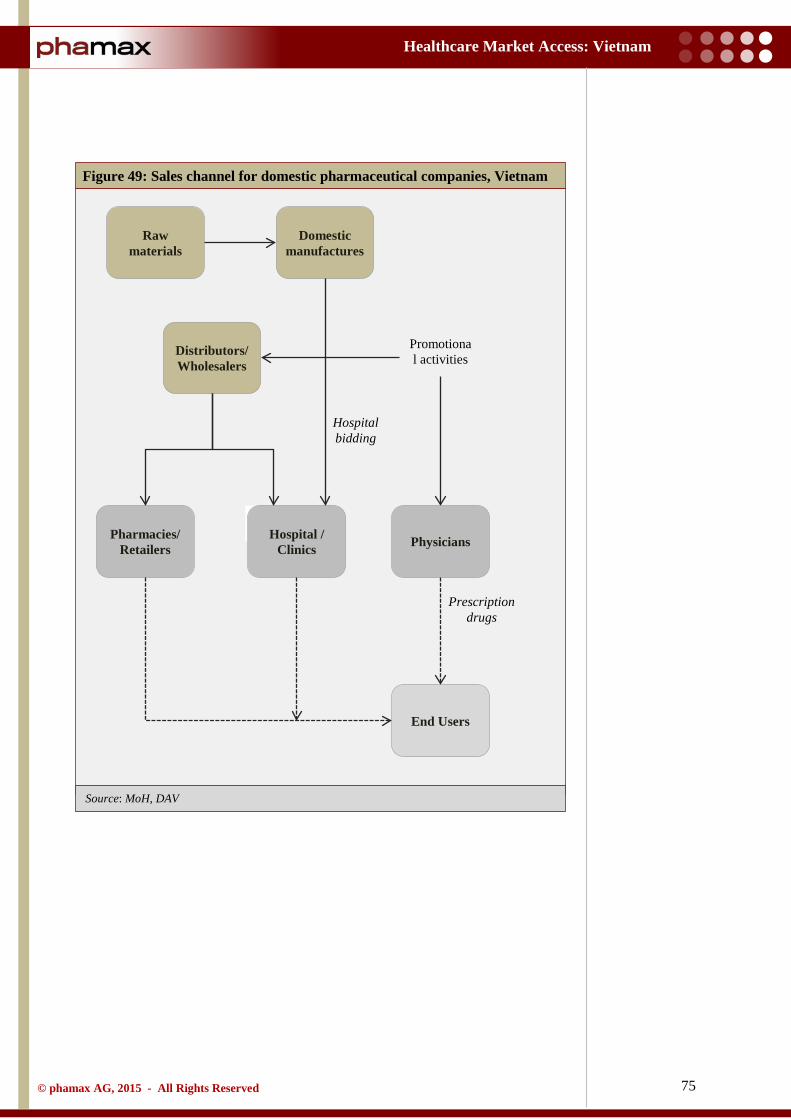

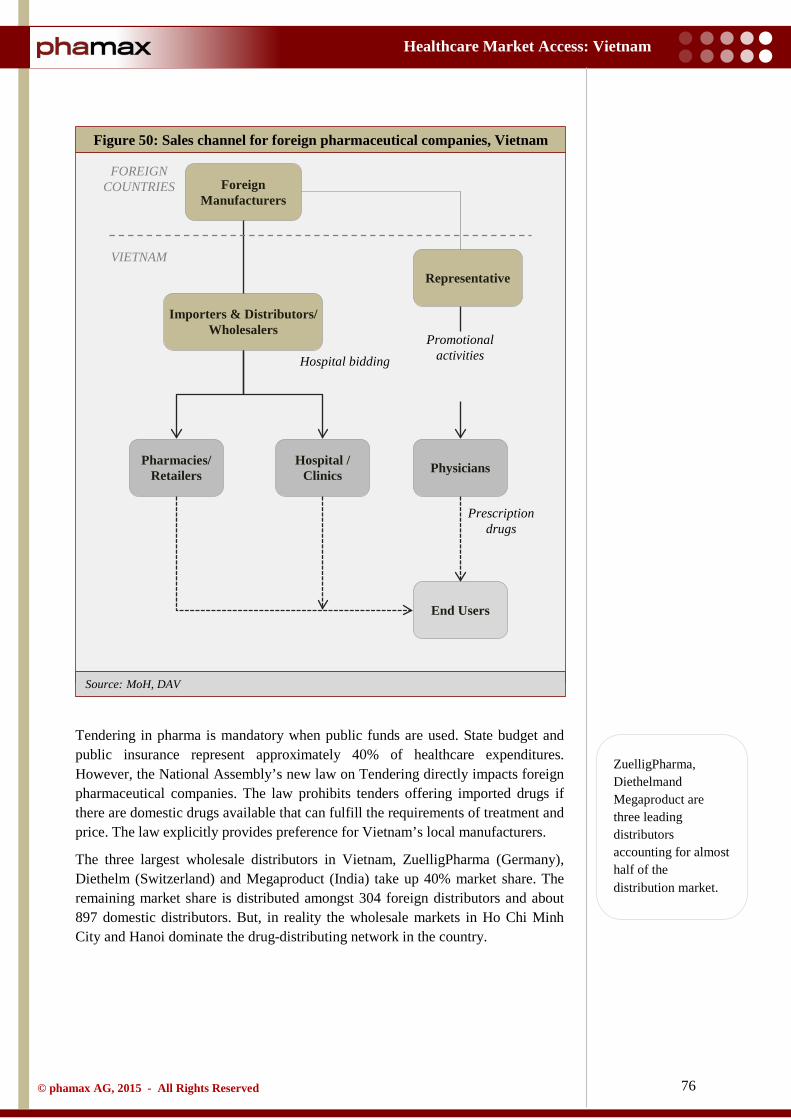

3.8 Supply chain ......................................................................................................................... 72

3.8.1 Distribution ................................................................................................................... 74

3.8.2 Retail ............................................................................................................................. 77

3.9 Sales and marketing .............................................................................................................. 78

3.10 FDI in pharmaceutical industry ............................................................................................ 80

3.11 Events ................................................................................................................................... 82

3.12 Major diseases ...................................................................................................................... 83

3.12.1 Stroke ............................................................................................................................ 83

3.12.2 Cancer ........................................................................................................................... 84

3.12.3 Road traffic accidents ................................................................................................... 84

3.12.4 Tuberculosis ................................................................................................................. 84

3.12.5 Diabetes mellitus .......................................................................................................... 85

4

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

3.12.6 HIV/AIDS ..................................................................................................................... 85

4 MARKET ACCESS............................................................................................................................................ 86

4.1 Stakeholder landscape .......................................................................................................... 86

4.2 Regulatory landscape ............................................................................................................ 88

4.2.1 Regulatory agencies ...................................................................................................... 88

4.2.2 Market authorization for pharmaceutical products ....................................................... 89

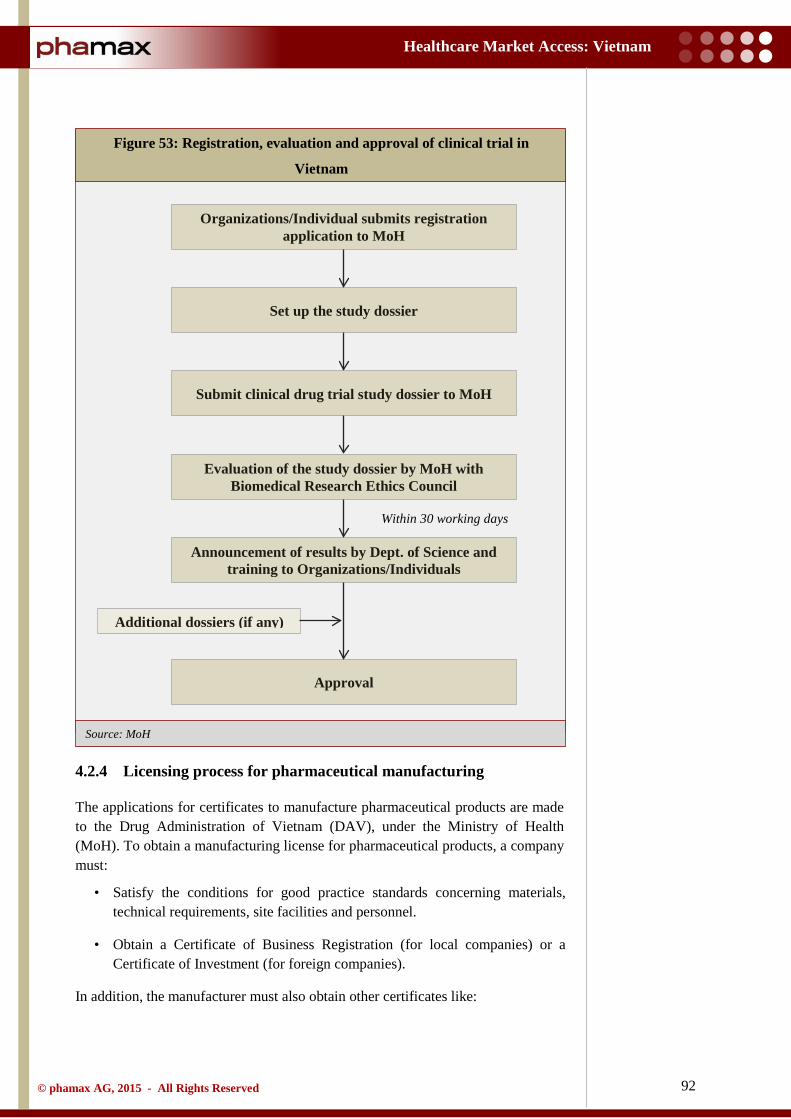

4.2.3 Clinical trial regulations ............................................................................................... 91

4.2.4 Licensing process for pharmaceutical manufacturing .................................................. 92

4.2.5 Licensing process for pharmaceutical imports ............................................................. 95

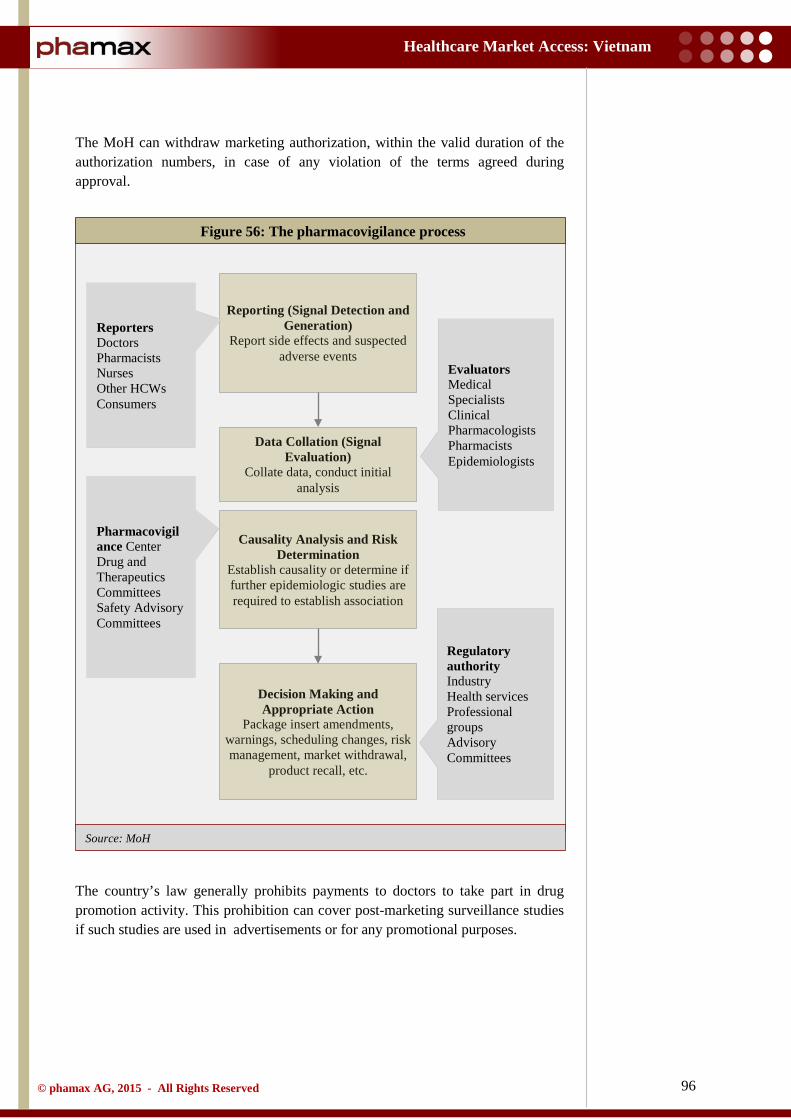

4.2.6 Post-marketing regulations ........................................................................................... 95

4.2.7 Advertising ................................................................................................................... 97

4.2.8 Labeling and packaging ................................................................................................ 97

4.2.9 Intellectual property rights ............................................................................................ 98

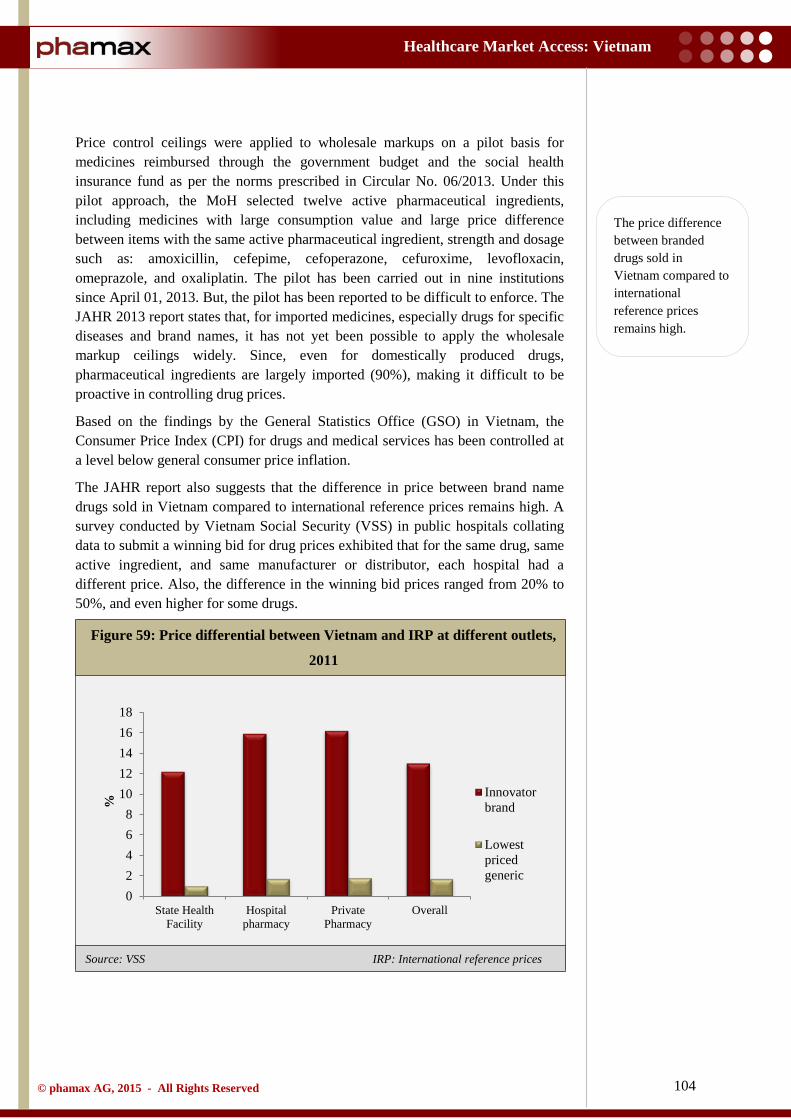

4.3 Pricing................................................................................................................................. 101

4.3.1 Pricing system............................................................................................................. 101

4.3.2 Pricing policy .............................................................................................................. 102

4.3.3 Price trends ................................................................................................................. 103

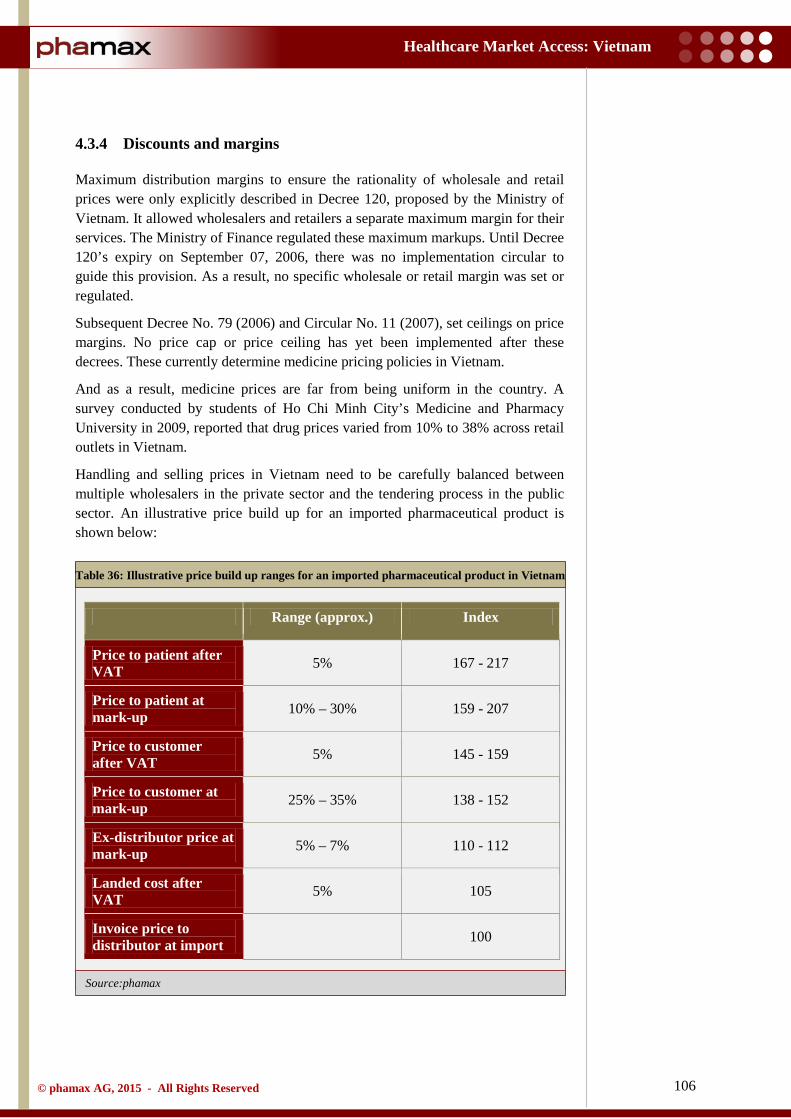

4.3.4 Discounts and margins ................................................................................................ 106

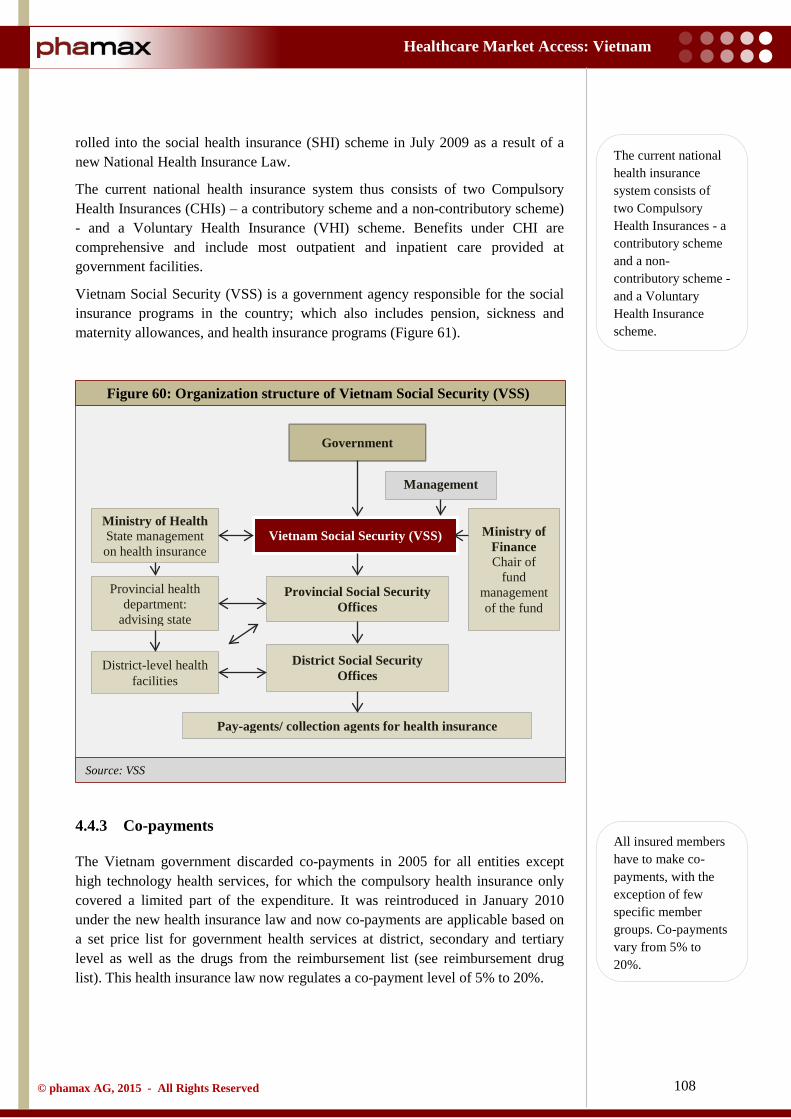

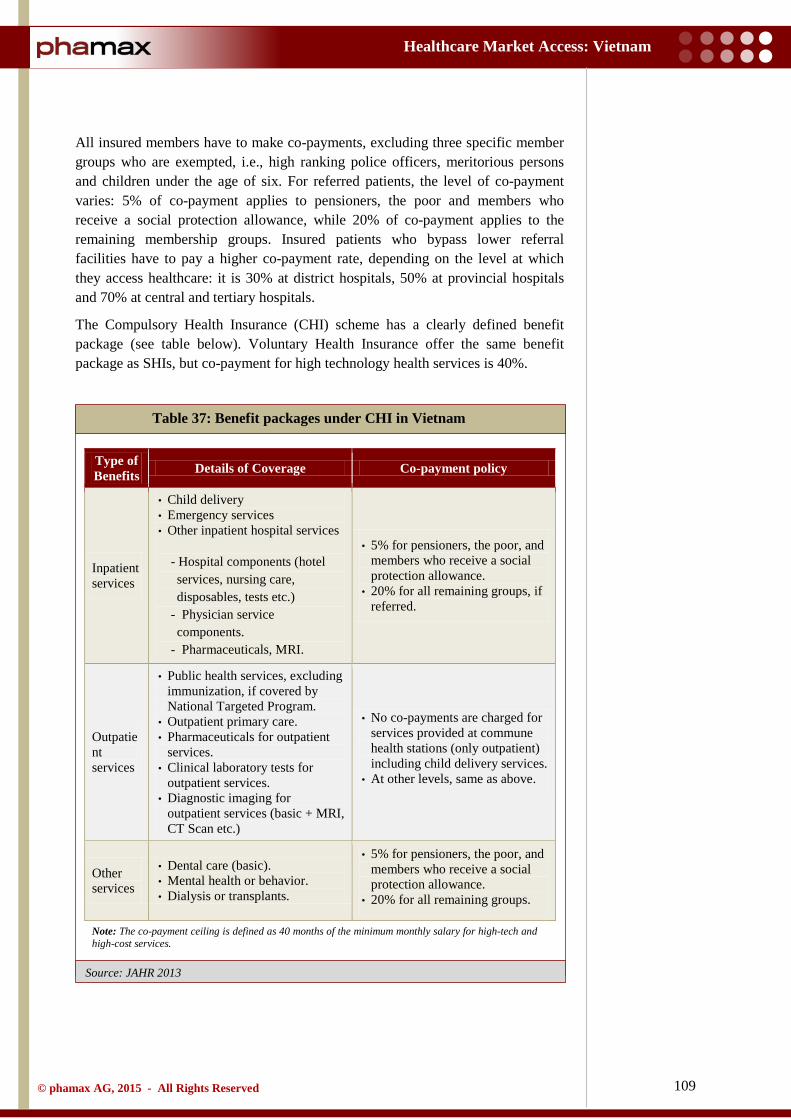

4.4 Reimbursement landscape .................................................................................................. 107

4.4.1 Reimbursement process .............................................................................................. 107

4.4.2 Insurance providers ..................................................................................................... 107

4.4.3 Co-payments ............................................................................................................... 108

4.5 Prescribing and dispensing ................................................................................................. 111

4.5.1 Prescribing guidelines ................................................................................................. 111

4.5.2 Prescribing influences ................................................................................................. 111

4.5.3 Dispensing .................................................................................................................. 112

4.6 Essential drug list ............................................................................................................... 113

4.7 Reimbursement drug list ..................................................................................................... 114

4.8 Drug procurement ............................................................................................................... 115

4.9 Hospital formulary .............................................................................................................. 117

5 APPENDIX........................................................................................................................................................ 118

5.1 Glossary .............................................................................................................................. 118

5.2 Bibliography ....................................................................................................................... 121

5.3 Methodology ....................................................................................................................... 125

5

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

5.3.1 Secondary research ..................................................................................................... 125

5.3.2 Primary research ......................................................................................................... 125

5.3.3 Data validation ............................................................................................................ 125

5.4 Disclaimer ........................................................................................................................... 126

5.5 Contact us ........................................................................................................................... 126

6

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Table 1: GDP ($bn), Vietnam, 2009 - 2013 ............................................................................................... 11 Table 2: GDP per capita ($), Vietnam, 2009 - 2013 ................................................................................... 11 Table 3: Real GDP growth (%), Vietnam, 2009 - 2013 ............................................................................. 12 Table 4: Gross national income ($bn), Vietnam, 2009 - 2013 ................................................................... 13 Table 5: GNI per capita ($), Vietnam, 2009 - 2013 .................................................................................... 13 Table 6: Inflation (%), Vietnam, 2009 - 2013 ............................................................................................ 15 Table 7: Consumer price index, Vietnam, 2009 - 2013 .............................................................................. 16 Table 8: Foreign exchange reserves ($bn), Vietnam, 2009 - 2013 ............................................................. 16 Table 9: Current account balance ($bn), Vietnam, 2009 - 2013 ................................................................ 17 Table 10: Government net debt (% to GDP), Vietnam, 2009 - 2013 ......................................................... 18 Table 11: Exchange rate (VND per USD), Vietnam, 2009 - 2013 ............................................................. 19 Table 12: Foreign direct investment, Vietnam, 2009 - 2013 ...................................................................... 20 Table 13: Foreign direct investment ($bn), Peer countries, 2009 - 2013 ................................................... 21 Table 14: Imports and Exports ($bn), Vietnam, 2009 - 2012 ..................................................................... 22 Table 15: Population (mn), Vietnam, 2009 - 2013 ..................................................................................... 23 Table 16: Urban and rural population (mn), Vietnam, 2009 - 2013 ........................................................... 24 Table 17: Population distribution by age groups (%), Vietnam, 2009 - 2013 ............................................ 25 Table 18: Gross enrolment ratio, Vietnam, 2009 - 2013 ............................................................................ 27 Table 19: Employment to population ratio (15+ age), Vietnam, 2009 - 2012 ........................................... 28 Table 20: Unemployment rate of labor force (%), Vietnam, 2009 - 2013 ................................................. 28 Table 21: Life expectancy at birth (years), Vietnam, 2008 - 2012 ............................................................. 36 Table 22: Mortality rate, Vietnam, 2008 - 2012 ......................................................................................... 37 Table 23: Mortality rate by gender, Vietnam, 2008–2012 ......................................................................... 38 Table 24: Healthcare expenditure, Vietnam, 2008 - 2012 .......................................................................... 40 Table 25: Healthcare expenditure per capita, PPP ($), Vietnam, 2008 - 2012 ........................................... 41 Table 26: Public healthcare expenditure (% of total), Vietnam, 2008 - 2012 ............................................ 41 Table 27: Out-of-pocket healthcare expenditure (% of total), .................................................................... 42 Table 28: Pharmaceutical expenditure, Vietnam, 2008 - 2012 .................................................................. 46 Table 29: Share of public - private healthcare expenditure (%), Vietnam, ................................................ 47 Table 30: Number of hospitals and beds by hospital, Vietnam, 2011 ........................................................ 53 Table 31: Number of hospitals, Vietnam, 2008 - 2012 .............................................................................. 54 Table 32: Number of beds (per 10,000 inhabitants), Vietnam, 2008 - 2012 .............................................. 54 Table 33: Number of doctors, Vietnam, 2008 - 2012 ................................................................................. 59 Table 34: Healthcare personnel, Vietnam, 2008 - 2012 ............................................................................. 59 Table 35: Summary of types of marketing activities allowed for............................................................... 79 Table 36: Illustrative price build up ranges for an imported pharmaceutical product in Vietnam ........... 106 Table 37: Benefit packages under CHI in Vietnam .................................................................................. 109

LIST OF TABLES

7

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Figure 1: GDP ($bn), Peer countries, 2013 .................................................................................................. 9 Figure 2: GDP ($bn), Peer countries, 2013 ................................................................................................ 10 Figure 3: GDP per capita ($), Vietnam, 2009 - 2013 ................................................................................. 11 Figure 4: Real GDP growth (%), Vietnam, 2009 - 2013 ............................................................................ 12 Figure 5: Gross national income ($bn), Vietnam, 2009 - 2013 .................................................................. 12 Figure 6: GNI per capita ($), Vietnam, 2009 - 2013 .................................................................................. 13 Figure 7: GNI, Peer countries, 2009 - 2013 ............................................................................................... 14 Figure 8: Inflation (%), Vietnam, 2009 - 2013 ........................................................................................... 15 Figure 9: Consumer price index, Vietnam, 2009 - 2013 ............................................................................ 15 Figure 10: Foreign exchange reserves ($bn), Vietnam, 2009 - 2013 ......................................................... 16 Figure 11: Current account balance ($bn), Vietnam, 2009 - 2012 ............................................................. 17 Figure 12: Government net debt (% to GDP), Vietnam, 2009 - 2013 ........................................................ 18 Figure 13: Exchange rate (VND per USD), Vietnam, 2009 - 2013............................................................ 19 Figure 14: Foreign direct investment, Vietnam, 2009 - 2013 ..................................................................... 20 Figure 15: Foreign direct investment ($bn), Peer countries, 2009 - 2013 .................................................. 20 Figure 16: GDP vs foreign direct investment, Peer countries, 2013 .......................................................... 21 Figure 17: Imports and Exports ($bn), Vietnam, 2009 - 2012 ................................................................... 22 Figure 18: Population (mn), Vietnam, 2009 - 2013.................................................................................... 23 Figure 19: Urban and rural population share (%), Vietnam, 2009 - 2013 .................................................. 24 Figure 20: Population distribution by age groups (%), Vietnam, 2009 - 2013........................................... 25 Figure 21: Gross enrolment ratio, Vietnam, 2009 - 2012 ........................................................................... 26 Figure 22: Employment to population ratio (15+ age), Vietnam, 2009 - 2012 .......................................... 27 Figure 23: Unemployment rate of labor force (%), Vietnam, 2009 - 2013 ................................................ 28 Figure 24: Employment by sectors (%), Vietnam, 2009 - 2013 ................................................................. 29 Figure 25: The structure of the healthcare system in Vietnam ................................................................... 35 Figure 26: Life expectancy at birth (years), Vietnam, 2008 - 2012............................................................ 36 Figure 27: Mortality rate, Vietnam, 2008 - 2012........................................................................................ 37 Figure 28: Mortality rate by gender, Vietnam, 2008–2012 ........................................................................ 38 Figure 29: Healthcare expenditure, Vietnam, 2008 - 2012 ........................................................................ 40 Figure 30: Healthcare expenditure per capita, PPP ($), Vietnam, 2008 - 2012 .......................................... 41 Figure 31: Public healthcare expenditure (% of total), Vietnam, 2008 - 2012 ........................................... 41 Figure 32: Out-of-pocket healthcare expenditure (% of total), .................................................................. 42 Figure 33: Share of sources of total health expenditure (%), Vietnam, 2010 ............................................. 43 Figure 34: Healthcare system financing, Vietnam ..................................................................................... 44 Figure 35: Pharmaceutical expenditure, Vietnam, 2008 - 2012 ................................................................. 45 Figure 36: Share of public-private healthcare expenditure (%), Vietnam, 2008 - 2012 ............................. 47 Figure 37: Health insurance coverage, Vietnam, 2002 - 2010 ................................................................... 49 Figure 38: Roadmap for universal healthcare in Vietnam .......................................................................... 50 Figure 39: Number of hospitals, Vietnam, 2008 - 2012 ............................................................................. 54 Figure 40: Number of beds (per 10,000 inhabitants), Vietnam, 2008 - 2012 ............................................. 54 Figure 41: Number of doctors, Vietnam, 2008 - 2012 ............................................................................... 58 Figure 42: Healthcare personnel, Vietnam, 2008 - 2012 ............................................................................ 59

LIST OF FIGURES

8

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Figure 43: Pharmaceutical market ($bn), Vietnam, 2008 - 2014 ............................................................... 60 Figure 44: Pharmaceutical imports, Vietnam, 2009 - 2013 ........................................................................ 61 Figure 45: Drug consumption distribution (%), Vietnam, 2013 ................................................................. 62 Figure 46: Revenues of notable domestic companies, Vietnam, 2013 ....................................................... 68 Figure 47: Market share of drugs by therapeutic area (%), Vietnam, 2010 ............................................... 71 Figure 48: Distribution channel for pharmaceuticals, Vietnam .................................................................. 73 Figure 49: Sales channel for domestic pharmaceutical companies, Vietnam ............................................. 75 Figure 50: Sales channel for foreign pharmaceutical companies, Vietnam ............................................... 76 Figure 51: Major diseases / conditions (DALY per 1,000,000), Vietnam .................................................. 83 Figure 52: Market authorization process, Vietnam .................................................................................... 90 Figure 53: Registration, evaluation and approval of clinical trial in Vietnam ........................................... 92 Figure 54: Process for obtaining pharmaceutical manufacturing license ................................................... 93 Figure 55: Process for obtaining GMP certificate for pharmaceutical manufacturing ............................... 94 Figure 56: The pharmacovigilance process ................................................................................................ 96 Figure 57: Organization structure of the IP management in Vietnam ........................................................ 99 Figure 58: Agencies involved in drug pricing policy in Vietnam ............................................................ 103 Figure 59: Price differential between Vietnam and IRP at different outlets, 2011 .................................. 104 Figure 60: Organization structure of Vietnam Social Security (VSS)...................................................... 108

9

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: World Bank

1. Country Landscape

1.1 Economic environment

Following its reunification in 1975, Vietnam went through a decade of economic stagnation. Post that era, Vietnam initiated a turnaround with an economic renovation in 1986, known as ‘Doi Moi’ to facilitate its transition from a centrally planned economy to a ‘socialist-oriented’ market economy. The country has since continued to experience strong growth in its economy and has gradually merged with the global community. The year 2013 proved to be a positive year for the Vietnamese economy in spite of posting its lowest growth rate in 2012 in more than a decade. The relatively stable economy in 2013 was attributed to the moderate inflation, stable exchange rates, current account surpluses and significant increase in forex reserves during the year. However, this growth was dampened due to unresolved issues in the banking sector and amongst State Owned Enterprises (SOEs). In an effort to resolve this issue of bad debts, the government did establish the Vietnam Asset Management Company (VAMC), a state owned enterprise in 2013. But, unless this process is hastened, the Non-performing Loan (NPL) crises that hovers over the banking sector will continue to undermine it and hinder Vietnam’s economic growth. The trade agreements that Vietnam signed with the European Union (EU) and other powers are expected to strengthen its economic capabilities, providing development opportunities, especially in the fields of economy, trade, science, technology, agriculture and tourism. According to the government’s directive on formulation of the next Socio-Economic Development plan for 2016 - 2020, Vietnam will target an annual growth of GDP between 6.5% and 7%. This is expected to help Vietnam become a modernized and industrialized country by 2020.

Figure 1: GDP ($bn), Peer countries, 2013

868

387 312 298 272

171

0

200

400

600

800

1,000

Indonesia Thailand Malaysia Singapore Philippines Vietnam

GD

P ($

bn)

10

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: World Bank

1.2 Economic indicators

1.2.1 Gross domestic product

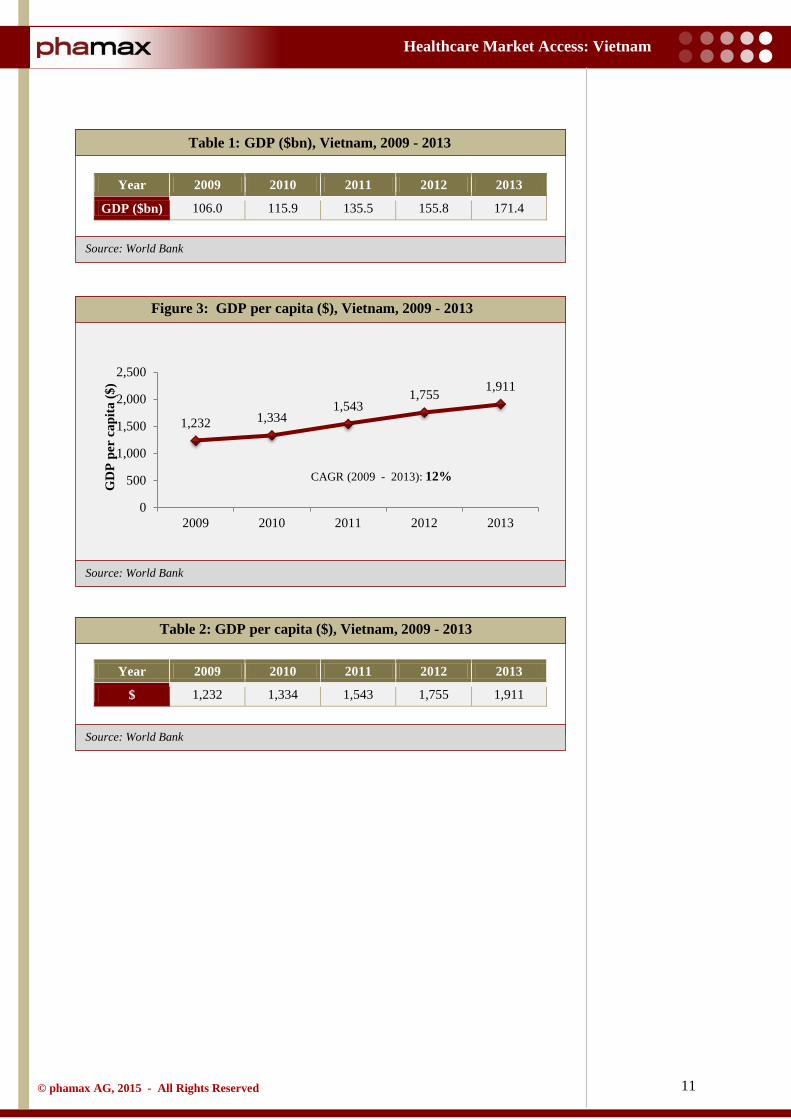

The Gross Domestic Product (GDP) of Vietnam was $171.4 bn in 2013, witnessing a substantial growth of 5.4% compared to 2012, fuelled by a strong rise in final consumption. The GDP growth had reached an all-time high in 2010 and contrastingly slumped in 2012, attributable to the rising inflation in the country. Although Vietnam’s GDP growth was not as high as its peers (Indonesia, Malaysia, Philippines, Singapore and Thailand), the signs were greeted with optimism.

Between 2009 and 2013, the GDP of Vietnam grew at an annual average rate of 5.7%. Based on the findings of the International Monetary Fund (IMF), Vietnam’s growing economy is being supported by both exports and increased foreign investment in the country. The growth in 2013 was led by the Services sector (43% of the GDP), which grew by 6.6% while Manufacturing (38% of the GDP) and Agriculture sectors grew by 5.4% and 2.7% respectively. Taking into account all these factors, many analysts expected the GDP growth to rise slightly further to 5.6% in 2014 and grow further to 5.8% in 2015, in alignment with the upward trends in the US and European zones. The corresponding improvements in the developed zones were expected to help Vietnam address its domestic banking drawbacks.

In 2010, Vietnam attained a per capita GDP of $1,333 and was categorized as a low middle-income country, based on guidelines designed by the World Bank. In 2013, Vietnam’s GDP per capita reached $1,911 and the National Congress (Ministry of Planning and Investment) expects to achieve its target of GDP per capita of $2,000 by 2015.

Figure 2: GDP ($bn), Peer countries, 2013

106.0 115.9 135.5

155.8 171.4

0

50

100

150

200

2009 2010 2011 2012 2013

GD

P ($

bn)

CAGR (2009 - 2013): 13%

The GDP of Vietnam has grown at an annual average rate of 5.7% over 2009 - 2013. Vietnam’s growing economy is being supported by both exports and increased foreign investment in the country.

GDP growth is estimated to be 5.8% in 2015 due to recovery in global economy.

11

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: World Bank

Source: World Bank

Source: World Bank

Table 1: GDP ($bn), Vietnam, 2009 - 2013

Year 2009 2010 2011 2012 2013

GDP ($bn) 106.0 115.9 135.5 155.8 171.4

Table 2: GDP per capita ($), Vietnam, 2009 - 2013

Year 2009 2010 2011 2012 2013

$ 1,232 1,334 1,543 1,755 1,911

Figure 3: GDP per capita ($), Vietnam, 2009 - 2013

1,232 1,334 1,543

1,755 1,911

0

500

1,000

1,500

2,000

2,500

2009 2010 2011 2012 2013

GD

P pe

r ca

pita

($)

CAGR (2009 - 2013): 12%

12

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: World Bank

Source: World Bank

Source: World Bank

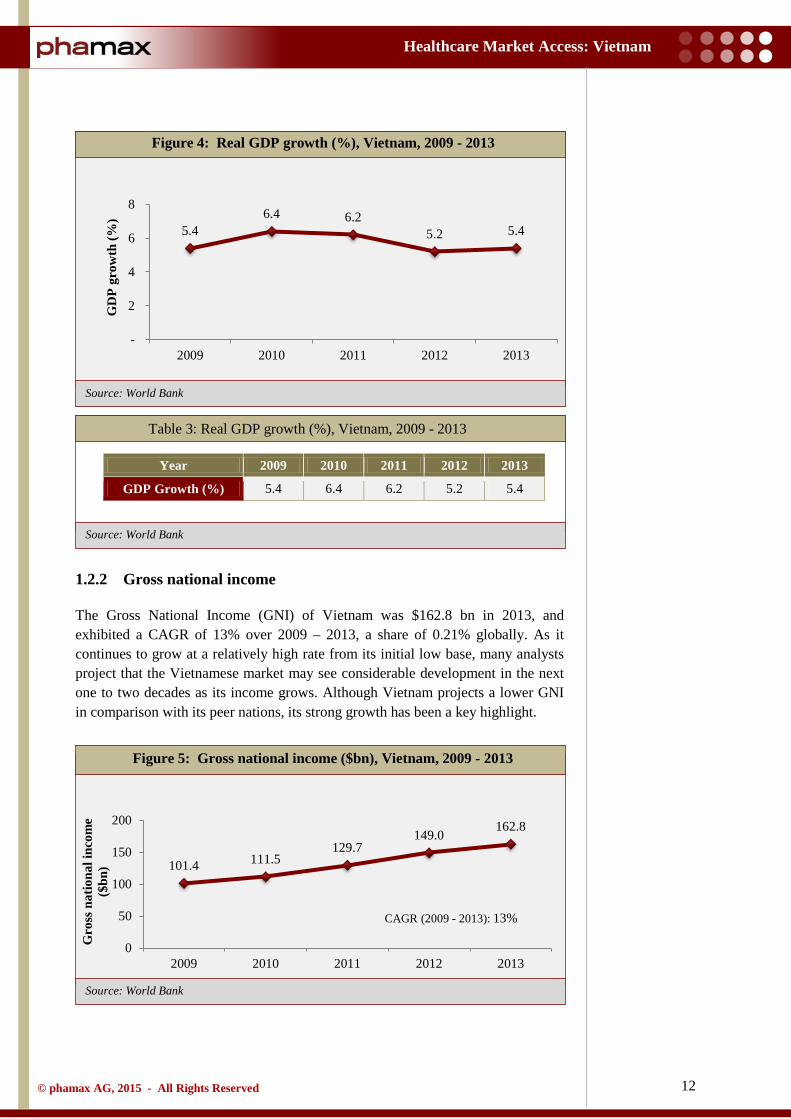

Table 3: Real GDP growth (%), Vietnam, 2009 - 2013

Year 2009 2010 2011 2012 2013

GDP Growth (%) 5.4 6.4 6.2 5.2 5.4

1.2.2 Gross national income

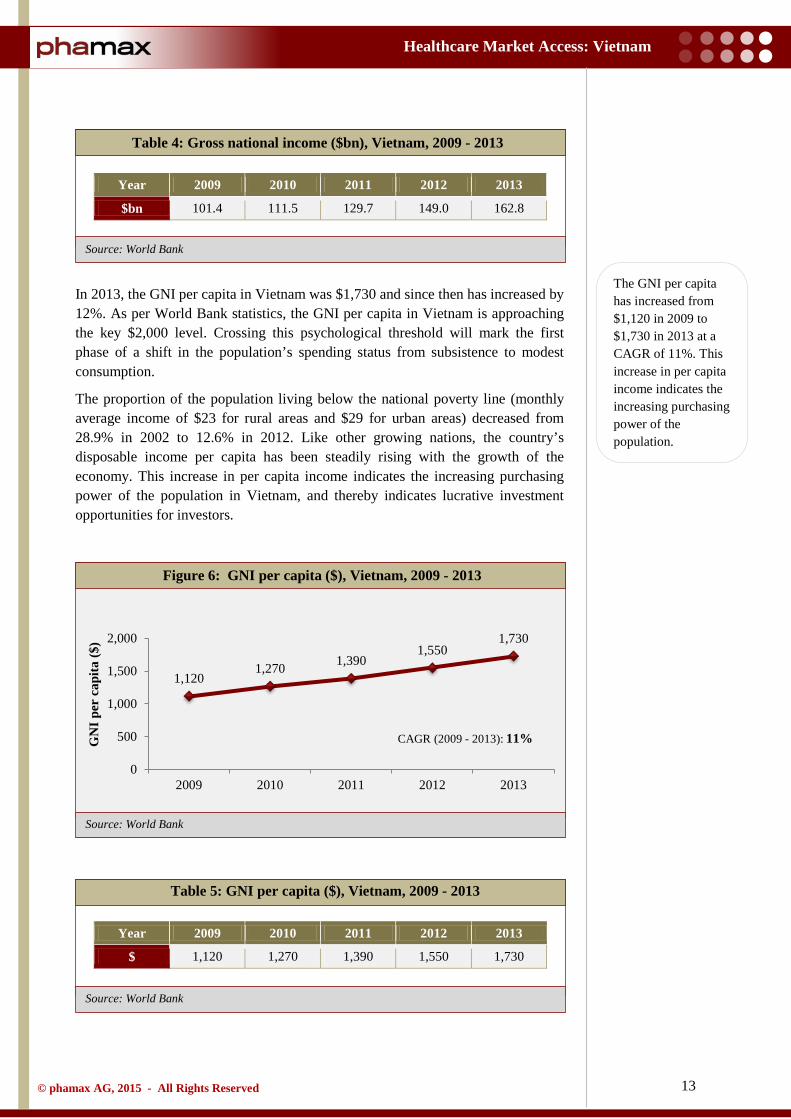

The Gross National Income (GNI) of Vietnam was $162.8 bn in 2013, and exhibited a CAGR of 13% over 2009 – 2013, a share of 0.21% globally. As it continues to grow at a relatively high rate from its initial low base, many analysts project that the Vietnamese market may see considerable development in the next one to two decades as its income grows. Although Vietnam projects a lower GNI in comparison with its peer nations, its strong growth has been a key highlight.

Figure 4: Real GDP growth (%), Vietnam, 2009 - 2013

Figure 5: Gross national income ($bn), Vietnam, 2009 - 2013

5.4 6.4 6.2

5.2 5.4

-

2

4

6

8

2009 2010 2011 2012 2013

GD

P gr

owth

(%)

101.4 111.5 129.7

149.0 162.8

0

50

100

150

200

2009 2010 2011 2012 2013

Gro

ss n

atio

nal i

ncom

e ($

bn)

CAGR (2009 - 2013): 13%

13

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: World Bank

Source: World Bank

Source: World Bank

Table 4: Gross national income ($bn), Vietnam, 2009 - 2013

Year 2009 2010 2011 2012 2013

$bn 101.4 111.5 129.7 149.0 162.8

In 2013, the GNI per capita in Vietnam was $1,730 and since then has increased by 12%. As per World Bank statistics, the GNI per capita in Vietnam is approaching the key $2,000 level. Crossing this psychological threshold will mark the first phase of a shift in the population’s spending status from subsistence to modest consumption.

The proportion of the population living below the national poverty line (monthly average income of $23 for rural areas and $29 for urban areas) decreased from 28.9% in 2002 to 12.6% in 2012. Like other growing nations, the country’s disposable income per capita has been steadily rising with the growth of the economy. This increase in per capita income indicates the increasing purchasing power of the population in Vietnam, and thereby indicates lucrative investment opportunities for investors.

Table 5: GNI per capita ($), Vietnam, 2009 - 2013

Year 2009 2010 2011 2012 2013

$ 1,120 1,270 1,390 1,550 1,730

Figure 6: GNI per capita ($), Vietnam, 2009 - 2013

1,120 1,270 1,390

1,550 1,730

0

500

1,000

1,500

2,000

2009 2010 2011 2012 2013

GN

I per

cap

ita ($

)

CAGR (2009 - 2013): 11%

The GNI per capita has increased from $1,120 in 2009 to $1,730 in 2013 at a CAGR of 11%. This increase in per capita income indicates the increasing purchasing power of the population.

14

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: World Bank

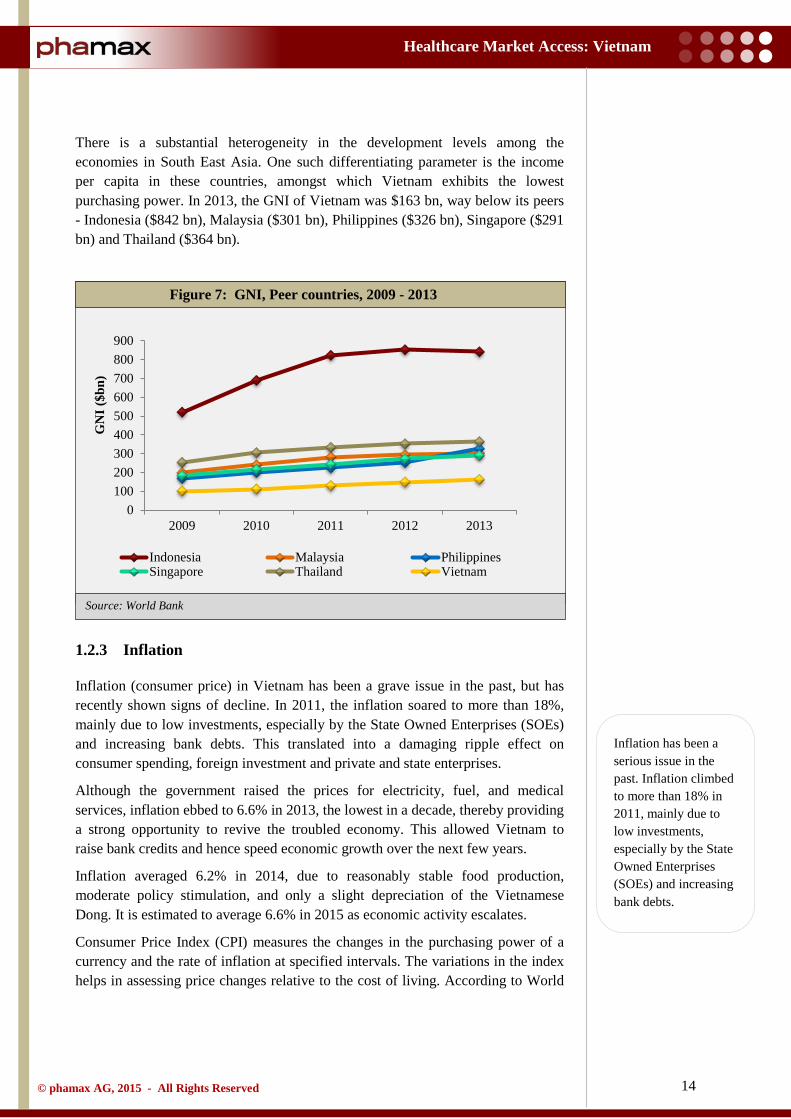

There is a substantial heterogeneity in the development levels among the economies in South East Asia. One such differentiating parameter is the income per capita in these countries, amongst which Vietnam exhibits the lowest purchasing power. In 2013, the GNI of Vietnam was $163 bn, way below its peers - Indonesia ($842 bn), Malaysia ($301 bn), Philippines ($326 bn), Singapore ($291 bn) and Thailand ($364 bn).

1.2.3 Inflation

Inflation (consumer price) in Vietnam has been a grave issue in the past, but has recently shown signs of decline. In 2011, the inflation soared to more than 18%, mainly due to low investments, especially by the State Owned Enterprises (SOEs) and increasing bank debts. This translated into a damaging ripple effect on consumer spending, foreign investment and private and state enterprises.

Although the government raised the prices for electricity, fuel, and medical services, inflation ebbed to 6.6% in 2013, the lowest in a decade, thereby providing a strong opportunity to revive the troubled economy. This allowed Vietnam to raise bank credits and hence speed economic growth over the next few years.

Inflation averaged 6.2% in 2014, due to reasonably stable food production, moderate policy stimulation, and only a slight depreciation of the Vietnamese Dong. It is estimated to average 6.6% in 2015 as economic activity escalates.

Consumer Price Index (CPI) measures the changes in the purchasing power of a currency and the rate of inflation at specified intervals. The variations in the index helps in assessing price changes relative to the cost of living. According to World

Figure 7: GNI, Peer countries, 2009 - 2013

0100200300400500600700800900

2009 2010 2011 2012 2013

GN

I ($b

n)

Indonesia Malaysia PhilippinesSingapore Thailand Vietnam

Inflation has been a serious issue in the past. Inflation climbed to more than 18% in 2011, mainly due to low investments, especially by the State Owned Enterprises (SOEs) and increasing bank debts.

15

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: World Bank

Source: World Bank

Source: World Bank

Bank, the CPI of Vietnam reached an all-time high of 138 (counting 2010 as the base year) in 2013 over the last five years.

Table 6: Inflation (%), Vietnam, 2009 - 2013

Year 2009 2010 2011 2012 2013

Inflation (Annual %) 7.1 8.9 18.7 9.1 6.6

Figure 8: Inflation (%), Vietnam, 2009 - 2013

Figure 9: Consumer price index, Vietnam, 2009 - 2013

7.1 8.9

18.7

9.1 6.6

-

5

10

15

20

2009 2010 2011 2012 2013

Infla

tion

(%)

92 100 119 129 138

- 20 40 60 80

100 120 140 160

2009 2010 2011 2012 2013

Con

sum

er P

rice

Inde

x

CAGR (2009 - 2013): 11%

CPI 2010 = 100

16

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: World Bank

Source: World Bank

Source: World Bank

Table 7: Consumer price index, Vietnam, 2009 - 2013

Year 2009 2010 2011 2012 2013

Consumer Price Index 92 100 119 129 138

1.2.4 Foreign exchange reserves

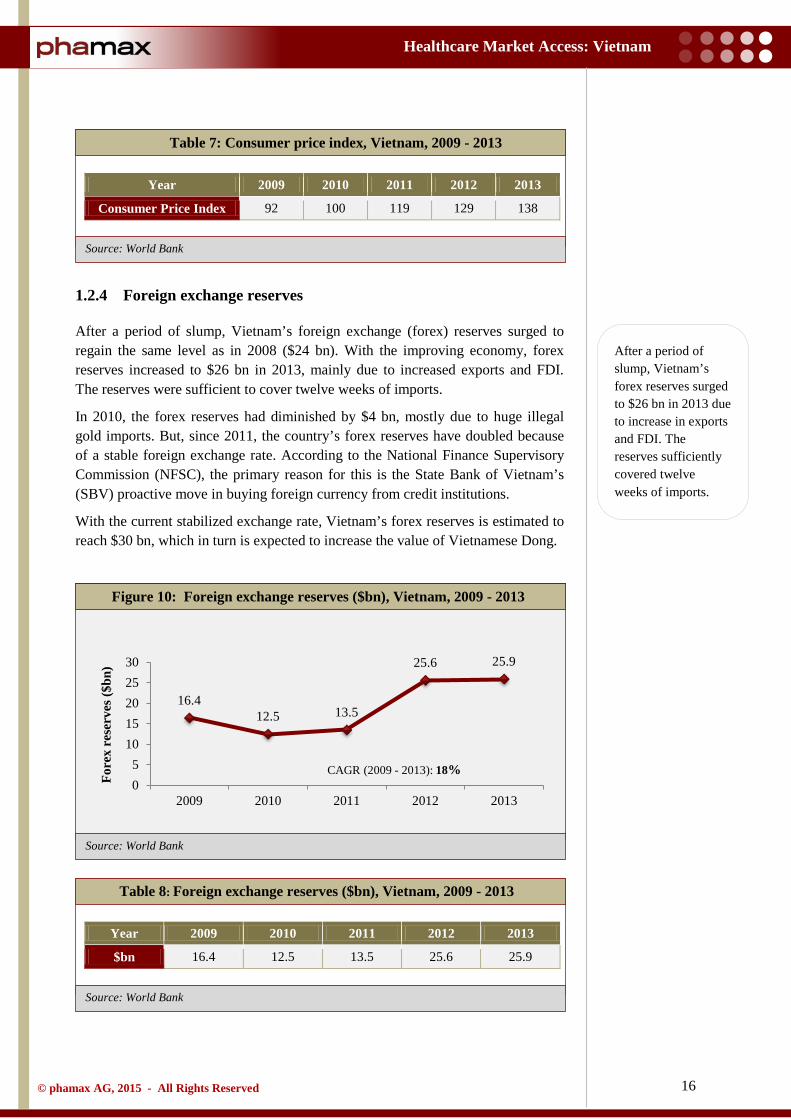

After a period of slump, Vietnam’s foreign exchange (forex) reserves surged to regain the same level as in 2008 ($24 bn). With the improving economy, forex reserves increased to $26 bn in 2013, mainly due to increased exports and FDI. The reserves were sufficient to cover twelve weeks of imports.

In 2010, the forex reserves had diminished by $4 bn, mostly due to huge illegal gold imports. But, since 2011, the country’s forex reserves have doubled because of a stable foreign exchange rate. According to the National Finance Supervisory Commission (NFSC), the primary reason for this is the State Bank of Vietnam’s (SBV) proactive move in buying foreign currency from credit institutions.

With the current stabilized exchange rate, Vietnam’s forex reserves is estimated to reach $30 bn, which in turn is expected to increase the value of Vietnamese Dong.

Table 8: Foreign exchange reserves ($bn), Vietnam, 2009 - 2013

Year 2009 2010 2011 2012 2013

$bn 16.4 12.5 13.5 25.6 25.9

Figure 10: Foreign exchange reserves ($bn), Vietnam, 2009 - 2013

16.4 12.5 13.5

25.6 25.9

05

1015202530

2009 2010 2011 2012 2013

Fore

x re

serv

es ($

bn)

CAGR (2009 - 2013): 18%

After a period of slump, Vietnam’s forex reserves surged to $26 bn in 2013 due to increase in exports and FDI. The reserves sufficiently covered twelve weeks of imports.

17

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: World Bank

Source: World Bank

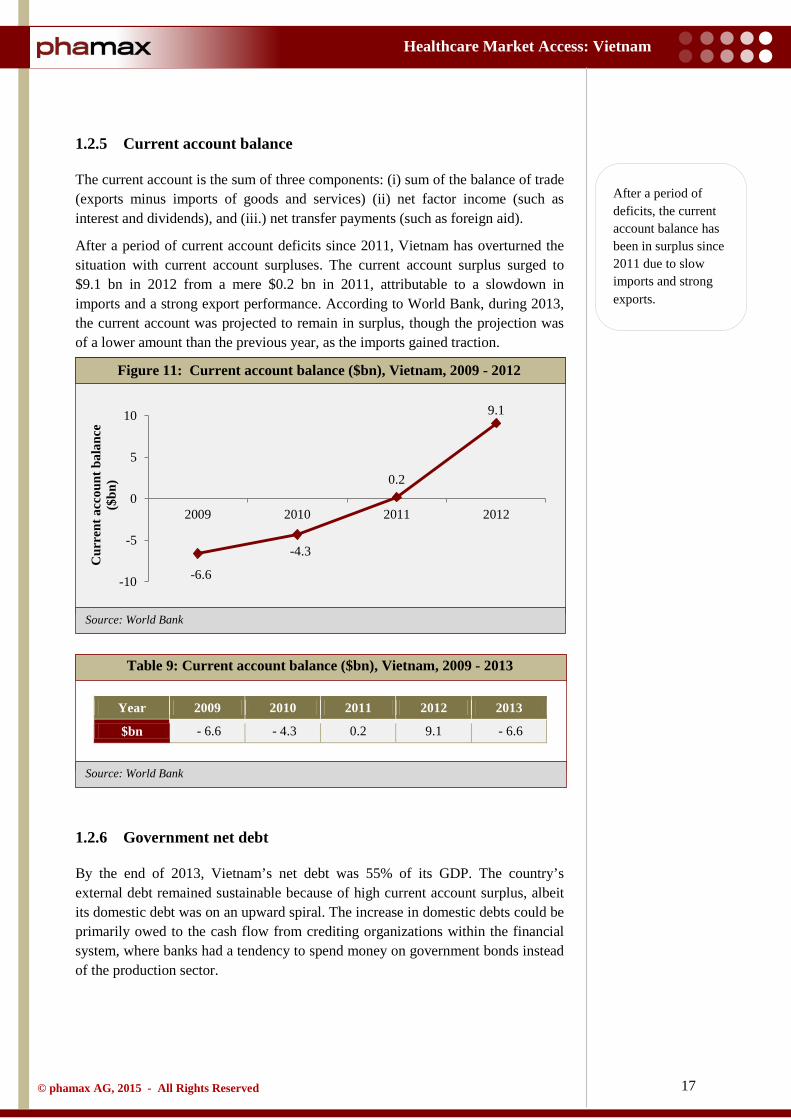

1.2.5 Current account balance

The current account is the sum of three components: (i) sum of the balance of trade (exports minus imports of goods and services) (ii) net factor income (such as interest and dividends), and (iii.) net transfer payments (such as foreign aid).

After a period of current account deficits since 2011, Vietnam has overturned the situation with current account surpluses. The current account surplus surged to $9.1 bn in 2012 from a mere $0.2 bn in 2011, attributable to a slowdown in imports and a strong export performance. According to World Bank, during 2013, the current account was projected to remain in surplus, though the projection was of a lower amount than the previous year, as the imports gained traction.

Table 9: Current account balance ($bn), Vietnam, 2009 - 2013

Year 2009 2010 2011 2012 2013

$bn - 6.6 - 4.3 0.2 9.1 - 6.6

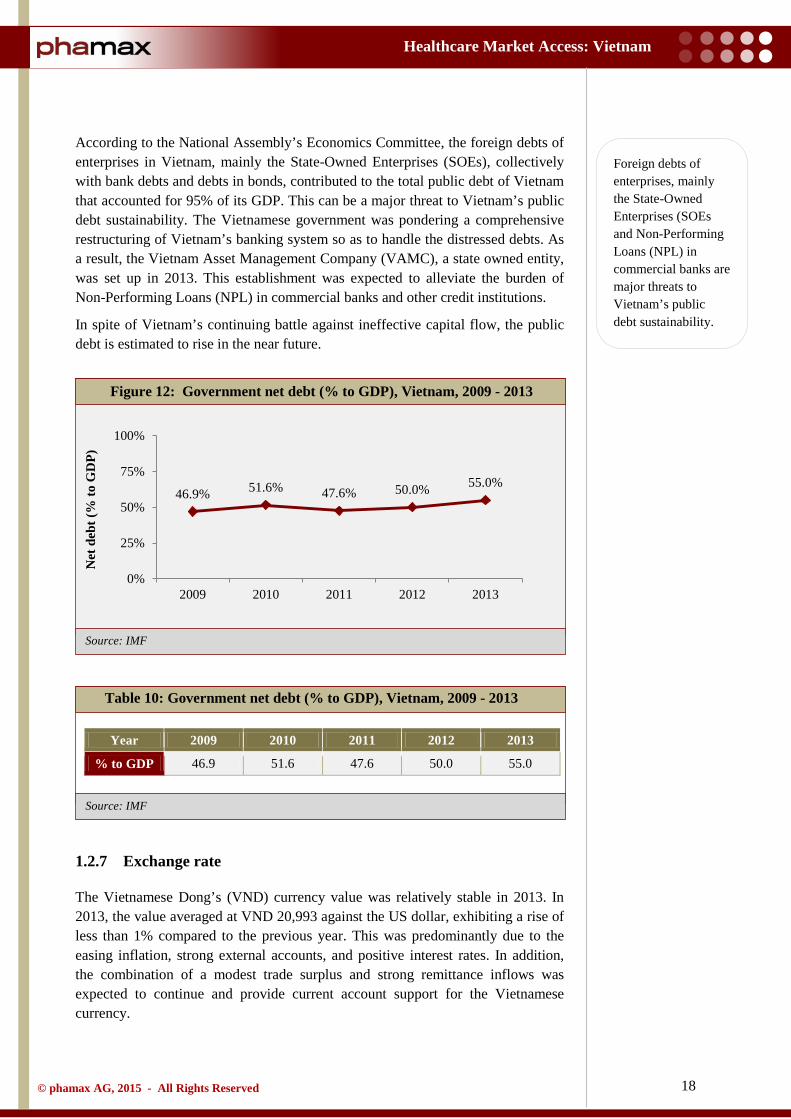

1.2.6 Government net debt

By the end of 2013, Vietnam’s net debt was 55% of its GDP. The country’s external debt remained sustainable because of high current account surplus, albeit its domestic debt was on an upward spiral. The increase in domestic debts could be primarily owed to the cash flow from crediting organizations within the financial system, where banks had a tendency to spend money on government bonds instead of the production sector.

Figure 11: Current account balance ($bn), Vietnam, 2009 - 2012

-6.6

-4.3

0.2

9.1

-10

-5

0

5

10

2009 2010 2011 2012

Cur

rent

acc

ount

bal

ance

($

bn)

After a period of deficits, the current account balance has been in surplus since 2011 due to slow imports and strong exports.

18

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: IMF

Source: IMF

According to the National Assembly’s Economics Committee, the foreign debts of enterprises in Vietnam, mainly the State-Owned Enterprises (SOEs), collectively with bank debts and debts in bonds, contributed to the total public debt of Vietnam that accounted for 95% of its GDP. This can be a major threat to Vietnam’s public debt sustainability. The Vietnamese government was pondering a comprehensive restructuring of Vietnam’s banking system so as to handle the distressed debts. As a result, the Vietnam Asset Management Company (VAMC), a state owned entity, was set up in 2013. This establishment was expected to alleviate the burden of Non-Performing Loans (NPL) in commercial banks and other credit institutions.

In spite of Vietnam’s continuing battle against ineffective capital flow, the public debt is estimated to rise in the near future.

Table 10: Government net debt (% to GDP), Vietnam, 2009 - 2013

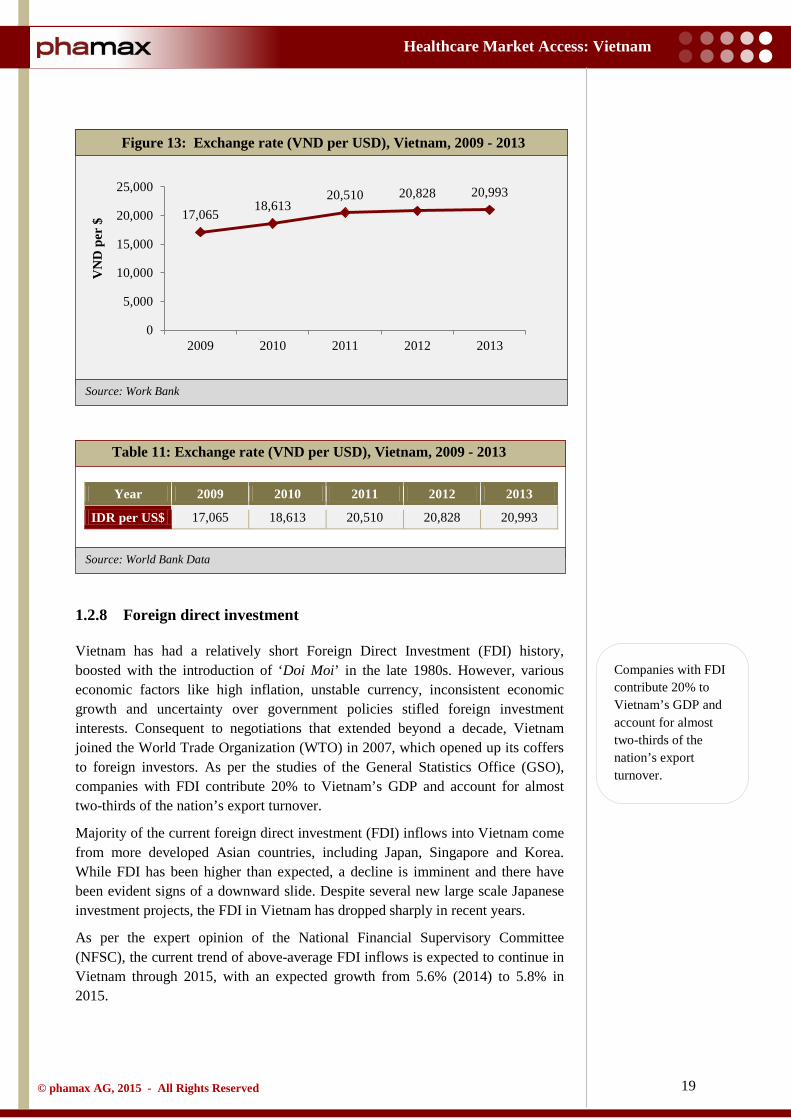

1.2.7 Exchange rate

The Vietnamese Dong’s (VND) currency value was relatively stable in 2013. In 2013, the value averaged at VND 20,993 against the US dollar, exhibiting a rise of less than 1% compared to the previous year. This was predominantly due to the easing inflation, strong external accounts, and positive interest rates. In addition, the combination of a modest trade surplus and strong remittance inflows was expected to continue and provide current account support for the Vietnamese currency.

Figure 12: Government net debt (% to GDP), Vietnam, 2009 - 2013

Year 2009 2010 2011 2012 2013

% to GDP 46.9 51.6 47.6 50.0 55.0

46.9% 51.6% 47.6% 50.0% 55.0%

0%

25%

50%

75%

100%

2009 2010 2011 2012 2013

Net

deb

t (%

to G

DP)

Foreign debts of enterprises, mainly the State-Owned Enterprises (SOEs and Non-Performing Loans (NPL) in commercial banks are major threats to Vietnam’s public debt sustainability.

19

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: World Bank Data

Source: Work Bank

Table 11: Exchange rate (VND per USD), Vietnam, 2009 - 2013

Year 2009 2010 2011 2012 2013

IDR per US$ 17,065 18,613 20,510 20,828 20,993

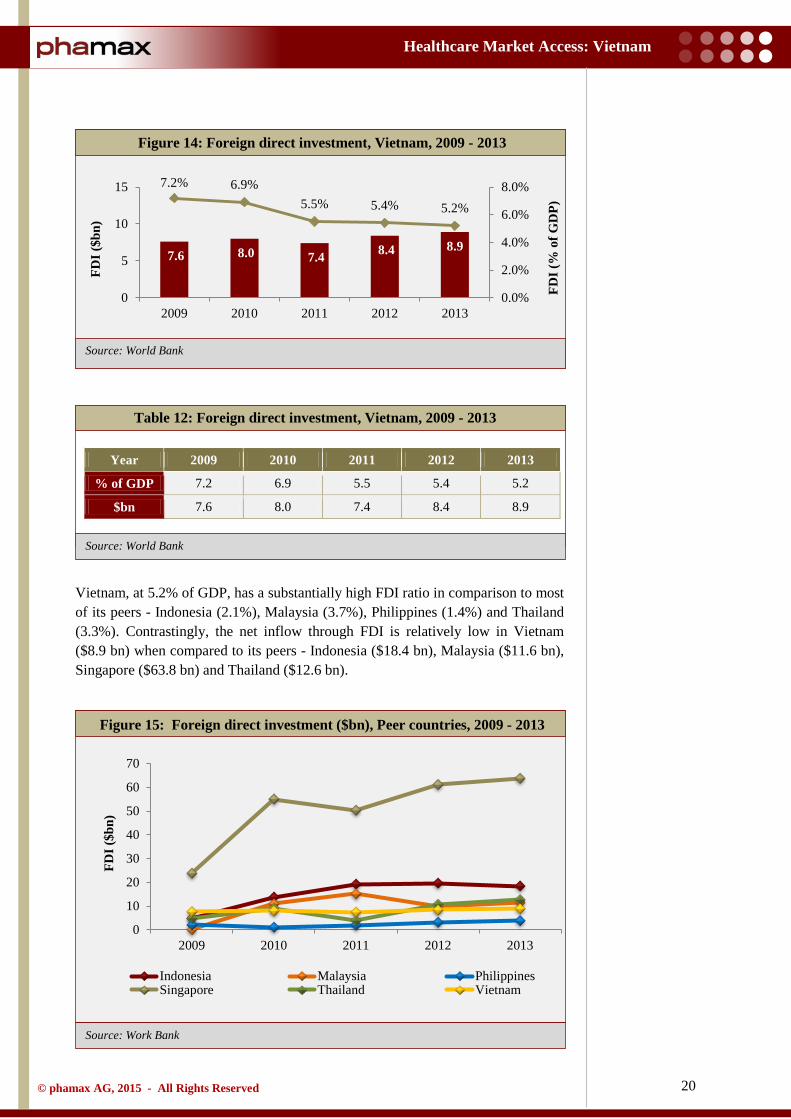

1.2.8 Foreign direct investment

Vietnam has had a relatively short Foreign Direct Investment (FDI) history, boosted with the introduction of ‘Doi Moi’ in the late 1980s. However, various economic factors like high inflation, unstable currency, inconsistent economic growth and uncertainty over government policies stifled foreign investment interests. Consequent to negotiations that extended beyond a decade, Vietnam joined the World Trade Organization (WTO) in 2007, which opened up its coffers to foreign investors. As per the studies of the General Statistics Office (GSO), companies with FDI contribute 20% to Vietnam’s GDP and account for almost two-thirds of the nation’s export turnover.

Majority of the current foreign direct investment (FDI) inflows into Vietnam come from more developed Asian countries, including Japan, Singapore and Korea. While FDI has been higher than expected, a decline is imminent and there have been evident signs of a downward slide. Despite several new large scale Japanese investment projects, the FDI in Vietnam has dropped sharply in recent years.

As per the expert opinion of the National Financial Supervisory Committee (NFSC), the current trend of above-average FDI inflows is expected to continue in Vietnam through 2015, with an expected growth from 5.6% (2014) to 5.8% in 2015.

Figure 13: Exchange rate (VND per USD), Vietnam, 2009 - 2013

17,065 18,613

20,510 20,828 20,993

0

5,000

10,000

15,000

20,000

25,000

2009 2010 2011 2012 2013

VN

D p

er $

Companies with FDI contribute 20% to Vietnam’s GDP and account for almost two-thirds of the nation’s export turnover.

20

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: World Bank

Source: World Bank

Source: Work Bank

Table 12: Foreign direct investment, Vietnam, 2009 - 2013

Year 2009 2010 2011 2012 2013

% of GDP 7.2 6.9 5.5 5.4 5.2

$bn 7.6 8.0 7.4 8.4 8.9

Vietnam, at 5.2% of GDP, has a substantially high FDI ratio in comparison to most of its peers - Indonesia (2.1%), Malaysia (3.7%), Philippines (1.4%) and Thailand (3.3%). Contrastingly, the net inflow through FDI is relatively low in Vietnam ($8.9 bn) when compared to its peers - Indonesia ($18.4 bn), Malaysia ($11.6 bn), Singapore ($63.8 bn) and Thailand ($12.6 bn).

Figure 14: Foreign direct investment, Vietnam, 2009 - 2013

Figure 15: Foreign direct investment ($bn), Peer countries, 2009 - 2013

7.6 8.0 7.4 8.4 8.9

7.2% 6.9% 5.5% 5.4% 5.2%

0.0%

2.0%

4.0%

6.0%

8.0%

0

5

10

15

2009 2010 2011 2012 2013

FDI (

% o

f GD

P)

FDI (

$bn)

0

10

20

30

40

50

60

70

2009 2010 2011 2012 2013

FDI (

$bn)

Indonesia Malaysia PhilippinesSingapore Thailand Vietnam

21

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: World Bank

Source: Work Bank

Table 13: Foreign direct investment ($bn), Peer countries, 2009 - 2013

Year 2009 2010 2011 2012 2013

Indonesia 4.9 13.8 19.2 19.6 18.4

Malaysia 0.1 10.9 15.1 9.7 11.6

Philippines 2.1 1.1 2.0 3.2 3.9

Singapore 23.8 55.1 50.4 61.2 63.8

Thailand 4.9 9.1 3.9 10.7 12.6

Vietnam 7.6 8.0 7.4 8.4 8.9

Note: Size of the bubble indicate the 2013, FDI inflows in respective countries

Figure 16: GDP vs foreign direct investment, Peer countries, 2013

Indonesia, $18.4bn

Malaysia, $11.6bn

Philippines, $3.9bn

Singapore, $63.8bn

Thailand, $12.6bn

Vietnam, $8.9bn

0

200

400

600

800

1000

1200

0 5 10 15 20 25

GD

P (c

urre

nt $

bn)

Foreign Direct Investment, inflows (FDI, % of GDP)

22

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: Work Bank

Source: World Bank

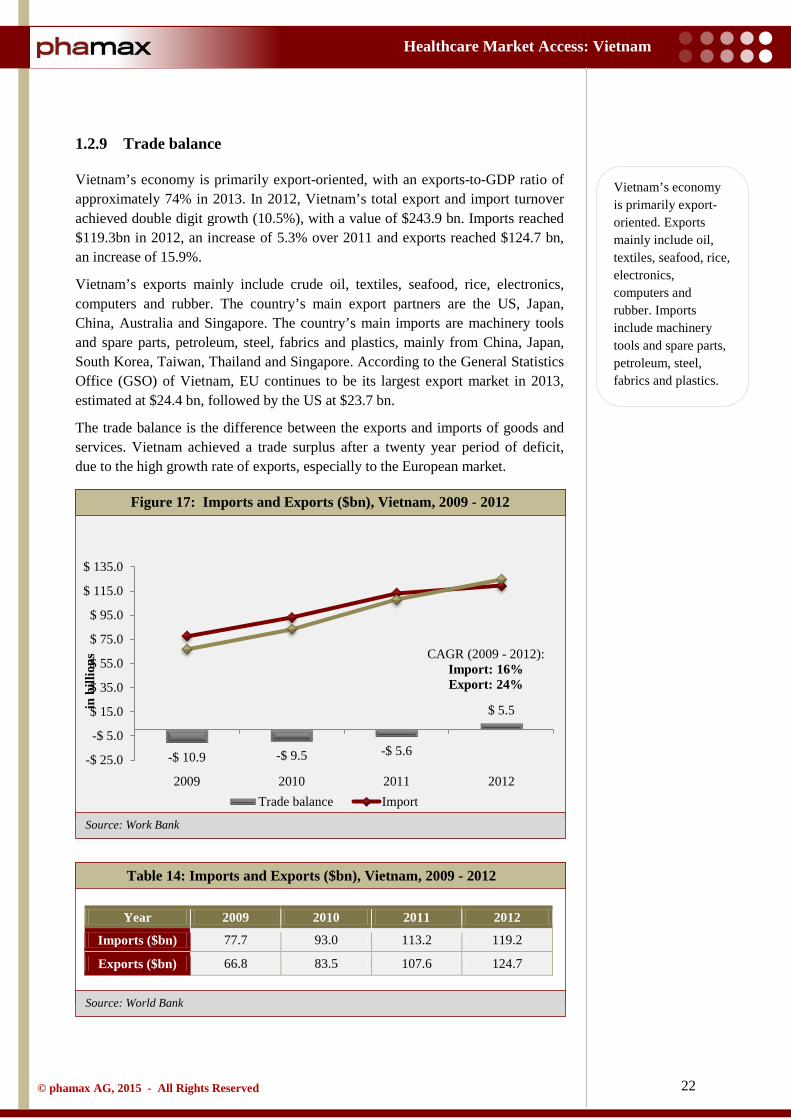

1.2.9 Trade balance

Vietnam’s economy is primarily export-oriented, with an exports-to-GDP ratio of approximately 74% in 2013. In 2012, Vietnam’s total export and import turnover achieved double digit growth (10.5%), with a value of $243.9 bn. Imports reached $119.3bn in 2012, an increase of 5.3% over 2011 and exports reached $124.7 bn, an increase of 15.9%.

Vietnam’s exports mainly include crude oil, textiles, seafood, rice, electronics, computers and rubber. The country’s main export partners are the US, Japan, China, Australia and Singapore. The country’s main imports are machinery tools and spare parts, petroleum, steel, fabrics and plastics, mainly from China, Japan, South Korea, Taiwan, Thailand and Singapore. According to the General Statistics Office (GSO) of Vietnam, EU continues to be its largest export market in 2013, estimated at $24.4 bn, followed by the US at $23.7 bn.

The trade balance is the difference between the exports and imports of goods and services. Vietnam achieved a trade surplus after a twenty year period of deficit, due to the high growth rate of exports, especially to the European market.

Table 14: Imports and Exports ($bn), Vietnam, 2009 - 2012

Year 2009 2010 2011 2012

Imports ($bn) 77.7 93.0 113.2 119.2

Exports ($bn) 66.8 83.5 107.6 124.7

Figure 17: Imports and Exports ($bn), Vietnam, 2009 - 2012

-$ 10.9 -$ 9.5 -$ 5.6

$ 5.5

-$ 25.0

-$ 5.0

$ 15.0

$ 35.0

$ 55.0

$ 75.0

$ 95.0

$ 115.0

$ 135.0

2009 2010 2011 2012

in b

illio

ns

Trade balance Import

CAGR (2009 - 2012): Import: 16% Export: 24%

Vietnam’s economy is primarily export-oriented. Exports mainly include oil, textiles, seafood, rice, electronics, computers and rubber. Imports include machinery tools and spare parts, petroleum, steel, fabrics and plastics.

23

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: World Bank

Source: World Bank

1.3 Demographics

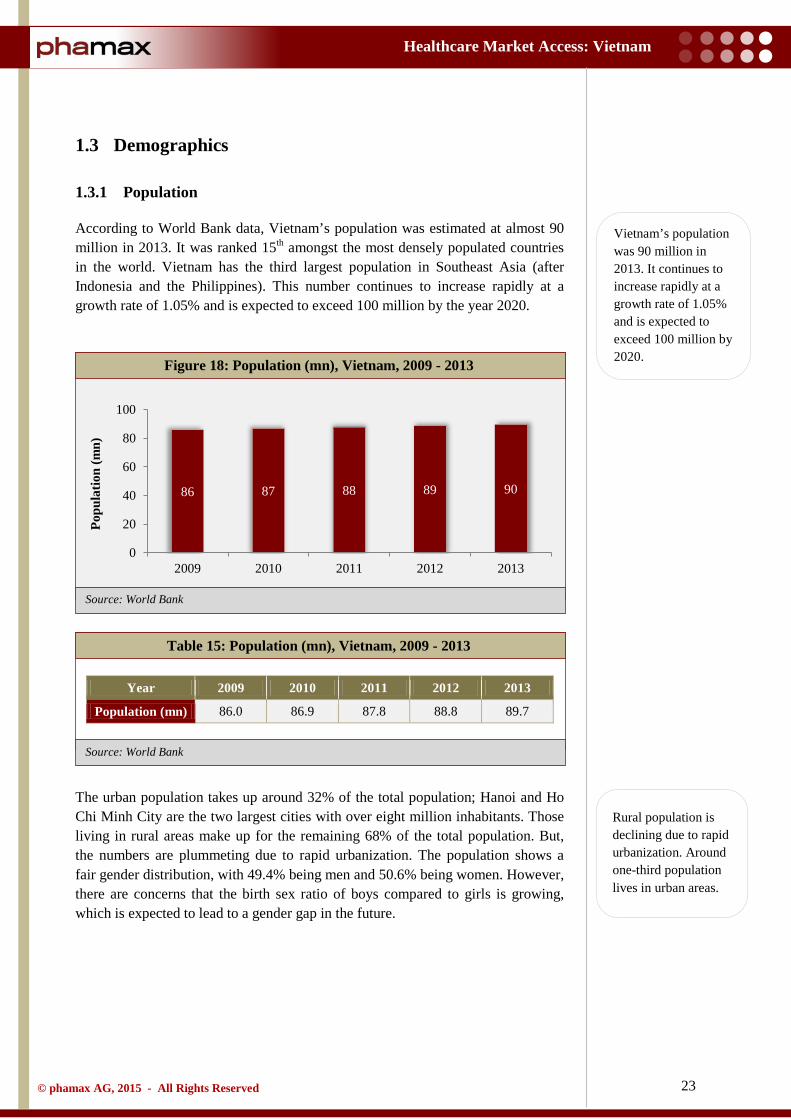

1.3.1 Population

According to World Bank data, Vietnam’s population was estimated at almost 90 million in 2013. It was ranked 15th amongst the most densely populated countries in the world. Vietnam has the third largest population in Southeast Asia (after Indonesia and the Philippines). This number continues to increase rapidly at a growth rate of 1.05% and is expected to exceed 100 million by the year 2020.

Table 15: Population (mn), Vietnam, 2009 - 2013

Year 2009 2010 2011 2012 2013

Population (mn) 86.0 86.9 87.8 88.8 89.7

The urban population takes up around 32% of the total population; Hanoi and Ho Chi Minh City are the two largest cities with over eight million inhabitants. Those living in rural areas make up for the remaining 68% of the total population. But, the numbers are plummeting due to rapid urbanization. The population shows a fair gender distribution, with 49.4% being men and 50.6% being women. However, there are concerns that the birth sex ratio of boys compared to girls is growing, which is expected to lead to a gender gap in the future.

Figure 18: Population (mn), Vietnam, 2009 - 2013

86 87 88 89 90

0

20

40

60

80

100

2009 2010 2011 2012 2013

Popu

latio

n (m

n)

Vietnam’s population was 90 million in 2013. It continues to increase rapidly at a growth rate of 1.05% and is expected to exceed 100 million by 2020.

Rural population is declining due to rapid urbanization. Around one-third population lives in urban areas.

24

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: World Bank

Source: World Bank

Table 16: Urban and rural population (mn), Vietnam, 2009 - 2013

Year 2009 2010 2011 2012 2013

Rural (mn) 60.4 60.5 60.6 60.7 60.7

Urban (mn) 25.6 26.4 27.3 28.1 29.0

In 2012, the life expectancy in Vietnam was 75.6 years, with 80.4 years for women and 71.1 years for men.

Vietnam has a young population structure, with the age group of 14 - 64 years constituting almost 71% of the total population, with other age groups (0 - 14 years) and ( > 65 years) being 23% and 7% respectively. The United Nations with the General Statistics Office (GSO), released a publication with the general census of population in Vietnam in 2009, stating that the nation had a period of ‘golden population structure’, i.e., the number of working people exceeded the number of dependent people. This ratio clearly indicated a steady supply of labor for manufacturers and suppliers, which further reinforced Vietnam as a land of lucrative opportunities for foreign investment and outsourcing.

Figure 19: Urban and rural population share (%), Vietnam, 2009 - 2013

70% 70% 69% 68% 68%

30% 30% 31% 32% 32%

2009 2010 2011 2012 2013

% o

f tot

al p

opul

atio

n

Rural Urban

Vietnam has a young population. The age group of 14 to 64 years constitutes almost 71% of the total population.

25

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: World Bank

Source: World Bank

Table 17: Population distribution by age groups (%), Vietnam, 2009 - 2013

Year 2009 2010 2011 2012 2013

Ages 0 – 14 (% of total) 24 23 23 23 23

Ages 15 – 64 (% of total) 69 70 70 71 71

Ages 64 and above (% of total) 7 7 7 7 7

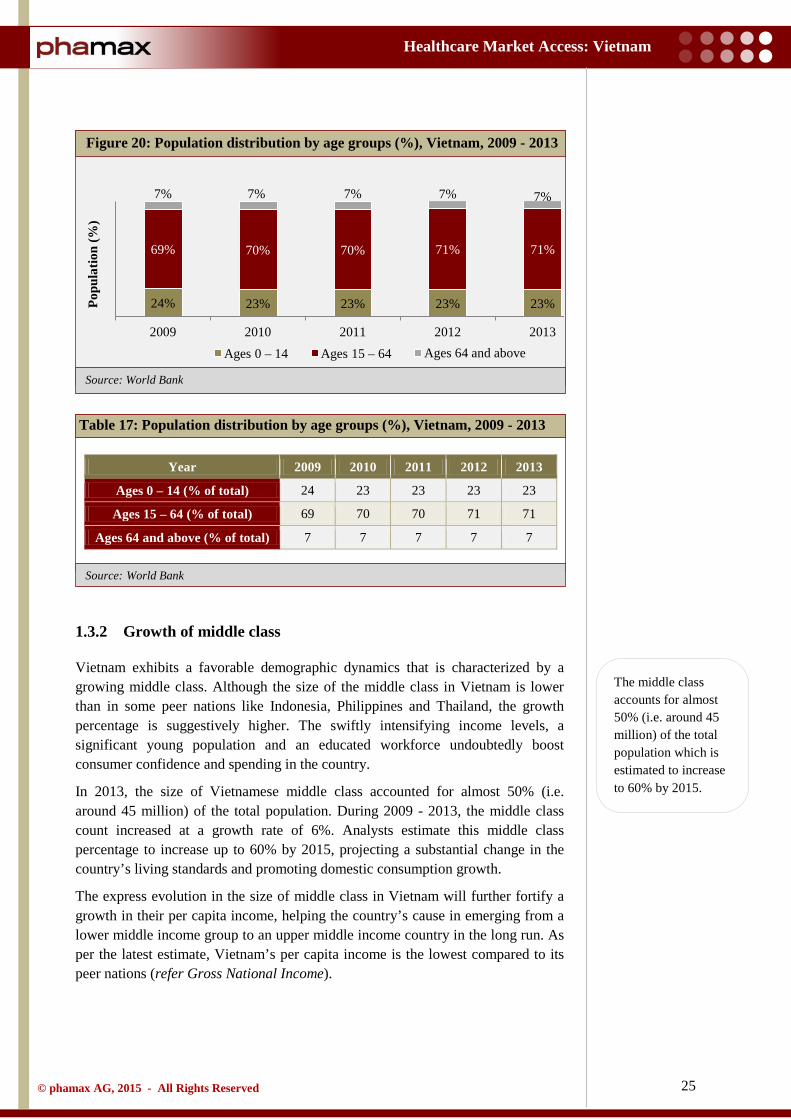

1.3.2 Growth of middle class

Vietnam exhibits a favorable demographic dynamics that is characterized by a growing middle class. Although the size of the middle class in Vietnam is lower than in some peer nations like Indonesia, Philippines and Thailand, the growth percentage is suggestively higher. The swiftly intensifying income levels, a significant young population and an educated workforce undoubtedly boost consumer confidence and spending in the country.

In 2013, the size of Vietnamese middle class accounted for almost 50% (i.e. around 45 million) of the total population. During 2009 - 2013, the middle class count increased at a growth rate of 6%. Analysts estimate this middle class percentage to increase up to 60% by 2015, projecting a substantial change in the country’s living standards and promoting domestic consumption growth.

The express evolution in the size of middle class in Vietnam will further fortify a growth in their per capita income, helping the country’s cause in emerging from a lower middle income group to an upper middle income country in the long run. As per the latest estimate, Vietnam’s per capita income is the lowest compared to its peer nations (refer Gross National Income).

Figure 20: Population distribution by age groups (%), Vietnam, 2009 - 2013

24% 23% 23% 23% 23%

69% 70% 70% 71% 71%

7% 7% 7% 7% 7%

2009 2010 2011 2012 2013

Popu

latio

n (%

)

Ages 0 – 14 Ages 15 – 64 Ages 64 and above

The middle class accounts for almost 50% (i.e. around 45 million) of the total population which is estimated to increase to 60% by 2015.

26

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: World Bank

1.3.3 Education and literacy

Although rated an underprivileged country with a low per capita income, Vietnam has persistently evolved in nurturing and preserving high literacy rates. According to the CIA World Fact book, the country’s literacy rate is 93.4% (95.4% for men and 91.4% for women). The literacy rate of Vietnam is higher than that of Malaysia and Indonesia, but lower than Singapore, Philippines and Thailand.

In 2005, the National Assembly of Vietnam approved a legislature, stating compulsory education at the primary and lower secondary levels. Demonstrating its keenness on the priority of education, the government of Vietnam has always allocated a part of its budget for the same. It had set substantial goals, under the Socio Economic Development Plan 2006 - 2010 and further reinforced it with the Resolution on Comprehensive and Fundamental Reform of Higher Education in Vietnam 2006 - 2020. The major objective of such plans was to increase enrolment in universities and colleges, increase proportion of qualified teachers and encourage private establishments with high-quality education and management.

Figure 21 displays the trends of Gross Enrolment Ratios for different levels of education in Vietnam. Gross Enrolment Ratio (GER) is the total enrolment, regardless of age, expressed as a percentage of the population. GER can exceed 100% based on the inclusion of over-aged and under-aged students because of early or late school entrances and grade repetitions.

The GER of pre-primary education in Vietnam has steadily increased from 66.7% in 2009 to 77.2% in 2012. The GER of primary education slightly decreased to 104.7% in 2012, although this decline was inconsistent. The Gross Enrolment Ratio of secondary education was not reflected whilst GER of tertiary education steadily increased during the period 2008 - 2012.

Figure 21: Gross enrolment ratio, Vietnam, 2009 - 2012

67 69 72 77

103 105 105 105

20 22 24 25 0

40

80

120

2009 2010 2011 2012

Gro

ss e

nrol

lmen

t ra

tio

Preprimary Primary Tertiary

In spite of a low per capita income, Vietnam has a high literacy rate of 93%.

27

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: World Bank

Source: World Bank

Table 18: Gross enrolment ratio, Vietnam, 2009 - 2013

Year 2009 2010 2011 2012

GER, pre - primary 44.8 40.4 41.5 47.6

GER, primary 109.9 109.9 109.1 108.5

GER, secondary 76.5 78.4 81.2 82.5

GER, tertiary 23.7 24.9 27.2 31.5

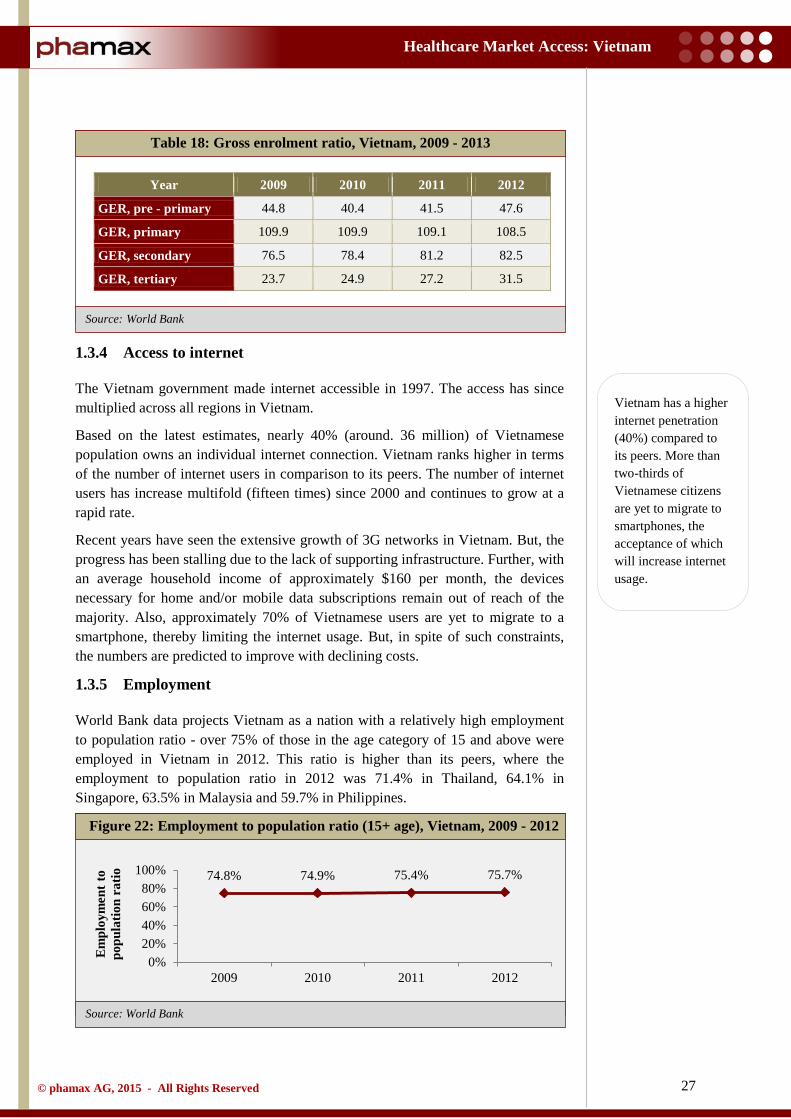

1.3.4 Access to internet

The Vietnam government made internet accessible in 1997. The access has since multiplied across all regions in Vietnam.

Based on the latest estimates, nearly 40% (around. 36 million) of Vietnamese population owns an individual internet connection. Vietnam ranks higher in terms of the number of internet users in comparison to its peers. The number of internet users has increase multifold (fifteen times) since 2000 and continues to grow at a rapid rate.

Recent years have seen the extensive growth of 3G networks in Vietnam. But, the progress has been stalling due to the lack of supporting infrastructure. Further, with an average household income of approximately $160 per month, the devices necessary for home and/or mobile data subscriptions remain out of reach of the majority. Also, approximately 70% of Vietnamese users are yet to migrate to a smartphone, thereby limiting the internet usage. But, in spite of such constraints, the numbers are predicted to improve with declining costs.

1.3.5 Employment

World Bank data projects Vietnam as a nation with a relatively high employment to population ratio - over 75% of those in the age category of 15 and above were employed in Vietnam in 2012. This ratio is higher than its peers, where the employment to population ratio in 2012 was 71.4% in Thailand, 64.1% in Singapore, 63.5% in Malaysia and 59.7% in Philippines.

Figure 22: Employment to population ratio (15+ age), Vietnam, 2009 - 2012

74.8% 74.9% 75.4% 75.7%

0%20%40%60%80%

100%

2009 2010 2011 2012

Em

ploy

men

t to

popu

latio

n ra

tio

Vietnam has a higher internet penetration (40%) compared to its peers. More than two-thirds of Vietnamese citizens are yet to migrate to smartphones, the acceptance of which will increase internet usage.

28

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: World Bank

Source: World Bank Data

Source: GSO Vietnam

Table 19: Employment to population ratio (15+ age), Vietnam, 2009 - 2012

Year 2009 2010 2011 2012

% of total labor force 74.8 74.9 75.4 75.7

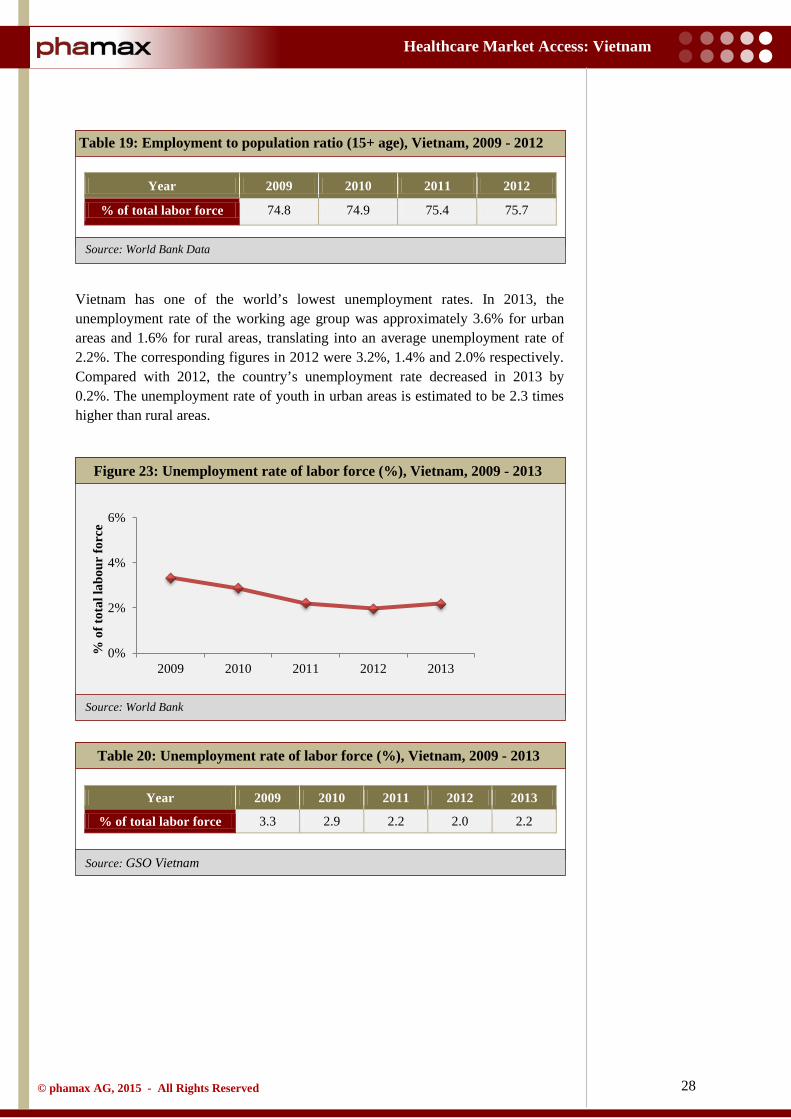

Vietnam has one of the world’s lowest unemployment rates. In 2013, the unemployment rate of the working age group was approximately 3.6% for urban areas and 1.6% for rural areas, translating into an average unemployment rate of 2.2%. The corresponding figures in 2012 were 3.2%, 1.4% and 2.0% respectively. Compared with 2012, the country’s unemployment rate decreased in 2013 by 0.2%. The unemployment rate of youth in urban areas is estimated to be 2.3 times higher than rural areas.

Table 20: Unemployment rate of labor force (%), Vietnam, 2009 - 2013

Year 2009 2010 2011 2012 2013

% of total labor force 3.3 2.9 2.2 2.0 2.2

Figure 23: Unemployment rate of labor force (%), Vietnam, 2009 - 2013

0%

2%

4%

6%

2009 2010 2011 2012 2013

% o

f tot

al la

bour

forc

e

29

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: GSO Vietnam

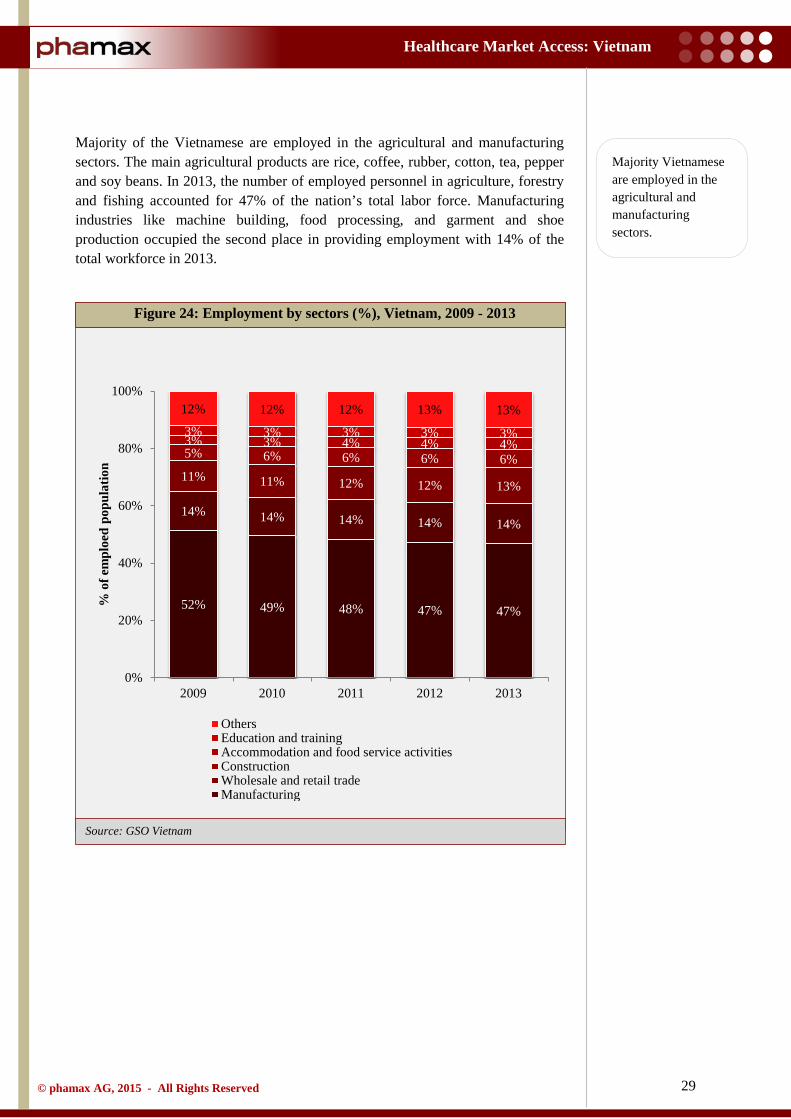

Majority of the Vietnamese are employed in the agricultural and manufacturing sectors. The main agricultural products are rice, coffee, rubber, cotton, tea, pepper and soy beans. In 2013, the number of employed personnel in agriculture, forestry and fishing accounted for 47% of the nation’s total labor force. Manufacturing industries like machine building, food processing, and garment and shoe production occupied the second place in providing employment with 14% of the total workforce in 2013.

Figure 24: Employment by sectors (%), Vietnam, 2009 - 2013

52% 49% 48% 47% 47%

14% 14% 14% 14% 14%

11% 11% 12% 12% 13%

5% 6% 6% 6% 6% 3% 3% 4% 4% 4% 3% 3% 3% 3% 3%

12% 12% 12% 13% 13%

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 2013

% o

f em

ploe

d po

pula

tion

OthersEducation and trainingAccommodation and food service activitiesConstructionWholesale and retail tradeManufacturing

Majority Vietnamese are employed in the agricultural and manufacturing sectors.

30

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

1.4 Political structure and environment

The Socialist Republic of Vietnam is a law governed state and one of the world's few remaining one-party communist states. The current political system of Vietnam encompasses the Communist Party of Vietnam (CPV), political organizations, socio-political organizations, socio-professional organizations, and mass associations.

The Communist Party of Vietnam (CPV) includes the Central Committee, which is a very powerful institution in Vietnam and formally vests much of the political power. It comprises 175 full and 25 alternate members elected at the Party Congress, held every five years (the Twelfth Party Congress is scheduled for 2016). The Central Committee meets twice a year and acts as the CPV's supreme decision-making body. The Central Committee elects a Politburo (currently sixteen members), which runs Party affairs. The three most powerful political positions in Vietnam are those of the General Secretary of the CPV, the Prime Minister and the President.

The President is elected by the National Assembly for a five year term and acts as the Commander-in- Chief of the Armed Forces and Chairman of the Council for Defense and Security. The government is the main executive power in Vietnam and is headed by the Prime Minister. The Prime Minister is elected by a proposal of the President of Vietnam to the National Assembly. The Prime Minister is responsible to the National Assembly, which elects all ministers of the government.

The country has a unicameral National Assembly, whose 450 members are elected every five years. The National Assembly exercises three main functions: to legislate, to decide on important national issues, to exercise supreme supervision over all activities of the state. In the last held election for the National Assembly in 2011, 92% of those elected were members from the CPV. In recent years, the National Assembly has been increasingly active and influential in setting national priorities and has become more assertive in exercising its authority over law making. However, it is still subject to the Communist Party directions.

Vietnam has an independent judicial system governed by the Constitution of Vietnam. However, lawyers are not available in ample numbers and the judicial system does not have the relevant power to administer law.

The increasing role of the National Assembly in reviewing legislation and policies and a more incisive media has contributed to greater transparency in Vietnam. On the flip side, individuals can incur long prison terms for broadly framed charges, such as spying, minor acts against national security and propaganda against the state.

Vietnam is one of the world's few remaining one-party communist states with the Communist Party of Vietnam (CPV) in power.

31

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

1.4.1 Current government

The government is the executive body of the National Assembly, the highest body of state administration in Vietnam. It manages the overall political, economic, cultural, social and national (defense, security and external duties) duties of the state.

The government is accountable to the National Assembly and reports to it, its Standing Committee, and the country's President. The government consists of the Prime Minister, who is a designated National Assembly deputy as declared by the Constitution, Deputy Prime Ministers, Ministers and other members.

In 2011, the CPV’s central committee re-elected Prime Minister Nguyen Tan Dung to the Politburo for a second five year term. In 2010, he was under tremendous public pressure to resign after a scandal involving a prominent ship building group, Vinashin. Several Vinashin officials were jailed for their roles in the scandal. But, he was spared disciplinary action by the Communist Party. Analysts believe that despite concerns about economic instability, Dung is widely expected to be re-appointed as Prime Minister for another term. However, the leaders will need to tame the inflation and mitigate further risks in the economic growth to justify re-election.

Earlier, under Dung's leadership, international human rights groups had accused Vietnam of taking a more than usual tougher stance against political rebels, including those peacefully expressing their views online. But the government has minimum any threat to its one - party rule, and people can be jailed for publicly demanding a multiparty system.

Truong Tan Sang was elected as the President in July 2011, winning 97% of the votes in parliament. Meanwhile, the Communist Party appointed Nguyen Phu Trong as its Secretary General in January 2011, replacing Nong Duc Manh, who retired after ten years of active service.

The government is the executive body of the National Assembly, the highest body of state administration in Vietnam.

The CPV’s central committee re-elected Prime Minister Nguyen Tan Dung to a second five year term in 2011. Truong Tan Sang was elected as the President in July 2011.

32

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

1.5 Trade associations

1.5.1 Vietnam Pharmaceutical Companies Association

Vietnam Pharmaceutical Companies Association (VNPCA) is a trade association that invites pharmaceutical companies to join its community and represents them. The main motive of the association is to benefit the community in alignment with the growth and nurture of the enterprises, enhance the Vietnamese pharmaceutical brands in the domestic and global markets and ultimately contribute to the development of the nation and the pharmaceutical industry

After nine years of operations, the association has assembled nearly hundred top Vietnamese pharmaceutical firms, assisted them in updating industry and legal information, accelerated trade promotion activities, provided consultancy and training, and acted as a bridge between enterprises and government organizations and the community.

33

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

1.6 Opportunity and challenges

Vietnam is a growing economy in the Asia Pacific region, and therefore provides lucrative opportunities for investors.

In 2013, the macroeconomic conditions in Vietnam were relatively stable and the country’s economy fought back to recover from earlier slumps. However, the struggle to boost the economy remains, In 2012, the decline in bank lending affected domestic demand, mounting pressure on the government to overhaul the financial system, thus deferring the economic growth. Added to this, a corrupt and bureaucratic administration was ineffective in taking the relevant measures to curtail entrepreneurs and investors.

Vietnam’s economy is bound to face adversities in the coming years, due to bad debts, liquidity of commercial banks and a shrinking market for locally manufactured goods. Unless domestic enterprises take initiatives to restructure themselves, cut production costs, develop strategies to multiply their business, seize opportunities as they arise, find means to access economical fund supplies, the supply and value chain in both domestic and international markets will remain affected. This, in turn, will pose risks in controlling inflation, reducing trade and budget deficit, attracting more foreign investment, reducing unemployment and ensuring social security.

In accordance with its economy boosting initiatives, in 2012, Vietnam revealed a broad ‘three pillar’ economic reform program, proposing the restructuring of public investment, State Owned Enterprises (SOEs) and the banking sector. However, the progress has been at a snail’s pace under the program.

The Vietnamese government initiatives under the Socio-Economic Development plan for the period 2011 - 2020 outlines a group of effective measures to accelerate the economic restructuring process. In line with this plan, in 2013, the government persisted in tightening the monetary policy, prioritizing macro stability and managing inflation at moderately low levels. Additionally, the government’s prime focus areas have always been clearing bad debts and restructuring state owned enterprises, two strategies that are imperative to drive economic growth in the upcoming years. But, the modifications are destined to happen only gradually.

A survey by the American Chamber of Commerce (AmCham) in Singapore reveals that American companies intend to slot Vietnam after Indonesia in Southeast Asia for investments in the coming years, replacing China. Notable trade agreements like the Trans-Pacific Partnership Agreement (TPP) and the EU - Vietnam Free Trade Agreement (EVFTA) are also positive moves to augment trade and boost investment activities in Vietnam.

Moreover, the large and increasingly affluent population represents a large workforce and an under-served consumer market providing an attractive avenue for foreign investors.

Vietnam’s economy is bound to face adversities in the coming years, due to bad debts, liquidity of commercial banks and a shrinking market for locally manufactured goods. However, recently signed trade agreements with the West will have a favorable impact on trade and investments.

34

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

2 Healthcare Infrastructure

2.1 Healthcare system

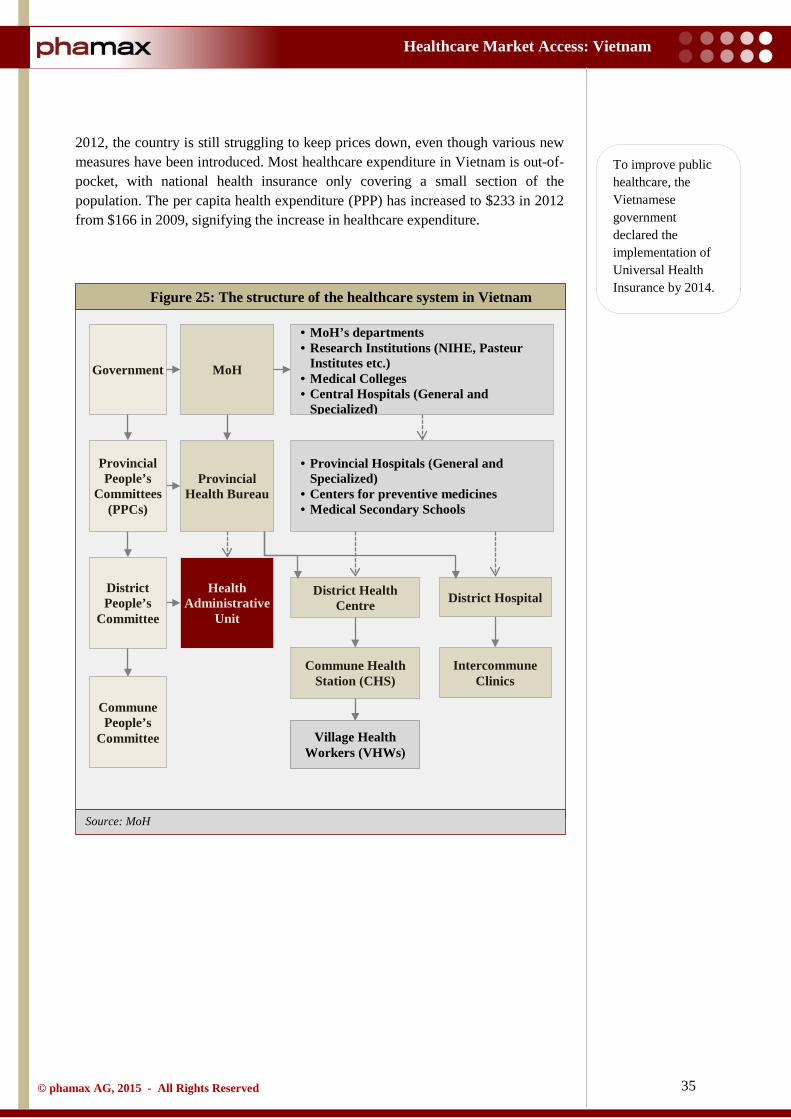

Since the introduction of the economic reforms initiated by ‘Doi Moi’ in 1986, Vietnam has made steady progress in healthcare. The country’s health indicators are better, and continue to improve at rates that equal or surpass its peers. The health sector is seeing a dramatic transformation due to programs concentrated on alleviating poverty and growing the economy. Twenty years ago, the country’s healthcare was firmly controlled by the central government, like any other socialist healthcare system. But, due to the rapid growth of the private sector, larger role of out-of-pocket expenditures, and the ongoing decentralization process, the role of the Ministry of Health (MoH) to shape activities has diminished significantly.

Vietnam healthcare system is a mix of public and private systems, in which the public system plays a key role, especially in policy, prevention, research and training. The public healthcare administration is organized at three levels - central, principal and local. At the central level, the Ministry of Health (MoH) formulates and executes health policies. It also directly controls and finances research institutions, and general and specialized hospitals. At the provincial level, there are 63 provincial health bureaus that follow the MoH policies, but are a part of local provincial governments under the Provincial People’s Committees (PPCs). These provincial health bureaus manage the provincial hospitals and Centers for Preventive Medicine, while the PPCs control their administration and financial aspects. At the primary level, there are Commune Health Stations (CHS), Village Health Workers (VHW) and district hospitals. They provide basic services like primary care, including preventive care, access to drugs, family planning and overall health promotion in the community.

The public healthcare expenditure in Vietnam is funded by the state’s limited budget because it is still a developing country. State hospitals do not have access to modern equipment because of restricted budgets. Consequently, the quality of service in state hospitals is weak, and not enough to cover the demand of patients, especially from the province levels to commune levels. Hence, the optimum choice for healthcare is the private sector. For example, in 2012, the health expenditure accounted for 6.6% of GDP, wherein government expenditure was just 42.6% and the rest was private expenditure.

To counter the inclination towards the private healthcare sector, in 2009, the Vietnamese Government declared the implementation of Universal Health Insurance by 2014. Since 2010, the government has been working for universal coverage with Vietnamese Social Security, a government affiliated agency responsible for implementation of health insurance policy in the country.

The chief concern for the Vietnamese government is to make healthcare universal and affordable to its population, especially in the case of pharmaceutical prices, which account for a significant portion of annual expenditure on health. But, since

The public sector is unable to cater to patient demands and lacks quality due to limited budgets. Hence, private expenditure is comparatively higher.

Vietnam healthcare system is a mix of public and private systems. In the public sector, the healthcare administration is organized at three levels: central, provincial and local.

35

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: MoH

2012, the country is still struggling to keep prices down, even though various new measures have been introduced. Most healthcare expenditure in Vietnam is out-of-pocket, with national health insurance only covering a small section of the population. The per capita health expenditure (PPP) has increased to $233 in 2012 from $166 in 2009, signifying the increase in healthcare expenditure.

Figure 25: The structure of the healthcare system in Vietnam

To improve public healthcare, the Vietnamese government declared the implementation of Universal Health Insurance by 2014.

Government

Provincial People’s

Committees (PPCs)

District People’s

Committee

Commune People’s

Committee

MoH

Intercommune Clinics

Commune Health Station (CHS)

District Hospital District Health Centre

Provincial Health Bureau

• MoH’s departments • Research Institutions (NIHE, Pasteur

Institutes etc.) • Medical Colleges • Central Hospitals (General and

Specialized)

• Provincial Hospitals (General and Specialized)

• Centers for preventive medicines • Medical Secondary Schools

Health Administrative

Unit

Village Health Workers (VHWs)

36

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved

Source: World Bank

Source: World Bank

2.2 Health status

The health status in Vietnam has shown improvement in the recent years, which is clearly evident in health indicators like average life expectancy at birth, mortality rate under the age of five years, maternal mortality ratio and malnutrition. These progresses are consequences of widespread healthcare delivery networks, increased number of qualified health workers and the expanding national public health programs.

2.2.1 Life expectancy

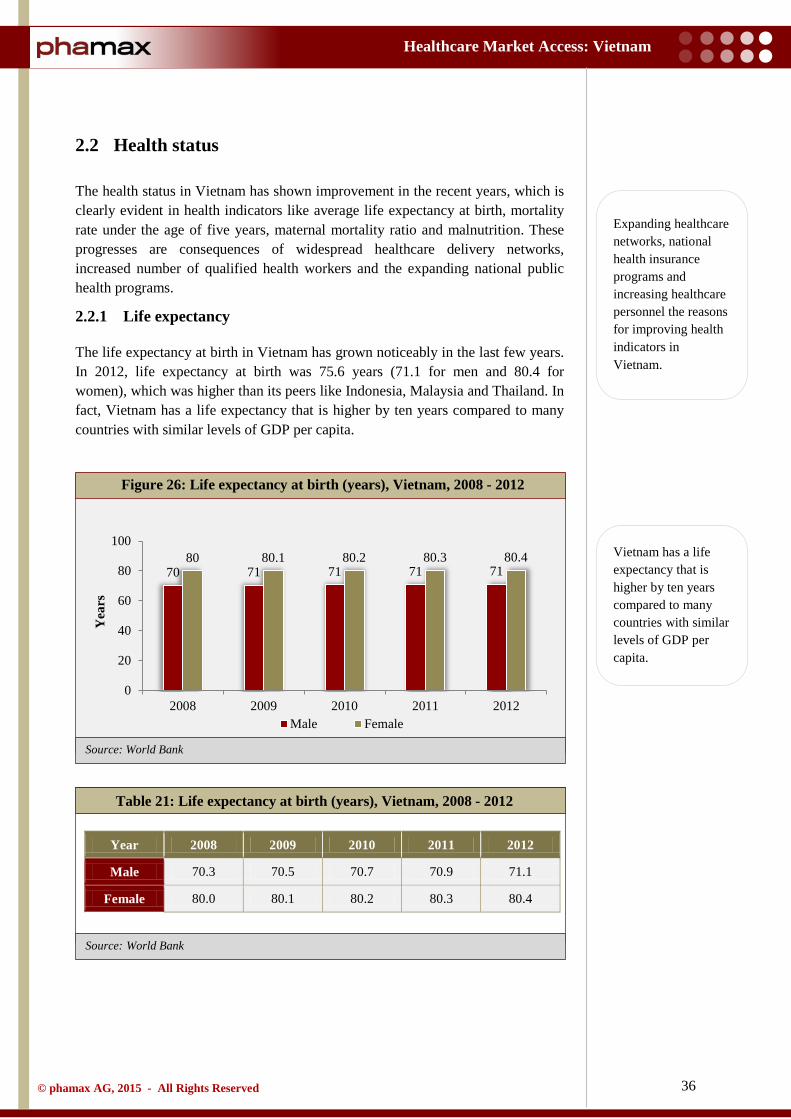

The life expectancy at birth in Vietnam has grown noticeably in the last few years. In 2012, life expectancy at birth was 75.6 years (71.1 for men and 80.4 for women), which was higher than its peers like Indonesia, Malaysia and Thailand. In fact, Vietnam has a life expectancy that is higher by ten years compared to many countries with similar levels of GDP per capita.

Table 21: Life expectancy at birth (years), Vietnam, 2008 - 2012

Year 2008 2009 2010 2011 2012

Male 70.3 70.5 70.7 70.9 71.1

Female 80.0 80.1 80.2 80.3 80.4

Figure 26: Life expectancy at birth (years), Vietnam, 2008 - 2012

70 71 71 71 71 80 80.1 80.2 80.3 80.4

0

20

40

60

80

100

2008 2009 2010 2011 2012

Yea

rs

Male Female

Vietnam has a life expectancy that is higher by ten years compared to many countries with similar levels of GDP per capita.

Expanding healthcare networks, national health insurance programs and increasing healthcare personnel the reasons for improving health indicators in Vietnam.

37

Healthcare Market Access: Vietnam

© phamax AG, 2015 - All Rights Reserved