gfk - consumer electronics summit (ces) china 2015

TRANSCRIPT

2

Innovations Consumer Electronics

InformationTechnology

Tele-communication

3

Source: Digital World by GfK Boutique in partnership with the Consumer Electronics Association

2015 will be driven by smartphone salesand launch of new smart technologies

+0.1%

2013

€ 771bn

• Decline in mature product categoriesslowdown.

+0.9%

2014€ 778 bn

• Slowdown in emerging markets and smartphones& tablets spending.

• Phablet segment driving growth.

+1.5%

2015 forecast

€ 790 bn

• GDP remains sub-par in emerging markets.

• Emerging market smartphone strength and new product categories.

Spending on digital devices is ongoing positive.

4

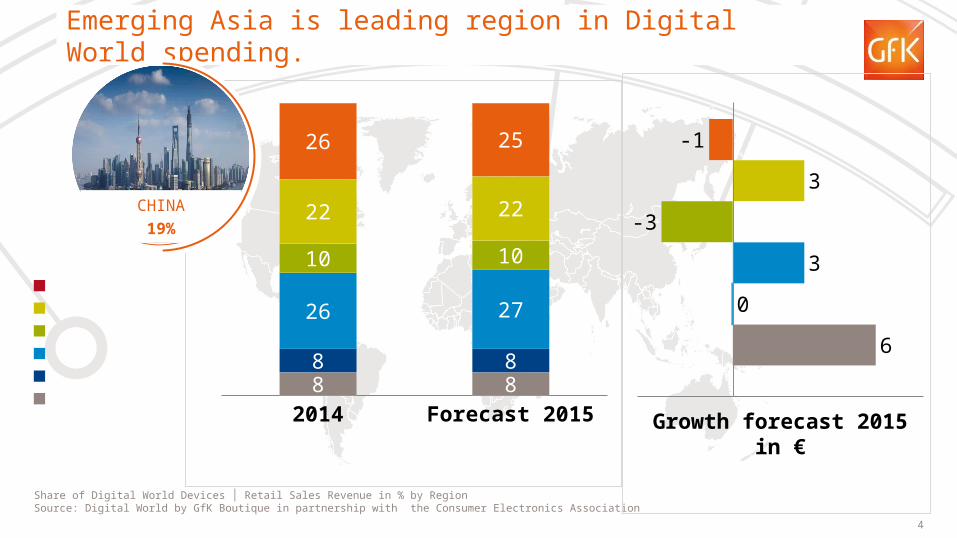

Share of Digital World Devices │ Retail Sales Revenue in % by RegionSource: Digital World by GfK Boutique in partnership with the Consumer Electronics Association

2014 Forecast 20158 88 8

26 27

10 10

22 22

26 25

Middle East/Africa

Latin America

Emerging Asia

Developed Asia

North America

Europe

6

0

3

-3

3

-1

Growth forecast 2015 in €

Emerging Asia is leading region in Digital World spending.

CHINA

19%

5

1 Includes mature products as DVD and HIFI | But also new gadgets as Action Cams and Smart WatchesShare of Digital World Devices │ Retail Sales Revenue in % by productsSource: Digital World by GfK Boutique in partnership with the Consumer Electronics Association

2014 Forecast 2015

21 18

2 2

13 14

6 6

12 12

8 8

38 40

-5

-15

2.3

-5

-6

1

8

Forecast 2015

All other categories1

Digital Still Camera

LCD TV

Desk PC

Mobile PC

Tablet PC

Smart-/Mobile Phones

Smartphones and Tablets are main drivers of Digital World.

6

2014 2015

1.23

1.4

Smartphones bill units

SmartphonesGlobal sales

Bill units

© GfK 2015 | GfK. Growth from Knowledge | Source: GfK Digital World by Boutique Research, in partnership with the Consumer Electronics Association

7

Source: Digital World by GfK Boutique in partnership with the Consumer Electronics Association

Smart glasses

Wearable headset

Wearable camera

Health & fitness tracker

Smartwatch

2014 2015 20161 2 55 7

11812

1514

25

38

4

26

46

Wearables MIO units

2014 2015 2016

31

72

114

Smartphones bear new markets: WEARABLES.

8

High-end LifestyleSmartwatches will come up not

only by Apple.

Consumers will look forsmartwatches by

their favorite luxury brands.

9

2010 2011 2012 2013 2014 2015

47 47.941.6

35.227.2

22.7

2010 2011 2012 2013 2014 2015

1.3 2.23.9

6.7

10.912.9

2010 2011 2012 2013 2014 2015

10.4

37.9 4033.9

25.320.2

2010 2011 2012 2013 2014 2015

0.2 0.81.6

3.3

6.9

9.6

Portable Car Navigation Mio Units

Action CamsMio Units

E-ReaderMio Units

Soundbar SpeakerMio Units

However: some new markets arose fast and went down fast as well

© GfK 2015 | GfK. Growth from Knowledge | GfK Digital World by Boutique Research, in partnership with the Consumer Electronics Association

10

Drones will be the next upcoming hype.

B2B market as well as

B2C market!

11

Internet innovationhappens also

at home.

Not only mobile internet

stands for innovation.

12

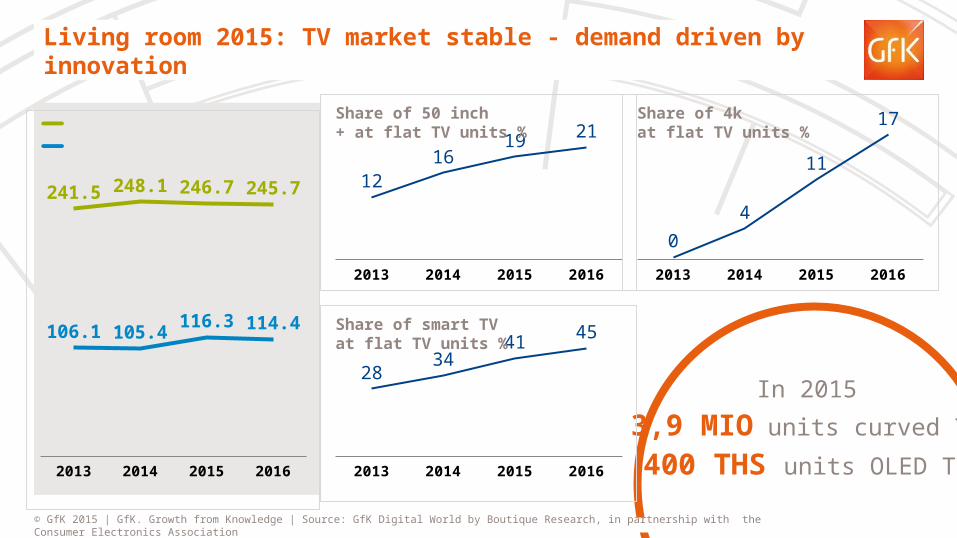

2013 2014 2015 2016

1216

19 21

In 2015

3,9 MIO units curved TV

400 THS units OLED TV

Share of 50 inch + at flat TV units %

2013 2014 2015 2016

0

4

11

17Share of 4k at flat TV units %

2013 2014 2015 2016

2834

41 45Share of smart TVat flat TV units %

2013 2014 2015 2016

241.5 248.1 246.7 245.7

106.1 105.4116.3 114.4

Global TV sales Mio units

Global TV sales Bn Euro

Living room 2015: TV market stable - demand driven by innovation

© GfK 2015 | GfK. Growth from Knowledge | Source: GfK Digital World by Boutique Research, in partnership with the Consumer Electronics Association

13

All available

at home and mobile

always and everywhere

Justin Bieber

House of Cards

The Walking Dead

Desperate Housewives

Gangnam Style

Internet Media Player

Apple TV Box

Smart-TV

AndroidTV

Amazon Fire TV

14

27,3 Mio 4k/UHD in 2015

expected.

+ 10% of LCD TV Market2013 2014 2015 2016 2017

0.910.5

27.3

42.3

55.2

4k/UHDGlobal Sales Mio units

52

More than 50% of global sales of 4k will happen in China in 2015

Ranking in Consumer TV-Demand: 1.) screensize but 2.) picture quality

© GfK 2015 | GfK. Growth from Knowledge | Source: GfK Digital World by Boutique Research, in partnership with the Consumer Electronics Association

15

Findings -> Consumer Electronics

16

putting puzzle together -> TV

• Driven by innovations TV market moved stepwise back into the

consumers interest: Flat, LED, Internet, 3D, 4k, OLED, Curved …

• However, on a total global level there is no significant growth in

unit based TV demand

• additional demand is coming from emerging countries (India, SEA

…), larger screen size and improved display quality (4k).

• Price is ongoing under pressure, driven by a continuous and

ongoing concentration on retail level (Technical Superstores vs.

Online Sales).

Conclusion

17

putting puzzle together -> Video

• Video content at home is global content and will be

streamed via internet to the Smart TV (similar experience

we had 5 years ago with Audio content via internet).

• DVD Player, even Blu Ray player will fade out of the

market.

• Streaming Media Player (Cromecast, Amazon Fire TV …)

will remain only a short time until all TV’s are Smart TVs.

Conclusion

18

And audio is growing

19

putting puzzle together -> Audio

• Sound today is streaming audio

• Devices have to be connected to the mobile internet devices

• Devices have to be controlled by a smartphone app.

• Potentials are:

• Docking Mini Speakers (several brands, also highend)

• Headphones/Headsets (e.g. Apple/Beats)

• Network Music Systems (Sonos / Bose)

Conclusion

20

Market forConsumer Electronics,

Telecom, Information Technologywill continue to grow.

As in the past market will be

driven by innovations.

Smartphones and mobile internet will

bear new innovative benefits for the consumers in their everyday

live.

Internet of things has started now.Conclusion

21

GfK is the trusted source of relevant market and consumer information that enables its clients to make smarter decisions. More than 13,000 market research experts combine their passion with GfK’s long-standing data science experience. This allows GfK to deliver vital global insights matched with local market intelligence from more than 100 countries. By using innovative technologies and data sciences, GfK turns big data into smart data, enabling its clients to improve their competitive edge and enrich consumers’ experiences and choices.