health plan reporting 101

TRANSCRIPT

06/03/2015

Diane Craney – Office of General Counsel

Mel Grau – Marketing Coordinator

ACA reporting

MEC reporting

Employer reporting

(Form 1095-C)

•

Subject: ACTION REQUIRED: 2014 Transitional Reinsurance Program Contribution Submission Not Found – Case ID #_____

•

•

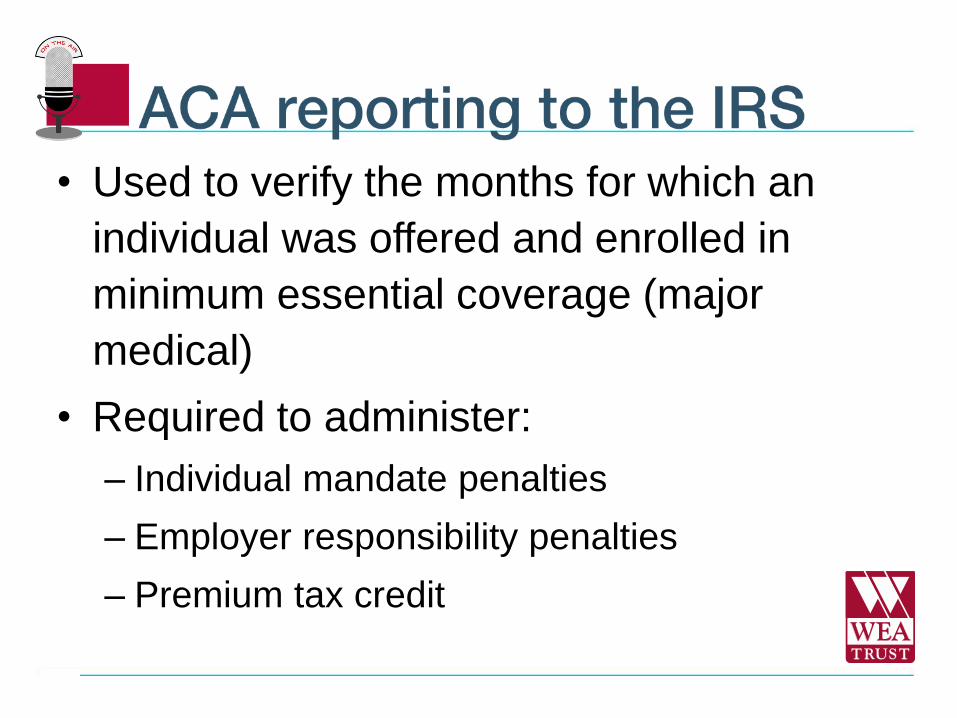

• Used to verify the months for which an

individual was offered and enrolled in

minimum essential coverage (major

medical)

• Required to administer:

– Individual mandate penalties

– Employer responsibility penalties

– Premium tax credit

Statements due to

subscribers

Returns due to IRS

(if filed manually)

Returns due to IRS

(if filed electronically)*

Jan. 31 Feb. 28 Mar. 31

*You must file electronically if you have 250 returns or more

• What is it for?

– Provides individuals and the IRS with

information about minimum essential

coverage

– Verifies whether an individual satisfied the

individual mandate for the preceding calendar

year

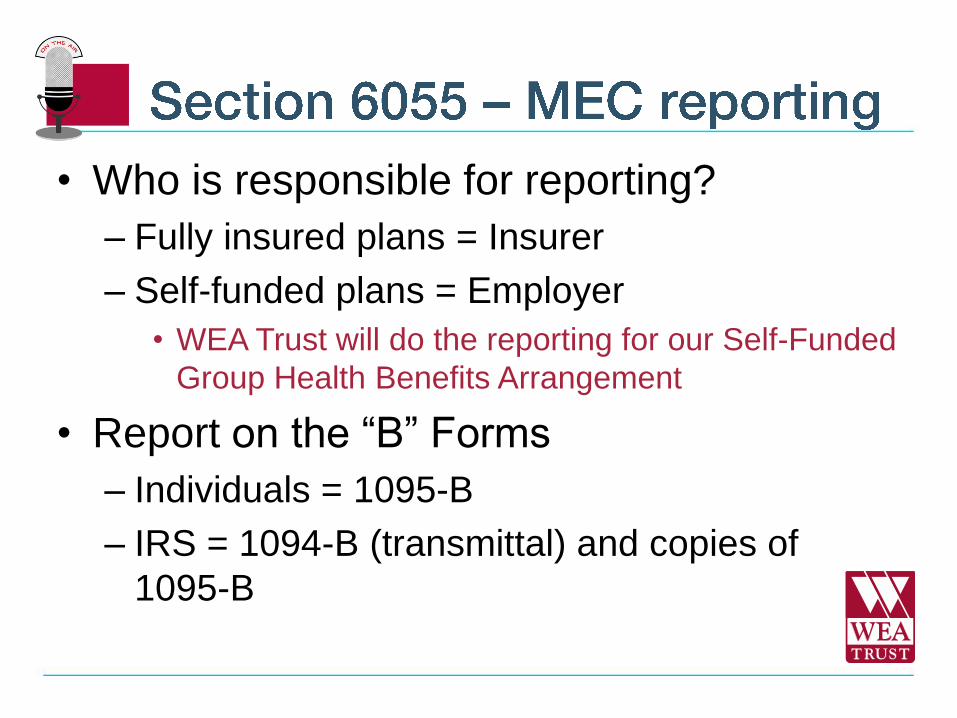

• Who is responsible for reporting?

– Fully insured plans = Insurer

– Self-funded plans = Employer

• WEA Trust will do the reporting for our Self-Funded

Group Health Benefits Arrangement

• Report on the “B” Forms

– Individuals = 1095-B

– IRS = 1094-B (transmittal) and copies of

1095-B

•

•

–

•

–

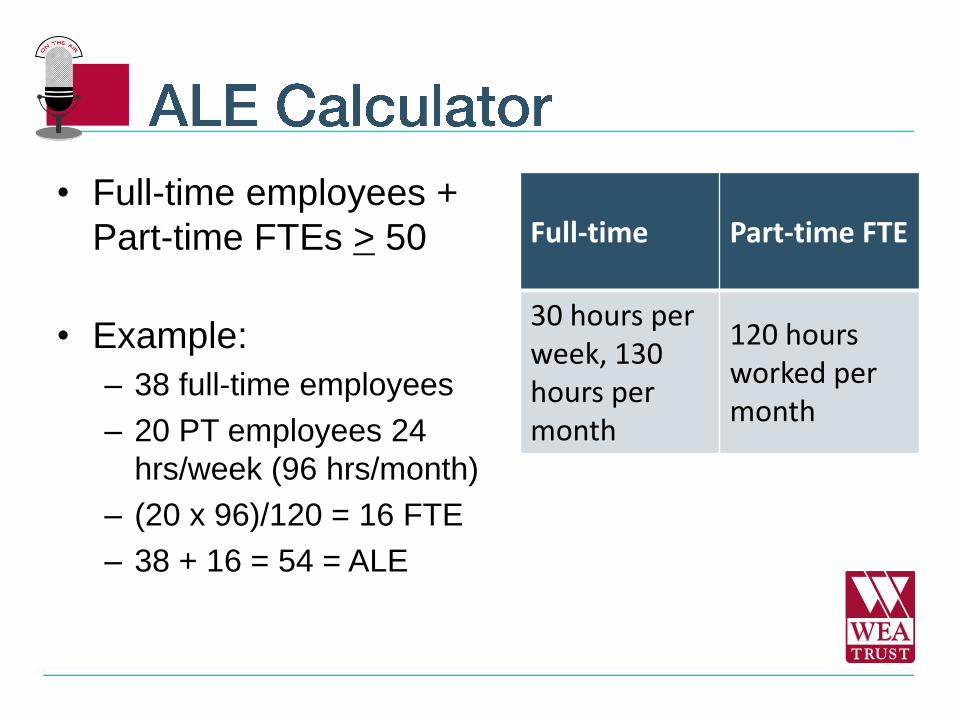

• Full-time employees +

Part-time FTEs > 50

• Example:

– 38 full-time employees

– 20 PT employees 24

hrs/week (96 hrs/month)

– (20 x 96)/120 = 16 FTE

– 38 + 16 = 54 = ALE

Full-time Part-time FTE

30 hours per week, 130 hours per month

120 hours worked per month

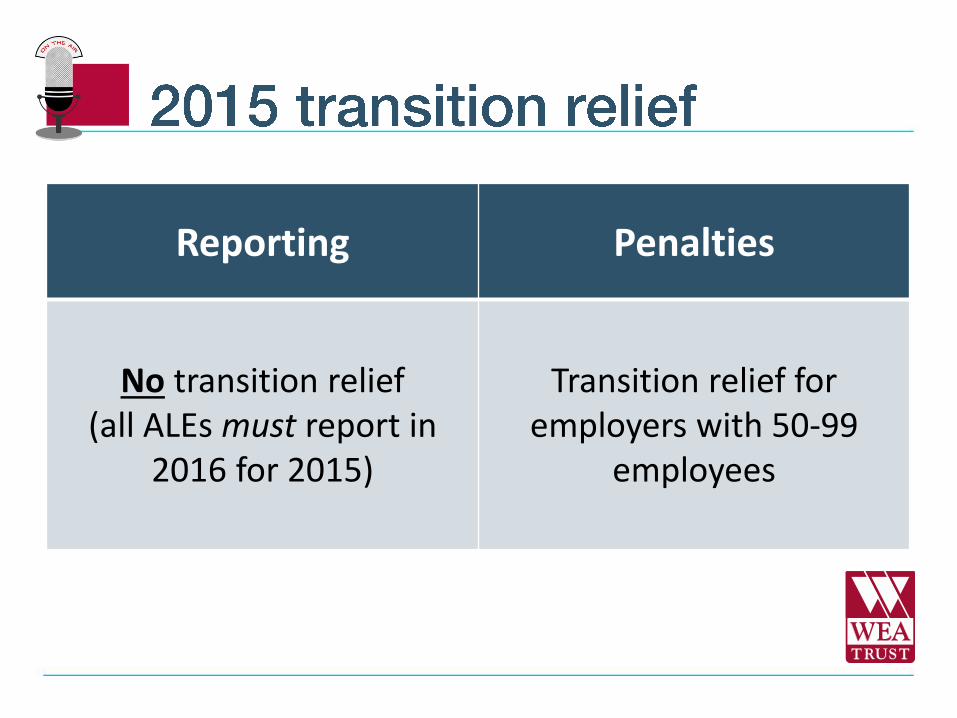

Reporting Penalties

No transition relief (all ALEs must report in

2016 for 2015)

Transition relief for employers with 50-99

employees

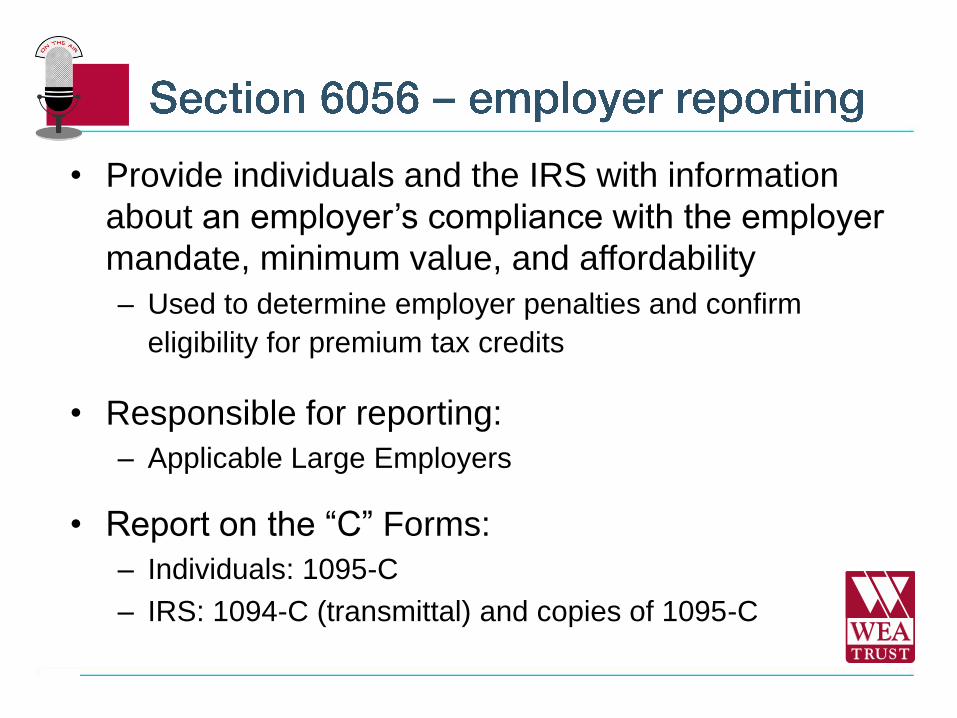

• Provide individuals and the IRS with information

about an employer’s compliance with the employer

mandate, minimum value, and affordability

– Used to determine employer penalties and confirm

eligibility for premium tax credits

• Responsible for reporting:

– Applicable Large Employers

• Report on the “C” Forms:

– Individuals: 1095-C

– IRS: 1094-C (transmittal) and copies of 1095-C

• Statement to every full-time employee

– Mailed to the last known address

– May be mailed with W2s

– May be provided electronically if employee

affirmatively consents for this document

First, determine if you are an ALE.

If you are an ALE:

How will you track information necessary

to file? Who will be responsible?

Who will actually file?

How will you deliver statements? If

electronically, determine how to get

affirmative consent.

Are you eligible for transition relief?