guide for auditors - chartered professional accountant/media/site/business-and-accounting... ·...

TRANSCRIPT

Guide for Auditors

First-time reporting on financial statements adopting

Canadian Accounting Standards for Not-for-Profit Organizations (CICA Handbook Accounting – Part III)

or

Public Sector Accounting Standards for Government Not-for-Profit Organizations (CICA Public Sector Accounting Handbook)

Aboutthispublication

The Guidance and Support group of the Canadian Institute of Chartered Accountants (CICA) under-takes initiatives to support practitioners and their clients in the implementation of standards. As part of these initiatives, this non-authoritative guide provides guidance for first-time reporting on financial statements adopting CICA Handbook – Accounting – Part III — Accounting standards for not-for-profit organizations or Standards for government not-for-profit organizations in the CICA Public Sector Accounting Handbook. This guide has not been adopted, endorsed, approved or otherwise acted on by the Auditing and Assurance Standards Board, Accounting Standards Board, Public Sector Accounting Board, any CICA board or committee, the governing body or membership of the CICA or any provin-cial institute/Ordre.

Auditors are expected to use professional judgment in determining whether the material in this publica-tion is both appropriate and relevant to the circumstances of their particular audit engagements. This publication is based on the CASs as updated in May 2011.

The CICA expresses its appreciation to the author and to CICA staff for preparing this publication.

Gordon Beal, CA Director, Guidance and Support group The Canadian Institute of Chartered Accountants

TableofContents

1. Introduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

2. Implicationsofadoptinganewfinancialreportingframework(ASNFPOorPSAS-GNFPO) . . . . . 4

2.1 ImplicationsofadoptingASNFPOorPSAS-GNFPOformanagement. . . . . . . . . . . . . . . . . . . . . 4

2.2 ImplicationsofadoptingASNFPOorPSAS-GNFPOfortheauditor. . . . . . . . . . . . . . . . . . . . . . . 8

3. Twoauditapproachesforfirst-timereportingonfinancialstatementsadoptingASNFPOorPSAS-GNFPO. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

4. Auditapproach1—Reportonallperiodspresented. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

4.1 Auditapproach1—Auditor’sopinion. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

4.2 Auditapproach1—Auditprocedures. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

5. Auditapproach2—Reportingonthecurrentperiodonly . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

5.1 Auditapproach2—Auditor’sopinion. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

5.2 Auditapproach2—Auditprocedures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

6. Appendices. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

AppendixA:Selectedtransitionadjustmentsandsampleauditprocedures. . . . . . . . . . . . . . . . . . 24

AppendixB:Selectedcomparisonofworkeffortinvolvedinauditapproaches1and2. . . . . . . . . 27

AppendixC:Auditapproach1—Reportingonallperiodspresented—Assumptions. . . . . . . . . . . . 28

AppendixC.1: Auditapproach1—Reportingonallperiodspresented—Excerptsfromanengagementletter. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

AppendixC.2: Auditapproach1—Reportingonallperiodspresented—Excerptsfromarepresentationletter. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

AppendixC.3: Auditapproach1—Reportingonallperiodspresented—Unmodifiedindependentauditor’sreport . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

AppendixC.4: Auditapproach1—Reportingonallperiodspresented—Qualifiedindependentauditor’sreport—Scopelimitation. . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

AppendixD:Auditapproach2—Reportingoncurrentperiodonly—Assumptions. . . . . . . . . . . . . 37

AppendixD.1: Auditapproach2—Reportingoncurrentperiodonly—Excerptsfromanengagementletter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

AppendixD.2: Auditapproach2—Reportingoncurrentperiodonly—Excerptsfromarepresentationletter. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .40

AppendixD.3: Auditapproach2—Reportingoncurrentperiodonly—Unmodifiedindependentauditor’sreport . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

AppendixD.4: Auditapproach2—Reportingoncurrentperiodonly—Qualifiedindependentauditor’sreport—Scopelimitation . . . . . . . . . . . . . . . . . . . . . . . . . . . .44

AppendixE:Otherresourcesavailable.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

1

1. Introduction

This guide provides guidance to auditors engaged to report on the first set of financial statements prepared in accordance with either:• Canadian accounting standards for not-for-profit organizations (CICA Handbook – Account-

ing – Part III — Accounting standards for not-for-profit organizations); or

• Canadian public sector accounting standards (standards for government not-for-profit organiza-tions set out in the CICA Public Sector Accounting (PSA) Handbook). [In other words, the guidance is for government not-for-profit organizations that adhere to CICA PSA Handbook Sections PS 4200 to PS 4270. It is NOT for organizations that adhere to the CICA PSA Handbook without Sections PS 4200 to PS 4270.]

The following table provides definitions of not-for-profit organizations and government not-for-profit organizations, the applicable financial reporting framework and the required adoption date.

Exhibit 1.0.1: Applicableaccountingstandards

Type of organization Definition

Applicable Accounting Standards

Required adoption date

Not-for-profit organization

An entity that is:a) normally without transferable

ownership interests;b) organized and operated exclu-

sively for social, educational, professional, religious, health, charitable or any other not-for-profit purpose.

A not-for-profit organization’s members, contributors and other resource providers do not, in such capacity, receive any financial return directly from the organization.

Part III — Accounting Standards for Not-for-Profit Organizations

or

Part I — International Financial Reporting Standards

in the CICA Hand-book – Accounting

Mandatory for fiscal periods beginning on or after January 1, 2012.

Earlier applica-tion is permitted.

21. Introduction

Type of organization Definition

Applicable Accounting Standards

Required adoption date

Government not-for-profit organization

An organization controlled by the government that has all of the following characteristics:a) It has counterparts outside the

public sector. b) It is an entity normally without

transferable ownership interests.c) It is an entity organized and

operated exclusively for social, educational, professional, reli-gious, health, charitable or any other not-for-profit purpose.

d) Its members, contributors and other resource providers do not, in such capacity, receive any financial return directly from the organization.

“Public sector” refers to federal, provincial, territorial and local governments, government organiza-tions, government partnerships and school boards.

Section PS 1300, Government Reporting Entity, in CICA PSA Handbook provides guidance on the interpretation and application of control.

Standards for not-for-profit organizations in the CICA Public Sector Accounting Handbook

or

Standards in the CICA Public Sector Accounting Handbook without Sec-tions PS 4200 to PS 4270

Mandatory for fiscal periods beginning on or after January 1, 2012.

Note: For additional information on accounting standards for not-for-profit organizations in Canada, refer to the CICA website at www.cica.ca/applying-the-standards/not-for-profit-organizations.

The following table provides a summary of requirements for first-time adoption of Canadian accounting standards for not-for-profit organizations (ASNFPO) [CICA Handbook – Accounting – Part III — Accounting standards for not-for-profit organizations] and Canadian public sector account-ing standards [Standards for government not-for-profit organizations in the CICA Public Sector Account-ing Handbook (PSAS-GNFPO).]

31. Introduction

Exhibit 1.0.2: Summaryofrequirementsforfirst-timeadoptionofASNFPOandPSAS-GNFPO

Role of Preparer of FS Evidence Requiredby Auditor

Auditor’s Role

Identify other adjustmentsrequired to restate the SFPat date of transition

Restate the SFP at dateof transition and preparecomparative FS withrequired note disclosures

Prepare current period FS,note disclosures andcomparatives in accordancewith the AFRF

Identify the exemptions to restatement as permitted under ASNFPO 1501 or PSAS PS 2125

Details and calculationsof transition adjustments

and note disclosures

SFP at date of transitionand comparative FS

in accordance with the AFRF

Current period FS preparedin accordance with AFRF

with comparative information

Details of exemptions used,resulting adjustments and

note disclosures

Read and understand the requirements of the AFRF

Examine details of adjust-ments to ensure they comply with requirements of the AFRF

Ensure SFP and comparative FS have been properly prepared in accordance with the AFRF

Audit current year plus:audit comparative FS; orexplain corresponding figures are unaudited in auditor’s report

Ensure exemptions used andresulting adjustments and FSdisclosures comply with AFRF

Read and understand the AFRF and relevant CAS requirements

AFRF = Applicable Financial Reporting Framework

FS = Financial Statements

SFP = Statement of Financial Position

Notes:• Although this guidance is intended for auditors, the basic principles involved are similar to those in review

engagements. The key differences are the work effort involved (examination of evidence vs. discussion and analysis) and the wording of the report issued as a result (audit vs. review engagement report).

• For additional information on reporting, refer to the CICA guide Reporting Implications of New Auditing and Accounting Standards (Issue No. 8, May 2012).

4

2. Implicationsofadoptinganewfinancialreportingframework(ASNFPOorPSAS-GNFPO)

2.1 ImplicationsofadoptingASNFPOorPSAS-GNFPOformanagementSome of the major areas that management needs to address in the transition from CICA Hand-book – Accounting – Part V — Pre-changeover accounting standards to the following financial reporting frameworks are outlined below in Exhibit 2.1.1:• Canadian accounting standards for not-for-profit organizations [CICA Handbook – Accounting

– Part III — Accounting standards for not-for-profit organizations]; and • Canadian public sector accounting standards [Standards for government not-for-profit organizations

in the CICA Public Sector Accounting Handbook].

Management is responsible for the preparation of the financial statements in accordance with the new applicable financial reporting framework.

Exhibit 2.1.1: MajorareasthatneedtobeaddressedbymanagementinthetransitiontoASNFPOandPSAS-GNFPO

Major areas ASNFPO PSAS-GNFPO

Retrospective application

Management is required to retroactively apply the accounting policies in effect at the end of the current period back to the date of transition. This will result in a restatement of the financial statements for the comparative period.

Section 1501 prohibits retrospective application of some aspects of other standards in Part II of the Handbook relat-ing to derecognition of financial assets and financial liabilities, hedge accounting, estimates and non-controlling interests.

Retrospective application of the account-ing policies under Section 1501 will require restating:• the opening statement of financial

position as at the date of transition [e.g., January 1, 2011];

Management is required to retroactively apply the accounting policies, in effect at the end of the current period, back to the date of transition. This will result in a restatement of the financial statements for the comparative period.

Section PS 2125 prohibits retroactive application to accounting estimates.

Retroactive application of the account-ing policies under Section PS 2125 will require restating:• the opening statement of financial

position as at date of transition [e.g., April 1, 2011];

• the comparative statement of opera-tions and statement of cash flows for the period ended [e.g., March 31, 2012];

52. Implications of adopting a new financial reporting framework

Major areas ASNFPO PSAS-GNFPO

Retrospective application (continued)

• the comparative statement of opera-tions and statement of cash flows for the period ended [e.g., December 31, 2011];

• the statement of changes in net assets and statement of financial position as at [e.g., December 31, 2011]; and

• [e.g., 2011] comparatives included in the notes to the financial statements.

• the statement of changes in net assets1 and statement of financial position as at [e.g., March 31, 2012]; and

• [e.g., 2012] comparatives included in the notes to the financial statements.

Date of transition The date of transition is the beginning of the earliest period for which an organiza-tion presents full comparative information (e.g., January 1, 2011 for financial state-ments for a period ending December 31, 2012).

The date of transition to Public Sector Accounting Standards is the beginning of the earliest period for which a government organization presents full comparative information in accordance with Public Sector Accounting Standards.

Exemptions Management is allowed to use certain specified exemptions to make retrospec-tive application easier. The exemptions available are: • business combinations; • fair value;• employee future benefits;• cumulative translation differences; • financial instruments; and• asset retirement obligations.

Management is allowed to use certain specified exemptions to make retroactive application easier. The exemptions avail-able are: • retirement and post-employment

benefits;• business combinations;• investments in government business

enterprises;• government business partnerships; and• tangible capital asset impairment.

Other transition adjustments

Some common adjustments resulting from differences between pre-changeover accounting standards and not-for-profit accounting standards include financial instruments and employee future benefits.

Transitioning to PSA standards from Part V may be a significant undertaking for an organization because there are dif-ferences between them; for example: • financial instruments;• retirement and post employment

benefits;• business combinations;• loan guarantees;• impairment of tangible capital asset;• revenue and deferred revenue.

1 Section PS 2601, Foreign Currency Translation, and Section PS 3450, Financial Instruments, may require an organization to present a statement of remeasure-ment gains and losses.

62. Implications of adopting a new financial reporting framework

Major areas ASNFPO PSAS-GNFPO

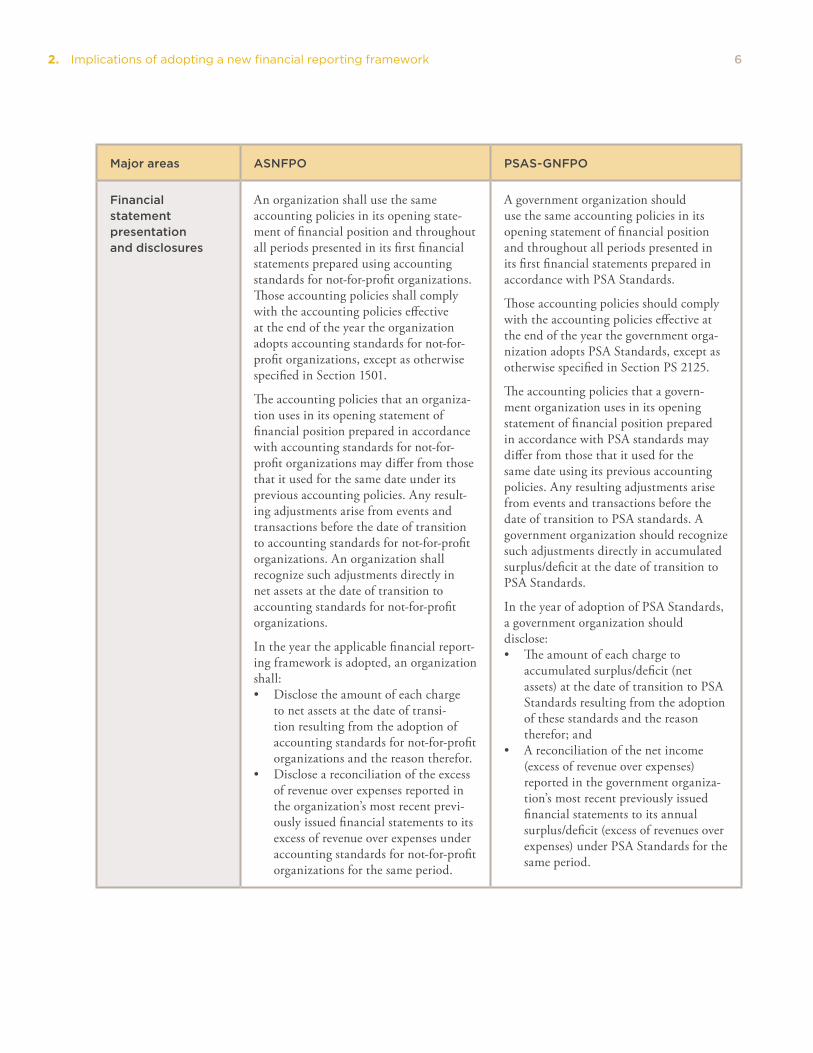

Financial statement presentation and disclosures

An organization shall use the same accounting policies in its opening state-ment of financial position and throughout all periods presented in its first financial statements prepared using accounting standards for not-for-profit organizations. Those accounting policies shall comply with the accounting policies effective at the end of the year the organization adopts accounting standards for not-for-profit organizations, except as otherwise specified in Section 1501.

The accounting policies that an organiza-tion uses in its opening statement of financial position prepared in accordance with accounting standards for not-for-profit organizations may differ from those that it used for the same date under its previous accounting policies. Any result-ing adjustments arise from events and transactions before the date of transition to accounting standards for not-for-profit organizations. An organization shall recognize such adjustments directly in net assets at the date of transition to accounting standards for not-for-profit organizations.

In the year the applicable financial report-ing framework is adopted, an organization shall:• Disclose the amount of each charge

to net assets at the date of transi-tion resulting from the adoption of accounting standards for not-for-profit organizations and the reason therefor.

• Disclose a reconciliation of the excess of revenue over expenses reported in the organization’s most recent previ-ously issued financial statements to its excess of revenue over expenses under accounting standards for not-for-profit organizations for the same period.

A government organization should use the same accounting policies in its opening statement of financial position and throughout all periods presented in its first financial statements prepared in accordance with PSA Standards.

Those accounting policies should comply with the accounting policies effective at the end of the year the government orga-nization adopts PSA Standards, except as otherwise specified in Section PS 2125.

The accounting policies that a govern-ment organization uses in its opening statement of financial position prepared in accordance with PSA standards may differ from those that it used for the same date using its previous accounting policies. Any resulting adjustments arise from events and transactions before the date of transition to PSA standards. A government organization should recognize such adjustments directly in accumulated surplus/deficit at the date of transition to PSA Standards.

In the year of adoption of PSA Standards, a government organization should disclose:• The amount of each charge to

accumulated surplus/deficit (net assets) at the date of transition to PSA Standards resulting from the adoption of these standards and the reason therefor; and

• A reconciliation of the net income (excess of revenue over expenses) reported in the government organiza-tion’s most recent previously issued financial statements to its annual surplus/deficit (excess of revenues over expenses) under PSA Standards for the same period.

72. Implications of adopting a new financial reporting framework

Major areas ASNFPO PSAS-GNFPO

Financial statement presentation and disclosures (continued)

• For the above disclosures, the level of detail shall be sufficient to enable users to understand the material adjustments made to the statement of financial position and statement of operations. If a statement of cash flows was presented under the previous accounting policies, the organization shall explain the material adjustments to the statement of cash flows as well.

• Disclose any exemptions used, when the organization elects to use one or more of the exemptions in paragraph 1501.10.

• The disclosures required above should give sufficient detail to enable users to understand the material adjustments made to the statement of financial position and statement of operations. If a government organization pre-sented a cash flow statement under its previous accounting policies, it should explain the material adjustments to the statement of cash flow.

• When a government organization elects to use one or more of the exemp- tions in paragraphs PS 2125.09.14, it should disclose the exemptions used.

Need for comparative information

Financial statements shall be prepared on a comparative basis, unless the compara-tive information is not meaningful or the standards set out in Part III of the Handbook permit otherwise.

Paragraph PS 1201.018 states that financial statements should present a com-parison of current period amounts with those of the prior period(s). To facilitate meaningful comparisons, prior period information needs to be reported on a basis and for a scope consistent with that used to report current period information.

Presentation of opening statement of financial position

An organization prepares and presents its opening statement of financial position at the date of transition.2

An organization prepares and presents its opening statement of financial position at the date of transition. The date of transi-tion is the beginning of the earliest period for which a government organization presents full comparative information in accordance with Public Sector Accounting Standards. A government organization should use the same accounting policies in its opening statement of financial posi-tion as those used throughout all periods presented in its first financial statements prepared in accordance with PSA Stan-dards.

2 For further guidance, refer to the CICA website at www.cica.ca/applying-the-standards/accounting-standards-for-private-enterprises/faqs/item63083.aspx (go to Can the opening balance sheet be presented in the notes?)

82. Implications of adopting a new financial reporting framework

2.2 ImplicationsofadoptingASNFPOorPSAS-GNFPOfortheauditorThe first-time adoption of ASNFPO or PSAS-GNFPO raises important matters that the auditor needs to address in the transition period.

As the applicable financial reporting framework has changed (to ASNFPO or PSAS-GNFPO), the auditor will need to get a new engagement letter from not-for-profit clients in both the private and public sectors.

Additional audit work will be needed to examine the elections, adjustments and note disclosures management has had to make to restate the financial statements in accordance with the new applicable financial reporting framework.

In the period of transition to the new applicable financial reporting framework, management is required to:• prepare and present an opening statement of financial position on the date of transition in accor-

dance with the new applicable financial reporting framework; and• use the same accounting policies throughout all periods presented.

This will likely result in presenting comparative information and note disclosures originally not included in the pre-changeover financial statements.

As a result, an auditor might perform different audit procedures for an engagement to report on the prior period financial statements prepared in accordance with the new applicable financial reporting framework than for one prepared under the pre-changeover accounting standards. An example would be where the accounting policies chosen under the new financial reporting framework differ signifi-cantly from those chosen under the pre-changeover accounting standards.

The CASs also require the auditor to obtain sufficient appropriate audit evidence on whether there is a material misstatement of the comparative information. The nature and extent of the audit procedures performed is a matter of professional judgment. It may take into account the audit work performed on the prior period financial statements, prepared in accordance with pre-changeover accounting standards.

For this reason, the auditor cannot assume that the audit evidence obtained when auditing the prior period financial statements (prepared in accordance with pre-changeover accounting standards) will be sufficient to report on the first financial statements prepared in accordance with the new financial reporting framework.

Consequently, the auditor may not refer to the comparative information (presented in accordance with the new financial reporting framework) as being audited without first determining what additional audit procedures may be required and then performing them.

92. Implications of adopting a new financial reporting framework

There are two different broad approaches to the auditor’s reporting responsibilities for such compara-tive information: corresponding figures and comparative financial statements. The two approaches for reporting on the first financial statements prepared in accordance with the new applicable financial reporting framework are outlined in Section 3 of this guide.

Sections 4 and 5 provide more detail on some of the specific audit procedures that may be required under Audit Approaches 1 and 2.

10

3. Twoauditapproachesforfirst-timereportingonfinancialstatementsadoptingASNFPOorPSAS-GNFPO

CAS 710, Comparative Information — Corresponding Figures and Comparative Financial Statements, addresses two types of comparative information (i.e., corresponding figures and comparative finan-cial statements) that may be presented in the financial statements. As a result, there are two possible approaches for reporting on comparative information. In other words, there are two audit approaches for reporting on the first-time financial statements adopting ASNFPO or PSAS-GNFPO: report on all periods presented or report on the current period only.

The auditor would discuss with the organization what approach to adopt for the first financial state-ments and how the auditor is being engaged to report. The approach to adopt can be specified by law or regulation; if not, it is to be specified in the terms of engagement.

The audit reporting differences between the two approaches are summarized in the table below.

Exhibit 3.0.1: Auditreportingdifferencesbetweenthetwoauditapproaches

Audit approach #

Audit reporting by type of comparative information

Description of comparative information

Scope of required audit opinion

1 Comparative financial statements

Comparative information where amounts and other dis-closures for the prior period are included for comparison with the financial statements of the current period but, if audited, are referred to in the auditor’s opinion.

The level of information included in those compara-tive financial statements is comparable with that of the financial statements of the current period.

Auditor’s opinion refers to each period for which finan-cial statements are presented.

113. Two audit approaches for first-time reporting on financial statements

adopting ASNFPO or PSAS-GNFPO

Audit approach #

Audit reporting by type of comparative information

Description of comparative information

Scope of required audit opinion

2 Corresponding figures Comparative information where amounts and other disclosures for the prior period are included as an integral part of the current period financial statements, and are intended to be read only in relation to current period amounts and other disclosures (referred to as “current period figures”).

The level of detail presented in the corresponding amounts and disclosures is dictated primarily by its relevance to the current period figures.

Auditor’s opinion refers to the current period only.

12

4. Auditapproach1—Reportonallperiodspresented

Under this approach, the audit opinion will refer to each period for which financial statements are presented.

While the auditor may have audited the financial statements for the prior years prepared in accordance with the pre-changeover accounting standards, the auditor will not have previously audited the finan-cial statements for periods prepared in accordance with the new applicable financial reporting framework.

When reporting on the first financial statements prepared in accordance with the new financial report-ing framework, the auditor will be reporting on the prior years’ financial statements and the opening statement of financial position prepared in accordance with the new financial reporting framework for the first time. Accordingly, the auditor will be required to obtain sufficient appropriate audit evidence to support the auditor’s opinion on those financial statements.

The auditor is able to use the work performed in auditing the financial statements for the prior years prepared in accordance with pre-changeover accounting standards. Because the comparative financial statements are prepared in accordance with the new applicable financial reporting framework, however, the auditor will have to perform additional audit procedures to support the auditor’s opinion on those financial statements, even when the financial statements prepared in accordance with the new financial reporting framework do not appear to be significantly different from those prepared under pre-change-over accounting standards.

4.1 Auditapproach1—Auditor’sopinionWhen comparative financial statements are presented, the auditor’s opinion should refer to each period for which financial statements are presented and on which an audit opinion is expressed. Some matters to address in the auditor’s opinion paragraph are summarized below:

Exhibit 4.1.1: Auditapproach1—Auditor’sopinion

Matters to address Comments

Scope limitation Consider whether a scope limitation is needed in the auditor’s report. This is often the case when it is not possible to determine the completeness of revenues from fund raising activities.3

Refer to Appendix C.4 for an example of a “Basis for Qualified Opinion” paragraph and for a qualified auditor’s opinion paragraph.

3 For further guidance refer to “Reports Arising from Circumstances Addressed in CAS 710, Comparative Information — Corresponding Figures and Compara-tive Financial Statements,” in Reporting Implications of New Auditing and Accounting Standards (Issue 8, May 2012).

134. Audit approach 1 — Report on all periods presented

Matters to address Comments

Not-for-profit organizations: description of financial statements and the applicable financial reporting framework

Paragraph 3 of Section 1401, General Standards of Financial Statement Presentation for not-for-profit organizations, in Part III of the CICA Handbook – Accounting, states that financial statements shall present fairly, in accordance with generally accepted accounting principles, the financial position, results of operations and cash flows of an organization.

Therefore, the auditor’s opinion will be worded accordingly (i.e., it will refer to the financial position of [the not-for-profit organization], the results of its operations and its cash flows).

The applicable financial reporting framework will be described as “Canadian accounting standards for not-for-profit organizations.”

Refer to Appendix C.3 for an example of an auditor’s opinion paragraph.

Government not-for-profit organizations: description of financial statements and the applicable financial reporting framework

Section PS 4200, Financial Statement Presentation by Not-for Profit Organizations, sets out the presentation and disclosure standards for financial statements for not-for-profit orga-nizations adhering to the standards for not-for-profit organizations in the CICA Public Sector Accounting Handbook. Paragraph PS 4200.05 states that the financial statements for a government not-for-profit organization are to provide the information necessary to meet the requirements of that Section and other Sections in a manner that results in the fair presentation, in accordance with generally accepted accounting principles, of the organi-zation’s financial position, results of operations and cash flows.

It is important to note that, for government not-for-profit organizations, Section PS 2601, Foreign Currency Translation, and Section PS 3450, Financial Instruments, apply to fiscal years beginning on or after April 1, 2012. These Sections detail when a statement of remeasurement gains and losses has to be presented.

Sections PS 3450 and PS 2601 detail transitional provisions. When a government not-for-profit organization applies these Sections in the same period it adopts Public Sector Accounting Standards for the first time, these Sections cannot be applied retroactively. Comparative amounts are presented in accordance with the accounting policies applied by the government not-for-profit organization immediately preceding its adoption of Public Sector Accounting Standards.

If a government not-for-profit organization is required to present a statement of remea-surement gains and losses for fiscal years beginning on or after April 1, 2012, the auditor’s opinion will be worded accordingly (i.e., it will refer to the financial position of [the government not-for-profit organization], the results of its operations, its remeasurement gains and losses and its cash flows.)

Another important point is that the applicable financial reporting framework will be described as “Canadian public sector accounting standards.”

Refer to Appendix C.3 for an example of an auditor’s opinion paragraph.

144. Audit approach 1 — Report on all periods presented

4.2 Auditapproach1—AuditproceduresThe auditor shall determine whether the financial statements include the comparative information required by the applicable financial reporting framework and whether such information is appropriately classified. For this purpose, the auditor shall evaluate whether:• the comparative information agrees with the amounts and other disclosures presented in the prior

period or, when appropriate, have been restated; and• the accounting policies reflected in the comparative information are consistent with those applied in

the current period or, if there have been changes in accounting policies, whether those changes have been properly accounted for and adequately presented and disclosed.

The following table provides more detail on some of the specific audit procedures that may be required under Audit Approach 1. Reference should also be made to CAS 710 and Appendix A to this guide.

Exhibit 4.2.1: Auditapproach1—Auditprocedures

Matters to address Comments

Terms of engagement

As the applicable financial reporting framework has changed (to ASNFPO or PSAS-GNFPO), the auditor will need to get a new engagement letter to ensure that manage-ment understands:• its responsibility to prepare financial statements in accordance with the new applicable

financial reporting framework;• that the audit opinion (which covers all periods presented) will refer to the fair pre-

sentation of the financial statements in accordance with the new applicable financial reporting framework; and

• that the comparative financial statements will be audited. This will likely require some additional audit work and, therefore, some additional cost.

Excerpts from a sample engagement letter are presented in Appendix C.1.

Discussion with management

The auditor will need to discuss with management:• the implications of the change to the new applicable financial reporting framework,

including the transitional adjustments management will have to make and the optional exemptions to retrospective application and financial statement disclosures;

• the impact of the transition on the planned scope/timing of the audit; and• information about the transition adjustments that will be required.

Risk assessment The auditor will need to identify and assess any new or increased risks of material misstatement (error and fraud) in the financial statements (as a result of the change in accounting standards) for all of the periods covered by the auditor’s report.

154. Audit approach 1 — Report on all periods presented

Matters to address Comments

New accounting policies and transition adjustments

The auditor will need to ensure that management has properly identified, calculated (including allocation to the correct period) and determined the nature, extent and impli-cations of changes to be made in the financial statements as a result of:• revised accounting policies and their consistent application;• first-time adjustments required by the new applicable financial reporting framework;• other transition adjustments; and• revised presentation and disclosures in the financial statements.

Opening balances The auditor will need to:• evaluate whether the comparative information agrees with the amounts and other

disclosures presented in the prior period under the pre-changeover standards or that such information/disclosures have, where appropriate, been restated to conform to the new applicable financial reporting framework;

• evaluate whether the accounting policies reflected in the comparative information are consistent with those applied in the current period;

• be alert for and give consideration throughout the engagement to events and circum-stances that may affect the comparative financial statements; and

• ensure that the relevant requirements of CAS 560 on subsequent events have been addressed.

If an auditor becomes aware of a possible material misstatement (as a result of the transi-tion or otherwise) in the comparative information, the auditor shall perform whatever additional audit procedures are necessary in the circumstances to obtain sufficient appropriate audit evidence to determine whether such a material misstatement exists.

Description of the new applicable financial reporting framework

The auditor shall evaluate whether the financial statements adequately refer to or describe the new applicable financial reporting framework.

Written management representations

The auditor shall obtain written representations for all periods referred to in the auditor’s report.

The auditor shall also obtain a specific written representation for any restatement made to correct a material misstatement in prior period financial statements that affects the comparative information.

The written representations will include a reference to the new applicable financial reporting framework (Canadian accounting standards for not-for-profit organizations or Canadian public sector accounting standards).

Refer to Appendix C.2 for excerpts from a representation letter.

164. Audit approach 1 — Report on all periods presented

Matters to address Comments

Documentation In addition to audit documentation required for the current period, the auditor will need to document:• the additional work performed on the opening balances; • the transition adjustments required; • any issues arising during the audit and how they were resolved; and • the revised financial statements and disclosures.

This documentation could be filed under “transition to the new applicable financial reporting framework” in the current period working papers in a separate section or sec-tions, for example, by financial statement area or in an entirely separate transition file.

Whatever filing method is used, the documentation shall be sufficient to enable an experienced auditor, having no previous connection with the audit, to understand: • the nature, timing and extent of the audit procedures performed;• the results of the audit procedures performed, and the audit evidence obtained; and • the conclusions reached, including any significant professional judgments made in

reaching those conclusions.

17

5. Auditapproach2—Reportingonthecurrentperiodonly

Under this approach, the audit opinion will refer to the current period only.

While the auditor may have audited the financial statements for the prior years in accordance with the pre-changeover accounting standards, the auditor will not have previously audited the financial state-ments for those periods prepared in accordance with the new applicable financial reporting framework.

When the auditor’s report refers to the current period only, using the audit reporting approach for corresponding figures, readers of the auditor’s report on the first financial statements prepared in accordance with the new applicable financial reporting framework might incorrectly presume that the auditor had previously issued an auditor’s report on the comparative information.

Unless the auditor has been specifically engaged to perform an audit of the prior year financial state-ments and the opening statement of financial position prepared in accordance with the new financial reporting framework, these financial statements are unaudited. In that case, the comparative informa-tion is presented in the form of corresponding figures, and the auditor complies with paragraph 14 of CAS 710 that requires the auditor to state, in an Other Matter paragraph in the auditor’s report, that the corresponding figures are unaudited. The Other Matter paragraph is included in the auditor’s report irrespective of whether the corresponding figures are marked as unaudited or the notes to the financial statements indicate that the auditor has not audited, and does not express an opinion on, the corresponding figures.

Paragraph 14 of CAS 710 also indicates that a statement in an Other Matter paragraph does not, however, relieve the auditor of the requirement to obtain sufficient appropriate audit evidence that the opening balances do not contain misstatements that materially affect the current period’s financial statements in accordance with paragraph 6 of CAS 510. The auditor’s work effort to comply with CAS 510 may not be significantly different than the work effort required to report on all periods presented. Accordingly, the auditor may wish to discuss with the organization whether it would be more appropriate for the auditor to report on all periods presented. It is important that the terms of the engagement appropriately reflect the financial statement periods on which the auditor has been engaged to report.

Some auditors may consider whether to make an additional reference in the auditor’s report to the fact that the financial statements for the prior years prepared in accordance with pre-changeover accounting standards were audited. While such a reference may be factually correct, including it in the auditor’s report may be seen to contradict the Other Matter paragraph. As a result, readers of the auditor’s report may misunderstand that the auditor was not engaged to provide an opinion on the prior years’ financial statements and the opening statement of financial position prepared in accordance with the new appli-cable financial reporting framework.

185. Audit approach 2 — Reporting on the current period only

5.1 Auditapproach2—Auditor’sopinionUnder this approach, the auditor’s opinion will refer to the current period only. Some matters to address in the auditor’s opinion are summarized below:

Exhibit 5.1.1: Auditapproach2—Auditor’sopinion

Matters to address Comments

Scope limitation Consider whether a scope limitation is needed in the auditor’s report. This is often the case when it is not possible to determine the completeness of revenues from fund raising activities.4

Refer to Appendix D.4 for an example of a “Basis for Qualified Opinion” paragraph and for a qualified auditor’s opinion paragraph.

Comparative information paragraph

When corresponding figures are presented, the auditor’s opinion shall not refer to the prior period financial statements except in the circumstances described in CAS 710 para-graphs 11, 12, and 14. The auditor shall state, in an additional paragraph in the auditor’s report, that the corresponding figures are unaudited. This paragraph shall be included immediately after the opinion paragraph in the auditor’s report. (Refer to Appendices D.3 and D.4 for an example of such paragraph (i.e., “Comparative information” paragraph)).

Not-for-profit organizations: description of financial statements and the applicable financial reporting framework

Paragraph 3 of Section 1401, General Standards of Financial Statement Presentation for not-for-profit organizations, in Part III of the CICA Handbook – Accounting, states that financial statements shall present fairly in accordance with generally accepted accounting principles the financial position, results of operations and cash flows of an organization.

Therefore, the auditor’s opinion will be worded accordingly (i.e., it will refer to the financial position of [the not-for-profit organization], the results of its operations and its cash flows.)

The applicable financial reporting framework will be described as “Canadian accounting standards for not-for-profit organizations.”

Refer to Appendix D.3 for an example of an auditor’s opinion paragraph.

4 For further guidance refer to “Reports Arising from Circumstances Addressed in CAS 710, Comparative Information — Corresponding Figures and Compara-tive Financial Statements,” in Reporting Implications of New Auditing and Accounting Standards (Issue 8, May 2012).

195. Audit approach 2 — Reporting on the current period only

Matters to address Comments

Government not-for-profit organizations: description of financial statements and the applicable financial reporting framework

Section PS 4200, Financial Statement Presentation by Not-for Profit Organizations, sets out the presentation and disclosure standards for financial statements for not-for-profit orga-nizations adhering to the standards for not-for-profit organizations in the CICA Public Sector Accounting Handbook. Paragraph PS 4200.05 states that the financial statements for a government not-for-profit organization are to provide the information necessary to meet the requirements of that Section and other Sections in a manner that results in the fair presentation in accordance with generally accepted accounting principles of the organiza-tion’s financial position, results of operations and cash flows.

It is important to note that, for government not-for-profit organizations, Section PS 2601, Foreign Currency Translation, and Section PS 3450, Financial Instruments, apply to fiscal years beginning on or after April 1, 2012. These Sections detail when a statement of remeasurement gains and losses has to be presented.

Sections PS 3450 and PS 2601 detail transitional provisions. When a government not-for-profit organization applies these Sections in the same period it adopts Public Sector Accounting Standards for the first time, these Sections cannot be applied retroactively. Comparative amounts are presented in accordance with the accounting policies applied by the government not-for-profit organization immediately preceding its adoption of Public Sector Accounting Standards.

If a government not-for-profit organization is required to present a statement of remea-surement gains and losses for fiscal years beginning on or after April 1, 2012, the auditor’s opinion will be worded accordingly (i.e., it will refer to the financial position of [the government not-for-profit organization], the results of its operations, its remeasurement gains and losses and its cash flows.)

Another important point is that the applicable financial reporting framework will be described as “Canadian public sector accounting standards.”

Refer to Appendix D.3 for an example of an auditor’s opinion paragraph.

205. Audit approach 2 — Reporting on the current period only

5.2 Auditapproach2—AuditproceduresThe auditor shall determine whether the financial statements include the comparative information required by the applicable financial reporting framework and whether such information is appropriately classified. For this purpose, the auditor shall evaluate whether:• the comparative information agrees with the amounts and other disclosures presented in the prior

period or, when appropriate, have been restated; and• the accounting policies reflected in the comparative information are consistent with those applied in

the current period or, if there have been changes in accounting policies, whether those changes have been properly accounted for and adequately presented and disclosed.

The following table provides more detail on some of the specific audit procedures that may be required under approach 2. Reference should also be made to CAS 710 and Appendix A to this guide.

Exhibit 5.2.1: Auditapproach2—Auditprocedures

Matters to address Comments

Terms of engagement

As the applicable financial reporting framework has changed (to ASNFPO or PSAS-GNFPO), the auditor will need to get a new engagement letter to ensure that manage-ment understands:• its responsibility to prepare financial statements in accordance with the new applicable

financial reporting framework;• that the audit opinion (which covers only the current period) will refer to the fair

presentation of the current financial statements prepared in accordance with the new applicable financial reporting framework;

• the corresponding figures will be regarded as unaudited because the auditor was not engaged to report on comparative information that was restated in accordance with the new applicable financial reporting framework; and

• the auditor shall state in a “comparative information” paragraph in the auditor’s report that the corresponding figures are unaudited. Such a statement does not, however, relieve the auditor of the requirement to obtain sufficient appropriate audit evidence that the opening balances do not contain misstatements that materially affect the current period’s financial statements.

Excerpts from a sample engagement letter are presented in Appendix D.1.

215. Audit approach 2 — Reporting on the current period only

Matters to address Comments

Discussion with management

The auditor will need to discuss with management:• The implications of the change to the applicable financial reporting framework. This

includes the transitional adjustments to be made by management, the optional exemp-tions to retrospective application and financial statement disclosures.

• The fact that the corresponding figures in the current period financial statements will be presented as unaudited. This would apply even when the financial statements prepared in accordance with the new applicable financial reporting framework do not appear to be significantly different from those prepared in accordance with pre-changeover accounting standards.

• The impact of the transition on the planned scope/timing of the audit.• The required information about the transition adjustments.

Risk assessment The auditor will need to identify and assess any new or increased risks of material misstatement (error and fraud) in the financial statements (as a result of the change in accounting standards) for the period covered by the auditor’s report.

New accounting policies and transition adjustments

The auditor will need to ensure that management has properly identified, calculated (including allocation to the correct period) and determined the nature, extent and impli-cations of changes to be made in the financial statements, as a result of:• revised accounting policies and their consistent application;• first-time adjustments required by the new financial reporting framework;• other transition adjustments; and• revised presentation and disclosures in the financial statements.

Opening balances The auditor’s objective with respect to opening balances is to obtain sufficient appropriate audit evidence about whether: opening balances contain misstatements that materially affect the current period’s financial statements; appropriate accounting policies reflected in the opening balances have been consistently applied in the current period’s financial statements; and any changes to accounting policies are appropriately accounted for and adequately presented and disclosed in accordance with the applicable financial reporting framework.

The auditor will need to:• evaluate whether the comparative information agrees with the amounts and other

disclosures presented in the prior period under the pre-changeover standards or that such information/disclosures have, where appropriate, been restated to conform to the new applicable financial reporting framework;

• evaluate whether the accounting policies reflected in the comparative information are consistent with those applied in the current period;

• be alert for and give consideration throughout the engagement to events and circum-stances that may affect the corresponding figures; and

• ensure that the relevant requirements of CAS 560 on subsequent events have been addressed.

If the auditor becomes aware of a possible material misstatement (as a result of the transi-tion or otherwise) in the comparative information, the auditor shall perform whatever additional audit procedures are necessary in the circumstances to obtain sufficient appropriate audit evidence to determine whether such a material misstatement exists.

225. Audit approach 2 — Reporting on the current period only

Matters to address Comments

Description of the new applicable financial reporting framework

The auditor shall evaluate whether the financial statements adequately refer to or describe the new applicable financial reporting framework.

Written management representations

The written representations for the current period will include a reference to the applicable financial reporting framework (Canadian accounting standards for not-for-profit organi-zations or Canadian public sector accounting standards).

Refer to Appendix D.2 for excerpts from a representations letter.

Obtaining new representations from management covering the “unaudited” correspond-ing figures is not necessary as management is already providing the auditor with a new representation that would cover the current period and the opening balances.

Documentation In addition to audit documentation required for the current period, the auditor will need to document:• the additional work performed on the opening balances; • the transition adjustments required; • any issues arising during the audit and how they were resolved; and • the revised financial statements and disclosures.

This documentation could be filed under “transition to the new applicable financial reporting framework” in the current period working papers in a separate section or sec-tions, for example, by financial statement area or in an entirely separate transition file.

Whatever filing method is used, the documentation should be sufficient to enable an experienced auditor, having no previous connection with the audit, to understand: • the nature, timing and extent of the audit procedures performed; • the results of the audit procedures performed and the audit evidence obtained; and • the conclusions reached, including any significant professional judgments made in

reaching those conclusions.

23

6. Appendices5

A. Selected transition adjustments and sample audit procedures

B. Selected comparison of work effort involved in audit approaches 1 and 2

C. Audit approach 1 — Reporting on all periods presented — Assumptions

C.1 Excerpts from an engagement letter

C.2 Excerpts from a representation letter

C.3 Unmodified independent auditor’s report

C.4 Qualified independent auditor’s report — Scope limitation

D. Audit approach 2 — Reporting on current period only — Assumptions

D.1 Excerpts from an engagement letter

D.2 Excerpts from a representation letter

D.3 Unmodified independent auditor’s report

D.4 Qualified independent auditor’s report — Scope limitation

E. Other resources available

5 The examples provided must be adapted to provincial legislation; for example, in Quebec, the “Chartered Accountant” designation cannot be used. Please refer to your provincial institute/Ordre for further details.

246. Appendices

AppendixA:SelectedtransitionadjustmentsandsampleauditproceduresSelected sample audit procedures have been presented for illustrative purposes only, assuming an adoption from CICA Handbook – Accounting – Part V — Pre-changeover accounting standards to CICA Handbook – Accounting – Part III — Accounting Standards for Not-for-Profit Organizations. Similar procedures would be required when adopting standards for government not-for-profit organizations in the CICA Public Sector Accounting Handbook.

Handbook reference Requirement Sample audit procedures

A first-time adopter6 may elect to use exemptions related to one or more of the following (the list below does not include all exemptions):

1501.13 Fair value Elect to measure an item of its tangible capital assets at the date of transition at fair value and use this fair value as its deemed cost.

• Review appropriateness of accounting policy note disclosing election made.

• Obtain and review property appraisal report (or similar evidence) and consider the requirements of CAS 500 paragraph 8 (management’s expert).

• Review the assumptions and meth-odology in the report supporting the property’s fair value.

• Review adjustments (gains/losses) to opening statement of financial position.

• Review the appropriateness of the note disclosure.

1501.15 Employee future benefitsElect to recognize all cumulative actuarial gains and losses and past service costs in opening net assets at the date of transi-tion.

• Review appropriateness of accounting policy note disclosing election made.

• Review transitional adjustment on opening statement of financial posi-tion to net assets.

1501.19 Cumulative translation differencesElect to set cumulative translation differ-ences for all foreign operations to zero at the date of transition.

• Review appropriateness of accounting policy note disclosing election made.

• Review transitional adjustment on the opening statement of financial position to net assets.

6 First-time adopter is defined in Section 1501 paragraph .03 (d) as an organization that presents its financial statements in accordance with accounting standards for not-for-profit organizations for the first time.

256. Appendices

Handbook reference Requirement Sample audit procedures

1501.20/3856.07 Financial instruments — Initial mea-surement (arm’s length transactions)Financial assets and liabilities shall be measured at fair value on initial recogni-tion. Where the financial asset or a financial liability will not be measured subsequently at fair value, its fair value shall be adjusted for financing fees and transaction costs that are directly attributable to its origination, acquisition, issuance or assumption.

If an entity elects to adopt Section 3856 at the date of transition, any difference between the recognition and measurement of financial instruments at that date, in accordance with Section 3856, and the prior year’s closing statement of financial position is recorded as an adjustment to opening net assets. Alternatively, if an entity does not choose to use the election, it has essentially elected to apply Section 3856 retrospectively.

• Ascertain whether management has elected to apply financial instruments retrospectively or apply Section 3856 as at the date of transition.

• Ensure that all financial assets and liabilities meet the definition of a financial instrument in the financial statements.

• Review appropriateness of, and application of, the accounting policy for financial instruments.

• Where financial instruments have been revalued as at the date of transi-tion, review evidence supporting the valuation (i.e., valuation, calculations, underlying assumptions and docu-mentation, etc.).

• Where a discounted cash flow model has been used, review appropriateness of assumptions and discount rates used by management (i.e., discount rates should be based on market rates on similar loans and advances).

• Review adjustments (gains/losses) to opening statement of financial position.

• Review appropriateness of note disclosure, including the accounting policy note.

266. Appendices

Handbook reference Requirement Sample audit procedures

1501.21/3856.12-13 Financial instruments — subsequent measurementInvestments in equity instruments that are quoted in an active market shall be accounted for at fair value with unreal-ized gains and losses going through net income.

An entity may irrevocably elect to measure any financial asset or financial liability at fair value by designating that fair value measurement shall apply when the asset or liability is first recognized in accordance with Section 3856.

• Review appropriateness of accounting policy note for portfolio investments.

• Where the organization had previ-ously classified financial instruments in categories that were not at fair value, ensure the reclassification to fair value is appropriate and that the entity has elected to do so.

• Obtain confirmation of, or examine brokerage statements or equivalent to obtain fair value for each security.

• Review adjustments (gains/losses) to opening statement of financial posi-tion and changes in net assets.

• Review appropriateness of note disclosure.

276. Appendices

AppendixB:Selectedcomparisonofworkeffortinvolvedinauditapproaches1and2The table below is relevant to both GNFPO and NFPO.

Subject matter Audit approach 1 Audit approach 2

Engagement letter State that auditor’s report will cover all periods presented.

Explain that the corresponding figures will be unaudited.

Management representation letter

Obtain representations for all periods presented.

As management will have already provided representations relating to prior periods, the only additional representations required under this approach will be for changes in the prior period’s financial statements.

Not required on comparative information unless there was a correction of a material misstatement in the comparative informa-tion.

Comparative information

The auditor needs to ensure that the level of information included in the compara-tive financial statements is comparable with that of the financial statements of the current period.

Note that the additional information required under this approach will be avail-able from the prior period audited financial statements. So the additional work effort required will only be for changes in the prior period’s financial statements.

The level of detail presented will be less than in Audit Approach 1, as correspond-ing amounts and disclosures will be driven primarily by their relevance to the current period figures.

286. Appendices

AppendixC:Auditapproach1—Reportingonallperiodspresented—AssumptionsIllustrative auditor’s reports (Appendices C.3 and C.4) and excerpts from an engagement letter (Appen-dix C.1) and a letter of representations (Appendix C.2) are based on the following assumptions:

GNFPO

• Transition from CICA Handbook – Accounting – Part V — Pre-changeover accounting standards.• Year end March 31.• Canadian public sector accounting standards were adopted on April 1, 2012 (GNFPO adheres to

the standards for government not-for-profit organizations in the CICA Public Sector Accounting Handbook).

• The auditor’s report refers to each period for which financial statements are presented.

NFPO

• Transition from CICA Handbook – Accounting – Part V — Pre-changeover accounting standards.• Year end March 31.• Canadian accounting standards for government not-for-profit organizations were adopted on April 1,

2012.• The auditor’s report refers to each period for which financial statements are presented.

296. Appendices

Appendix C.1: Auditapproach1—Reportingonallperiodspresented—Excerptsfromanengagementletter

These excerpts from an engagement letter apply to GNFPO and NFPO unless specified otherwise. A scope limitation paragraph is not included in this example.

[Date]

Dear [Mr. Bones]:

You have requested that we audit the financial statements of ABC Organization, which comprise the statements of financial position as at March 31, 2013, March 31, 2012 and April 1, 2011, and the statements of operations, changes in net assets and cash flows for the years ended March 31, 2013 and March 31, 2012, and [for GNFPO if required add: the statement of remeasurement gains and losses for the year ended March 31, 2013 and] a summary of significant accounting policies and other explanatory information. We are pleased to confirm our acceptance and our understanding of this audit engagement by means of this letter. Our audit will be conducted with the objective of our expressing an opinion on the financial statements.

Our Responsibilities[Not reproduced here]

Comparative financial statements — Adoption of [Canadian public sector accounting standards or Canadian accounting standards for not-for-profit organizations]ABC Organization has adopted the [Canadian public sector accounting standards or Canadian accounting standards for not-for-profit organizations] on [April 1, 2012]. Adopting these standards will require retroactive restatement of the opening balances at [April 1, 2011] and the financial statements for the period ended [March 31, 2012] and providing additional financial statement disclosures relating to the transition.

It is the responsibility of management to review the requirements of the [Canadian public sector accounting standards or Canadian accounting standards for not-for-profit organizations] standards to:• Identify the material differences that have an impact on ABC Organization (adjustments and

disclosures) between the pre-changeover accounting standards and the [Canadian public sec-tor accounting standards or Canadian accounting standards for not-for-profit organizations]; and

• Appropriately calculate and account for each of the transition adjustments required and then to provide us with supporting documentation.

We will perform such audit procedures, as outlined above, to obtain audit evidence about the amounts and disclosures in the financial statements in the comparative period.

306. Appendices

Content of Auditor’s ReportUnless unanticipated difficulties are encountered, our report will be substantially in the form outlined below [not included in this illustrative letter].

If our opinion on the financial statements is other than unmodified, we will discuss the reasons with you in advance. If, for any reason, we are unable to complete the audit or are unable to form, or have not formed, an opinion, we may decline to express an opinion as a result of this engagement.

[Remainder of letter not included in this illustrative letter]

316. Appendices

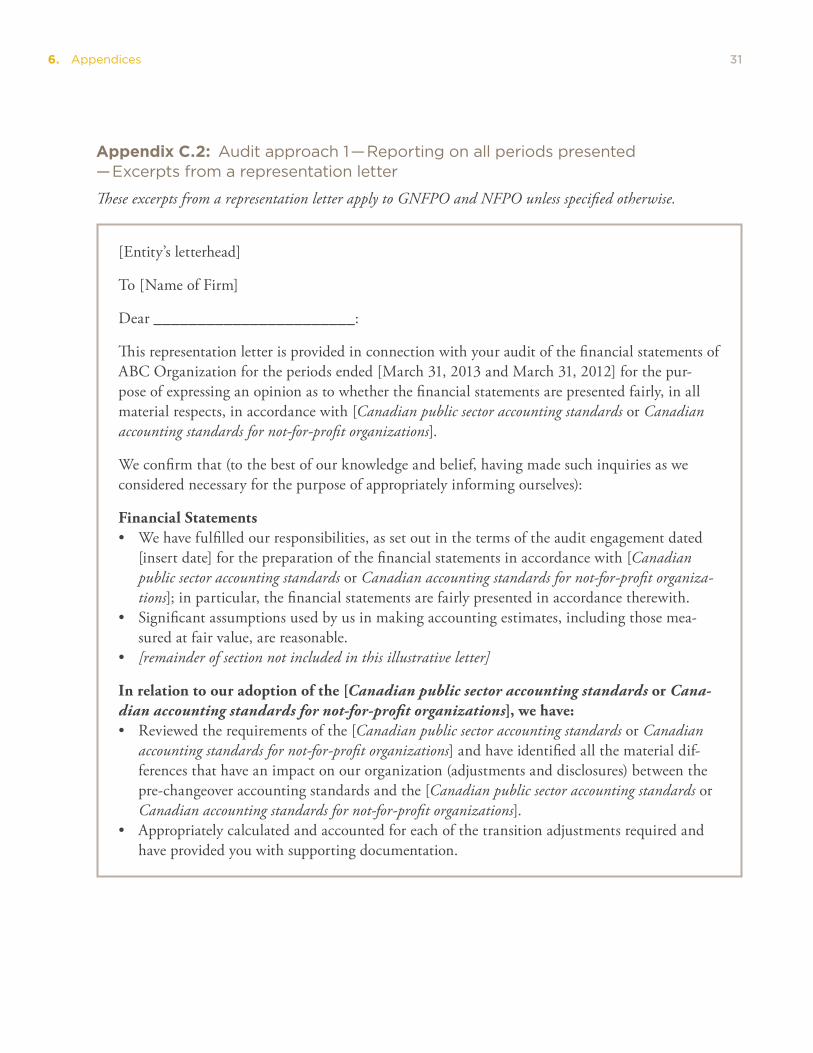

Appendix C.2: Auditapproach1—Reportingonallperiodspresented—Excerptsfromarepresentationletter

These excerpts from a representation letter apply to GNFPO and NFPO unless specified otherwise.

[Entity’s letterhead]

To [Name of Firm]

Dear _______________________:

This representation letter is provided in connection with your audit of the financial statements of ABC Organization for the periods ended [March 31, 2013 and March 31, 2012] for the pur-pose of expressing an opinion as to whether the financial statements are presented fairly, in all material respects, in accordance with [Canadian public sector accounting standards or Canadian accounting standards for not-for-profit organizations].

We confirm that (to the best of our knowledge and belief, having made such inquiries as we considered necessary for the purpose of appropriately informing ourselves):

Financial Statements• We have fulfilled our responsibilities, as set out in the terms of the audit engagement dated

[insert date] for the preparation of the financial statements in accordance with [Canadian public sector accounting standards or Canadian accounting standards for not-for-profit organiza-tions]; in particular, the financial statements are fairly presented in accordance therewith.

• Significant assumptions used by us in making accounting estimates, including those mea-sured at fair value, are reasonable.

• [remainder of section not included in this illustrative letter]

In relation to our adoption of the [Canadian public sector accounting standards or Cana-dian accounting standards for not-for-profit organizations], we have:• Reviewed the requirements of the [Canadian public sector accounting standards or Canadian

accounting standards for not-for-profit organizations] and have identified all the material dif-ferences that have an impact on our organization (adjustments and disclosures) between the pre-changeover accounting standards and the [Canadian public sector accounting standards or Canadian accounting standards for not-for-profit organizations].

• Appropriately calculated and accounted for each of the transition adjustments required and have provided you with supporting documentation.

326. Appendices

• Restated the opening statement of financial position at [April 1, 2011] and the comparative financial statements for the period ending [March 31, 2012] in accordance with the [Cana-dian public sector accounting standards or Canadian accounting standards for not-for-profit organizations], including the transition disclosures.

[Remainder of letter not included in this illustrative letter]

336. Appendices

INDEPENDENT AUDITOR’S REPORT

[Appropriate Addressee]

Report on the Financial Statements [Insert this title if a section “Report on Other Legal and Regulatory Requirements” is included]We have audited the accompanying financial statements of ABC Organization, which comprise the statements of financial position as at March 31, 2013, March 31, 2012 and April 1, 2011, and the statements of operations, changes in net assets and cash flows for the years ended March 31, 2013 and March 31, 2012, and [for GNFPO if required add: the statement of remeasurement gains and losses for the year ended March 31, 2013 and] a summary of significant accounting policies and other explanatory information.

Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with [Canadian public sector accounting standards or Canadian accounting stan-dards for not-for-profit organizations], and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstate-ment, whether due to fraud or error.

Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with Canadian generally accepted auditing standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material mis-statement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judg-ment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit

Appendix C.3: Auditapproach1—Reportingonallperiodspresented—Unmodifiedindependentauditor’sreport

This illustrative auditor’s report applies to GNFPO and NFPO unless specified otherwise.

346. Appendices

also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained in our audits is sufficient and appropriate to provide a basis for our audit opinion.

Opinion In our opinion, the financial statements present fairly, in all material respects, the financial position of ABC Organization as at March 31, 2013, March 31, 2012 and April 1, 2011, and the results of its operations and its cash flows for the years ended March 31, 2013 and March 31, 2012 [for GNFPO if required add: and its remeasurement gains and losses for the year ended March 31, 2013] in accordance with [Canadian public sector accounting standards or Canadian accounting standards for not-for-profit organizations].

Report on Other Legal and Regulatory Requirements [Form and content of this section of the auditor’s report will vary depending on the nature of the auditor’s other reporting responsibilities. (For example: As required by [specify legislation or regulation], we report that, in our opinion, the accounting principles in Canadian public sector accounting standards have been applied on a consistent basis.)]

[Auditor’s signature]

[Date of the auditor’s report]

[Auditor’s address]

356. Appendices

Appendix C.4: Auditapproach1—Reportingonallperiodspresented—Qualifiedindependentauditor’sreport—Scopelimitation

This illustrative auditor’s report applies to GNFPO and NFPO unless specified otherwise.

INDEPENDENT AUDITOR’S REPORT

[Appropriate Addressee]

Report on the Financial Statements [Insert this title if a section “Report on Other Legal and Regulatory Requirements” is included]We have audited the accompanying financial statements of ABC Organization, which comprise the statements of financial position as at March 31, 2013, March 31, 2012 and April 1, 2011, and the statements of operations, changes in net assets and cash flows for the years ended March 31, 2013 and March 31, 2012, and [for GNFPO if required add: the statement of remeasurement gains and losses for the year ended March 31, 2013 and] a summary of significant accounting policies and other explanatory information.

Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with [Canadian public sector accounting standards or Canadian accounting stan-dards for not-for-profit organizations], and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstate-ment, whether due to fraud or error.

Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with Canadian generally accepted auditing standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material mis-statement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judg-ment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit

366. Appendices

also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained in our audits is sufficient and appropriate to provide a basis for our qualified audit opinion.

Basis for Qualified OpinionIn common with many not-for-profit organizations, ABC Organization derives revenue from fundraising activities the completeness of which is not susceptible to satisfactory audit verifica-tion. Accordingly, verification of these revenues was limited to the amounts recorded in the records of ABC Organization. Therefore, we were not able to determine whether any adjust-ments might be necessary to fundraising revenue, excess of revenues over expenses, and cash flows from operations for the years ended March 31, 2013 and March 31, 2012, current assets and net assets as at March 31, 2013, March 31, 2012 and April 1, 2011.

Qualified Opinion In our opinion, except for the possible effects of the matter described in the Basis for Qualified Opinion paragraph, the financial statements present fairly, in all material respects, the financial position of ABC Organization as at March 31, 2013, March 31, 2012 and April 1, 2011, and the results of its operations and its cash flows for the years ended March 31, 2013 and March 31, 2012 [for GNFPO if required add: and its remeasurement gains and losses for the year ended March 31, 2013] in accordance with [Canadian public sector accounting standards or Canadian accounting standards for not-for-profit organizations].

Report on Other Legal and Regulatory Requirements [Form and content of this section of the auditor’s report will vary depending on the nature of the auditor’s other reporting responsibilities. (For example: As required by [specify legislation or regulation], we report that, in our opinion, the accounting principles in Canadian public sector accounting standards have been applied on a consistent basis.)]

[Auditor’s signature]

[Date of the auditor’s report]

[Auditor’s address]

376. Appendices

AppendixD:Auditapproach2—Reportingoncurrentperiodonly—AssumptionsIllustrative auditor’s reports (Appendices D.3 and D.4) and excerpts from an engagement letter (Appen-dix D.1) and a letter of representations (Appendix D.2) are based on the following assumptions:

GNFPO