hackett 2012 offshoring forecast

TRANSCRIPT

7/30/2019 Hackett 2012 Offshoring Forecast

http://slidepdf.com/reader/full/hackett-2012-offshoring-forecast 1/9

© 2012 Te Hackett Group, Inc.; All Rights Reserved.Page 1

CR_ES0041

E xEcutivE Summary

The first signs of modest growth are returning to developed economies, resulting in new jobs in corporate business services functions (finance, human resources,IT and procurement) domestically. However, the transformation of global oper-ating models for these support services, which started well before the recession,continues to eliminate jobs (through productivity improvements) or move them

to low-cost geographies. As a result, rather than increasing, the total number of business services jobs located in North America and Europe will actually continueto shrink. According to new research by The Hackett Group, only about 4.5 mil-lion of the 8.2 million business services jobs located in North America and Europeat the start of 2002 will still exist in 2016. Companies in these regions are quickly changing their global operating models to remain competitive. By 2016, thenumber of potentially “offshorable” jobs will have been reduced to one million.This decline has far-reaching implications for India, China and Eastern Europe, which will need to develop alternative sources of demand in order to maintaingrowth in the offshoring/outsourcing business services industries that have ener-gized their economies.

tranSforming BuSinESS SErvicES DElivEry : thE JournEy

continuES

The movement of jobs from developed into low-cost geographies is an increasingly sensitive political issue. Understandably, the recession and subsequent “joblessrecovery” have drawn even more attention to this phenomenon.

From the executive suite perspective, movement of jobs around the globe is anintegral element of the execution of business strategies that increasingly involveglobalization of the operating model of the business. Research by The HackettGroup has covered the globalization trend extensively (see Related Hackett

Research section). In contrast with the continued movement of service jobs off-shore, the movement of manufacturing jobs appears to have reached an equilib-rium with reshoring (see sidebar ). However, manufacturing job movement isdriven by a different set of forces than business services jobs, and analysis of theformer rarely includes the latter.

This research focuses on jobs in business services in finance, IT, procurement andhuman resources. In these pages, we assess the past, current and projected state

By Michel Janssen, Erik Dorr and Martijn Geerling

EntErprisE stratEgy

Management Issue

Job LossEs from offshoring and productivity improvEmEnts f ar outpacE g ains from Economic growth

Projected slowdown in services offshoring after 2014 poses challenge to India and other low-cost destinations

Manufacturing offshoring

and reshoring to reach

equilibrium by 2014

H G nly n-dd sdy n gll mnf-ing sing sgis.

sdy sls indid mnfing indsis n-ing s f qiliim, wi smiy mving f dvldnmis in lw-s ggis,nd sm mving in vs di-in (“sing”). Ms mvmndy is ing wn lw-sggis (Fig. A).

M in-d nlysis f sdy sls will lsd in ming

ws.

FIG. A Movement of manufacturingcapacity between regions, 2012-14*

Percent of manufacturing capacity impacted

9%

24%

23%

19%

Betweenhigh-cost countries

Betweenlow-cost countries

From high-costto low-cost countries

"Reshoring"(i.e., from low-cost

to high-cost countries)

Source: Supply Chain Optimization Study,

The Hackett Group, 2012

* projected

C o m p l i m

e n t a r y R e s e a

7/30/2019 Hackett 2012 Offshoring Forecast

http://slidepdf.com/reader/full/hackett-2012-offshoring-forecast 2/9

© 2012 Te Hackett Group, Inc.; All Rights Reserved. Page 2

CR_ES0041

of these jobs in the North American and European economies. To uncover new insights about productivity gains, outsourcing and offshoring of the delivery of business services, we analyzed our proprietary benchmarking and study data aboutthe processes, organization, technology, governance and other aspects of businessservices in large global companies in combination with IMF data on historical

and projected economic growth rates in North America and Europe

1

and financialreports filed by publicly traded companies.

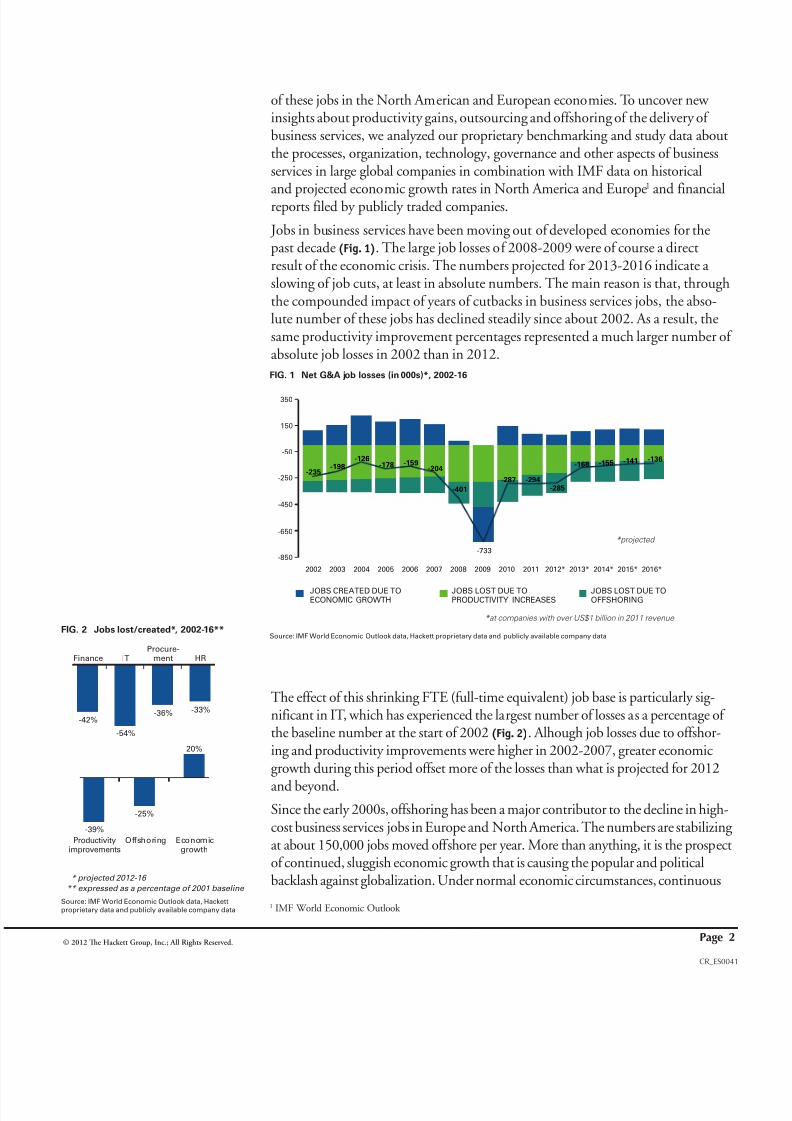

Jobs in business services have been moving out of developed economies for thepast decade (Fig. 1). The large job losses of 2008-2009 were of course a directresult of the economic crisis. The numbers projected for 2013-2016 indicate a slowing of job cuts, at least in absolute numbers. The main reason is that, throughthe compounded impact of years of cutbacks in business services jobs, the abso-lute number of these jobs has declined steadily since about 2002. As a result, thesame productivity improvement percentages represented a much larger number of absolute job losses in 2002 than in 2012.

The effect of this shrinking FTE (full-time equivalent) job base is particularly sig-nificant in IT, which has experienced the largest number of losses as a percentage of the baseline number at the start of 2002 (Fig. 2). Alhough job losses due to offshor-ing and productivity improvements were higher in 2002-2007, greater economicgrowth during this period offset more of the losses than what is projected for 2012

and beyond.Since the early 2000s, offshoring has been a major contributor to the decline in high-cost business services jobs in Europe and North America. The numbers are stabilizing at about 150,000 jobs moved offshore per year. More than anything, it is the prospectof continued, sluggish economic growth that is causing the popular and politicalbacklash against globalization. Under normal economic circumstances, continuous

1 IMF Wld Enmi Ol

FIG. 1 Net G&A job losses (in 000s)*, 2002-16

JOBS CREATED DUE TOECONOMIC GROWTH

JOBS LOST DUE TOPRODUCTIVITY INCREASES

JOBS LOST DUE TOOFFSHORING

-850

-650

-450

-250

-50

150

350

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012* 2013* 2014* 2015* 2016*

-235-198

-126-178 -159

-204

-401

-733

-287 -294-285

-168 -155 -141 -136

* projected

Source: IMF World Economic Outlook data, Hackett proprietary data and publicly available company data

* at companies with over US$1 billion in 2011 revenue

FIG. 2 Jobs lost/created*, 2002-16**

Finance ITProcure-

ment HR

Productivityimprovements

Offshoring Economicgrowth

-39%

-25%

20%

-42%

-54%

-36% -33%

* projected 2012-16

** expressed as a percentage of 2001 baseline

Source: IMF World Economic Outlook data, Hackett

proprietary data and publicly available company data

7/30/2019 Hackett 2012 Offshoring Forecast

http://slidepdf.com/reader/full/hackett-2012-offshoring-forecast 3/9

© 2012 Te Hackett Group, Inc.; All Rights Reserved. Page 3

CR_ES0041

productivity improvement combined with economic growth would be considered a healthy pattern.

Of course, the other side of the coin is the creation of a proportional number of jobs inthe primary offshore destination geographies, led by India. Considering the decline intotal business services jobs, the stable absolute number indicates only a small increase

in the percentage of jobs moving offshore each year. Hackett research indicates that by 2016 the total cumulative number of offshored jobs will reach 60%- 65% of the totalnumber of jobs with the potential to be offshored.

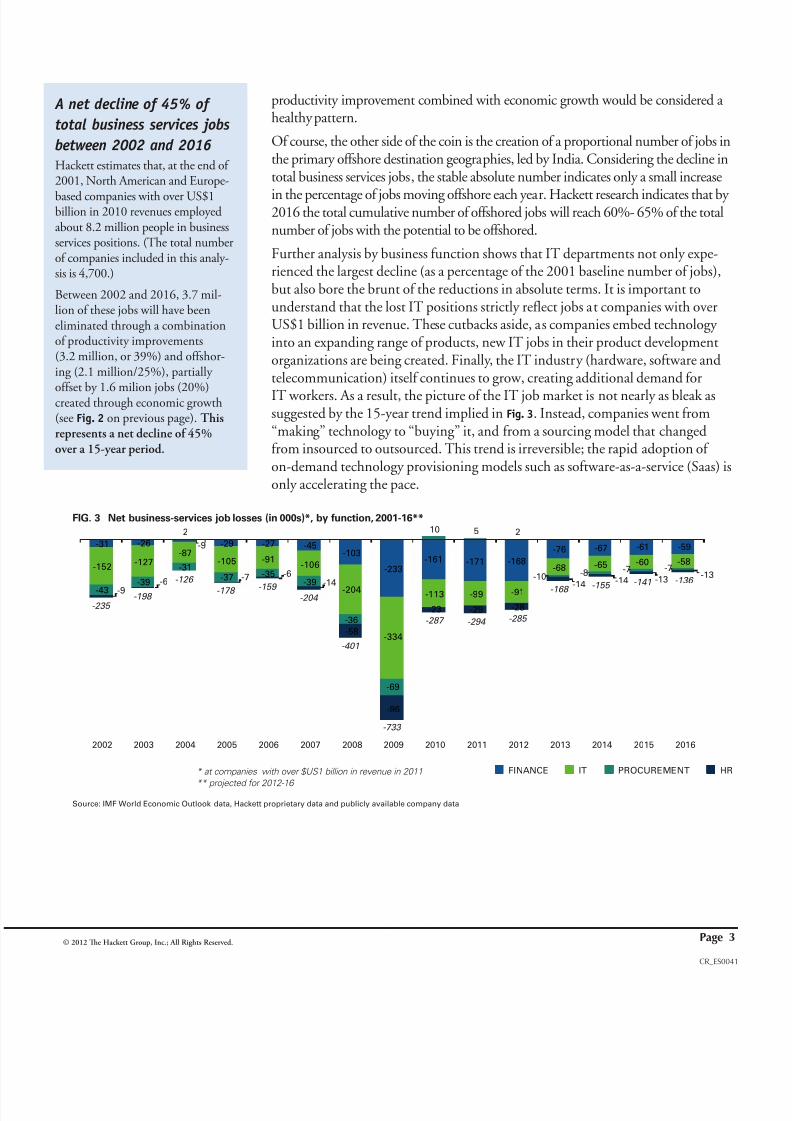

Further analysis by business function shows that IT departments not only expe-rienced the largest decline (as a percentage of the 2001 baseline number of jobs),but also bore the brunt of the reductions in absolute terms. It is important tounderstand that the lost IT positions strictly reflect jobs at companies with overUS$1 billion in revenue. These cutbacks aside, as companies embed technology into an expanding range of products, new IT jobs in their product developmentorganizations are being created. Finally, the IT industry (hardware, software andtelecommunication) itself continues to grow, creating additional demand for

IT workers. As a result, the picture of the IT job market is not nearly as bleak assuggested by the 15-year trend implied in Fig. 3. Instead, companies went from“making” technology to “buying” it, and from a sourcing model that changedfrom insourced to outsourced. This trend is irreversible; the rapid adoption of on-demand technology provisioning models such as software-as-a-service (Saas) isonly accelerating the pace.

A net decline of 45% of

total business services jobs

between 2002 and 2016

H sims , nd f 2001, N Amin nd E-

sd mnis wi v US$1illin in 2010 vns mlyd 8.2 millin l in sinsssvis siins. ( l nmf mnis inldd in is nly-sis is 4,700.)

Bwn 2002 nd 2016, 3.7 mil-lin f s js will v nlimind g mininf diviy imvmns(3.2 millin, 39%) nd ffs-ing (2.1 millin/25%), illy

ffs y 1.6 milin js (20%)d g nmi gw(s Fig. 2 n vis g). hisrepresents a net decline of 45%over a 15-year period.

FINANCE IT PROCUREMENT HR

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 20162002

-235

-233

-334

-733

-69

-96

-27 -45-103

10 5 2

-161 -171 -168-91-106

-204 -113 -99 -91-159 -204

-401

-287 -294 -285

-35-39

-36

-6-14

-58

-23 -29 -28

-76 -67 -61 -59

-68 -65 -60 -58

-168 -155 -141 -136

-10 -8 -7

-14 -14 -13-13

-43

-31

-152

-9

-26

2

-9

-127-87

-198

-126 -39

-31

-6

-29

-105

-178

-37 -7-7

FIG. 3 Net business-services job losses (in 000s)*, by function, 2001-16**

* at companies with over $US1 billion in revenue in 2011

** projected for 2012-16

Source: IMF World Economic Outlook data, Hackett proprietary data and publicly available company data

7/30/2019 Hackett 2012 Offshoring Forecast

http://slidepdf.com/reader/full/hackett-2012-offshoring-forecast 4/9

© 2012 Te Hackett Group, Inc.; All Rights Reserved. Page 4

CR_ES0041

unDErStanDing thE DrivErS of BuSinESS SErvicES DElivEry

r ationalization

The previous section presented the macro view of the decline in traditional North American and European back-office jobs resulting from productivity gains andoffshoring. Next, we turn our attention to the initiatives by individual compa-

nies that underlie this trend. The most powerful by far in the early 2000s was theconsolidation of routine, transactional business-support activities into sharedservices centers. More recently, companies have expanded the portfolio of servicesoffered by these organizations to include higher-value, knowledge-centric pro-cesses. Multifunction service centers have overtaken the previous model of single-function entities, allowing further leverage of skills. Hackett’s 2011 study of theseGlobal Business Services (GBS) organizations (as this next-generation approachto shared services is known) revealed that some companies now execute over 50%of their transactional business services work in a GBS organization. Notably,the percentage of knowledge-centric activities performed in the GBS is not farbehind(Fig. 4). The evolution and expansion of GBS organizations is the driving

force behind the productivity gains being anticipated.

GBS organizations, like the companies they serve, function best if they move work to wherever it can be done most efficiently and effectively. (This is the “global” in“Global” Business Services.) The result is that GBS organizations are themselvesalso expanding their global footprint, moving substantial numbers of jobs to low-cost geographies. Thus, the rise of GBS organizations accounts for much of therise in offshoring of business services jobs.

A 2011 Hackett study of globalization trends showed that companies are planning to accelerate the movement of work into low-cost geographies across the entirespectrum of services (Fig. 5).2 The study data offers a micro-level explanation of the macro trend outlined in the first part of this research. (For more in-depthanalysis of the evolution of GBS organizations, see the Related Hackett Researchsection.)

FIG. 4 Percentage of FTEs residing in Global Business Services (GBS) organization

30%

3%

58%

13%

47%

9%

46%

n/a

19%

45%

20%

45%

7%

44%

13%

Captive GBS Outsourced GBS Captive GBS Outsourced GBS

Knowledge-centric Transactional

n/a

FINANCE HR IT PROCUREMENT

Source: Global Business Services Performance Study, The Hackett Group, 2011

2 I is imn n sdy iins w mnis ldy v sn in lw-s gg-is. Tf, sl nms swn in Fig. 5 ig n s sning mn f glliz-in f sinss svis y ll mnis.

7/30/2019 Hackett 2012 Offshoring Forecast

http://slidepdf.com/reader/full/hackett-2012-offshoring-forecast 5/9

© 2012 Te Hackett Group, Inc.; All Rights Reserved. Page 5

CR_ES0041

A second driver behind the disappearance of business services jobs in developedeconomies is the broad-based globalization of all aspects of typical company operating models. As product/service lines, go-to-market strategies and supply chains become more global, the portfolio of business services required to supportthese global operations must become more global as well. The result is that it is

no longer natural or even appropriate for the center of business services delivery to remain in the traditional domestic market. If, for example, India evolves intothe optimal location for a global application-development competency center, theIndian IT organization progresses from an offshore arm providing capacity to theNorth American or European-headquartered organization into the global IT cen-ter itself. The same transition could take place for elements of the procurement,finance and HR services portfolio. This explains the ongoing movement of busi-ness services capacity away from developed economies.

FIG. 5 Percentage of FTEs located in a low-cost geography

CURRENT IN 2-3 YEARS

37%

26%

50%

36%

18%

13%

34%

18%

30%

17%

43%

24%

30%

13%

40%

22%

24%

15%

40%

23%

64%

43%

47%

26%Finance - Revenue cycle

Finance - Cash disbursements

Finance - General accounting andexternal reporting

Finance - Knowledge-centric

Procurement - PO processing,scheduling, receipt processing

Procurement: Knowledge-centric

HR - Payroll administration

HR - Total rewards administration

HR - Time and attendance,data management and reporting

HR - Knowledge-centric

IT - Operational

IT - Knowledge-centric

Source: Business Services Globalization Study, The Hackett Group, 2011

4 Tax management, compliance management, planning and performance

management, business analysis, function management

3

1 1 Infrastructure development, application development and

implementation, planning and strategy, function management

22 Staffing services, workforce development services, labor relations,

organizational effectiveness services, total rewards planning and function

management

4

3 Sourcing execution, supply data management, compliance management,

supplier management and development, sourcing strategy and analysis,

customer management

7/30/2019 Hackett 2012 Offshoring Forecast

http://slidepdf.com/reader/full/hackett-2012-offshoring-forecast 6/9

© 2012 Te Hackett Group, Inc.; All Rights Reserved. Page 6

CR_ES0041

Put slightly differently, the redesign of the value chain has forced companies torethink business services delivery. The expansion of GBS organizations is certainly one aspect of this evolution, but the impact is much broader. The need to supporta global operating model for the business translates into a need for global stan-dards for information, process and technology platforms. Not only is this neces-

sary to support the business, but essential if companies are to remain competitive.

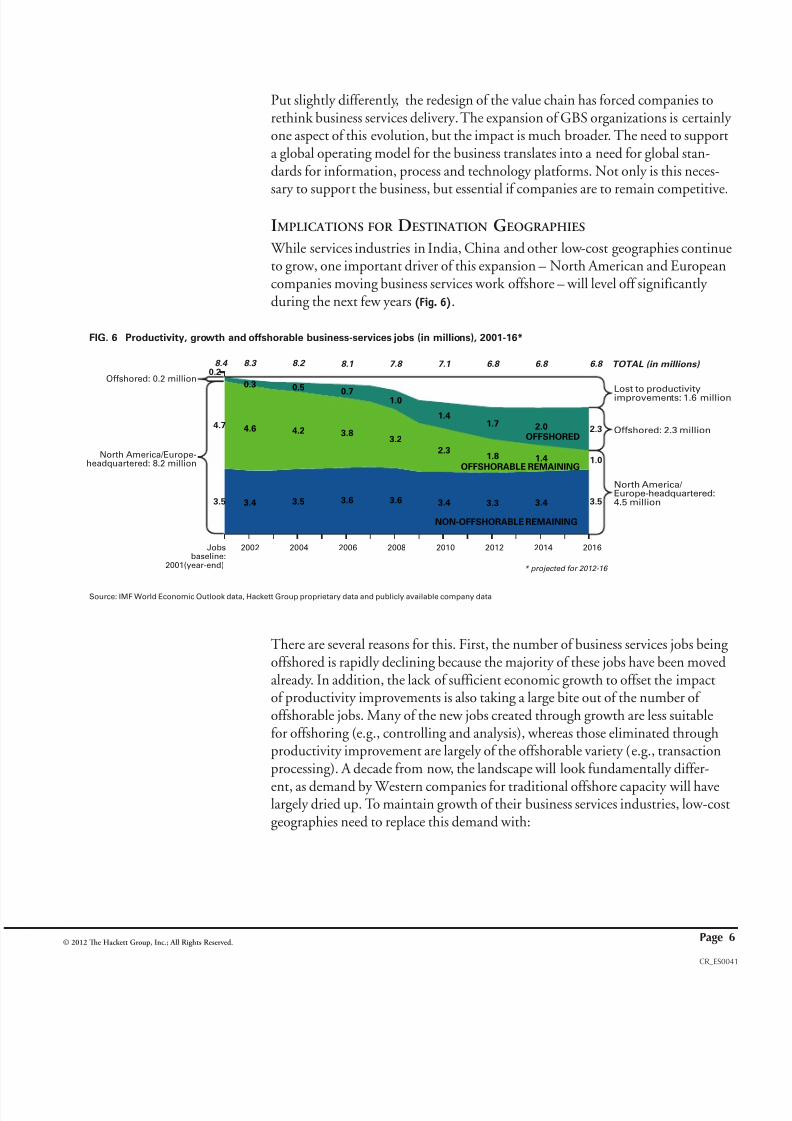

implicationS for DEStination gEographiES

While services industries in India, China and other low-cost geographies continueto grow, one important driver of this expansion – North American and Europeancompanies moving business services work offshore – will level off significantly during the next few years (Fig. 6).

There are several reasons for this. First, the number of business services jobs being offshored is rapidly declining because the majority of these jobs have been movedalready. In addition, the lack of sufficient economic growth to offset the impactof productivity improvements is also taking a large bite out of the number of offshorable jobs. Many of the new jobs created through growth are less suitablefor offshoring (e.g., controlling and analysis), whereas those eliminated throughproductivity improvement are largely of the offshorable variety (e.g., transactionprocessing). A decade from now, the landscape will look fundamentally differ-

ent, as demand by Western companies for traditional offshore capacity will havelargely dried up. To maintain growth of their business services industries, low-costgeographies need to replace this demand with:

FIG. 6 Productivity, growth and offshorable business-services jobs (in millions), 2001-16*

Jobsbaseline:

2001(year-end)

2002 2004 2006 2008 2010 2012 2014 2016

0.3 0.50.7 1.0

1.41.7 2.0 2.34.7 4.6 4.2 3.8

3.2

2.31.8 1.4 1.0

3.5 3.4 3.5 3.6 3.6 3.4 3.3 3.4 3.5

0.2Offshored: 0.2 million

Lost to productivityimprovements: 1.6 million

Offshored: 2.3 million

North America/ Europe-headquartered:4.5 million

North America/Europe-headquartered: 8.2 million

NON-OFFSHORABLE REMAINING

OFFSHORABLE REMAINING

OFFSHORED

Source: IMF World Economic Outlook data, Hackett Group proprietary data and publicly available company data

6.8 6.8 6.8 7.17.8 8.18.2 8.3 8.4 TOTAL (in millions)

* projected for 2012-16

7/30/2019 Hackett 2012 Offshoring Forecast

http://slidepdf.com/reader/full/hackett-2012-offshoring-forecast 7/9

© 2012 Te Hackett Group, Inc.; All Rights Reserved. Page 7

CR_ES0041

1. Domestic demand, including local industries and local operations of Western companies in low-cost countries.

2. Demand for new services beyond traditional finance, HR, procurementand IT “back-office” services.

3. Demand from technology providers (software, services and hardware),

in particular in the information technology industries.

In the more advanced low-cost destinations such as India, all three sources of demand are currently driving strong growth. In China, nurturing greater domes-tic demand will be of particular importance.

focuS: inDia

India remains the destination of choice for most companies that have estab-lished GBS organizations or plan to do so. Hackett’s 2011 Business ServicesGlobalization research identified India as the number-one location for GBS cen-ters: 74% of companies consider India to be a top potential destination for new

capacity, followed by China at 55%. Nevertheless, India’s overall share in totalbusiness services capacity in low-cost destinations is expected to decline slightly,from 39% in 2011 to 38% in 2013.

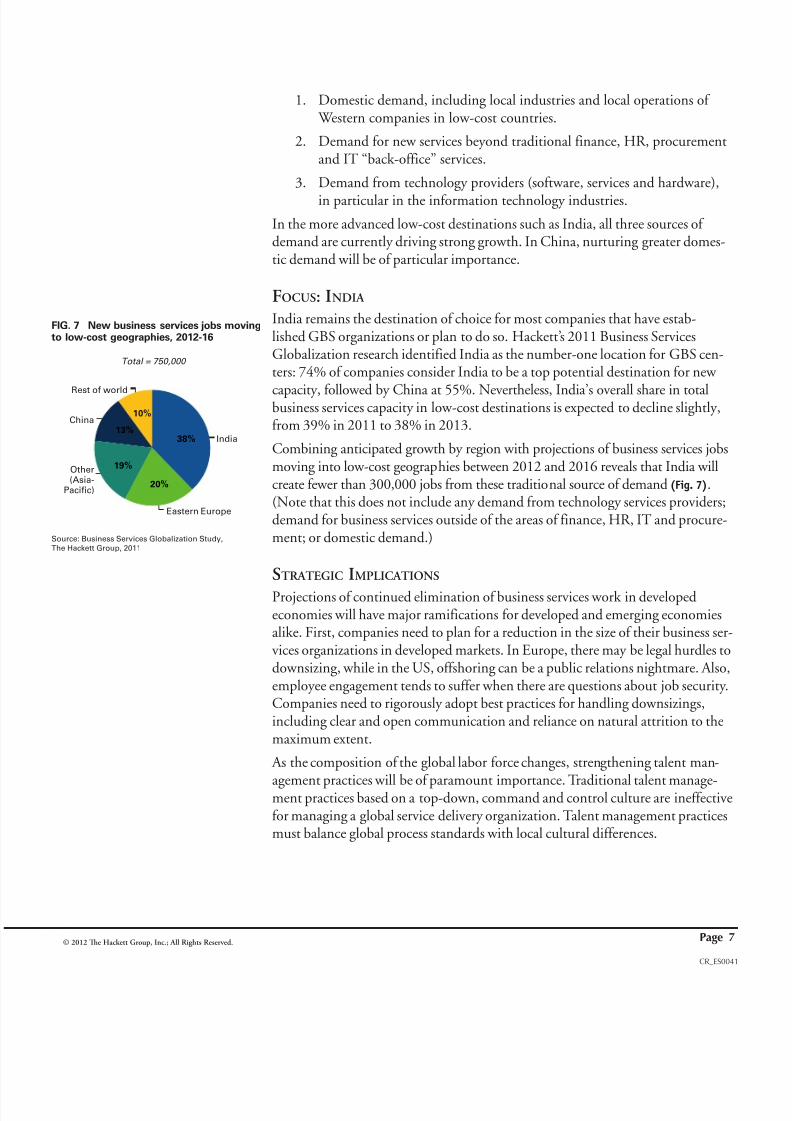

Combining anticipated growth by region with projections of business services jobsmoving into low-cost geographies between 2012 and 2016 reveals that India willcreate fewer than 300,000 jobs from these traditional source of demand (Fig. 7).(Note that this does not include any demand from technology services providers;demand for business services outside of the areas of finance, HR, IT and procure-ment; or domestic demand.)

StratEgic implicationS

Projections of continued elimination of business services work in developedeconomies will have major ramifications for developed and emerging economiesalike. First, companies need to plan for a reduction in the size of their business ser-vices organizations in developed markets. In Europe, there may be legal hurdles todownsizing, while in the US, offshoring can be a public relations nightmare. Also,employee engagement tends to suffer when there are questions about job security.Companies need to rigorously adopt best practices for handling downsizings,including clear and open communication and reliance on natural attrition to themaximum extent.

As the composition of the global labor force changes, strengthening talent man-

agement practices will be of paramount importance. Traditional talent manage-ment practices based on a top-down, command and control culture are ineffectivefor managing a global service delivery organization. Talent management practicesmust balance global process standards with local cultural differences.

Rest of world

FIG. 7 New business services jobs movingto low-cost geographies, 2012-16

Total = 750,000

India

Eastern Europe

Other(Asia-

Pacific)

China10%

20%

19%

13%38%

Source: Business Services Globalization Study,

The Hackett Group, 2011

7/30/2019 Hackett 2012 Offshoring Forecast

http://slidepdf.com/reader/full/hackett-2012-offshoring-forecast 8/9

© 2012 Te Hackett Group, Inc.; All Rights Reserved. Page 8

CR_ES0041

Operations in emerging markets also must make preparations. There is an urgentneed to elevate the capabilities of staff to be able to function in a globally con-nected organization. This transition may involve transfer of senior executives intothese geographies, developing local leadership talent, and facilitating the adoptionof company cultures and values. India, which has the longest history of providing

business services in a global context, will be most affected by this transition.

r ElatED h ackEtt r ESEarch

“Business Services Globalization, Part 1: Accelerating the Pace,” July 2011

“Business Services Globalization, Part 2: Managing the Risks and Realizing theValue,” July 2011

“Business Services Globalization, Part 3: Globalization Practices,” July 2011

“Delivery of Business Services: The Case for a Leveraged Model,” May 2011

“New Data: 2.8 Million Business-Support Jobs Eliminated Since 2000; OneMillion More to Disappear by 2014,” November 2010

7/30/2019 Hackett 2012 Offshoring Forecast

http://slidepdf.com/reader/full/hackett-2012-offshoring-forecast 9/9

© 2012 Te Hackett Group, Inc.; All Rights Reserved. Page 9

CR_ES0041

a Bout thE a DviSorS

Michel JanssenPrincipal and Chie Research Ofcer

Mr. Janssen is responsible for developing The Hackett Group’s core

intellectual property, including thought leadership. He works withthe company’s Executive Advisory Council to understand the strategicimpact of new and emerging trends on the business functions. He also

heads Hackett’s team of researchers and analysts in the US, Europe and India inthe design and implementation of research studies; analysis of results; and pro-duction of resulting findings. Previously Mr. Janssen was president of SupplierSolutions for Everest Group and co-founded the Everest Research Institute. Inaddition, he provided strategic oversight for Everest’s Outsourcing Center, the world’s largest outsourcing community and vehicle for identifying early industry trends. He was also a senior director in Gartner Group’s Strategic Sourcing prac-tice and held numerous management positions with EDS.

Erik Dorr

Senior Research Director, Finance and EPM Executive Advisory Programs

Mr. Dorr started his professional career of over 20 years as an IT con-sultant, and then moved on to a CIO position at a large manufacturing company. Next, he worked as a research analyst covering enterprisebusiness applications and technology strategy. Leveraging the extensive

experience he gained working with financial organizations and optimizing finan-cial processes, he was named to his present role in early 2010.

Martijn Geerling

Europe Practice Leader, Global Business Services

Mr. Geerling has over 10 years of consulting experience in busi-ness process redesign, shared services development, outsourcing andbenchmarking. During this time he has worked with global companiesdelivering transformation engagements in finance and other business

functions. Prior to joining The Hackett Group, he worked at KPMG Consulting assisting clients in finance function optimization and compliance management.

About heHackett GroupThe Hackett Group, a global strategicbusiness advisory, operations consultingand nance strategy rm, is a leadern business best practices, businessbenchmarking, and transormationconsulting services including strategy andoperations, working capital management,and globalization advice.

Utilizing business best practices andmplementation insights rom morethan 5,000 business benchmarkingengagements, executives use The HackettGroup’s empirically-based approach toquickly dene and implement initiativesto enable world-class perormance.

Through its REL group, The HackettGroup oers working capital managementsolutions ocused on delivering signicantcash fow improvements. Throughts Archstone Consulting group, The

Hackett Group oers Strategy consulting& Operations consulting services inthe Consumer and Industrial Products,Pharmaceutical, Manuacturing andFinancial Services industry sectors.Through its Hackett TechnologySolutions group, The Hackett Groupoers business application consultingservices, including SAP implementationand Oracle implementation, that helpmaximize returns on IT investments.The Hackett Group has completed over5,000 best practices benchmarkingstudies with 2,800 major corporationsand government agencies, including 97%

o the Dow Jones Industrials, 84% o theFortune 100, 80% o the DAX 30 and49% o the FTSE 100.

Founded in 1991, The Hackett Group wasacquired by Answerthink, Inc. in 1997.Answerthink was renamed The HackettGroup, Inc. in 2008. The Hackett Grouphas global oces in the United States,Europe and Asia/Pacic and is publiclytraded on the NASDAQ as HCKT.

Email: [email protected]

Amsterdam: +31 36 535 00 82

Atlanta: +1 770 225 3600Frankurt am Main: +49 69 900 217 0

London: +44 20 7398 9100

Paris: +33 1 53 43 0400

Sydney: +61 2 9299 8830

Zurich: +41 43 813 3010

www.thehackettgroup.com